1. Introduction

Non-performing, overdue debts are regularly incurred in credit cycles, usually to an accelerated extent after a crisis. It is well-documented in the literature that employment is an important factor in repaying household loans. If someone loses their job, the probability of non-payment increases significantly (

Ben-Galim and Lanning 2010;

Balás et al. 2015;

Campbell and Cocco 2015;

Dimitrios et al. 2016). Some recent papers recognized, however, that there is reverse causality, too, as overdue debts have a negative effect on employment as well. According to

Mian and Sufi (

2014), through the housing net worth channel, a decline in the housing net worth reduces consumer demand, hence labor demand. Similarly,

Verner and Gyöngyösi (

2020) showed that overdue foreign currency mortgage loans reduced aggregate demand, leading to job losses, and, thus lowering employment levels and economic growth. However, overdue debts can reduce not only labor demand but also labor supply. For example, through the financial distress channel, deteriorating creditworthiness reduces an employee’s chances of finding a job, keeping a job, or choosing working conditions (

Herkenhoff 2019;

Dobbie et al. 2020). In addition, through the housing lock channel, the deterioration in the collateral value of mortgages leads to a decrease in or a complete lack of labor mobility (

Bernstein and Struyven 2017).

Bernstein (

2017) introduced the household debt overhang channel, which means that due to the renegotiation of overdue debts, repayments become income-contingent, hence debtors become motivated to hide their incomes.

In the present study, we investigate the effects of overdue debts on employments, as well, but in a specific context. Filling a gap in the literature, we do not analyze the debtors in the average situation, but people living in small villages in a disadvantaged region of Hungary. A novelty of our research is that we investigate the relationship between overdue debts and employment in the context of financial exclusion. Financial exclusion is a well-researched area, especially in the US and UK. Still, some vulnerable groups such as rural inhabitants are completely neglected (

Fernández-Olit et al. 2019), overdue debts do not receive enough attention (

Krumer-Nevo et al. 2017), and researchers do not ask unbanked people directly (

Koku 2015). Our study fills a gap in all three respects.

We define debts in a broader sense, including all types that can trigger a debt collection process in the case of non-payment (utility bills, bank loans, and tax liabilities). We introduce a new channel that has so far been unexplored in the literature, such as

escape from debt collection and deductions. At the first sight, it is similar to the household debt overhang channel described by

Bernstein (

2017), but in our case, debts are not renegotiated, so they remain unresolved for decades. The escape from debt collection can curb economic growth in several ways: it can reduce legal employment and the willingness to use a bank account. Moreover, it can damage the mental and physical health of the debtors and their families in the long run due to the constant stress they live with (

Fitch et al. 2011).

Relative to the financial literature focusing on the relationship between overdue debts and employment, in our sample, overdue debts are more common while the institutional system dealing with financial difficulties is less developed and accessible. On the one hand, the Hungarian personal bankruptcy system is much stricter, hence less attractive than in the US and most EU countries. On the other hand, in this special segment, debt renegotiations with banks or debt collectors are much less effective. Debts are relatively small, communication with debtors is more difficult and costly, and the collateral is less valuable compared to the average indebted household. These conditions may explain why small overdue debts remain unsettled en masse and for decades, while large non-performing loans are renegotiated much more efficiently and quickly. Furthermore, larger borrowers can obtain significantly larger discounts (

Tirole 2006) contrary to moral intuition (

Kornai 2016). In our research, the negative effects of overdue debts last typically longer than in the financial literature and undermine economic growth and social cohesion across several business cycles.

Escape from debt collection creates a special poverty trap, as it creates a positive feedback mechanism through which poverty is reproduced and even exacerbated (

Azariadis 1996). Due to overdue debts, the lender avoids declared work and electronic payment, trying instead to make a living from casual work in the black economy and paying for everything in cash. Thus, overdue debtors benefit less from the services of the welfare systems (unemployment benefits, health care, pensions, etc.) and formal financial services (payment services, savings opportunities, loans, etc.), becoming more vulnerable and being forced to make worse compromises (

Allen et al. 2016).

Escape from debt collection as a life strategy severely limits the debtors’ and their families’ capabilities as defined by

Sen (

2014). Several kinds of poverty traps, although based on different mechanisms, were presented by

Banerjee and Duflo (

2011), mainly in relation to education, health, and financial systems.

Mullainathan and Shafir (

2013) examined the mechanism of the debt trap, its psychological, behavioral effects, the ‘scarcity mindset’, and the role of unexpected expenditures.

The thought experiment underlying our empirical analysis is what would happen if long-standing non-performing loans were renegotiated and restructured (combined with partial debt relief), thus the threat of recovery over the debtors’ heads would be averted. Our research aims to find out what impact such a program is expected to have on employment, bank accounts, and the health of the population.

Krugman (

1988) introduced the concept of the so-called debt relief Laffer-curve. According to this concept, debt relief can increase lenders’ income (just like tax cuts can increase tax revenue of the state through improved tax incentives) and, at the same time, a borrower’s well-being by removing barriers to employment and financial inclusion (

World Bank 2012).

Kanz (

2016) examined the impact of the most extensive debt relief program in economic history targeting households (agricultural entrepreneurs) in India and found that the expected positive effects had not materialized. On the contrary, the saved debtors had piled up their informal debts and decreased their investments, and their productivity had fallen compared to debtors who had not been saved.

Mukherjee et al. (

2018), analyzing the same debt relief program, showed that the situation of those who found themselves in difficult situations due to exogenous shocks (weather) and not their own faults have significantly improved and became financially more included. Similar conclusions were drawn by

Dobbie and Song (

2020) on a different sample, performing a randomized controlled experiment on overdue credit card debts in the US.

Ong et al. (

2019) found that debt relief programs positively affected the mental state of the debtors; particularly, anxiety and present-biasedness decreased. Therefore, they supported debt relief programs in addressing poverty.

Academic views regarding the effectiveness of debt relief programs are mixed. Moreover, there are only a few studies in the field, not least because quality data are not available for research. Creditors have the interest to hide information if they agree with the debtor on partial or complete debt relief of non-performing debts, as debt reliefs increase moral hazard (

Fudenberg and Tirole 1990) and lead to the soft budget constraint syndrome (

Kornai 1998). In addition, it is the payment discipline of not only the borrowers who have received the debt relief that deteriorates in the future (if they expect to be rescued again and again) but also of other previously performing debtors if discounts become known. However, examining the decision of US mortgage debtors on strategic default,

Guiso et al. (

2013) found that the willingness-to-pay depends also on non-pecuniary factors, such as fairness and morality.

Bhutta et al. (

2017) also concluded that US mortgage borrowers are reluctant to walk away even if it were beneficial for them, thus, moral hazard can be lower than suspected.

It is clear, therefore, that debt relief programs can have significant individual and social costs and benefits in the long run. In this light, instruments that can efficiently prevent the excessive build-up of households’ credit risk and are also able to address complex tradeoffs in case of crisis can create huge value. The present study is aimed at contributing to the development of more efficient debt relief instruments.

