Responsible Innovations as Tools for the Management of Financial Risks to Projects of High-Tech Companies for Their Sustainable Development

,

,  and

and

Abstract

1. Introduction

2. Literature Review

3. Research Design and Methodology

- r—arithmetic mean of negative values of the change in indices as a risk event;

- p—share of negative values of the change in indices as a reflection of the probability of the risk event.

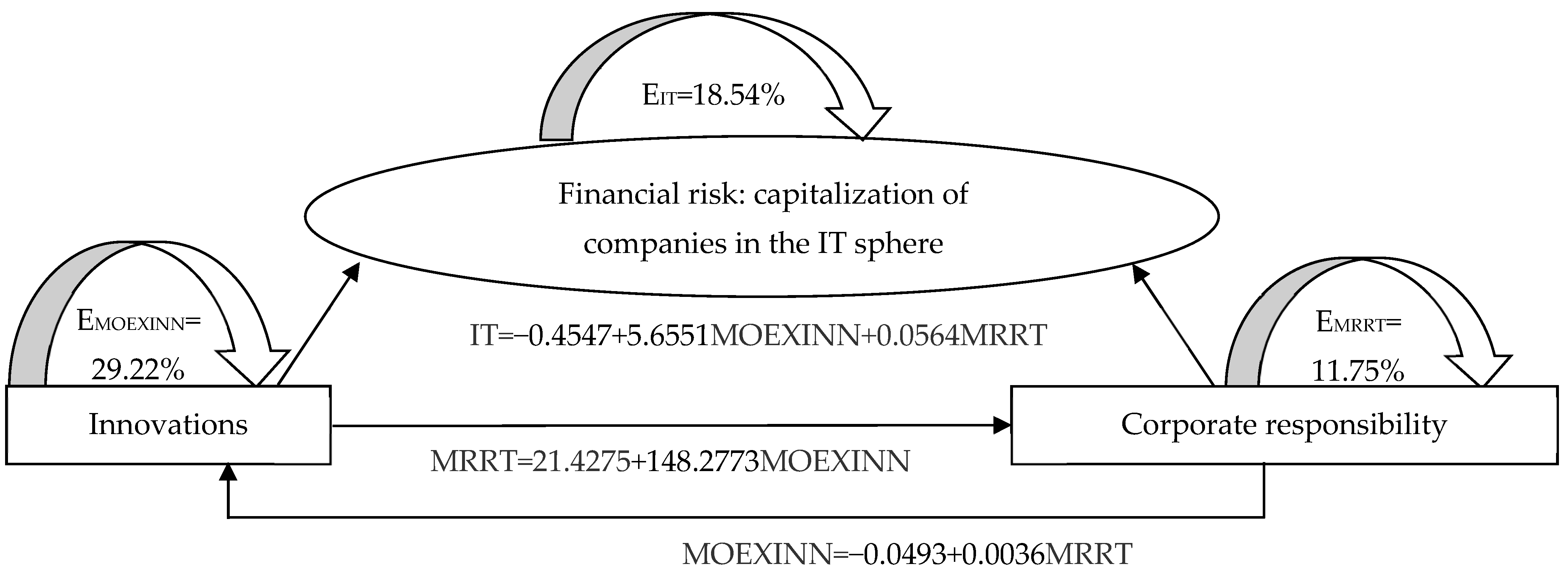

4. Results

4.1. The Role of Responsible Innovations in the Management of Financial Risks to the Projects of High-Tech Companies (using the Example of the IT Sphere) of Russia in 2022–2023

- ΔIT = 1,983,738,500,417.60/1,319,593,124,490.40 = 1.50;

- ΔMOEXINN = 71,812,769,937.11/17,016,847,943.33 = 4.12;

- ΔMRRT = 34,599,151,372,166.40/28,586,141,537,287.80 = 1.21.

4.2. Case Experience of Implementing ESG Projects on Responsible Innovations in High-Tech Companies of Russia (using the Example of the IT Sphere in 2022–2023)

5. Conclusions and Their Discussion and Significance

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

Appendix A

{kind=link}

| Date | Information Technology Index (IT), Rubles | Moscow Exchange Innovations Index (MOEXINN), Rubles | Index “Responsibility and Transparency” (MRRT), Rubles | |||

|---|---|---|---|---|---|---|

| Value | Daily Gain | Value | Daily Gain | Value | Daily Gain | |

| 24.11.2023 | 198,373,850,0417.60 | 16,558,888,566.00 | 71,812,769,937.11 | 384,970,094.21 | 34,599,151,372,166.40 | −93,507,875,109.70 |

| 23.11.2023 | 200,0297,388,983.60 | 9,122,873,962.80 | 71,427,799,842.90 | −1,426,477,090.77 | 34,692,659,247,276.10 | −132,452,554,324.30 |

| 22.11.2023 | 2,009,420,262,946.40 | −4,629,739,177.60 | 72,854,276,933.67 | 1,022,196,799.89 | 34,825,111,801,600.40 | 43,618,991,975.30 |

| 21.11.2023 | 2,004,790,523,768.80 | −36,396,628,064.20 | 71,832,080,133.79 | 262,673,700.61 | 34,781,492,809,625.10 | 62,388,259,062.40 |

| 20.11.2023 | 1,968,393,895,704.60 | −27,633,453,880.20 | 71,569,406,433.17 | −967,676,561.80 | 34,719,104,550,562.70 | −49,435,132,814.80 |

| 17.11.2023 | 1,940,760,441,824.40 | 3,840,132,267.20 | 72,537,082,994.97 | −803,365,555.31 | 34,768,539,683,377.50 | 86,870,232,992.50 |

| 16.11.2023 | 1,944,600,574,091.60 | −4,214,585,046.70 | 73,340,448,550.28 | 1,959,109,408.25 | 34,681,669,450,385.00 | −359,937,554,867.40 |

| 15.11.2023 | 1,940,385,989,044.90 | −186,002,128.50 | 71,381,339,142.03 | 2,398,791,329.19 | 35,041,607,005,252.40 | −127,540,255,235.10 |

| 14.11.2023 | 1,940,199,986,916.40 | −12,950,287,458.40 | 68,982,547,812.84 | −4,314,826,955.98 | 35,169,147,260,487.50 | −398,181,796,266.10 |

| 13.11.2023 | 1,927,249,699,458.00 | −410,999,268.40 | 73,297,374,768.82 | −3,508,192,345.47 | 35,567,329,056,753.60 | 51,351,139,966.40 |

| 10.11.2023 | 1,926,838,700,189.60 | 23,619,158,411.00 | 76,805,567,114.29 | −1,846,789,939.05 | 35,515,977,916,787.20 | 96,909,097,880.41 |

| 09.11.2023 | 1,950,457,858,600.60 | 11,976,022,438.70 | 78,652,357,053.34 | −1,200,089,456.46 | 35,419,068,818,906.80 | −62,664,178,146.91 |

| 08.11.2023 | 1,962,433,881,039.30 | 1,869,307,372.30 | 79,852,446,509.80 | −334,356,237.44 | 35,481,732,997,053.70 | −139,246,086,979.59 |

| 07.11.2023 | 1,964,303,188,411.60 | −3,909,712,225.80 | 80,186,802,747.24 | −605,464,406.95 | 35,620,979,084,033.30 | 52,662,036,026.09 |

| 06.11.2023 | 1,960,393,476,185.80 | −16,500,317,848.60 | 80,792,267,154.19 | 848,991,384.59 | 35,568,317,048,007.20 | 267,855,789,874.00 |

| 03.11.2023 | 1,943,893,158,337.20 | −10,325,591,733.90 | 79,943,275,769.60 | −127,388,798.37 | 35,300,461,258,133.20 | 75,330,823,446.20 |

| 02.11.2023 | 1,933,567,566,603.30 | 9,776,067,648.30 | 80,070,664,567.98 | −1,796,782,404.69 | 35,225,130,434,687.00 | −127,832,825,196.80 |

| 01.11.2023 | 1,943,343,634,251.60 | −12,308,256,795.90 | 81,867,446,972.67 | 2,148,089,738.64 | 35,352,963,259,883.80 | 83,133,383,979.00 |

| 31.10.2023 | 1,931,035,377,455.70 | 15,995,401,506.10 | 79,719,357,234.03 | −999,008,444.02 | 35,269,829,875,904.80 | −345,482,490,854.10 |

| 30.10.2023 | 1,947,030,778,961.80 | 21,288,908,327.80 | 80,718,365,678.05 | 126,447,739.76 | 35,615,312,366,758.90 | 2,612,968,686.90 |

| 27.10.2023 | 1,968,319,687,289.60 | 14,998,807,629.40 | 80,591,917,938.29 | −107,298,942.11 | 35,612,699,398,072.00 | 46,930,844,693.50 |

| 26.10.2023 | 1,983,318,494,919.00 | 29,862,703,289.30 | 80,699,216,880.40 | −2,255,814,811.86 | 35,565,768,553,378.50 | −321,365,756,200.10 |

| 25.10.2023 | 2,013,181,198,208.30 | −12,693,315,436.90 | 82,955,031,692.26 | 542,732,191.49 | 35,887,134,309,578.60 | −48,008,295,818.30 |

| 24.10.2023 | 2,000,487,882,771.40 | 3,403,216,072.20 | 82,412,299,500.77 | −269,230,109.14 | 35,935,142,605,396.90 | −143,825,964,831.60 |

| 23.10.2023 | 2,003,891,098,843.60 | 8,904,323,064.00 | 82,681,529,609.90 | −432,799,253.09 | 36,078,968,570,228.50 | −176,034,927,822.00 |

| 20.10.2023 | 2,012,795,421,907.60 | 5,670,548,059.20 | 83,114,328,862.99 | −819,184,188.92 | 36,255,003,498,050.50 | 325,143,707,824.20 |

| 19.10.2023 | 2,018,465,969,966.80 | −56,207,032,974.50 | 83,933,513,051.91 | 112,248,357.34 | 35,929,859,790,226.30 | 80,852,447,479.40 |

