Risks for Companies during the COVID-19 Crisis: Dataset Modelling and Management through Digitalisation

Abstract

:1. Introduction

2. Literature Review and Gap Analysis

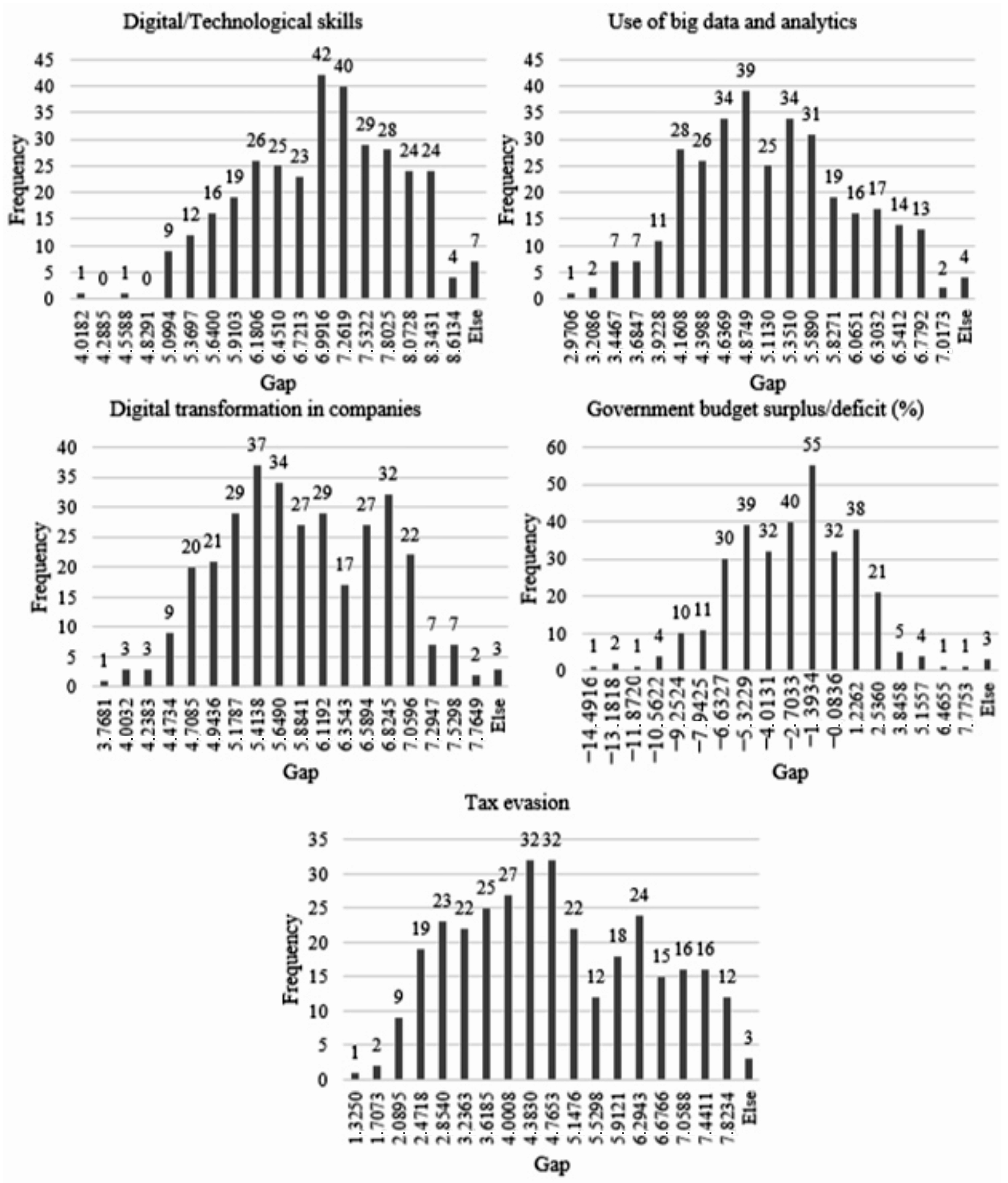

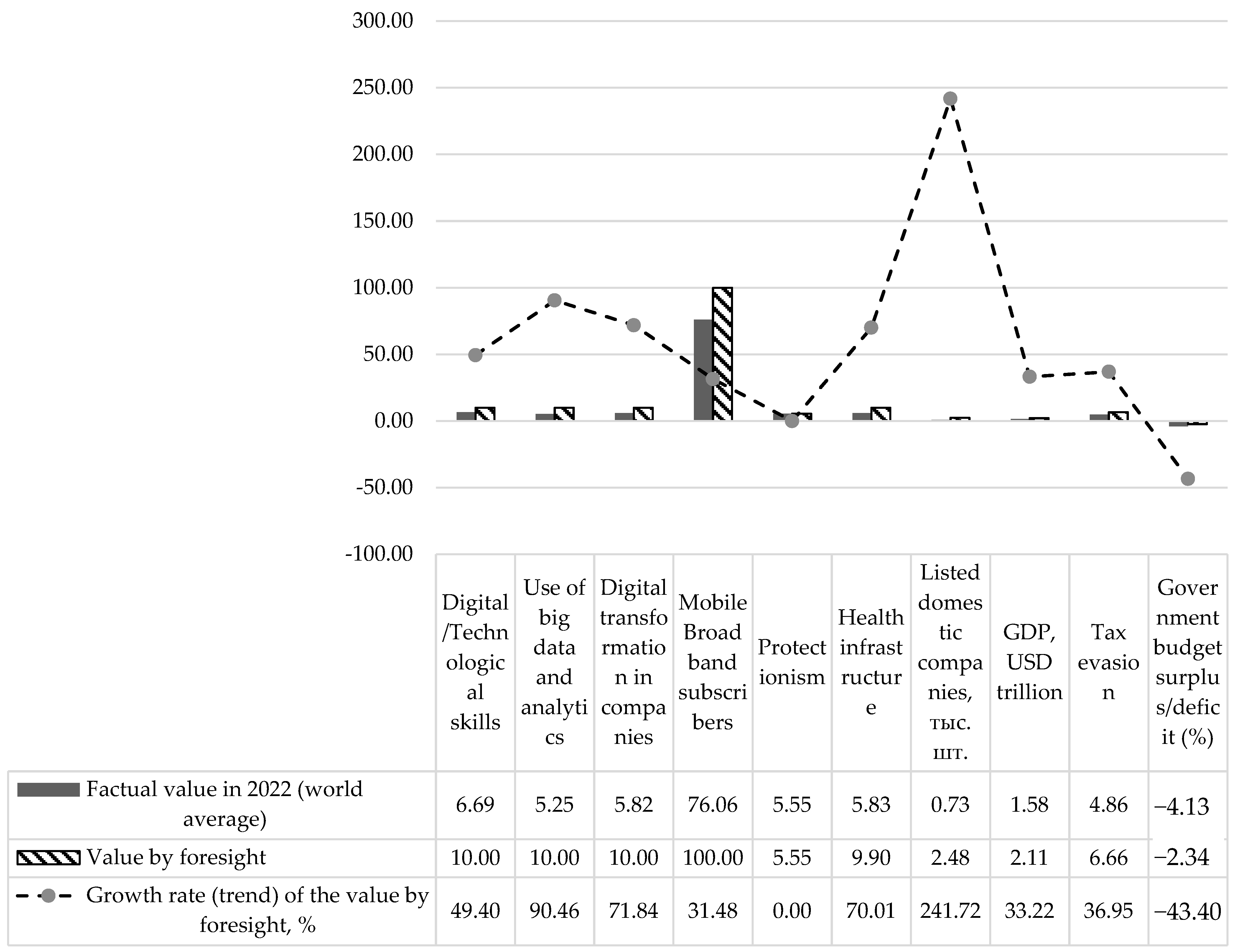

- Development of digital/technological skills of employees to implement digital innovations in business (Türk 2022);

- Raising the activity of the use of big data and analytics to create and develop smart productions with a high level of automatisation of all business operations (Cui et al. 2022);

- Performing digital transformation in companies to raise their effectiveness and digital competitiveness (Busco et al. 2023);

- Dissemination of mobile broadband subscribers (transition to 4G and 5G mobile Internet) for the development of e-commerce (Attran 2023)