Section 2 discusses the hypotheses of the study. In

Section 3, the considered database is presented.

Section 4 provides a comparative description of households living with and without overdue debts.

Section 5 analyzes the impacts of overdue debts in a multivariable setting. Finally, the conclusions are summarized in

Section 6.

2. Development of Hypotheses

At the start of this research, we conducted 14 in-depth interviews with local residents, mostly women, in a chosen settlement of Borsod-Abaúj-Zemplén (BAZ) County. We collected information on households’ financial management, their savings, and borrowing habits. During the interviews, the issue of utility, bank, and other debts and problems arising from default was raised several times.

In many cases, the pattern emerged that the household obtained general-purpose, consumer, or mortgage credit(s) from banks either in Hungarian forint (HUF) or in foreign currency and then failed to repay them due to some exogenous shock (job loss, health deterioration, exchange rate and interest rate changes, etc.). Banks handed over non-performing loans to debt collectors, and, since then, overdue debts have just further accumulated.

The formal process for dealing with overdue debts can be summarized as follows. We distinguish three stages if the debtor does not pay his debt. The

recovery phase is the first 90 days after arrears, during which the creditor actively contacts the debtor and seeks alternative solutions for payment. If the debtor is overdue for more than 90 days (with the repayment of a bank loan, utility bill, etc.), the unpaid financial obligation enters the

claim phase. The lender will usually continue to look for alternative solutions, but the claim will be handed over to a claim manager. After 180 days from the date of non-payment, in the

enforcement phase, the contract is terminated, the claim is sold, and debt is collected based on out-of-court or in-court proceedings. In addition to penalty interest, the collection and enforcement costs borne by the debtor can significantly increase the debt’s value. The debtor’s assets, income, and movable and immovable property are under the scope of enforcement. Hungarian legislation does not recognize the institution of

datio in solutum. If the collateral of the loan is not sufficient to repay the outstanding debt, the debtor remains liable for the outstanding part of the debt. During the enforcement, movable and immovable property may be sold to cover the outstanding debt, and a certain amount may be automatically deducted from the debtor’s registered tax-paying income before the debtor receives it (

MNB 2019). Act LIII of 1994 on Judicial Enforcement states that the claim must be recovered primarily from the debtor’s wages; the amount recovered may not exceed 33%, or, exceptionally, 50% (e.g., in case of child support or multiple foreclosures). Accordingly, the debt collector is required to examine whether the debtor has a declared job.

Our interviewees, who reported overdue debts, were already in the enforcement phase without exception, so all their legal income was subject to a 33% or 50% deduction. As the market value of the movable and immovable property is typically very low in this segment, foreclosures and evictions were not worthwhile for the debt collectors; consequently, unresolved debts have persisted for many years, and the penalty interest has accumulated. The initial loans of a few hundred thousand forints have since grown to debts of several million. The creditors renounced ever being able to repay these huge sums, so they gave up trying. Letters sent by debt collectors are not even opened, the exact amount of the debt is not known. The debtors equipped themselves to hide their incomes and potential savings from debt collectors throughout their lives. Interviewees reported that, in many cases, they do not apply for registered jobs or open a bank account specifically because of overdue debts. Overdue debts have a negative effect also on debtors’ mental and physical health. They are angry at banks and debt collectors, feel misled, and do not want to have any business with the banks, thus accepting their long-term financial exclusion.

Based on the existing literature and the findings of the in-depth interviews, we formulate the following three hypotheses in relation to the negative impacts of overdue debts:

Hypothesis 1 (H1). Debtors with overdue debts are less likely to apply for a registered job.

Hypothesis 2 (H2). Debtors with overdue debts are less likely to open a bank account.

Hypothesis 3 (H3). Debtors with overdue debts suffer from worse mental and physical conditions than debtors without overdue debts.

In the following sections, we examine these hypotheses in detail based on the questionnaire survey.

3. Data Collection

To collect targeted data, Soreco Research Limited conducted a questionnaire-based survey in March and April 2019, on behalf of the Corvinus University of Budapest and under the framework of the “Financial and Public Services” research project of the Higher Education Institutional Excellence Program. All the procedures were performed in compliance with relevant laws and institutional research ethical guidelines. The research focused on the financial management of households in the small settlements of BAZ County. The sample is representative of non-urban households in the county. Data were collected by personal interviews, via the so-called multistage stratified random sampling procedure.

In the first stage of the sampling procedure, the settlements to be sampled were selected and the number of households to be interviewed in each settlement was determined to reflect the proportion of the non-urban population of the districts. In the second stage of sampling, the interviewers selected the households to be interviewed using a predetermined selection algorithm, the so-called random walk method. In other words, households were not selected based on a preliminary address list but randomly. In the given settlement, there was a pre-recorded starting point. From this starting point, based on a fixed-route algorithm, every fifth household was selected for an interview. In each household, the household member most competent in financial matters was asked to complete the questionnaire. If the randomly chosen household refused to respond, the nearest household was contacted. Sampling was carried out anonymously, and no personal data were collected, so households cannot be identified.

In total, we have information on 504 households and 1794 individuals; 1196 were of active age (18–65 years), and 179 had overdue debts. Households with no active-age members were excluded from the analysis. Of the remaining 496 households, 136 were inhabited by individuals who had some form of overdue debts (177 individuals in total). The questionnaire included questions for each adult, for the household, and for the respondent only. Economic activity, the possession of a bank account, and overdue debts play a key role in our analysis, and information on these is known for all adult members of the interviewed households. The majority of the respondents (72%) were women as they were more familiar with household financial management. See

Appendix A for details on the variables used in the analysis.

4. Descriptive Statistics

In this section, we use data obtained from the questionnaire to characterize the individuals and households with and without overdue debts. First, we present the results of a direct inquiry on what the respondents think about the causal relationships formulated in H1, H2, and H3; second, we perform a one-dimensional comparative analysis of their characteristics.

4.1. Direct Inquiry

In the questionnaire, we asked directly whether the interviewee knows someone who, because of his or her overdue debts and the fear of debt collection does not take up a declared job (H1), does not open a bank account (H2), or has experienced a deterioration in his or her health (H3). Respondents also had to indicate whether this kind of causality exists for him- or herself, for a close family member living in the household, for somebody in the wider family, or for someone living in the settlement or in a wider circle of acquaintances.

Nearly half of all respondents (49%) know someone who does not have a declared job because of overdue debts. Similarly, nearly half of the respondents reported the negative effects of overdue debt on bank accounts and health (45% and 58%, respectively). Considering only the households with overdue debts, almost a quarter of the respondents reported that there is at least one person in their household who, specifically because of the outstanding overdue debts, does not take up a declared job (18%), does not open a bank account (21%), or has experienced a health deterioration (34%). It is noteworthy that the deterioration in health, both in a narrower and wider context, was given greater emphasis by the respondents than the other two consequences.