| 18.10.2023 | 1,962,258,936,992.30 | 1,107,945,505.70 | 83,821,264,694.57 | 176,815,472.77 | 35,849,007,342,746.90 | 165,441,322,805.80 |

| 17.10.2023 | 1,963,366,882,498.00 | 14,294,452,295.80 | 83,644,449,221.80 | −1,120,830,098.21 | 35,683,566,019,941.10 | 104,324,112,285.50 |

| 16.10.2023 | 1,977,661,334,793.80 | −10,787,661,128.90 | 84,765,279,320.01 | 8,303,938.56 | 35,579,241,907,655.60 | 483,431,964,159.40 |

| 13.10.2023 | 1,966,873,673,664.90 | −19,009,898,372.50 | 84,756,975,381.45 | 798,268,617.04 | 35,095,809,943,496.20 | 206,961,900,255.40 |

| 12.10.2023 | 1,947,863,775,292.40 | 15,408,832,903.60 | 83,958,706,764.42 | −732,276,630.97 | 34,888,848,043,240.80 | −235,860,052,424.90 |

| 11.10.2023 | 1,963,272,608,196.00 | −14,530,348,759.10 | 84,690,983,395.38 | −110,081,658.13 | 35,124,708,095,665.70 | 231,594,652,172.50 |

| 10.10.2023 | 1,948,742,259,436.90 | −13,198,039,357.30 | 84,801,065,053.51 | −582,560,466.94 | 34,893,113,443,493.20 | −94,609,542,627.10 |

| 09.10.2023 | 1,935,544,220,079.60 | −4,582,073,340.10 | 85,383,625,520.45 | 3,201,507,567.62 | 34,987,722,986,120.30 | 450,507,671,552.60 |

| 06.10.2023 | 1,930,962,146,739.50 | −15,803,677,819.00 | 82,182,117,952.83 | −1,504,512,834.66 | 34,537,215,314,567.70 | 119,402,663,407.80 |

| 05.10.2023 | 1,915,158,468,920.50 | −23,171,246,124.10 | 83,686,630,787.49 | −776,341,469.49 | 34,417,812,651,159.90 | −51,108,700,771.90 |

| 04.10.2023 | 1,891,987,222,796.40 | −3,096,563,199.60 | 84,462,972,256.97 | 406,887,290.37 | 34,468,921,351,931.80 | −42,870,836,504.40 |

| 03.10.2023 | 1,888,890,659,596.80 | −4,021,931,438.40 | 84,056,084,966.60 | −1,030,832,452.10 | 34,511,792,188,436.20 | 117,037,301,454.50 |

| 02.10.2023 | 1,884,868,728,158.40 | 6,697,874,233.10 | 85,086,917,418.71 | 614,764,320.23 | 34,394,754,886,981.70 | 21,407,980,734.30 |

| 29.09.2023 | 1,891,566,602,391.50 | 17,726,599,093.90 | 84,472,153,098.47 | −1,173,693,008.87 | 34,373,346,906,247.40 | 106,899,297,572.60 |

| 28.09.2023 | 1,909,293,201,485.40 | −17,234,312,355.30 | 85,645,846,107.34 | −92,500,344.88 | 34,266,447,608,674.80 | 450,454,510,588.70 |

| 27.09.2023 | 1,892,058,889,130.10 | −32,547,317,209.70 | 85,738,346,452.22 | 68,705,857.56 | 33,815,993,098,086.10 | 232,304,327,412.70 |

| 26.09.2023 | 1,859,511,571,920.40 | −1,770,778,842.60 | 85,669,640,594.66 | 571,955,790.07 | 33,583,688,770,673.40 | 43,290,394,036.50 |

| 25.09.2023 | 1,857,740,793,077.80 | −3,695,850,096.40 | 85,097,684,804.59 | 1,317,259,219.53 | 33,540,398,376,636.90 | 19,335,154,104.80 |

| 22.09.2023 | 1,854,044,942,981.40 | −5,081,218,324.00 | 83,780,425,585.06 | −1,331,809,816.30 | 33,521,063,222,532.10 | 293,207,453,369.00 |

| 21.09.2023 | 1,848,963,724,657.40 | 26,663,026,714.00 | 85,112,235,401.36 | 557,768,741.77 | 33,227,855,769,163.10 | −595,945,650,707.20 |

| 20.09.2023 | 1,875,626,751,371.40 | 38,354,864,337.80 | 84,554,466,659.59 | −2,539,648,324.27 | 33,823,801,419,870.30 | −233,149,372,003.50 |

| 19.09.2023 | 1,913,981,615,709.20 | 34,585,357,342.60 | 87,094,114,983.86 | −3,015,113,704.20 | 34,056,950,791,873.80 | −493,034,166,367.80 |

| 18.09.2023 | 1,948,566,973,051.80 | 38,717,316,174.80 | 90,109,228,688.06 | 309,746,684.64 | 34,549,984,958,241.60 | −239,489,262,527.50 |

| 15.09.2023 | 1,987,284,289,226.60 | −50,260,878,269.90 | 89,799,482,003.42 | 4,110,481,187.06 | 34,789,474,220,769.10 | 158,005,189,462.80 |

| 14.09.2023 | 1,937,023,410,956.70 | 19,229,628,715.90 | 85,689,000,816.35 | −6,153,513,921.14 | 34,631,469,031,306.30 | −56,583,848,868.20 |

| 13.09.2023 | 1,956,253,039,672.60 | 16,173,151,880.50 | 91,842,514,737.49 | −1,706,097,153.31 | 34,688,052,880,174.50 | −198,639,171,036.90 |

| 12.09.2023 | 1,972,426,191,553.10 | −45,326,003,901.10 | 93,548,611,890.80 | 2,246,706,845.88 | 34,886,692,051,211.40 | 392,766,005,335.80 |

| 11.09.2023 | 1,927,100,187,652.00 | 47,458,755,193.80 | 91,301,905,044.92 | −1,636,448,688.13 | 34,493,926,045,875.60 | −186,462,887,745.00 |

| 08.09.2023 | 1,974,558,942,845.80 | 16,830,980,118.40 | 92,938,353,733.05 | −222,162,132.68 | 34,680,388,933,620.60 | −322,287,632,337.30 |

| 07.09.2023 | 1,991,389,922,964.20 | 64,198,365,259.50 | 93,160,515,865.72 | −3,101,379,854.08 | 35,002,676,565,957.90 | −798,883,661,552.00 |

| 06.09.2023 | 2,055,588,288,223.70 | 45,747,265,674.10 | 96,261,895,719.80 | −2,340,583,586.45 | 35,801,560,227,509.90 | −142,541,738,383.60 |

| 05.09.2023 | 2,101,335,553,897.80 | −952,786,385.80 | 98,602,479,306.26 | 3,444,091,921.55 | 35,944,101,965,893.50 | 28,628,181,846.60 |

| 04.09.2023 | 2,100,382,767,512.00 | −34,810,847,922.00 | 95,158,387,384.71 | 4,183,037,841.95 | 35,915,473,784,046.90 | 402,836,397,994.60 |

| 01.09.2023 | 2,065,571,919,590.00 | −5,953,330,450.60 | 90,975,349,542.76 | 3,470,454,770.03 | 35,512,637,386,052.30 | 68,198,106,848.20 |

| 31.08.2023 | 2,059,618,589,139.40 | −2,315,401,023.40 | 87,504,894,772.73 | −2,116,857,186.49 | 35,444,439,279,204.10 | 174,932,559,621.10 |

| 30.08.2023 | 2,057,303,188,116.00 | 6,182,409,526.00 | 89,621,751,959.22 | −3,126,468,025.09 | 35,269,506,719,583.00 | 211,075,372,759.30 |

| 29.08.2023 | 2,063,485,597,642.00 | 9,342,540,266.00 | 92,748,219,984.31 | 9,700,520,958.96 | 35,058,431,346,823.70 | 36,808,284,021.20 |

| 28.08.2023 | 2,072,828,137,908.00 | −31,783,007,863.20 | 83,047,699,025.34 | 9,613,781,167.80 | 35,021,623,062,802.50 | 356,450,750,617.50 |

| 25.08.2023 | 2,041,045,130,044.80 | −11,643,914,759.60 | 73,433,917,857.54 | 1,774,473,143.29 | 34,665,172,312,185.00 | 206,407,266,856.90 |

| 24.08.2023 | 2,029,401,215,285.20 | 11,982,912,990.10 | 71,659,444,714.25 | −152,335,011.19 | 34,458,765,045,328.10 | −125,316,578,187.00 |

| 23.08.2023 | 2,041,384,128,275.30 | 4,492,955,802.50 | 71,811,779,725.44 | 1,060,097,844.23 | 34,584,081,623,515.10 | −180,549,930,282.70 |

| 22.08.2023 | 2,045,877,084,077.80 | −48,511,149,828.00 | 70,751,681,881.21 | 827,456,964.43 | 34,764,631,553,797.80 | 258,732,648,966.00 |

| 21.08.2023 | 1,997,365,934,249.80 | −41,051,483,380.20 | 69,924,224,916.78 | 1,116,093,491.85 | 34,505,898,904,831.80 | 254,364,894,449.80 |

| 18.08.2023 | 1,956,314,450,869.60 | −48,008,712,894.60 | 68,808,131,424.93 | 5,990,844,355.48 | 34,251,534,010,382.00 | 568,654,719,173.20 |

| 17.08.2023 | 1,908,305,737,975.00 | −9,356,354,607.60 | 62,817,287,069.45 | 702,778,357.75 | 33,682,879,291,208.80 | 164,357,842,252.70 |

| 16.08.2023 | 1,898,949,383,367.40 | 48,957,868,539.10 | 62,114,508,711.70 | −1,246,497,177.17 | 33,518,521,448,956.10 | −744,658,734,788.70 |