3. Methodology

4. Results

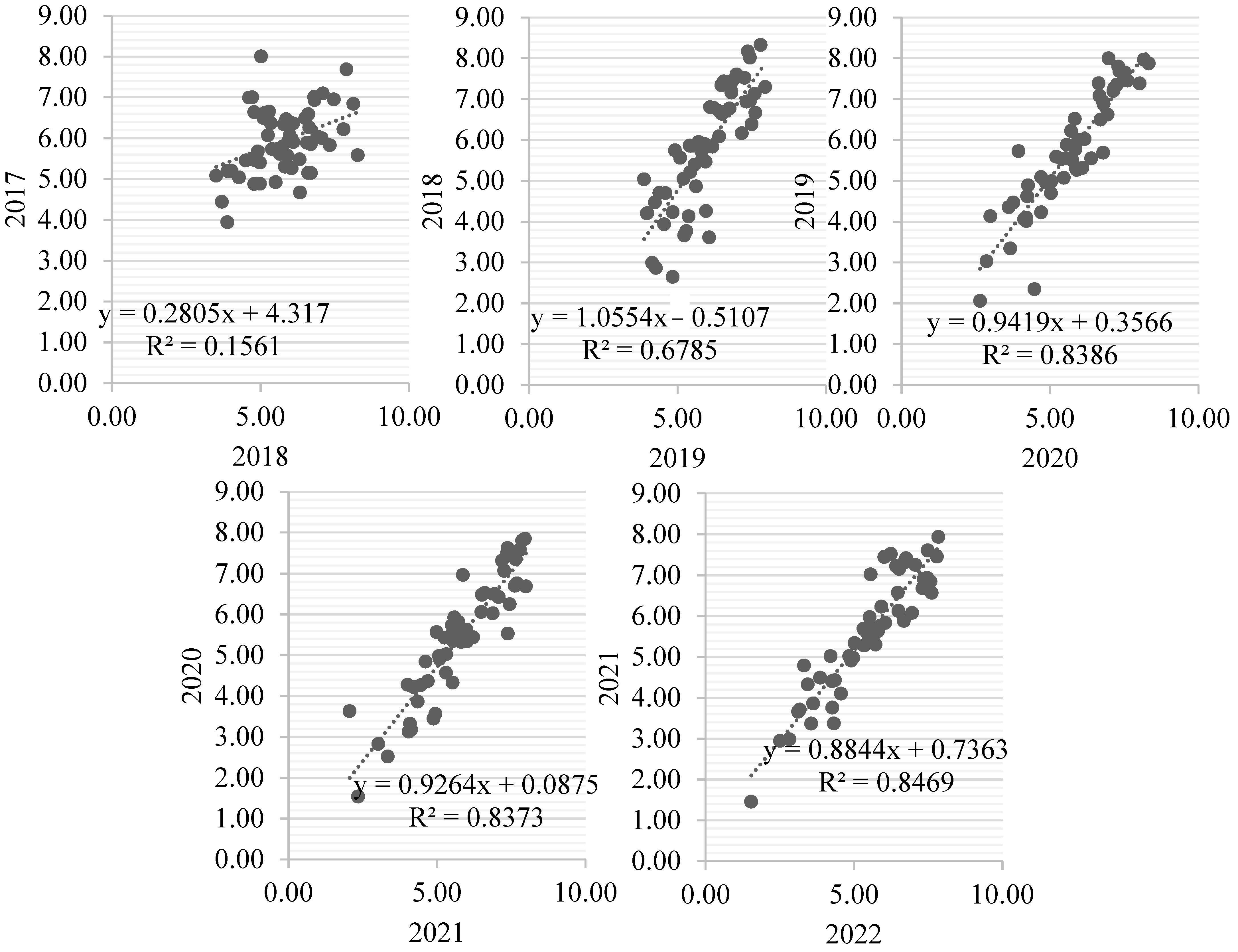

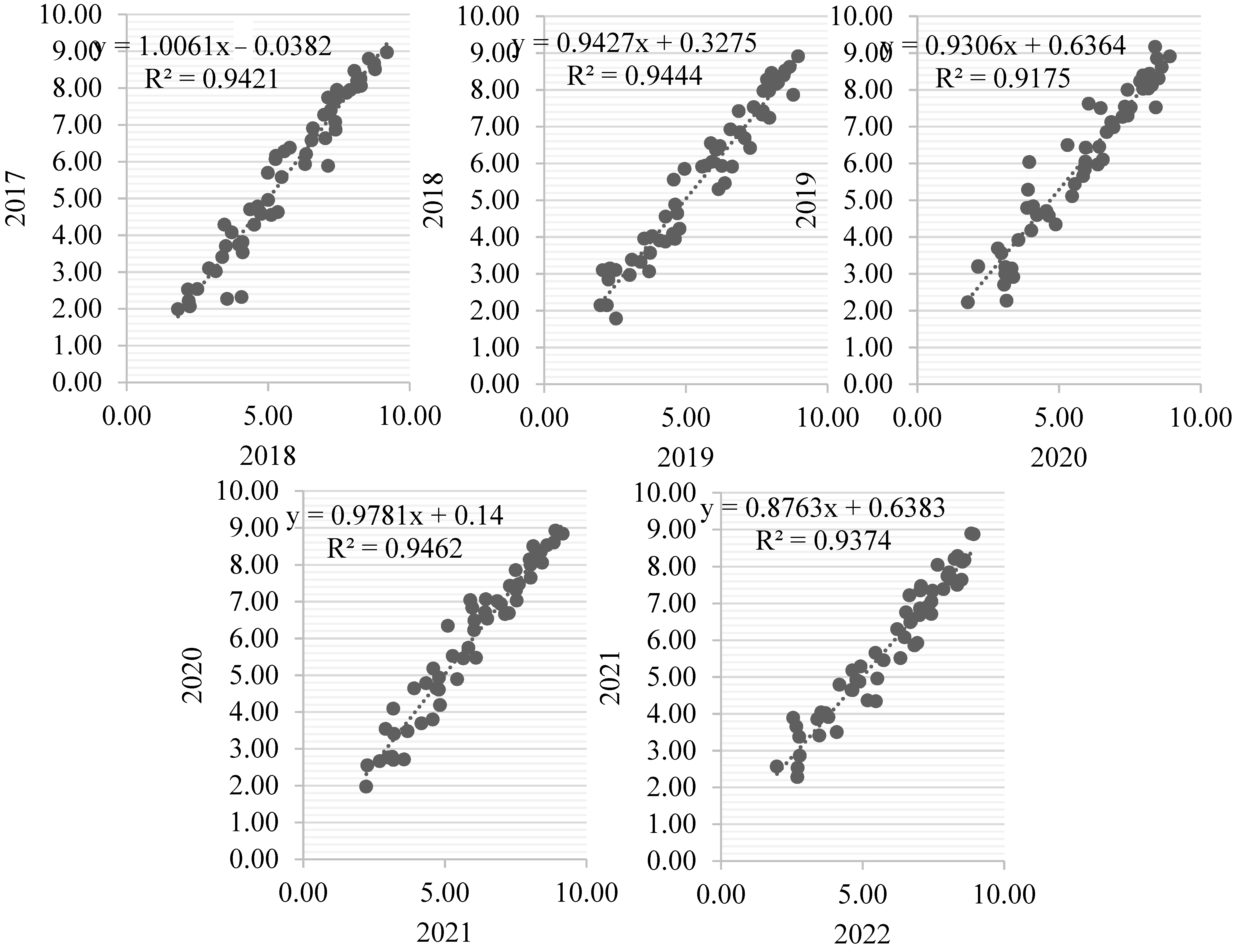

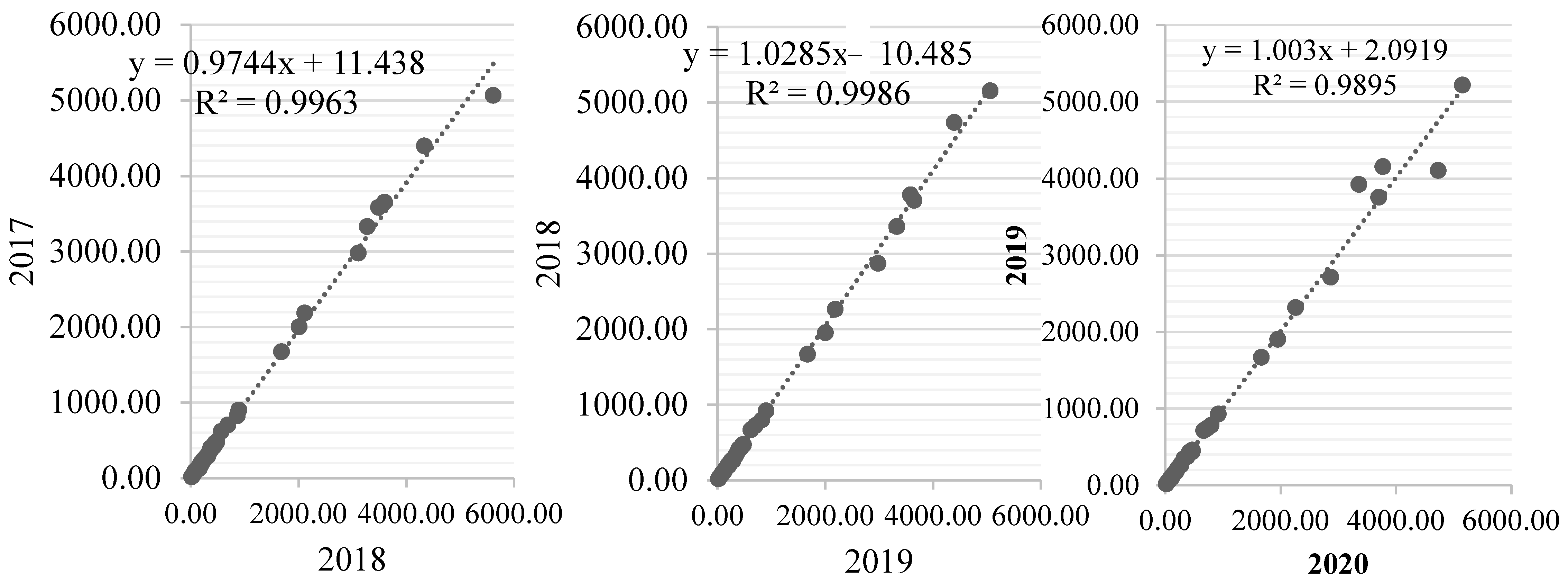

