In the dynamic world of financial markets, detecting and understanding the complex phenomenon of price bubbles poses a crucial challenge for investors, analysts, and decision-makers in the financial sector. In this context, the use of advanced models such as Exponential Curve Fitting and Generalized Supremum Augmented Dickey–Fuller becomes essential for assessing and anticipating the evolution of prices within benchmark indices like the BET-FI, DJIA, IXIC, and S&P 500. The significance of employing EXCF and GSADF in the analysis of financial indices like the BET-FI, DJIA, IXIC, and S&P 500 becomes evident amidst high volatility and rapid changes in global markets. Identifying price bubbles in these indices is vital for investors and decision-makers, providing them with the opportunity to adjust strategies and effectively manage risks.

On the other hand, the analysis of price bubble detection is complemented by the use of the ARDL model, where the BET-FI serves as the dependent variable, while the S&P 500, DJIA, and IXIC act as independent variables. The ARDL model was employed to assess the relationships between variables, interdependencies, influences, and causality, as well as the effects of financial contagion. The BET-FI, as the dependent variable, represents the BET-FI Index, reflecting the overall performance of the financial market in Romania. Modeling this variable enables an understanding of its impact and interactions with other relevant variables. Thus, the ARDL model can unveil whether and how changes in the independent variables may influence the BET-FI, highlighting connections and interdependencies among financial markets. Additionally, the ARDL model provides the opportunity to analyze both short-term and long-term relationships, allowing the identification of immediate effects and adjustments in the dependent variable’s response to changes in the independent variables. The outcomes of the ARDL model can offer valuable insights for strategic decision-making, risk management, and the development of more effective strategies within financial markets.

4.1. Detecting Financial Bubbles: EXCF and GSADF Models Unveiled

In the dynamic landscape of financial markets, identifying and managing risks associated with price bubbles is a critical challenge. The use of models such as Exponential Curve Fitting and Generalized Supremum Augmented Dickey–Fuller becomes paramount in understanding price movements and anticipating potential shifts in market behavior. These analytical tools are particularly relevant in the case of key financial indices such as the BET-FI, DJIA, IXIC, and S&P 500.

According to

Watanabe et al. (

2007a,

2007b) and

Cabello Sánchez et al. (

2021), EXCF makes a significant contribution to time series analysis, providing insights into market trends and volatility. By fitting exponential curves to price data, EXCF helps highlight significant patterns, facilitating the identification of potential price bubbles and the anticipation of directional changes. On the other hand, GSADF, with its robust approach, according to

Peng et al. (

2023) explores the phenomenon of price bubbles and contributes to validating the results obtained with EXCF. By integrating this model into our analysis, we had the opportunity to confirm and strengthen warning signals, adding an additional level of confidence to the process of identifying price bubbles. The importance of this analysis extends beyond the identification and quantification of price bubbles in isolation. As financial markets are interconnected, the phenomenon of financial contagion becomes a crucial component. Identifying a bubble in a major index, such as the S&P 500, can influence the behavior of other indices, such as the BET-FI, DJIA, and IXIC. By using EXCF and GSADF to examine these interdependencies, we gain a broader and more precise view of how changes in one index can propagate and affect the entire financial landscape. The EXCF model uses rolling estimates with the aim of providing information about the variation in volatility and significant changes in the dynamics of the analyzed time series. These estimates offer insight into how volatility changes over time and can help identify periods where it increases significantly, indicating potential points of interest for the analysis of financial bubbles. The interpretation of these estimates is performed in the context of the analyzed time series. When the rolling estimates present higher values, this suggests increased volatility during those periods, which may be associated with potentially significant changes in market prices. Generally, areas with high values of the rolling estimates can draw attention to periods where there is an increased probability of the formation of financial bubbles or significant events in the market.

Through this integrated analysis, we aimed to make a significant contribution to understanding the dynamics of financial markets, allowing investors and decision-makers to approach the risks associated with price bubbles with more confidence and develop more informed strategies in the face of global market challenges.

