A Tale of Two Layers: The Mutual Relationship between Bitcoin and Lightning Network

Abstract

1. Introduction

2. Methodology

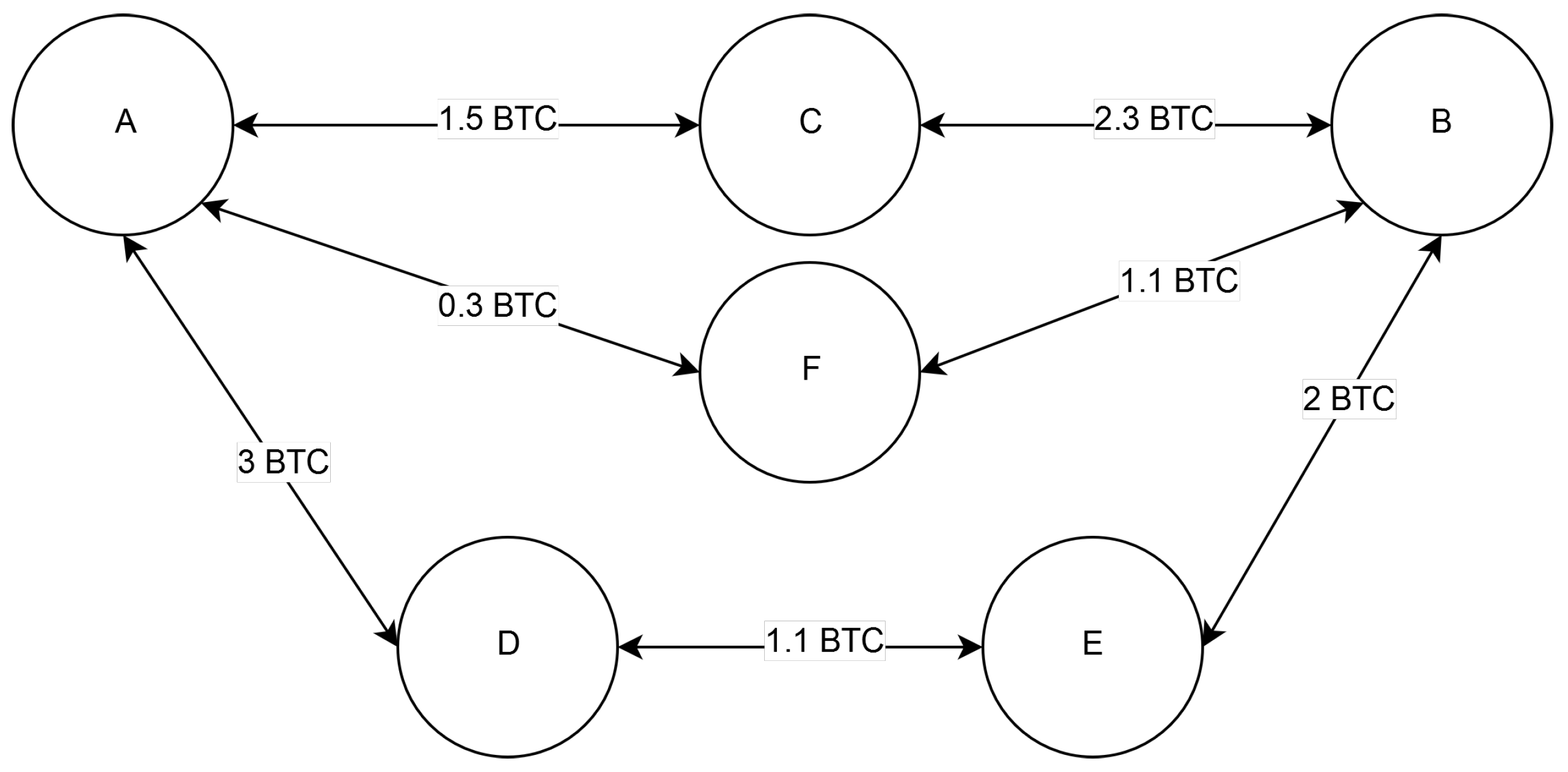

2.1. The Lightning Network

2.2. Market Efficiency

- : long-term memory and anti-correlation;

- : long-term memory and correlation;

- : uncorrelated signal (no memory);

- : non-stationary signal.