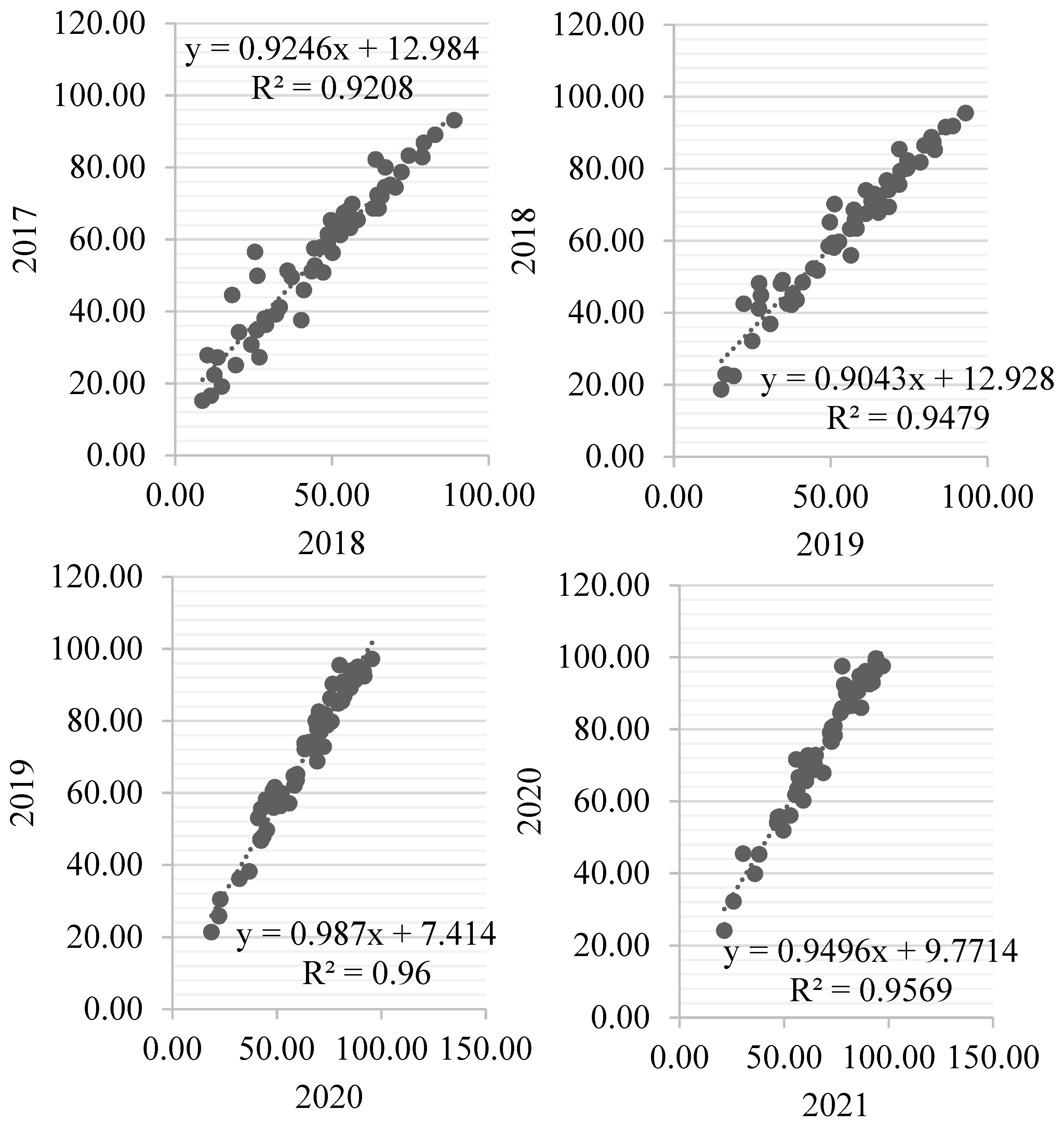

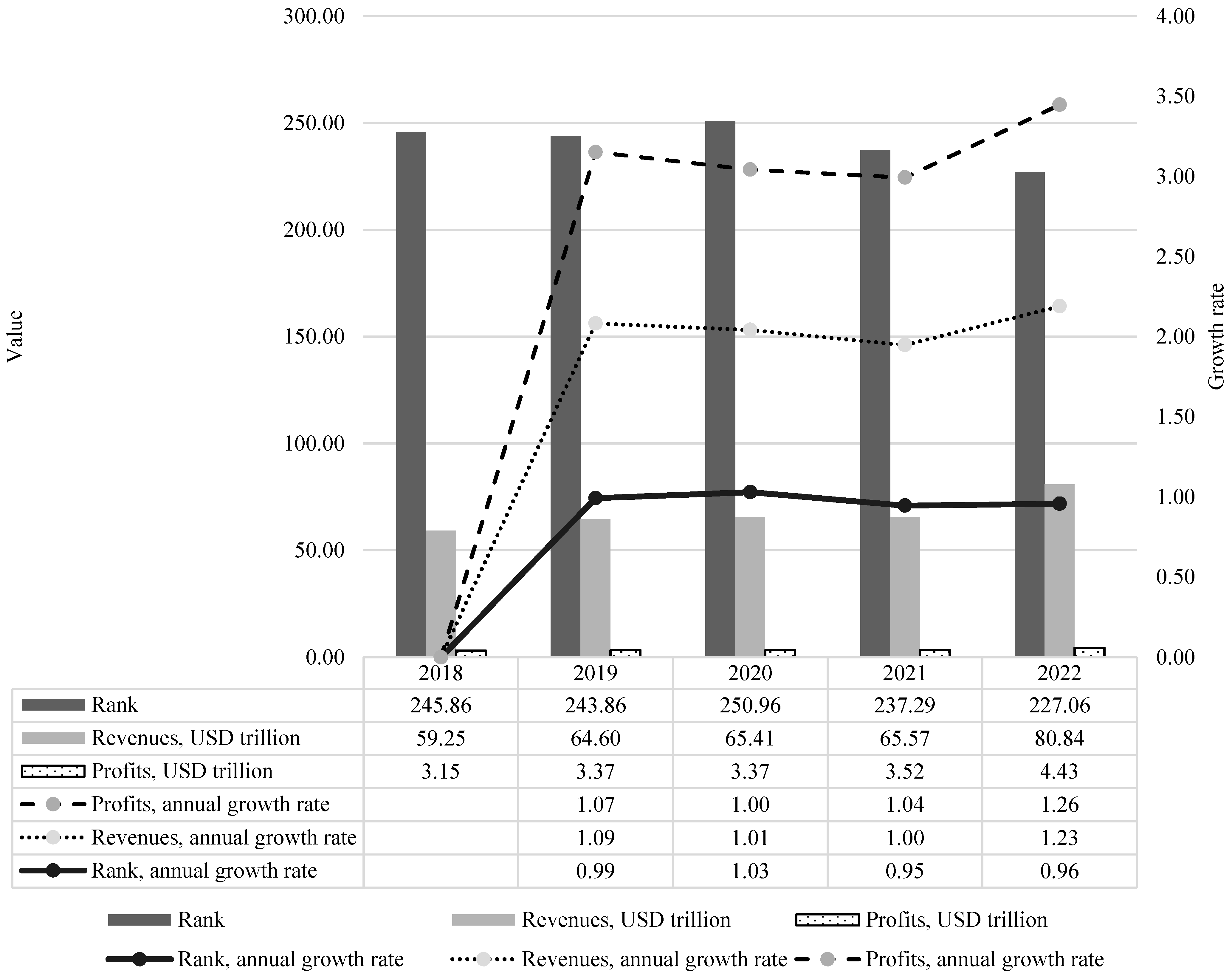

4.1. Risks for Companies during the COVID-19 Crisis: Specifics of Developed and Developing Countries