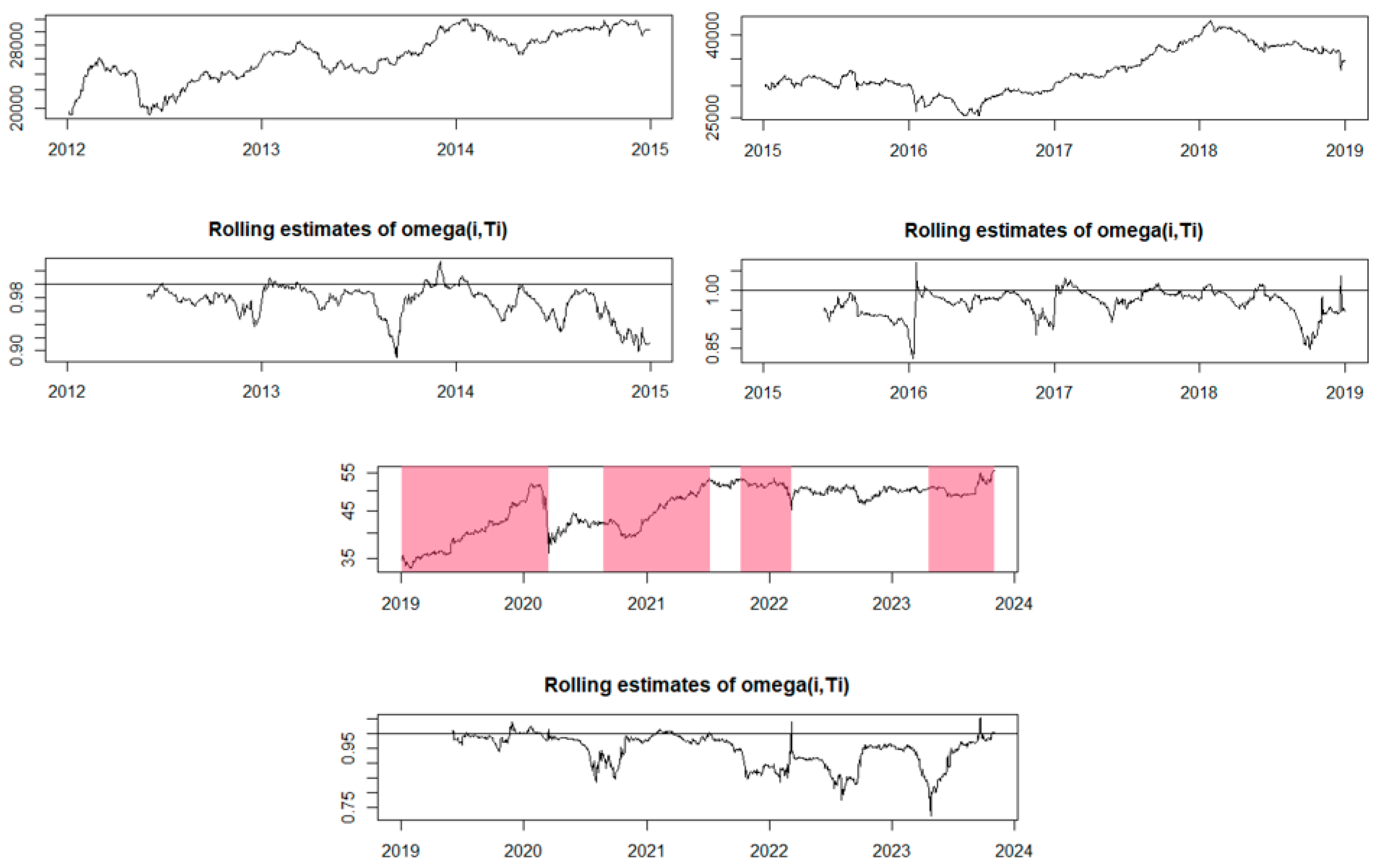

In

Figure 1, the evolution of closing prices for the analyzed indices has been depicted for the period from 2012 to October 2023. The BET-FI reflects the performance of the most liquid companies listed on the Bucharest Stock Exchange, particularly those in the financial sector. The evolution of this index is influenced by the economic conditions in Romania and events specific to the local market. It is observed that throughout the analyzed period, the evolution of this index has been quite volatile, with many periods of growth or decline.

The S&P 500 is one of the most closely monitored indices of the American stock exchange, representing the performance of 500 large companies listed on American exchanges. Its evolution is closely tied to the state of the American economy, government policies, and global trends in financial markets. The S&P 500 index showed relatively steady growth from 2012 until 2015, with a slight decline observed in 2016 followed by subsequent increases. Additionally, three distinct periods of decline with larger amplitudes can be observed in 2017, 2020, and the end of 2022.

The Nasdaq Composite (IXIC) comprises the stocks of a broad range of technology and other sector companies listed on the Nasdaq. The evolution of this index is influenced by technological innovations, the financial results of tech companies, and changes in investor preferences.

The DJIA represents the performance of 30 large and significant companies in the United States. This index is often considered a barometer of the health of the American economy, with an emphasis on industrial and consumer sectors.

Next, we used the EXCF test to detect financial bubbles. This model has a very short execution time compared to GSADF, which can take several hours. GSADF can be considered a more robust option, allowing comparisons between periods identified as the time of a price bubble’s emergence. We used RStudio (version 2023.09.1+494, developed by Posit, PBC) to implement these two methods.

In

Figure 2, we can observe that for the period from 2012 to 2018, the model did not identify any financial bubbles. However, during the period from 2019 to 2023, the model identified four potential price bubble formation periods (marked by pink bands). In 2019, a significant increase was noted, indicating the presence of a potential positive bubble, followed by a financial bubble forming at the end of 2020, extending for three quarters into 2021. A positive price bubble occurs when the prices of the analyzed indices rise rapidly and significantly. This can be caused by increased investor interest, speculation, or positive events that are relevant or impactful in the financial market. In a positive bubble, prices can exponentially rise and reach very high levels in a short period. On the other hand, a negative bubble refers to a period when cryptocurrency prices decline rapidly and significantly. This may result from a decrease in investor interest, negative external factors, or normal market corrections after a period of excessive price growth. In a negative bubble, prices can suddenly drop and reach much lower values than those recorded during the previous growth. The end of 2021 and the beginning of 2022 were marked by another period in which a potential price bubble could be identified, this time negative, as it was characterized by an unusual decline, according to the model. Additionally, it appeared that a fourth financial bubble was forming even in 2023.

The EXCF model has a limitation in its ability to accurately distinguish between genuine bubbles and artificial price fluctuations in a dataset. While it can identify apparent price increases, the EXCF test does not provide conclusive evidence to confirm the presence of a genuine positive price trend. To assess the precision of the models in detail and for a more comprehensive comparison, we also conducted the GSADF test. It is noted that the EXCF test has a relatively short processing time, typically requiring only a few seconds on a standard computer. In contrast, the GSADF test requires a longer processing time due to higher computational resource demands. It is essential to emphasize that, although the GSADF test provides more precise and advanced results, it does not offer the same cost efficiency as the EXCF test and requires more powerful equipment for long-term analyses.

