Cryptocurrencies’ Impact on Accounting: Bibliometric Review

Abstract

1. Introduction

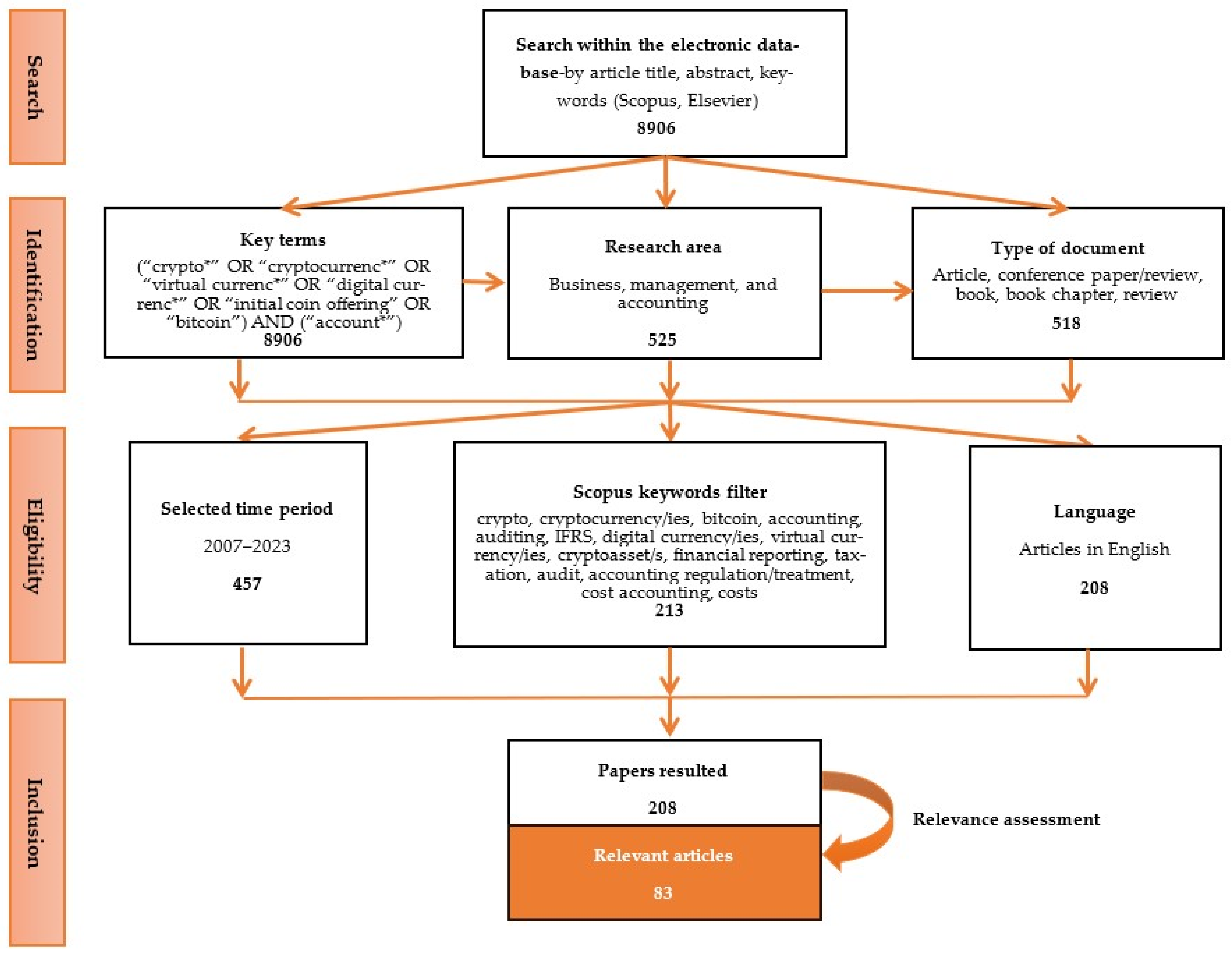

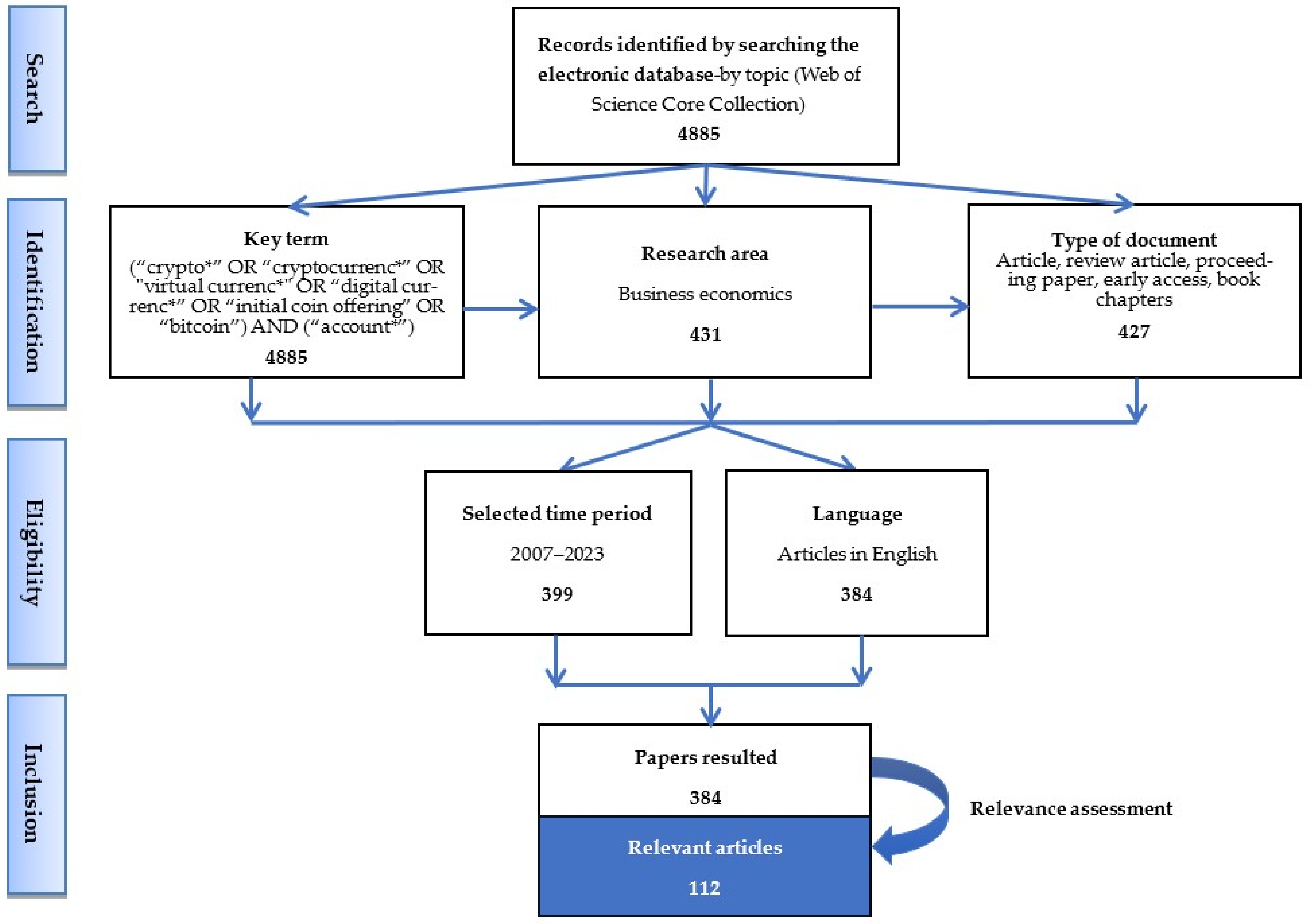

2. Research Method

2.1. Keywords and Data Selection

2.2. Method of Data Refining and Data Analysis

3. Descriptive Bibliometric Analysis

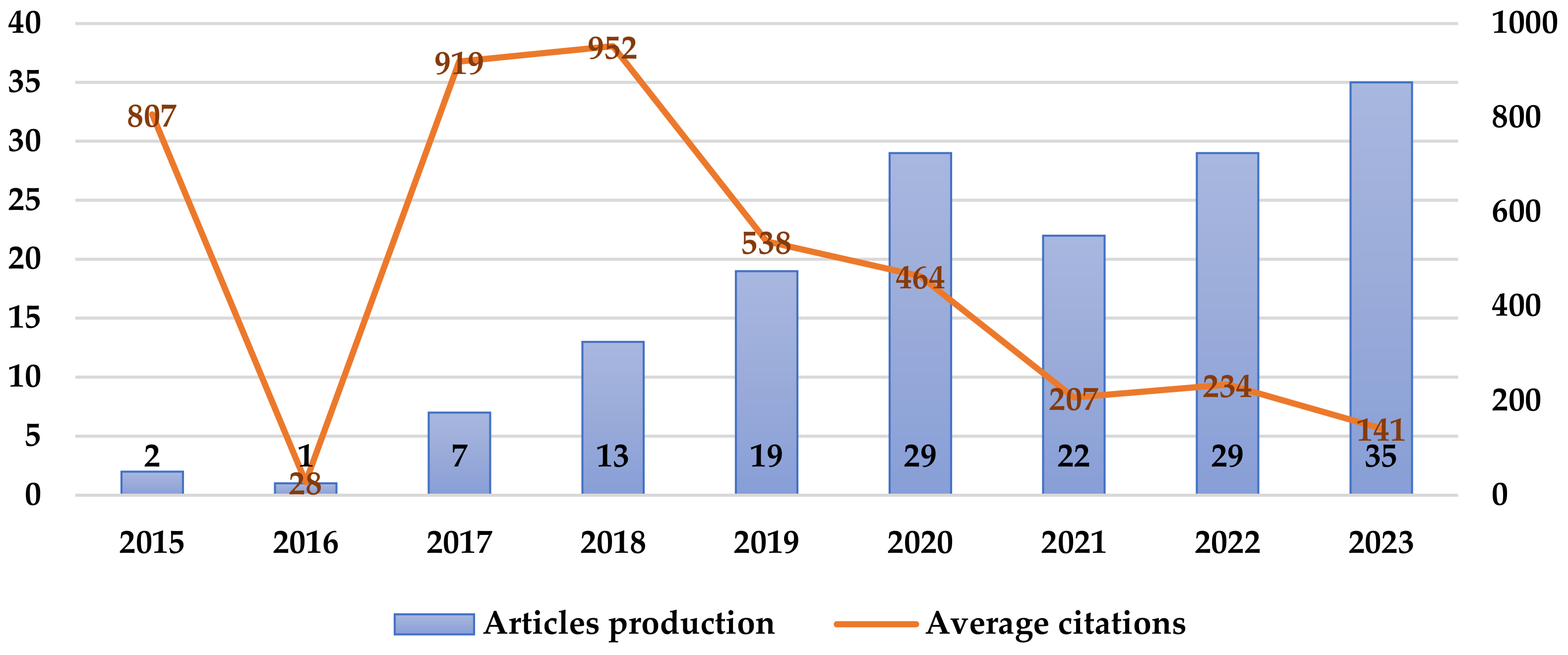

3.1. Annual Scientific Production and Citations

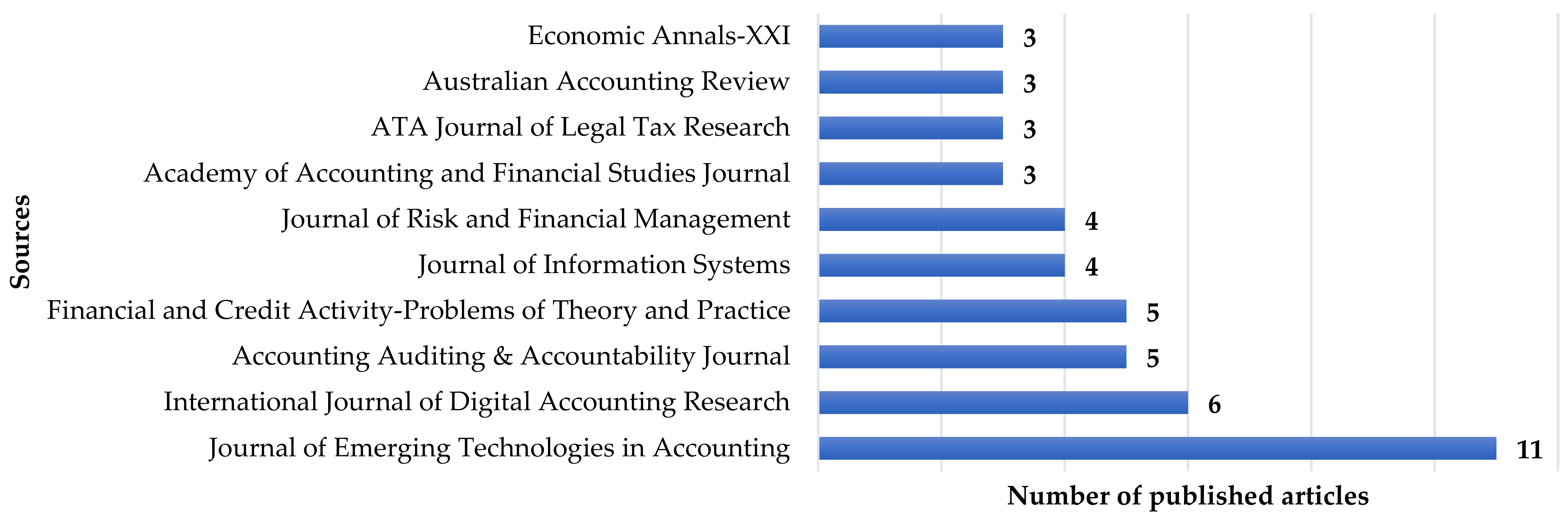

3.2. Publications’ Sources

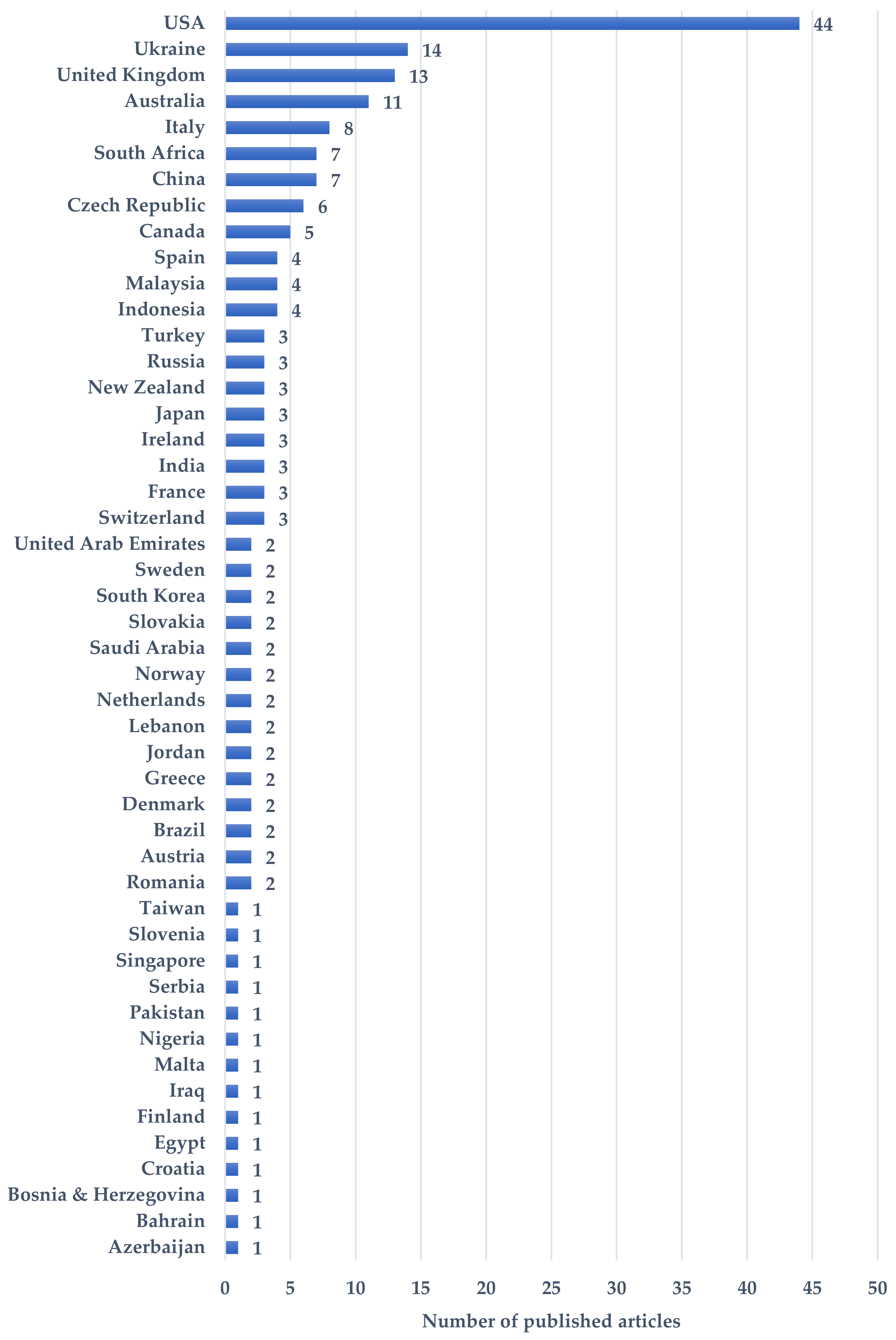

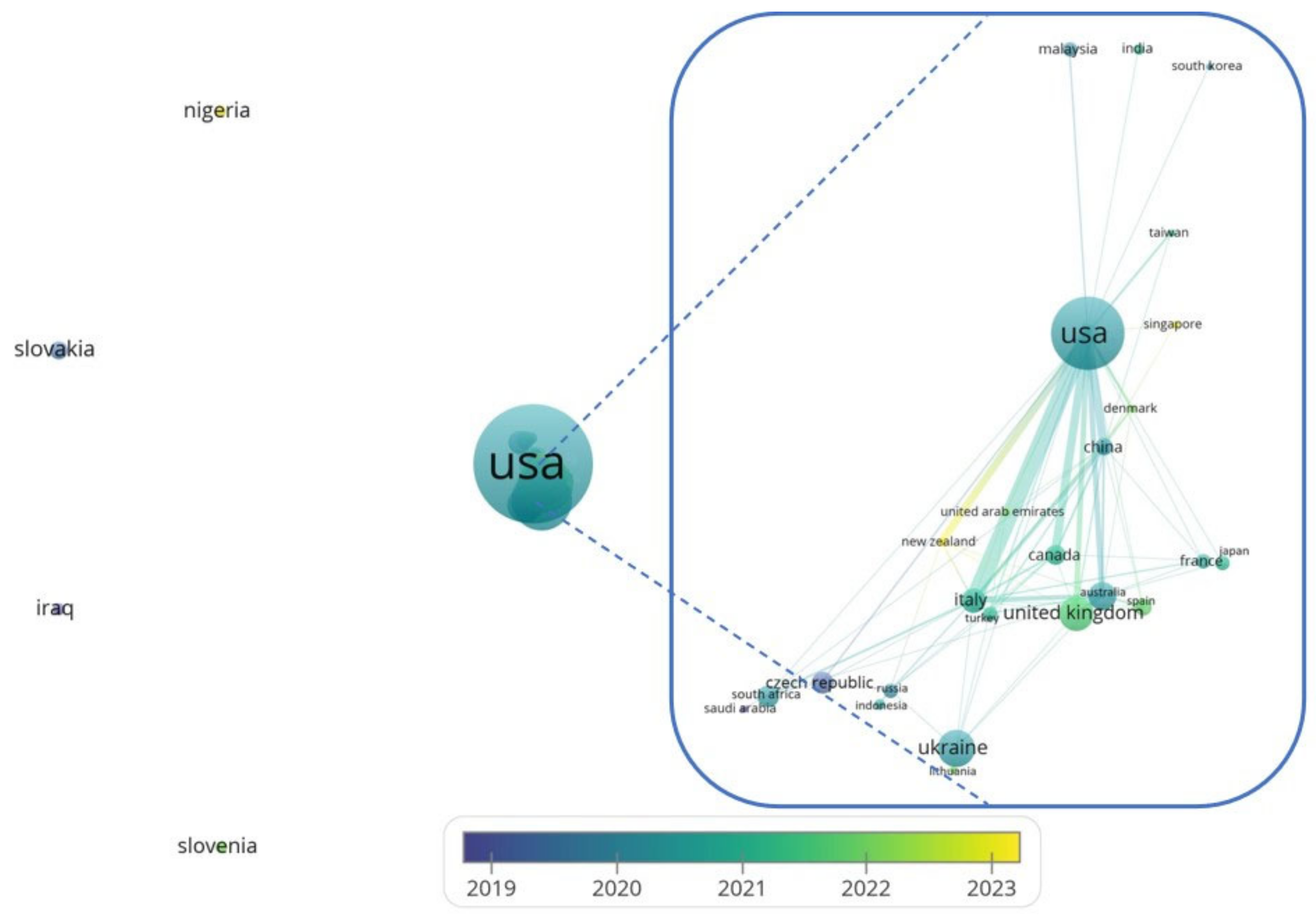

3.3. Countries’ Scientific Production and Citation Analysis

- The first cluster contains the Czech Republic (six articles, 5 total link power), Indonesia (two articles, 2 total link power), Italy (seven documents, 54 total link power), Russia (three documents, 7 total link power), and South Africa (six articles, 8 total link power), which added their contribution to the research topic between 2019 and 2020.

- The second network is formed by a central node, the USA (41 documents, 91 total link power), indicating a significant role in international research; India (2 articles, 1 total link power); Malaysia (3 articles, 2 total link power); and South Korea (1 article, 1 total link power), with articles released around 2020.

- The third cluster shows the interconnection between China (four manuscripts, 34 total link power), Singapore (one document, 2 total link power), and Taiwan (one item, 4 total link power), and it added its contribution recently, between 2021 and 2023.

- The fourth network contains the United Kingdom as a central node because it released 12 documents, with a total link strength of 18. It is followed by Australia (nine articles, 31 total link power) and Spain (four documents, 7 total link power), which contributed between 2021 and 2022.

- The fifth interconnection was created between the United Arab Emirates (UAE) (one article released, 5 total link strength), Canada (five documents, 22 total link power), and Turkey (three documents, 13 total link power), and it added its contribution around the year 2022.

- France (three articles, seven total link power) and Japan (three documents, three total link power) form the sixth couple, being active between 2020 and 2021.

- In the seventh cluster, we note Ukraine (14 articles, seven total link power) and Lithuania (1 article, one total link power), with published articles between 2021 and 2022.