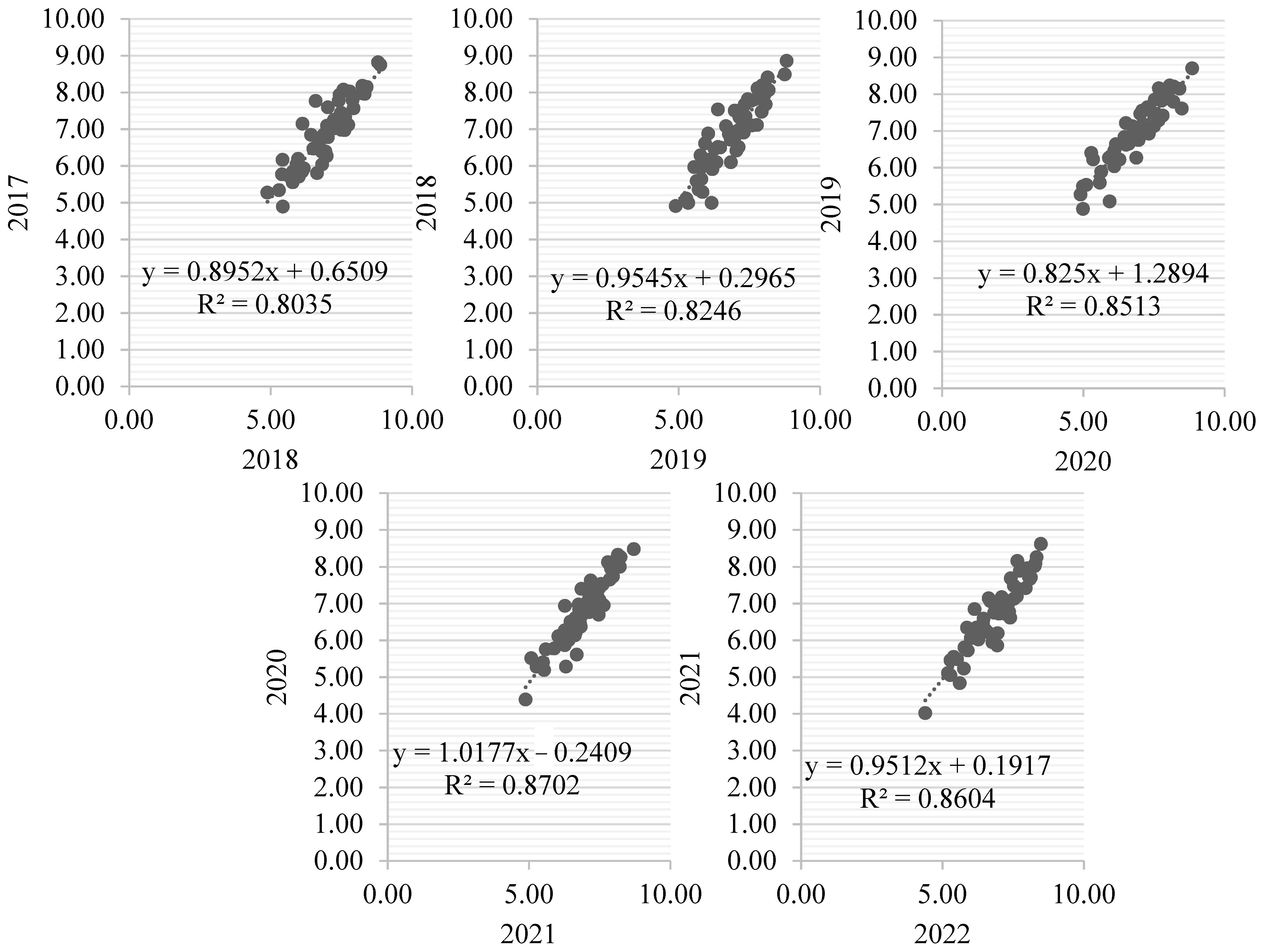

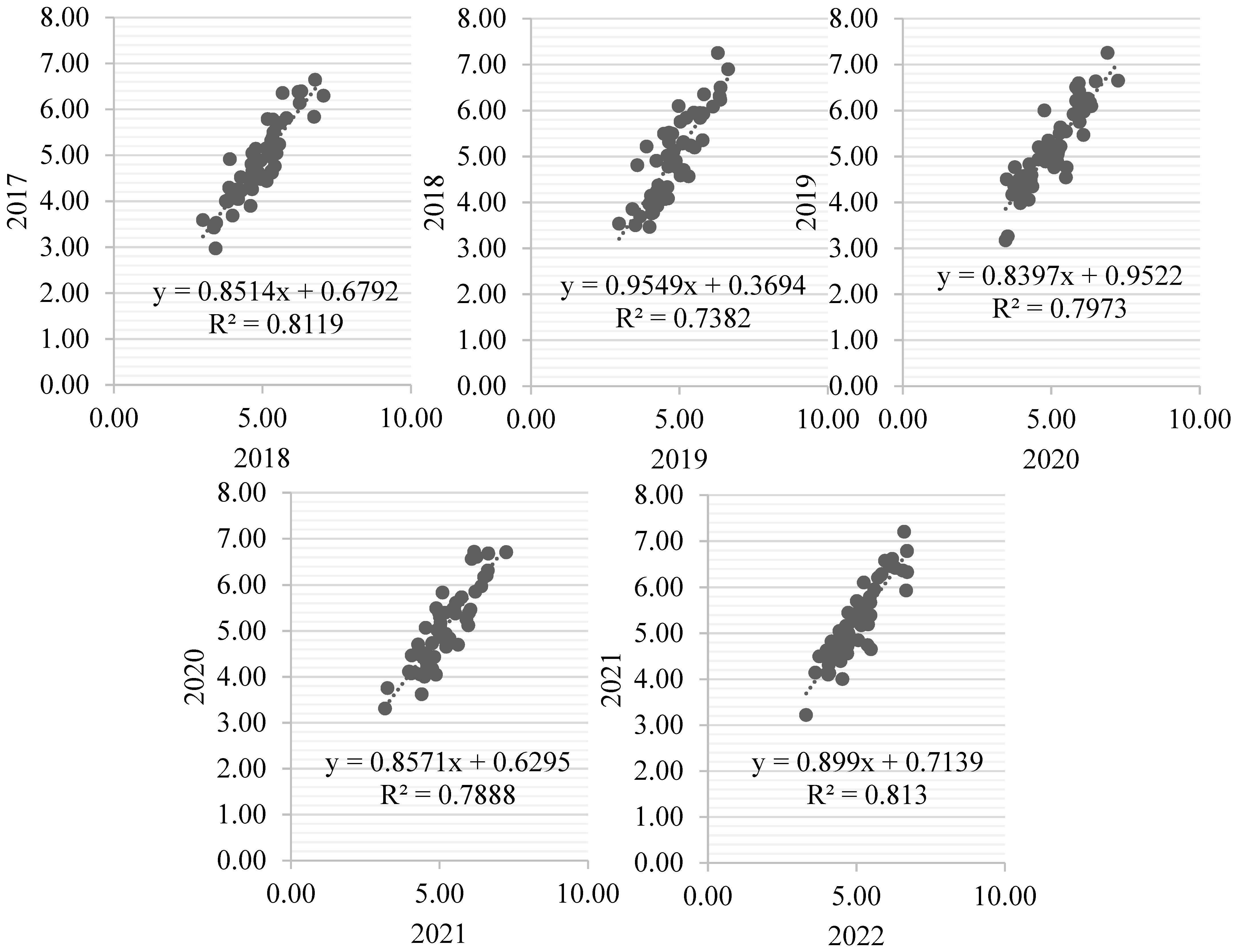

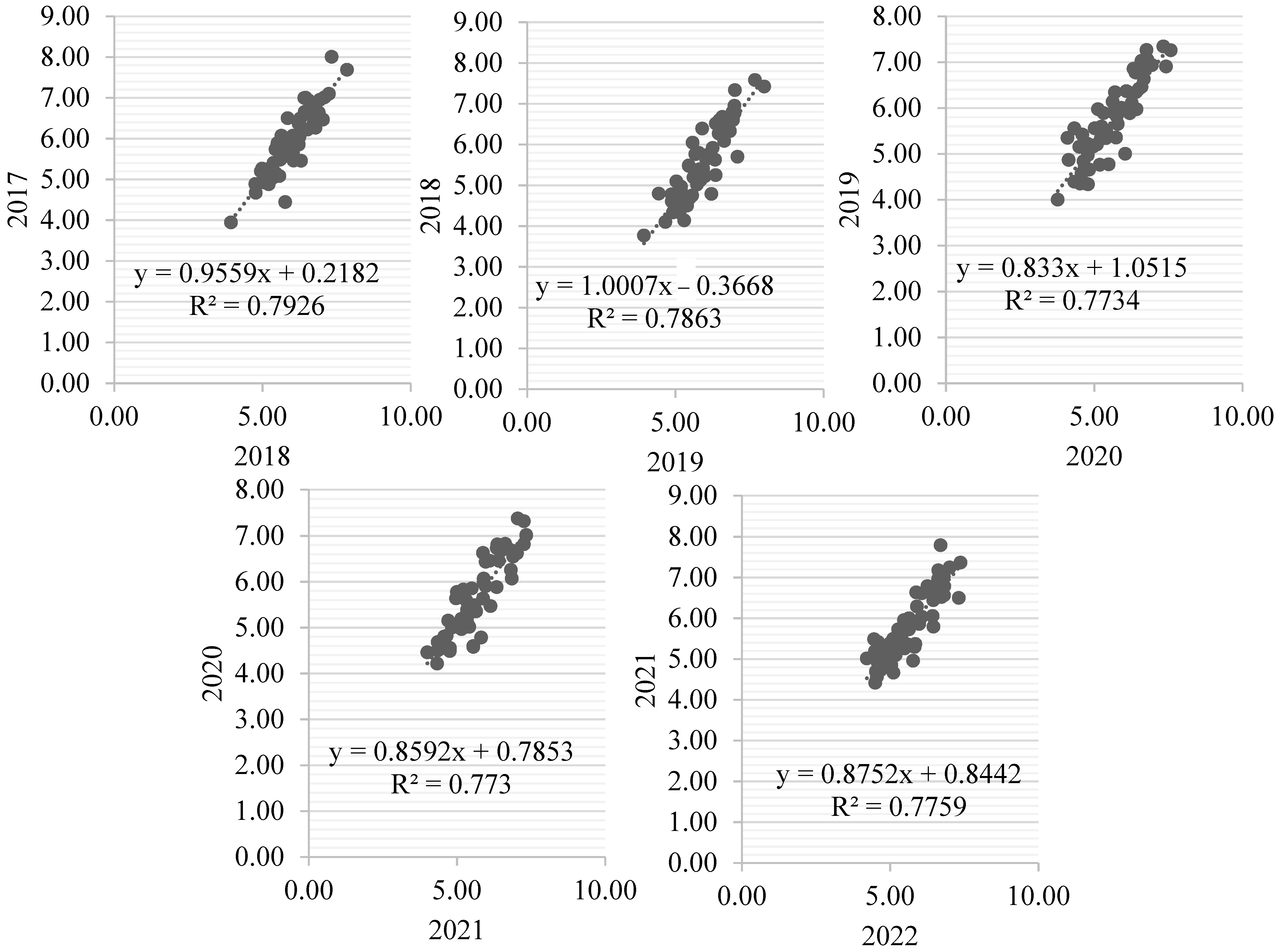

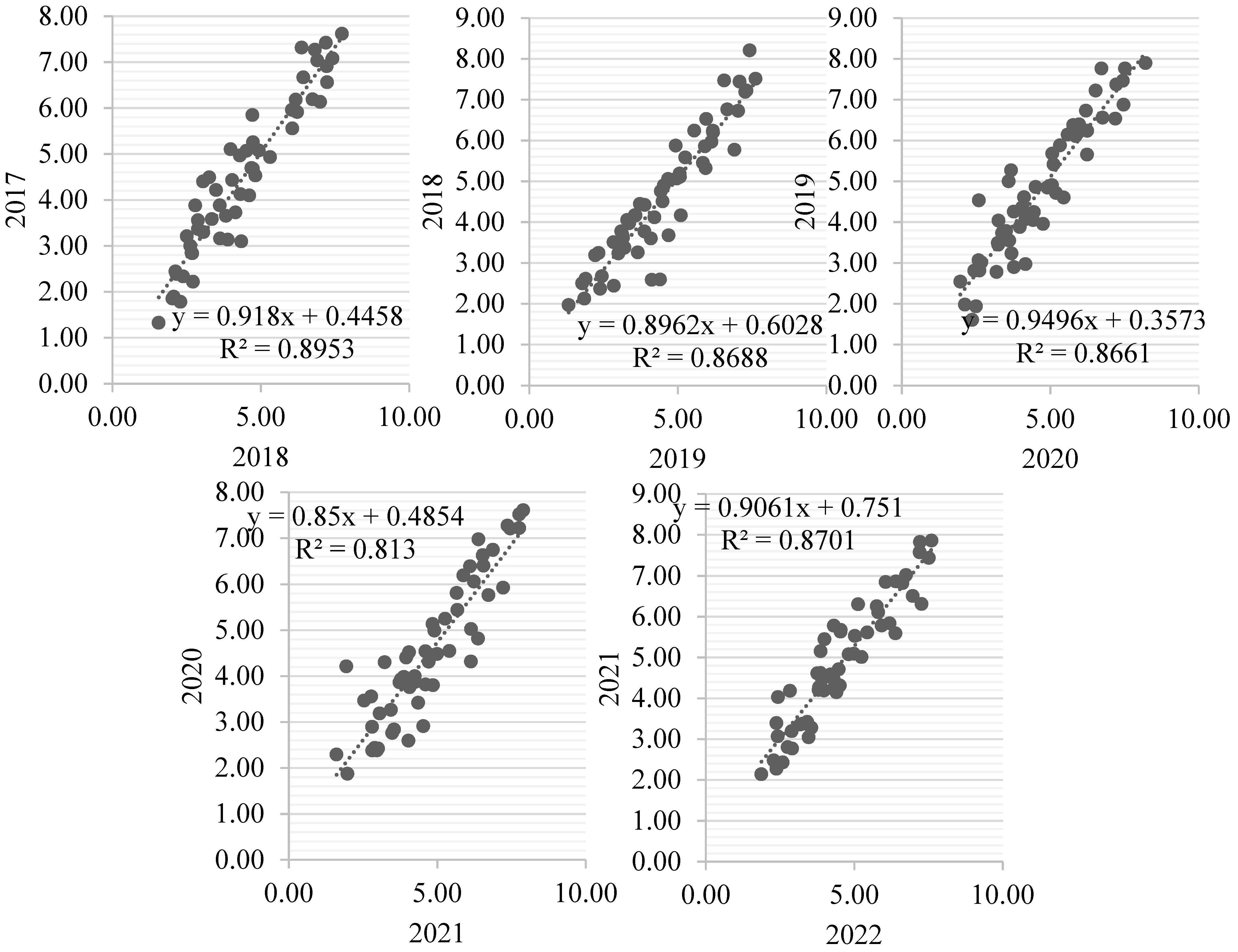