We examined those households where no one had a bank account (30% of all households) in more detail. In previous research, representative of the whole country, the proportion of such households was lower: 24% (

Illyés and Varga 2015) and 17% (

Horn and Kiss 2019). In our case, the main reason for the lack of a bank account was that it is not needed (60%) and/or it is too expensive (51%), but 21% of the respondents referred to the fear of debt collection. At the national level, 90% of those who did not have a bank account said they did not need it, 25% said it was too expensive, 10–11% did not trust credit institutions, and 3–4% feared security risks (

Illyés and Varga 2015). We note that the questionnaire of

Illyés and Varga (

2015) did not include the possibility of fear of debt collection, hence such fears probably appeared in the answers “do not trust credit institutions” and “fear of security risks.” Clearly, in our sample (villages of BAZ County), costs play a significantly larger role than in the national-level sample, which may be due to lower incomes.

Although not listed in

Table 1, we also directly asked the interviewees about the extent to which overdue debts are a problem in general. According to respondents, this is a serious problem in their immediate environment (66%), in the village (81%), and nationally (89%).

The answers to the above questions are consistent, and we have no reason to suspect that the interviewees did not understand the questions or that the answers were significantly distorted for other reasons, although smaller biases are possible in both directions. At the level of the closest family members, due to the personal involvement and the need for self-discharge, the impact of overdue debts may be somewhat exaggerated. On the other hand, respondents are likely to admit neither overdue debts nor hiding from enforcement. Therefore, the two opposite biases may extinguish each other to some extent. At the same time, at the level of a wider circle of acquaintances, the lack of information may have skewed the responses downwards. Nevertheless, if there is some bias, the respondents are more likely to present the problem as being less severe than it is. The above results, therefore, support our hypotheses based on in-depth interviews.

4.2. Comparative Analysis

Next, analyzing the answers to the questionnaire, we examine whether the statistical characteristics of the sample are consistent with our hypotheses. Our primary goal is to characterize individuals and households with and without overdue debts. In some cases when data were missing, observations were removed from the sample.

Table 2 shows the extent to which the subsamples of individuals with (179 individuals) and without (1017) overdue debts differ from each other. Variables in bold are included in the multivariate regression analysis to examine the combined effects of the variables (in

Section 5).

Looking at the full-time jobs or all declared jobs in

Table 2, the difference is notable for the two subsamples (31 and 32 percentage points, respectively) and statistically significant. Hence, there is a close negative association between employment and overdue debts. However, it is not clear whether overdue debts cause lower employment (overdue debts → employment) or vice versa, the lack of employment causes non-payment (employment → overdue debts). It is likely that both effects occur simultaneously and this positive feedback loop creates a vicious circle leading to a poverty trap. Considering that the year 2019 (when the survey was taken) was characterized by a strong economic boom and general labor shortages, we can assume that the causality of interest (overdue debts → employment) was strongly present as someone who wanted a full-time and declared job during this period had plenty of opportunities. Anecdotes also support the fact that, in many cases, employers offer special employment contracts specifically designed to avoid deductions (for example, by paying the wages in cash with daily settlements); moreover, some foreign job opportunities have been advertised explicitly as a tool to evade debt collections.

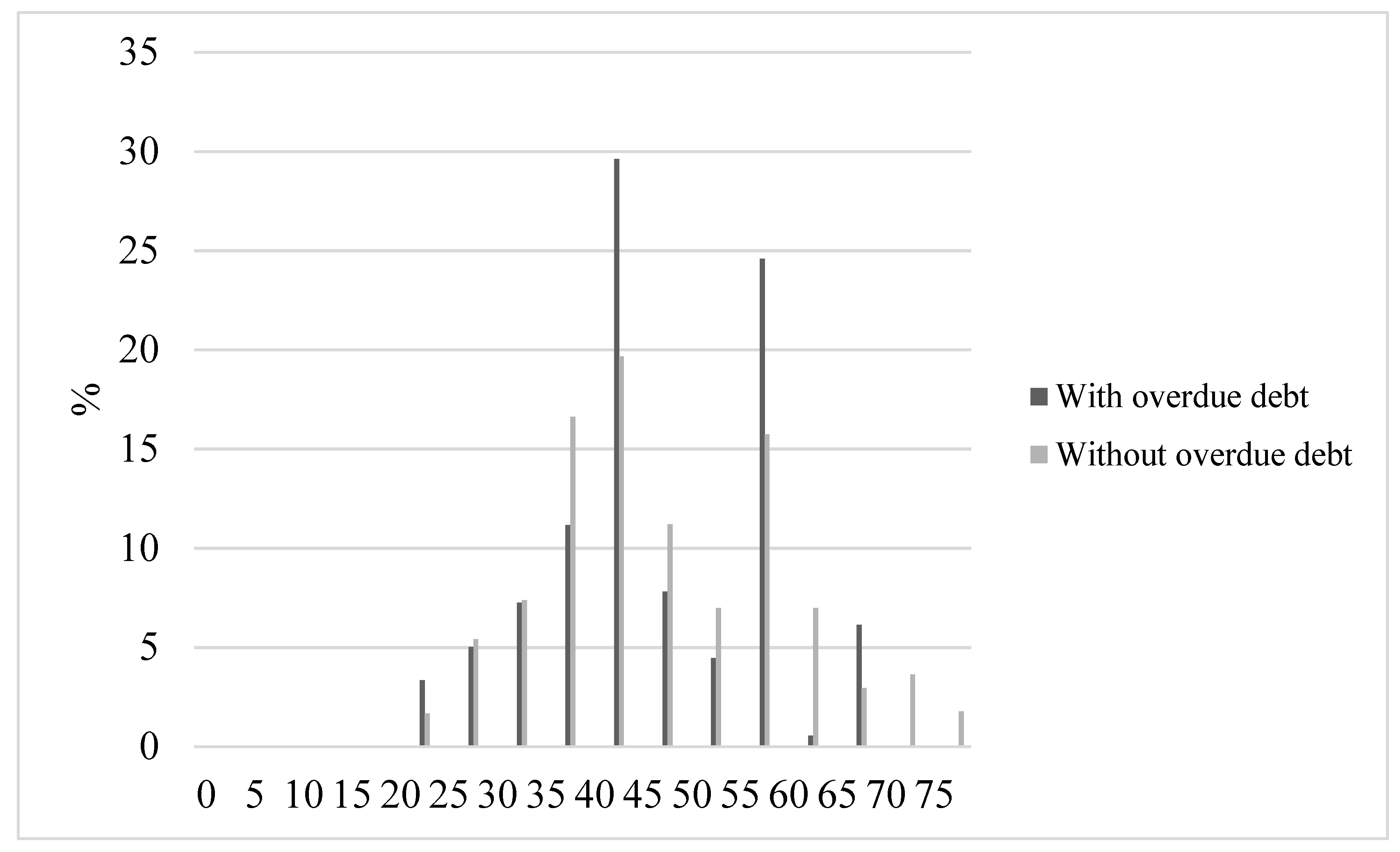

There is no difference in gender between those with overdue debts and those without. Those with overdue debts are a few years older, but the difference, while statistically significant, is not remarkable.