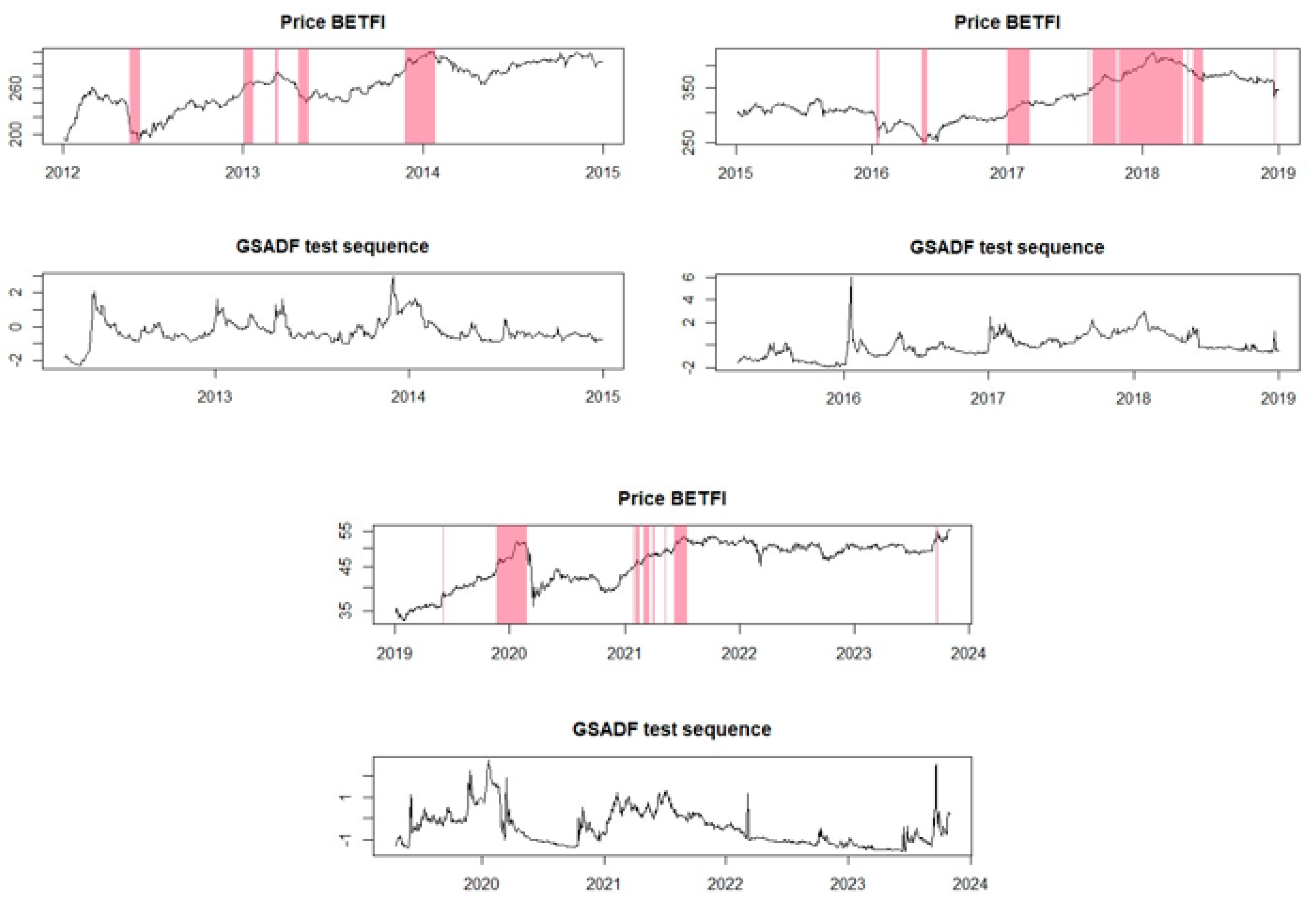

Regarding the financial bubble identification test using the GSADF method, it was conducted as shown in

Figure 3. We can observe that there are periods similar to those identified as price bubbles using the EXCF method, but it also brings to light additional periods. For instance, the GSADF model highlighted potential price bubbles during the period 2012–2018, which the EXCF model did not identify. Thus, during this period, 10 time intervals were identified where these financial bubbles occurred. Additionally, the GSADF test confirmed the bubbles from the recent years analyzed, 2019–2023, also identified by the EXCF model.

To understand how these price bubbles of the BET-FI Index formed, we sought various information to identify possible factors underlying the formation of financial bubbles.

At the end of 2009, according to

Finance Newspaper (

2009), the BET-FI Index, which monitors the performance of five financial investment companies on the Bucharest Stock Exchange, recorded a 6% decline in Wednesday’s session, marking the most significant downturn in the last four months, amid a 4% overall market decline. The BET Index, representing the top ten most liquid companies, depreciated by 3.29%. This development followed a recorded major decline, influenced by the negative trend in European markets.

According to information from Banking News in 2015, the Bucharest Stock Exchange experienced a significant decline, and analysts believed that, in the absence of a rapid recovery in the Chinese economy, a more severe crisis than the one in 2008 could follow. On 24 August 2015, all stock exchanges faced a price shock, driven by the crisis in the Chinese economy, according to specialists’ opinions. This day was dubbed “Black Monday.” Stock exchanges in several Asian countries opened lower due to the dramatic fall of the Shanghai Stock Exchange. Financial market panic began with the depreciation of the yuan, the Chinese national currency. Economists argued that everything was triggered by the decision of major investment funds to withdraw their capital under investor pressures. The Shanghai Stock Exchange closed down 8.5%, the most drastic decline in the last eight years, initiating a domino effect, meaning a financial contagion.

According to the

Bucharest Stock Exchange (

2023) for the BET-FI Index, 2019 was the year the index registered one of its best rentabilities since its apparition (1995), considering that all of the market indexes had also registered exponential rentability growth (up to 47%, if we consider the BET-TR Index). This immense increase in the rentability of the index was mainly a result of Hidroelectrica being listed in the market, considering its very high importance in the Romanian market. Between late 2020 and late 2021, it seems like the BET-FI Index registered a significant increase due to the fact that the dividends have paid off for investors, showing a 40% return on investment.

It seems like the armed war between Russia and Ukraine triggered a decrease in the financial markets. Russia’s late February invasion of Ukraine caused a global shock within the financial markets, BET-FI included, right in the next month. Yet, until 2022, the BET-FI Index managed to partially recover from this event, mainly due to how the other financial markets evolved, but also due to the dividend’s proposal. Even though the index registered small ups and downs throughout 2021, the beginning of 2022 registered a decrease in the index caused by a “solidarity tax” imposed by the local government, a tax that reduced the index by 3.7% (

Bursa.ro 2022).

As for the abovementioned period, Hidroelectrica played a crucial role in how Romania’s financial market evolved during this year. The main reason for the increase that we can observe at the end of the year is the 170,000 investors in the Hidroelectrica company that directly impacted the direction of the local financial markets, the BET-FI included (

Forbes.ro 2023).

This analysis indicates that the evolution of the BET-FI Index has been influenced by several key factors, leading to distinct periods of financial bubble formation. For example, in 2019, a significant growth period of the index was observed, marking a potential positive bubble. This was largely attributed to the listing of Hidroelectrica, which held significant importance in the Romanian financial market. Investors benefited from substantial dividends, contributing to the index’s rise. Between the end of 2020 and the end of 2021, the BET-FI Index experienced significant growth, primarily due to dividend payments to investors, yielding a 40% return. This contributed to the formation of a potential positive bubble. Furthermore, the beginning of 2022 was marked by a decline in the index following Russia’s invasion of Ukraine. This geopolitical instability triggered a global shock in financial markets, impacting the BET-FI as well. However, the index managed a partial recovery, reflecting the evolution of other financial markets. Additionally, in 2023, Hidroelectrica continued to play a crucial role in the financial market’s evolution, significantly influencing the BET-FI Index.

In summary, the multiple financial bubbles identified in the analyzed period can be attributed to a complex mix of events, listings of significant companies, geopolitical factors, and government decisions. Each period of growth or decline reflects the specific dynamics of the Romanian financial market and the factors that influenced it during those moments. Furthermore, each period of growth or decline in the BET-FI Index can be understood in the context of financial contagion, where external events and internal decisions have an amplified impact on financial markets, directly influencing the index’s evolution. Financial contagion manifests through the rapid transmission of shocks and instability from one area of financial markets to others.

