1. Introduction

Modern prediction algorithms such as random forests and deep learning use training sets, often very large ones, to produce rules for predicting new responses from a set of available predictors. A second question—right after “How should the prediction rule be constructed?”—is “How accurate are the rule’s predictions?” Resampling methods have played a central role in the answer. This paper is intended to provide an overview of what are actually several different answers, while trying to keep technical complications to a minimum.

This is a Special Issue of

STATS devoted to resampling, and before beginning on prediction rules it seems worthwhile to say something about the general effect of resampling methods on statistics and statisticians.

Table 1 shows the

law school data [

1], a small data set but one not completely atypical of its time. The table reports average scores of the 1973 entering class at 15 law schools on two criteria: undergraduate grade point average (GPA) and result on the “LSAT”, a national achievement test. The observed Pearson correlation coefficient between GPA and LSAT score is

How accurate is

?

Suppose that Dr. Jones, a 1940s statistician, was given the data in

Table 1 and asked to attach a standard error to

; let’s say a nonparametric standard error since a plot of (LSAT,GPA) looks definitely non-normal. At his disposal is the

nonparametric delta method, which gives a first-order Taylor series approximation formula for

. For the Pearson correlation coefficient this turns out to be

where

and

is the mean of

, the bars indicating averages.

Table 1.

Average scores for admitees to 15 American law schools, 1973. GPA is undergraduate grade point average, LSAT “law boards” score. Pearson correlation coefficient between GPA and LSAT is 0.776.

Table 1.

Average scores for admitees to 15 American law schools, 1973. GPA is undergraduate grade point average, LSAT “law boards” score. Pearson correlation coefficient between GPA and LSAT is 0.776.

| GPA | LSAT |

|---|

| 3.39 | 576 |

| 3.30 | 635 |

| 2.81 | 558 |

| 3.03 | 578 |

| 3.44 | 666 |

| 3.07 | 580 |

| 3.00 | 555 |

| 3.43 | 661 |

| 3.36 | 651 |

| 3.13 | 605 |

| 3.12 | 653 |

| 2.74 | 575 |

| 2.76 | 545 |

| 2.88 | 572 |

| 2.96 | 594 |

Jones either looks up or derives (

2), evaluates the six terms on his mechanical calculator, and reports

after which he goes home with the feeling of a day well spent.

Jones’ daughter, a 1960s statistician, has a much easier go of it. Now she does not have to look up or derive Formula (

2). A more general resampling algorithm, the Tukey–Quenouille

jackknife is available, and can be almost instantly evaluated on her university’s mainframe computer. It gives her the answer

Dr. Jones is envious of his daughter:

- 1.

She does not need to spend her time deriving arduous formulas such as (

2).

- 2.

She is not restricted to traditional estimates such as that have closed-form Taylor series expansions.

- 3.

Her university’s mainframe computer is a million times faster than his old Marchant calculator (though it is across the campus rather than on her desk).

If now, 60 years later, the Jones family is still in the statistics business they’ll have even more reason to be grateful for resampling methods. Faster, cheaper, and more convenient computation combined with more aggressive methodology have pushed the purview of resampling applications beyond the assignment of standard errors.