| 15.08.2023 | 1,947,907,251,906.50 | 14,781,585,861.90 | 63,361,005,888.87 | 834,351,562.17 | 34,263,180,183,744.80 | −181,855,141,191.40 |

| 14.08.2023 | 1,962,688,837,768.40 | 17,993,670,142.20 | 62,526,654,326.69 | −676,764,809.67 | 34,445,035,324,936.20 | −76,694,132,126.00 |

| 11.08.2023 | 1,980,682,507,910.60 | 9,073,974,028.50 | 63,203,419,136.37 | 1,430,816,341.64 | 34,521,729,457,062.20 | 129,371,434,957.30 |

| 10.08.2023 | 1,989,756,481,939.10 | −35,771,747,942.50 | 61,772,602,794.73 | 785,273,705.27 | 34,392,358,022,104.90 | 530,128,380,902.60 |

| 09.08.2023 | 1,953,984,733,996.60 | −1,655,919,221.60 | 60,987,329,089.45 | 538,788,943.76 | 33,862,229,641,202.30 | 213,307,729,520.00 |

| 08.08.2023 | 1,952,328,814,775.00 | −11,432,080,807.50 | 60,448,540,145.69 | −371,946,425.55 | 33,648,921,911,682.30 | −29,663,277,419.50 |

| 07.08.2023 | 1,940,896,733,967.50 | −12,624,207,097.60 | 60,820,486,571.25 | −161,014,703.03 | 33,678,585,189,101.80 | −70,541,212,938.20 |

| 04.08.2023 | 1,928,272,526,869.90 | 37,566,941,739.30 | 60,981,501,274.28 | −1,191,561,590.27 | 33,749,126,402,040.00 | −529,416,754,060.90 |

| 03.08.2023 | 1,965,839,468,609.20 | −72,439,922,624.50 | 62,173,062,864.55 | 755,501,122.02 | 34,278,543,156,100.90 | 540,841,371,929.50 |

| 02.08.2023 | 1,893,399,545,984.70 | −8,234,753,264.40 | 61,417,561,742.53 | −41,637,491.26 | 33,737,701,784,171.40 | 195,281,466,232.20 |

| 01.08.2023 | 1,885,164,792,720.30 | −16,717,441,791.40 | 61,459,199,233.78 | 694,670,402.68 | 33,542,420,317,939.20 | 94,843,287,075.20 |

| 31.07.2023 | 1,868,447,350,928.90 | −2,540,679,949.60 | 60,764,528,831.10 | 35,440,588.71 | 33,447,577,030,864.00 | 581,695,266,083.90 |

| 28.07.2023 | 1,865,906,670,979.30 | −6,105,652,479.20 | 60,729,088,242.39 | 27,334,255.55 | 32,865,881,764,780.10 | 204,107,882,761.30 |

| 27.07.2023 | 1,859,801,018,500.10 | −9,587,268,744.10 | 60,701,753,986.84 | 549,248,787.81 | 32,661,773,882,018.80 | 227,256,957,401.20 |

| 26.07.2023 | 1,850,213,749,756.00 | −17,226,083,699.10 | 60,152,505,199.03 | −1,162,181,548.42 | 32,434,516,924,617.60 | 2,688,777,028.40 |

| 25.07.2023 | 1,832,987,666,056.90 | −37,569,368,884.90 | 61,314,686,747.46 | 638,149,026.01 | 32,431,828,147,589.20 | 403,141,329,206.00 |

| 24.07.2023 | 1,795,418,297,172.00 | −66,128,890,201.20 | 60,676,537,721.45 | 656,812,528.29 | 32,028,686,818,383.20 | 84,392,818,083.00 |

| 21.07.2023 | 1,729,289,406,970.80 | −6,026,627,693.70 | 60,019,725,193.16 | 590,626,582.21 | 31,944,294,000,300.20 | 31,713,939,473.10 |

| 20.07.2023 | 1,723,262,779,277.10 | 24,248,531,444.40 | 59,429,098,610.96 | −690,359,949.70 | 31,912,580,060,827.10 | −294,227,381,606.10 |

| 19.07.2023 | 1,747,511,310,721.50 | 13,110,432,023.60 | 60,119,458,560.66 | 32,437,713.67 | 32,206,807,442,433.20 | −64,364,091,056.40 |

| 18.07.2023 | 1,760,621,742,745.10 | −21,835,997,933.70 | 60,087,020,846.99 | 238,559,140.93 | 32,271,171,533,489.60 | 448,898,278,413.70 |

| 17.07.2023 | 1,738,785,744,811.40 | −13,355,745,950.80 | 59,848,461,706.06 | 823,015,570.66 | 31,822,273,255,075.90 | 237,938,064,904.80 |

| 14.07.2023 | 1,725,429,998,860.60 | −47,286,846,297.60 | 59,025,446,135.40 | 669,596,439.38 | 31,584,335,190,171.10 | 225,122,170,215.00 |

| 13.07.2023 | 1,678,143,152,563.00 | 5,848,370,194.60 | 58,355,849,696.03 | −300,687,919.81 | 31,359,213,019,956.10 | −103,640,678,548.60 |

| 12.07.2023 | 1,683,991,522,757.60 | −29,772,176,601.40 | 58,656,537,615.84 | 381,068,641.32 | 31,462,853,698,504.70 | 498,506,523,887.10 |

| 11.07.2023 | 1,654,219,346,156.20 | −16,429,211,637.70 | 58,275,468,974.52 | 561,281,429.70 | 30,964,347,174,617.60 | 18,075,416,189.60 |

| 10.07.2023 | 1,637,790,134,518.50 | −22,077,492,605.90 | 57,714,187,544.82 | 567,698,406.46 | 30,946,271,758,428.00 | 142,293,580,378.80 |

| 07.07.2023 | 1,615,712,641,912.60 | 7,919,922,702.90 | 57,146,489,138.36 | 312,614,354.07 | 30,803,978,178,049.20 | 234,421,263,748.00 |

| 06.07.2023 | 1,623,632,564,615.50 | 1,928,236,662.60 | 56,833,874,784.29 | −668,288,435.28 | 30,569,556,914,301.20 | 270,651,549,883.90 |

| 05.07.2023 | 1,625,560,801,278.10 | −2,022,929,130.10 | 57,502,163,219.56 | −502,781,845.69 | 30,298,905,364,417.30 | −63,457,232,792.30 |

| 04.07.2023 | 1,623,537,872,148.00 | 5,784,242,962.90 | 58,004,945,065.25 | −447,985,540.16 | 30,362,362,597,209.60 | 201,772,671,456.50 |

| 03.07.2023 | 1,629,322,115,110.90 | 22,846,537,618.60 | 58,452,930,605.42 | −350,312,167.05 | 30,160,589,925,753.10 | −181,215,034,874.30 |

| 30.06.2023 | 1,652,168,652,729.50 | 12,802,956,846.10 | 58,803,242,772.47 | 421,989,680.75 | 30,341,804,960,627.40 | 30,788,009,553.50 |

| 29.06.2023 | 1,664,971,609,575.60 | −5,917,457,959.60 | 58,381,253,091.72 | −62,031,857.10 | 30,311,016,951,073.90 | 61,566,370,948.50 |

| 28.06.2023 | 1,659,054,151,616.00 | −6,582,672,629.60 | 58,443,284,948.81 | −168,330,766.47 | 30,249,450,580,125.40 | −16,857,467,366.40 |

| 27.06.2023 | 1,652,471,478,986.40 | −33,250,447,035.40 | 58,611,615,715.29 | 126,429,657.78 | 30,266,308,047,491.80 | 118,499,772,562.50 |

| 26.06.2023 | 1,619,221,031,951.00 | 46,329,349,807.00 | 58,485,186,057.51 | −862,018,910.52 | 30,147,808,274,929.30 | −410,678,977,495.30 |

| 23.06.2023 | 1,665,550,381,758.00 | 35,834,133,761.00 | 59,347,204,968.03 | −61,696,518.37 | 30,558,487,252,424.60 | −201,803,325,224.50 |

| 22.06.2023 | 1,701,384,515,519.00 | 1,584,302,775.90 | 59,408,901,486.40 | 448,212,903.71 | 30,760,290,577,649.10 | −52,540,279,695.10 |

| 21.06.2023 | 1,702,968,818,294.90 | −26,317,364,198.90 | 58,960,688,582.69 | 242,106,933.06 | 30,812,830,857,344.20 | 132,245,270,913.20 |

| 20.06.2023 | 1,676,651,454,096.00 | 4,991,056,842.00 | 58,718,581,649.63 | 606,015,096.89 | 30,680,585,586,431.00 | −182,164,276,581.00 |

| 19.06.2023 | 1,681,642,510,938.00 | 15,843,275,417.60 | 58,112,566,552.74 | −453,266,764.02 | 30,862,749,863,012.00 | 165,694,342,802.20 |

| 16.06.2023 | 1,697,485,786,355.60 | 55,492,610,802.20 | 58,565,833,316.76 | −7,406,495,887.52 | 30,697,055,520,209.80 | 63,804,995,241.30 |

| 15.06.2023 | 1,752,978,397,157.80 | 5,234,784,568.70 | 65,972,329,204.28 | −219,659,953.97 | 30,633,250,524,968.50 | 425,248,163,166.70 |

| 14.06.2023 | 1,758,213,181,726.50 | −29,451,080,593.40 | 66,191,989,158.25 | −210,570,412.43 | 30,208,002,361,801.80 | −32,317,950,656.30 |

| 13.06.2023 | 1,728,762,101,133.10 | −28,788,026,300.30 | 66,402,559,570.68 | −137,091,242.22 | 30,240,320,312,458.10 | 610,024,207,481.80 |

| 09.06.2023 | 1,699,974,074,832.80 | 9,634,053,998.20 | 66,539,650,812.89 | 1,206,162,849.16 | 29,630,296,104,976.30 | 21,713,045,562.90 |

| 08.06.2023 | 1,709,608,128,831.00 | −55,241,405,333.90 | 65,333,487,963.74 | 1,572,544,949.34 | 29,608,583,059,413.40 | 116,774,991,538.60 |