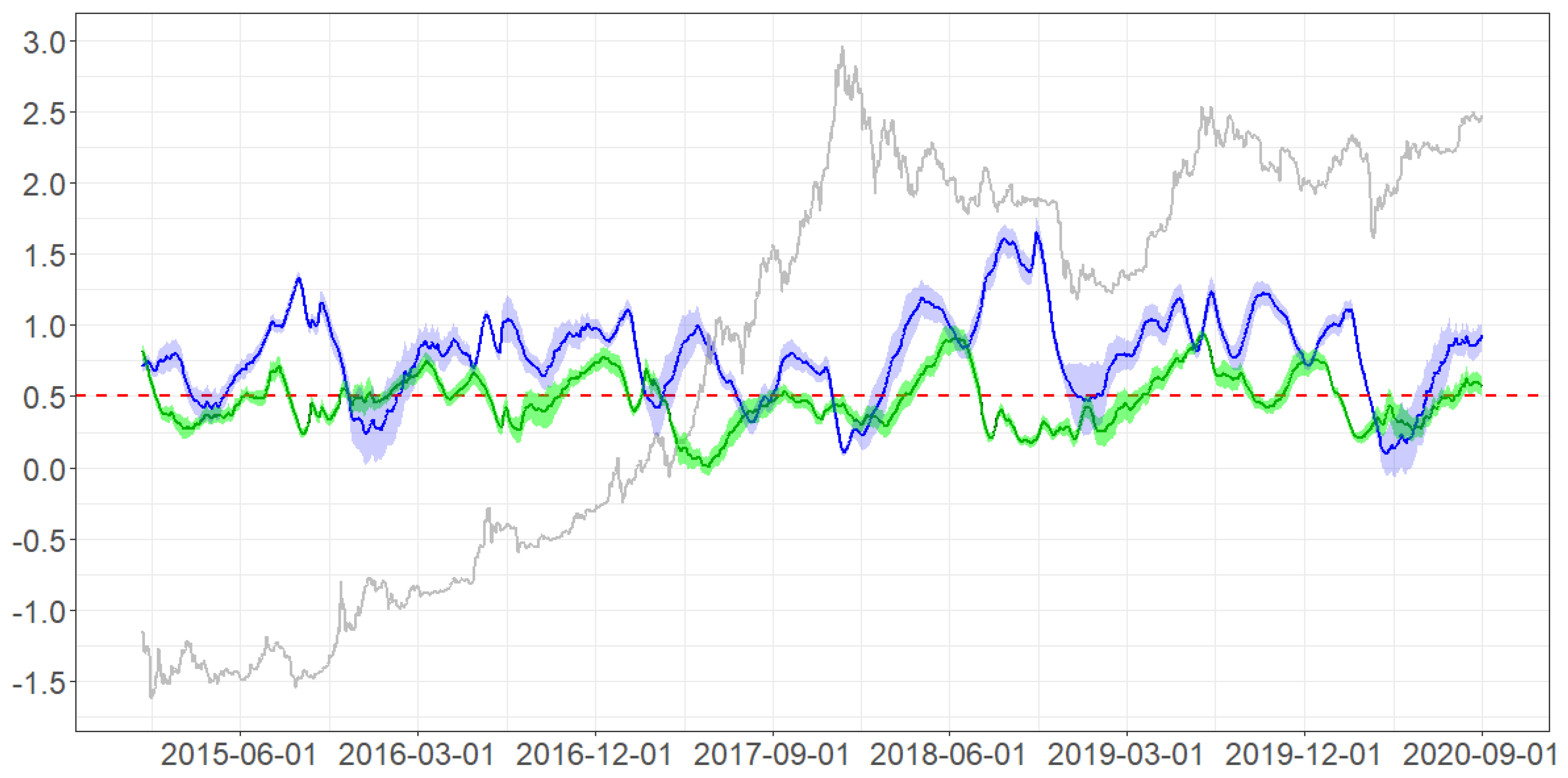

3. Results

4. Conclusions

Author Contributions

Funding

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Panel A: Column G-Causes Row | BTC Alpha | BTC Vol Alpha | BTC Alpha | BTC Vol Alpha | ||

