Laplace Transform Homotopy Perturbation Method for the Two Dimensional Black Scholes Model with European Call Option

{kind=link}

{kind=link}

{kind=link}

Abstract

:1. Introduction

2. Two-Dimensional Black Scholes Equation

3. Basic Ideas of Laplace Transform Homotopy Perturbation Method

4. Two-Dimensional Black Scholes Equation with Laplace Transformation Homotopy Perturbation Method

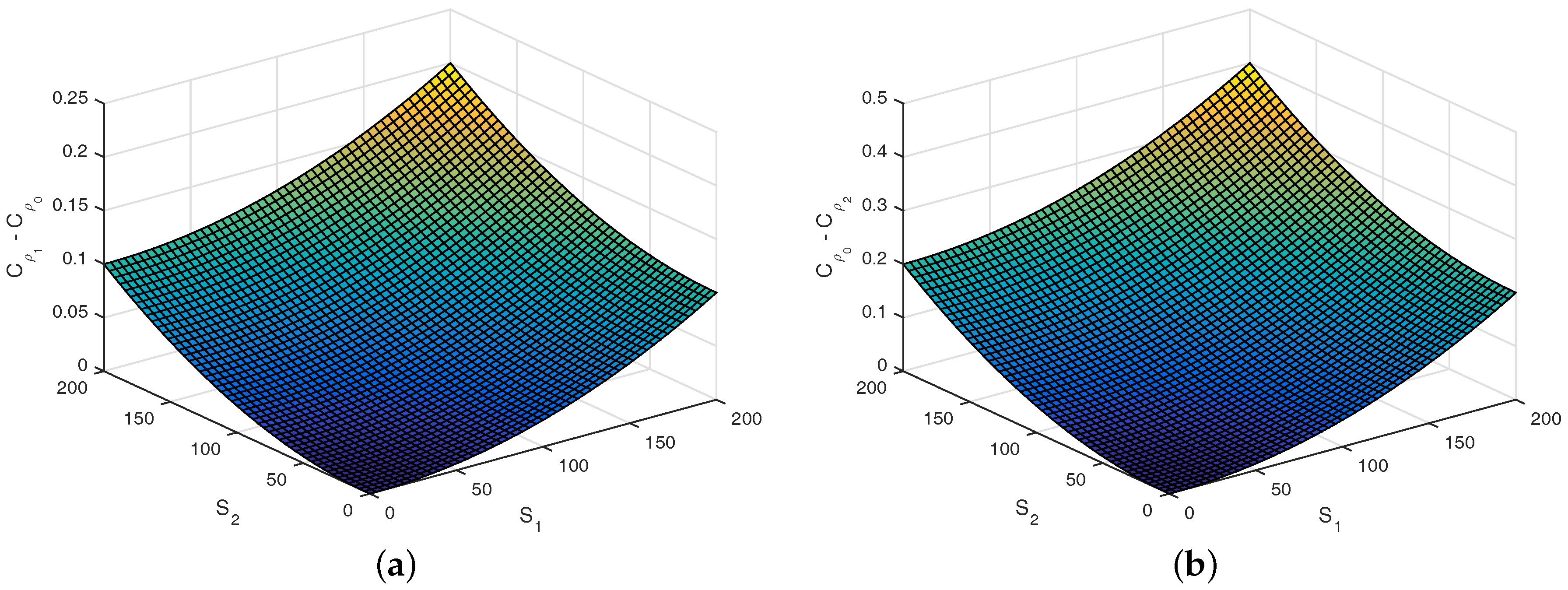

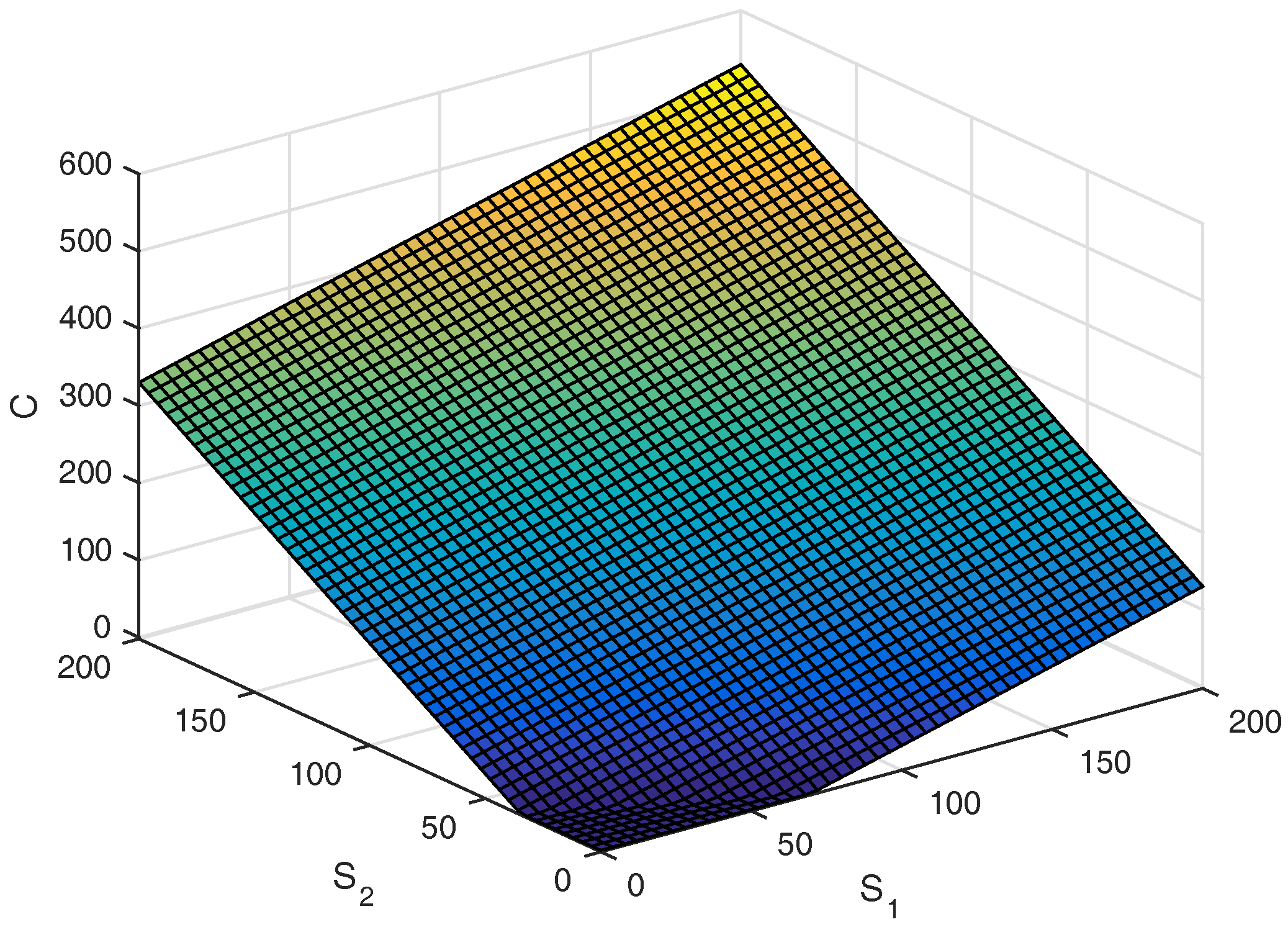

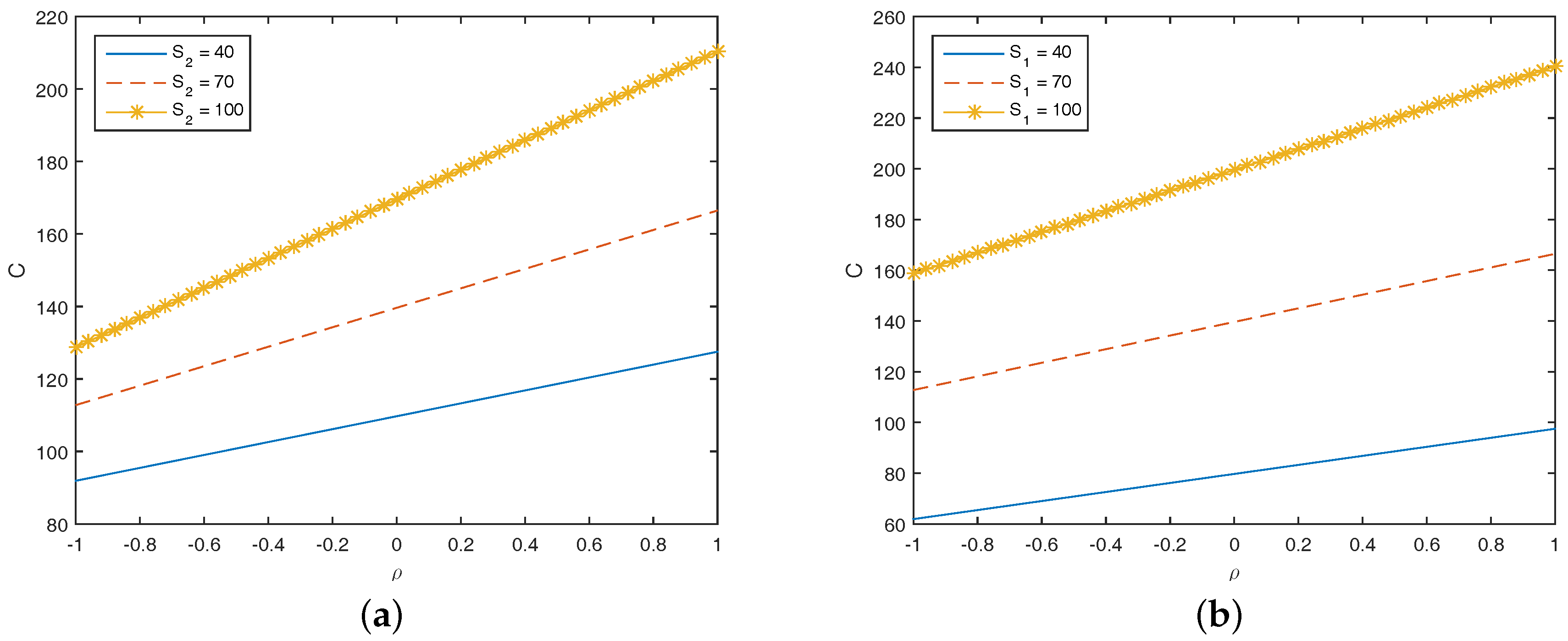

5. Solution Example

6. Conclusions

Acknowledgments

Author Contributions

Conflicts of Interest

References

- Black, F.; Scholes, M. The pricing of options and corporate liabilities. J. Political Econ. 1973, 81, 637–654. [Google Scholar] [CrossRef]

- Buhmann, M.D. Radial Basis Functions: Theory and Implementations; Cambridge University Press: Cambridge, UK, 2003. [Google Scholar]

- Fasshauer, G.E. Meshfree Approximation Methods with MATLAB; World Scientific Publishing Co. Pte. Ltd.: Hackensack, NJ, USA, 2007. [Google Scholar]

- Fasshauer, G.E.; Khaliq, A.Q.M. Using mesh-free approximation for multi-asset american option problems. J. Chin. Inst. Eng. 2004, 27, 563–571. [Google Scholar] [CrossRef]