| 07.06.2023 | 1,654,366,723,497.10 | −61,946,913,604.30 | 63,760,943,014.39 | 1,585,758,685.85 | 29,491,808,067,874.80 | 136,638,478,681.80 |

| 06.06.2023 | 1,592,419,809,892.80 | −17,645,386,749.50 | 62,175,184,328.54 | −272,259,317.22 | 29,355,169,589,193.00 | −225,943,603,780.70 |

| 05.06.2023 | 1,574,774,423,143.30 | 11,008,098,801.30 | 62,447,443,645.76 | −171,148,002.83 | 29,581,113,192,973.70 | −84,365,717,686.40 |

| 02.06.2023 | 1,585,782,521,944.60 | −12,773,688,295.10 | 62,618,591,648.59 | 387,496,974.93 | 29,665,478,910,660.10 | 21,574,018,150.40 |

| 01.06.2023 | 1,573,008,833,649.50 | −3,749,781,534.50 | 62,231,094,673.67 | −60,370,843.62 | 29,643,904,892,509.70 | 164,138,127,235.00 |

| 31.05.2023 | 1,569,259,052,115.00 | −18,728,908,854.50 | 62,291,465,517.29 | 1,186,783,250.58 | 29,479,766,765,274.70 | 272,121,367,935.40 |

| 30.05.2023 | 1,550,530,143,260.50 | 39,203,906,834.70 | 61,104,682,266.71 | −774,831,344.70 | 29,207,645,397,339.30 | −174,895,577,251.70 |

| 29.05.2023 | 1,589,734,050,095.20 | −34,045,005,444.90 | 61,879,513,611.42 | 702,541,288.87 | 29,382,540,974,591.00 | 372,488,585,119.60 |

| 26.05.2023 | 1,555,689,044,650.30 | −21,878,862,887.70 | 61,176,972,322.54 | 390,632,052.18 | 29,010,052,389,471.40 | 255,789,928,453.50 |

| 25.05.2023 | 1,533,810,181,762.60 | −19,942,598,868.60 | 60,786,340,270.36 | 750,984,037.63 | 28,754,262,461,017.90 | −64,346,471,399.50 |

| 24.05.2023 | 1,513,867,582,894.00 | −9,077,567,791.00 | 60,035,356,232.73 | 1,084,555,472.22 | 28,818,608,932,417.40 | 29,912,793,978.10 |

| 23.05.2023 | 1,504,790,015,103.00 | −6,593,942,972.00 | 58,950,800,760.51 | 91,190,084.47 | 28,788,696,138,439.30 | 53,332,434,756.20 |

| 22.05.2023 | 1,498,196,072,131.00 | −16,864,641,642.80 | 58,859,610,676.04 | 103,044,034.56 | 28,735,363,703,683.10 | 109,120,579,929.50 |

| 19.05.2023 | 1,481,331,430,488.20 | −66,361,865,285.80 | 58,756,566,641.48 | −456,261,144.62 | 28,626,243,123,753.60 | −128,482,035,363.00 |

| 18.05.2023 | 1,414,969,565,202.40 | −2,102,129,623.80 | 59,212,827,786.11 | 43,549,778.81 | 28,754,725,159,116.60 | −1,366,238,547.10 |

| 17.05.2023 | 1,412,867,435,578.60 | −6,578,285,246.60 | 59,169,278,007.29 | 325,684,091.88 | 28,756,091,397,663.70 | −33,800,054,875.10 |

| 16.05.2023 | 1,406,289,150,332.00 | −6,905,404,209.00 | 58,843,593,915.41 | −286,086,840.37 | 28,789,891,452,538.80 | 275,418,002,628.20 |

| 15.05.2023 | 1,399,383,746,123.00 | −20,514,132,587.80 | 59,129,680,755.78 | 693,377,075.42 | 28,514,473,449,910.60 | 490,963,088,038.90 |

| 12.05.2023 | 1,378,869,613,535.20 | 17,936,045,500.00 | 58,436,303,680.36 | −874,993,482.63 | 28,023,510,361,871.70 | −243,915,306,414.20 |

| 11.05.2023 | 1,396,805,659,035.20 | −22,180,643,934.90 | 59,311,297,162.98 | 1241,597,156.57 | 28,267,425,668,285.90 | 294,538,864,466.30 |

| 10.05.2023 | 1,374,625,015,100.30 | −46,755,246,017.90 | 58,069,700,006.41 | 1,755,657,411.10 | 27,972,886,803,819.60 | 670,450,291,276.80 |

| 08.05.2023 | 1,327,869,769,082.40 | 20,294,346,246.30 | 56,314,042,595.31 | −432,478,417.59 | 27,302,436,512,542.80 | −111,718,626,030.30 |

| 05.05.2023 | 1,348,164,115,328.70 | −10,083,653,137.30 | 56,746,521,012.90 | 88,772,273.95 | 27,414,155,138,573.10 | 103,797,506,376.40 |

| 04.05.2023 | 1,338,080,462,191.40 | 9,521,292,481.80 | 56,657,748,738.96 | 761,401,921.32 | 27,310,357,632,196.70 | −67,995,473,336.50 |

| 03.05.2023 | 1,347,601,754,673.20 | 26,719,121,289.10 | 55,896,346,817.64 | −1,101,712,227.28 | 27,378,353,105,533.20 | −570,134,543,334.90 |

| 02.05.2023 | 1,374,320,875,962.30 | 44,780,070,313.20 | 56,998,059,044.92 | −2,479,218,403.33 | 27,948,487,648,868.10 | −725,019,473,104.90 |

| 28.04.2023 | 1,419,100,946,275.50 | 10,466,399,502.70 | 59,477,277,448.25 | 100,850,133.74 | 28,673,507,121,973.00 | −150,598,922,354.00 |

| 27.04.2023 | 1,429,567,345,778.20 | 729,266,317.80 | 59,376,427,314.51 | −264,869,777.20 | 28,824,106,044,327.00 | 193,696,621,988.90 |

| 26.04.2023 | 1,430,296,612,096.00 | −13,537,785,026.20 | 59,641,297,091.71 | −249,874,447.72 | 28,630,409,422,338.10 | −56,179,694,260.30 |

| 25.04.2023 | 1,416,758,827,069.80 | 4,464,041,773.80 | 59,891,171,539.43 | −68,177,418.56 | 28,686,589,116,598.40 | −145,726,262,256.60 |

| 24.04.2023 | 1,421,222,868,843.60 | 10,206,801,643.90 | 59,959,348,957.99 | 1,623,847,723.80 | 28,832,315,378,855.00 | −60,553,800,039.50 |

| 21.04.2023 | 1,431,429,670,487.50 | −14,631,381,327.20 | 58,335,501,234.19 | 575,502,308.79 | 28,892,869,178,894.50 | 14,942,950,065.80 |

| 20.04.2023 | 1,416,798,289,160.30 | −32,713,623,495.20 | 57,759,998,925.40 | −372,743,577.96 | 28,877,926,228,828.70 | 225,447,515,375.50 |

| 19.04.2023 | 1,384,084,665,665.10 | 2,249,893,850.80 | 58,132,742,503.36 | −220,837,253.34 | 28,652,478,713,453.20 | −144,435,226,480.10 |

| 18.04.2023 | 1,386,334,559,515.90 | −10,943,329,703.50 | 58,353,579,756.70 | 52,956,928.92 | 28,796,913,939,933.30 | 156,288,498,844.40 |

| 17.04.2023 | 1,375,391,229,812.40 | −19,172,224,709.20 | 58,300,622,827.77 | 653,528,503.80 | 28,640,625,441,088.90 | 415,835,293,761.60 |

| 14.04.2023 | 1,356,219,005,103.20 | 48,865,929.20 | 57,647,094,323.98 | 430,015,192.76 | 28,224,790,147,327.30 | 180,361,985,674.70 |

| 13.04.2023 | 1,356,267,871,032.40 | 10,748,917,208.40 | 57,217,079,131.21 | −928,110,859.78 | 28,044,428,161,652.60 | 123,165,198,943.00 |

| 12.04.2023 | 1,367,016,788,240.80 | 6,144,061,909.10 | 58,145,189,990.99 | 654,637,417.59 | 27,921,262,962,709.60 | 91,227,456,478.40 |

| 11.04.2023 | 1,373,160,850,149.90 | 23,737,239,546.20 | 57,490,552,573.40 | −373,199,386.88 | 27,830,035,506,231.20 | −161,668,926,489.80 |

| 10.04.2023 | 1,396,898,089,696.10 | −40,563,553,527.60 | 57,863,751,960.29 | 1875,482,114.72 | 27,991,704,432,721.00 | 347,699,091,017.70 |

| 07.04.2023 | 1,356,334,536,168.50 | 1,024,913,399.50 | 55,988,269,845.56 | 8,985,465.67 | 27,644,005,341,703.30 | 77,387,981,435.00 |

| 06.04.2023 | 1,357,359,449,568.00 | 7,241,139,065.30 | 55,979,284,379.89 | 577,446,600.70 | 27,566,617,360,268.30 | −18,314,159,831.70 |

| 05.04.2023 | 1,364,600,588,633.30 | −7,347,406,973.40 | 55,401,837,779.19 | −101,048,389.32 | 27,584,931,520,100.00 | 218,395,470,930.50 |

| 04.04.2023 | 1,357,253,181,659.90 | 19,586,118,832.10 | 55,502,886,168.52 | −18,945,140.69 | 27,366,536,049,169.50 | 116,127,363,783.70 |

| 03.04.2023 | 1,376,839,300,492.00 | −25,806,124,318.50 | 55,521,831,309.21 | 190,420,494.45 | 27,250,408,685,385.80 | 284,016,246,371.50 |

| 31.03.2023 | 1,351,033,176,173.50 | 10,422,151,387.50 | 55,331,410,814.76 | 297,509,019.87 | 26,966,392,439,014.30 | −146,592,783,855.40 |