| LN efficiency | statistics | 1.90 | 1.90 | 2.20 | 1.10 | |

| p-value | 0.60 | 0.87 | 0.81 | 0.98 | ||

| Panel B: Row G-Causes Column | BTC Alpha | BTC Vol Alpha | BTC Alpha | BTC Vol Alpha | ||

| LN efficiency | statistics | 0.90 | 3.40 | 3.10 | 5.30 | |

| p-value | 0.83 | 0.64 | 0.68 | 0.50 |

References

- Al-Yahyaee, Khamis Hamed, Walid Mensi, and Seong-Min Yoon. 2018. Efficiency, multifractality, and the long-memory property of the bitcoin market: A comparative analysis with stock, currency, and gold markets. Finance Research Letters 27: 228–34. [Google Scholar] [CrossRef]

- Alvarez-Ramirez, José, Eduardo Rodriguez, and Carlos Ibarra-Valdez. 2018. Long-range correlations and asymmetry in the bitcoin market. Physica A: Statistical Mechanics and Its Applications 492: 948–55. [Google Scholar] [CrossRef]

- Angel, James J., and Douglas McCabe. 2015. The ethics of payments: Paper, plastic, or bitcoin? Journal of Business Ethics 132: 603–11. [Google Scholar] [CrossRef]

- Aslanidis, Nektarios, Aurelio F. Bariviera, and Alejandro Perez-Laborda. 2020. Are cryptocurrencies becoming more interconnected? arXiv arXiv:2009.14561. [Google Scholar]

- Baek, Chung, and Matt Elbeck. 2015. Bitcoins as an investment or speculative vehicle? A first look. Applied Economics Letters 22: 30–34. [Google Scholar] [CrossRef]

- Barber, Simon, Xavier Boyen, Elaine Shi, and Ersin Uzun. 2012. Bitter to better—How to make bitcoin a better currency. In International Conference on Financial Cryptography and Data Security. Berlin and Heidelberg: Springer, pp. 399–414. [Google Scholar]

- Bariviera, Aurelio F. 2017. The inefficiency of bitcoin revisited: A dynamic approach. Economics Letters 161: 1–4. [Google Scholar] [CrossRef]

- Bariviera, Aurelio F., María José Basgall, Waldo Hasperué, and Marcelo Naiouf. 2017. Some stylized facts of the bitcoin market. Physica A: Statistical Mechanics and Its Applications 484: 82–90. [Google Scholar] [CrossRef]

- Bartels, Robert. 1982. The rank version of von neumann’s ratio test for randomness. Journal of the American Statistical Association 77: 40–46. [Google Scholar] [CrossRef]

- Baur, Aaron W., Julian Bühler, Markus Bick, and Charlotte S. Bonorden. 2015. Cryptocurrencies as a disruption? empirical findings on user adoption and future potential of bitcoin and co. In Conference on e-Business, e-Services and e-Society. Berlin and Heidelberg: Springer, pp. 63–80. [Google Scholar]

- Baur, Dirk G., Kihoon Hong, and Adrian D. Lee. 2018. Bitcoin: Medium of exchange or speculative assets? Journal of International Financial Markets, Institutions and Money 54: 177–89. [Google Scholar] [CrossRef]

- Bech, Morten L., and Rodney Garratt. 2017. Central Bank Cryptocurrencies. BIS Quarterly Review. Basel: BIS, September. [Google Scholar]

- Begušić, Stjepan, Zvonko Kostanjčar, H. Eugene Stanley, and Boris Podobnik. 2018. Scaling properties of extreme price fluctuations in bitcoin markets. Physica A: Statistical Mechanics and Its Applications 510: 400–6. [Google Scholar]

- Blundell-Wignall, Adrian. 2014. The bitcoin question. In OECD Working Papers on Finance, Insurance and Private Pensions. Paris: OECD. [Google Scholar]