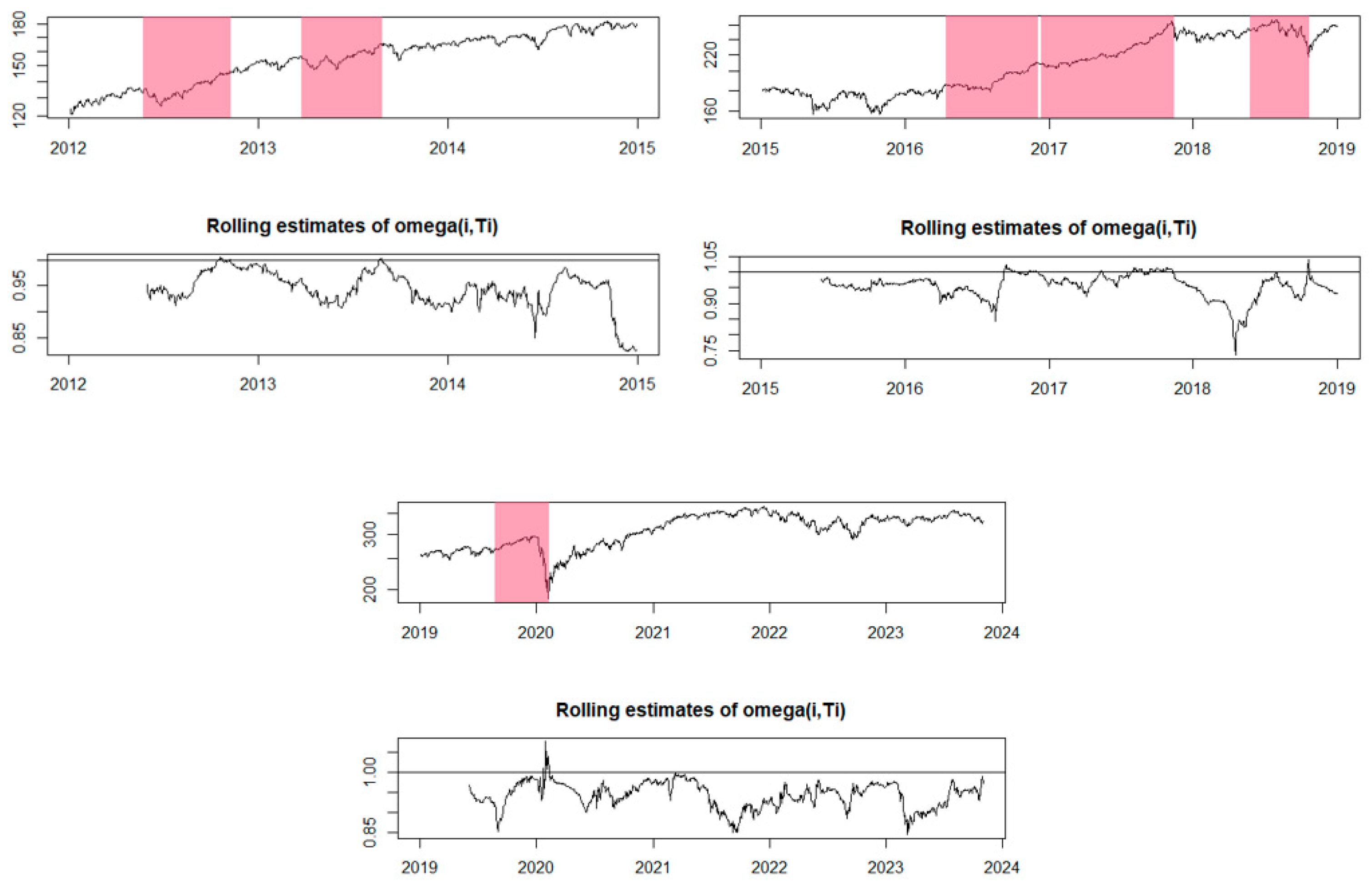

In

Figure 4, the EXCF test was conducted to highlight financial bubbles for the S&P 500 index. In this case, the model identified six periods in which price bubbles formed, spanning from 2015 to 2023.

In 2015, the S&P 500 index experienced varied performance throughout the year. Concerns arose about the global economic growth slowdown, particularly in China (

CNBC.com 2015). Weak economic data and volatility in global financial markets raised worries about their impact on American companies and the potential for a recession. Additionally, oil prices significantly declined in 2015, impacting energy sector companies and causing concerns about the overall health of the global economy. This had a negative effect on the stocks of many S&P 500 companies, as a significant number of them are either directly related to or have ties with the energy sector (

Yahoo Finance 2016;

The Guardian.com 2015).

In 2016 and 2017, the S&P 500 index exhibited positive performance, with relatively limited periods of decline during those years. In the first part of 2016, concerns about the health of the Chinese economy and financial market volatility negatively impacted the S&P 500. However, the market later rebounded, partly due to global economic stimuli. The presidential elections in November 2016 were a significant moment for financial markets. Following the election of the president, the initial market reaction was negative, but a reversal occurred, and the market showed positive trends, fueled by optimism regarding pro-business policies announced by the presidential administration (

CNBC.com 2017a).

The year 2017 witnessed a strong rally in financial markets, including the S&P 500, amid expectations of tax cuts, deregulation, and fiscal incentives under the presidential administration. In 2017, the U.S. economy continued to grow, and companies reported robust profits. These factors supported the positive performance of the S&P 500 (

CNBC.com 2017b).

Trade tensions between the United States and China escalated in 2018, with the mutual imposition of customs tariffs. Investors were concerned about the potential impacts of these tensions on global economic growth and corporate profitability (

International Monetary Fund 2019).