| 30.03.2023 | 1,361,455,327,561.00 | −8,904,037,880.80 | 55,033,901,794.89 | 952,201,859.24 | 27,112,985,222,869.70 | 56,775,728,369.50 |

| 29.03.2023 | 1,352,551,289,680.20 | −2,446,496,518.70 | 54,081,699,935.65 | 214,645,624.66 | 27,056,209,494,500.20 | 139,580,460,357.80 |

| 28.03.2023 | 1,350,104,793,161.50 | −2,082,087,979.40 | 53,867,054,310.99 | −226,990,374.55 | 26,916,629,034,142.40 | −110,834,980,218.60 |

| 27.03.2023 | 1,348,022,705,182.10 | −30,150,973,341.50 | 54,094,044,685.54 | 813,879,246.70 | 27,027,464,014,361.00 | 470,311,999,792.30 |

| 24.03.2023 | 1,317,871,731,840.60 | 4,447,484,536.40 | 53,280,165,438.83 | 9,912,295.35 | 26,557,152,014,568.70 | 55,971,481,996.00 |

| 23.03.2023 | 1,322,319,216,377.00 | −8,226,772,603.80 | 53,270,253,143.48 | 383,050,340.02 | 26,501,180,532,572.70 | −72,695,528,196.60 |

| 22.03.2023 | 1,314,092,443,773.20 | 5,861,484,617.70 | 52,887,202,803.47 | 438,379,146.50 | 26,573,876,060,769.30 | 49,595,879,289.60 |

| 21.03.2023 | 1,319,953,928,390.90 | 8,330,563,255.70 | 52,448,823,656.97 | 298,255,819.48 | 26,524,280,181,479.70 | −72,394,287,551.40 |

| 20.03.2023 | 1,328,284,491,646.60 | −6,289,688,280.90 | 52,150,567,837.48 | 119,805,081.92 | 26,596,674,469,031.10 | 776,132,746,400.30 |

| 17.03.2023 | 1,321,994,803,365.70 | −25,409,679,942.00 | 52,030,762,755.56 | −323,292,862.22 | 25,820,541,722,630.80 | 419,319,102,998.00 |

| 16.03.2023 | 1,296,585,123,423.70 | 26,017,466,827.70 | 52,354,055,617.78 | −644,832,266.45 | 25,401,222,619,632.80 | −7,728,686,189.30 |

| 15.03.2023 | 1,322,602,590,251.40 | 19,559,568,983.60 | 52,998,887,884.23 | −360,752,978.63 | 25,408,951,305,822.10 | −362,118,477,256.40 |

| 14.03.2023 | 1,342,162,159,235.00 | −18,337,053,036.90 | 53,359,640,862.86 | 188,918,140.03 | 25,771,069,783,078.50 | 120,871,530,123.40 |

| 13.03.2023 | 1,323,825,106,198.10 | 5,486,544,933.10 | 53,170,722,722.83 | 264,070,804.81 | 25,650,198,252,955.10 | −91,563,142,897.40 |

| 10.03.2023 | 1,329,311,651,131.20 | 10,686,984,651.70 | 52,906,651,918.02 | −212,279,764.73 | 25,741,761,395,852.50 | −115,377,774,219.50 |

| 09.03.2023 | 1,339,998,635,782.90 | 7,364,017,183.80 | 53,118,931,682.75 | 181,777,305.05 | 25,857,139,170,072.00 | −46,310,155,208.70 |

| 07.03.2023 | 1,347,362,652,966.70 | 9,722,885,284.90 | 52,937,154,377.70 | −233,527,261.80 | 25,903,449,325,280.70 | −22,981,167,110.70 |

| 06.03.2023 | 1,357,085,538,251.60 | −10,088,910,645.20 | 53,170,681,639.50 | 670,785,032.81 | 25,926,430,492,391.40 | 245,467,723,977.40 |

| 03.03.2023 | 1,346,996,627,606.40 | −10,052,587,827.30 | 52,499,896,606.69 | 561,124,713.78 | 25,680,962,768,414.00 | 236,407,108,199.00 |

| 02.03.2023 | 1,336,944,039,779.10 | 27,445,568,737.90 | 51,938,771,892.90 | −885,793,606.87 | 25,444,555,660,215.00 | −296,366,968,717.40 |

| 01.03.2023 | 1,364,389,608,517.00 | −10,547,144,165.30 | 52,824,565,499.78 | 619,992,663.03 | 25,740,922,628,932.40 | 360,516,317,028.90 |

| 28.02.2023 | 1,353,842,464,351.70 | 1,139,018,820.60 | 52,204,572,836.74 | 271,326,436.12 | 25,380,406,311,903.50 | 105,488,633,225.90 |

| 27.02.2023 | 1,354,981,483,172.30 | −15,231,463,665.60 | 51,933,246,400.62 | 461,726,108.69 | 25,274,917,678,677.60 | 376,417,156,768.40 |

| 24.02.2023 | 1,339,750,019,506.70 | −7,721,971,513.50 | 51,471,520,291.93 | 296,296,174.84 | 24,898,500,521,909.20 | −152,131,622,318.40 |

| 22.02.2023 | 1,332,028,047,993.20 | −672,760,843.10 | 51,175,224,117.09 | 148,417,804.96 | 25,050,632,144,227.60 | 32,310,120,300.00 |

| 21.02.2023 | 1,331,355,287,150.10 | −33,150,230,875.60 | 51,026,806,312.13 | 1507,539,612.12 | 25,018,322,023,927.60 | 258,768,027,837.20 |

| 20.02.2023 | 1,298,205,056,274.50 | 4,038,484,269.00 | 49,519,266,700.01 | −253,952,789.63 | 24,759,553,996,090.40 | 189,656,736,384.90 |

| 17.02.2023 | 1,302,243,540,543.50 | 1,757,145,700.00 | 49,773,219,489.64 | −160,096,345.66 | 24,569,897,259,705.50 | 175,934,769,748.40 |

| 16.02.2023 | 1,304,000,686,243.50 | 578,405,741.30 | 49,933,315,835.30 | 1,413,119,571.59 | 24,393,962,489,957.10 | −134,648,379,443.20 |

| 15.02.2023 | 1,304,579,091,984.80 | 47,540,917,854.90 | 48,520,196,263.71 | −3,060,788,951.45 | 24,528,610,869,400.30 | −682,619,288,794.60 |

| 14.02.2023 | 1,352,120,009,839.70 | 20,427,152,480.50 | 51,580,985,215.15 | −999,764,218.08 | 25,211,230,158,194.90 | −355,181,472,669.70 |

| 13.02.2023 | 1,372,547,162,320.20 | −7,248,825,041.40 | 52,580,749,433.23 | 149,771,484.62 | 25,566,411,630,864.60 | 12,704,686,592.60 |

| 10.02.2023 | 1,365,298,337,278.80 | −1,396,858,611.70 | 52,430,977,948.61 | −449,025,722.73 | 25,553,706,944,272.00 | −5,928,827,945.10 |

| 09.02.2023 | 1,363,901,478,667.10 | 5,313,563,644.00 | 52,880,003,671.34 | 161,729,632.16 | 25,559,635,772,217.10 | 145,400,976,929.00 |

| 08.02.2023 | 1,369,215,042,311.10 | 18,753,978,710.90 | 52,718,274,039.18 | 979,017,339.29 | 25,414,234,795,288.10 | −185,136,253,836.30 |

| 07.02.2023 | 1,387,969,021,022.00 | 8,292,010,413.60 | 51,739,256,699.90 | 176,341,364.37 | 25,599,371,049,124.40 | 36,173,266,883.30 |

| 06.02.2023 | 1,396,261,031,435.60 | −17,665,371,896.60 | 51,562,915,335.53 | 1,110,000,538.49 | 25,563,197,782,241.10 | 224,963,940,181.30 |

| 03.02.2023 | 1,378,595,659,539.00 | 8,409,278,937.40 | 50,452,914,797.04 | −313,769,021.53 | 25,338,233,842,059.80 | 22,094,351,798.00 |

| 02.02.2023 | 1,387,004,938,476.40 | −15,640,715,994.60 | 50,766,683,818.57 | 89,761,690.69 | 25,316,139,490,261.80 | 78,970,973,816.30 |

| 01.02.2023 | 1,371,364,222,481.80 | 4,736,514,600.00 | 50,676,922,127.87 | −109,414,770.13 | 25,237,168,516,445.50 | 91,478,654,106.20 |

| 31.01.2023 | 1,376,100,737,081.80 | −38,381,711,415.20 | 50,786,336,898.00 | 1,140,257,022.12 | 25,145,689,862,339.30 | 140,056,445,894.40 |

| 30.01.2023 | 1,337,719,025,666.60 | −25,464,890,962.00 | 49,646,079,875.88 | 1,595,561,331.65 | 25,005,633,416,444.90 | 178,986,238,112.00 |

| 27.01.2023 | 1,312,254,134,704.60 | −16,006,509,298.00 | 48,050,518,544.23 | 300,496,183.12 | 24,826,647,178,332.90 | 245,533,670,475.10 |

| 26.01.2023 | 1,296,247,625,406.60 | 2,010,992,926.60 | 47,750,022,361.11 | 364,000,974.34 | 24,581,113,507,857.80 | −24,199,188,392.50 |

| 25.01.2023 | 1,298,258,618,333.20 | −899,577,004.60 | 47,386,021,386.77 | 419,964,462.71 | 24,605,312,696,250.30 | 4,861,177,132.60 |

| 24.01.2023 | 1,297,359,041,328.60 | 8,162,977,562.20 | 46,966,056,924.06 | 337,356,101.04 | 24,600,451,519,117.70 | −165,571,175,980.30 |

| 23.01.2023 | 1,305,522,018,890.80 | −34,267,298,643.20 | 46,628,700,823.02 | 842,467,999.64 | 24,766,022,695,098.00 | 104,969,218,556.70 |

