1. Introduction

Since the magnitude of the 2008 financial crisis, discourses pertinent to risk management variations have emerged denoting the interrelated role of economic cycles, as well as derivative markets and geopolitical fragmentation (

Gouliamos 2014;

Han et al. 2019). Reducing business risk is a prime concern of corporate managers. This type of risk is indicated by the extent of fluctuations of income streams (

Gerhart and Trevor 1996;

Miller and Chen 2003), which can significantly impact a firm’s survival. Lower risk results in greater credibility, with increased access to financial resources; this reduces capital costs and the likelihood of bankruptcy (

Matta and McGuire 2008;

Miller and Chen 2004). Conventionally, the process of diversification has been considered the most effective way to reduce corporate risk (

Andersen et al. 2007;

Maurer 2011;

Sun et al. 2020), with much empirical evidence supporting a negative diversification-risk relationship (

Hoskisson 1987;

Keats and Hitt 1988). However, the debate regarding the effectiveness of diversification for risk reduction remains inconclusive. Some researchers believe that the diversification to risk relationship is curvilinear (

Tallman and Li 1996), while others maintain that the relationship is no discernible (

Lubatkin and O’Neill 1987). In addition, some researchers have suggested that, due to the lack of statistical difference in business risk between the diversified and non-diversified firms, not all diversification strategies lead to risk reduction (

Lubatkin and O’Neill 1987). Given this continuing uncertainty and the importance of diversification and risk to practitioners, this study re-examines the diversification-risk relationship from the new perspective of Organizational Portfolio Analysis (OPA).

Further investigation of the diversification-risk relationship is warranted for three reasons. First, clearer understanding of the theoretical foundation of this relationship could provide scholars and corporate managers with a new perspective on how to better allocate resources (

Hill and Hansen 1991). Second, further understanding may assist to reduce costs of creating, merging, or acquiring new business units (BUs), in order to diversify a firm’s portfolio (

Amihud and Lev 1981). Third, by examining this relationship, scholars and managers can better determine the overall mechanisms of corporate risk reduction (

Bettis and Hall 1982).

Based on Organizational Portfolio Analysis (OPA), this study re-examines the diversification-risk relationship from three perspectives. First, OPA views a corporation as a portfolio comprising several individual BUs, and this suggests that diversification may not be a key factor directly contributing to risk reduction. If diversification strategies were based solely on numbers of BUs and sales contributions of BUs, simply rising the extent of diversification does not guarantee a risk reduction, as it may not influence correlations between BU income streams. Second, OPA explains the measures to analyze the portfolio effect, which is a measure of the cumulative contributions of all BUs to the firm’s business risk. OPA focuses on the extent of diversification and the movements of individual BU incomes. This income movement for each BU is similar to a sinewave, where BU income rises and falls. If all BU incomes are synchronized, moving in the same direction, then BU coefficient correlations are 1. This means that there will be no risk reduction, regardless of what the level of diversification might be. Third, OPA specifically introduces the concept of ‘synchronization compensation’ to capture the amount of risk reduction where there is a low level of correlation between BU income flows (

Donaldson et al. 2012). While conventional diversification-risk research does not measure such correlations, OPA has highlighted the possibility of incorporating relationships between income flows of BUs into the assessment.

As the prime objective of this research is to examine how the diversification strategy may affect corporate risk, it is relevant to briefly review the concept of risk, together with the relationship of diversification to risk as well as the OPA perspective. The development of the three working hypotheses is discussed below.

2. Concepts, Relationships and Development of Hypotheses

There are different definitions for risk (

Miller and Reuer 1996). Risk management, relationships, and approaches have also been hot research topics, involving many aspects of business and society (

Liu et al. 2020;

Luo et al. 2020;

Yue et al. 2020;

Shao et al. 2020;

He et al. 2019). The literature describes two forms of corporate risk: first, there is accounting risk, or fluctuation, in a firm’s aggregate earning streams such as sales or profitability (

Ball and Brown 1969); and second is market risk, relating to fluctuations of stock market prices (

Blume 1970). This study focuses on accounting risk, since it is more directly connected to managerial decisions (

Bettis and Hall 1982). Although potentially relevant, market risk includes both internal influences (controllable by managers), as well as external stock market factors, and so is considered outside the scope of this study (

Chang and Thomas 1989).

