1. Introduction

Liquidity risk is the risk caused by the adverse movement of a price which corresponds to a trading size. A large buy order drives the price up and a large sale order drives it down. Therefore, a large trader is always exposed to this hidden possible loss. Although the idea that the evolution of the stock price depends on the trading volume has existed for several decades, it was not widely studied until only about a decade ago. In the past decade, the literature on the liquidity risk has been growing rapidly; for example,

Jarrow (

1992,

1994,

2001);

Back (

1993);

Frey (

1998,

2000);

Frey and Stremme (

1997);

Cvitanic and Ma (

1996);

Subramanian and Jarrow (

2001);

Duffie and Ziegler (

2001);

Bank and Baum (

2004);

Cetin et al. (

2004);

Jarrow (

1992,

1994) proposed a discrete-time framework where prices depend on the large trader’s activities via a reaction function of his/her instantaneous holdings. He found conditions for the existence of arbitrage opportunities for a large trader.

Cvitanic and Ma (

1996) studied a diffusion model for the price dynamics where the drift and volatility coefficients depend on the large investor’s trading strategy.

Frey and Stremme (

1997) developed a continuous-time analogue to Jarrow’s discrete-time framework. They derived an explicit expression for the transformation of market volatility with a large trader.

Although the cost caused by the liquidity risk have been studied widely both theoretically and empirically, most models in mathematical finance did not include it.

Cetin et al. (

2004,

2006) introduced a rigorous mathematical model of the liquidity cost and showed modified fundamental theorems of the asset pricing.

Bank and Baum (

2004) introduced a general continuous-time model for an illiquid financial market with a single large trader. They proved the absence of arbitrage for a large trader, characterized the set of approximately attainable claims and showed how to compute superreplication prices. Studies related to this topic extend to

Cetin et al. (

2010);

Rogers and Singh (

2010).

Ku et al. (

2012) studied a discrete time hedging strategy with liquidity risk under the Black-Scholes model

Black and Scholes (

1973). They used the Leland discretization scheme to find the optimal discrete time hedging strategy under the Black-Scholes model. As an extension of it, we study in this paper a more general underlying model which is called the constant elasticity of variance (CEV) model. The CEV model generalizes the Black-Scholes model so that it can capture volatility smile effect. The model is widely used by practitioners in the financial industry, especially to model equities and commodities. The CEV model, introduced by

Cox (

1975);

Cox and Ross (

1976) is the following,

Here,

(elasticity),

(mean return rate) and

(volatility) are given constants. Note that the particular case

corresponds to the well-known Black-Scholes model

Black and Scholes (

1973).

On the other hand, many underlying assets are still approximately close to a log-normal distribution. This suggests that the elasticity constant is not exactly 2, but is close to 2. In this sence, we set to apply the asymptotic analysais where .

In

Cetin et al. (

2004,

2006), the stock price

depends on the time

t and trading volume

x. They assume the multiplicative model

, where

f is smooth and increasing function with

.

becomes a marginal stock price. Empirical studies suggest that the liquidity cost is relatively small compared to the stock price, as in

Cetin et al. (

2006). In other words,

is a small positive number. We refer to

Cetin et al. (

2006) for details.

These two observations motivate us to use the perturbation theory

Hinch (

2003) for partial differential equations (PDEs) in the liquidity risk problem. The perturbation method is a mathematical method for obtaining an approximate solution to a given problem which cannot be solved exactly, by starting from the exact solution of a related problem. Perturbation theory is used when the problem is formulated by a small term to a mathematical description of the exactly solvable problem. For example, see

Park and Kim (

2011). Perturbation theory is a useful tool to deal with liquidity risk under the CEV diffusion model based on some small parameters. It gives us a practical advantage in pricing of financial derivatives with the liquidity risk.

