Abstract

Organizational strategic programs are continuously evolving and gaining the attention of policy makers in order to construct organizations’ ecological and socioeconomic systems. The purpose of this study is to examine the relationship between the balanced scorecard (BSC) and sustainable development involving the mediated effect of political and regulatory influence. To achieve the core objectives of the research, the quantitative (positivism) research method is applied. The goal of the current research is made possible through the quantitative method because of its objective nature of reality. A total of 320 questionnaires were distributed among the different levels of managers; 280 respondents returned the questionnaire. The data are analyzed through a modern statistical tool called Smart-PLS, Partial Least Squares (PLS) is high graphical user interference software that is used to calculate Structural Equation Modeling (SEM) through PLS path modeling. Factor analysis is conducted to eliminate the variables that have no contribution and to reduce the variables to obtain better results in regression. The implications are for energy organizations that are struggling to deal with sustainable development and these tools can help them to achieve their sustainability goals. The study concludes that the adoption of BSC is essential to ensure sustainable development regardless of its challenges. Moreover, consideration of meta-constitutional rules as political influence is important to understand and address in order to mitigate financial loss. In nutshell, the use of BSC is highly recommended to eliminate the routine problems and to ensure environmental sustainability.

1. Introduction

The strategic agenda of companies is evolving and gaining the attention of policymakers aiming to improve organizations’ competitiveness. It is pivotal to investigate emerging issues of the balanced scorecard (BSC) because it significantly contributes to organizational success and sustainability (Kaplan et al. 2001). A balanced scorecard is a comprehensive framework of decisions and actions that results in the development and application of strategy designs for the organization’s goals (Singh and Arora 2018). In today’s dynamic environment, stiff competition is pushing organizations to work aggressively on competitive systems with better strategies that can make firms work independently (Punniyamoorthy and Murali 2008; Singh and Arora 2018). The situation is demanding that organizations work visibly and invisibly on a sustainable system that should be inimitable, meanwhile readily adaptable by the organization to enhance its capacity. Traditionally, organizations were considered as money-making machines. Therefore, all strategies revolved around financial considerations. The recent trend is more likely acceptable if those incorporate non-financial measures as it is becoming imperative for firms (Kaplan and Norton 1992, 2001). To make organizations stand out from the competition, a sustainable development agenda backed by a strong management system is becoming an urge in the recent era (Ardito and Dangelico 2018; Walls et al. 2012).

The current research benchmarks BSC to study the critical aspect of a firm’s elements for growth and development (Kaplan and Norton 2001) has the following four perspectives (1) Financial perspective (FP), (2) Customers’ perspective (CP), (3) Internal business perspective (IBP), and Learning and growth perspective (LGP) used for effectiveness of organizational performance (Kaplan and Norton 2001). BSC is an important and common point of reference for all employees and business units to perform effectively. BSC is being used as an strategic management system (SMS) tool in organizations widely to develop uniformity for efficient control and to address all relevant perspectives for sustainable development in a balanced way (Alani et al. 2018; Bontis et al. 2007). The evidence of the implementational success of BSC are louder and wider across the globe such as, USA, England, Canada, Spain, China and other developed nations that have yielded short- and long-term benefits. Firms in the United States and England are widely using this tool with 50 percentage. 75% of Canadian firms are using BSC to improve their strategic management system while in Jordan, and China 35% and 25% of firms respectively are using BSC (Soderberg et al. 2011; Wang 2016; Williams 2001). The facts advocate the best utilization of BSC as the best tool to gain sustainable development in all aspects. For better utilization of BSC results, it is fundamental to synchronize sustainable development and strategic management systems. The negative nuance of the environment cannot be reduced without linking SMS and sustainable development (SD) from business activities (Baumgartner and Rauter 2017). Another important variable, political and regulatory influence (PRI), that mediates the linkage is important to consider while measuring the effect. Moreover, a stable and transparent political and regulatory system can impact the ecological intentions that route sustainable development. Eco-friendly companies increase the chances of sustainable corporate behavior. The study is designed to investigate the empirical link between the strategic management system and sustainable development by measuring political and regulatory influence as a mediating variable.

The significance of BSC and its connection with sustainable development and political and regulatory influences is discussed and measured in this study. Importantly, this study is to gauge the vibrance of sustainable development. The reasons due to which many companies fail to execute strategy are because of: (a) only 5% of the workers understand company’s strategy (b) the manager who can link performance with incentives are only 25% (c) budget and strategy linkage is missing in 60% of the organizations (d) less than one hour is spent on strategy discussion in 86% organizations (Kaplan and Norton 2000). Additionally, global warming is becoming a serious threat and challenge for organizations. Hence, the study is fundamental because the linkage between BSC and SD through political and regulatory influence is measured. The notion of BSC in different sectors of Pakistan such as health, banking, education, and the telecom sector is studied but the energy sector, the most dominant sector, is not been studied and ignored by researchers (Ahmad and Hasnu 2013; Al-Najjar and Kalaf 2012; Rabbani et al. 2011; Tariq et al. 2013).

Business, industry, government institutions, and non-profit organizations use the balanced scorecard as a cohesive strategic planning system for performance measurement that is widely used around the globe to align organizational actions in order to translate vision and mission. Moreover, it is a helpful tool to increase internal and external communications and to look after sustainable development.

The rationale of the study is underpinned in the issues remained unattended in the research field, especially in developing countries. The reason for being unexplored, is the lack of interest of researchers in developing countries. Moreover, the companies which want to operate in foreign countries, face many strategic and regime (regulation and policies) problems. Therefore, this study addresses the issues of companies regarding the political and regulatory factors consistent with environmental sustainability.

Energy is a key issue for economies round the globe. Pakistan is an emerging economy in the region and has strategic importance for the world due to its geological location. Due to the unstable political and economic system, Pakistan is suffering a shortfall of 7000 MW approximately. In this situation, China took an initiative and started the project named China Pakistan Economic Corridor (CPEC) in the year 2013. The project is worth $62 billion. In this project, China started investing heavily in Pakistan especially in the energy sector.

Leaving aside the alleged corruption, bad governance and bad law and order situation, there are few other problems that renewable power companies faced while their operations in the developing world. Financial transgression is another problem that energy corporations face during their initial setups due to improper financial check and balances. Above all, the main problem is to reduce the cost of electricity production. Therefore, in this regard there is huge pressure on companies to reduce the cost by improvising their management practices that can ensure ecologically responsive system. The study aimed to explore the impact of the balanced scorecard on SD, with respect to environmental sustainability, by using political and regulatory influence as a mediating variable.

2. Literature

Cutting-edge performance remains essential for every organization. The recent era is not only focused on financial measures but, also on non-financial measures of firms due to increased competition. The social cost is becoming vital to compensate. Thus, organizations are striving to develop and implement a competitive strategic management system because it is becoming essential for companies to deal with ecological matters.