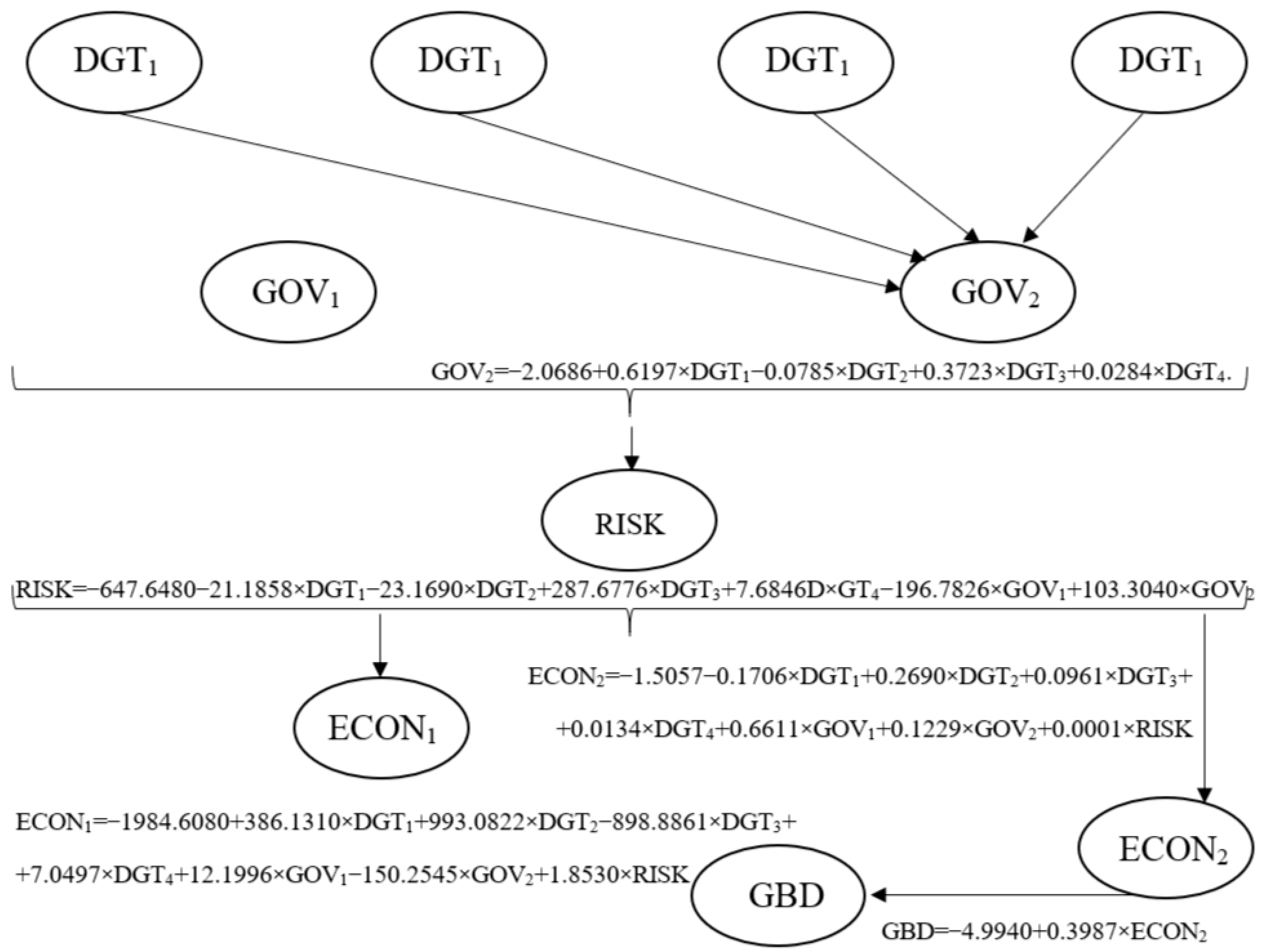

4.2. Cause-and-Effect Relationships of the Change and Digital Management of Risks for Companies during the COVID-19 Crisis