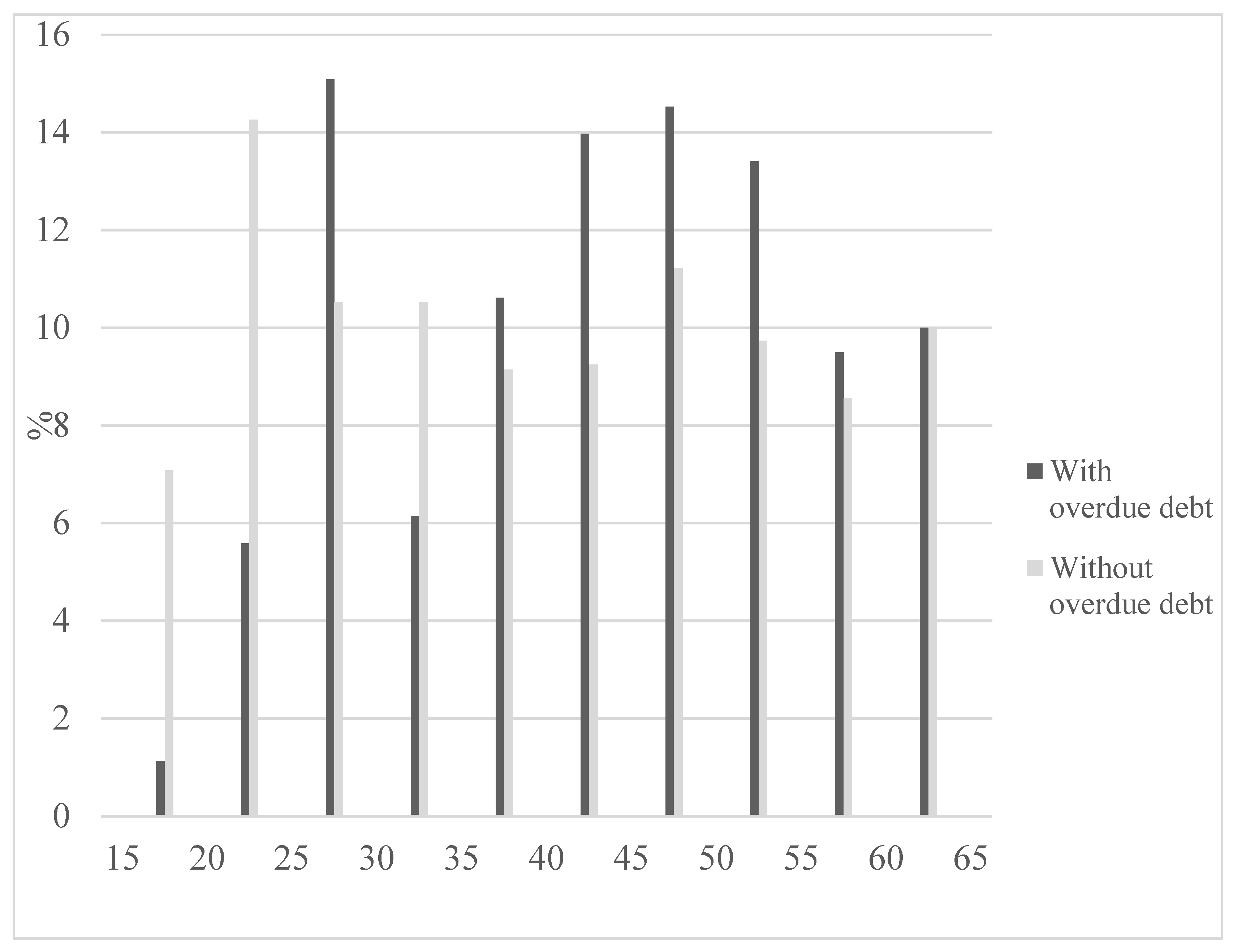

Figure 1 shows that the relationship is non-linear (middle-aged people are more likely to take out a loan and more likely to become insolvent than young or older people).

In terms of education, we found a significant difference (Mann–Whitney test p-value = 0.000) between the two subsamples. Those with overdue debts have a lower education level in general. Among them, the proportion of those who have not completed the eight classes of elementary school is significantly higher, and the proportion of those who do not have a high school diploma is significantly lower. As education can have an effect on both overdue debts and employment, we will control for this variable in the multivariate regression model.