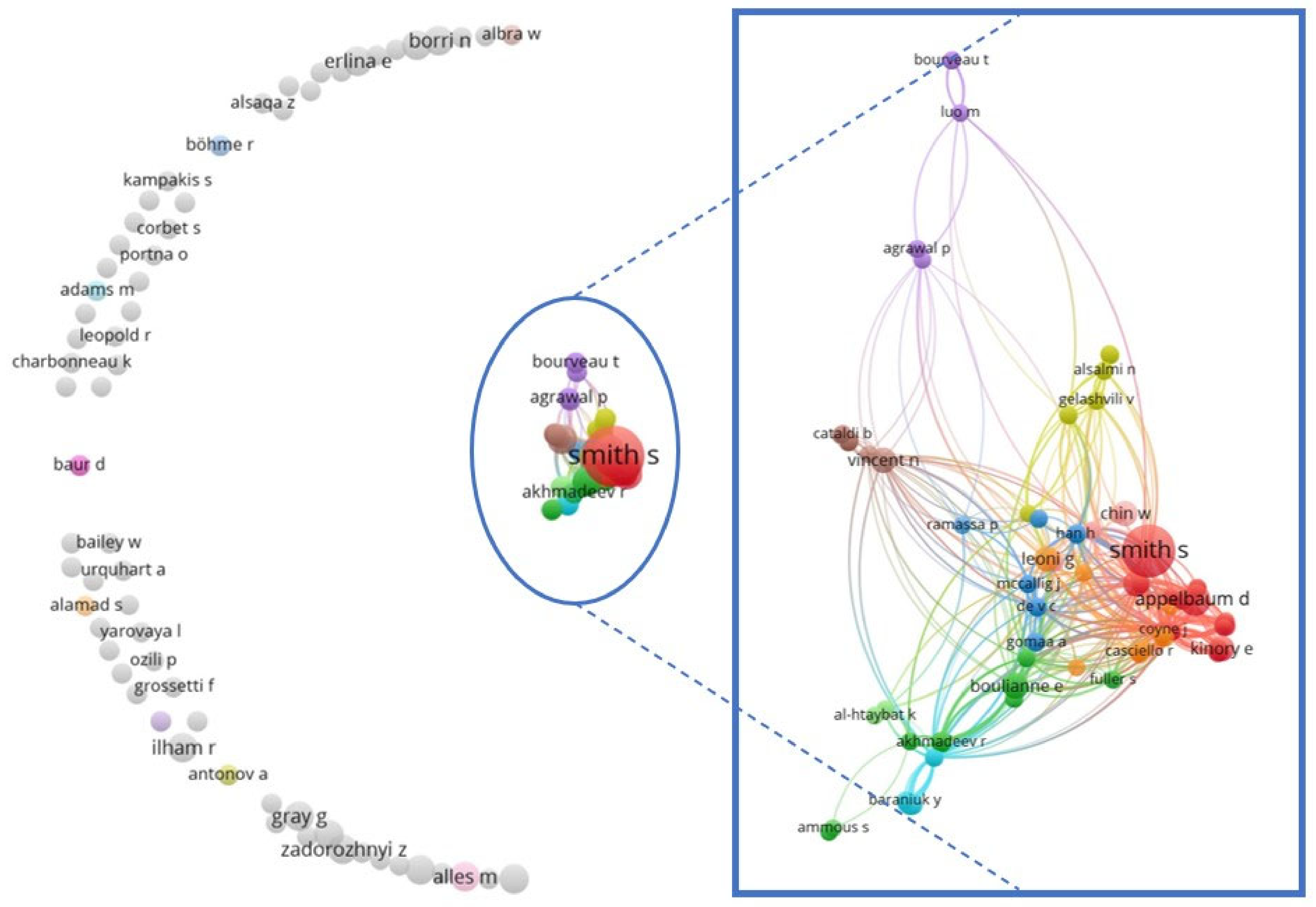

3.4. Author Network and Productivity

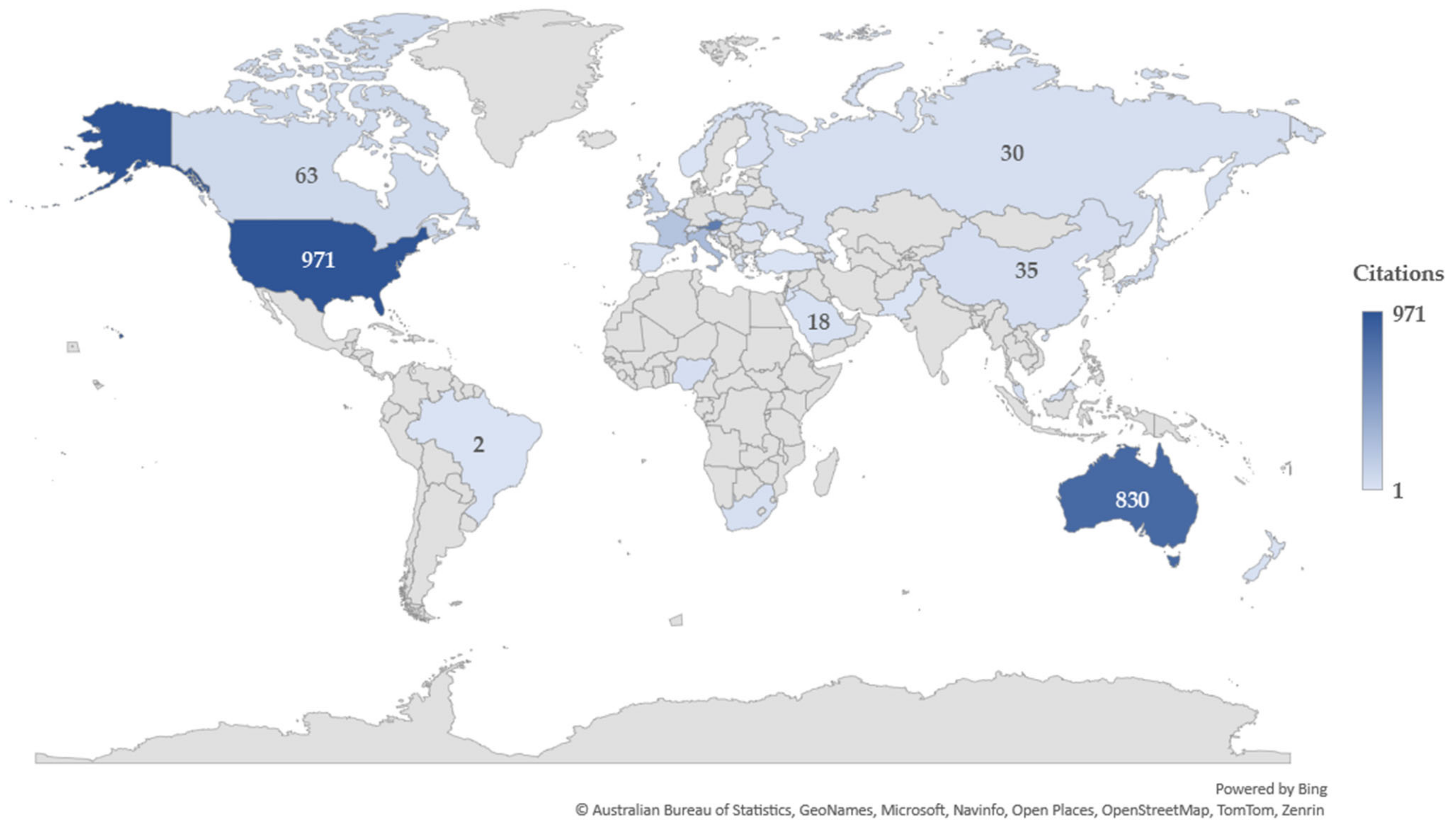

3.5. Citations at Institutions Level

4. Bibliometric Analyses of the Topics Researched

4.1. Keyword Co-Occurrence Analysis

4.2. Thematic Analysis

4.3. Results and Discussion

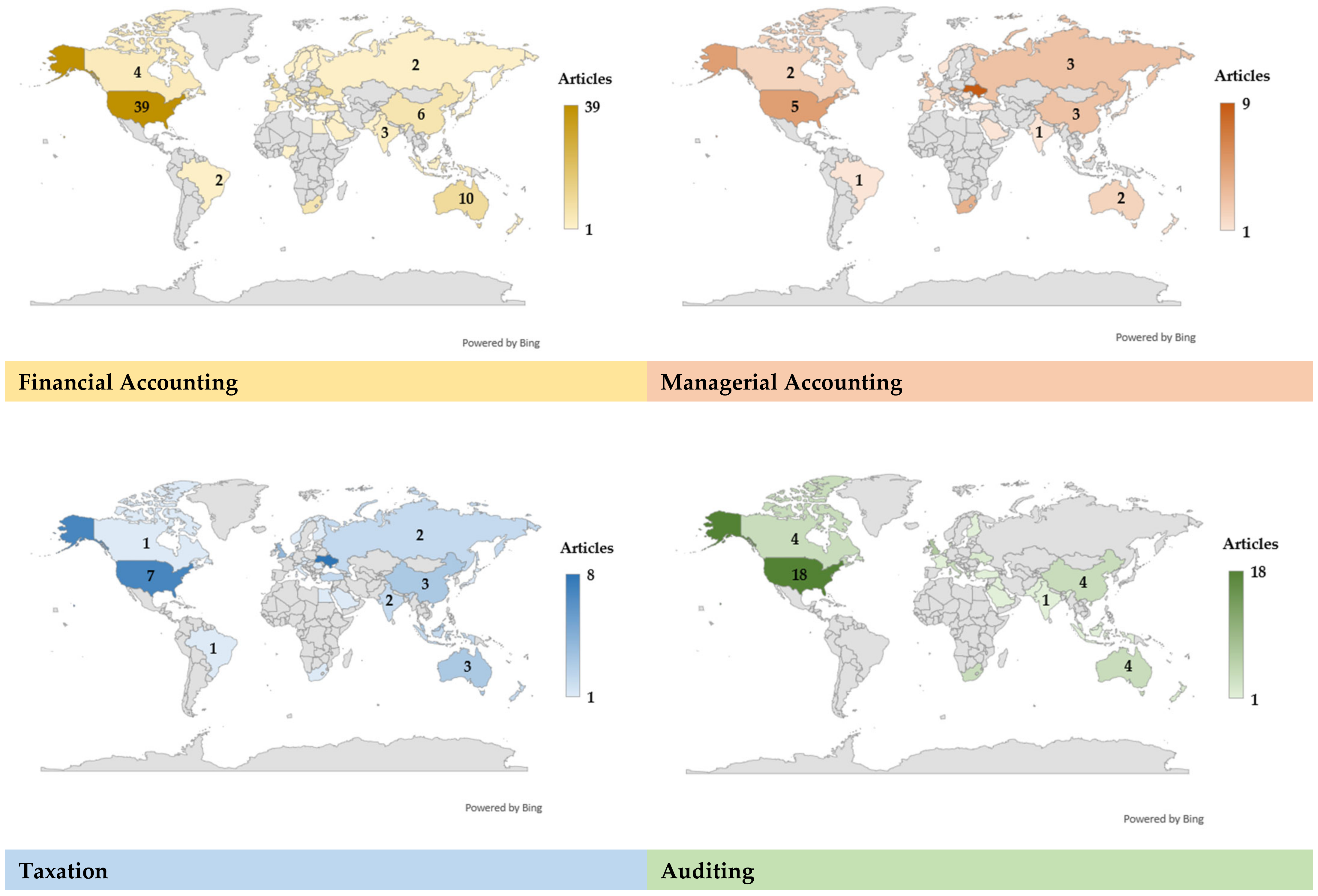

4.3.1. Insights into Financial Accounting Regarding Cryptocurrencies

4.3.2. Insights into Managerial Accounting Regarding Cryptocurrencies

4.3.3. Insights into Taxation of Cryptocurrencies

4.3.4. Insights into Auditing of Cryptocurrencies

5. Conclusions

- How does pseudonymity interact with regulation regarding cryptocurrency holdings?