- Marcozzi, M.D.; Choi, S.; Chen, C.S. On the use of boundary conditions for variational formulations arising in financial mathematics. Appl. Math. Comput. 2001, 124, 197–214. [Google Scholar] [CrossRef]

- Wendland, H. Scattered Data Approximation; Cambridge University Press: Cambridge, UK, 2005. [Google Scholar]

- Jodar, L.; Sevilla-Peris, P.; Cortes, J.C.; Sala, R. A new direct method for solving the Black Scholes equation. Appl. Math. Lett. 2002, 18, 29–32. [Google Scholar] [CrossRef]

- Cen, Z.; Le, A. A robust finite difference scheme for pricing american put options with singularity-separating method. Numer. Algorithms 2010, 53, 497–510. [Google Scholar] [CrossRef]

- Cen, Z.; Le, A. A robust and accurate finite difference method for a generalized Black Scholes equation. J. Comput. Appl. Math. 2011, 235, 2728–2733. [Google Scholar] [CrossRef]

- Cox, J.C.; Ross, S.; Rubinstein, M. Option pricing: A simplified approach. J. Financ. Econ. 1979, 7, 229–263. [Google Scholar] [CrossRef]

- Lesmana, D.C.; Wang, S. An upwind finite difference method for a nonlinear Black Scholes equation governing European option valuation under transaction costs. J. Appl. Math. Comput. 2013, 219, 8811–8828. [Google Scholar] [CrossRef]