In today’s many organizational issues such as dynamism, complex future planning and integration of disciplines, BSC is a well-thought-out solution to those discrepancies. The roots of BSC are pinned to market analysis, understanding rivals, negotiations with suppliers, agilities in distribution and dealing with governments. As time has passed, the role of strategic managers has also changed from the traditional way of business activities to modern trends. The role of government and regulatory institutions has changed hence, it changed the role of managers as well. In the early 1990s Kaplan and Norton introduced such a framework that provided multiple solutions to strategic managers. The balanced scorecard is being used widely round the globe especially in developed world.

2.1. Using the Balanced Scorecard

To differentiate between non-performers and performers, the balanced scorecard was introduced in early 1990s for the purpose of enhancing the performance of organizations. (Krasniqi and Tullumi 2013; Ronda-Pupo 2015; Ronda-Pupo et al. 2015; Wright and Stigliani 2013). Many theories were introduced and research undertaken to measure the performances and at initial level these theories and approaches were borrowed from different disciplines to streamline the process (Furrer et al. 2008; Grant 2016; Guerras-Martin et al. 2014; Kenworthy and Verbeke 2015; Molina-Azorín 2014). Journals like Academy of Management Journal and Strategic Management Journal during the late 1980s played and an important role to enhance the knowledge to related field and strengthen the research and pragmatism in the said field of management. (Guerras-Martin et al. 2014; Ronda-Pupo and Guerras-Martín 2010). Two additional factors contributed by and large to evolution of the field of SMS. First, the heterogeneous and epistemological perspective have influenced the nature of strategic management system and influenced the nature of the subject for the purpose to enrich the academic field. Second, the managers are responsible for formulating and implementing the strategies (Furrer et al. 2008; Hoskisson et al. 2013).

2.2. Balanced Scorecard and Political and Regulatory Influence

Undoubtedly, the balanced scorecard was a great innovation and influential tool that facilitated organizations to grow and develop (Modell 2012). Nonetheless, many aspects need to be studied and analyzed. The political and regulatory aspects are one of the emerging issues that are not linked with BSC practiced (Modell 2012). Hence, this study bridges the gap and investigates the phenomenon. It is asserted that within the implementation of this system an organization can obtain a significant breakthrough in its whole system especially in sustainable development policies (Kaplan and Norton 2001). The early adopters of BSC as an SMS tool achieved tremendous results and they dispersed the results to the entire organization. Eventually, it was proved that success is not merely dependent on new product launches, service addition or new venture capitalization but rather maturity through the strategic system and implementation of BSC as a trigger for motivating factors (Kaplan et al. 2001). However, companies have sheer intention to invest heavily in tangible resources rather the adoption of policies for future growth (Lucianetti 2010). Recent studies have shown high integration between the balanced scorecard and sustainable development. According to Figge et al. (2002) non-financial measures are motivating factors to enhance sustainable development regarding environmental issues (Nathan 2010). As narrated by Farid and Mirfakhredini (2008), financial perspectives increase the wealth of organization that can be utilized by a whole country as a byproduct while non-financial measures enhance human capital and other factors of sustainable development. Additionally, characterization in operation, independence in decision making and flexibility are gained at certain level by adoption of BSC (Free and Qu 2011). As mentioned by Ferreira and Otley (2009), learning and growth are essential for organizational growth and development. Hence the following hypothesis can be postulated;

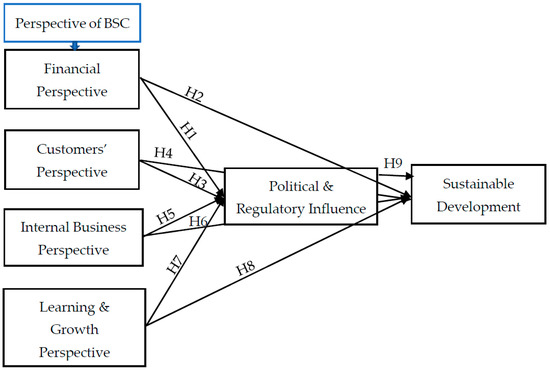

Hypothesis 1 (H1).

Financial Perspective (FP) positively affects political and regulatory influence (PRI).

Hypothesis 2 (H2).

Customer Perspective has an impact on Political and Regulatory Influence.

Hypothesis 3 (H3).

Customers’ Perspective (CP) positively affects political and regulatory influence (PRI).

Hypothesis 4 (H4).

Learning and Growth Perspective has an impact on Political and Regulatory Influence.

Hypothesis 5 (H5).

Internal Business Perspective (IBP) positively affects political and regulatory influence (PRI).

Hypothesis 6 (H6).

Customer Perspective has an impact on Sustainable Development.

Hypothesis 7 (H7).

The Learning and Growth Perspective positively affects political and regulatory influence (PRI).

Hypothesis 8 (H8).

Learning and Growth Perspective has an impact on Sustainable Development.

Hypothesis 9 (H9).

Political and Regulatory Influence has an impact on Sustainable Development.

2.3. Balanced Scorecard and Environmentally Sustainable Development

Strategic management practitioners considered sustainable development as a secondary function for businesses many years ago, but in recent business trends it is considered as an essential activity to progress and grow. To rightly focus on environmental sustainability, it is pivotal to device right mechanisms (Cierna and Sujova 2015; Radomska 2015). Thus, understanding the notion of environmental sustainability is becoming essential. The literature suggests three major parts of sustainable development such as: social values, economic development, and environmental sustainability. However, this research incorporates the concept of environmental sustainability as one of the leading concepts of sustainable development. Hereafter, sustainable development will be used in terms of environmental sustainability. The studies have shown a strong cohesion between a balanced scorecard and environmental sustainability (Cierna and Sujova 2015). Hence, it is imperative to study a proper mechanism between BSC and environmental sustainability. The latest concept of BSC known as sustainable BSC has full integration with environmental sustainability (Hristov et al. 2019). It is also evolved that strategic thinking of the organizations for environmental sustainability is dependent on political and regulatory influences for the stable operation of businesses (Rafiq et al. 2020; Stead and Stead 2013). Additionally, many researchers have indicated the potential gains of BSC for environmental sustainability as a competitive advantage over other organizations (Duman et al. 2018; Figge et al. 2002; Hansen and Schaltegger 2016). Few researchers have aligned financial and customers’ perspectives with economic sustainability of sustainable development (Dias-Sardinha et al. 2002; Falle et al. 2016; Kramer 2009). Hence, Hypothesis 2 (H2) the Financial Perspective (FP) has a positive influence on SD (SD). By Hypothesis 4 (H4) the Consumers’ Perspective (CP) has a relationship with the SD Customers’ Perspective (CP) that positively influences SD. Before, many organizations focused on considering sustainable development as a routine matter rather a seasonal activity or activity at will (Henrique da Rocha Vencato et al. 2014). As a consequence, the social domain of sustainable development received the attention of researchers for betterment of society for long run (Yilmaz and Flouris 2010). Therefore, a strong link between the social domain of sustainability and the learning and growth perspective of BSC alongside the internal business perspective of BSC were explored (Dias-Sardinha et al. 2002; Epstein and Wisner 2001; Falle et al. 2016; Figge et al. 2002; Kramer 2009). Hence, the above studies formulate Hypothesis 6 (H6). The Internal Business Perspective (IBP) has an influence on sustainable development. By Hypothesis 8 (H8) SD is influenced by the learning and growth perspective as postulated by relating this with the values of society’s enrichment and its capitalization (Araújo and Sampaio 2014).