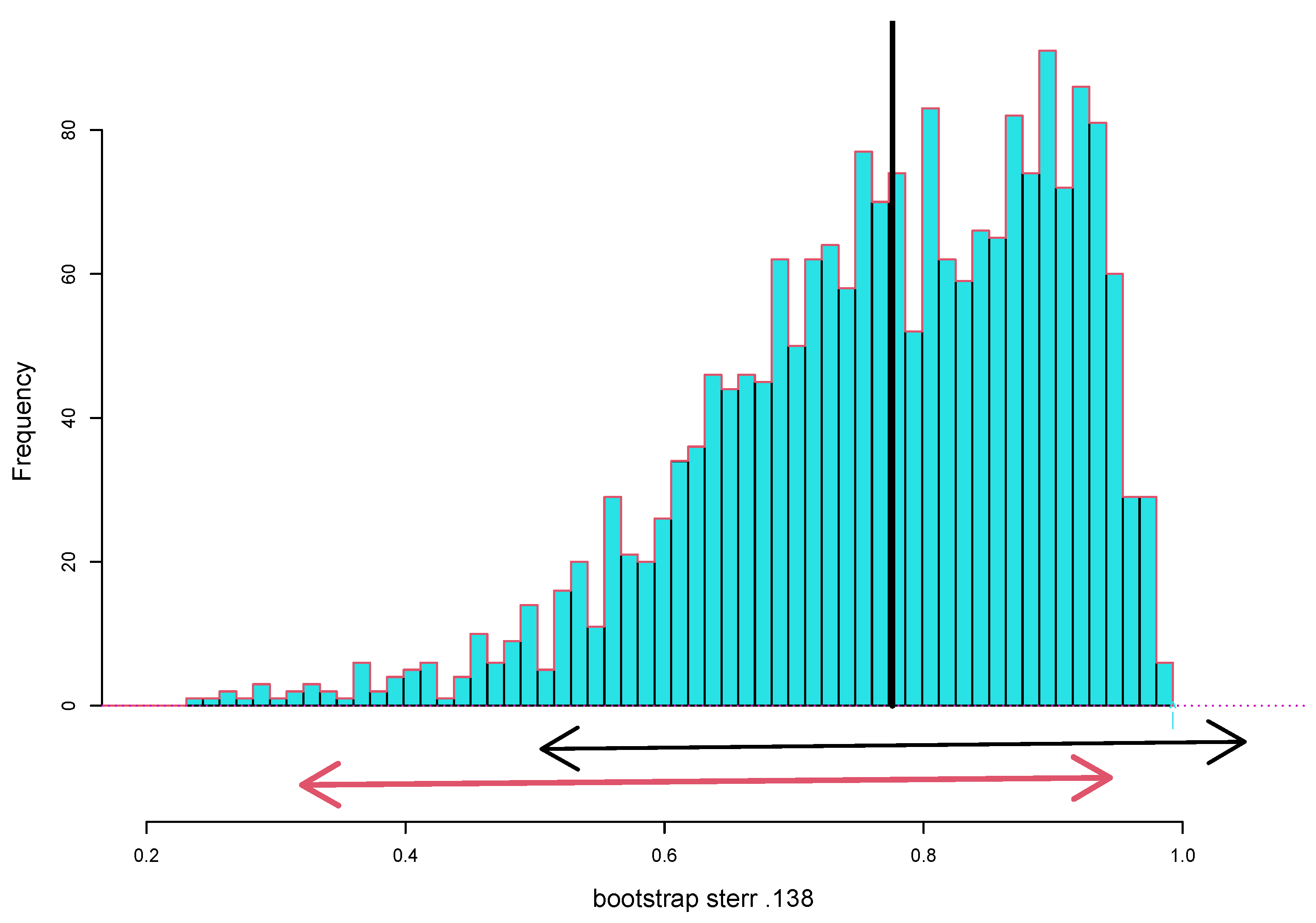

Figure 1 shows 2000 nonparametric bootstrap replications

from the law school data (Each

is the correlation from a bootstrapped data matrix obtained by resampling the 15 rows of the

matrix in

Table 1 15 times with replacement. See Chapter 11 of [

2]). Their empirical standard deviation is the nonparametric bootstrap estimate of standard error for

,

Two thousand is 10 times too many replications needed for a standard error, but it is not too many for a bootstrap confidence interval. The arrowed segments in

Figure 1 compare the standard approximate 95% confidence limit

, with the nonparametric bootstrap interval. (This is the

bca interval, constructed using program

bcajack from the CRAN package

bcaboot [

3]. Chapter 11 of [

2] shows why bca’s “second-order corrections”, here very large, improve on the standard method.)

The standard method does better if we first make Fisher’s

z transformation

compute the standard interval on the

scale, and transform the endpoints back to the

scale. This gives 0.95 interval

not so different from the bootstrap interval (

7), and at least not having its upper limit above 1.00!

This is the kind of trick Dr. Jones would have known. Resampling, here in the form of the bca algorithm, automates devices such as (

8) without requiring Fisher-level insight for each new application.

If there was a statistics’ “word of the year” it would be two words: deep learning. This is one of a suite of prediction algorithms that input data sets, often quite massive ones, and output prediction rules. Others in the suite include random forests, support vector machines, and gradient boosting.

Having produced a prediction rule, it is natural to wonder how accurately it will predict future cases, our subject in what follows:

Section 2 gives a careful definition of the prediction problem, and describes a class of loss functions (the “

Q class”) that apply to discrete as well as continuous response variables.

Section 3 concerns nonparametric estimates of prediction loss (cross-validation and the bootstrap “632 rule”) as well as Breiman’s

out-of-bag error estimates for random forests.

Covariance penalties, including Mallows’

and the Akaike Information Criterion, are parametric methods discussed in

Section 4 along with the related concept of

degrees of freedom.

Section 5 briefly discusses

conformal inference, the most recent addition to the resampling catalog of prediction error assessments.

2. The Prediction Problem

Statements of the prediction problem are often framed as follows:

A data set

of

n pairs is observed,

where the

are

p-dimensional predictor vectors and the

are one-dimensional responses.