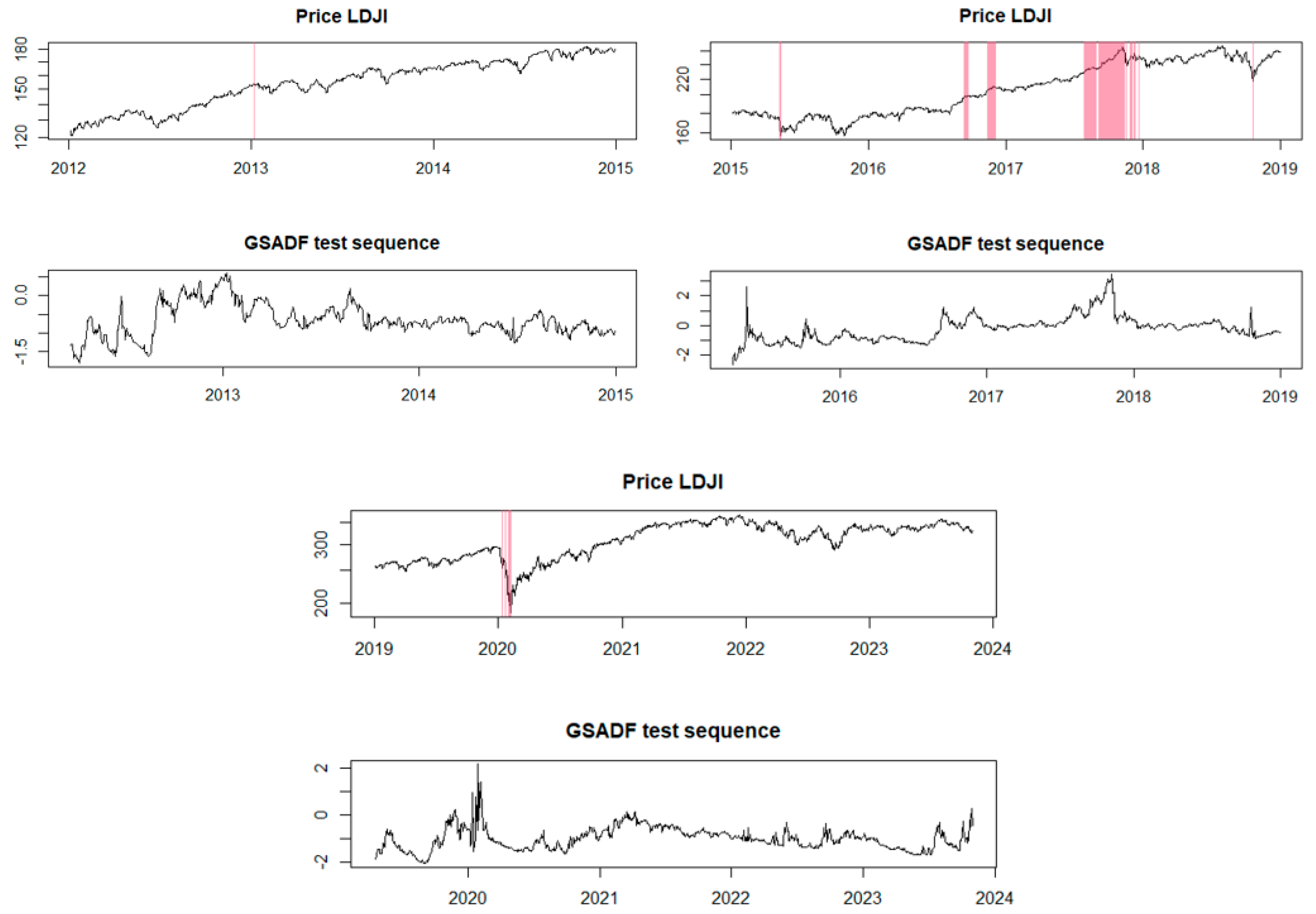

The GSADF model sequence in

Figure 5 also illustrates periods during which price bubbles were identified, similar to the EXCF model, starting from the year 2015 but extending until the year 2021. Therefore, we can conclude that the financial bubbles identified for the S&P500 index between 2015 and 2023 were influenced by various factors such as global economic concerns, presidential elections, and economic and trade tensions. All of these events can create panic among investors, leading to immediate decisions that may cause disruptions in the financial market.

Regarding the IXIC index, the EXCF model was applied in

Figure 6. It can be observed that the periods of identified financial bubbles are similar to those identified in the S&P 500 index.

In the first half of 2014, the IXIC index experienced robust growth, marked by significant increases and reaching new highs. The technology sector played a pivotal role in driving this growth, with companies such as Apple, Google, and Facebook delivering strong performances, contributing significantly to the index’s advancement. Additionally, the biotechnology sector saw significant growth during the same period, further adding to the rise of the IXIC. Smaller biotechnology companies recorded notable gains due to progress in drug development and positive results from clinical studies. All of these factors contributed to the formation of price bubbles (

Techcrunch.com 2014).

Moreover, the other identified bubbles are justified by the same factors as those for the S&P 500, such as electoral elections, global concerns about economic growth, especially in China, but also factors like the performance growth of the tech sector (

International Banker.com 2017). Additionally, the biotechnology and healthcare sectors were active contributors to the index’s volatility. The performance of smaller biotech firms and healthcare companies continued to impact the Nasdaq Composite’s movements.

Furthermore, the explosive growth of cryptocurrencies, especially Bitcoin, has captured the attention and interest of investors. While not directly linked to the IXIC index, this trend reflects an appetite for innovative assets with high growth potential among investors.

The GSADF test for the IXIC index can be identified in

Figure 7. Unlike the EXCF model, this test identified fewer price bubbles for the analyzed index.

The EXCF model has been tested for the last index analyzed by us, the DJIA index. We observe in

Figure 8 that six periods with financial bubbles have been identified. Both positive and negative bubbles are observed.

Additionally, the GSADF test also identified periods in which there were potential price bubbles for the DJIA index. In

Figure 9, one can observe the periods marked for these price bubbles, which are relatively similar to the EXCF test but over shorter time frames.

All of these analyses highlight that political tensions, armed conflicts, and economic imbalances in major countries with systemic importance in the global economy, such as China, can generate contagion effects that affect the financial market. Investor panic and changes in investment behavior are also impacted and can contribute to the formation of price bubbles. Additionally, we observed for all of the analyzed indices that during the COVID-19 pandemic period, price bubbles were identified, emphasizing that the pandemic itself represented a factor in the formation of these bubbles.

The analysis in this section concludes with the determination of the Value at Risk (VaR) and Expected Shortfall (ES). The VaR is a measure of the maximum expected loss at a certain confidence level, expressed in percentages. The ES (Expected Shortfall) represents the expected value of losses in case they exceed the specified VaR level. These values can provide investors with useful information about the level of risk associated with the analyzed stock indices.

The graphs in

Figure 10 depict the VaR (Value at Risk) and ES (Expected Shortfall) levels for the analyzed indices: BET-FI, S&P 500, IXIC, and DJIA. The blue horizontal line represents the 5% VaR level, while the green horizontal line indicates the 5% ES level. The VaR represents the maximum expected loss in the worst 5% of scenarios, while the ES represents the expected value of losses in the worst 5% of scenarios. The graphs track moments when the returns of the four analyzed indices exceed the estimated risk levels. It is observed that most of the instances where the risk level was exceeded coincide with periods when the analyzed stock indices were in a negative or positive bubble. This may suggest that, despite the financial market being quite volatile, it is not advisable to invest during periods of identified financial bubbles.

4.2. Exploring Stock Index Modeling with ARDL: Insights into Performance Metrics

This study delved into the complex world of financial indices, with a specific focus on the BET-FI as the dependent variable. Through advanced econometric techniques, we aimed to uncover hidden patterns, assess the impact of various factors, and provide valuable predictive insights into the performance of stock indices. According to

Nica et al. (

2023a), the ARDL model stands out as a flexible instrument for scrutinizing time series data and unraveling relationships among research variables. Its proficiency in addressing both short-term and long-term dynamics, as well as handling cointegration and ensuring robustness, renders it indispensable for empirical research. This section delves into the fundamental steps of applying the ARDL model to our dataset. Descriptive statistics play a crucial role in comprehending and priming the data before implementing the ARDL model.

Table 2 provides a detailed overview of the basic statistical characteristics of the data distribution for the BET-FI, S&P 500, IXIC, and DJIA indices. Statistics such as mean, median, minimum and maximum values, standard deviation, skewness, kurtosis, and the Jarque–Bera test for normality of skewness and kurtosis are presented. According to the information in

Table 2, all indices have median values close to the means, suggesting a relatively symmetric distribution around the central value. Additionally, small standard deviations indicate a relatively tight concentration of values around the mean. Skewness values close to zero indicate a relatively symmetric distribution for the analyzed stock indices, and the kurtosis values suggest that the peaks of the distributions are generally within the normal range, reflecting a moderate concentration around the mean. For all indices, the Jarque–Bera values are significant at a significance level of 0.10 or 0.08, suggesting a small deviation from a normal distribution.