2.4. Political and Regulatory Influence and Sustainable Development

There is a dearth of studies on the political and sustainable development relationship. The notion has not been explored up to its potential. Hence, this scarcity of literature on the subject has created an opportunity of this study to explore this phenomenon. Nevertheless, numerous guidelines are available from different researchers. Political and regulatory support triggers to sustainable development that prevents developmental projects from negative extenuations and builds a positive image in society (Zuhair and Kurian 2016). Moreover, it is asserted that environmental impact assessment is an important and deliberate political decision that leads organizations towards gaining sustainable development goals. The role of governments is to facilitate business ventures so that these businesses can run the engine of the economy; meanwhile, it is also the responsibility of government to preserve resources for the future. Government and regulatory bodies ensure that environmental degradation is minimized and scarce resources are rationally utilized. As a result, responsible governments and regulatory institution make laws to bind business activities to preserve the environment. Emission trading is introduced to facilitate businesses to marginalize the environmental effect.

The role of government is also seen as a preventive measure that stresses long-term transformation of the energy system without political governance will be more messy, disjointed, and conflictive (Meadowcroft 2009). The political and regulatory influence for sustainable development is related to governance, policies and practices that can encourage and shift the pattern of business activities towards environmental sustainability (Meadowcroft 2009). Modern governance must be prepared to meet the multiple layered uncertainties and normative foundations for sustainable development. It is worthwhile discussing that sustainable development lies as central discussion part in politics and political processes for wellbeing of socio-economic activity. Hence, Hypothesis 9 can be postulated. By Hypothesis 9 (H9) political and regulatory influence (PRI) positively affect SD.

2.5. Benefits of Using Balance Scorecard in Strategy Implementation

The benefits of balanced scorecard are dependent on the purpose for what BSC is being used, designed, and applied to gain desired goals. Well-structured and implemented BSC may include the prospective benefits to prevent firms from drowning in measures and system collapse (Braam and Nijssen 2004). Measuring everything became easier due to the technological revolution, and managers now have choice to actively select what to measure, when to measure and are also empowered to decide what is important through consensus. Before the inclusion of BSC as systematic approach, choosing was hard, and when managers were unable to choose the organizations were ending up with many measures and as result firms had scattered information that crucially did not inform them on key activities. Therefore, BSC benefited with all these solutions to make managers clearer and more spontaneous. The balanced scorecard is a complete framework that is more focused on the strategic management system and performance management system that empowers users to be involved in strategy process (Rafiq et al. 2020). Additionally, when users are involved in the strategy process, they have more chances of consensus and oppose resistance when the time comes for strategy execution. A balanced scorecard helped managers to develop a concise set of operationally focused measure across the organizational activities as it collects information in a well-mannered way and highlights key information that is necessary to highlight important information reflecting the help to future goals. It has a rigorous and typical focus on innovation and implementation of activities beyond the traditional concerns of customer satisfaction, financial and operational measures (Kaplan and Norton 2004). Understanding, awareness, innovation and synchronization in operations are the key arising benefits yielded from a BSC for the control process of operation. Well designed and developed BSC system helps strategic partners to generate a single and concise reports explained for operational performance across the board (Braam and Nijssen 2004).

Monitoring key required activities, developing the main strategic destinations, agreeing on managers to implement the results are part of a BSC. Furthermore, it articulates the vision and mission into strategy for key strategic alignment and clarity concerning the link between operational activities and strategic goals. The trade-offs between objectives and cost reduction including marketing expenses encourage debate within a firm regarding strategic objectives and prospects (Kaplan and Norton 2004).

However, the application of a BSC is dependent on its understanding and practices of the organizations. Implementing a BSC as a performance management system is different from implementing it as tool for sustainable development. The studies of Davis and Albright (2004) also show performance outcomes pursued organizations to fulfill their commitments with environmental sustainability. In a nutshell, there is room for investigating the relationship between BSC and PRI and even to explore the relationship between PRI and environmental sustainability (Henrique da Rocha Vencato et al. 2014; Hoque 2014). The following Figure 1 shows the research framework alongside the hypothesis postulated to understand the possible link between variables.

Figure 1.

Research model with the hypothesis.

3. Research Methodology

The claim of knowledge in research is based on some procedures and determinations to carry on the inquiry of work that follow some specific assumptions (Creswell et al. 2003). Usually, the claim about knowledge by the researcher is known as ‘Ontology’, the procedure to know it ‘epistemology’, the values ‘axiology’, the language that should be used ‘rhetoric’, and the procedure to conduct it ‘methodology’ (Creswell 1998). The prerogatives in the research are called paradigms (Lincoln and Guba 2000). The interrelated assumptions about the social world is known as a paradigm that offers a conceptual framework developed for scientific study. Selecting an appropriate paradigm is the footstep about philosophical assumptions, data collection instruments, respondents and methods to be applied for the study (Madriz et al. 2000).

To achieve the core objectives of the research, a quantitative (positivism) research method is applied. The goal of the current research is possible through the quantitative method because of its objective nature which is to examine the SMS as a trigger for sustainable development for Chinese power corporations operating in Pakistan. Additionally, the generalization purpose can only be satisfied through a quantitative approach hence it justifies the selection of the approach. Descriptive, intervention and associational studies are types of quantitative research. The rationale of using a quantitative method is underpinned in examining the relationship between variables—a key concern of this study (Fraenkel 2000).

