1. Introduction

Increasing the pace and scale of prescribed fire is recognized as a critical need for mitigating increasing wildfire risks [

1,

2]. Prescribed fire is a tool used globally for conserving biological diversity, reducing fire hazard, maintaining wildlife habitat, increasing agricultural productivity, and for promoting a host of other ecosystem and cultural services [

1,

3]. Each year in the United States, a wide range of public, private, and non-governmental organization (NGO) land managers conduct prescribed burns on more than 4 million ha (10 million ac) of public and private lands [

4]. The majority of prescribed fires in the United States of America (U.S.) are ignited in Florida, Georgia, Alabama, Oklahoma, and Kansas (consistently among the top five for prescribed fire extent); the Southeastern states account for ca. 70% of area burned with prescribed fire in the U.S. annually [

4].

In spite of its widespread acceptance, there are a number of impediments to the continued use and expansion of prescribed fire [

5,

6]. Liability for prescribed burn practitioners, from smoke or escaped fire, is a consistent and growing impediment to scaling up prescribed fire activities [

4,

5,

7]. The expansion of the wildland–urban interface has not only increased the complexity of wildfire suppression [

8], but it also has increased the difficulty of prescribed fire management [

7] and raised the potential of impacts to the public through smoke intrusion or escaped prescribed fire. This liability for damages in the face of increasing complexity will continue to constrain the pace and effectiveness of prescribed fires in fire-prone landscapes, perpetuating the “wildfire trap” [

9] at a time when climate change is expected to worsen wildfire activity.

Prescribed fires are notable for their high success rates for safety and modest smoke impacts relative to wildfire. Prescribed fire “escapes”—defined as prescribed burns that cannot be contained with on-site resources [

10]—are rare, with rates of <1% across federal and private burns in the U.S. [

11,

12]. Of the fires that do escape, even fewer cause damages or public harm [

12,

13]. Prescribed fire smoke can also be a liability, with smoke-impaired visibility leading to automobile accidents and other damages [

13,

14,

15]. Even with these two “beyond the burn unit” issues, human safety hazards from prescribed fires are minimal [

16]. In spite of the rarity of escapes and smoke issues, however, fire practitioners consistently report that concern about liability is a major impediment to applying fire [

7,

17,

18]. While rare, losses from accidents related to prescribed fire can be costly, with the Cerro Grande Fire being a most noteworthy example. Having originated as a prescribed fire on the Bandelier National Monument in New Mexico, this escaped fire burned nearly 400 structures, with the General Accounting Office estimating costs at US

$1 billion [

19].

Many U.S. states have codified “right to burn” language for landowners who use prescribed fire. Embedded within these laws are liability standards [

20,

21]. These state standards fall into three general categories: strict liability (12 states); simple negligence (26 states); and gross negligence (seven states) [

20]. In states with the strict liability standard, courts can hold the burn practitioner liable for damages regardless of any precautions or care taken. In states following the simple negligence standard, the practitioner can be found liable for damages if they do not employ “reasonable care.” In states with the gross negligence standard, liability is incurred only where the injured parties show that the burner used reckless disregard in burn preparation and implementation. The gross negligence standard provides significant relief for prescribed fire managers in recognition of the public good that results from sustaining prescribed fire at scales needed to reduce wildfire risks and preserve wildlife habitat and biodiversity [

22].

States like Georgia have enacted gross negligence liability laws that provide protection for all private burners. Other states—like Florida, Colorado, and, most recently, Washington—have gross negligence standards tied to a certified burner program. In these states, certified burners who meet training and planning criteria must be proven to have been grossly negligent for damages caused by prescribed fire, whereas non-certified practitioners are subject to a stricter negligence standard [

22]. State and federal prescribed fire practitioners are provided varying levels of protection from tort liability by federal and state laws [

20,

21]. Federal liability for prescribed fire damages is governed by the Federal Tort Claims Act, while states vary as to the process and recourse for recovery of damages following loss. Governmental prescribed burn managers acting within their job duties are generally shielded from personal liability through sovereign immunity.