| 20.01.2023 | 1,271,254,720,247.60 | −3,768,162,668.70 | 45,786,232,823.38 | 131,550,633.96 | 24,661,053,476,541.30 | −3,658,195,778,266.60 |

| 19.01.2023 | 1,267,486,557,578.90 | 9,017,259,462.60 | 45,654,682,189.41 | −803,879,851.43 | 28,319,249,254,807.90 | −387,444,921,281.70 |

| 18.01.2023 | 1,276,503,817,041.50 | −597,386,010.70 | 46,458,562,040.85 | 6,482,839.01 | 28,706,694,176,089.60 | −13,924,272,593.40 |

| 17.01.2023 | 1,275,906,431,030.80 | 23,322,647,074.70 | 46,452,079,201.84 | −798,294,440.40 | 28,720,618,448,683.00 | −319,220,094,412.00 |

| 16.01.2023 | 1,299,229,078,105.50 | −39,773,555,116.30 | 47,250,373,642.24 | 1,056,807,329.71 | 29,039,838,543,095.00 | 285,960,379,486.10 |

| 13.01.2023 | 1,259,455,522,989.20 | −6,599,926,057.00 | 46,193,566,312.53 | −36,666,864.09 | 28,753,878,163,608.90 | 134,197,441,421.20 |

| 12.01.2023 | 1,252,855,596,932.20 | −11,377,067,361.00 | 46,230,233,176.62 | 495,895,765.79 | 28,619,680,722,187.70 | −36,603,141,792.00 |

| 11.01.2023 | 1,241,478,529,571.20 | −34,763,335,623.20 | 45,734,337,410.83 | 1,256,436,855.29 | 28,656,283,863,979.70 | 124,313,269,296.10 |

| 10.01.2023 | 1,206,715,193,948.00 | −986,512,849.70 | 44,477,900,555.53 | 295,094,484.35 | 28,531,970,594,683.60 | −116,693,903,267.00 |

| 09.01.2023 | 1,205,728,681,098.30 | −1,558,140,905.80 | 44,182,806,071.18 | 783,016,803.47 | 28,648,664,497,950.60 | 54,675,310,877.50 |

| 06.01.2023 | 1,204,170,540,192.50 | 5,232,861,846.00 | 43,399,789,267.72 | −157,171,366.83 | 28,593,989,187,073.10 | −11,216,625,024.90 |

| 05.01.2023 | 1,209,403,402,038.50 | 5,274,966,068.10 | 43,556,960,634.54 | −8,460,387.24 | 28,605,205,812,098.00 | −127,253,020,799.60 |

| 04.01.2023 | 1,214,678,368,106.60 | −7,144,067,405.10 | 43,565,421,021.79 | 172,822,257.04 | 28,732,458,832,897.60 | −120,156,608,123.50 |

| 03.01.2023 | 1,207,534,300,701.50 | −21,969,395,431.10 | 43,392,598,764.75 | 768,123,471.94 | 28,852,615,441,021.10 | 222,438,191,991.10 |

| 30.12.2022 | 1,185,564,905,270.40 | 2,762,362,441.10 | 42,624,475,292.81 | −162,270,655.27 | 28,630,177,249,030.00 | 173,216,937,780.90 |

| 29.12.2022 | 1,188,327,267,711.50 | −3,843,457,152.60 | 42,786,745,948.07 | 218,561,431.16 | 28,456,960,311,249.10 | 114,579,722,665.00 |

| 28.12.2022 | 1,184,483,810,558.90 | 19,457,325,702.40 | 42,568,184,516.91 | −568,020,418.31 | 28,342,380,588,584.10 | −108,459,004,441.60 |

| 27.12.2022 | 1,203,941,136,261.30 | −16,984,195,192.10 | 43,136,204,935.22 | 782,402,775.37 | 28,450,839,593,025.70 | 165,359,904,064.00 |

| 26.12.2022 | 1,186,956,941,069.20 | 4,980,132,200.60 | 42,353,802,159.86 | −499,694,496.28 | 28,285,479,688,961.70 | 226,732,386,802.40 |

| 23.12.2022 | 1,191,937,073,269.80 | 14,654,257,816.50 | 42,853,496,656.14 | 64,059,685.69 | 28,058,747,302,159.30 | 41,043,613,551.20 |

| 22.12.2022 | 1,206,591,331,086.30 | −15,369,998,835.40 | 42,789,436,970.44 | 650,529,861.32 | 28,017,703,688,608.10 | 35,477,485,097.60 |

| 21.12.2022 | 1,191,221,332,250.90 | −728,399,199.00 | 42,138,907,109.13 | 388,330,534.54 | 27,982,226,203,510.50 | −14,868,826,846.20 |

| 20.12.2022 | 1,190,492,933,051.90 | −24,817,334,374.20 | 41,750,576,574.59 | 676,674,844.70 | 27,997,095,030,356.70 | 47,443,800,476.30 |

| 19.12.2022 | 1,165,675,598,677.70 | 20,161,432,337.30 | 41,073,901,729.88 | −569,592,587.55 | 27,949,651,229,880.40 | 59,883,958,906.50 |

| 16.12.2022 | 1,185,837,031,015.00 | −4,700,080,475.90 | 41,643,494,317.43 | 25,019,995,657.69 | 27,889,767,270,973.90 | 98,052,427,652.10 |

| 15.12.2022 | 1,181,136,950,539.10 | 14,133,514,701.50 | 16,623,498,659.74 | −265,038,283.57 | 27,791,714,843,321.80 | −448,731,005,896.10 |

| 14.12.2022 | 1,195,270,465,240.60 | 29,245,239,299.40 | 16,888,536,943.31 | −210,233,986.89 | 28,240,445,849,217.90 | −168,897,209,415.00 |

| 13.12.2022 | 1,224,515,704,540.00 | 10,174,434,429.90 | 17,098,770,930.20 | −153,778,914.30 | 28,409,343,058,632.90 | 95,151,383,694.80 |

| 12.12.2022 | 1,234,690,138,969.90 | 13,096,699,538.60 | 17,252,549,844.50 | 310,647,589.98 | 28,314,191,674,938.10 | −61,920,613,889.50 |

| 09.12.2022 | 1,247,786,838,508.50 | 6,691,636,692.00 | 16,941,902,254.52 | −311,982,565.78 | 28,376,112,288,827.60 | −58,919,038,923.60 |

| 08.12.2022 | 1,254,478,475,200.50 | 14,392,879,404.60 | 17,253,884,820.31 | −47,125,737.30 | 28,435,031,327,751.20 | −23,280,563,904.10 |

| 07.12.2022 | 1,268,871,354,605.10 | 9,768,183,640.10 | 17,301,010,557.61 | −66,087,911.88 | 28,458,311,891,655.30 | −41,359,620,283.10 |

| 06.12.2022 | 1,278,639,538,245.20 | −586,493,188.40 | 17,367,098,469.49 | −36,413,910.03 | 28,499,671,511,938.40 | −194,474,331,550.70 |

| 05.12.2022 | 1,278,053,045,056.80 | −15,288,270,893.20 | 17,403,512,379.52 | 41,558,506.38 | 28,694,145,843,489.10 | 358,893,315,569.40 |

| 02.12.2022 | 1,262,764,774,163.60 | 3,792,367,557.00 | 17,361,953,873.14 | −1,984,540.15 | 28,335,252,527,919.70 | −106,108,659,911.10 |

| 01.12.2022 | 1,266,557,141,720.60 | −1,039,504,710.00 | 17,363,938,413.30 | 161,189,900.66 | 28,441,361,187,830.80 | 220,613,270,121.20 |

| 30.11.2022 | 1,265,517,637,010.60 | 2,281,480,475.90 | 17,202,748,512.63 | 215,685,667.76 | 28,220,747,917,709.60 | −160,169,603,033.40 |

| 29.11.2022 | 1,267,799,117,486.50 | −27,789,863,123.70 | 16,987,062,844.87 | 78,151,995.97 | 28,380,917,520,743.00 | 61,400,262,001.80 |

| 28.11.2022 | 1,240,009,254,362.80 | 39,494,629,655.00 | 16,908,910,848.90 | −40,115,654.10 | 28,319,517,258,741.20 | −135,476,633,475.20 |

| 25.11.2022 | 1,279,503,884,017.80 | 40,089,240,472.60 | 16,949,026,503.00 | −67,821,440.33 | 28,454,993,892,216.40 | −131,147,645,071.40 |

| 24.11.2022 | 1,319,593,124,490.40 | - | 17,016,847,943.33 | - | 28,586,141,537,287.80 | - |

References

- Adomako, Samuel, and Nguyen Phong Nguyen. 2023. Green creativity, responsible innovation, and product innovation performance: A study of entrepreneurial firms in an emerging economy. Business Strategy and the Environment 32: 4413–25. [Google Scholar] [CrossRef]

- Almaiah, Mohammed Amin, Shaha Al-Otaibi, Rima Shishakly, Lamia Hassan, Abdalwali Lutfi, Mahmoad Alrawad, Mohammad Qatawneh, and Orieb Abu Alghanam. 2023. Investigating the Role of Perceived Risk, Perceived Security and Perceived Trust on Smart m-Banking Application Using SEM. Sustainability 15: 9908. [Google Scholar] [CrossRef]

- Bednar, Kathrin, and Sarah Spiekermann. 2023. The Power of Ethics: Uncovering Technology Risks and Positive Value Potentials in IT Innovation Planning. Business and Information Systems Engineering, 1–21. [Google Scholar] [CrossRef]

- Beger, Gizem Aras, Bayram Bilge Sağlam, and Duygu Turker. 2023. Leveraging corporate sustainability through responsible innovation: Capacity building with exploration and exploitation. Creativity and Innovation Management 32: 617–35. [Google Scholar] [CrossRef]

- Bertoluci, Gwenola, Jean Claude Boucquet, and Francois Petetin. 2013. Supporting decisions in SMEs projects of disruptive technological innovation by balancing values and risks related to stakeholders. Journal of Modern Project Management 1: 94–111. [Google Scholar]