- How can the financial reporting of cryptocurrencies comply with the existing standards, or can we explore whether new standards are necessary?

- Which valuation approach is more effective for measuring cryptocurrency value over time?

- Which tax regulations would be appropriate for mining, trading, or staking activities with cryptocurrencies?

- The development of audit methodologies designed explicitly for crypto assets.

- The application of blockchain technology and triple-entry accounting in auditing and accounting of crypto assets.

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Abdennadher, Sonia, Rihab Grassa, Hareb Abdulla, and Abdulla Alfalasi. 2022. The Effects of Blockchain Technology on the Accounting and Assurance Profession in the UAE: An Exploratory Study. Journal of Financial Reporting and Accounting 20: 53–71. [Google Scholar] [CrossRef]

- Adams, Mollie T., and William A. Bailey. 2021. Emerging Cryptocurrencies and IRS Summons Power: Striking the Proper Balance between IRS Audit Authority and Taxpayer Privacy. The ATA Journal of Legal Tax Research 19: 61–81. [Google Scholar] [CrossRef]

- Adelowotan, Michael, and Daniel Coetsee. 2021. Blockchain Technology and Implications for Accounting Practice. Academy of Accounting and Financial Studies Journal 25: 1–14. [Google Scholar]

- Alamad, Samir. 2019. Financial and Accounting Principles in Islamic Finance. New York: Springer International Publishing. [Google Scholar] [CrossRef]

- Alhasana, Khaled Ahmad Haroun, and Anas Mohammad Mousa Alrowwad. 2022. National Standards of Accounting and Reporting in the Era of Digitalization of the Economy. Financial and Credit Activity: Problems of Theory and Practice 1: 154–61. [Google Scholar] [CrossRef]

- Al-Htaybat, Khaldoon, Khaled Hutaibat, and Larissa von Alberti-Alhtaybat. 2019. Global Brain-Reflective Accounting Practices Forms of Intellectual Capital Contributing to Value Creation and Sustainable Development. Journal of Intellectual Capital 20: 733–62. [Google Scholar] [CrossRef]

- Alles, Michael, and Glen L. Gray. 2020. What Accountants Need to Know about Blockchain. Information For Efficient Decision Making: Big Data, Blockchain and Relevance 19: 303–23. [Google Scholar] [CrossRef]

- Alles, Michael, and Glen L. Gray. 2023. Hope or Hype? Blockchain and Accounting. International Journal of Digital Accounting Research 23: 19–45. [Google Scholar] [CrossRef] [PubMed]

- Alsalmi, Noora, Subhan Ullah, and Muhammad Rafique. 2023. Accounting for Digital Currencies. Research in International Business and Finance 64: 101897. [Google Scholar] [CrossRef]

- ALSaqa, Zeyad Hashim, Ali Ibrahim Hussein, and Saddam Mohammed Mahmood. 2019. The Impact of Blockchain on Accounting Information Systems. Journal of Information Technology Management 11: 62–80. [Google Scholar] [CrossRef]

- Altukhov, P. L., E. B. Nozhkina, and E. M. Dushevina. 2020. Process Approach to the Creation of Intellectual-Information Management System of Industrial Enterprise Development. In International Scientific Conference. Edited by D. B. Solovev. Amsterdam: Atlantis Press, vol. 128, pp. 1758–65. [Google Scholar]

- Al-Wreikat, Assyad, Adel Almasarwah, and Ola Al-Sheyab. 2023. Blockchain Technology, Cryptocurrencies and Transforming Accounting Fees. International Journal of Electronic Business 19: 95–122. [Google Scholar] [CrossRef]

- Ammous, Saifedean. 2018. Can Cryptocurrencies Fulfil the Functions of Money? Quarterly Review of Economics and Finance 70: 38–51. [Google Scholar] [CrossRef]

- Angeline, Yap Kiew Heong, Wong Siew Chin, Melissa Teoh Teng Tenk, and Zakiah Saleh. 2021. Accounting Treatments for Cryptocurrencies in Malaysia: The Hierarchical Component Model Approach. Asian Journal of Business and Accounting 14: 137–71. [Google Scholar]

- Appelbaum, Deniz, and Robert A. Nehmer. 2020. Auditing Cloud-Based Blockchain Accounting Systems. Journal of Information Systems 34: 5–21. [Google Scholar] [CrossRef]

- Appelbaum, Deniz, Eric Cohen, Ethan Kinory, and Sean Stein Smith. 2022. Impediments to Blockchain Adoption. Journal of Emerging Technologies in Accounting 19: 199–210. [Google Scholar] [CrossRef]

- Aria, Massimo, and Corrado Cuccurullo. 2017. bibliometrix: An R-tool for comprehensive science mapping analysis. Journal of Inometrics 11: 959–75. Available online: https://www.bibliometrix.org/home/ (accessed on 11 May 2024). [CrossRef]

- Atik, Asuman, and Goksal Selahatdin Kelten. 2021. Blockchain Technology and Its Potential Effects on Accounting: A Systematic Literature Review. Istanbul Business Research 50: 495–515. [Google Scholar] [CrossRef]

- Barros, Fernando, Jr., Jefferson Bertolai, and Matheus Carrijo. 2023. Cryptocurrency Is Accounting Coordination: Selfish Mining and Double Spending in a Simple Mining Game? Mathematical Social Sciences 123: 25–50. [Google Scholar] [CrossRef]

- Bauer, Tim D., J. Efrim Boritz, Krista Fiolleau, Bradley Pomeroy, Adam Vitalis, and Pei Wang. 2023. Cataloging the Marketplace of Assurance Services. Auditing: A Journal of Practice & Theory, 1–27. [Google Scholar] [CrossRef]

- Baur, Dirk G., KiHoon Hong, and Adrian D. Lee. 2018. Bitcoin: Medium of Exchange or Speculative Assets? Journal of International Financial Markets Institutions & Money 54: 177–89. [Google Scholar] [CrossRef]

- Beigman, Eyal, Gerard Brennan, Sheng-Feng Hsieh, and Alexander J. Sannella. 2023. Dynamic Principal Market Determination: Fair Value Measurement of Cryptocurrency. Journal of Accounting, Auditing and Finance 38: 731–48. [Google Scholar] [CrossRef]

- Bellucci, Marco, Damiano Cesa Bianchi, and Giacomo Manetti. 2022. Blockchain in Accounting Practice and Research: Systematic Literature Review. Meditari Accountancy Research 30: 121–46. [Google Scholar] [CrossRef]

- Bennett, Sheldon, Ken Charbonneau, Ryan Leopold, Linda Mezon, Carol Paradine, Anthony Scilipoti, and Rebecca Villmann. 2020. Blockchain and Cryptoassets: Insights from Practice*. Accounting Perspectives 19: 283–302. [Google Scholar] [CrossRef]

- Blahušiaková, Miriama. 2022. Accounting for Holdings of Cryptocurrencies in the Slovak Republic: Comparative Analysis. Contemporary Economics 16: 16–31. [Google Scholar] [CrossRef]

- Bondarenko, Olena, Oksana Kichuk, and Andrii Antonov. 2019. The Possibilities of Using Investment Tools Based on Cryptocurrency in the Development of the National Economy. Baltic Journal of Economic Studies 5: 10–17. [Google Scholar] [CrossRef]

- Bonyuet, Derrick. 2020. Overview and Impact of Blockchain on Auditing. International Journal of Digital Accounting Research 20: 31–43. [Google Scholar] [CrossRef] [PubMed]

- Borri, Nicola. 2019. Conditional Tail-Risk in Cryptocurrency Markets. Journal of Empirical Finance 50: 1–19. [Google Scholar] [CrossRef]

- Borri, Nicola, and Kirill Shakhnov. 2022. The Cross-Section of Cryptocurrency Returns. Review of Asset Pricing Studies 12: 667–705. [Google Scholar] [CrossRef]

- Bouri, Elie, Naji Jalkh, Peter Molnar, and David Roubaud. 2017. Bitcoin for Energy Commodities before and after the December 2013 Crash: Diversifier, Hedge or Safe Haven? Applied Economics 49: 5063–73. [Google Scholar] [CrossRef]

- Bourveau, Thomas, Emmanuel T. De George, Atif Ellahie, and Daniele Macciocchi. 2022. The Role of Disclosure and Information Intermediaries in an Unregulated Capital Market: Evidence from Initial Coin Offerings. Journal of Accounting Research 60: 129–67. [Google Scholar] [CrossRef]

- Bozdoğanoğlu, Burçin. 2022. Evaluation of the Effects of Technology Literacy and Digital Financial Literacy on the Investment and Taxation Process in Crypto Assets. In Current Issues and Empirical Studies in Public Finance. Bandirma: Peter Lang AG. Available online: https://www.scopus.com/inward/record.uri?eid=2-s2.0-85138957012&partnerID=40&md5=5eaf96405cfa6b1f821d82dae2bc58e5 (accessed on 10 May 2024).

- Böhme, Rainer, Nicolas Christin, Benjamin Edelman, and Tyler Moore. 2015. Bitcoin: Economics, Technology, and Governance. Journal of Economic Perspectives 29: 213–38. [Google Scholar] [CrossRef]

- Buhussain, Ghadeer, and Allam Hamdan. 2023. Blockchain Technology and Audit Profession. Contributions to Management Science 1640: 715–24. [Google Scholar] [CrossRef] [PubMed]

- Bunget, Ovidiu-Constantin, and Cristian Lungu. 2023. A Bibliometric Analysis of the Implications of Artificial Intelligence on the Accounting Profession. CECCAR Business Review 4: 65–72. [Google Scholar] [CrossRef]

- Bunget, Ovidiu-Constantin, and Georgiana-Iulia Trifa. 2023. Cryptoassets–Perspectives of Accountancy Recognition in the Technological Era. Audit Financiar 21: 526–51. [Google Scholar] [CrossRef]

- Caliskan, Koray. 2020. Data Money: The Socio-Technical Infrastructure of Cryptocurrency Blockchains. Economy And Society 49: 540–61. [Google Scholar] [CrossRef]

- Casey, Michael, and Paul Vigna. 2018. The Truth Machine: The Blockchain and the Future of Everything, 1st ed. New York: HarperCollins. [Google Scholar]

- Cassidy, Julie, Man Hung Alvin Cheng, Toan Le, and Eva Huang. 2020. A Toss of a (Bit)Coin: The Uncertain Nature of the Legal Status of Cryptocurrencies. Journal of Tax Research 17: 168–92. [Google Scholar]

- Chou, Chi-Chun, Nen-Chen Richard Hwang, Gary P. Schneider, Tawei Wang, Chang-Wei Li, and William Wei. 2021. Using Smart Contracts to Establish Decentralized Accounting Contracts: An Example of Revenue Recognition. Journal of Information Systems 35: 17–52. [Google Scholar] [CrossRef]

- Chou, Jun Heng, Prerana Agrawal, and Jacqueline Birt. 2022. Accounting for Crypto-Assets: Stakeholders’ Perceptions. Studies in Economics and Finance 39: 471–89. [Google Scholar] [CrossRef]

- Church, Kimberly Swanson, Sean Stein Smith, and Ethan Kinory. 2021. Accounting Implications of Blockchain: A Hyperledger Composer Use Case for Intangible Assets. Journal of Emerging Technologies in Accounting 18: 23–52. [Google Scholar] [CrossRef]