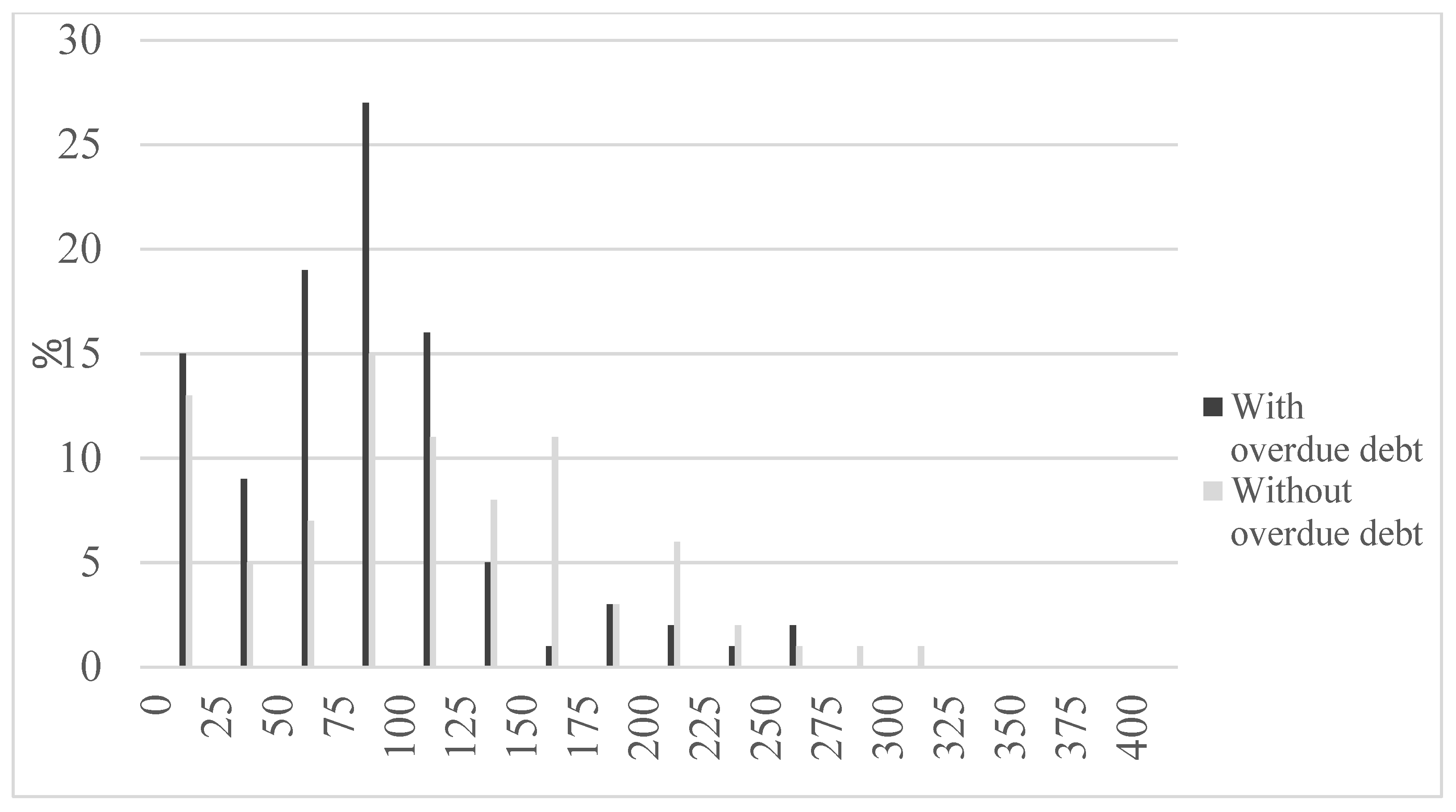

The net income from work in the previous month is strongly correlated with declared and full-time jobs. The difference is significant in this respect, too, as those without overdue debts have an income advantage of more than HUF 35,000.

Figure 2 shows the distribution of net incomes across the two subsamples.

We find that in the lower-income categories overdue debtors are significantly overrepresented. Returning to

Table 2, bank account ownership is much (28 percentage points) lower among those with overdue debts, and the difference is significant, which is in line with our expectations. In the regression analysis, we examine bank account ownership in detail as a dependent variable. Few data are available on the size of the loan instalments and the data are not reliable because the respondents were uncertain about the instalments.

Those with overdue debts have significantly more children and, thus, significantly larger families (see

Table 2); this raises serious questions about child protection and intergenerational social mobility (these issues, however, go beyond the scope of this study). In a household, per capita income is significantly higher where there is no overdue debt, but it is not much different from the individual incomes’ measures. Contrary to our previous expectations, there is no difference between the two groups in terms of whether there was a foreign currency loan in the family or not (

Bethlendi 2011;

Verner and Gyöngyösi 2020). At the household level, we define the so-called ability-to-pay ratio, which is the total monthly net income of the household divided by the total monthly expenditure. The financial situation of a household is characterized by this ratio being below, equal to, or above 1 (see

Figure 3).

As shown in

Figure 3, a significant proportion of households—more than half—spends all their monthly income for the living costs even in the subsample without overdue debts, at least in terms of official incomes. Unsurprisingly, households that have difficulty financing their monthly living expenses have more overdue debts.

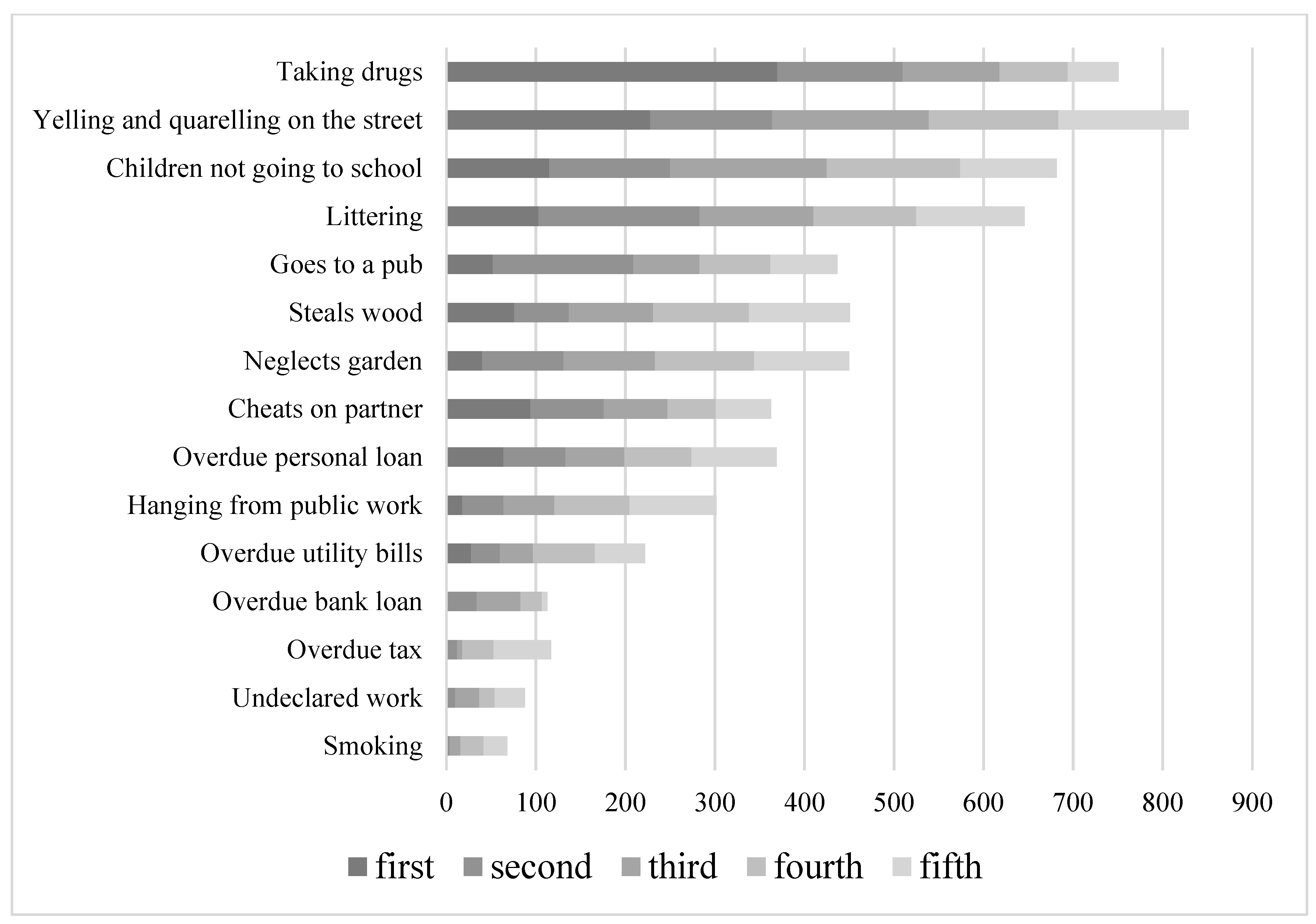

In the questionnaire, we listed some behaviors that are mostly convicted by society. Respondents were asked to select and rank the five behaviors they believe are most convicted by those living in a given settlement.