The

pairs are assumed to be independent and identically distributed draws from an unknown

-dimensional distribution

F,

Using some algorithm

, the statistician constructs a prediction rule

that provides a prediction

,

for any vector

x in the space of possible predictors.

A new pair

is independently drawn from

F,

but with only

x observable.

The statistician predicts the unseen

y by

and wishes to assess prediction error. Later the prediction error will turn out to directly relate to the estimation error of

for the true conditional expectation of

y given

x,

Prediction error is assessed as the expectation of loss under distribution

F,

for a given loss function such as squared error:

.

Here,

indicates expectation over the random choice of all

pairs

and

in (

11) and (

13). The

u in

reflects the unconditional definition of error in (

15). The resampling algorithms we will describe calculate an estimate of

from the observed data. (One might hope for a more conditional error estimate, say one applying to the observed set of predictors

, a point discussed in what follows.)

Naturally, the primary concern within the prediction community has been with the choice of the algorithm that produces the rule . Elaborate computer-intensive algorithms such as random forests and deep learning have achieved star status, even in the popular press. Here, however, the “prediction problem” will focus on the estimation of prediction error. To a large extent the prediction problem has been a contest of competing resampling methods, as discussed in the next three sections.

Figure 2 illustrates a simple example:

pairs

have been observed, in this case with

x real. A fourth-degree polynomial

has been fit by ordinary least squares applied to

with the heavy curve tracing out

.

In the usual OLS notation, we’ve observed

from the notional model

where

is the

matrix with

ith row

,

the unknown 5-dimensional vector of regression coefficients, and

a vector of 20 uncorrelated errors having mean 0 and variance

,

The fitted curve

is given by

for

and

(the OLS estimate), this being algorithm

.

The

apparent error, what will be called

in what follows, is

which equals 1.99 for

. The usual unbiased estimate for the noise parameter

, not needed here, modifies the denominator in (

19) to take account of fitting a 5-vector

to

,

Dividing the sum of squared errors by

rather than

n can be thought of as a classical prediction error adjustment; err usually underestimates future prediction error since the

have been chosen to fit the observations

.

Because this is a simulation, we know the true function

(

14), the light dotted curve in

Figure 2:

the points

were generated with normal errors, variance 2,

Given model (

22), we can calculate the true prediction error for estimate

(

18). If

is a new observation, independent of the original data

which gave

, then the true prediction error

is

the notation

indicating expectation over

. Let

denote the average true error over the

observed values

,

equaling 2.40 in this case.

figures prominently in the succeeding sections. Here, it exceeds the apparent error

(

19) by 21%. (

is not the same as

(

15).)

Prediction algorithms are often, perhaps most often, applied to situations where the responses are dichotomous,

or 0; that is, they are

Bernoulli random variables, binomials of sample size 1 each,

Here

is the probability that

given prediction vector

x,

The probability model

F in (

11) can be thought of in two steps: as first selecting

x according to some

p-dimensional distribution

G and then “flipping a biased coin” to generate

.

Squared error is not appropriate for dichotomous data. Two loss (or “error”) functions

are in common use for measuring the discrepancy between

and

, the true and estimated probability that

in (

25). The first is

counting error,

For

or 1,

equals 0 or 1 if

y and

are on the same or different sides of

.

The second error function is

binomial deviance (or twice the Kullback–Leibler divergence),

Binomial deviance plays a preferred role in maximum likelihood estimation. Suppose that

is a

p-parameter family for the true vector of means in model (

25),

Then, the maximum likelihood estimate (MLE)

is the minimizer of the average binomial deviance (

28) between

and

,

see Chapter 8 of [

2]. Most of the numerical examples in the following sections are based on binomial deviance (

30). (If

equals 0 or 1 then (

30) is infinite. To avoid infinities, our numerical examples truncate

to

.)

Squared error, counting error, and binomial deviance are all members of the

Q-class, a general construction illustrated in

Figure 3 ([

4] Section 3). The construction begins with some concave function

; for the dichotomous cases considered here,

with

. The error

between a true value

and an estimate

is defined by the illustrated tangency calculation:

(equivalent to the “Bregman divergence” [

5]).

The entropy function

makes

equal binomial deviance. Two other common choices are

for counting error and

for squared error.

Working within the

Q-class (

31), it is easy to express the

true error of prediction

at predictor value

x where the true mean is

. Letting

be an independent realization from the distribution of

y given

x, the true error at

x is, by definition,

only

being random in the expectation.