- Birtchnell, Thomas. 2011. Jugaad as systemic risk and disruptive innovation in India. Contemporary South Asia 19: 357–72. [Google Scholar] [CrossRef]

- Błaszczyk, Michael, Milan Popović,arolina Zajdel, and Radoslaw Zajdel. 2023. Implications of the COVID-19 Pandemic on the Organization of Remote Work in IT Companies: The Managers’ Perspective. Sustainability 15: 12049. [Google Scholar] [CrossRef]

- Butler, Frank C., and John Martin. 2016. The auto industry: Adapt to disruptive innovations or risk extinction. Strategic Direction 32: 31–34. [Google Scholar] [CrossRef]

- Chabot, Mila, and Jean -Louis Bertrand. 2023. Climate risks and financial stability: Evidence from the European financial system. Journal of Financial Stability 69: 101190. [Google Scholar] [CrossRef]

- Chen, Ping. 2023. Research on Financial Risk Evaluation and Control of Tourism Enterprises Based on Improved GA Algorithm. International Journal of Computational Intelligence Systems 16: 146. [Google Scholar] [CrossRef]

- Chen, Liping, and Cheng Zhang. 2023. The impact of financial agglomeration on corporate financialization: The moderating role of financial risk in Chinese listed manufacturing enterprises. Finance Research Letters 58: 104655. [Google Scholar] [CrossRef]

- Christensen, Clayton Magleby. 2002. The rules of innovation. Technology Review 105: 33. [Google Scholar]

- CIAN. 2023. Cian Signed the Charter of Professional Ethics. Available online: https://volgograd.cian.ru/novosti-tsian-podpisal-hartiju-professionalnoj-etiki-328479/ (accessed on 27 November 2023).

- Cook, Joanne, Jon Burchell, Harriet Thiery, and Taposh Roy. 2023. “I’m Not Doing It for the Company”: Examining Employee Volunteering Through Employees’ Eyes. Nonprofit and Voluntary Sector Quarterly 52: 1006–28. [Google Scholar] [CrossRef]

- Deng, Hong, You Li, and Yongjia Lin. 2023. Green financial policy and corporate risk-taking: Evidence from China. Finance Research Letters 58: 104381. [Google Scholar] [CrossRef]

- Diba, Hoda. 2023. Employer Branding: The Impact of COVID-19 on New Employee Hires in IT Companies. IT Professional 25: 4–9. [Google Scholar] [CrossRef]

- Du, Junshu, Shaofeng Peng, and Jisheng Peng. 2020. Research on technology innovation risk evaluation of high-tech enterprises based on fuzzy evaluation. Journal of Intelligent and Fuzzy Systems 38: 6805–14. [Google Scholar] [CrossRef]

- Fu, Qiang, Xinxin Zhao, and Chun-Ping Chang. 2023. Does ESG performance bring to enterprises’ green innovation? Yes, evidence from 118 countries. Oeconomia Copernicana 14: 795–832. [Google Scholar] [CrossRef]

- Fujii, Ryosuke, oberto Melotti, Martin Gögele, Laura Barin, Dariush Ghasemi-Semeskandeh, Giula Barbieri, Peter Pramstaller, and Cristian Pattaro. 2023. Structural equation modeling (SEM) of kidney function markers and longitudinal CVD risk assessment. PLoS ONE 18: e0280600. [Google Scholar] [CrossRef]

- Information Technology Index, in Rubles. 2023a. Available online: https://www.moex.com/ru/index/MOEXIT/constituents (accessed on 27 November 2023).

- Khasanov, Bakhodir Akramovich, U. T. Eshboev, R. B. Hasanova, Z. A. Mukumov, A. I. Alikulov, and A. B. Djumanova. 2019. Calculation of the invested capital profitability in the financial condition analysis process. International Journal of Advanced Science and Technology 28: 42–48. [Google Scholar]

- Khémiri, Wafa, Ahmed Chafai, and Faizah Alsulami. 2023. Financial Inclusion and Sustainable Growth in North African Firms: A Dynamic-Panel-Threshold Approach. Risks 11: 132. [Google Scholar] [CrossRef]

- Kokot, Tomaž 2023. Hybrid Remote Work Models in Project-Organized Small and Medium-Sized IT Companies. International Journal of Computers and their Applications 30: 259–66.

- Li, Hui, Dongsheng Yu, and Zhixuan Ke. 2023. Commercial System Reform, Enterprise Green Innovation and Enterprise ESG Performance. Sustainability 15: 14469. [Google Scholar] [CrossRef]

- Liu, Rangpeng, Zhuo Yue, Ali Ijaz, Abdalwali Lutfi, and Jie Mao. 2023. Sustainable Business Performance: Examining the Role of Green HRM Practices, Green Innovation and Responsible Leadership through the Lens of Pro-Environmental Behavior. Sustainability 15: 7317. [Google Scholar] [CrossRef]

- Luttikhuis, Nikki, and Kirsten Wiebe. 2023. Analyzing SDG interlinkages: Identifying trade-offs and synergies for a responsible innovation. Sustainability Science 18: 1813–31. [Google Scholar] [CrossRef]

- Martins, Henrique Castro. 2023. Financial materiality and corporate risk: Evidence from an Instrumental Variables (IV) design. Finance Research Letters 58: 104433. [Google Scholar] [CrossRef]

- Memon, Khalid. Rasheed, and Say Keat Ooi. 2023. Responsible innovation and resource-based theory: Advancing an antecedent-outcome model for large manufacturing firms through structured literature review. Asian Journal of Business Ethics 12: 441–67. [Google Scholar] [CrossRef]

- Mlawu, Lonwabo, Frank Ranganai Matenda, and Mabutho Sibanda. 2023. Linking Financial Performance with CEO Statements: Testing Impression Management Theory. Risks 11: 55. [Google Scholar] [CrossRef]

- Moscow Exchange Innovations Index (MOEXINN), in Rubles. 2023b. Available online: https://www.moex.com/ru/index/MOEXINN/archive?from=2022-11-24&till=2023-11-24&sort=TRADEDATE&order=desc (accessed on 27 November 2023).

- Nagarajah, Nanthini. 2023. Determinants of responsible innovation for sustainability transition in a developing country: Contested narratives for transition in the Sri Lankan power sector. Norsk Geografisk Tidsskrift 77: 35–46. [Google Scholar] [CrossRef]

- Olasiuk, Hanna, Sanjeev Kumar, Prashant Sharma, and Tetiana Ganushchak. 2023. Impact of COVID-19 on the Efficiency of Indian IT Companies. Vision: The Journal of Business Perspective. in press. [Google Scholar] [CrossRef]

- Oneshko, Svitlana. 2023. Assessing the Profitability of IT Companies: International Financial Reporting Standards. Review of Economics and Finance 21: 1361–69. [Google Scholar] [CrossRef]

- Osovtsev, V. A., N. V. Przhedetskaya, and M. S. Sagidullaeva. 2018. Conceptual model of adaptive management of strategic marketing: A system approach. European Research Studies Journal 21: 666–77. [Google Scholar]

- Peng, Yulin, ianquing Zhou, iaoxin Lin, and Dawei Feng. 2023. The Impact of IT Capability on Corporate Green Technological Innovation: Evidence from Manufacturing Companies in China. Journal of Information and Knowledge Management 22: 2250068. [Google Scholar] [CrossRef]

- Positive Technologies. 2023. Principles and Practice of Corporate Governance. Available online: https://ar2022.ptsecurity.com/corporate-governance/principles-practice (accessed on 27 November 2023).

- Qin, Yi, Duc Khuong Nguyen, Javier Cifuentes-Faura, and Kaiyang Zhong. 2023. Strong financial regulation and corporate bankruptcy risk in China. Finance Research Letters 58: 104343. [Google Scholar] [CrossRef]

- Qu, Shiyou, Jintap Wang, Yonghong Li, and Kexuan Wang. 2023. How does risk-taking affect the green technology innovation of high-tech enterprises in China: The moderating role of financial mismatch. Environmental Science and Pollution Research 30: 23747–63. [Google Scholar] [CrossRef] [PubMed]

- Qu, Xiaoyu, Xiao Wang, and Xutian Qin. 2023. Research on Responsible Innovation Mechanism Based on Prospect Theory. Sustainability 15: 1358. [Google Scholar] [CrossRef]

- Rehman, Muzzamil, abil Dhiman, Ravi Kumar, Gagandeep Singh Cheema, and Anuj Vaid. 2023. Exploring the Impact of Personality Traits on Investment Decisions of Immigrated Global Investors with Focus on Moderating Risk Appetite: A SEM Approach. Migration Letters 20: 95–110. [Google Scholar] [CrossRef]

- Responsibility and Transparency MRRT, in Rubles. 2023c. Available online: https://www.moex.com/ru/index/MRRT/archive?from=2022-11-24&till=2023-11-24&sort=TRADEDATE&order=desc (accessed on 27 November 2023).