Figure 4 shows the results for the entire sample.

Figure 4 shows that yelling and quarrelling on the street is believed to be the most convicted behavior; if we look at the number of first ranks (i.e., highest negative rank), it is drug use. Interestingly, non-payment of personal loans, utility bills, bank loans, and taxes are seen as much less negative behavior. Non-payment of official debts (utility bills, bank loans, taxes) in particular seems to be a “forgivable sin,” with only undeclared work and smoking being less convicted.

Based on the responses in

Figure 4, we assigned a composite index specific to the respondent—the perceived social aversion—separately to overdue debts and to undeclared work. The former was calculated so that the behaviors “overdue utility bills”, “overdue bank loan”, and “overdue tax” received 5 points if the behavior was ranked first; 4, if ranked second; 3, if ranked third; 2, if fourth; and 1, if fifth (zero, if not mentioned in the first five), and then these points were averaged over the three behaviors. The (perceived) aversion to undeclared work was quantified in the same way (but it did not need to be averaged because there was only one such behavior). The variable of perceived social aversion reflects higher perceived rejection if its value is greater. This is a perception that contains objective and subjective elements; we did not separate these in our analysis. What matters for our estimates is what the respondent thinks about the level of aversion in his or her environment, as it may have a direct impact on loan repayments.

In

Table 2, the perceived social aversion to overdue debts is significantly smaller among those who have overdue debts, which seems logical. Interestingly, there is no difference between the two subsamples in terms of aversion to undeclared work.

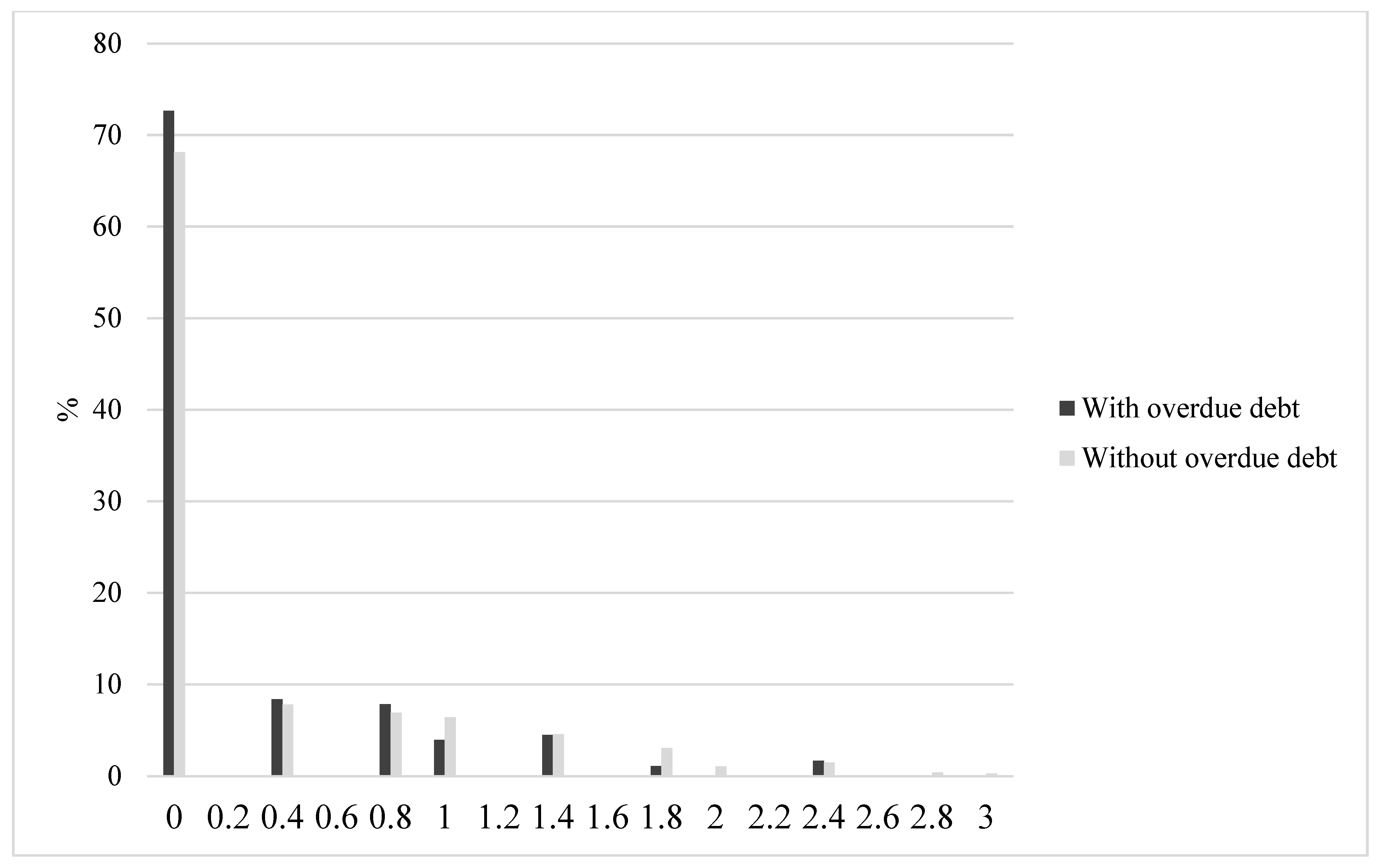

Figure 5 shows the distribution of perceived social aversion to overdue debts across the two subsamples.

Perceived social aversion to overdue debts differs significantly in the two subsamples: those with overdue debts think less that society convicts them for this behavior and vice versa.

The development of the settlement was measured with the Hungarian Central Statistical Office’s composite settlement indicator and a significant difference was found (see

Figure 6).

The composite settlement indicator aggregates a number of different characteristics in terms of society, demography, housing and living conditions, the local economy and labor market, infrastructure and environment. In

Figure 6, both subsamples show a two-mode distribution, which can be explained by the settlement structure of BAZ County. Although difficult to discern in the figure, those with overdue debts typically live in less developed settlements. This difference may also affect both overdue debts and employment, therefore, we include this variable in the multivariate regression analysis in

Section 5.

We can find one health variable in

Table 2 that relates to the household, it is “chronic illness”, indicating whether there is a family member in the household not able to work due to poor health conditions, which occurs 10 times more frequently among those with overdue debts. The other health variables (addictions, health status, mental status, etc.), relating directly to the respondent, also show significant differences in favor of those without overdue debts, with the exception of alcohol and medication. Surprisingly, there are more heavy drinkers among those without overdue debts, but the difference is significant only at the 10% level. In this respect, the fact that the majority of respondents are women may distort the picture. When investigating the impacts of overdue debts on health (H3), we compute an aggregate health index from the above variables.