In short, numerous research approaches are available to address the research questions and problems. Since the purpose of this study is to examine the relationship between balanced scorecard (independent variable) and sustainable development (dependent variable) involving the mediated effects of political and regulatory influence, the associational approach was utilized for data analys3.1. Data Collection Tool

The most integral part of the study is deciding about the data collection tool. The data collection instrument used for the study is split into four parts: Section-I, the demographic part indicates participants’ profiles like; gender, age, job position, and experience. Section-II BSC that studies four aspects; (a) learning and growth (b) internal business perspective (c) customers’ perspective and (d) financial perspective. The concept of BSC is utilized on the basis of (Kaplan and Norton 2001). Section-III political and regulatory influence, part of the instrument captures the basic elements of political and regulatory influence such as policies. Section 4 discusses the ecological perspective of sustainable development. A close-ended data collection tool was applied to collect the data to ensure the unbiased participation of the study, as this method supports the research paradigm of the study. The five-point Likert scale questionnaire indicating strongly disagree to strongly agree was applied with values from 1–5. Five is the highest value that indicates strongly agree while 1 is the least value that indicates strongly disagree. The questionnaire is adapted from the study of (M’Maiti 2014). The adopted instrument has covered all perspectives used in this study while, it is little changed to contextualize the instrument. Furthermore, a reliability test was also used to make sure that questionnaire was valid. The acceptable internal reliability was indicated though the value of Cronbach’s Alpha greater than 0.80 (Yang 2005).

Sampling

To reach the relevant sample of the population, stratified random sampling strategy was used. Renewable power organizations were selected for this study. The size of the sample was measured with the help of software known as Rao-soft. It depicts the range of participants according to the following rule;

A sum of 320 questionnaires were distributed among the different levels of management. A total of 280 participants sent back the questionnaire. Questionnaires with improper or incomplete information were discarded from the study. We made sure that respondents had proper knowledge about the concept.

4. Research Results and Findings

Demographics of the Study

This part of the study is about the demographical situation of the participants in the study. Table 1 indicates constructs like gender, age group, designation, and experience. The gender construct used male and female category as respondents. The Table 1 depicts that 75% of the respondents who contributed to the study were male and 25% were female. The graphical representation of the results is shown in graph that prominently elicits that male gender bar is higher than a female that means male participants were dominating in the study. Furthermore, Table 1 illustrates about the age group of the participants, there were five age categories used for the study. It is evident from the table that 9%, 67%, 19%, 5% and 1% participants were 25, 26–35, 36–45, 46–55 and 56 years of age, respectively. The results indicate that 67% of participants were aged 25–35 and this is also shown in the graph. The participants aged 56 years or above were the least as participants in the study. Additionally, the table also narrates about the designation position of participants. It specifies that 4%, 28%, 60%, and 8% participants were from operational, lower, middle and top management correspondingly. It shows that most participants were from middle-level management who contributed to the study with a sixty percent ratio, while operational level management was the lowest with 4% of contributors. The situation is also shown in the graph. The last segment of Table 1 depicts the experience demographics of the respondents. Three categories of experience were studied: less than two years, between two to four years, and between five to seven years of experience, with percentages of 34%, 59%, and 7%, respectively. The statistics reflect the fact that most participants have experience from two to four years who contributed to the study.

Table 1.

Descriptive analysis of demographic variables.

Table 2 illustrates a descriptive analysis of the latent variables of the study. Descriptive analysis usually explains the fundamental features of the data used for the research. Moreover, it asserts simple summaries of sample and its measures, they provide quantitative figures of data used for analysis and graphical representation. The descriptive analysis includes the mean, standard deviation, minimum and maximum. The values derived from the research are given below.

Table 2.

Descriptive analysis of constructs.

Measuring data reliability is an important and essential stage to make research trustworthy. The most commonly used method to assess internal consistency is Cronbach’s Alpha. It measures the internal consistency of survey questionnaires made up with multiple Likert-type items and scales as the current study also uses Likert-type scales and items to find the solution to the research problem. According to Tingley et al. (2014) accurate measurement of the construct is denoted in a scale with a value above 0.70. The following table indicates the values of Cronbach’s Alpha. According to data FP (Financial Perspective) has the highest value of 0.921 while contrary SD (Sustainable Development) has the lowest value of 0.818. Resultantly all values are above the accepted range of 0.70. The composite reliability of each variable should also exceed the minimum value of 0.70. Table 3 expresses that none of the values is less than 0.70. Additionally, FP has the highest values of 0.942 while SD has the lowest values of 0.879 which is eventually greater than expected value. Average Variance Extracted (AVE) is a common measuring method for discriminant validity. All AVE values are reasonably above the bottom line of 0.50. the highest value of AVE is illustrated in FP with the denomination of 0.760 while CP has the lowest value.

Table 3.

Reliability.

As stated by Tabachnick and Fidell (1996), 0.5 is the minimum accepted value for good factor loading analysis. Three criteria are suitable to estimate the convergent validity of scale items used for the study. In the first step, according to Hair (1998) factor loading values should be higher than 0.50. Following the first step, the composite reliability value of each item should be greater than 0.70. Finally, the average variance extracted (AVE) as suggested by Fornell (1981) should have a cut-off value greater than 0.50 to measure each construct of the study.

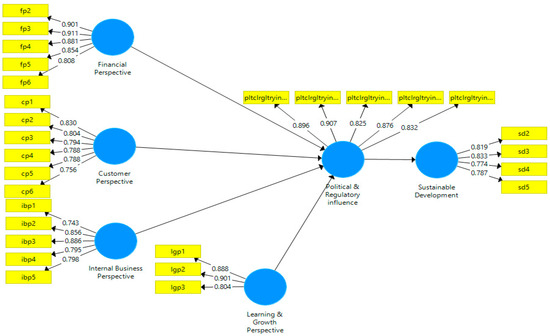

The study reveals in Table 4 that factor loadings support to convergent validity for all the constructs except Financial Perspective-1 (FP1), Learning and Growth Perspective 4,5 (LGP4,5), Political and Regulatory Influence-1 (pltclrgltryinfl-1), and Sustainable Development 1,6 (SD 1,6) the values of which are less than accepted value of 0.50. Hence, we dropped these values and run the test again to ensure the validity of the constructs. The items were deleted as rule of thumb, that twenty percent of the total items can be skipped. The following table depicts the factor loading values of the study. According to the data, the highest factor loading in customer’s perspective variable loads in cp1 construct while the lowest value of loading is 0.756 which is still in the accepted range. Moving forward, the financial perspective variable’s highest values is shown in fp3 valuing 0.911 while fp6 shows the lowest values of 0.808. Furthermore, the internal business perspective also has different values ranges from 0.886 to 0.743, highest to lowest respectively. The learning and growth perspective variables also have ranged from 0.901 to 0.804 lgp2 and lgp3, highest to lowest respectively. Pltclrgltry3 has the highest value of 0.907 and pltclrgltry4 has the lowest value of 0.825 in the political and regulatory influence variable. The last variable, sustainable development, also shows diverse values. The highest value is depicted in the sd3 (0.833) construct while the lowest value is depicted in sd4 that is 0.774. It is evident from the data that all ranges are above the accepted value of 0.50. Hence, it is proved that the instrument has convergent validity. The graphical representation of factor loading is depicted in Figure 2.