- Cong, Lin William, Wayne Landsman, Edward Maydew, and Daniel Rabetti. 2023. Tax-Loss Harvesting with Cryptocurrencies. Journal of Accounting and Economics 76: 101607. [Google Scholar] [CrossRef]

- Corbet, Shaen, Andrew Urquhart, and Larisa Yarovaya. 2020. Cryptocurrency and Blockchain Technology. Berlin: De Gruyter. [Google Scholar] [CrossRef]

- Coyne, Joshua G., and Peter L. McMickle. 2017. Can Blockchains Serve an Accounting Purpose? Journal of Emerging Technologies in Accounting 14: 101–11. [Google Scholar] [CrossRef]

- Cyrus, Rocher. 2023. Custody, Provenance, and Reporting of Blockchain and Cryptoassets. In The Emerald Handbook on Cryptoassets: Investment Opportunities and Challenges. Leeds: Emerald Publishing Limited, pp. 233–48. [Google Scholar] [CrossRef]

- Dai, Jun, and Miklos A. Vasarhelyi. 2017. Toward Blockchain-Based Accounting and Assurance. Journal of Information Systems 31: 5–21. [Google Scholar] [CrossRef]

- Dai, Jun, Na He, and Haizong Yu. 2019. Utilizing Blockchain and Smart Contracts to Enable Audit 4.0: From the Perspective of Accountability Audit of Air Pollution Control in China. Journal of Emerging Technologies in Accounting 16: 23–41. [Google Scholar] [CrossRef]

- Davenport, Stephan A., and Spencer C. Usrey. 2023. Crypto Assets: Examining Possible Tax Classifications. Journal of Emerging Technologies in Accounting 20: 55–70. [Google Scholar] [CrossRef]

- Derun, Ivan, and Hanna Mysaka. 2022. Digital Assets in Accounting: The Concept Formation and the Further Development Trajectory. Economic Annals-XXI 195: 59–70. [Google Scholar] [CrossRef]

- Desai, Hrishikesh. 2023. Infusing Blockchain in Accounting Curricula and Practice: Expectations, Challenges, and Strategies. International Journal of Digital Accounting Research 23: 97–135. [Google Scholar] [CrossRef] [PubMed]

- DeVries, Peter D. 2016. An Analysis of Cryptocurrency, Bitcoin, and the Future. International Journal of Business Management and Commerce 1: 1–9. [Google Scholar]

- Dunn, Ryan T., J. Gregory Jenkins, and Mark D. Sheldon. 2021. Bitcoin and Blockchain: Audit Implications of the Killer Bs. Issues in Accounting Education 36: 43–56. [Google Scholar] [CrossRef]

- Dyball, Maria Cadiz, and Ravi Seethamraju. 2022. Client Use of Blockchain Technology: Exploring Its (Potential) Impact on Financial Statement Audits of Australian Accounting Firms. Accounting, Auditing and Accountability Journal 35: 1656–84. [Google Scholar] [CrossRef]

- Fomina, Olena, Olena Moshkovska, Olena Avhustova, Olha Romashko, and Daria Holovina. 2019. Current Aspects of the Cryptocurrency Recognition in Ukraine. Banks and Bank Systems 14: 203–13. [Google Scholar] [CrossRef]

- Fuller, Stephen H., and Ariel Markelevich. 2020. Should Accountants Care about Blockchain? Journal of Corporate Accounting and Finance 31: 34–46. [Google Scholar] [CrossRef]

- Gan, Jingxing, Gerry Tsoukalas, and Serguei Netessine. 2021. Initial Coin Offerings, Speculation, and Asset Tokenization. Management Science 67: 914–31. [Google Scholar] [CrossRef]

- Gao, Xiaoxue. 2023. Digital Transformation in Finance and Its Role in Promoting Financial Transparency. Global Finance Journal 58: 100903. [Google Scholar] [CrossRef]

- Garanina, Tatiana, Mikko Ranta, and John Dumay. 2022. Blockchain in Accounting Research: Current Trends and Emerging Topics. Accounting, Auditing and Accountability Journal 35: 1507–33. [Google Scholar] [CrossRef]

- García-Monleón, Fernando, Anett Erdmann, and Ramón Arilla. 2023. A Value-Based Approach to the Adoption of Cryptocurrencies. Journal of Innovation and Knowledge 8: 1003–42. [Google Scholar] [CrossRef]

- Gietzmann, Miles, and Francesco Grossetti. 2021. Blockchain and Other Distributed Ledger Technologies: Where Is the Accounting? Journal of Accounting and Public Policy 40: 1068–81. [Google Scholar] [CrossRef]

- Gomaa, Ahmed A., Mohamed I. Gomaa, and Ashley Stampone. 2019. A Transaction on the Blockchain: An AIS Perspective, Intro Case to Explain Transactions on the ERP and the Role of the Internal and External Auditor. Journal of Emerging Technologies in Accounting 16: 47–64. [Google Scholar] [CrossRef]

- Gurdgiev, Constantin, and Adam Fleming. 2021. Informational Efficiency and Cybersecurity: Systemic Threats to Blockchain Applications. In Innovations in Social Finance: Transitioning Beyond Economic Value. New York: Palgrave Macmillan. [Google Scholar] [CrossRef]

- Hampl, Filip, and Lucie Gyönyörová. 2021. Can Fiat-Backed Stablecoins Be Considered Cash or Cash Equivalents Under International Financial Reporting Standards Rules? Australian Accounting Review 31: 233–55. [Google Scholar] [CrossRef]

- Handoko, Bambang Leo, Bryan Aurelio Gunawan, and Muhammad Fikri Permana Djati. 2022. Importance of Blockchain within The Big 4 CPA Firms: Cryptocurrency’s Existence. West Jakarta: Association for Computing Machinery, pp. 190–96. [Google Scholar] [CrossRef]

- Han, Hongdan, Radha K. Shiwakoti, Robin Jarvis, Chima Mordi, and David Botchie. 2023. Accounting and Auditing with Blockchain Technology and Artificial Intelligence: A Literature Review. International Journal of Accounting Information Systems 48: 100598. [Google Scholar] [CrossRef]

- Harrast, Steven A., Debra McGilsky, and Yan Sun. 2022. Determining the Inherent Risks of Cryptocurrency: A Survey Analysis. Current Issues in Auditing 16: A10–A17. [Google Scholar] [CrossRef]

- Hazar, Hulya Boydas. 2020. Anonymity in Cryptocurrencies. Eurasian Studies in Business and Economics 14: 171–78. [Google Scholar] [CrossRef] [PubMed]

- Holub, Mark, and Jackie Johnson. 2018. Bitcoin Research across Disciplines. Information Society 34: 114–26. [Google Scholar] [CrossRef]

- Huang, Robin Hui, Hui Deng, and Aiden Foon Lok Chan. 2023. The Legal Nature of Cryptocurrency as Property: Accounting and Taxation Implications. Computer Law and Security Review 51: 1058–60. [Google Scholar] [CrossRef]

- Hubbard, Benjamin. 2023. Decrypting Crypto: Implications of Potential Financial Accounting Treatments of Cryptocurrency. Accounting Research Journal 36: 369–83. [Google Scholar] [CrossRef]

- IFRS Foundation. 2019. Holding of Cryptocurrencies. Available online: https://www.ifrs.org/content/dam/ifrs/meetings/2019/june/ifric/ap12-holdings-of-cryptocurrencies.pdf (accessed on 11 May 2024).

- IFRS Foundation. 2024. IAS 2 Inventories. Available online: https://www.ifrs.org/issued-standards/list-of-standards/ias-2-inventories/ (accessed on 11 May 2024).

- IFRS Foundation. 2024. IAS 7 Statement of Cash Flows. Available online: https://www.ifrs.org/issued-standards/list-of-standards/ias-7-statement-of-cash-flows/ (accessed on 11 May 2024).

- IFRS Foundation. 2024. IAS 16 Property, Plant and Equipment. Available online: https://www.ifrs.org/issued-standards/list-of-standards/ias-16-property-plant-and-equipment/ (accessed on 11 May 2024).

- IFRS Foundation. 2024. IAS 21 The Effects of Changes in Foreign Exchange Rates. Available online: https://www.ifrs.org/issued-standards/list-of-standards/ias-21-the-effects-of-changes-in-foreign-exchange-rates/ (accessed on 11 May 2024).

- IFRS Foundation. 2024. IAS 32 Financial Instruments: Presentation. Available online: https://www.ifrs.org/issued-standards/list-of-standards/ias-32-financial-instruments-presentation/ (accessed on 11 May 2024).

- IFRS Foundation. 2024. IAS 38 Intangible Assets. Available online: https://www.ifrs.org/issued-standards/list-of-standards/ias-38-intangible-assets/ (accessed on 11 May 2024).

- IFRS Foundation. 2024. IAS 39 Financial Instruments: Recognition and Measurement. Available online: https://www.ifrs.org/issued-standards/list-of-standards/ias-39-financial-instruments-recognition-and-measurement/ (accessed on 11 May 2024).

- IFRS Foundation. 2024. IAS 40 Investment Property. Available online: https://www.ifrs.org/issued-standards/list-of-standards/ias-40-investment-property/ (accessed on 11 May 2024).

- IFRS Foundation. 2024. IFRS 9 Financial Instruments. Available online: https://www.ifrs.org/issued-standards/list-of-standards/ifrs-9-financial-instruments/ (accessed on 11 May 2024).

- IFRS Foundation. 2024. IFRS 13 Fair Value Measurement. Available online: https://www.ifrs.org/issued-standards/list-of-standards/ifrs-13-fair-value-measurement/ (accessed on 11 May 2024).

- Ilham, Rico Nur, Khairah Amalia Fachrudin Erlina, Amlys Syahputra Silalahi, and Jumadil Saputra. 2019a. Comparative of the Supply Chain and Block Chains to Increase the Country Revenues via Virtual Tax Transactions and Replacing Future of Money. International Journal of Supply Chain Management 8: 1066. [Google Scholar]

- Ilham, Rico Nur, Khairah Amalia Fachrudin Erlina, Amlys Syahputra Silalahi, Jumadil Saputra, and Wahyuddin Albra. 2019b. Investigation of the Bitcoin Effects on the Country Revenues via Virtual Tax Transactions for Purchasing Management. International Journal of Supply Chain Management 8: 737. [Google Scholar]

- Jackson, Andrew B., and Steven Luu. 2023. Accounting For Digital Assets. Australian Accounting Review 33: 302–12. [Google Scholar] [CrossRef]

- Jayasuriya, D. Dulani, and Alexandra Sims. 2023. From the Abacus to Enterprise Resource Planning: Is Blockchain the Next Big Accounting Tool? Accounting Auditing & Accountability Journal 36: 24–62. [Google Scholar] [CrossRef]

- Jumde, Avaneesh, and Boo Yun Cho. 2020. Can Cryptocurrencies Overtake the Fiat Money? International Journal of Business Performance Management 21: 6–20. [Google Scholar] [CrossRef]

- Juškaitė, Lina, and Laura Gudelytė-Žilinskienė. 2022. Investigation of the Feasibility of Including Different Cryptocurrencies in the Investment Portfolio for its Diversification. Business, Management and Economics Engineering 20: 172–88. [Google Scholar] [CrossRef]

- Kaden, Stacey R., Jeff W. Lingwall, and Trevor T. Shonhiwa. 2021. Teaching Blockchain through Coding: Educating the Future Accounting Professional. Issues in Accounting Education 36: 281–90. [Google Scholar] [CrossRef]

- Kampakis, Stylianos. 2022. Auditing Tokenomics: A Case Study and Lessons from Auditing a Stablecoin Project. Journal of the British Blockchain Association 5: 1–7. [Google Scholar] [CrossRef] [PubMed]

- Klopper, Nicolette, and Sophia Magaretha Brink. 2023. Determining the Appropriate Accounting Treatment of Cryptocurrencies Based on Accounting Theory. Journal of Risk and Financial Management 16: 379. [Google Scholar] [CrossRef]

- Kochergin, Dmitrii A. 2020. Economic Nature and Classification of Stablecoins. Finance: Theory and Practice 24: 140–60. [Google Scholar] [CrossRef]

- Koker, Thomas E., and Dimitrios Koutmos. 2020. Cryptocurrency Trading Using Machine Learning. Journal of Risk and Financial Management 13: 178. [Google Scholar] [CrossRef]

- Kokina, Julia, Ruben Mancha, and Dessislava Pachamanova. 2017. Blockchain: Emergent Industry Adoption and Implications for Accounting. Journal of Emerging Technologies in Accounting 14: 91–100. [Google Scholar] [CrossRef]

- Kolková, Andrea. 2018. The Use of Cryptocurrency in Enterprises in Czech Republic. Edited by O. Dvoulety, M. Lukes and J. Misar. Ostrava: Vysoká škola ekonomická v Praze, pp. 541–52. [Google Scholar]

- Kontozis, Nikolas. 2019. VAT Treatment of Cryptocurrencies. PwC. Available online: https://www.pwc.com.cy/en/press-room/articles-2019/vat-treatment-of-cryptocurrencies.html (accessed on 10 May 2024).