Fires resulting in harm can have lasting negative effects on public perception of prescribed fire and undermine its acceptance despite its societal benefits [

23,

24]. Protecting the public from loss and providing remedies quickly when loss occurs are critical policy needs as states and Federal agencies seek to increase prescribed fire application. With a few notable exceptions [

19], damages from prescribed fire escapes or smoke tend to result in losses at local scales [

13]. This means that, unlike large wildfires where a disaster declaration may provide some forms of aid, the options for immediate redress of loss for affected parties from prescribed fires is unlikely in the absence of insurance claims or civil lawsuits or both. In states where the standard of gross negligence protects prescribed burners, any resulting losses to homeowners and timberland under this model may be borne wholly by the individuals impacted. As recent cases in Florida—a gross negligence state—illustrate, some neighborhoods impacted by prescribed fire escapes have little in the way of immediate help to compensate losses because the burns were conducted within the State’s certification standards [

18].

New combinations of public policy solutions are needed to balance liability and losses more effectively as the U.S. seeks to expand the application of prescribed fire in many at-risk landscapes. State statutes that recognize the right to burn, and reward certified burn practitioners with liability relief, offer the best opportunity to protect responsible burn managers from accidental escape or smoke impacts. For consistent protection of the public, we propose an additional and complementary approach to private insurance in the form of “catastrophe funds,” as used in other natural hazards. In addition to protecting practitioners, these funds may ensure broader public support for burning.

2. Catastrophe Fund Concept

To balance the public good with private loss from rare but impactful all-hazard events that overwhelm private insurance, so-called “catastrophe funds” (or catastrophe bonds) have been used for decades to compensate individuals or insurance companies (i.e., reinsurance) unintentionally injured or harmed, while financially relieving the companies and or entities responsible. The U.S. Congress developed the National Vaccine Injury Compensation Program (42 USCS §§ 300aa-10 et seq.) in 1986 to promote the continued production of vaccines by pharmaceutical companies while providing a release from liability for claims of injury from adverse vaccine reactions. In this case, US

$0.75 from each administered vaccine is deposited in a fund that pays individuals who can definitively relate an injury to the administration of a vaccine. As of 1 April 2020, over US

$4.3 billion had been paid to injured individuals through the program (from

https://www.hrsa.gov/sites/default/files/hrsa/vaccine-compensation/data/data-statistics-report.pdf, accessed on 17 October 2021). In 1993, Florida created a Hurricane Catastrophe Fund (Fla. Stat. §215.555) to encourage private insurance companies to continue covering properties in the state following substantial losses caused by Hurricane Andrew. The fund is supported by a surcharge on individual insurance policies, providing compensation to insurance companies to promote continued property insurance availability across the state. Some western states, including Idaho (Idaho Code §36-1108 et seq.), provide landowners with compensation for property damage caused by nuisance wildlife through a fund supported by access fees and big game hunting tag fees. In 2003, following a number of catastrophic wildfires, the California Community Foundation’s Wildfire Relief Fund was established. Different from some of the other Catastrophe Funds, the Wildfire Relief Fund is a relief grant that goes to community foundations or organizations affected by wildfire.

Major utilities have explored catastrophe bonds as a way to mitigate losses from wildfire with mixed results. In 2008, Pacific Gas and Electric Company (PG&E) sold a US$200 million catastrophe bond in order to insure against wildfires in the event that they were found liable for their start and spread. The bond by PG&E was thought to be the first of its kind. Costly wildfires in 2017 and 2018 resulted in US$30 billion in damage claims, grossly exceeding the catastrophe bond funds. Thus, without some shield or limits to liability for providing a public service that has inherent risks (e.g., transmission lines), PG&E was ultimately undercapitalized for the company’s liability exposure—this despite attempting to spread risk among bondholders. In subsequent litigation, PG&E was also found liable for contributing to wildfire risks by failing to maintain infrastructure.