Lemma 1. The true error at x (33) iswith in the dichotomous case. Proof. From definition (

31) of the

Q-class,

giving (

34) with

. In the dichotomous case

for

equal 0 or 1, so

. ☐

To simplify notation, let

and

, with

and

. The

average true error is defined to be

It is “true” in the desirable sense of applying to the given prediction rule

. If we average

over the random choice of

in (

11), we get the less desirable unconditional error

(

15).

is minimized by

,

Subtraction from (

36) gives

This is an exact analogue of the familiar squared error relationship. Suppose

and

are independently

vectors, and that

produces an estimate

. Then

which is (

38) if

.

At a given value of

x, say

, a prediction

can also be thought of as an estimate of

. Lemma 1 shows that the optimum choice of a prediction rule

is also the optimum choice of an estimation rule: for any rule

,

(

as in (

11)), so that the rule that minimizes the expected prediction error also minimizes the expected estimation error

.

Predicting y and estimating its mean μ are equivalent tasks within the Q-class. 3. Cross-Validation and Its Bootstrap Competitors

Resampling methods base their inferences on recomputations of the statistic of interest derived from systematic modifications of the original sample. This is not a very precise definition, but it cannot be if we want to cover the range of methods used in estimating prediction error. There are intriguing differences among the methods concerning just what the modifications are and how the inferences are made, as discussed in this and the next two sections.

Cross-validation has a good claim to being the first resampling method. The original idea was to randomly split the sample into two halves, the training and test sets, and . A prediction model is developed using only , and then validated by its performance on . Even if we cheated in the training phase, say by throwing out “bad” points, etc., the validation phase guarantees an honest estimate of prediction error.

One drawback is that inferences based on

data points are likely to be less accurate than those based on all

n, a concern if we are trying to accurately assess prediction error. “One-at-a-time“ cross-validation almost eliminates this defect: let

be data set (

10) with point

removed, and define

the prediction for case

i based on

using the rule

, constructed using only the data in

. The cross-validation estimate of prediction error is then

(This assumes that we know how to apply the construction rule

to subsets of size

). Because

is not involved in

, overfitting is no longer a concern. Under the independent-draws model (

11),

is a nearly unbiased estimate of

(

15) (“nearly” because it applies to samples of size

rather than

n).

The little example in

Figure 2 has

points

. Applying (

42) with

gave

, compared with apparent error

(

19) and true error

(

24). This not-very-impressive result has much to do with the small sample size resulting in large differences between the original estimates

and their cross-validated counterparts

. The single data point at

accounted for 40% of

.

Figure 4 concerns a larger data set that will serve as a basis for simulations comparing cross-validation with its competitors: 200 transplant recipients were followed to investigate the subsequent occurrence of anemia; 138 did develop anemia (coded as

) while 62 did not (

). The goal of the study was to predict

y from

x, a vector of

baseline variables including the intercept term (The predictor variables were body mass index, sex, race, patient and donor age, four measures of matching between patient and donor, three baseline medicine indicators, and four baseline general health measures).

A standard logistic regression analysis gave estimated values of the anemia probability

for

that we will denote as

Figure 4 shows a histogram of the 200

values. Here we will use

as the “ground truth” for a simulation study (rather than analyzing the transplant study itself). The

will play the role of the true mean

in Lemma 1 (

34), enabling us to calculate true errors for the various prediction error estimates.

A

matrix

of dichotomous responses

was generated as independent Bernoulli variables (that is, binomials of sample size 1),

for

and

. The

jth column of

,

is a simulated binomial response vector (

25) having true mean vector

.

provides 100 such response vectors.

Figure 4.

Logistic regression estimated anemia probabilities for the 200 transplant patients.

Figure 4.

Logistic regression estimated anemia probabilities for the 200 transplant patients.

For each one, a logistic regression was run,

in the language R, with

the

matrix of predictors from the transplant study. Cross-validation (“10-at-a-time” cross-validation rather than one-at-a-time: the 200 (x,y) pairs were randomly split into 20 groups of 10 each; each group was removed from the prediction set in turn and its 10 estimates obtained by logistic regression based on the other 190) gave an estimate of prediction error for the

jth simulation,

while (

36) gave true error

where

was the estimated mean from (

46).

In terms of mean ± standard deviation the 100 simulations gave

averaged 8% more than

(a couple percent of which came from having sample size 190 rather than 200). The standard deviation of

is not much bigger than the standard deviation of

, which might suggest that

was tracking

as it varied across the simulations.

Sorry to say, that was not at all the case. The pairs

,

, are plotted in

Figure 5. It shows

actually

decreasing as the true error

increases. The unfortunate implication is that

is not estimating the true error, but only its expectation

(

15). This is not a particular failing of cross-validation. It is habitually observed for all prediction error estimates—see for instance Figure 9 of [

4]—though the phenomenon seems unexplained in the literature.