- Digital/technological skills (DGT1) in 2021 compared with that in 2020;

- Digital transformation in companies (DGT3) in 2019 compared with that in 2018;

- Protectionism (GOV1) in 2019 compared with that in 2018;

- Health infrastructure (GOV2) in 2018 compared with that in 2017;

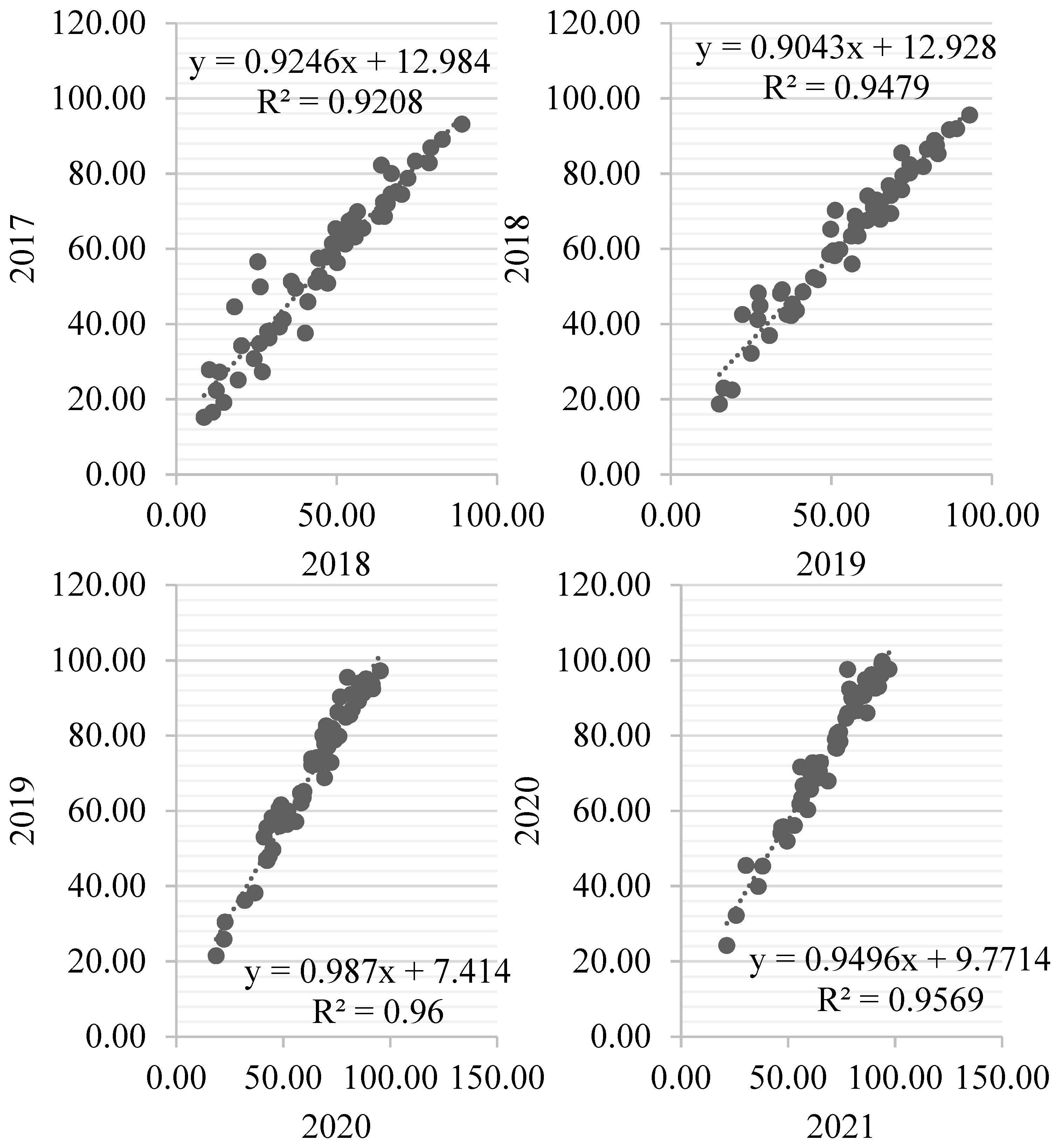

- “listed domestic companies” (RISK) in 2019 compared with those in 2018 and in 2020 compared with in 2019.

4.3. Potential of Digital Management of Risks for Companies under the Conditions of a Crisis of a Non-Economic Nature via the Example of the COVID-19 Pandemic

5. Discussion

6. Conclusions

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Observation | RISK | ECON1 | ECON2 | GBD | GOV2 | |||||

|---|---|---|---|---|---|---|---|---|---|---|

| Predicted RISK | Residuals | Predicted ECON1 | Residuals | Predicted ECON2 | Residuals | Predicted GBD | Residuals | Predicted GOV2 | Residuals | |

| 1 | 437.1073 | −341.1073 | 791.6584 | −148.0301 | 2.7052 | −0.5473 | −4.1337 | −2.5596 | 3.7562 | 0.6122 |

| 2 | 486.1902 | 1526.8098 | 674.6055 | 706.7617 | 5.9143 | −0.6024 | −2.8763 | 0.9344 | 5.4648 | 1.7526 |

| 3 | 778.1272 | −711.1272 | 1400.8041 | −983.5428 | 4.8576 | 1.1906 | −2.5828 | 1.7667 | 5.4595 | 2.5886 |

| 4 | 615.0006 | −499.0006 | 540.4818 | −37.7171 | 5.4934 | −1.3463 | −3.3407 | 2.6569 | 5.3307 | 3.4155 |

| 5 | 628.6902 | −293.6902 | 360.6878 | 1702.8269 | 2.4056 | 0.4787 | −3.8441 | −3.9216 | 4.4742 | −2.6522 |

| 6 | 194.9956 | 121.0044 | −861.2992 | 920.4997 | 2.8857 | 0.1698 | −3.7759 | 5.3981 | 5.2176 | −1.6621 |

| 7 | 731.9983 | 2546.0017 | 1751.1808 | −69.3935 | 5.4563 | 1.2878 | −2.3053 | 2.1950 | 5.9359 | 1.4594 |

| 8 | 262.2065 | −50.2065 | 351.7989 | −74.7230 | 5.7205 | 1.4999 | −2.1155 | −0.5053 | 5.6087 | −0.9754 |

| 9 | 1063.8207 | 2421.1793 | 2204.2606 | 10,106.2299 | 4.1081 | 0.1894 | −3.2807 | −0.5406 | 6.4867 | −1.4950 |

| 10 | 203.6079 | −136.6079 | 104.9160 | 206.9678 | 2.6844 | −0.6154 | −4.1692 | 1.6737 | 3.4651 | −1.2897 |

| 11 | 477.7187 | −322.7187 | 756.1133 | −699.8989 | 2.7334 | 0.8952 | −3.5474 | 4.3005 | 4.4508 | 0.6635 |

| 12 | −171.1790 | 245.1790 | −1046.4973 | 1069.3677 | 3.6188 | 0.9923 | −3.1557 | 5.0549 | 4.0659 | 0.6563 |

| 13 | 532.1477 | −509.1477 | 442.5295 | −223.5934 | 4.9032 | −0.1862 | −3.1135 | 4.6128 | 5.5232 | 1.4580 |

| 14 | 811.7080 | −795.7080 | 492.8692 | −465.9443 | 5.7064 | −0.8867 | −3.0726 | 2.5972 | 5.9931 | −0.7144 |

| 15 | 757.3294 | −292.3294 | 567.4872 | 2027.6639 | 4.9505 | −0.2642 | −3.1257 | 0.1673 | 5.6213 | 2.6559 |

| 16 | 496.5550 | −46.5550 | 421.8043 | 3260.7981 | 5.1465 | 0.9171 | −2.5766 | 3.9157 | 4.8295 | 3.4353 |

| 17 | 242.7985 | −46.7985 | 251.4477 | −47.8593 | 2.9031 | −1.3406 | −4.3711 | 4.9399 | 5.0438 | −1.3295 |

| 18 | 691.5918 | −650.5918 | 997.0235 | −855.5129 | 3.2056 | −0.3222 | −3.8445 | 1.3576 | 4.9029 | −1.9893 |

| 19 | 493.8904 | 5121.1096 | 667.2530 | 1958.3447 | 3.8713 | −1.1790 | −3.9207 | −1.9109 | 5.1087 | −1.6472 |

| 20 | 494.5051 | 71.4949 | 347.6521 | 667.8898 | 3.8687 | 0.1705 | −3.3837 | 0.7801 | 4.1824 | 0.8176 |