- Böhme, Rainer, Nicolas Christin, Benjamin Edelman, and Tyler Moore. 2015. Bitcoin: Economics, technology, and governance. Journal of Economic Perspectives 29: 213–38. [Google Scholar]

- Bouri, Elie, Luis A. Gil-Alana, Rangan Gupta, and David Roubaud. 2019. Modelling long memory volatility in the bitcoin market: Evidence of persistence and structural breaks. International Journal of Finance & Economics 24: 412–26. [Google Scholar]

- Brauneis, Alexander, and Roland Mestel. 2018. Price discovery of cryptocurrencies: Bitcoin and beyond. Economics Letters 165: 58–61. [Google Scholar] [CrossRef]

- Brito, Jerry, Houman Shadab, and Andrea Castillo. 2014. Bitcoin financial regulation: Securities, derivatives, prediction markets, and gambling. Columbia Science and Technology Law Review 16: 144. [Google Scholar] [CrossRef][Green Version]

- Broock, William A., José Alexandre Scheinkman, W. Davis Dechert, and Blake LeBaron. 1996. A test for independence based on the correlation dimension. Econometric Reviews 15: 197–235. [Google Scholar] [CrossRef]

- Caginalp, Carey, and Gunduz Caginalp. 2018. Opinion: Valuation, liquidity price, and stability of cryptocurrencies. Proceedings of the National Academy of Sciences 115: 1131–34. [Google Scholar] [CrossRef]

- Carrick, Jon. 2016. Bitcoin as a complement to emerging market currencies. Emerging Markets Finance and Trade 52: 2321–34. [Google Scholar] [CrossRef]

- Choi, In. 1999. Testing the random walk hypothesis for real exchange rates. Journal of Applied Econometrics 14: 293–308. [Google Scholar] [CrossRef]

- Chu, Jeffrey, Saralees Nadarajah, and Stephen Chan. 2015. Statistical analysis of the exchange rate of bitcoin. PLoS ONE 10: e0133678. [Google Scholar] [CrossRef]

- Corbet, Shaen, Andrew Meegan, Charles Larkin, Brian Lucey, and Larisa Yarovaya. 2018. Exploring the dynamic relationships between cryptocurrencies and other financial assets. Economics Letters 165: 28–34. [Google Scholar] [CrossRef]

- Croman, Kyle, Christian Decker, Ittay Eyal, Adem Efe Gencer, Ari Juels, Ahmed Kosba, Andrew Miller, Prateek Saxena, Elaine Shi, Emin Gün Sirer, and et al. 2016. On scaling decentralized blockchains. In International Conference on Financial Cryptography and Data Security. Berlin and Heidelberg: Springer, pp. 106–25. [Google Scholar]

- Decker, Christian, and Roger Wattenhofer. 2015. A fast and scalable payment network with bitcoin duplex micropayment channels. In Symposium on Self-Stabilizing Systems. Berlin and Heidelberg: Springer, pp. 3–18. [Google Scholar]

- Dierksmeier, Claus, and Peter Seele. 2018. Cryptocurrencies and business ethics. Journal of Business Ethics 152: 1–14. [Google Scholar] [CrossRef]

- Dimpfl, Thomas, and Franziska J. Peter. 2019. Group transfer entropy with an application to cryptocurrencies. Physica A: Statistical Mechanics and Its Applications 516: 543–51. [Google Scholar] [CrossRef]

- Dolado, Juan J., and Helmut Lütkepohl. 1996. Making wald tests work for cointegrated var systems. Econometric Reviews 15: 369–86. [Google Scholar] [CrossRef]

- Domínguez, Manuel A., and Ignacio N. Lobato. 2003. Testing the martingale difference hypothesis. Econometric Reviews 22: 351–77. [Google Scholar] [CrossRef]

- Drożdż, Stanisław, Robert Gebarowski, Ludovico Minati, Paweł Oświecimka, and Marcin Watorek. 2018. Bitcoin market route to maturity? evidence from return fluctuations, temporal correlations and multiscaling effects. Chaos: An Interdisciplinary Journal of Nonlinear Science 28: 071101. [Google Scholar] [CrossRef]