5. Multivariate Analysis

In this section, we examine the variables’ overall effects on employment, bank account, and health in multivariate linear regression models, with a particular emphasis on overdue debts as a possible explanatory variable. The Ramsey RESET test supports the use of linear models in all three cases. The control variables in the linear regression models were chosen to meet two requirements. First, the questionnaire answers should be reliable, and second, drawing a map of causality, we identified those variables that have an effect on both the dependent variable and the main explanatory variable (overdue debts); hence, their omission would have brought endogeneity to the model. For all independent variables, vector inflation factors are below 5, indicating no multicollinearity problems.

We checked several specifications during the robustness tests, and the most realistic variants are presented below.

Education is further detailed as a category variable: less than 8 classes of elementary school (reference point), elementary school, vocational exam, high school diploma, and university degree. In addition to age, the square of the age is also included in the model to take into account the potentially nonlinear relationship between age and employment. The detailed content of the variables is described in

Section 4 and in

Appendix A.

5.1. Overdue Debts and Employment

Our first hypothesis states that overdue debts have a negative effect on declared work because debtors try to avoid debt collections. In principle, overdue debts (especially mortgage loans) might affect labor supply through other channels as well (housing net worth, financial stress, housing lock, household debt overhang, etc). These causes, however, were not mentioned by the interviewees; thus, our analysis focuses only on the escape from debt collection channel.

Table 3 shows the regression results separately for any type of declared work and for only the 8-h declared job (full-time job) as dependent variables.

As shown in

Table 3, there is a strong relationship between declared work and overdue debts; on average, ceteris paribus, the probability of having a registered job is 23 percentage points lower in the case of overdue debts. Middle-aged men with more degrees are more likely to have a declared job. The ability-to-pay ratio (total official net income of the household/total living expenses) is not significant for employment either economically or statistically; it is likely that the effect is (partly) overtaken by other variables like overdue debts and education. There is a negative correlation between declared job and the variable “chronic illness”. The development of the settlement has a significant direct impact on employment: one standard deviation increase in the value of this variable increases the likelihood of having a registered job by almost 4 percentage points. If we examine the impact of overdue debts only on full-time jobs, we receive similar results.

The question may arise as to whether the coefficients shown above also represent a direction of causality. Due to overdue debts, employment is lower or vice versa, and due to the lack of declared work, repayment is more difficult and therefore the probability of overdue debts will be higher (

Ben-Galim and Lanning 2010;

Balás et al. 2015;

Campbell and Cocco 2015;

Dimitrios et al. 2016). In the above model, we account for a number of explanatory variables affecting both overdue debts and employment, but it is worth considering what other potential confounding variables may be omitted from the analysis. Such omitted variables can be personality traits, such as reliability, accuracy, and conscientiousness, which are likely to have a negative impact on overdue debts and a positive impact on employment. Thus, these omitted variables are likely to skew the coefficient of overdue debts downwards. This could mean that the 23% and 21% negative impacts on declared work and full-time jobs, respectively, are overestimated. In absolute terms, somewhat smaller coefficients are more realistic. Patience and risk-taking may also be important additional missed variables, but their respective impacts are less clear. In any case, large negative coefficients are consistent with the results of the direct inquiry in

Section 4.1.

Since our analysis focuses specifically on the “overdue debts → registered work” effect, we also examine the relationship through a specific instrumental variable, the perceived social aversion to overdue debts.

A suitable instrumental variable IV is required to (i) affect the assumed explanatory variable X, (ii) be independent of the control variables Zi, and (iii) have no direct impact on the outcome variable Y (only via X). In practice, it is usually difficult to find a variable that unarguably meets all expectations. We show below which results it leads to; if X is the overdue debts, Y is the declared job, and the IV is the perceived social aversion to overdue debts.

Figure 4 and

Figure 5 show the distribution of perceived social aversion of each behavior in the studied population. To recap, interviewees were asked to select from a pre-defined list and rank the five most convicted behavioral patterns, based on which we calculated a composite indicator for overdue debts (utility bills, bank loans, tax). We then extended this indicator to all members of the household.

The composite indicator—the perceived social aversion to overdue debts—is presumably not strongly related to the control variables as the question refers to the opinion of the village. At the same time, it is possible that the individual view on the opinion of the village is also determined by individual and household characteristics. In any case, in our sample, the perceived social aversion to overdue debts hardly correlates with any other control variables; therefore, the hypothesis of independence cannot be rejected. It is possible that there is a link between various deviant behaviors, such as undeclared work and refusal to pay loans. However, we did not find any indication of this in a statistical sense. It is also possible that societal expectations may change, for example, because of an exogenous shock. The foreign currency credit crisis in Hungary (

Bethlendi 2011) could be considered as an exogenous shock, as a result of which, the society may become less likely to convict those who do not pay their debts if the proportion of non-paying households increases (

Becker and Murphy 2000). In our database, however, there is no significant relationship between foreign currency loans and the perceived social aversion (Mann–Whitney test

p value is 0.391). The relationship is examined by breaking down by settlements, but the

t-tests and Mann–Whitney tests do not indicate a relationship between the two variables. Further, the development of the settlement can, in principle, be related to social aversions, but we do not see a close correlation here either (+0.05). Logically, we can assume that the perceived social aversion to overdue debts affects the repayment of loans but does not directly affect employment, except through the channel of overdue debts, so it can be considered as a suitable instrumental variable in this context.

In a linear probability model (LPM), we first regress the variable X (overdue debts) and then the variable Y (declared work) on the IV (perceived social aversion to overdue debts), and we get the values of −0.033 and +0.133 for the coefficients (the standard error is 0.018 and 0.024, respectively), which implies 0.133/−0.033 = −4.03 coefficient for the relationship between X and Y. Although the signs are as expected, the coefficient of 4.03 is incomprehensible in the LPM. By performing the same analysis but in a logit regression model, we conclude that overdue debts reduce the chances of the debtor having a declared job by 14%.

Despite the theoretical and practical limitations of our analysis based on the selected instrumental variable, the estimated coefficient of 14% seems realistic, considering the results of the in-depth interviews, direct interviews, and multivariate regression analyses accounting for the effects of the potential omitted variables.

Bernstein (

2017) found on a sample of US mortgage borrowers representative for the whole population that overdue debts decrease employability by 2–6%. Our estimate (14%) is much higher, not least because our sample is representative of people living in small villages in one of the most disadvantaged counties of Hungary.

5.2. Overdue Debts and Bank Account

As a next step, we examine our second hypothesis more closely, namely that overdue debts have a negative effect on bank account ownership. Bank account ownership is the best proxy for financial inclusion as this is the prerequisite for all other financial services (

Allen et al. 2016). Several studies showed a close relationship between declared work and a bank account (

Illyés and Varga 2015;

Koku 2015;

Allen et al. 2016;

Krumer-Nevo et al. 2017;

Horn and Kiss 2019;

Fernández-Olit et al. 2019). Thus, if overdue debts negatively affect declared work (see

Table 3), these can indirectly affect bank accounts too. However, based on the in-depth interviews, we assume that there is a direct channel between overdue debts and the bank account, as well, through the

escape from debt collection channel.