| 21 | 243.6591 | −202.6591 | 455.3019 | −119.6386 | 5.9084 | 1.3257 | −2.1100 | 1.8164 | 5.9752 | −1.4645 |

| 22 | 1254.3717 | −823.3717 | 2809.3310 | −2456.6631 | 4.2682 | 0.6652 | −3.0272 | 1.0740 | 7.1099 | −0.0877 |

| 23 | 331.6749 | 37.3251 | −472.2995 | 2434.0959 | 4.7687 | −2.7427 | −4.1863 | 1.7672 | 4.2783 | 2.3061 |

| 24 | 979.0276 | 2618.9724 | −185.6586 | 5116.4960 | 5.1107 | 1.8893 | −2.2033 | −1.1136 | 5.1413 | 2.2929 |

| 25 | 535.6489 | −341.6489 | 1350.9353 | −1310.2268 | 3.8782 | 0.0117 | −3.4432 | 0.8556 | 4.4907 | 1.0833 |

| 26 | 551.6202 | −461.6202 | 1430.6992 | −1263.8933 | 4.4791 | −0.1650 | −3.2741 | −0.9914 | 4.6249 | 0.7194 |

| 27 | 1387.3952 | 726.6048 | 1087.0913 | 535.9829 | 4.0816 | −0.7322 | −3.6587 | 5.8468 | 6.9298 | 0.3321 |

| 28 | 795.6294 | −768.6294 | 945.2202 | −914.7364 | 4.2871 | −1.7743 | −3.9922 | 3.2110 | 6.6328 | −2.5302 |

| 29 | 960.1246 | −932.1246 | 2033.6945 | −1985.9358 | 3.5409 | −0.7478 | −3.8805 | 4.2977 | 6.6867 | −1.2040 |

| 30 | 775.5562 | −747.5562 | 776.0356 | −710.3232 | 5.0945 | 1.2784 | −2.4533 | 3.8202 | 5.6712 | 2.2271 |

| 31 | 1061.6701 | −171.6701 | 2091.3720 | −1772.2628 | 4.4083 | 0.1102 | −3.1926 | 0.2544 | 5.6780 | 1.7109 |

| 32 | 138.2176 | 2.7824 | 181.3832 | 976.8459 | 4.0418 | −1.3233 | −3.9103 | 2.8472 | 4.1839 | −0.7993 |

| 33 | 2.6507 | 215.3493 | −1296.4555 | 1307.9363 | 2.4824 | 0.1843 | −3.9309 | 0.1654 | 3.4327 | −1.2355 |

| 34 | 905.9958 | −803.9958 | 1200.2668 | −367.6376 | 5.9331 | 0.4971 | −2.4305 | 3.7487 | 6.8642 | 1.9149 |

| 35 | 188.6269 | −24.6269 | −208.8377 | 412.5625 | 6.2963 | 0.6057 | −2.2424 | 3.5144 | 4.5643 | 2.5557 |

| 36 | 975.4821 | −795.4821 | 1929.2461 | −1530.8521 | 5.6669 | 1.1528 | −2.2752 | 7.2743 | 6.8743 | 1.6831 |

| 37 | 24.9844 | 193.0156 | −536.6038 | 750.7570 | 3.1744 | −1.0474 | −4.1461 | 1.3120 | 3.2342 | −0.7263 |

| 38 | 541.9590 | −277.9590 | 341.3416 | −12.8609 | 2.9077 | −0.2814 | −3.9470 | 3.5750 | 4.4843 | −0.3833 |

| 39 | 532.7044 | 328.2956 | 819.6529 | −314.9938 | 3.4145 | −0.1514 | −3.6931 | 2.1416 | 5.4206 | −2.2627 |

| 40 | 640.6952 | −597.6952 | −400.9076 | 622.2655 | 4.0752 | −0.0895 | −3.4050 | 0.4490 | 5.4741 | 1.8974 |

| 41 | 985.0466 | −940.0466 | 2641.7800 | −2480.6809 | 5.9641 | 0.2619 | −2.5119 | 0.0238 | 6.6908 | 0.4278 |

| 42 | 128.1210 | −42.1210 | 657.2064 | −445.5105 | 3.1699 | −0.7844 | −4.0430 | 1.4076 | 5.0973 | −2.8563 |

| 43 | 389.2393 | −159.2393 | 415.6918 | 1158.5068 | 2.8628 | 0.2057 | −3.7707 | 2.3018 | 5.0142 | −1.0416 |

| 44 | 616.8316 | −428.8316 | 1474.5720 | −785.9859 | 4.8957 | −0.1589 | −3.1056 | −6.1305 | 5.4265 | 0.8828 |

| 45 | 1048.7074 | −565.7074 | 1977.9357 | −1634.7485 | 5.6425 | 2.0924 | −1.9103 | 4.2021 | 6.8961 | 1.2520 |

| 46 | 829.7674 | −722.7674 | 1623.2816 | −1527.8891 | 2.9909 | −0.6958 | −4.0790 | 3.0967 | 4.8581 | −0.7926 |

| 47 | 710.4776 | −675.4776 | 1887.5003 | −1838.9116 | 4.5560 | −1.0597 | −3.6001 | 3.5360 | 6.7800 | −2.0245 |

| 48 | 115.1602 | 178.8398 | 280.6484 | 68.6197 | 3.8536 | 0.4912 | −3.2619 | −1.1204 | 3.7223 | −0.2135 |

| 49 | 655.7578 | 2454.2422 | 401.6783 | 910.8609 | 4.8244 | −1.2053 | −3.5512 | 0.4479 | 5.3119 | 2.8310 |

| 50 | 1059.9551 | −831.9551 | 1950.1581 | −1245.3862 | 5.9404 | 1.4784 | −2.0363 | 3.1514 | 7.0131 | 2.1835 |

| 51 | 693.8135 | −5.8135 | 622.0959 | −165.7391 | 4.7893 | −0.0496 | −3.1044 | 2.6862 | 4.9650 | 1.3775 |

| 52 | 795.5029 | −421.5029 | 1280.5963 | −421.6077 | 4.4685 | −0.6440 | −3.4693 | 1.2867 | 6.1114 | 0.4243 |

| 53 | 1021.0167 | −894.0167 | 2468.1169 | −2082.5485 | 6.7789 | 0.4126 | −2.1270 | 0.4464 | 7.3127 | 0.4581 |

| 54 | 601.4743 | 1082.5257 | 1228.0495 | 1434.5233 | 5.3069 | 0.8486 | −2.5400 | 0.1222 | 6.1980 | −0.9314 |

| 55 | 952.2794 | 3383.7206 | 3028.5767 | 16,514.4028 | 4.7479 | 1.4291 | −2.5314 | −2.0852 | 6.8501 | −1.0822 |

| 56 | 487.6461 | −394.6461 | 281.2045 | 243.6154 | 2.9755 | −0.5895 | −4.0428 | −1.3983 | 3.7344 | 0.9674 |

| 57 | 792.4713 | 1211.5287 | 1401.9965 | 13.1110 | 6.0862 | −1.1542 | −3.0278 | 2.4945 | 6.0354 | 1.3626 |

| 58 | 874.9428 | −807.9428 | 1070.2815 | −615.1133 | 5.5345 | 0.4234 | −2.6188 | 2.7888 | 5.3604 | 3.1028 |

| 59 | 791.5333 | −680.5333 | 429.1374 | 114.1364 | 5.4203 | −1.6942 | −3.5086 | 2.6387 | 5.4995 | 3.1672 |

| 60 | 515.7988 | −181.7988 | 164.6722 | 1752.2618 | 3.0174 | 0.3499 | −3.6516 | −3.3077 | 4.4175 | −2.4288 |

| 61 | 189.3884 | 101.6116 | −360.9752 | 427.3368 | 3.7544 | 0.6456 | −3.2399 | 4.9672 | 5.6600 | −3.3933 |

| 62 | 812.4578 | 2517.5422 | 1894.8550 | −168.8348 | 5.6727 | 0.5160 | −2.5268 | 2.8865 | 6.4930 | 1.2052 |

| 63 | 354.9452 | −149.9452 | 188.6310 | 109.6001 | 5.4246 | 1.4845 | −2.2396 | 0.7714 | 5.9184 | −1.1407 |

| 64 | 1258.2058 | 2325.7942 | 2527.9652 | 11,366.9419 | 4.5598 | 0.4052 | −3.0146 | −1.2526 | 7.0095 | −1.3172 |

| 65 | 246.6397 | −180.6397 | 379.0904 | −44.8922 | 2.4559 | −0.5621 | −4.2390 | −0.4286 | 3.7482 | −1.2257 |

| 66 | 521.7323 | −394.7323 | 449.4775 | −387.2296 | 2.8224 | 0.3370 | −3.7345 | 3.7047 | 4.6813 | −0.1306 |

| 67 | −42.4716 | 133.4716 | −799.0110 | 824.5350 | 3.3720 | 0.7232 | −3.3614 | −0.2702 | 3.8211 | 0.7979 |

| 68 | 594.5839 | −571.5839 | 146.4659 | 102.7830 | 5.7818 | 0.0643 | −2.6633 | 3.5549 | 5.9424 | 1.3268 |