4. Combining Policies to Share Risk

It is widely recognized that increasing the pace and scale of prescribed fire is required to reduce overall societal risk of wildfire and increase ecosystem resilience in fire-prone landscapes. To be successful in sustaining prescribed fire, mechanisms must quickly compensate property owners’ losses from prescribed fires without overwhelming burn managers in potential liability. The establishment of a catastrophe fund enables policy makers to insure potential losses in a variety of models, but compensation must be paired with complementary policies to protect prescribed fire managers from the full burden of liability. This “policy pairing” could sustain public support of prescribed fire in states where liability protection (e.g., gross negligence) has already been adopted, and encourage prescribed fire in states where liability represents the key impediment to needed action to reduce wildfires.

Despite the fact that prescribed fire can provide public benefit, liability protection is critical for individual practitioners or organizations to accept the responsibility of taking action that comes with inherent risks (i.e., the burden of intentional action; sensu [

25]). Thus, while the effectiveness of any prescribed fire catastrophe fund for increasing the pace and scale of prescribed fire will depend on the specific context of each state, liability protection is a key policy component for success [

4]. In a state with a strict (or undefined) liability standard, the catastrophe fund might cover losses for projects only where the burner was acting with reasonable care (i.e., meeting a simple negligence standard). In that case, a catastrophe fund would help mitigate liability for the practitioner, thereby facilitating and encouraging increased use of prescribed fire in states where practitioners are currently wary of the risks. In states with ordinary or gross negligence laws, a catastrophe fund would focus less on the burner—who already has some level of protection—and could instead foster more public support for prescribed fire, because there would be a mechanism for covering losses from burning even if the burner was acting within the bounds of the law.

While the rare losses from prescribed fire losses are usually small—often limited by the deliberate choice of favorable burning conditions on fire behavior—the potential in high-risk complex landscapes will present a challenge to any catastrophe plan options. Where fuels are particularly hazardous due to infrequent history of prescribed fire combined with a rapidly expanding WUI (

Figure 2), liabilities could quickly exceed capitalization of most catastrophic fund options, similar to the PG&E example above. In such high-risk landscapes, limiting the scope of a catastrophe fund to reinsurance of homeowner’s policies or using funds as supplemental insurance with fixed payouts for documented losses may be necessary. In landscapes where the risk of losses remains relatively low (e.g., many southeastern U.S. states where substantial burning already exists), the options for creating and sustaining a catastrophe fund tied to liability release could be more flexible.

Since the passage of the 1990 Florida Prescribed Fire Law that established a standard of gross negligence for liability of certified burners [

22], other U.S. states have followed suit as a way of sustaining and expanding prescribed fire. Adopting a standard of gross negligence represents the best incentive for practitioners to expand prescribed fire activities. The Florida law was also significant in that it tied the release of liability to state certification and use of best management practices designed to reduce the risk of loss to the public. While best management practices, certification programs, and smoke management plans differ across geography, tying liability release to best management practices is a powerful incentive for practitioners to take steps that both manage risks of escape or smoke impacts, but also build the public trust for expanded prescribed fire application.

Prompt compensation must be a priority for catastrophe fund payout to sustain public support for the liability release granted the practitioner. In many parts of the U.S., rural communities are at the greatest risk of loss from prescribed fire. Many of these same communities are otherwise underserved, and as in the case of the Limerock Fire in Florida, many individuals impacted directly by the wildfire were already experiencing economic hardships. The adoption of clear planning and implementation standards that govern liability for burn managers can facilitate rapid compensation of potential loss. A review of the prescribed fire implementation process by state officials can be undertaken rapidly to determine whether these best management standards were followed, and thus, liability protections apply. This review quickly informs the burn managers of their obligations regarding liability (if any), prevents frivolous lawsuits, and can be tied to levels of catastrophe fund compensation beyond emergency expenses. The State of Florida already produces such reports quickly where escapes occur, with the focus on (1) whether the required procedure was followed and (2) lessons that can be learned to improve future burn practices. If the practitioner is found grossly negligent, additional compensation may be sought through the courts. While states unable to fund programs to cover losses from more costly prescribed fires would benefit from a federal fund to spread risk, disaster declarations already provide Federal support in the largest wildfires.