Cross-validation tends to pay for its low bias with high variability. Efron [

1] proposed bootstrap estimates of prediction error intended to decrease variability without adding much bias. Among the several proposals the most promising was the

632 rule. (An improved version

632+ was introduced in Efron and Tibshirani [

6], designed for reduced bias in overfit situations where

(

19) equals zero. The calculations here use only

632.) The 632 rule is described as follows:

Nonparametric bootstrap samples

are formed by drawing

n pairs

with replacement from the original data set

(

10).

Applying the original algorithm

to

gives prediction rule

and predictions

as in (

12).

B bootstrap data sets

are independently drawn, giving predictions

for

and

.

Two numbers are recorded for each choice of

i and

j, the error of

as a prediction of

,

and

the number of times

occurs in

.

The

zero bootstrap is calculated as the average value of

for those cases having

,

Finally, the 632 estimate of prediction error is defined to be

being the apparent error rate (

19).

was calculated for the same 100 simulated response vectors

(

45) used for

(each using

replications), the 100 simulations giving

an improvement on

at (

49). This is in line with the 24 sampling experiments reported in [

6]. (There, rule

was used, with loss function

counting error (

27) rather than binomial deviance.

is discontinuous for counting error, which works to the advantage of 632 rules.)

Table 2 concerns the rationale for the 632 rule. The

80,000 values

for the first of the 100 simulated

vectors were averaged according to how many times

appeared in

,

for

. Not surprisingly,

decreases with increasing

k.

(

55), which would seem to be the bootstrap analogue of

, is seen to exceed the true error

, while

is below

. The intermediate linear combination

is motivated in Section 6 of [

1], though in fact the argument is more heuristic than compelling. The 632 rules

do usually reduce variability of the error estimates compared to cross-validation, but bias can be a problem.

The 632 rule recomputes a prediction algorithm by nonparametric bootstrap resampling of the original data.

Random forests [

7], a widely popular prediction algorithm, carries this further: the algorithm itself as well as estimates of its accuracy depend on bootstrap resampling calculations.

Regression trees are the essential component of random forests.

Figure 6 shows one such tree (constructed using

rpart, the R version of

CART [

8]; Chapters 9 and 15 of [

9] describe CART and random forests) as applied to

, the first of the 100 response vectors for the transplant data simulation (

44);

consists of 57 0 s and 143 1 s, average value

. The tree-making algorithm performs successive splits of the data, hoping to partition it into bins that are mostly 0 s or 1 s. The bin at the far right—comprising

cases having low body mass index, low age, and female gender—has just one 0 and 28 1 s, for an average of 0.97. For a new transplant case

, with only

x observable, we could follow the splits down the tree and use the terminal bin average as a quantitative prediction of

y.

Random forests improves the predictive accuracy of any one tree by

bagging (“bootstrap aggregation”), sometimes also called

bootstrap smoothing:

B bootstrap data sets

are drawn at random (

51), each one generating a tree such as that in

Figure 6. (Some additional variability is added to the tree-building process: only a random subset of the

p predictors is deemed eligible at each splitting point.) A new

x is followed down each of the

B trees, with the random forest prediction being the average of

x’s

B terminal values. Letting

, the prediction at

for the tree based on

, the random forest prediction at

is

Figure 6.

Regression tree for transplant data, simulation 1.

Figure 6.

Regression tree for transplant data, simulation 1.

The predictive accuracy for

uses a device such as that for

(

55): Let

be the average value of

for bootstrap samples

not containing

,

called the “out-of-bag” (oob) estimate of

. The oob error estimate is then

The overall oob estimate of prediction error is

(Notice that the leave-out calculations here are for the estimates

, while those for

(

56) are for the errors

.) Calculated for the 100 simulated response vectors

(

45), this gave

a better match to the true error

than either

(

49) or

(

57). In fact the actual match was even better than (

63) suggests, as shown in

Table 3 of

Section 4. This is all the more surprising given that, unlike

and

,

is fully nonparametric: it makes no use of the logistic regression model

(

46), which was involved in generating the simulated response vectors

(

44) (It has to be added that

is not an estimate for the prediction error of the logistic regression model

(

46), but rather for the random forest estimates

).

4. Covariance Penalties and Degrees of Freedom

A quite different approach to the prediction problem was initiated by Mallows’

formula [

10]. An observed

n-dimensional vector

is assumed to follow the homoskedastic model

the notation indicating uncorrelated errors of mean 0 and variance

as in (

17);

is known. A linear rule

is used to estimate

with

a fixed and known matrix. How accurate is

as a predictor of future observations?