- Dwyer, Gerald P. 2015. The economics of bitcoin and similar private digital currencies. Journal of Financial Stability 17: 81–91. [Google Scholar] [CrossRef]

- Dyhrberg, Anne H., Sean Foley, and Jiri Svec. 2018. How investible is bitcoin? analyzing the liquidity and transaction costs of bitcoin markets. Economics Letters 171: 140–43. [Google Scholar] [CrossRef]

- Escanciano, J. Carlos, and Ignacio N. Lobato. 2009. An automatic portmanteau test for serial correlation. Journal of Econometrics 151: 140–49. [Google Scholar] [CrossRef]

- Fama, Eugene F. 1970. Efficient capital markets: A review of theory and empirical work. The Journal of Finance 25: 383–417. [Google Scholar] [CrossRef]

- Flori, Andrea. 2019a. Cryptocurrencies in finance: Review and applications. International Journal of Theoretical and Applied Finance 22: 1950020. [Google Scholar] [CrossRef]

- Flori, Andrea. 2019b. News and subjective beliefs: A bayesian approach to bitcoin investments. Research in International Business and Finance 50: 336–56. [Google Scholar] [CrossRef]

- Flori, Andrea, Simone Giansante, Claudia Girardone, and Fabio Pammolli. 2019. Banks’ business strategies on the edge of distress. Annals of Operations Research, 1–50. [Google Scholar] [CrossRef]

- Fry, John. 2018. Booms, busts and heavy-tails: The story of bitcoin and cryptocurrency markets? Economics Letters 171: 225–29. [Google Scholar] [CrossRef]

- Garcia, David, Claudio J. Tessone, Pavlin Mavrodiev, and Nicolas Perony. 2014. The digital traces of bubbles: Feedback cycles between socio-economic signals in the bitcoin economy. Journal of the Royal Society Interface 11: 20140623. [Google Scholar] [CrossRef]

- Gomber, Peter, Jascha-Alexander Koch, and Michael Siering. 2017. Digital finance and fintech: Current research and future research directions. Journal of Business Economics 87: 537–80. [Google Scholar] [CrossRef]

- Guo, Yuwei, Jinfeng Tong, and Chen Feng. 2019. A measurement study of bitcoin lightning network. Paper presented at 2019 IEEE International Conference on Blockchain (Blockchain), Atlanta, GA, USA, July 14–17; pp. 202–11. [Google Scholar]

- Hong, KiHoon. 2017. Bitcoin as an alternative investment vehicle. Information Technology and Management 18: 265–75. [Google Scholar] [CrossRef]

- Jiang, Yonghong, He Nie, and Weihua Ruan. 2018. Time-varying long-term memory in bitcoin market. Finance Research Letters 25: 280–84. [Google Scholar] [CrossRef]

- Katsiampa, Paraskevi. 2019. Volatility co-movement between bitcoin and ether. Finance Research Letters 30: 221–27. [Google Scholar] [CrossRef]

- Khan, Nida, and Radu State. 2019. Lightning network: A comparative review of transaction fees and data analysis. In International Congress on Blockchain and Applications. Berlin and Heidelberg: Springer, pp. 11–18. [Google Scholar]

- Kim, Jae H. 2009. Automatic variance ratio test under conditional heteroskedasticity. Finance Research Letters 6: 179–85. [Google Scholar] [CrossRef]

- Kristoufek, Ladislav. 2018. On bitcoin markets (in) efficiency and its evolution. Physica A: Statistical Mechanics and Its Applications 503: 257–62. [Google Scholar] [CrossRef]

- Kumhof, Michael, and Clare Noone. 2018. Central Bank Digital Currencies-Design Principles and Balance Sheet Implications. London: Bank of England. [Google Scholar]

- Latora, Vito, and Massimo Marchiori. 2001. Efficient behavior of small-world networks. Physical Review Letters 87: 198701. [Google Scholar] [CrossRef] [PubMed]

- Latora, Vito, and Massimo Marchiori. 2003. Economic small-world behavior in weighted networks. The European Physical Journal B-Condensed Matter and Complex Systems 32: 249–63. [Google Scholar] [CrossRef]

- Lee, Timothy. 2018. Bitcoin’s Transaction Fee Crisis is Over-For Now. Available online: https://arstechnica.com/tech-policy/2018/02/bitcoins-transaction-fee-crisis-is-over-for-now/ (accessed on 5 April 2019).