- Song, L.; Wang, W. Solution of the fractional Black Scholes option pricing model by finite difference method. Abstr. Appl. Anal. 2013, 2013, 194286. [Google Scholar] [CrossRef]

- Mohammadi, R. Quintic B-spline collocation approach for solving generalized Black Scholes equation governing option pricing. J. Comput. Math. Appl. 2015, 69, 777–797. [Google Scholar] [CrossRef]

- Allahviranloo, T.; Behzadi, S.H.S. The use of iterative methods for solving Black Scholes equation. Int. J. Ind. Math. 2013, 5, 1–11. [Google Scholar]

- Gülkac, V. The homotopy pertubation method for the Black Scholes equation. J. Stat. Comput. Simul. 2010, 80, 1349–1354. [Google Scholar] [CrossRef]

- He, J.H. Homotopy perturbation method: A new nonlinear analytical technique. Appl. Math. Comput. 2003, 135, 73–79. [Google Scholar] [CrossRef]

- He, J.H. The homotopy perturbation method for nonlinear oscillations with discontinuities. Appl. Math. Comput. 2004, 151, 287–292. [Google Scholar]

- He, J.H. Homotopy perturbation method for bifurcation of nonlinear problems. Int. J. Nonlinear Sci. Numer. Simul. 2005, 6, 207–208. [Google Scholar] [CrossRef]