Table 4.

Factor loading.

Figure 2.

Factor loading.

The below Table 5 narrates about the correlation between latent variables. 1 indicates the perfect relationship between two variables, 0.70 shows the strong relationship, 0.50 or above shows a moderate relationship and below 0.50 is a weak relationship between variables. The maximum value of correlation is 1 that means positive perfect correction and the minimum value of correlation is –1 that means perfect negative correlation. the significance level is <0.05 two-tailed. The statistics in the above table depicts that all variables are significant at the 0.01 level. The table shows that learning and growth have a weak relationship with FP and IBP while other variables have moderate to a strong relationship with each other.

Table 5.

Correlation matrix.

Regression is the analysis that expresses the change in the dependent variable due to change in an independent variable Table 6 indicates the values of regression. Furthermore, it expresses the significance level of variables also. Regression is calculated through the following formula;

where = ƞ observations

Table 6.

Regression analysis.

= Dependent variable

xi = descriptive variables

= constant term

βp = descriptive variable slop coefficient

ϵ = residual (error term)

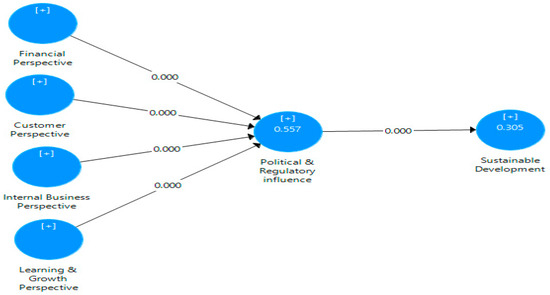

Multiple regression can only be measured when there is more than an independent variable that affects the dependent variable. R2 measures the variation that can be explained as an outcome by the outcome of independent variables. The increase in the value of R2 means a greater effect on the dependent value. The table above indicates that all variables have a significance relationship with each other at the 0.05 level. It is suggested that when there is 0.05 or less value of p then there is a relationship between variables. The contribution of indigenous variables is as mentioned in the table. The lowest effect is transferred in H7 (IBP-SD) with value 0.259 while the highest value is H1 (FP-PRI).

Table 7 is about mediation analysis. The most common method for mediation is Hayes (2009) indirect effect method and a more advanced package of mediation is suggested by (Tingley et al. 2014). The original method for testing mediation is Baron and Kelly but it has low statistical power as compared to new methods. Up to now, many researchers have still been using this method because it supplements a vivid method to explore the relationships between latent variables and is eventually strongly suggested as more adaptable and statistically powerful.

Table 7.

Mediation table.

The mediation can also be checked by two primary tests that have an indirect effect: the Sobel test and bootstrapping that projects the mediation method. Limitations of the Sobel test are overcome through the package of the most recent method (Hayes 2009). Over a large number of samples, normally more than 1000, this method is more appropriate to estimate the indirect effect. Hence, it does not hypothesize the normality of data. Additionally, it works more effectively for the small size of the sample than the method of Barron and Kenny. Therefore, this study uses the bootstrapping method by using Smart-PLS, Partial Least Squares (PLS) is high graphical user interference software that is used to calculate Structural Equation Modeling (SEM) through PLS path modeling, to check the mediation. The values are shown in the above table that designates that all variables are significant at level 0.05. It means there is full mediation between the independent and dependent variables. As a result, it can be asserted that political and regulatory influence is mediating between BSC and SD.

Regression analysis and mediation analysis shows a significant relationship among variables. All p-values are at a significant level that supports the positive relationship between constructs. Hence, it is asserted that all hypotheses are supported by data analysis. Table 8 shows an overall scenario of the hypotheses supported by data analysis. The graphical representation of data is shown is Figure 3.

Table 8.

Hypothesis status.

Figure 3.

Research model with inner loadings.

5. Discussion

The study took numerous methods to come up with some practical suggestions to academicians and practitioners. The results of the research are worthwhile due to its various advantages for researchers and policymakers. The basic objective of the research is to explore the relationship between sustainable development and balanced scorecard. The research used political and regulatory influence as a mediating variable. The studies in the past so far have not explicitly explored the combination of BSC and sustainable development by engaging political and regulatory influence in the power sector’s setting (Siva et al. 2016; Testa et al. 2014). Therefore, to date the studies were dispersed and did not depict a holistic picture about BSC and SD and showed unclear concepts and understanding about the phenomena.

The findings of the study are multidimensional for top management, human resources (HR) professionals and academicians specifically for energy organizations. First, the study advocates that upper management should consider BSC as an important tool to support sustainable development activities because sustainable development is an emerging issue for energy organizations. Hence to resolve and address the non-financial and financial issues of energy organizations, a balanced scorecard is effective tool. Additionally, to ensure the environmental sustainability, it is important to highlight the social aspect of business. Second, the organizations should implement the environmental sustainability and balanced scorecard at the same time, as study has found strong relationship between these two factors. Third, sustainable development is affected by the financial aspect of organization which indicates that organization should focus more on its customers who are the main stream of cash inflow for organization. The customers’ satisfaction can be gained by improving internal business operations and through a learning and growth perspective.

The study reveals that there is no mediation of political and regulatory factor on implementation of balanced scorecard and sustainable development, hence it is suggested that organizations can focus on sustainability without government influence. The understanding about ecological responsiveness can be maximized through the non-financial aspect of BSC and the non-financial aspect is also helpful to enhance employees’ performance unlike, in the past, the fact that the financial performance was considered the most important aspect; the results are associated with findings of Kaplan and Norton (2004) who referred to the measures of non-financials. Therefore, utilization and recommendations of non-financial measure are evident to increase organizational capacity for implementing sustainable development practices. For instance, to persuade the practices of sustainable development, organizations should focus on recycling, reduction of wastage and careful utilization of scarce resources.

Stakeholders’ pressure to be environmentally friendly is becoming clear and loud in organizations. Hence, the findings of the study depict that contribution to the ecological system is not only considered as a formality but as a necessity. Similar findings are shown in other studies (Fernandez-Feijoo et al. 2014; Guerci et al. 2016).

The concept of globalization has increased the urge of organizations to grow across borders, but it also created numerous challenges. Political and regulatory risk evaluation is pivotal for organizations to study, to hedge the risk of failure. The study divulged that meta-constitutional rules are embedded in the system of developing countries which are in lieu of formalized rules. This is a system of axioms as recommended in the studies of also. Therefore, it is recommended to companies to make policies that are not contradicting to meta-constitution like social norms and beliefs, as evoked in this study. However, this system makes the ‘exit option’ easier. It is for the safety of companies to take mutual consensus of civil-military authorities otherwise it may lead to a collision as happened in the case of the Enron (Dabhol-India) power plant. The same ideas are also presented in the studies of (Rafiq et al. 2020; Ullah et al. 2017; Williamson 2000) but, in previous studies, the contextual analysis of power sector was lacking.