At the time of publication, the state of California passed Senate Bill 170, the Budget Act of 2021 (Skinner 2021). The budget includes US

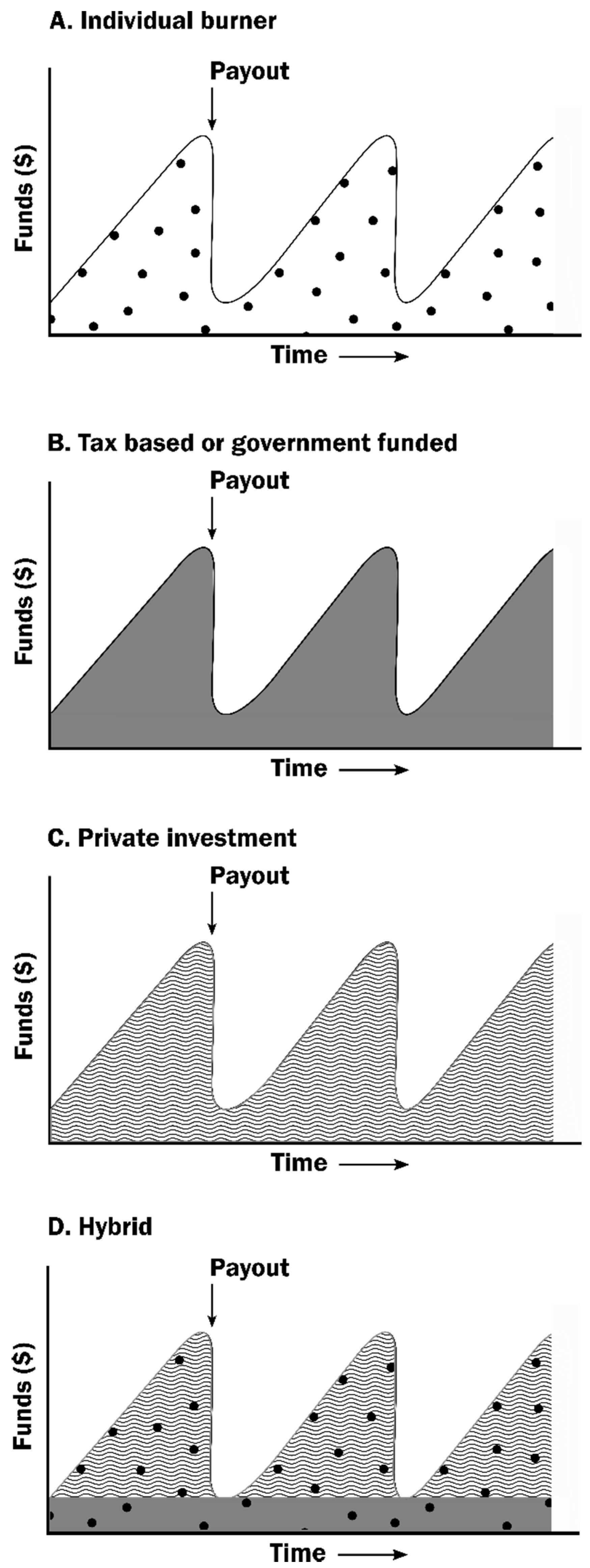

$20 million to establish a Prescribed Fire Claims Fund, which will “support coverage for losses from permitted prescribed fire by non-public entities, such as Native American tribes, private landowners, and non-governmental entities” (SB170 2021). Although details on the structure and implementation of the fund have yet to be determined, its intention is to provide the kinds of coverage described in this paper. The California fund is being treated as a pilot program, and early conversations have pointed to the potential of what we describe as a hybrid model (

Figure 1D), where the sustainability of the program may depend on future user fees, additional state funds, and/or complementary offerings by the private insurance market. The fund is complemented by the passage of Senate Bill 332 (Dodd 2021), which changed the state’s liability law from simple to gross negligence for fire suppression costs associated with escaped prescribed fire. California’s advances during this legislative session will likely inspire and provide critical lessons learned for other states that are working to scale up their prescribed fire efforts.

{kind=link}

{kind=link}