- Lazea, Georgiana-Iulia, Ovidiu-Constantin Bunget, and Anca Diana Sumănaru. 2023. “Comparative Analysis of Cryptocurrencies Versus Fiat Money”. The Annals of the University of Oradea. Economic Sciences 32: 111–20. [Google Scholar] [CrossRef]

- Lee, Lorraine S., Deniz Appelbaum, and Richard D. Mautz III. 2022. Blockchains: An Experiential Accounting Learning Activity. Journal of Emerging Technologies in Accounting 19: 181–97. [Google Scholar] [CrossRef]

- Lombardi, Rosa, Charl de Villiers, Nicola Moscariello, and Michele Pizzo. 2022. The Disruption of Blockchain in Auditing—A Systematic Literature Review and an Agenda for Future Research. Accounting, Auditing and Accountability Journal 35: 1534–65. [Google Scholar] [CrossRef]

- Luo, Mei, and Shuangchen Yu. 2022. Financial Reporting for Cryptocurrency. Review of Accounting Studies 29: 1707–40. [Google Scholar] [CrossRef]

- Maffei, Marco, Raffaela Casciello, and Fiorenza Meucci. 2021. Blockchain Technology: Uninvestigated Issues Emerging from an Integrated View within Accounting and Auditing Practices. Journal of Organizational Change Management 34: 462–76. [Google Scholar] [CrossRef]

- Makurin, Andrii. 2023. Technological Aspects and Environmental Consequences of Mining Encryption. Economics Ecology Socium 7: 61–70. [Google Scholar] [CrossRef]

- Makurin, Andrii, Andrii Maliienko, Olena Tryfonova, and Lyudmyla Masina. 2023. Management of Cryptocurrency Transactions from Accounting Aspects. Economics Ecology Socium 7: 26–35. [Google Scholar] [CrossRef]

- Matusky, Tomas. 2017. Accounting of Cryptocurrencies. Paper presented at EDAMBA 2017: Conference Proceedings: Knowledge and Skills for Sustainable Development: The Role of Economics, Business, Management and Related Disciplines: [20th] International Scientific Conference for Doctoral Students and Post-Doctoral Scholars, Bratislava, Slovakia, April 4–6; pp. 313–21. [Google Scholar]

- McCallig, John, Alastair Robb, and Fiona Rohde. 2019. Establishing the Representational Faithfulness of Financial Accounting Information Using Multiparty Security, Network Analysis and a Blockchain. International Journal of Accounting Information Systems 33: 47–58. [Google Scholar] [CrossRef]

- McGuigan, Nicholas, Alessandro Ghio, and Thomas Kern. 2021. Designing Accounting Futures: Exploring Ambiguity in Accounting Classrooms through Design Futuring. Issues in Accounting Education 36: 325–51. [Google Scholar] [CrossRef]

- Morozova, Tatiana, Ravil Akhmadeev, Liubov Lehoux, Alexei Yumashev, Galina Meshkova, and Marina Lukiyanova. 2020. Crypto Asset Assessment Models in Financial Reporting Content Typologies. Entrepreneurship and Sustainability Issues 7: 2196–212. [Google Scholar] [CrossRef]

- Mosteanu, Narcisa Roxana, and Alessio Faccia. 2020. Digital Systems and New Challenges of Financial Management—FinTech, XBRL, Blockchain and Cryptocurrencies. Quality-Access to Success 21: 159–66. [Google Scholar]

- Munteanu, Ionela, Kamer-Ainur Aivaz, Adrian Micu, Alexandru Capatana, and Valentin Jakubowicz. 2023. Digital Transformations Imprint Financial Challenges: Accounting Assessment of Crypto Assets and Building Resilience in Emerging Innovative Businesses. Economic Computation and Economic Cybernetics Studies and Research 57: 1–18. [Google Scholar]

- Nakamoto, Satoshi. 2009. Bitcoin: A Peer-to-Peer Electronic Cash System. Available online: https://bitcoin.org/bitcoin.pdf (accessed on 11 May 2024).

- Niftaliyev, Sultan Gurban. 2023. Problems Arising in the Accounting of Cryptocurrencies. Financial and Credit Activity: Problems of Theory and Practice 3: 76–86. [Google Scholar] [CrossRef]

- Ntanos, Stamatios, Sofia Asonitou, Dimitrios Karydas, and Grigorios Kyriakopoulos. 2020. Blockchain Technology: A Case Study from Greek Accountants. In Springer Proceedings in Business and Economics. Edited by A. Kavoura, E. Kefallonitis and P. Theodoridis. Cham: Springer. [Google Scholar] [CrossRef]

- Nylen, Paul C., and Brian W. Huels. 2022. Using Unrelated IRS Guidance as a Framework for Taxing Crypto Transactions: Revenue Procedure 2019–18. The ATA Journal of Legal Tax Research 20: 30–46. [Google Scholar] [CrossRef]

- Obu, Osiebuni Collins, and Wilfred I. Ukpere. 2022. The Implications of the Incursion of Cryptocurrency on the Effectiveness of Fiscal Policy. Review of Applied Socio-Economic Research 23: 134–50. [Google Scholar] [CrossRef]

- O’Leary, Daniel E. 2018. Open Information Enterprise Transactions: Business Intelligence and Wash and Spoof Transactions in Blockchain and Social Commerce. Intelligent Systems in Accounting, Finance and Management 25: 148–58. [Google Scholar] [CrossRef]

- Ozeran, Alla, and Nadiia Gura. 2020. Audit and Accounting Considerations on Cryptoassets and Related Transactions. Economic Annals-XXI 184: 124–32. [Google Scholar] [CrossRef]

- Ozili, Peterson K. 2023. CBDC, Fintech and Cryptocurrency for Financial Inclusion and Financial Stability. Digital Policy, Regulation and Governance 25: 40–57. [Google Scholar] [CrossRef]

- Pandey, Durgesh, and Paul Gilmour. 2024. Accounting Meets Metaverse: Navigating the Intersection between the Real and Virtual Worlds. Journal of Financial Reporting and Accounting 22: 211–26. [Google Scholar] [CrossRef]

- Pan, Liuxuan, Owen Vaughan, and Craig Steven Wright. 2023. A Private and Efficient Triple-Entry Accounting Protocol on Bitcoin. Journal of Risk and Financial Management 16: 400. [Google Scholar] [CrossRef]

- Pantielieieva, N. M., N. V. Rogova, S. M. Braichenko, S. V. Dzholos, and A. S. Kolisnyk. 2019. Current Aspects of Transformation of Economic Relations: Cryptocurrencies and Their Legal Regulation. Financial and Credit Activity-Problems of Theory and Practice 4: 410–18. [Google Scholar] [CrossRef]

- Papp, Anna, Douglas Almond, and Shuang Zhang. 2023. Bitcoin and Carbon Dioxide Emissions: Evidence from Daily Production Decisions. Journal of Public Economics 227: 105003. [Google Scholar] [CrossRef]

- Parrondo, Luz. 2020. DLT-Based Tokens Classification towards Accounting Regulation. In FEMIB—Proceedings International Conference on Finance, Economics, Management and IT Business. Edited by P. Baudier, M. Arami and V. Chang. Setúbal: SciTePress, pp. 15–26. Available online: https://www.scopus.com/inward/record.uri?eid=2-s2.0-85088368491&partnerID=40&md5=8079373cce7b9633805456da0502ee83 (accessed on 11 May 2024).

- Parrondo, Luz. 2023. Cryptoassets: Definitions and Accounting Treatment under the Current International Financial Reporting Standards Framework. Intelligent Systems in Accounting, Finance and Management 30: 208–27. [Google Scholar] [CrossRef]

- Păunescu, Mirela. 2018. The Accountant’s Headache: Accounting for Virtual Currencies Transactions. București: Bucharest University of Economic Studies, pp. 145–59. [Google Scholar]

- Pedreño, Eladio Pascual, Vera Gelashvili, and Laura Pascual Nebreda. 2021. Blockchain and Its Application to Accounting. Intangible Capital 17: 1–16. [Google Scholar] [CrossRef]

- Pelucio-Grecco, Marta Cristina, Jacinto Pedro dos Santos Neto, and Diego Constancio. 2020. Accounting for Bitcoins in Light of IFRS and Tax Aspects. Revista Contabilidade e Financas 31: 275–82. [Google Scholar] [CrossRef]

- Peters, Gareth William, Efstathios Panayi, and Ariane Chapelle. 2015. Trends in Crypto-Currencies and Blockchain Technologies: A Monetary Theory and Regulation Perspective. SSRN Electronic Journal. [Google Scholar] [CrossRef]

- Pflueger, Dane, Martin Kornberger, and Jan Mouritsen. 2022. What Is Blockchain Accounting? A Critical Examination in Relation to Organizing, Governance, and Trust. European Accounting Review, 1–26. [Google Scholar] [CrossRef]

- Pieters, Gina, and Sofia Vivanco. 2017. Financial Regulations and Price Inconsistencies across Bitcoin Markets. Information Economics and Policy 39: 1–14. [Google Scholar] [CrossRef]

- Pimentel, Erica, and Emilio Boulianne. 2020. Blockchain in Accounting Research and Practice: Current Trends and Future Opportunities. Accounting Perspectives 19: 325–61. [Google Scholar] [CrossRef]

- Pimentel, Erica, Emilio Boulianne, Shayan Eskandari, and Jeremy Clark. 2021. Systemizing the Challenges of Auditing Blockchain-Based Assets. Journal of Information Systems 35: 61–75. [Google Scholar] [CrossRef]

- Procházka, David. 2018. Accounting for Bitcoin and Other Cryptocurrencies under IFRS: A Comparison and Assessment of Competing Models. International Journal of Digital Accounting Research 18: 161–88. [Google Scholar] [CrossRef] [PubMed]

- Procházka, David. 2019. Is Bitcoin a Currency or an Investment? An IFRS View. In Springer Proceedings in Business and Economics. Edited by David Procházka. Dordrecht and Cham: Springer, pp. 217–26. [Google Scholar] [CrossRef]