BSC enables organizations to transform their vision and mission according to the sustainable development agenda by equally aware of the political and regulatory influences of the region. The study also formed a better understanding of the resource-based view (RBV). RBV suggests a variety of management tools and techniques, especially formed to support administrators working in dynamic settings. It also recognizes that resources are dispersed and heterogeneous, prevailing in an organization and are also not perfectly moveable. Hence, BSC connects vision and mission logically with all four aspects that are financial and non-financial, and are coherent with each other. Moreover, it also makes a connection with strategies, plans, services, and actions that an individual must take to contribute to the environment in order to make this world safer and more livable. The role of this study is to draw attention toward these issues and device mechanisms to assist them to resolve it effectively and efficiently.

6. Conclusions

The research suggests that organizations should make themselves outcome-oriented to meet the challenges of sustainable development. The study laid stress on the command and control perspective of sustainable development. Moreover, the study showed that a well-performing organization can contribute ecologically. Another finding of this research claimed that regulatory factors compel companies to work deeply in environmental sustainability. Hence, it is concluded that an effective BSC system is possible with the help of incorporating green practices to ensure sustainable development.

The study concludes applying BSC is obligatory to ensure sustainable development regardless of its challenges in adoption. It is a helpful tool especially for power organizations as they need more sophisticated efforts to meet environmental challenges. Moreover, consideration of meta-constitutional rules as political influence is important to understand how to mitigate the financial loss. Concluding the study, the effective use of BSC is recommended as a tool to aware of organizations at all levels about initial problems that may be caused in its application.

7. Limitations and Future Work

One of the ways to interrogate the future research direction is underpinned in the limitation of the research. Like other studies, this research also has some limitations that need to be addressed in the future. First, it is suggested to analyze four perspectives individually to know the deeper and customized effect on each variable. These individual perspectives will provide more knowledge to researchers and help them also decide the weight of each perspective and contribution in overall BSC and strategic management system. Digging more into different levels within the organization will give a clear picture to employees about BSC. It will also give an idea of how to improve the usage of BSC and then come up with a better solution.

The second limitation is with the selection of sample size. The study uses a case-based sample which may create ambiguity in the generalization of results. Furthermore, this sector is high tech- and high capital-oriented which requires control variables as well to investigate the problem in all its aspects, for which this study is limited to three main variables. Future research may address this challenge by including more variables like leadership issues and socio-cultural aspects etc. additionally this study only incorporates political and regulatory influence while other mediating variables are not addressed like customers, rivals’ activities, or pressure from NGOs (non-governmental organizations).

Author Contributions

Conceptualization, M.R. and S.M.; methodology, J.M.M.; software, M.N.M.; validation, R.M.D.; formal analysis, S.N.; investigation, writing—original draft preparation, M.R., and S.M.; writing—review and editing, M.R. and A.B.C.; supervision, J.M.M. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Data Availability Statement

After indicating the purpose of research the data can be obtained by corresponding author upon request. The data are supplemented by all researchers of the study.

Conflicts of Interest

No conflict of interest was observed in the study.

References

- Ahmad, Syed Touseef, and Syed Amjad Farid Hasnu. 2013. Balanced Scorecard Implementation: Case Study of COMSATS. Researcher 5: 88–109. Available online: https://www.researchgate.net/publication/279182285_Balanced_Scorecard_Implementation_Case_Study_of_COMSATS_Abbottabad_Pakistan (accessed on 3 June 2021).

- Alani, Farooq Salman, M. Firdouse Rahman Khan, and Diana F. Manuel. 2018. University performance evaluation and strategic mapping using balanced scorecard (BSC) case study–Sohar University, Oman. International Journal of Educational Management 32: 689–700. [Google Scholar]

- Al-Najjar, Sabah M., and Khawla H. Kalaf. 2012. Designing a balanced scorecard to measure a bank’s performance: A case study. International Journal of Business Administration 3: 44. [Google Scholar] [CrossRef]

- Araújo, Maria, and Paulo Sampaio. 2014. The path to excellence of the Portuguese organisations recognised by the EFQM model. Total Quality Management & Business Excellence 25: 427–38. [Google Scholar]

- Ardito, Lorenzo, and Rosa Maria Dangelico. 2018. Firm environmental performance under scrutiny: The role of strategic and organizational orientations. Corporate Social Responsibility and Environmental Management 25: 426–40. [Google Scholar] [CrossRef]

- Baumgartner, Rupert J., and Romana Rauter. 2017. Strategic perspectives of corporate sustainability management to develop a sustainable organization. Journal of Cleaner Production 140: 81–92. [Google Scholar] [CrossRef]

- Bontis, Nick, Christopher K. Bart, Sanjoy Bose, and Keith Thomas. 2007. Applying the balanced scorecard for better performance of intellectual capital. Journal of Intellectual Capital. [Google Scholar] [CrossRef]

- Braam, Geert J. M., and Edwin J. Nijssen. 2004. Performance effects of using the balanced scorecard: A note on the Dutch experience. Long Range Planning 37: 335–49. [Google Scholar] [CrossRef]

- Cierna, Helena, and Erika Sujova. 2015. Parallels between corporate social responsibility and the EFQM excellence model. MM Science Journal 10: 670–76. [Google Scholar] [CrossRef]

- Creswell, John W. 1998. Qualitative Inquiry and Research Design: Choosing among Five Traditions. Thousand Oaks: Sage. [Google Scholar]

- Creswell, John W., V. L. Plano Clark, and A. L. Garrett. 2003. Advanced mixed methods research. In Handbook of Mixed Methods in Social and Behavioural Research. Thousand Oaks: Sage, pp. 209–40. [Google Scholar]

- Davis, Stan, and Tom Albright. 2004. An investigation of the effect of balanced scorecard implementation on financial performance. Management Accounting Research 15: 135–53. [Google Scholar] [CrossRef]

- Dias-Sardinha, Idalina, Lucas Reijnders, and Paula Antunes. 2002. From environmental performance evaluation to eco-efficiency and sustainability balanced scorecards. Environmental Quality Management 12: 51–51. [Google Scholar] [CrossRef]

- Duman, Gazi Murat, Murat Taskaynatan, Elif Kongar, and Kurt A. Rosentrater. 2018. Integrating environmental and social sustainability into performance evaluation: A Balanced Scorecard-based Grey-DANP approach for the food industry. Frontiers in Nutrition 5: 65. [Google Scholar] [CrossRef] [PubMed]