- Lo, Andrew W., and A. Craig MacKinlay. 1988. Stock market prices do not follow random walks: Evidence from a simple specification test. The Review of Financial Studies 1: 41–66. [Google Scholar] [CrossRef]

- Lütkepohl, Helmut. 2005. New Introduction to Multiple Time Series Analysis. Berlin and Heidelberg: Springer. [Google Scholar]

- Martinazzi, Stefano, and Andrea Flori. 2020. The evolving topology of the lightning network: Centralization, efficiency, robustness, synchronization, and anonymity. PLoS ONE 15: e0225966. [Google Scholar] [CrossRef] [PubMed]

- Miller, Andrew, Iddo Bentov, Surya Bakshi, Ranjit Kumaresan, and Patrick McCorry. 2019. Sprites and state channels: Payment networks that go faster than lightning. In International Conference on Financial Cryptography and Data Security. Berlin and Heidelberg: Springer, pp. 508–26. [Google Scholar]

- Nadarajah, Saralees, and Jeffrey Chu. 2017. On the inefficiency of bitcoin. Economics Letters 150: 6–9. [Google Scholar] [CrossRef]

- Noldus, Rogier, and Piet Van Mieghem. 2015. Assortativity in complex networks. Journal of Complex Networks 3: 507–42. [Google Scholar] [CrossRef]

- Nowostawski, Mariusz, and Jardar Tøn. 2019. Evaluating methods for the identification of off-chain transactions in the lightning network. Applied Sciences 9: 2519. [Google Scholar] [CrossRef]

- Peng, C.-K., Sergey V. Buldyrev, Shlomo Havlin, Michael Simons, H. Eugene Stanley, and Ary L. Goldberger. 1994. Mosaic organization of dna nucleotides. Physical Review e 49: 1685. [Google Scholar] [CrossRef]

- Peng, C.-K., Shlomo Havlin, H. Eugene Stanley, and Ary L. Goldberger. 1995. Quantification of scaling exponents and crossover phenomena in nonstationary heartbeat time series. Chaos: An Interdisciplinary Journal of Nonlinear Science 5: 82–87. [Google Scholar] [CrossRef]

- Phillip, Andrew, Jennifer Chan, and Shelton Peiris. 2019. On long memory effects in the volatility measure of cryptocurrencies. Finance Research Letters 28: 95–100. [Google Scholar] [CrossRef]

- Phillip, Andrew, Jennifer SK Chan, and Shelton Peiris. 2018. A new look at cryptocurrencies. Economics Letters 163: 6–9. [Google Scholar] [CrossRef]

- Pieters, Gina, and Sofia Vivanco. 2017. Financial regulations and price inconsistencies across bitcoin markets. Information Economics and Policy 39: 1–14. [Google Scholar] [CrossRef]

- Polasik, Michal, Anna Iwona Piotrowska, Tomasz Piotr Wisniewski, Radoslaw Kotkowski, and Geoffrey Lightfoot. 2015. Price fluctuations and the use of bitcoin: An empirical inquiry. International Journal of Electronic Commerce 20: 9–49. [Google Scholar] [CrossRef]

- Poon, Joseph, and Thaddeus Dryja. 2016. The Bitcoin Lightning Network: Scalable Off-Chain Instant Payments. Available online: https://scholar.google.com/scholar?q=The+bitcoin+lightning+network:+Scalable+off-chain+instant+payments&hl=zh-CN&as_sdt=0&as_vis=1&oi=scholart (accessed on 1 October 2020).