The apparent error

is likely to underestimate the true error of

given a hypothetical new observation vector

independent of

,

the

notation indicating that

is fixed in (

67). Mallows’

formula says that

is an unbiased estimator of

,

that is,

is not unbiased for

but

is unbiased for

(

fixed in the expectation) under model (

64)–(

65).

One might wonder what has happened to the covariates

in

(

10)? The answer is that they are still there but no longer considered random–rather as fixed ancillary quantities such as the sample size

n. In the OLS model

for

Figure 3 (

16)–(

18) the covariates

determine

,

and

Formula (

65). We could, but do not, write

as

.

Mallows’

Formula (

68) can be extended to the

Q class of error measures,

Figure 4. An unknown probability model

—notice that

is not the same as

f in (

12)— is assumed to have produced

and its true mean vector

,

an estimate

has been calculated using some algorithm

,

the apparent error

(

19) and true error

(

33) are defined as before,

with the

fixed and

independently of

. Lemma 1 for the true error (

36) still applies,

The

Q-class version of Mallows’ Formula (

68) is derived as

Optimism Theorem 1 in Section 3 of [

4]:

Theorem 1. DefineThenwhere indicates covariance under model (72), is an unbiased estimate of in the same sense as (69), The covariance terms in (

76) measure how much each

affects its own estimate. They sum to a

covariance penalty that must be added to the apparent error to account for the fitting process. If

is binomial deviance then

the logistic parameter; the theorem still applies as stated whether or not

is logistic regression.

as stated in (

76) is not directly usable since the covariance terms

are not observable statistics. This is where resampling comes in.

Suppose that the observed data

provides an estimate

of

. For instance in a normal regression model

we could take

to be

for some estimate

. We replace (

72) with the

parametric bootstrap model

and generate

B independent replications

, from which are calculated

B pairs,

for

as in (

75). The covariances in (

76) can then be estimated as

and

, yielding a useable version of (

76),

“cp” standing for “covariance penalty”.

Table 3 compares the performances of cross-validation, covariance penalties, the 632 rule, and the random forest out-of-bag estimates on the 100 transplant data simulations. The results are given in terms of

total prediction error, rather than average error as in (

47). The bottom line shows their root-mean-square differences from true error

,

is highest, with

,

, and

respectively 71%, 83%, and 65% as large.

Table 3.

Transplant data simulation experiment. Top: First 5 of 100 estimates of total prediction error using cross-validation, covariance penalties (cp), the 632 rule, the out-of-bag random forest results, and the apparent error; degrees of freedom (df) estimate from cp. Bottom: Mean of the 100 simulations, their standard deviations, correlations with Errtrue, and root mean square differences from Errtrue. Cp and 632 rules used bootstrap replications per simulation.

Table 3.

Transplant data simulation experiment. Top: First 5 of 100 estimates of total prediction error using cross-validation, covariance penalties (cp), the 632 rule, the out-of-bag random forest results, and the apparent error; degrees of freedom (df) estimate from cp. Bottom: Mean of the 100 simulations, their standard deviations, correlations with Errtrue, and root mean square differences from Errtrue. Cp and 632 rules used bootstrap replications per simulation.

| | Errtrue | ErrCv | ErrCp | Err632 | Erroob | err | df |

| | 194 | 216.5 | 232.9 | 260.6 | 240.3 | 180.4 | 26.2 |

| | 199 | 245.8 | 220.9 | 241.0 | 230.9 | 173.8 | 23.5 |

| | 192 | 221.2 | 225.9 | 247.6 | 232.7 | 180.6 | 22.7 |

| | 234 | 197.4 | 200.9 | 215.2 | 219.7 | 162.2 | 19.4 |

| | 302 | 175.7 | 178.3 | 187.1 | 211.2 | 144.6 | 16.9 |

| | Errtrue | ErrCv | ErrCp | Err632 | Erroob | err | df |

| mean | 214.0 | 231.1 | 216.1 | 229.4 | 223.8 | 169.9 | 23.1 |

| stdev | 23.0 | 28.7 | 15.8 | 19.0 | 14.6 | 13.5 | 4.0 |

| cor.true | | −0.58 | | | | | |

| rms | | 48.8 | 34.8 | 40.7 | 31.6 | 54.2 | |

For the

jth simulation vector

(

45) the parametric bootstrap replications (

79) were generated as follows: the logistic regression estimate

was calculated from (

46),

; the bootstrap replications

had independent Bernoulli components

independent replications

were generated for each

, giving

according to (

81)–(

82).

Because the resamples were generated by a model of the same form as that which originally gave the

’s (

43)–(

44),

is unbiased for

. In practice our resampling model

in (

79) might not match

in (

72), causing

to be downwardly biased (and raising its rms).