- Epstein, Marc J., and Peter Wisner. 2001. Good neighbours: Implementing social and environmental strategies with the BSC. Balanced Scorecard Report 3: 8–11. [Google Scholar]

- Falle, Susanna, Romana Rauter, Sabrina Engert, and Rupert Baumgartner. 2016. Sustainability management with the sustainability balanced scorecard in SMEs: Findings from an Austrian case study. Sustainability 8: 545. [Google Scholar] [CrossRef]

- Farid, Daryush, and Heydar Mirfakhredini. 2008. Balanced scorecard application in universities and higher education institutes: Implementation guide in an Iranian context. Universitatii Bucuresti Analele Seria Stiinte Economice Si Administrative 2: 29. [Google Scholar]

- Fernandez-Feijoo, Belen, Silvia Romero, and Silvia Ruiz. 2014. Effect of stakeholders’ pressure on transparency of sustainability reports within the GRI framework. Journal of Business Ethics 122: 53–63. [Google Scholar] [CrossRef]

- Ferreira, Aldónio, and David Otley. 2009. The design and use of performance management systems: An extended framework for analysis. Management Accounting Research 20: 263–82. [Google Scholar] [CrossRef]

- Figge, Frank, Tobias Hahn, Stefan Schaltegger, and Marcus Wagner. 2002. The sustainability balanced scorecard–linking sustainability management to business strategy. Business Strategy and the Environment 11: 269–84. [Google Scholar] [CrossRef]

- Fornell, Claes. 1981. A Comparative Analysis of Two Structural Equation Models: LISREL and PLS Applied to Market Data. New York: Sage. [Google Scholar]

- Fraenkel, Jack R. 2000. Research design and implentation. How to Design and Evaluate Research in Education 104. [Google Scholar] [CrossRef]

- Free, Clinton, and Sandy Q. Qu. 2011. The use of graphics in promoting management ideas: An analysis of the Balanced Scorecard, 1992–2010. Journal of Accounting & Organizational Change 7: 158–89. [Google Scholar]

- Furrer, Olivier, Howard Thomas, and Anna Goussevskaia. 2008. The structure and evolution of the strategic management field: A content analysis of 26 years of strategic management research. International Journal of Management Reviews 10: 1–23. [Google Scholar] [CrossRef]

- Grant, Robert M. 2016. Contemporary Strategy Analysis: Text and Cases Edition. Hoboken: John Wiley & Sons. [Google Scholar]

- Guerci, Marco, Annachiara Longoni, and Davide Luzzini. 2016. Translating stakeholder pressures into environmental performance–the mediating role of green HRM practices. The International Journal of Human Resource Management 27: 262–89. [Google Scholar] [CrossRef]

- Guerras-Martin, Luis Ángel, Anoop Madhok, and Ángeles Montoro-Sánchez. 2014. The evolution of strategic management research: Recent trends and current directions. BRQ Business Research Quarterly 17: 69–76. [Google Scholar] [CrossRef]

- Hair, Anderson. 1998. Multivariate Analysis. New York: Prentice Hall College Div. [Google Scholar]

- Hansen, Erik G., and Stefan Schaltegger. 2016. The sustainability balanced scorecard: A systematic review of architectures. Journal of Business Ethics 133: 193–221. [Google Scholar] [CrossRef]

- Hayes, Andrew F. 2009. Beyond Baron and Kenny: Statistical mediation analysis in the new millennium. Communication Monographs 76: 408–20. [Google Scholar] [CrossRef]

- Henrique da Rocha Vencato, Carlos, Clandia Maffini Gomes, Flavia Luciane Scherer, Jordana Marques Kneipp, and Roberto Schoproni Bichueti. 2014. Strategic sustainability management and export performance. Management of Environmental Quality: An International Journal 25: 431–45. [Google Scholar] [CrossRef]

- Hoque, Zahirul. 2014. 20 years of studies on the balanced scorecard: Trends, accomplishments, gaps and opportunities for future research. The British Accounting Review 46: 33–59. [Google Scholar] [CrossRef]

- Hoskisson, Robert E., Wei Shi, Xiwei Yi, and Jing Jin. 2013. The evolution and strategic positioning of private equity firms. Academy of Management Perspectives 27: 22–38. [Google Scholar] [CrossRef]

- Hristov, Ivo, Antonio Chirico, and Andrea Appolloni. 2019. Sustainability Value Creation, Survival, and Growth of the Company: A Critical Perspective in the Sustainability Balanced Scorecard (SBSC). Sustainability 11: 2119. [Google Scholar] [CrossRef]

- Kaplan, Robert S., and David P. Norton. 1992. The balanced scorecard: Measures that drive performance. Available online: https://pubmed.ncbi.nlm.nih.gov/10119714/ (accessed on 3 June 2021).

- Kaplan, Robert S., and David P. Norton. 2000. Having trouble with your strategy? Then map it. Focusing Your Organization on Strategy—with the Balanced Scorecard, 167–76. Available online: https://hbr.org/2000/09/having-trouble-with-your-strategy-then-map-it (accessed on 3 June 2021).

- Kaplan, Robert S., Thomas H. Davenport, Norton P. David Kaplan S. Robert, Robert Steven Kaplan, and David P. Norton. 2001. The Strategy-Focused Organization: How Balanced Scorecard Companies Thrive in the New Business Environment. Cambridge: Harvard Business Press. [Google Scholar]

- Kaplan, Robert S., and David P. Norton. 2001. Transforming the Balanced Scorecard from Performance Measurement to Strategic Management: Part I. Accounting Horizons 15: 1. [Google Scholar]

- Kaplan, Robert S., and David P. Norton. 2004. The strategy map: Guide to aligning intangible assets. Strategy & Leadership 32: 10–17. [Google Scholar]

- Kenworthy, Thomas P., and Alain Verbeke. 2015. The future of strategic management research: Assessing the quality of theory borrowing. European Management Journal 33: 179–90. [Google Scholar] [CrossRef]

- Kramer, Sebastian. 2009. Strategic Sustainability: The case of the New Zealand Energy Sector. Wellington: Victoria University. [Google Scholar]

- Krasniqi, Besnik A, and Malush Tullumi. 2013. What perceived success factors are important for smalll business owners in a transition economy? International Journal of Business and Management Studies 5: 21–32. [Google Scholar]

- Lincoln, Yvonna S., and Egon G. Guba. 2000. The only generalization is: There is no generalization. Case Study Method, 27–44. [Google Scholar]

- Lucianetti, Lorenzo. 2010. The impact of the strategy maps on balanced scorecard performance. International Journal of Business Performance Management 12: 21–36. [Google Scholar] [CrossRef]

- M’Maiti, Hellen Igoki. 2014. Balanced Score Card as a Strategic Management Tool in the Kenyan Commercial State Corporations. Nairobi: University of Nairobi. [Google Scholar]