- Proelss, Juliane, Denis Schweizer, and Stephane Sevigny. 2023. Is Bitcoin ESG-Compliant? A Sober Look. European Financial Management 30: 680–726. [Google Scholar] [CrossRef]

- Raiborn, Cecily, and Marcos Sivitanides. 2015. Accounting Issues Related to Bitcoins. Journal of Corporate Accounting and Finance 26: 25–34. [Google Scholar] [CrossRef]

- Ram, Asheer, Warren Maroun, and Robert Garnett. 2016. Accounting for the Bitcoin: Accountability, Neoliberalism and a Correspondence Analysis. Meditari Accountancy Research 24: 2–35. [Google Scholar] [CrossRef]

- Ramassa, Paola, and Giulia Leoni. 2022. Standard Setting in Times of Technological Change: Accounting for Cryptocurrency Holdings. Accounting, Auditing and Accountability Journal 35: 1598–624. [Google Scholar] [CrossRef]

- Rana, Tarek, Jan Svanberg, Peter Öhman, and Alan Lowe. 2023. Introduction: Analytics in Accounting and Auditing. In Handbook of Big Data and Analytics in Accounting and Auditing. Singapore: Springer, pp. 1–13. [Google Scholar] [CrossRef]

- Reepu. 2019. Blockchain: Social Innovation in Finance & Accounting. International Journal of Management 10: 14–18. [Google Scholar] [CrossRef] [PubMed]

- Rella, Ludovico. 2020. Steps towards an Ecology of Money Infrastructures: Materiality and Cultures of Ripple. Journal of Cultural Economy 13: 236–49. [Google Scholar] [CrossRef]

- Salawu, Mary Kehinde, and Tankiso Moloi. 2018. Benefits of Legislating Cryptocurrencies: Perception of Nigerian Professional Accountants. Academy of Accounting and Financial Studies Journal 22: 1–17. Available online: https://www.scopus.com/inward/record.uri?eid=2-s2.0-85061856468&partnerID=40&md5=c82546d028992b4ce7a1f44284df2182 (accessed on 11 May 2024).

- Sarwar, Muhammad Imran, Kashif Nisar, Imran Khan, and Danish Shehzad. 2023. Blockchains and Triple-Entry Accounting for B2B Business Models. Ledger 8: 37–57. [Google Scholar] [CrossRef]

- Schmitz, Jana, and Giulia Leoni. 2019. Accounting and Auditing at the Time of Blockchain Technology: A Research Agenda. Australian Accounting Review 29: 331–42. [Google Scholar] [CrossRef]

- Sethibe, Tebogo, and Sibusiso Malinga. 2021. Blockchain Technology Innovation: An Investigation of the Accounting and Auditing Use-Cases. In European Conference on Innovation and Entrepreneurship. Edited by Florinda Matos, Maria de Fátima Ferreiro, Isabel Salavisa and Álvaro Rosa. Reading and New York: Academic Conferences International Limited, pp. 892–900. [Google Scholar] [CrossRef]

- Sheldon, Mark D. 2023. Preparing Auditors to Evaluate Blockchains Used to Track Tangible Assets. Current Issues in Auditing 20: 1–22. [Google Scholar] [CrossRef]

- Shvayko, M. L., and N. O. Grebeniuk. 2020. Current Crediting Instruments Influencing Investment Climate in Ukraine. Financial and Credit Activity-Problems of Theory and Practice 1: 414–23. [Google Scholar] [CrossRef]

- Smith, Sean Stein. 2018. Implications of Next Step Blockchain Applications for Accounting and Legal Practitioners: A Case Study. Australasian Accounting, Business and Finance Journal 12: 77–90. [Google Scholar] [CrossRef]

- Smith, Sean Stein. 2021a. Crypto Accounting Valuation, Reporting, and Disclosure. In The Emerald Handbook of Blockchain for Business. Leeds: Emerald Publishing Limited. [Google Scholar] [CrossRef]

- Smith, Sean Stein. 2021b. Decentralized Finance & Accounting—Implications, Considerations, and Opportunities for Development. International Journal of Digital Accounting Research 21: 129–53. [Google Scholar] [CrossRef] [PubMed]

- Smith, Sean Stein. 2023. The Cryptoasset Auditing and Accounting Landscape. In The Emerald Handbook on Cryptoassets: Investment Opportunities and Challenges. Leeds: Emerald Publishing Limited. [Google Scholar] [CrossRef]

- Smith, Sean Stein, and John Jack Castonguay. 2020. Blockchain and Accounting Governance: Emerging Issues and Considerations for Accounting and Assurance Professionals. Journal of Emerging Technologies in Accounting 17: 119–31. [Google Scholar] [CrossRef]

- Smith, Sean Stein, Rossen Petkov, and Richard Lahijani. 2019. Blockchain and Cryptocurrencies—Considerations for Treatment and Reporting for Financial Services Professionals. International Journal of Digital Accounting Research 19: 59–78. [Google Scholar] [CrossRef] [PubMed]

- Soepriyanto, Gatot, Shinta Amalina Hazrati Havidz, and Rangga Handika. 2023. Crypto Goes East: Analyzing Bitcoin, Technological and Regulatory Contagions in Asia–Pacific Financial Markets Using Asset Pricing. International Journal of Emerging Markets. Published electronically December 5. [Google Scholar] [CrossRef]

- Sokolenko, Liudmyla, Tetiana Ostapenko, Olga Kubetska, Oksana Portna, and Thuy Tran. 2019. Cryptocurrency: Economic Essence and Features of Accounting. Academy of Accounting and Financial Studies Journal 23. Available online: https://www.scopus.com/inward/record.uri?eid=2-s2.0-85071699405&partnerID=40&md5=aae414a62836e6bbf8b4416444e8d6be (accessed on 11 May 2024).

- Stern, Myles, and Alan Reinstein. 2021. A Blockchain Course for Accounting and Other Business Students. Journal of Accounting Education 56: 100742. [Google Scholar] [CrossRef]

- Stratopoulos, Theophanis C. 2020. Teaching Blockchain to Accounting Students. Journal of Emerging Technologies in Accounting 17: 63–74. [Google Scholar] [CrossRef]

- Tapscott, Don, and Alex Tapscott. 2016. Blockchain Revolution: How the Technology behind Bitcoin Is Changing Money, Business, and the World, International ed. New York: Penguin. [Google Scholar]

- Terando, William D., Bryan Cataldi, and Brian E. Mennecke. 2017. Impact of the IRC Section 475 Mark-to-Market Election on Bitcoin Taxation. ATA Journal of Legal Tax Research 15: 66–76. [Google Scholar] [CrossRef]

- Tiron-Tudor, Adriana, Stefania Mierlita, and Francesca Manes Rossi. 2024. Exploring the Uncharted Territories: A Structured Literature Review on Cryptocurrency Accounting and Auditing. The Journal of Risk Finance 25: 253–76. [Google Scholar] [CrossRef]

- Tsujimura, Kazusuke, and Masako Tsujimura. 2019. Flow of Funds Analysis: A Combination of Roman Law, Accounting and Economics. Statistical Journal of the IAOS 35: 691–702. [Google Scholar] [CrossRef]

- Tzagkarakis, George, and Frantz Maurer. 2023. Horizon-Adaptive Extreme Risk Quantification for Cryptocurrency Assets. Computational Economics 62: 1251–86. [Google Scholar] [CrossRef]

- van Eck, Nees Jan, and Ludo Waltman. 2023. VOSviewer Manual. Available online: https://www.vosviewer.com/documentation/Manual_VOSviewer_1.6.20.pdf (accessed on 10 May 2024).

- Vasicek, Davor, Veljko Dmitrovic, and Josip Cicak. 2019. Accounting of Cryptocurrencies under IFRS. Edited by M. L. Simic and B. Crnkovic. Rijeka: University of Rijeka, pp. 550–63. [Google Scholar]

- Vedapradha, R., and Hariharan Ravi. 2023. Blockchain: An EOM Approach to Reconciliation in Banking. Innovation & Management Review 20: 17–27. [Google Scholar] [CrossRef]

- Veuger, Jan. 2021. Digitization and Blockchain in Finance, The Netherlands in 2020 and 2021. International Journal of Applied Economics, Finance and Accounting 11: 1–22. [Google Scholar] [CrossRef]

- Vičič, Jernej, and Aleksandar Tošić. 2022. Application of Benford’s Law on Cryptocurrencies. Journal of Theoretical and Applied Electronic Commerce Research 17: 313–26. [Google Scholar] [CrossRef]

- Vigna, Paul, and Michael J. Casey. 2015. The Age of Cryptocurrency: How Bitcoin and the Block-Chain Are Challenging the Global Economic Order. New York: Macmillan. [Google Scholar]

- Vincent, Nishani Edirisinghe, and Anne M. Wilkins. 2020. Challenges When Auditing Cryptocurrencies. Current Issues in Auditing 14: A46–58. [Google Scholar] [CrossRef]

- Vincent, Nishani Edirisinghe, and Stephan A. Davenport. 2022. Accounting Research Opportunities for Cryptocurrencies. Journal of Emerging Technologies in Accounting 19: 79–93. [Google Scholar] [CrossRef]

- Vodáková, Jana, and Jiri Foltyn. 2020a. Financial Reporting of Cryptocurrencies. Edited by K. S. Soliman. New York: Springer, pp. 12325–30. [Google Scholar]

- Vodáková, Jana, and Jiri Foltyn. 2020b. Valuation of Cryptocurrencies in Selected EU Countries. Edited by K. S. Soliman. New York: Springer, pp. 15529–34. [Google Scholar]

- Volosovych, Svitlana, and Yurii Baraniuk. 2018. Tax Control of Cryptocurrency Transactions in Ukraine. Banks and Bank Systems 13: 89–106. [Google Scholar] [CrossRef] [PubMed]

- Vumazonke, Namhla, and Shaun Parsons. 2023. An Analysis of South Africa’s Guidance on the Income Tax Consequences of Crypto Assets. South African Journal of Economic and Management Sciences 26: 11. [Google Scholar] [CrossRef]

- Yang, Lu, and Shigeyuki Hamori. 2021. The Role of the Carbon Market in Relation to the Cryptocurrency Market: Only Diversification or More? International Review of Financial Analysis 77: 101864. [Google Scholar] [CrossRef]

- Yan, Huqin, Kejia Yan, and Rakesh Gupta. 2022. A Survey of the Accounting Industry on Holdings of Cryptocurrencies in Xiamen City, China. Journal of Risk and Financial Management 15: 175. [Google Scholar] [CrossRef]

- Yatsyk, Tetiana, and Viktor Shvets. 2020. Cryptoassets as an Emerging Class of Digital Assets in the Financial Accounting. Economic Annals-XXI 183: 106–15. [Google Scholar] [CrossRef]

- Yee, Teh Sin, Angeline Yap Kiew Heong, and Wong Siew Chin. 2020. Accounting Treatment of Cryptocurrency: A Malaysian Context. Management and Accounting Review 19: 119–49. [Google Scholar]

- Yu, Ting, Zhiwei Lin, and Qingliang Tang. 2018. Blockchain: The Introduction and Its Application in Financial Accounting. Journal of Corporate Accounting and Finance 29: 37–47. [Google Scholar] [CrossRef]

- Zadorozhnyi, Zenovii-Mykhaylo, Volodymyr Muravskyi, and O. A. Shevchuk. 2018. Management Accounting of Electronic Transactions with the Use of Cryptocurrencies. Financial and Credit Activity-Problems of Theory and Practice 3: 169–77. [Google Scholar] [CrossRef]