The topic of corporate diversification has been widely studied (

Chen and Chu 2012;

Palich et al. 2000;

Park and Jang 2012), and two major approaches to investigating diversification are identified (

Datta et al. 1991). The first approach, relating to degree or extent, involves the Berry-Herfindahl and Jacquemin-Berry’s entropy methods; the second approach, relating to type of diversification, most commonly applies Rumelt’s Scheme (

Rumelt 1974). Both approaches are used here to investigate diversification as it relates to risk.

Most previous diversification-risk studies have argued that diversification leads to lowered risk, in one of three ways. The first mechanism is via portfolio logic: this is where managers apply a diversification strategy to achieve a particular portfolio effect, to reduce the overall variance in total revenue or profitability (

Chakrabarti et al. 2007). Companies’ BUs might have differing income flows in different fields and the movements might anticipate, lag behind, or coincide with the macro business cycle. Where firms have BUs with varying performances over time, there is reduced volatility in sales and profitability, meaning lower risk.

Parenting advantage is another reason that risk may be lowered through diversification, as it involves companies re-allocating resources among BUs (

Campbell et al. 1995;

Goold et al. 1998). This strategy allows a firm to overcome crisis events, such as possible bankruptcy, or to reinforce a vulnerable BU (

Datta et al. 1991). This ability to move financial resources as required confers advantage by enhancing firm competitiveness and reducing risk (

Campbell et al. 1995).

The third way to ensure a lowering of risk is to expand the size of the company (

Chang and Thomas 1989). Larger companies are usually able to attract investment more easily, and obtain the benefits from economies of scale, to survive during critical periods (

Balakrishnan and Fox 1993). Building on the above understanding we hypothesize that:

Hypothesis 1. Diversification is negatively related to corporate risk.

Donaldson et al. (

2012), from an OPA perspective, incorporated correlations between income flows into an overall analysis of risk to the firm. They argued that firms may reduce risk more by diversifying into a single BU, with an income flow that is temporally the reverse of the existing income; in this instance, a decline in revenue of one BU can be offset by a rising income in another BU (

Donaldson et al. 2012). Therefore, to enhance a firm’s portfolio effect on risk reduction, BUs with opposite income cycles are more important than traditional ideas of diversification (number of BU, size of BU). To conceptualize this situation,

Donaldson et al. (

2012) introduced the idea of synchronization compensation, which captures the extent to which risk is reduced as a result of income fluctuations of different BUs inside the portfolio offsetting each other. In theory, in a firm with only two business units, generating equal incomes countercyclically, then the corporate risk will be close to zero.

Donaldson et al. (

2012), however, did not assess synchronization compensation to empirically examine how this affects risk. Hence, building on the work of these researchers, we developed the notion of desynchronicity, which is designed to: (i) assess the extent to which a firm’s portfolio achieves synchronization compensation by capturing the combined effects of BU incomes; and (ii) estimate the degree to which these incomes are minimally correlated with the remaining income streams in the corporate portfolio of a firm (

Shughart and Donaldson 2004).