In

Table 3, the results of the Augmented Dickey–Fuller test are presented, indicating whether the time series of the analyzed variables has a unit root and providing information about the order of integration required to make these series stationary. At that level, the t-statistics coefficient is −1.28, with a probability (

p-value) of 0.63. However, upon applying the first differencing, the t-statistics coefficient becomes significant at −10.95, with a probability of 0.00. This result suggests that the BET-FI variable requires differencing to become stationary, and the order of integration is I(1). Similarly, for the S&P 500, at that level, we have a t-statistics coefficient of −1.32 with a probability of 0.61, and through differencing the data once, the coefficient becomes significant at −13.28, with a probability of 0.00. This also indicates an order of integration of I(1). The same observations hold for the variables IXIC and DJIA. At that level, the t-statistics coefficients are not significant, but they become significant upon differencing the data once, and the order of integration is I(1). In the case of the ADF test, which includes both the intercept and trend, the results are similar. The t-statistics coefficients become significant at that level (with the intercept) and become even more significant upon differencing once. The order of integration for all variables is I(1). According to (

Shrestha and Bhatta 2018), an Autoregressive Distributed Lag (ARDL) model represents a regression model based on Ordinary Least Squares (OLS) methodology. It is suitable for analyzing both non-stationary time series and time series with a mixed order of integration. The ARDL model incorporates an adequate number of lags to effectively capture the underlying data-generating process within a general-to-specific modeling framework.

The subsequent step involves determining the suitable lag structure for the ARDL model, as outlined in

Figure A1 from

Appendix A.

Enders (

2014) emphasized the importance of meticulously choosing the optimal lag length before implementing the ARDL model. This step is critical for several reasons, including ensuring the model’s proper alignment with the data. A lag length that is too short could lead to the model missing key dynamics, potentially causing an omitted variable bias.

Table 4 displays the outcomes of the cointegration bounds test, designed to explore the existence of long-term causality. The F-statistic, computed at 6.61, exceeds the critical upper bounds associated with I(1), signifying the presence of cointegration among the variables under scrutiny. In this instance, the chosen model is ARDL (1, 0, 2, 0).

The results of the cointegration bounds test (ARDL) indicate that the F-statistic is relevant for analyzing the cointegration among the involved variables. The F-statistic values, along with critical bounds for different significance levels, are presented in

Table 4. Since the F-statistic exceeds all critical values for a significance level of 1%, there is cointegration among the analyzed variables at a confidence level of 99%. This suggests a stable, long-term relationship between the respective variables.

The use of the Error Correction Model (ECM) equation is crucial for understanding short-term adjustments toward long-term equilibrium. In

Table 5, it is observed that for each unit increase in the S&P 500, a corresponding increase of 1.31 units in the dependent variable BET-FI is expected in the long term. This result is significant at a 0.05 significance level. Regarding the IXIC index, for each unit increase, a corresponding decrease of 0.75 units in the dependent variable BET-FI is anticipated in the long term. This result is significant at a 0.05 significance level. The constant term, denoted as C, represents the expected value of the dependent variable BET-FI in the long term when all other regressors are zero. Although it is not significant at a 0.05 significance level, it contributes to the baseline level of the dependent variable. Also, in Equation (10), the mathematical form of the error correction term has been represented, indicating the short-term adjustments of the variable BET-FI toward the long-term equilibrium determined by the regressors included in the model.

In

Table 6, the ARDL Error Correction Regression was employed to estimate short-term adjustments within the ARDL model. This type of regression is crucial for assessing the immediate impact of temporary deviations from long-term equilibrium, as well as for studying the dynamics of variables within the model. Thus, we observe that for a one-unit increase in the D(IXIC) (the first difference of the IXIC), a corresponding short-term increase of 0.16 units is expected in the dependent variable BET-FI. This result is significant at a 0.05 significance level. Additionally, a 0.22-unit increase in D(IXIC) in the previous period (a lagged difference of the IXIC) is associated with a significant short-term increase of 0.22 units in the dependent variable BET-FI. This result is significant at a 0.01 significance level. The symbol “*” signifies that this variable is lagged by one period in the regression model. The error correction term indicates adjustments toward long-term equilibrium. A negative coefficient suggests a negative correction toward equilibrium in the short term. This term is significant and contributes to immediate adjustments of the variables. Regarding the model quality metrics, the coefficient of determination (R-squared) indicates the proportion of variance in the dependent variable explained by the model. Measures of the AIC, BIC, and HQC criteria are used to evaluate the model efficiency, with lower values indicating a better model. The Durbin–Watson statistic measures the autocorrelation of residuals, with a value close to two indicating the absence of autocorrelation.

Regarding the diagnosis of coefficients, a coefficient confidence interval test was conducted. The confidence interval (CI) for the variables analyzed in our ARDL model indicates the range in which the respective coefficients are likely to fall with a certain level of confidence. For example, as shown in

Table A2 from

Appendix A, the estimated coefficient for the BET-FI (−1) is 0.77, and the 99% confidence interval is [0.65, 0.90]. This interval indicates with 99% confidence that the true coefficient of the BET-FI (−1) variable is between 0.65 and 0.90. The values for the all confidence intervals are presented in

Table A2 from

Appendix A.

To conduct the residuals diagnosis, a histogram–normality test was performed.

Figure 11 presents information about the distribution of the residuals. The value of the mean very close to zero indicates that the mean of the residuals is close to zero, which is positive for the accuracy of the model. Similar to the mean, a median close to zero suggests symmetry in the distribution of the residuals. The maximum and minimum values indicate the range in which the residuals fall. The fact that these values are relatively small may suggest a good fit of the model. The low standard deviation value of 0.03 indicates a low dispersion of the residuals around the mean, suggesting a better fit of the model. The Jarque–Bera test checks whether the residuals have a normal distribution. A lower probability suggests a significant deviation from normality. In our model, the probability is 0.09, suggesting that there is not enough evidence to reject the null hypothesis of normality at a significance level of 0.05.

To check for signs of functional misspecification in the model, the Ramsey reset test was employed, and the results are presented in

Table 7. For the restricted model (original), the probabilities associated with the t-statistics, F-statistic, and likelihood ratio are quite high (0.29 and 0.28). This suggests that there is not enough evidence to reject the null hypothesis of correct model specification. Therefore, the original model seems to be well-specified. Regarding the unrestricted model, probabilities around 0.85 indicate that there is not enough evidence to reject the null hypothesis of correct specification for the unrestricted model either. The high R-squared (97%) indicates a good fit of the data within the unrestricted model.