- Puliga, Michelangelo, Andrea Flori, Giuseppe Pappalardo, Alessandro Chessa, and Fabio Pammolli. 2016. The accounting network: How financial institutions react to systemic crisis. PLoS ONE 11: e0162855. [Google Scholar] [CrossRef] [PubMed]

- Raimundo, Júnior, Gerson de Souza, Rafael Baptista Palazzi, Ricardo de Souza Tavares, and Marcelo Cabus Klotzle. 2020. Market stress and herding: A new approach to the cryptocurrency market. Journal of Behavioral Finance, 1–15. [Google Scholar] [CrossRef]

- Selgin, George. 2015. Synthetic commodity money. Journal of Financial Stability 17: 92–99. [Google Scholar] [CrossRef]

- Spelta, Alessandro, Andrea Flori, and Fabio Pammolli. 2018. Investment communities: Behavioral attitudes and economic dynamics. Social Networks 55: 170–88. [Google Scholar] [CrossRef]

- Spelta, Alessandro, Andrea Flori, Nicolò Pecora, Sergey Buldyrev, and Fabio Pammolli. 2020. A behavioral approach to instability pathways in financial markets. Nature Communications 11: 1–9. [Google Scholar] [CrossRef]

- Takaishi, Tetsuya. 2018. Statistical properties and multifractality of bitcoin. Physica A: Statistical Mechanics and Its Applications 506: 507–19. [Google Scholar] [CrossRef]

- Tiwari, Aviral Kumar, Rabin K. Jana, Debojyoti Das, and David Roubaud. 2018. Informational efficiency of bitcoin—An extension. Economics Letters 163: 106–9. [Google Scholar] [CrossRef]

- Toda, Hiro Y., and Taku Yamamoto. 1995. Statistical inference in vector autoregressions with possibly integrated processes. Journal of Econometrics 66: 225–50. [Google Scholar] [CrossRef]

- Urquhart, Andrew. 2016. The inefficiency of bitcoin. Economics Letters 148: 80–82. [Google Scholar] [CrossRef]

- Urquhart, Andrew. 2018. What causes the attention of bitcoin? Economics Letters 166: 40–44. [Google Scholar] [CrossRef]

- Vidal-Tomás, David, Ana M. Ibáñez, and José E. Farinós. 2019. Herding in the cryptocurrency market: Cssd and csad approaches. Finance Research Letters 30: 181–86. [Google Scholar] [CrossRef]

- Wald, Abraham, and Jacob Wolfowitz. 1940. On a test whether two samples are from the same population. The Annals of Mathematical Statistics 11: 147–62. [Google Scholar] [CrossRef]

- Weber, Beat. 2016. Bitcoin and the legitimacy crisis of money. Cambridge Journal of Economics 40: 17–41. [Google Scholar] [CrossRef]

- Yermack, David. 2015. Is bitcoin a real currency? an economic appraisal. In Handbook of Digital Currency. Amsterdam: Elsevier, pp. 31–43. [Google Scholar]

- Yermack, David. 2017. Corporate governance and blockchains. Review of Finance 21: 7–31. [Google Scholar] [CrossRef]

- Zhang, Wei, Pengfei Wang, Xiao Li, and Dehua Shen. 2018. Some stylized facts of the cryptocurrency market. Applied Economics 50: 5950–65. [Google Scholar] [CrossRef]

| 12 February 2018 | 12 August 2020 | |

|---|---|---|

| Nodes | 538 | 7916 |

| Channels | 1985 | |

| Density | ||

| Median Degree | 2 | 3 |

| Average Degree | ||

| Median Strength(USD) | ||

| Average Strength (USD) | ||

| Average Capacity (USD) | ||

| Median Capacity (USD) | ||

| Total Capacity (USD) | ||

| Assortativity | ||

| Assortativity (W) | ||

| Diameter | 6 | 12 |

| Radius (LCC) | 4 | 6 |

| Transitivity (W) | ||

| Global Efficiency Norm |

| PANEL A | |||||||

| Period | Runs Test | Bartels Test | BDS Test | Automatic Portmanteau Test | AVR Test | DL (cp) Test | DL (kp) Test |

| 2015/01/01–2015/12/31 | 0.00053 | 0.00005 | 0.00000 | 0.10644 | 0.35000 | 0.00000 | |

| 2016/01/01–2016/12/31 | 0.01605 | 0.00016 | 0.00000 | 0.08296 | 0.04800 | 0.00000 | 0.00000 |