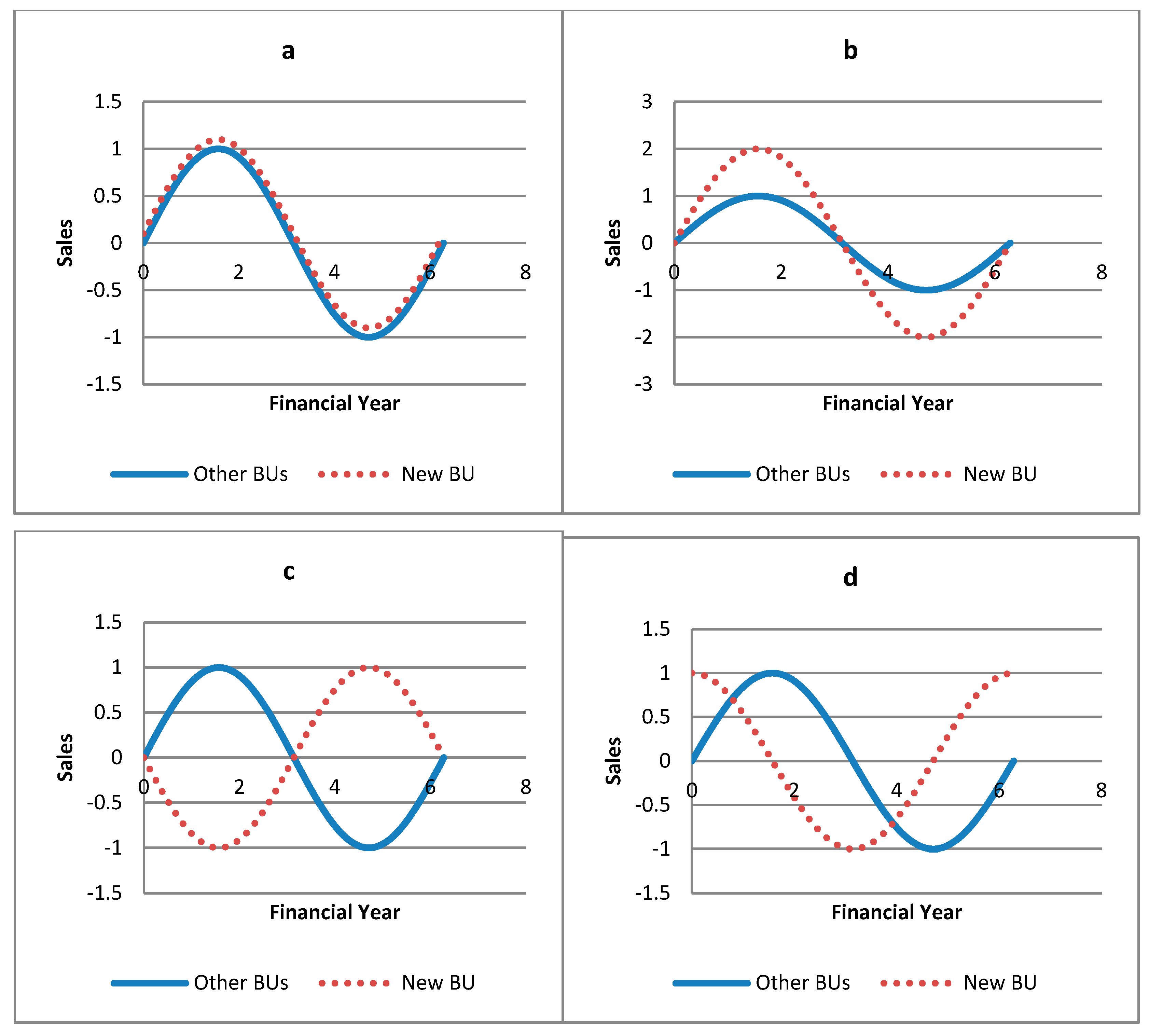

Figure 1 illustrates different circumstances to further explain the concept of desynchronicity. If all BUs of a firm, including new acquisitions, have income flows moving in the same direction simultaneously (

Figure 1a), there is high correlation, no synchronization compensation, and no risk reduction. If a high-risk BU (i.e., volatile, fluctuating income) is acquired, with income movement coinciding with existing BUs (

Figure 1b), the new BU will significantly increase risk. However, if a new BU’s income stream is moving with a different frequency or pattern to existing BUs (

Figure 1c), this will increase desynchronicity of the portfolio and reduce risk. Thus, an effective diversification strategy for risk management is expanding to BUs that increase desynchronicity in the portfolio. Even moderate desynchronicity (

Figure 1d) can result in significant reduction of corporate risk.

In contrast to previous studies, desynchronicity is presented as an integrative measure that incorporates all risk reduction, where BUs are not in exactly the same cycle. From the above, a second hypothesis is proposed:

Hypothesis 2. Desynchronicity is negatively related to corporate risk.