The CEV diffusion model is the easiest model to explain the volatility smile phenomenon. It has the disadvantage that the implied volatility estimated by the deep OTM(Out of The Money) option does not match the actual data, but it is easy to apply and the accuracy is guaranteed near the ATM(At The Money). Therefore, when reflecting the skewed phenomenon and hedge the options near ATM, it has a practical advantage compared to the stochastic volatility model. However, it is inadequate to deal with the hedge of a complex structured derivatives, which is inadequate compared to the stochastic volatility model, and subsequent studies need to address the liquidity model under the stochastic volatility model.

We study the liquidity risk under the CEV diffusion model. We apply the Leland approximation scheme (

Leland 1985) to obtain a nonlinear partial differential equation for the option pricing. We find an approximation solution of this problem using the perturbation method.

The rest of this paper is organized as follows.

Section 2 introduces the Cetin et al. model and the CEV diffusion.

Section 3 gives us a nonlinear partial differential equation for the option pricing with the liquidity cost.

Section 4 discusses an analytic solution for the PDE given in

Section 3.

3. The Pricing Equation

We consider a European put option

with the expiration date

T with the strike price

K, and let

be the price of it at time

t. (We can similarly deal with call options and other European options, however, we only deal with a put option here.) We consider the delta hedging

defined by

for a price function

P. Although the market is still complete, since we deal with a discrete time trading with the liquidity cost, a perfect hedging is not possible. Therefore, we cannot make the hedging error 0. However, we can provide a sufficient pricing equation whose expected hedging error approaches zero as

. We assume that

is a class of

.

The next theorem gives us a hedging strategy which makes the expected hedging error go to 0 as the size of the time step gets smaller. Recall that .

Theorem 1. Let be the solution of the nonlinear partial differential equationwith the terminal condition . Then the expected hedging error of the corresponding delta hedging strategy approaches 0 as . Proof. First, we consider Taylor expansion formulas of

P,

X.

From (

7) and

, we have

On the other hands, by the Taylor expansion formula, we also have

Moreover, from (

5),

Therefore, (

12) becomes

Now, the hedging error is

Since

Z is a standard normal, we have

Therefore,

if

P satisfies

Finally, the terminal condition follows from the definition of the put option. □

We notice that the the effect of the liquidity cost appear through the first derivative . We now study the convergence of the discrete hedging strategy to the payoff of the option. Let be the hedging error over , .

Theorem 2. Consider the discrete hedging strategy where is a solution of the Equation (9). Its value at the terminal time T converges almost surely to the payoff of the option as . Proof. Since

is smooth, we can check that

where

M is a constant which does not depend on

. Therefore, we have

Moreover, we have

Therefore, by the Law of Large Numbers for Martingales (refer to

Feller 1970), we obtain

This implies that the total error

as

a.s.. □

The above theorem tells us that the delta hedging strategy in Equation (

9) asymptotically replicates the contingent claim as the time interval gets smaller. So, the next step is to calculate

so that we can calculate the corresponding hedging strategy. We study this in the following section.

4. Asymptotic Expansion of the Solution

In this section, we discuss an analytic solution of the Equation (

9). Since

satisfies the nonlinear partial differential equation (NPDE) (9), it is hard to find a closed form solution. However, as we already discussed before for the expansion of

f, we can apply the asymptotic expansion to (9). We first assume that there exists a series

such that

. Now, we reformulate the NPDE (Nonlinear Partial Differential Equations) (

9),

Note that the first term is an

order term, the second is an

order one, and the third term is an

term. Inserting these series form into (

24), we obtain following equations for each coefficient

for

,

where terminal conditions are given by

and

. In general, we obtain the partial differential equation for

,

where

.

4.1. A Solution of Each Coefficient

To find

for

, we need a lemma about the Feynman-Kac formula for our nonhomogeneous PDE. First, we define a geometric Brownian motion

by

and a differential operator

Then, we have the following.

Lemma 1. If the solution of the PDE problem satisfies the condition and , then is given by Proof. This is the well-known Feynman-Kac formula for the Black-Scholes model. It provides a stochastic representation of the solution of PDEs. We refer to the chapter 8 of

Oksendal (

2003) for details. □

The next theorem give us , which is the first term of the expansion.