’s nonparametric resamples make it nearly unbiased for the unconditional error rate

(

15) irrespective of the true model, accounting for the overwhelming popularity of cross-validation in applications.

4.1. A Few Comments

In computing

it is not necessary for

in (

79) to be constructed from the original estimate

. We might base

on a bigger model than that which led to the choice of

for

; in the little example of

Figure 3, for instance, we could take

to be

where

is the OLS sixth degree polynomial fit, while still taking

to be fourth degree as in (

18). This reduces possible model-fitting bias in

, while increasing its variability.

A major conceptual difference between

and

concerns the role of the covariates

, considered as random in model (

10) but fixed in (

72). Classical regression problems have usually been analyzed in a fixed-

framework for three reasons:

- 1.

mathematical tractability;

- 2.

not having to specify ’s distribution;

- 3.

inferential relevance.

The reasons come together in the classic covariance formula for the linear model

,

A wider dispersion of the

’s in

Figure 3 would make

more accurate, and conversely.

It can be argued that because

is estimating the conditional error

given it is more relevant to what is being estimated. See [

11,

12] for a lot more on this question.

On the other hand, “fixed-

” methods such as Mallows’

can be faulted for missing some of the variability contributing to the unconditional prediction error

(

15). Let

be the conditional error given

for predicting

y given

x,

according to Lemma 1 (

34). Then

where

is the marginal density of

x and

E indicates expectation over the choice of the training data

.

In the fixed-

framework of (

36),

replaces the integrand in (

87) with its

average

. We expect

since

typically increases for values of

x farther away from

. Rosset and Tibshirani [

12] give an explicit formula for the difference in the case of normal-theory ordinary least squares when they show that the factor 2 for the penalty term in Mallows’

formula should be increased to

. Cross-validation effectively estimates

while

estimates the fixed-

version of

.

With (

88) in mind,

and

are often contrasted as

This is dangerous terminology if it’s taken to mean that

applies to prediction errors

at specific points

x outside of

. In

Figure 3 for instance it seems likely that

exceeds

, but this is a fixed-

question and beyond the reach of the random-

assumptions underlying (

88). See the discussion of Figure 8 in

Section 5.

The sad story told in

Figure 5 shows

negatively correlated with the true

. The same is the case for

and

, as can be seen from the negative correlations in the

cor.true row of

Table 3.

is also negatively correlated with

, but less so. In terms of

rms, the bottom row shows that the fully nonparametric

estimates beat even the parametric

ones.

Figure 7 compares the 200

estimates from the logistic regression estimates (

46) with those from random forests, for

y the first of the 100 transplant simulations. Random forests is seen to better separate the

from the

cases.

relates to error prediction for random forest estimates,

not for logistic regression, but this does not explain how

could provide excellent estimates of the true error

–which in fact were based on the logistic regression model (

43)–(

44). If this is a fluke it’s an intriguing one.

There is one special case where the covariance penalty formula (

76) can be unbiasedly estimated without recourse to resampling: if

is the normal model

, and

—so

—then

Stein’s unbiased risk estimate (SURE) is defined to be

where the partial derivatives are calculated directly from the functional form of

. Section 2 of [

4] gives an example comparing

with

. Each term

measures the influence of

on its own estimate.

4.2. Degrees of Freedom

The OLS model

yields the familiar estimate

of

, where

is the projection matrix

as in (

70);

has

where

. Mallows’

formula

becomes

in this case. In other words, the covariance penalty that must be added to the apparent error

is directly proportional to

p, the degrees of freedom of the OLS model.

Suppose that

with matrix

not necessarily a projection. It has become common to define

’s degrees of freedom as

playing the role of

p in the

Formula (

92). In this way,

becomes a

lingua franca for comparing linear estimators

of different forms. (The referee points out that formulas such as (

92) are more often used for model selection rather than error rate prediction. Zhang and Yang [

13] consider model selection applications, as does Remark B of [

4].)

A nice example is the

ridge regression estimator

a fixed non-negative constant;

is the usual OLS estimator while

“shrinks”

toward

, more so as

increases. Some linear algebra gives the degrees of freedom for (

94) as

where the

are the eigenvalues of

.

The generalization of Mallows’ Formula (

68) in Theorem 1 (

76) has penalty term

which again measures the self-influence of each

on its own estimate

. The choice of

in

Figure 3 results in

, squared error, and

, in which case

equals

, and (

96) becomes

, as in Mallows’ Formula (

68). This suggests using

as a measure of degrees of freedom (or its estimate

from (

81)) for a general estimator

.