| 2017/01/01–2017/12/31 | 0.00164 | 0.00000 | 0.00000 | 0.00041 | 0.00000 | 0.00000 | 0.00000 |

| 2018/01/01–2018/12/31 | 0.07434 | 0.00070 | 0.00000 | 0.02037 | 0.01400 | 0.00000 | 0.00000 |

| 2019/01/01–2019/12/31 | 0.00078 | 0.00000 | 0.00148 | 0.00033 | 0.00800 | 0.00000 | 0.00000 |

| 2018/02/12–2020/08/12 | 0.00002 | 0.00000 | 0.00000 | 0.00002 | 0.00200 | 0.00000 | 0.00000 |

| 2015/01/01–2020/08/12 | 0.00000 | 0.00000 | 0.00000 | 0.00000 | 0.00000 | 0.00000 | 0.00000 |

| PANEL B | |||||||

| Period | Runs Test | Bartels Test | BDS Test | Automatic Portmanteau Test | AVR Test | DL (cp) Test | DL (kp) Test |

| 2015/01/01–2015/12/31 | 0.00036 | 0.00000 | 0.00000 | 0.00000 | 0.00000 | 0.00000 | 0.00000 |

| 2016/01/01–2016/12/31 | 0.02127 | 0.00001 | 0.00000 | 0.00055 | 0.00000 | 0.00000 | 0.00000 |

| 2017/01/01–2017/12/31 | 0.00016 | 0.00000 | 0.00037 | 0.00000 | 0.00000 | 0.00000 | 0.00000 |

| 2018/01/01–2018/12/31 | 0.00000 | 0.00000 | 0.00081 | 0.00000 | 0.00000 | 0.00000 | 0.00000 |

| 2019/01/01–2019/12/31 | 0.00016 | 0.00000 | 0.03740 | 0.00092 | 0.00000 | 0.00000 | 0.00000 |

| 2018/02/12–2020/08/12 | 0.00000 | 0.00000 | 0.00009 | 0.00000 | 0.00000 | 0.00000 | 0.00000 |

| 2015/01/01–2020/08/12 | 0.00000 | 0.00000 | 0.00000 | 0.00000 | 0.00000 | 0.00000 | 0.00000 |

| Panel A: Column G-Causes Row | BTC Alpha | BTC Vol Alpha | BTC Price | BTC Returns | |

| LN efficiency | statistics | 5.50 | 0.70 | 1.70 | 1.60 |

| p-value | 0.36 | 0.98 | 0.42 | 0.46 | |

| Panel B: Row G-Causes Column | BTC Alpha | BTC Vol Alpha | BTC Price | BTC Returns | |

| LN efficiency | statistics | 7.40 | 2.90 | 0.41 | 0.31 |

| p-value | 0.19 | 0.72 | 0.81 | 0.86 |

| Row G-Causes Column | Assortativity | Density | Transitivity | Median Strength | Median Capacity | |

|---|---|---|---|---|---|---|

| BTC returns | statistics | 0.17 | 0.96 | 3.10 | 0.69 | 4.70 |

| p-value | 0.68 | 0.33 | 0.21 | 0.41 | 0.03 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Martinazzi, S.; Regoli, D.; Flori, A. A Tale of Two Layers: The Mutual Relationship between Bitcoin and Lightning Network. Risks 2020, 8, 129. https://doi.org/10.3390/risks8040129

Martinazzi S, Regoli D, Flori A. A Tale of Two Layers: The Mutual Relationship between Bitcoin and Lightning Network. Risks. 2020; 8(4):129. https://doi.org/10.3390/risks8040129

Chicago/Turabian StyleMartinazzi, Stefano, Daniele Regoli, and Andrea Flori. 2020. "A Tale of Two Layers: The Mutual Relationship between Bitcoin and Lightning Network" Risks 8, no. 4: 129. https://doi.org/10.3390/risks8040129

APA StyleMartinazzi, S., Regoli, D., & Flori, A. (2020). A Tale of Two Layers: The Mutual Relationship between Bitcoin and Lightning Network. Risks, 8(4), 129. https://doi.org/10.3390/risks8040129