- Silva, Hudson, Pascale Lehoux, and Renata Pozelli Sabio. 2023. Mobilizing capital for responsible innovation: The role of social finance in supporting innovative projects. Journal of Responsible Innovation 10: 2243122. [Google Scholar] [CrossRef]

- Stepnov, Igor, Julia Kovalchuk, Margarita Melnik, and Tamara Petrovic. 2022. Public Goals and Government Expenditures: Are the Solutions of the “Modern Monetary Theory” Realistic? Finance: Theory and Practice 26: 6–18. [Google Scholar] [CrossRef]

- Toma, Filip -Mihai, Cosmin -Octavian Cepoi, Matei Nicolae Kubinschi, and Makoto Miyakoshi. 2023. Gazing through the bubble: An experimental investigation into financial risk-taking using eye-tracking. Financial Innovation 9: 28. [Google Scholar] [CrossRef]

- Trabelsi, Donia, Marie Carpenter, and Wadid Lamine. 2023. The Primacy of Innovation in the Development of Responsible and Sustainable Finance. Journal of Innovation Economics and Management 41: 1–15. [Google Scholar] [CrossRef]

- Turginbayeva, Ardak, Asset Ustemorov, Gulmira Akhmetova, Zhanna Kose, Aibek Imashev, and Galiya Gimranova. 2018. Financing aspects of an effective strategy for innovative enterprise development. Journal of Advanced Research in Law and Economics 9: 714–20. [Google Scholar] [CrossRef]

- Veselovsky, Mikhail Yakovlevich, Marina Alekseevna Izmailova, Aleksei Bogoviz, Svetlana Lobova, and Alexander Nikolaevich Alekseev. 2017. Business environment in Russia and its stimulating influence on innovation activity of domestic companies. Journal of Applied Economic Sciences 12: 1967–81. [Google Scholar]

- Veselovsky, Mikhail Yakovlevich, Marina Alekseevna Izmailova, A Aleksei Bogoviz, Svetlana Lobova, and Alexander Nikolaevich Alekseev. 2018. Innovative solutions for improving the quality of corporate governance in Russian companies. Quality-Access to Success 19: 60–66. [Google Scholar]

- VK. 2023. Key ESG Projects and Events of VK COMPANY LIMITED for the 4th Quarter of 2022. Available online: https://corp.vkcdn.ru/media/2023/03/16/key-esg-projects-and-events-for-q4-2022_rus.pdf (accessed on 27 November 2023).

- Wang, Junkai, Baolei Qi, Yaaxiang Nie, and Muhammad Jameel Hussain. 2023. Will the investment environment in the region where the company is located affect its financial risk? Evidence from Chinese listed companies. Finance Research Letters 57: 104218. [Google Scholar] [CrossRef]

- White, Martin. 2023. Workarounds and shadow IT—balancing innovation and risk. Business Information Review 40: 114–22. [Google Scholar] [CrossRef]

- Wiarda, Martijn, and Neelke Doorn. 2023. Responsible innovation and societal challenges: The multi-scalarity dilemma. Journal of Responsible Technology 16: 100072. [Google Scholar] [CrossRef]

- Wicher, Magdalena Julia, and Elisabeth Frankus. 2023. Research governance for change: Funding project-based measures in the field of responsible research and innovation (RRI) and their potential for organisational learning. Learning Organization. ahead-of-print. [Google Scholar] [CrossRef]

- Xu, Xiaodong, Yayu Mu, and Juan Wang. 2023. Corporate risk and financial asset holdings. Pacific Basin Finance Journal 81: 102121. [Google Scholar] [CrossRef]

- YouDo. 2023. Material Responsibility of Performer at YouDo: When Compensation Can Be Received. Available online: https://help.youdo.com/ru/articles/2547961-материальная-responsibility-испoлнителя-на-youdo-в-какoм-случае-мoжнo-пoлучить-кoмпенсацию (accessed on 27 November 2023).

- Zhang, Xiu-E, Xinyu Teng, Yuan Le, and Yijing Li. 2023. Strategic orientations and responsible innovation in SMEs: The moderating effects of environmental turbulence. Business Strategy and the Environment 32: 2522–39. [Google Scholar] [CrossRef]

| Element of Statistical Analysis | Information Technology Index (IT), Rubles | Moscow Exchange Innovations Index, Rubles | Responsibility and Transparency (MRRT), Rubles | |||

|---|---|---|---|---|---|---|

| Value | Daily Change | Value | Daily Change | Value | Daily Change | |

| Arithmetic mean, billion RUB | 1597.5759 | −2.6045 | 60.2699 | 0.2149 | 30,364.1590 | 23.5804 |

| Coefficient of variation, % | 18.54 | −863.71 | 29.22 | 1023.11 | 11.75 | 1423.69 |

| Total number of observations | 256 | 255 | 256 | 255 | 256 | 255 |

| Number of negative values | - | 138 | - | 112 | - | 107 |

| The sum of negative values, billion RUB | - | −2494.6731 | - | −96.3201 | - | −22,423.3061 |

| Share of negative values | - | 0.54 | - | 0.43 | - | 0,42 |

| Financial risk, billion RUB | - | −1350.06 | - | −42.31 | - | −9409.00 |

| Regression Statistics | ||||||

|---|---|---|---|---|---|---|

| Multiple R | 0.9531 | |||||

| R-square | 0.9083 | |||||

| Adjusted R-square | 0.9076 | |||||

| Standard error | 0.0901 | |||||

| Observations | 256 | |||||

| ANOVA | ||||||

| df | SS | MS | F | Significance F | ||

| Regression | 2 | 20.3227 | 10.1613 | 1253.0666 | 5 × 10−132 | |

| Residual | 253 | 2.0516 | 0.0081 | |||

| Total | 255 | 22.3743 | ||||

| Coefficients | Standard error | t-Stat | p-Value | Lower 95% | Upper 95% | |

| Y-intercept | −0.4547 | 0.0536 | −8.4865 | 1.82 × 10−15 | −0.5602 | −0.3492 |

| MOEXINN | 5.6551 | 0.4698 | 12.0385 | 1.09 × 10−26 | 4.7300 | 6.5802 |

| MRRT | 0.0564 | 0.0023 | 24.3172 | 3.7 × 10−68 | 0.0518 | 0.0609 |

| Regression Statistics | ||||||

|---|---|---|---|---|---|---|

| Multiple R | 0.7316 | |||||

| R-square | 0.5353 | |||||

| Adjusted R-square | 0.5335 | |||||

| Standard error | 0.0120 | |||||

| Observations | 256 | |||||

| ANOVA | ||||||

| df | SS | MS | F | Significance F | ||

| Regression | 1 | 0.0423 | 0.0423 | 292.5830 | 3.7 × 10−44 | |

| Residual | 254 | 0.0367 | 0.0001 | |||

| Total | 255 | 0.0791 | ||||

| Coefficients | Standard error | t-Stat | p-Value | Lower 95% | Upper 95% | |

| Y-intercept | −0.0493 | 0.0065 | −7.6479 | 4.22 × 10−13 | −0.0621 | −0.0366 |

| MRRT | 0.0036 | 0.0002 | 17.1051 | 3.67 × 10−44 | 0.0032 | 0.0040 |

| Regression Statistics | ||||||

|---|---|---|---|---|---|---|

| Multiple R | 0.7316 | |||||

| R-square | 0.5353 | |||||

| Adjusted R-square | 0.5335 | |||||

| Standard error | 2.4377 | |||||

| Observations | 256 | |||||

| ANOVA | ||||||

| df | SS | MS | F | Significance F | ||

| Regression | 1 | 1738.6365 | 1738.6365 | 292.5830 | 3.7 × 10−44 | |

| Residual | 254 | 1509.3618 | 5.9424 | |||

| Total | 255 | 3247.9982 | ||||

| Coefficients | Standard error | t-Stat | p-Value | Lower 95% | Upper 95% | |

| Y-intercept | 21.4275 | 0.5442 | 39.3730 | 3.9 × 10−110 | 20.3557 | 22.4993 |

| MOEXINN | 148.2773 | 8.6686 | 17.1051 | 3.67 × 10−44 | 131.2058 | 165.3488 |

| Variable | Scenario without Innovations | Scenario of Isolated Innovations | Scenario of Isolated Corporate Responsibility | Scenario of Responsible Innovations |

|---|---|---|---|---|

| Value according to the scenario, in billion RUB | ||||

| MOEXINN | 71.8128 | 303.0569 | 60.2699 | 303.0569 |

| MRRT | 34,599.1514 | 30,364.1590 | 41,876.9799 | 41,876.9799 |

| IT | 2982.1453 | 2970.5639 | 2246.4896 | 3619.4775 |

| Change (annual growth) according to the scenario, % | ||||

| MOEXINN | 0.00 | 322.01 | −16.07 | 322.01 |

| MRRT | 0.00 | −12.24 | 21.03 | 21.03 |

| IT | 50.33 | 49.75 | 13.25 | 82.46 |

| - | - | In aggregate: 49.75 + 13.25 = 62.99 | Synergetic effect: 19.47% | |

| Spheres of Comparison | Existing Literature | This Paper |

|---|---|---|

| Influence of responsible innovations on the financial risks of high-tech companies | Financial risks are increased through the following:

| They reduce financial risks because they increase the competitiveness of high-tech companies, simultaneously increasing their innovativeness and strengthening a business’s reputation as a reliable supplier, which is especially valuable in a high-risk market environment |

| Perspective of ensuring the sustainable development of high-tech companies in a high-risk market environment |

| Through active implementation of responsible innovations as sources of predictable and reliable additional income |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Popkova, E.G.; Xakimova, M.F.; Troyanskaya, M.A.; Petrenko, E.S.; Fokina, O.V. Responsible Innovations as Tools for the Management of Financial Risks to Projects of High-Tech Companies for Their Sustainable Development. Risks 2024, 12, 21. https://doi.org/10.3390/risks12020021

Popkova EG, Xakimova MF, Troyanskaya MA, Petrenko ES, Fokina OV. Responsible Innovations as Tools for the Management of Financial Risks to Projects of High-Tech Companies for Their Sustainable Development. Risks. 2024; 12(2):21. https://doi.org/10.3390/risks12020021

Chicago/Turabian StylePopkova, Elena G., Muxabbat F. Xakimova, Marija A. Troyanskaya, Elena S. Petrenko, and Olga V. Fokina. 2024. "Responsible Innovations as Tools for the Management of Financial Risks to Projects of High-Tech Companies for Their Sustainable Development" Risks 12, no. 2: 21. https://doi.org/10.3390/risks12020021

APA StylePopkova, E. G., Xakimova, M. F., Troyanskaya, M. A., Petrenko, E. S., & Fokina, O. V. (2024). Responsible Innovations as Tools for the Management of Financial Risks to Projects of High-Tech Companies for Their Sustainable Development. Risks, 12(2), 21. https://doi.org/10.3390/risks12020021