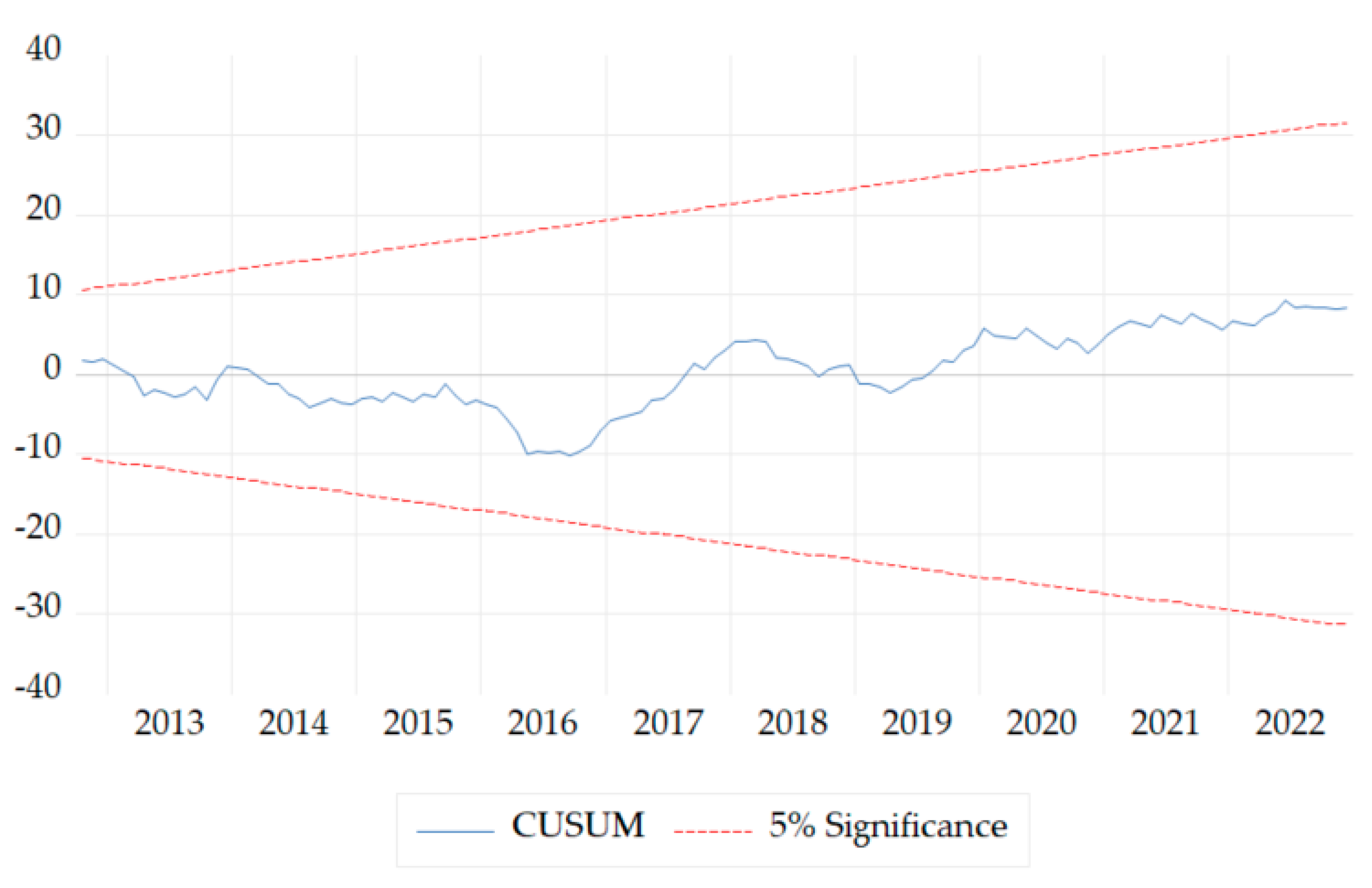

The CUSUM test is a method used to assess the stability of a model over time. In

Figure 12, we can observe the blue line (CUSUM) constructed to track the cumulative sums of residuals from the model as we observe new data. There are two critical significance lines (red) at 5%. Given that the CUSUM line does not cross the significance critical lines, this suggests that the model is stable, and there are no significant signs of performance degradation over time.