- He, J.H. Homotopy perturbation technique. Comput. Methods Appl. Mech. Eng. 1999, 178, 257–262. [Google Scholar] [CrossRef]

- Khan, Y. A novel Laplace decomposition method for non-linear stretching sheet problem in the presence of MHD and slip condition. Int. J. Numer. Methods Heat Fluid Flow 2014, 24, 73–85. [Google Scholar] [CrossRef]

- Khan, Y.; Abdou, M.A.; Faraz, N.; Yildirim, A.; Wu, Q. Numerical Solution of MHD Flow over a Nonlinear Porous Stretching Sheet. Iran. J. Chem. Chem. Eng. 2012, 31, 125–132. [Google Scholar]

- Khan, Y.; Madani, M.; Yildirim, A.; Abdou, M.A.; Faraz, N. A New Approach to Van der Pol’s Oscillator Problem. Z. Naturforsch. 2011, 66a, 620–624. [Google Scholar] [CrossRef]

- Khan, Y.; Sayevand, K.; Fardi, M.; Ghasemi, M. A novel computing multi-parametric homotopy approach for system of linear and nonlinear Fredholm integral equations. Appl. Math. Comput. 2014, 249, 229–236. [Google Scholar] [CrossRef]

- Khan, Y.; Usman, M. Modified homotopy perturbation transform method: A paradigm for nonlinear boundary layer problems. Int. J. Nonlinear Sci. Numer. Simul. 2014, 15, 19–25. [Google Scholar] [CrossRef]

- Khan, Y.; Vazquez-Leal, H.; Faraz, N. An auxiliary parameter method using Adomian polynomials and Laplace transformation for nonlinear differential equations. Appl. Math. Model. 2013, 37, 2702–2708. [Google Scholar] [CrossRef]

- Madani, M.; Khan, Y.; Fathizadeh, M.; Yildirim, A. Application of homotopy perturbation and numerical methods to the magneto-micropolar fluid flow in the presence of radiation. Eng. Comput. 2012, 29, 277–294. [Google Scholar] [CrossRef]

- Shateyi, S.; Motsa, S.S.; Khan, Y. A new piecewise spectral homotopy analysis of the Michaelis-Menten enzymatic reactions model. Numer. Algorithms 2014, 66, 495–510. [Google Scholar] [CrossRef]

- Khan, Y.; Wu, Q. Homotopy perturbation transform method for nonlinear equations using He’s polynomials. Comput. Math. Appl. 2011, 61, 1963–1967. [Google Scholar] [CrossRef]

- Kumar, S.; Yildirim, A.; Khan, Y.; Jafari, H.; Sayevand, K.; Wei, L. Analytical Solution of Fractional Black Scholes European Option Pricing Equation by using Laplace Transform. J. Fract. Calc. Appl. 2012, 2, 1–9. [Google Scholar]

- Madani, M.; Fathizadeh, M.; Khan, Y.; Yildirim, A. On the coupling of the homotopy perturbation method and Laplace transformation. Math. Comput. Model. 2011, 53, 1937–1945. [Google Scholar] [CrossRef]

- Joonglee, J.; Yongsik, K. Comparison of numerical schemes on multi-dimensional Black Scholes equations. Bull. Korean Math. Soc. 2013, 6, 2035–2051. [Google Scholar]

- Baholian, E.; Azizi, A.; Saeidian, J. Some notes on using the homotopy perturbation method for solving time-dependent differential equations. Math. Comput. Model. 2009, 50, 213–224. [Google Scholar] [CrossRef]

- Mathai, A.M.; Haubold, H.J. Special Functions for Applied Scientists; Springer: New York, NY, USA, 2008. [Google Scholar]

© 2017 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license ( http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Trachoo, K.; Sawangtong, W.; Sawangtong, P. Laplace Transform Homotopy Perturbation Method for the Two Dimensional Black Scholes Model with European Call Option. Math. Comput. Appl. 2017, 22, 23. https://doi.org/10.3390/mca22010023

Trachoo K, Sawangtong W, Sawangtong P. Laplace Transform Homotopy Perturbation Method for the Two Dimensional Black Scholes Model with European Call Option. Mathematical and Computational Applications. 2017; 22(1):23. https://doi.org/10.3390/mca22010023

Chicago/Turabian StyleTrachoo, Kamonchat, Wannika Sawangtong, and Panumart Sawangtong. 2017. "Laplace Transform Homotopy Perturbation Method for the Two Dimensional Black Scholes Model with European Call Option" Mathematical and Computational Applications 22, no. 1: 23. https://doi.org/10.3390/mca22010023

APA StyleTrachoo, K., Sawangtong, W., & Sawangtong, P. (2017). Laplace Transform Homotopy Perturbation Method for the Two Dimensional Black Scholes Model with European Call Option. Mathematical and Computational Applications, 22(1), 23. https://doi.org/10.3390/mca22010023