To develop OPA,

Donaldson et al. (

2012) examined four leading corporations, to study how their corporate risk was affected by their diversification strategies. In their study, the mildly diversified firm (e.g., IBM) reduces corporate risk far below the average risk of its original BUs. On the other hand, they found that after the highly diversified Colonial Sugar Refining (CSR) decreased its level of diversification, it also had decreased corporate risk. This was because the sales of the divested BU were positively correlated with the main sales of the corporation, and, hence, did not create much portfolio effect. Moreover, this BU had a higher BU risk if standing alone, thereby increasing the corporate risk. Thus, the extent to which a firm diversifies does not necessarily correlate with risk reduction.

In contrast,

Donaldson et al. (

2012) argued that synchronization compensation is more efficient in reducing corporate risk compare to just low risk BUs only. The introduction of desynchronicity makes it possible for us to compare the effectiveness in risk reduction by diversification and synchronization compensation (measured by desynchronicity). Based on this OPA capacity, we propose a third hypothesis:

Hypothesis 3. Desynchronicity is more negatively related than diversification to corporate risk.

4. Results and Models

This section presents the statistics and summarizes the outcomes of previously described analyses.

Table 1 shows results for the 737 firms with information about BUs’ sales.

Table 2 shows results for the 332 firms with information about BUs’ ROA. Descriptive statistics are not presented for calculating the change in sales/ROA; time-series methods eliminated fixed-effects.

To test Hypothesis 1, both the Jacquemin-Berry entropy and Berry-Herfindahl methods were used; key results are presented in

Table 3 and

Table 4, respectively. For each method, the study ran four models displaying regressions between product diversification and corporate risk. Model 1 and Model 2 applied the CV of sales and the SD of ROA, respectively, and acted as benchmarks for the calculation of risk levels. A no discernible relationship still held in first difference methods, which is the difference between two periods (2002–2006 vs. 2007–2011). Model 3 and Model 4 applied CV of sales and SD of ROA, respectively, to calculate each variable by the change between two periods.

Table 3 summarizes the Jacquemin-Berry entropy method results. None of the models supported a negative diversification-risk relationship. Model 1 showed that diversification had a negative, although not significant, impact on corporate risk, measured by CV of sales (b = −0.05,

p > 0.05). Similarly, Model 2 showed that entropy diversification had a nonsignificant relationship with corporate risk, measured by SD of ROA (b = −0.05,

p > 0.05). In Model 3, this entropy method did not demonstrate statistical significance related to corporate risk, measured by ∆ CV of Sales (b = −0.18,

p > 0.05), or to ∆ SD of ROA (b = −0.16,

p > 0.05) in Model 4. These findings suggest that the diversification is not significantly related to corporate risk.

Table 4 shows that the Berry-Herfindahl method had similar p-values and R-squared values to the entropy method. Models 1, 2, and 4 all suggested insignificant results between product diversity and corporate risk. Model 1 indicated that the Berry-Herfindahl diversification does not significantly impact on risk, as measured by CV of sales (b = −0.12,

p > 0.05). This was consistent with when risk was measured by the SD of ROA in Model 2 (b = −0.08,

p > 0.05). When first difference data were considered (in Model 3), the Berry-Herfindahl diversification had a marginal statistical significance in relation to ∆ CV of Sales (b = −0.39,

p < 0.10). Nevertheless, there is no association with ∆ SD of ROA (b = −0.46,

p > 0.05) in Model 4. In summary, the evidence for the diversification-risk hypothesis is very limited; no model showed a relationship between diversification and risk that was statistically significant, where

p < 0.05.

Based on Rumelt’s scheme, this study categorized the sample into four groups, which comprised single, dominant, related, and unrelated businesses.

Table 5 summarizes results of an ANOVA of these subgroups for corporate risk. In the sample of 737 firms in which risk was measured by CV of sales, 48 were single businesses, 292 were dominant, 262 were related diversified businesses, and 135 were unrelated diversified businesses. As the ANOVA model demonstrates, the effect for diversification on corporate risk was marginally significant to nonsignificant. In the sample of 332 firms where risk was measured by SD of ROA, 22 were single businesses, 124 were dominant firms, 107 were related diversified businesses, and 79 were unrelated diversified firms. The significance level calculated from this method exceeded 0.10 and, thus, no significant effect of diversification groups for corporate risk was detected.