Some support comes from the following special situation: suppose

is obtained from a

p-parameter generalized linear model, with prediction error measured by the appropriate deviance function. (Binomial deviance for logistic regression as in the transplant example.) Theorem 2 of [

14], Section 6, then gives the asymptotic approximation

as in (

91)–(

92), the intuitively correct answer.

Approximation (

99) leads directly to

Akaike’s information criterion (AIC). In a generalized linear model, the total deviance from the MLE

is

denoting the density function ([

2], Hoeffding’s Lemma). Suppose we have glm’s of different sizes

p we wish to compare. Minimizing

over the choice of model is then equivalent to maximizing the total log likelihood

minus a dimensionality penalty,

which is the AIC.

Approximation (

99) is not razor-sharp:

is the transplant simulation logistic regression but the 100 estimates

averaged 23.08 with standard error 0.40. Degrees of freedom play a crucial role in model selection algorithms. Resampling methods allow us to assess

(

98) even for very complicated fitting algorithms

.

5. Conformal Inference

If there is a challenger to cross-validation for “oldest resampling method” it is permutation testing, going back to Fisher in the 1930s. The newest prediction error technique, conformal inference, turns out to have permutation roots, as briefly reviewed next.

A clinical trial of an experimental drug has yielded independent real-valued responses for control and treatment groups:

Student’s

t-test could be used to see if the new drug was giving genuinely larger responses but Fisher, reacting to criticism of normality assumptions, proposed what we would now call a nonparametric two-sample test.

Let

be the combined data set,

and choose some score function

that contrasts the last

m z-values with the first

n, for example the difference of means,

Define

as the set of scores for all permutations of

,

ranging over the

permutations.

The permutation

p-value for the treatment’s efficacy in producing larger responses is defined to be

the proportion of

having scores

exceeding the observed score

. Fisher’s key idea was that if in fact all the observations came from the same distribution

F,

(implying that Treatment is the same as Control), then all

permutations would be equally likely. Rejecting the null hypothesis of No Treatment Effect if

has null probability (nearly)

.

Usually

is too many for practical use. This is where the sampling part of resampling comes in. Instead of all possible permutations, a randomly drawn subset of

B of them, perhaps

, is selected for scoring, giving an estimated permutation

p-value

In 1963, Hodges and Lehmann considered an extension of the null hypothesis (

107) to cover location shifts; in terms of cumulative distribution functions (cdfs), they assumed

where

is a fixed but unknown constant that translates the

v’s distribution by

units to the right of the

u’s.

For a given trial value of

let

and compute its permutation

p-value

A 0.95 two-sided nonparametric confidence interval for

is then

The only assumption is that, for the true value of

, the

components of

are i.i.d., or more generally exchangeable, from some distribution

F.

Vovk has proposed an ingenious extension of this argument applying to prediction error estimation, a much cited reference being [

15]; see also [

16]. Returning to the statement of the prediction problem at the beginning of

Section 2,

is the observed data and

a new (predictor, response) pair, all

pairs assumed to be random draws from the same distribution

F,

is observed but not

, and it is desired to predict

. Vovk’s proposal,

conformal inference, produces an exact nonparametric distribution of the unseen

.

Let

be a proposed trial value for

, and define

as the data set

augmented with

,

A prediction rule

gives estimates

(It is required that

be invariant under reordering of

’s elements.)

For some score function

let

where

measures disagreement between

y and

, larger values of

indicating less conformity between observation and prediction. (More generally

can be any function

.)

If the proposed trial value

were in fact the unobserved

then

and

would be exchangeable random variables, because of the i.i.d. assumption (

113). Let

be the ordered values of

. Assuming no ties, the

n values

partition the line into

intervals, the first and last of which are semi-infinite. Exchangeability implies that

has probability

of falling into any one of the intervals.

A conformal interval for the unseen

consists of those values of

for which

“conforms” to the distribution (

117). To be specific, for a chosen miscoverage level

, say 0.05, let

and

be integers approximately proportion

from the endpoints of

,

The conservative two-sided level

conformal prediction interval

for

is

The argument is the same as for the Hodges–Lehmann interval (

112), now with

and

.

Interval (

119) is computationally expensive since all of the

, not just

, change with each choice of trial value

. The

jackknife conformal interval begins with the jackknife estimates

where

, that is

(

10) with

deleted. The scores

(

116) are taken to be

for some function

s, for example

. These are compared with

, and

is computed as at (

119). Now the score distribution (

117) does not depend on

(nor does

), greatly reducing the computational burden.

The jackknife conformal interval at

was calculated for the small example of

Figure 2 using

for

. For this choice of scoring function, interval (

119) is

with conformal probability

. The square dots in

Figure 8 are the values

for

, with

having probability

of falling into each of the 21 intervals. Conformal probability for the full range

is

.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}