Table 4 shows the results of the multivariate regression analysis. To make our results comparable with the results of similar, albeit nationally representative research (

Illyés and Varga 2015;

Horn and Kiss 2019), we extended our regression model with net income and declared work.

Opening a bank account is impacted by the banking services’ accessibility which is not necessarily reflected in the settlement development indicator. Therefore, we used district dummy variables instead of the settlement development indicator. District dummies proved to be significant, indicating remarkable differences between different regions in terms of the available banking services.

According to

Table 4, overdue debts are negatively related to bank accounts: if an individual has overdue debts, the likelihood of using a bank account decreases by 9 percentage points on average ceteris paribus. A declared job increases the chances of using a bank account by 21 percentage points, and, in line with our expectations, the income has a positive impact on bank account ownership. If net income and employment is left out from the model, the coefficient of overdue debts increases to 15 percentage points.

Women are more likely to open a bank account, but this finding is not robust across different model specifications. The use of a bank account initially increases with age, which is consistent with the results of (

Illyés and Varga 2015;

Horn and Kiss 2019). However, in our sample, there is no subsequent negative effect of age, probably because we only examined those of active age (18–65 years). Education also has a strong effect on our dataset: the higher the degree, the higher the probability of having a bank account, and the magnitude of this effect is similar to the findings of (

Illyés and Varga 2015;

Horn and Kiss 2019). The coefficients of the variables “ability-to-pay” and “chronic illness” have the expected sign, but they are only significant in model specifications without the net income and employment variables.

5.3. Overdue Debts and Health

In this section, we investigate our third hypothesis i.e., overdue debts have a negative impact on health. Health is measured by a factor derived from 10 variables related to mental and physical health (smoking, alcohol, medication, stressed, hopeless, tired, unhappy, no socializing, dissatisfied with health, and chronic illness) using a principal component analysis. Based on the KMO value (=0.605) and the Bartlett test (

p-value is 0.000), we determined one common factor, the so-called unhealthy index. The higher the value of the unhealthy index, the worse the health condition of the individual (the value of the index varies between −1.54 and +2.37). In

Table 5, the outcome variable is the unhealthy index and the main explanatory variable is overdue debts again, and we control for important individual-, household-, and settlement-level variables.

Variables determining the unhealthy index are known only for the respondents, therefore, in this model, the number of cases is only 480 (some did not provide the information needed to produce the unhealthy index). While in the case of employment and the bank account, the negative effects occur only in the case of a person with overdue debts; the stress caused by overdue debts can destroy the mental and physical health of the whole family. So, in this model, the main explanatory variable—overdue debts—indicates whether there are overdue debts in a given household or not.

As expected, the sign of the coefficient of overdue debts is positive and significant in both specifications, which means that overdue debts destroy health.

Table 5 also suggests that, in absolute terms, the size effect of overdue debts on health is comparable to that of a vocational exam or a high school diploma after completing elementary school. Age is not significant, but gender is, women have slightly worse health in this sample. Education matters again, the more someone studies, the healthier they live. Similarly, the ability-to-pay ratio, which is a more balanced family budget, has a positive impact on health too. Net income is irrelevant, and surprisingly, declared work has a weak negative impact on health. Having had a foreign currency loan in the past has no significant impact. Similarly, the settlement development is not significant, and controlling for this effect at the district level instead of the settlement level does not significantly change the results. The above models, thus, support the negative relationship between overdue debts and health revealed during the in-depth interviews and through the direct inquiries.

6. Conclusions

We examine the negative impacts of overdue debts on employment, bank accounts, and health using several methods (in-depth interviews, direct inquiries, and statistical analyses). According to our estimations, overdue debts reduce the likelihood of having a declared job by nearly 14 percentage points. Not having a declared job reduces the probability of owning a bank account by 21 percentage points; in addition, overdue debts further decrease the probability of having a bank account by 9 percentage points. Furthermore, overdue debts have a negative effect on the health of the family members living in the household of the debtor, and this negative effect is roughly of the same magnitude as the positive impact of obtaining a vocational certificate or a high school diploma after completing primary school.

Overdue debts slow down economic growth not only through the decreased labor demand, as (

Mian and Sufi 2014;

Verner and Gyöngyösi 2020) showed, but also through the decreased labor supply as we presented. Overdue debts can have negative effects not only in a crisis but also in a boom for many decades thereafter.

Our research methodology has limitations. Most of all, one can never be sure that endogeneity is fully excluded from the models. Endogeneity can emerge from simultaneous causality, omitted variables, and measurement errors (

Bascle 2008). In our multivariate regression models with control variables, all three are relevant issues. Therefore, we performed an additional analysis using an instrumental variable (perceived social aversion to overdue debts) as well. Literature review, in-depth interviews, direct inquiries, multivariate analysis, instrumental variable method, and robustness checks strengthen each other and indicate that our results are reliable. The intuitive new channel (

escape from debt collection) and the comprehensive and representative survey data also add to the quality of our research.

We can conclude that overdue bills, tax, and bank loans have similar effects on employment, bank services, and health through the escape from debt collection channel. The estimated size effects refer to a disadvantaged population in Hungary, and these proved to be highly significant in economic terms. Results can be generalized for other populations of overdue debtors, too, as debt collection can create perverse incentives and poverty trap mechanisms everywhere if overdue debts are not settled effectively. Of course, side effects can vary widely depending on institutions, personal bankruptcy systems, labor market tendencies, cultural factors, etc.

To reduce the negative social and economic impacts of overdue debts, policymakers should pay more attention to attenuating credit cycles (debt control rules, consumer protection, and other anticyclical policies) and settling non-performing debts, especially in this fragile segment of the society.

Thus, specific debt relief programs are needed, and state intervention can be justified by the positive external effects in terms of employment, growth, tax income, subsidies, health care costs, children’s perspective, black economy, etc. Most of all, we argue in favor of more lenient personal bankruptcy regulations to promote the fresh start of overdue borrowers and their families. A bad financial decision should not ruin entire families.

Market-based debt renegotiations should also be more effective for example by using FinTech solutions (for example, online platforms for renegotiations and bargaining, income-contingent repayments, smart contracts and decentralized clearing, etc.). According to (

Kshetri 2017;

Fernández-Olit et al. 2019) this is an under-researched but promising direction.

Our results indicate that well-designed debt relief programs could be attractive for borrowers, too, as hiding from credit collectors for a lifetime has high personal costs. In these programs, moral hazard issues should be carefully addressed. International evidence suggests, however, that moral hazard can be much less serious as it is widely believed (

Guiso et al. 2013;

Bhutta et al. 2017).

As far as development policies are concerned, we believe that financial inclusion is not possible without the settlement of existing overdue debts. This must be the first step and well before promoting saving accounts and regular savings plans.

Our database is not suitable for estimating the extent of the problem at the national level. This would require a sufficiently detailed representative sample of the entire population with a large number of observations. A critical study of existing debt relief programs and the development of possible solutions would also require a separate study.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}