Theorem 3. The leading order solution is given by Proof. This is the well-known Black-Scholes put option price. We refer to

Shreve (

2000) for details. □

Next, we find a solution of remaining terms for general l and m.

Theorem 4. For , the solution is recursively given by Proof. First, we consider the case

. In this case,

. Since

is smooth on only

and continuous at

, we have to deal with it carefully. First, note that there exist a smooth function

on

such that

. Now we consider the PDE

where

. By Lemma 1, we have

It is well-known that the solution of PDE

and

is

(the uniqueness of a solution). Therefore,

as

. By the dominated convergence theorem, we have

On the other hand,

leads to

Moreover,

is twice continuously differentiable with respect to

s. On the other hand, we can obtain the similar result for

using the same argument. Now, we use the induction argument. Suppose that

satisfies the assumption of Lemma 1. Then we have

□

Using the above theorem, we can calculate

and the corresponding hedging strategy

. While it is hard to calculate these quantities analytically, we can calculate these relatively easily numerically.

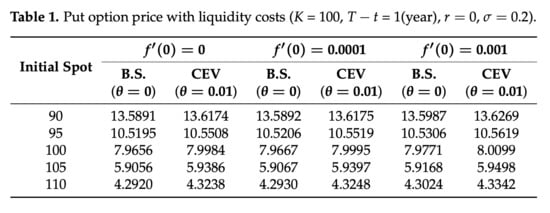

Table 1 shows the European put option price with the liquidity cost computed by our approximation formula. We present an approximate option price,

. Option prices are obtained by solving the formula given in Theorem 4. Parameters that we use here are

,

,

and

year.

Table 1 presents numerical results for several cases. We use the formula (31) and numerical integration for the first order (

or

) calculation. The first example,

is the case without the liquidity cost. In this case, we can buy and sell the underlying asset at the spot price. However, in reality, the liquidity provider quotes different prices for buying and selling, and the liquidity cost does exist. So we can only buy or sell the underlying asset after adding the bid and ask spread. The second and the third cases are when the regular bid and ask spread rates are 0.000001 and 0.00001 percent of spot, respectively. The second case,

, considers 0.000001 percent spread of the spot price. For example, if the spot price is 10000 dollars, then the spread is one cent. This means that liquidity risk causes an additional hedge cost for the dynamic hedging that is, we need more asset and funding money. This comparison result is reasonable in the sense that a higher liquidity cost produces a bigger option premium for the same spot price. Since the liquidity cost makes the hedging cost higher, an option price should be higher for a bigger liquidity cost. In addition, the CEV parameter provides a non-flat volatility risk. Therefore, the CEV option price should be higher than the Black-Scholes price. We observe this from the fact that the second column is larger than the first column.

Remark 1. For a practical application, we can apply our method as follows. From real market data, we observe two small parameters ϵ and θ. Then, we can apply the perturbation method for this problem. By applying the perturbation method, we can derive an approximation solution of option price with liquidity costs.

4.2. Convergence of the Series

In this subsection, we study the convergence of

Previously, we assumed that the existence of the series. However, to guarantee the existence of the series, we need to prove it. In this case, the existence of the series is equivalent to convergence of the series. Therefore, we show the convergence. Let

, then we have the following.

Theorem 5. For all , we have Proof. First, we show

. Note that

where

K is the exercise price. Moreover,

and

are

as

and bounded by

, since

for all

. By the probabilistic representation of

, we have

On the other hand, the integration formula of

implies that

and

,

are also

as

. Therefore, all of them are bounded and infinitely differentiable. By the same argument, we have the same result for

. Now, we apply the induction. Suppose that

for

,

and

and

are smooth and bounded. Then, we have

where

is a positive constant determined by

. Then,

On the other hand,

is a martingale under

. Let

. Then, by the Doob’s maximal inequality, we have

This implies that

. Moreover, the integration formula of

implies that

and

are also

as

. Therefore, by the induction argument, we have

for all

. □

By the above theorem, the series satisfies

for given

. We now define

. Clearly,

and

satisfies NPDE (

24) by (

28). Therefore, we can conclude that

and

{kind=link}