- Madriz, Esther, N. K. Denzin, and Y. S. Lincoln. 2000. Handbook of Qualitative Research. Thousand Oaks: Denzin & Lincoln, SAGE Publications, Inc. [Google Scholar]

- Meadowcroft, James. 2009. What about the politics? Sustainable development, transition management, and long term energy transitions. Policy Sciences 42: 323. [Google Scholar] [CrossRef]

- Modell, Sven. 2012. The politics of the balanced scorecard. Journal of Accounting & Organizational Change 8: 475–89. [Google Scholar]

- Molina-Azorín, José F. 2014. Microfoundations of strategic management: Toward micro–macro research in the resource-based theory. BRQ Business Research Quarterly 17: 102–14. [Google Scholar] [CrossRef]

- Nathan, Maria L. 2010. ‘Lighting tomorrow with today’: Towards a (strategic) sustainability revolution. International Journal of Sustainable Strategic Management 2: 29–40. [Google Scholar] [CrossRef]

- Punniyamoorthy, M., and R. Murali. 2008. Balanced score for the balanced scorecard: A benchmarking tool. Benchmarking: An International Journal 15: 420–43. [Google Scholar] [CrossRef]

- Rabbani, Fauziah, Sabrina N. H. Lalji, Farhat Abbas, S. M. Wasim Jafri, Junaid A. Razzak, Naheed Nabi, Firdous Jahan, Agha Ajmal, Max Petzold, and Mats Brommels. 2011. Understanding the context of balanced scorecard implementation: A hospital-based case study in Pakistan. Implementation Science 6: 31. [Google Scholar] [CrossRef] [PubMed]

- Radomska, Joanna. 2015. The concept of sustainable strategy implementation. Sustainability 7: 15847–56. [Google Scholar] [CrossRef]

- Rafiq, Muhammad, XingPing Zhang, Jiahai Yuan, Shumaila Naz, and Saif Maqbool. 2020. Impact of a balanced scorecard as a strategic management system tool to improve sustainable development: Measuring the mediation of organizational performance through PLS-smart. Sustainability 12: 1365. [Google Scholar] [CrossRef]

- Ronda-Pupo, Guillermo, and Luis Guerras-Martín. 2010. Dynamics of the scientific community network within the strategic management field through the Strategic Management Journal 1980–2009: The role of cooperation. Scientometrics 85: 821–48. [Google Scholar] [CrossRef]

- Ronda-Pupo, Guillermo Armando. 2015. Growth and consolidation of strategic management research: Insights for the future development of strategic management. Academy of Strategic Management Journal 14: 155. [Google Scholar]

- Ronda-Pupo, Guillermo Armando, Carlos Díaz-Contreras, Guillermo Ronda-Velázquez, and Jorge Carlos Ronda-Pupo. 2015. The role of academic collaboration in the impact of Latin-American research on management. Scientometrics 102: 1435–54. [Google Scholar] [CrossRef]

- Singh, Reetesh K., and Simple Sethi Arora. 2018. The adoption of balanced scorecard: An exploration of its antecedents and consequences. Benchmarking: An International Journal 25: 874–92. [Google Scholar] [CrossRef]

- Siva, Vanajah, Ida Gremyr, Bjarne Bergquist, Rickard Garvare, Thomas Zobel, and Raine Isaksson. 2016. The support of Quality Management to sustainable development: A literature review. Journal of Cleaner Production 138: 148–57. [Google Scholar] [CrossRef]

- Soderberg, Marvin, Suresh Kalagnanam, Norman T. Sheehan, and Ganesh Vaidyanathan. 2011. When is a balanced scorecard a balanced scorecard? International Journal of Productivity and Performance Management 60: 688–708. [Google Scholar] [CrossRef]

- Stead, Jean Garner, and W. Edward Stead. 2013. The coevolution of sustainable strategic management in the global marketplace. Organization & Environment 26: 162–83. [Google Scholar]

- Tabachnick, Barbara G., and Linda S. Fidell. 1996. Using Multivariate Statistics. Northridge: Harper Collins. [Google Scholar]

- Tariq, Muhammad, Arslan Ahmed, Shuaib Ahmed, and Syed Kashif Rafi. 2013. Investigating the Impact of Balanced Scorecard on Performance of Business: A study based on the Banking Sector of Pakistan. IBT Journal of Business Studies (JBS) 9. [Google Scholar] [CrossRef]

- Testa, Francesco, Francesco Rizzi, Tiberio Daddi, Natalia Marzia Gusmerotti, Marco Frey, and Fabio Iraldo. 2014. EMAS and ISO 14001: The differences in effectively improving environmental performance. Journal of Cleaner Production 68: 165–73. [Google Scholar] [CrossRef]

- Tingley, Dustin, Teppei Yamamoto, Kentaro Hirose, Luke Keele, and Kosuke Imai. 2014. Mediation: R package for causal mediation analysis. Journal of Statistical Software 59. [Google Scholar] [CrossRef]

- Ullah, Kafait, Maarten J. Arentsen, and Jon C. Lovett. 2017. Institutional determinants of power sector reform in Pakistan. Energy Policy 102: 332–39. [Google Scholar] [CrossRef]

- Walls, Judith L., Pascual Berrone, and Phillip H. Phan. 2012. Corporate governance and environmental performance: Is there really a link? Strategic Management Journal 33: 885–913. [Google Scholar] [CrossRef]

- Wang, Manyi. 2016. Issues of Balanced Scorecard and Its Implication for Chinese Companies. Auckland: Auckland University of Technology. [Google Scholar]

- Williams, Simon. 2001. Drive your business forward with the Balanced Scorecard. Management Services 45: 28–30. [Google Scholar]

- Williamson, Oliver E. 2000. The new institutional economics: Taking stock, looking ahead. Journal of Economic Literature 38: 595–613. [Google Scholar] [CrossRef]

- Wright, Mike, and Ileana Stigliani. 2013. Entrepreneurship and growth. International Small Business Journal 31: 3–22. [Google Scholar] [CrossRef]

- Yang, Baiyin. 2005. Factor analysis methods. Research in Organizations: Foundations and Methods of Inquiry, 181–99. [Google Scholar] [CrossRef]

- Yilmaz, Ayse Kucuk, and Triant Flouris. 2010. Managing corporate sustainability: Risk management process based perspective. African Journal of Business Management 4: 162–71. [Google Scholar]

- Zuhair, Mohamed Hamdhaan, and Priya A. Kurian. 2016. Socio-economic and political barriers to public participation in EIA: Implications for sustainable development in the Maldives. Impact Assessment and Project Appraisal 34: 129–42. [Google Scholar] [CrossRef]

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).