To examine whether any group could be distinguished from others, in terms of risk, the risk means of all groups were compared. The

Table 6 results indicated that dominant (DOM) and related diversified (RD) firms were less risky than single or unrelated diversified (UD) firms. Among all the groups, only related diversification had a marginal significantly lower risk (

p < 0.10) than single businesses and, overall, there was no statistically significant difference (

p < 0.05) between the four groups. This indicates that the diversification measure, based on Rumelt’s scheme, could not detect a risk reduction.

Table 7 shows that, in Model 1, where CV of sales was applied to measure risk, a significant negative relationship between desynchronicity and risk (b = −0.18,

p < 0.001) was demonstrated. For risk measured by the SD of ROA (Model 2), a negative association between desynchronicity and corporate risk (b = −0.36,

p < 0.001) was shown. In conjunction with regression results in Model 3 (b = −0.19,

p < 0.001) and Model 4 (b = −0.32,

p < 0.001), the findings supported Hypothesis 2 (that corporate risk decreases when desynchronicity increases). Moreover,

R2 and Adjusted

R2 in the models for desynchronicity were significantly higher than models for diversification. For example, Model 1 of desynchronicity had a

R2 of 0.26, which was twice that of Model 1 of both entropy methods’

R2 (0.13) and Berry-Herfindahl methods’

R2 (0.13). These findings support our argument that desynchronicity, rather than diversification, could reduce the levels of corporate risk.

A bootstrapping technique was used to investigate whether desynchronicity is more accurate than diversification in predicting corporate risk reduction. As shown in

Table 8, the results of a bootstrapping estimation with 1000 bootstrap resamples supported the sign and significance of Hypothesis 3, regardless of the measures of diversification and corporate risk. Specifically, all eight bootstrapping results were positive, which means the impact of desynchronicity was significantly stronger than diversification on risk. Moreover, all the confidence intervals excluded zero, indicating that desynchronicity, rather than diversification, should be applied for risk prediction. The results suggested that desynchronicity, rather than diversification, could explain more corporate risk.

5. Discussion

In summary, Hypothesis 1 was not supported, as very limited evidence supported the postulation that diversification is negatively associated with risk; no statistical significance was found between product diversification and corporate risk. The empirical findings presented also support the idea that diversification is not the key to reducing risk. All three diversification measures (Berry-Herfindahl, entropy, and Rumelt) failed to follow portfolio logic, and had little or no correlation with low levels of corporate risk. This study has provided the first empirical evidence that challenges the conventional understanding that diversification significantly affects the level of corporate risk. However, this unexpected finding, of a no discernible relationship between diversification and corporate risk, merits further investigation. This research contributes to existing debate and managerial practice in two ways. First, it has led to the development of an integrative quantitative measure of desynchronicity to operationalize the concept of synchronization compensation, which is one of the most important elements in OPA. Second, it has provided empirical evidence that although no significant relationship is found between diversification and risk, there is a significant negative desynchronicity-risk relationship.

There are three managerial implications from this study. First, managers promoting diversification strategies should be more realistic about the relationship of diversification and risk. As diversification is not significantly related to low risk, it may not be the most appropriate strategy. Second, the firm needs to ensure that BUs within the corporate portfolio continue to generate income streams with low levels of correlation. Assessing this correlation requires sufficient time (e.g., up to 10 years) to detect and trace cycles in each BU. Third, desynchronicity can be used as a quantitative indicator of risk in a portfolio. This permits a more precise understanding of the impact of any BU on risk levels. For example, the indirect and long-term benefits of desynchronicity, an investment into a new high-risk BU, with low incomes correlation with existing BUs, can be assessed in terms of a significant portfolio effect to reduce corporate risk.

While contributing to knowledge of the mechanisms of risk reduction, this study has some limitations that may offer opportunities for future study. The majority of firms in the dataset did not have comprehensive BU data for 10 consecutive years, and the models based on historical data. Whether the desynchronicity would have similar effect on risks in different periods can be another field for study. This study focused mainly on corporate risk without considering corporate return; however, a more comprehensive understanding could be achieved by examining the impact of desynchronicity on returns. Finally, there is a potential issue in this study of endogeneity, in terms of missing variables, and this area is of great interest to management scholars (

Hamilton and Nickerson 2003).

,

,

{kind=link}