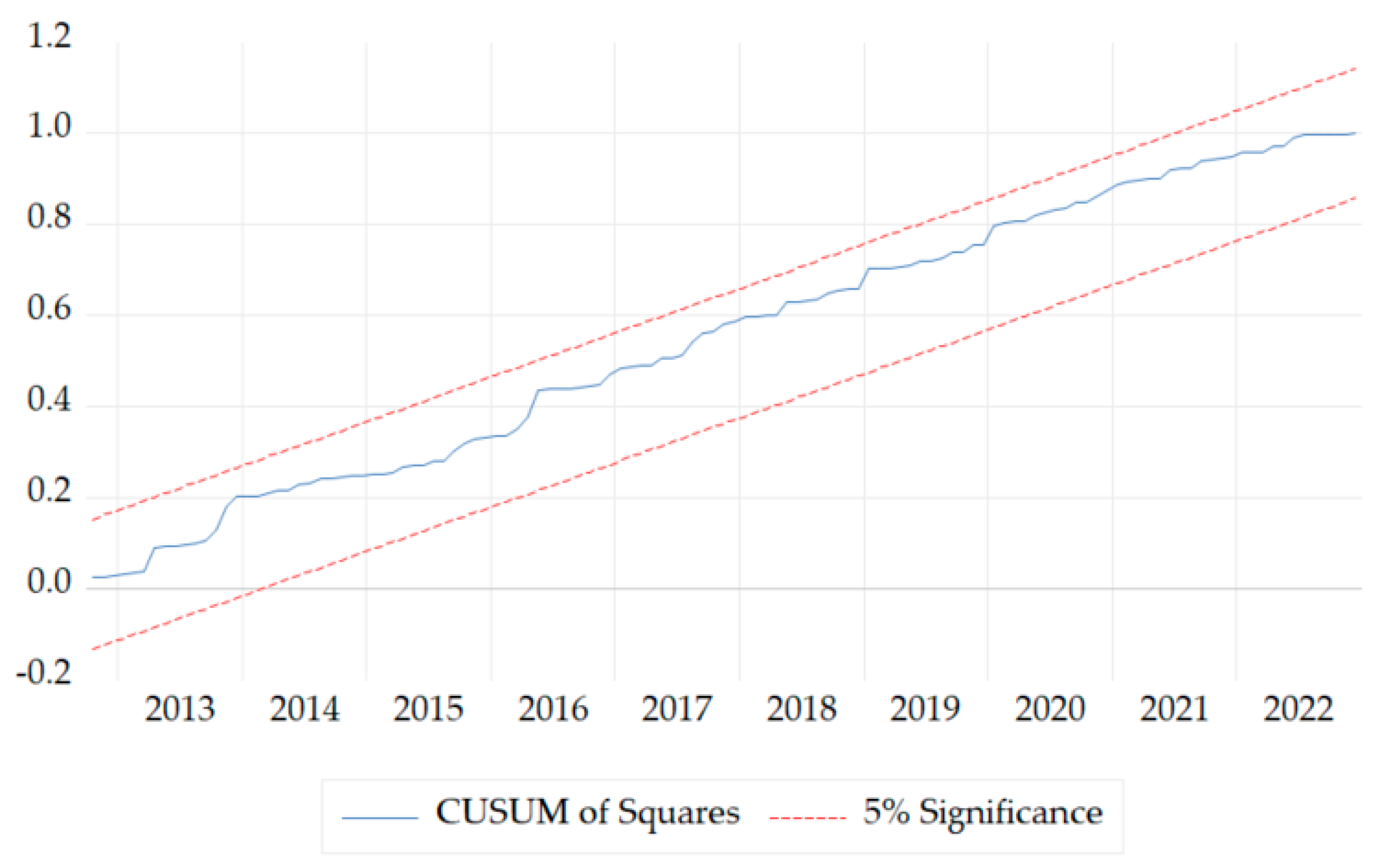

Regarding the graph in

Figure 13, CUSUM of squares refers to a CUSUM plot based on the squares of the residuals or the squares of the differences between the observed values and those predicted by the model. This CUSUM plot is used to assess the model’s stability over time concerning the variability of the residuals. If the CUSUM of squares line moves consistently and does not cross the critical significance lines, it indicates stability in the variability of the residuals. Overall, a CUSUM of squares plot provides information about significant changes in residual variability and can help identify moments when the model might require adjustments.

In order to provide a more comprehensive analysis and strengthen the obtained results, the VAR model results from

Table A3 in

Appendix A provides estimates of the lagged effects of variability in stock indices and measures for assessing the model’s quality. According to the values of R-squared and adjusted R-squared, we can confirm that the observed data fit the model. Additionally, the standard error equation shows that the results are precise, considering the very low values. In

Figure 14, the variance decomposition using Cholesky factors for different periods and the analyzed stock indices have been illustrated. Numeric values are presented in

Table A1 in

Appendix A, representing the percentages of the total variation in each stock index explained by Cholesky factors in different periods. For instance, as observed in

Figure 15, for the BET-FI Index in period 1, the entire variation (100%) is explained by the Cholesky factor associated with the BET-FI. In subsequent periods (5, 10, 15, and 20), a gradual reduction in the relative contribution of the Cholesky factor associated with the BET-FI to the total variance is noticeable. Similar to the BET-FI, each stock index has its own associated Cholesky factor. Overall, Cholesky factors associated with the respective stock indices have a significant contribution in period 1. As time progresses, the relative contribution of these factors decreases, suggesting that other factors (other stock indices and additional factors) begin to play a more prominent role in explaining the variation. In subsequent periods, a redistribution of variance among the stock indices is observed, indicating changes in the interactions and their impact on variation. From the perspective of financial contagion effects, Cholesky factors indicate how the variability of one stock index is correlated with others. A strong correlation may suggest that changes in one index are associated with similar or opposite changes in other indices, thereby indicating interdependence.

Historical decomposition using generalized weights is a method employed in time series analysis that decomposes the historical movements of a variable of interest into the contributions of various shocks or structural innovations that occurred in the past (

Figure 15). The interpretation of the historical decomposition graph is achieved by analyzing the individual contributions of the factors to the total variation of the variable. Each line or component of the graph represents the relative contribution of a specific factor or shock to the movements of the variable at a particular point in time. For example, the first graph illustrating the decomposition of the BET-FI includes different time series such as “actuals,” “baseline,” “baseline+BET-FI,” “baseline+S&P 500,” “baseline+IXIC,” and “baseline+DJIA.” “Actuals” represents the time series of the BET-FI variable in this case. “Baseline” depicts the evolution of the BET-FI Index in the absence of other factors or additional influences, serving as a baseline for comparison and showing how the variable would evolve if there were no external factors. The other lines represent how the BET-FI evolves, influenced only by the S&P 500 factor (green line), only by the IXIC factor (red line), or only by the DJIA factor (black line). We observed differences between the actuals and baseline, indicating the impact of the other indices or external influences on the actual time series.

According to the results in

Table 8, the mathematical form of the ARDL (1, 0, 2, 0) model has been written in Equation (11), where the dependent variable is the BET-FI Index, and the independent variables are the S&P 500, IXIC, and DJIA indices. The specification (1, 0, 2, 0) of the ARDL model means that it uses an autoregressive order of 1, indicating that a previous period of the dependent variable is included; an integration order of 0, meaning that the variables have not been differenced to become stationary; a moving average order of 2, indicating that two moving average terms are included in the model (IXIC(-1) and IXIC(-2)); and the last parameter in the specification, 0, refers to the fact that no seasonal components are included. In the case of BET-FI (-1), the coefficient of 0.77 indicates that an increase by one unit in the BET-FI variable in the previous period is associated with an increase of 0.77 units in the BET-FI variable in the current period. The coefficient for the S&P 500 index is 0.29, suggesting that an increase by one unit in the S&P 500 variable is associated with an increase of 0.29 units in the BET-FI variable. Regarding the IXIC index, the coefficient is 0.16, indicating that an increase by one unit in the IXIC variable is associated with an increase of 0.16 units in the BET-FI variable. The coefficient is −0.11 for IXIC (-1), suggesting that an increase by one unit in the lagged value of the IXIC variable is associated with a decrease of −0.11 units in the BET-FI variable. Also, the coefficient of 0.22 for IXIC (-2) indicates that an increase by one unit in the second lagged values of the IXIC variable is associated with a decrease of −0.22 units in the BET-FI variable. Regarding the DJIA index, an increase by one unit in the DJIA variable is associated with an increase of 0.12 units in the BET-FI variable. According to the results of the model, the equation can be written in accordance with Equation (11).

From the perspective of the ARDL model’s performance, the R-squared value is 0.97, indicating that the model explains approximately 97% of the variation in the dependent variable. The F-statistic value indicates that the model is globally significant, and the Durbin–Watson test suggests that the residuals do not have significant autocorrelation. The low values of the AIC, Schwarz, and log-likelihood metrics indicate a good model, with these metrics used to evaluate the efficiency of the model. Regarding the prediction of the dependent variable, it has been illustrated in

Figure 16.

To assess the forecast quality, metrics such as RMSE (root mean squared error), MAE (mean absolute error), MAPE (mean absolute percent error), bias proportion, covariance proportion, and Theil’s U2 coefficient were used. RMSE measures the dispersion between the predicted and observed values. The lower the RMSE value, the higher the model’s accuracy. MAE is the average of the absolute differences between the forecasts and observations. A lower value indicates higher accuracy. MAPE measures the percentage of absolute error relative to the observed values. Theil’s coefficient compares the variability of the forecasts to the variability of the observations. A lower value suggests a more precise forecast. Bias proportion indicates the percentage of average error (bias) relative to the mean of observations. A very low value indicates no tendency to over- or under-estimate forecasts. Covariance proportion indicates the percentage of covariance between the forecasts and observations relative to the variance of the observations. A high value, close to one, suggests good agreement between the forecasts and observations. Theil’s U2 coefficient provides a measure of forecast quality relative to a simple base forecast (e.g., the mean). A lower value indicates better accuracy, and a value of 1.29 suggests that our forecast is better than a simple base forecast.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}