- Zadorozhnyi, Zenovii-Mykhaylo, Volodymyr Muravskyi, Mariia Humenna-Derij, and Nataliia Zarudna. 2022. Innovative Accounting and Audit of the Metaverse Resources. Marketing and Management of Innovations 13: 10–19. [Google Scholar] [CrossRef]

- Zakaria, Hesham. 2022. The Role of International Tax Accounting in Assessing Digital and Virtual Tax Issues. In Accounting, Finance, Sustainability, Governance and Fraud. Singapore: Springer. [Google Scholar] [CrossRef]

- Zelic, Dragan, and Nenad Baros. 2018. Cryptocurrency: General Challenges of Legal Regulation and the Swiss Model of Regulation. In Economic and Social Development (Esd 2018): 33rd International Scientific Conference on Economic and Social Development “Managerial Issues in Modern Business”. Edited by T. Studzieniecki, M. Kozina and D. S. Alilovic. Varazdin: Histoire. [Google Scholar]

- Zianko, V. V., T. D. Nechyporenko, and I. M. Waldshmidt. 2022. Adaptation Mechanism of the Crypto Industry in the Process of Virtualization of Financial Flows. Academy Review 2: 69–86. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Country | Citations | Country | Citations | Country | Citations |

|---|---|---|---|---|---|

| USA | 971 | Malta | 47 | Saudi Arabia/Spain | 18 |

| Australia | 830 | Czech Republic | 45 | New Zealand | 10 |

| Austria | 696 | China | 35 | Slovakia/UAE | 7 |

| Italy | 269 | Russia | 30 | South Korea | 6 |

| France | 219 | Malta | 47 | Lithuania/Turkey | 4 |

| United Kingdom | 135 | Nigeria | 26 | Singapore/Slovenia | 3 |

| Ireland | 71 | Ukraine | 26 | Brazil/Jordan/Norway | 2 |

| Canada | 63 | Finland | 25 | Romania/Switzerland | 2 |

| Lebanon | 61 | South Africa | 24 | Croatia/Greece/Pakistan | 1 |

| Japan | 47 | Malaysia | 21 | Azerbaijan/Netherlands | 1 |

| Cluster | Authors |

|---|---|

| Cluster 1—red (27 items): | Appelbaum, Castonguay, Chou, Church, Clark, Cohen, Coyne, Dai, Dunn, Dyball, Eskandari, Hwang, Jenkins, Kinory, Kokina, Li, Mancha, McMickle, Nehmer, Pachamanova, Schneider, Seethamraju, Sheldon, Smith, Vasarhelyi, Wang, Wei |

| Cluster 2—green (19 items): | Akhmadeev, Ammous, Boulianne, Cho, Fuller, Gilmour, Gyönyörová, Hampl, Jayasuriya, Jumde, Lehoux, Lukiyanova, Markelevich, Morozova, Pandey, Pimentel, Sims, Yumashev |

| Cluster 3—blue (18 items): | Botchie, De V, Gomaa A, Gomaa M, Han, Holub, Jarvis, Johnson, Lombardi, McCallig, Mordi, Moscariello, Pizzo, Ramassa, Robb, Rohde, Shiwakoti, Stampone |

| Cluster 4—yellow (16 items): | Alsalmi, Avhustova, Fomina, Gelashvili, Lin, Moshkovska, Nebreda, Pedreno, Rafique, Raiborn, Romashko, Sivitanides, Tang, Ullah, Yu T |

| Cluster 5—purple (15 items): | Agrawal, Birt, Bourveau, Chou, Cong, De G, Ellahie, Jackson, Landsman, Luo, Luu, Macciocchi, Maydew, Rabetti, Yu S |

| Cluster 6—turquoise (12 items): | Baraniuk, Beigman, Bellucci, Bianchi, Brennan, Gan, Hsieh, Manetti, Netessine, Sannella, Tsoukalas, Volosovych |

| Publication Title | Authors | Journal | Year | Citations | Average/Year |

|---|---|---|---|---|---|

| “Bitcoin: Economics, Technology, and Governance” | Böhme, R et al. | “Journal of Economic Perspectives” | 2015 | 696 | 69.60 |

| “Bitcoin: Medium of Exchange or Speculative Assets?” | Baur, DG; Hong, K and Lee, AD | “Journal of International Financial Markets, Institutions and Money” | 2018 | 604 | 86.29 |

| “Toward Blockchain-Based Accounting and Assurance” | Dai, J and Vasarhelyi, MA | “Journal of Information Systems” | 2017 | 297 | 37.13 |

| “Bitcoin for Energy Commodities Before and After the December 2013 Crash: Diversifier, Hedge or Safe Haven?” | Bouri, E et al. | “Applied Economics” | 2017 | 216 | 27.00 |

| “Conditional Tail-Risk in Cryptocurrency Markets” | Borri, N | “Journal of Empirical Finance” | 2019 | 168 | 28.00 |

| “Blockchain: Emergent Industry Adoption and Implications for Accounting” | Kokina, J; Mancha, R and Pachamanova, D | “Journal of Emerging Technologies in Accounting” | 2017 | 134 | 16.75 |

| “Accounting and Auditing at the Time of Blockchain Technology: A Research Agenda” | Schmitz, J and Leoni, G | “Australian Accounting Review” | 2019 | 128 | 21.33 |

| “Can Blockchains Serve an Accounting Purpose?” | Coyne, JG and McMickle, PL | “Journal of Emerging Technologies in Accounting” | 2017 | 101 | 12.63 |

| “Financial Regulations and Price Inconsistencies Across Bitcoin Markets” | Pieters, G and Vivanco, S | “Information Economics and Policy” | 2017 | 93 | 11.63 |

| “Bitcoin Research Across Disciplines” | Holub, M and Johnson, J | “The Information Society” | 2018 | 75 | 10.71 |

| Institution | Documents | Citations | Total Link Power |

|---|---|---|---|

| City University of New York Cuny System | 6 | 81 | 20 |

| Rutgers State University | 5 | 310 | 51 |

| Columbia University | 3 | 91 | 8 |

| Concordia University | 3 | 56 | 26 |

| Montclair State University | 3 | 36 | 22 |

| Masaryk University Brno | 3 | 9 | 12 |

| Taras Shevchenko National University Kyiv | 3 | 7 | 12 |

| Southwestern University of Finance & Economics | 2 | 326 | 55 |

| Luiss University | 2 | 183 | 0 |

| University of Genoa | 2 | 139 | 33 |

| RMIT University | 2 | 128 | 23 |

| Shenzhen University | 2 | 94 | 19 |

| University of Auckland | 2 | 40 | 47 |

| University Witwatersrand | 2 | 24 | 15 |

| Clusters | Most Relevant Key Terms | Occurrences | Total Link Strength | Main Topic |

|---|---|---|---|---|

| Cluster 1 red (ten items) | accounting | 58 | 167 | Financial accounting and reporting |

| crypto assets | 20 | 59 | ||

| IFRS | 15 | 35 | ||

| distributed ledger technology | 11 | 40 | ||

| financial reporting | 10 | 27 | ||

| stablecoins | 4 | 19 | ||

| intangible assets | 4 | 13 | ||

| ICO (initial coin offering) | 3 | 12 | ||

| tokens | 3 | 8 | ||

| banking | 3 | 6 | ||

| Cluster 2 green (nine items) | cryptocurrency | 84 | 182 | Taxation |

| taxation | 16 | 32 | ||

| digital assets | 5 | 12 | ||

| crypto | 5 | 10 | ||

| IRS | 3 | 10 | ||

| NFT | 3 | 10 | ||

| accounting information systems | 3 | 7 | ||

| mining | 3 | 6 | ||

| electronic money | 3 | 4 | ||

| Cluster 3 blue (four items) | auditing | 31 | 92 | Auditing |

| smart contract | 13 | 46 | ||

| triple-entry accounting | 6 | 20 | ||

| assurance | 3 | 9 | ||

| Cluster 4 yellow (four items) | innovation | 5 | 18 | Innovation management |

| artificial intelligence | 4 | 10 | ||

| management | 3 | 10 | ||

| digital finance | 3 | 5 | ||

| Cluster 5 purple (four items) | bitcoin | 43 | 91 | Investments |

| digital currency | 6 | 18 | ||

| virtual currency | 5 | 11 | ||

| safe haven | 3 | 5 | ||

| Cluster 6 turquoise (two items) | blockchain | 80 | 196 | Accounting education trends |

| accounting education | 3 | 2 | ||

| Cluster 7 orange (two items) | governance | 4 | 11 | Frameworks |

| technology | 3 | 5 |

| Authors | Fair Value or Revaluation Treatment | Cost Treatment |

|---|---|---|

| Alsalmi et al. (2023) | ✓ | |

| Alhasana and Alrowwad (2022) | ✓ | |

| Angeline et al. (2021) | ✓ | |

| Beigman et al. (2023) | ✓ | |

| Bellucci et al. (2022) | ✓ | |

| Blahušiaková (2022) | ✓ | ✓ |

| Corbet et al. (2020) | ✓ | |

| Derun and Mysaka (2022) | ✓ | ✓ |

| Fomina et al. (2019) | ✓ | ✓ |

| Huang et al. (2023) | ✓ | ✓ |

| Hubbard (2023) | ✓ | |

| Jackson and Luu (2023) | ✓ | ✓ |

| Jayasuriya and Sims (2023) | ✓ | ✓ |

| Klopper and Brink (2023) | ✓ | |

| Luo and Yu (2022) | ✓ | ✓ |

| Makurin et al. (2023) | ✓ | |

| Morozova et al. (2020) | ✓ | |

| Niftaliyev (2023) | ✓ | |

| Pandey and Gilmour (2024) | ✓ | |

| Parrondo (2023) | ✓ | ✓ |

| Păunescu (2018) | ✓ | ✓ |

| Pimentel and Boulianne (2020) | ✓ | ✓ |

| Procházka (2018) | ✓ | ✓ |

| Raiborn and Sivitanides (2015) | ✓ | ✓ |

| Ram et al. (2016) | ✓ | ✓ |

| Ramassa and Leoni (2022) | ✓ | |

| Smith et al. (2019) | ✓ | ✓ |

| Vasicek et al. (2019) | ✓ | |

| Vodáková and Foltyn (2020b) | ✓ | |

| Volosovych and Baraniuk (2018) | ✓ | |

| Yan et al. (2022) | ✓ | |

| Yatsyk and Shvets (2020) | ✓ | |

| Yee et al. (2020) | ✓ | |

| Zadorozhnyi et al. (2018) | ✓ | ✓ |

| Total | 31 | 18 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Lazea, G.-I.; Bunget, O.-C.; Lungu, C. Cryptocurrencies’ Impact on Accounting: Bibliometric Review. Risks 2024, 12, 94. https://doi.org/10.3390/risks12060094

Lazea G-I, Bunget O-C, Lungu C. Cryptocurrencies’ Impact on Accounting: Bibliometric Review. Risks. 2024; 12(6):94. https://doi.org/10.3390/risks12060094

Chicago/Turabian StyleLazea, Georgiana-Iulia, Ovidiu-Constantin Bunget, and Cristian Lungu. 2024. "Cryptocurrencies’ Impact on Accounting: Bibliometric Review" Risks 12, no. 6: 94. https://doi.org/10.3390/risks12060094

APA StyleLazea, G.-I., Bunget, O.-C., & Lungu, C. (2024). Cryptocurrencies’ Impact on Accounting: Bibliometric Review. Risks, 12(6), 94. https://doi.org/10.3390/risks12060094