| 69 | 787.4924 | −769.4924 | 667.9899 | −637.5000 | 6.1517 | −1.6205 | −3.1875 | 2.6321 | 6.3419 | −0.1856 |

| 70 | 540.5973 | −83.5973 | 833.7283 | 1957.2285 | 5.6426 | −0.9503 | −3.1233 | 0.8344 | 6.1130 | 1.9452 |

| 71 | 468.8869 | −3.8869 | 168.6975 | 3808.5919 | 5.0648 | 0.4894 | −2.7797 | 4.6930 | 4.1480 | 4.1050 |

| 72 | 613.0593 | −430.0593 | 1153.4987 | −941.2493 | 3.1791 | −1.8541 | −4.4658 | 5.3972 | 5.7367 | −1.6617 |

| 73 | 693.0180 | −650.0180 | 1082.3192 | −924.4363 | 3.7609 | −0.2053 | −3.5765 | 1.4283 | 5.2047 | −2.1066 |

| 74 | 616.3022 | 4448.6978 | 926.8075 | 1847.1924 | 4.2808 | −1.4441 | −3.8631 | −1.9495 | 5.2941 | −1.0084 |

| 75 | 771.9200 | −152.9200 | 591.9062 | 450.2670 | 4.1154 | 0.3164 | −3.2272 | 1.0305 | 4.8492 | 0.1054 |

| 76 | 344.9839 | −301.9839 | 163.5314 | 219.1427 | 5.6152 | 0.9448 | −2.3787 | 2.5241 | 6.0844 | −1.8044 |

| 77 | 1326.8385 | −906.8385 | 2534.8241 | −2161.1828 | 5.1192 | −0.0460 | −2.9715 | 0.0741 | 7.6469 | −1.0127 |

| 78 | 422.2689 | −23.2689 | −93.1939 | 2185.1262 | 4.5264 | −2.6734 | −4.2553 | 2.0691 | 4.5356 | 2.3681 |

| 79 | 981.2331 | 2670.7669 | 589.7953 | 4448.0400 | 5.1170 | 1.0163 | −2.5488 | 0.0766 | 5.6430 | 2.3066 |

| 80 | 631.0638 | −436.0638 | 2032.8602 | −1989.9278 | 4.7578 | −1.6238 | −3.7446 | 1.3563 | 5.6508 | 0.6228 |

| 81 | 544.1948 | −447.1948 | 1022.6742 | −843.3343 | 4.2094 | −0.0844 | −3.3495 | 5.9291 | 4.5957 | 0.0293 |

| 82 | 1581.0703 | 604.9297 | 1810.6111 | −85.2377 | 4.6443 | −1.0640 | −3.5667 | 6.1297 | 6.9884 | 0.7366 |

| 83 | 603.1790 | −579.1790 | 1327.1652 | −1292.7362 | 4.7145 | −1.5062 | −3.7150 | 2.8746 | 6.4924 | −2.9605 |

| 84 | 869.7252 | −841.7252 | 2267.5290 | −2213.7781 | 3.8244 | 0.0544 | −3.4477 | 3.9848 | 6.7221 | −1.1463 |

| 85 | 571.4936 | −544.4936 | 785.8581 | −714.5734 | 5.6883 | 1.6260 | −2.0780 | 5.0643 | 5.2610 | 2.6819 |

| 86 | 1004.3769 | −102.3769 | 2113.3407 | −1754.5518 | 4.7515 | 0.3152 | −2.9741 | −0.7133 | 5.6961 | 1.1706 |

| 87 | 357.8798 | −217.8798 | 298.1347 | 925.2242 | 3.6963 | −1.4785 | −4.1098 | 1.9137 | 4.5925 | −1.1865 |

| 88 | 60.5249 | 155.4751 | −851.5278 | 864.7059 | 2.2349 | 0.6136 | −3.8584 | 6.7127 | 3.4003 | −1.1849 |

| 89 | 1002.0882 | −899.0882 | 1520.1650 | −606.8467 | 6.0812 | 0.5855 | −2.3362 | 3.7668 | 7.0639 | 1.4428 |

| 90 | 161.4946 | −30.4946 | −342.7317 | 552.1158 | 5.8771 | 1.1573 | −2.1896 | 3.4413 | 4.8544 | 1.0294 |

| 91 | 985.6543 | −799.6543 | 1606.0306 | −1169.0309 | 6.3664 | 0.9039 | −2.0956 | 9.9591 | 6.9506 | 1.8439 |

| 92 | 6.5612 | 204.4388 | −329.9797 | 555.3854 | 3.6807 | −1.2389 | −4.0205 | 2.0585 | 3.7731 | −1.2382 |

| 93 | 489.0184 | −225.0184 | 585.1044 | −238.2625 | 2.5764 | 0.4236 | −3.7980 | 2.2455 | 3.9762 | −0.1657 |

| 94 | 374.0492 | 448.9508 | 968.3543 | −380.9452 | 3.9980 | 0.4918 | −3.2041 | 2.9593 | 5.6716 | −2.6512 |

| 95 | 469.4999 | −426.4999 | −230.1836 | 472.4967 | 4.9137 | 0.1874 | −2.9603 | 2.6113 | 5.8065 | 1.2721 |

| 96 | 1116.4272 | −1070.4272 | 2971.9395 | −2788.6046 | 6.1112 | −0.1988 | −2.6369 | 8.2407 | 7.2724 | 0.4667 |

| 97 | 267.3436 | −182.3436 | 897.2571 | −655.8007 | 3.2621 | −0.9287 | −4.0638 | 1.2232 | 5.7576 | −3.6909 |

| 98 | 410.9344 | −189.9344 | 174.3220 | 1483.0068 | 2.5941 | 0.7046 | −3.6789 | 6.6022 | 4.8378 | −1.0975 |

| 99 | 716.3317 | −516.3317 | 871.5920 | −55.0133 | 4.8907 | 0.3623 | −2.8998 | −2.7544 | 5.5527 | 0.3759 |

| 100 | 1047.0055 | −565.0055 | 1671.5931 | −1294.6066 | 5.8051 | 1.8126 | −1.9571 | 2.6137 | 7.0317 | 0.9978 |

| 101 | 110.4857 | −7.4857 | 1519.8752 | −1414.2624 | 3.1656 | −1.3851 | −4.2842 | 3.2722 | 5.3191 | −3.0021 |

| 102 | 790.4793 | −759.4793 | 1966.4756 | −1912.3123 | 4.7262 | −0.5106 | −3.3133 | 4.0486 | 6.9630 | −2.3888 |

| 103 | 208.4564 | 80.5436 | −146.8161 | 551.6574 | 3.5842 | −0.4874 | −3.7594 | 0.0233 | 3.7765 | −0.0716 |

| 104 | 719.5717 | 2259.4283 | 468.3278 | 952.6664 | 5.2328 | −1.3504 | −3.4462 | 0.8513 | 5.5679 | 2.6204 |

| 105 | 1112.6708 | −876.6708 | 1994.3967 | −1258.8636 | 5.7756 | 1.3050 | −2.1712 | 3.4441 | 6.9286 | 2.0390 |

| 106 | 809.2043 | −105.2043 | 738.6682 | −231.9141 | 4.9287 | −0.2508 | −3.1290 | 3.1923 | 5.1713 | 1.0321 |

| 107 | 718.8156 | −341.8156 | 1367.1009 | −588.6242 | 4.8693 | −1.2154 | −3.5373 | −0.1972 | 6.2097 | 0.3672 |

| 108 | 1150.6587 | −1020.6587 | 1979.0209 | −1556.6928 | 6.4219 | 1.0003 | −2.0350 | 3.1568 | 7.2694 | 0.5973 |

| 109 | 665.9359 | 1007.0641 | 2210.4023 | 690.5830 | 5.4214 | 0.5147 | −2.6274 | 0.4682 | 6.1920 | −0.1275 |

| 110 | 1105.8308 | 3291.1692 | 3214.4267 | 17,312.7321 | 5.1000 | 1.0818 | −2.5295 | −2.9091 | 7.0896 | −0.7112 |

| 111 | 524.5183 | −433.5183 | 803.9233 | −351.1048 | 3.2913 | −0.9246 | −4.0505 | −0.3445 | 4.5070 | 0.1371 |

| 112 | 607.8430 | 1344.1570 | 1664.1141 | −277.9890 | 6.5927 | −0.7177 | −2.6518 | 2.6167 | 6.0699 | 1.4620 |

| 113 | 741.7190 | −670.7190 | 991.0111 | −545.9988 | 5.5021 | 1.0254 | −2.3917 | 3.0020 | 5.4940 | 2.9016 |

| 114 | 516.0622 | −408.0622 | 1120.4275 | −585.1388 | 5.8334 | −1.3857 | −3.2208 | 1.2682 | 5.4308 | 3.1961 |

| 115 | 652.7548 | −328.7548 | 802.3887 | 1070.8995 | 2.2643 | 1.7097 | −3.4097 | −2.3982 | 4.3372 | −2.1934 |

| 116 | 618.8076 | −356.8076 | 2211.6540 | −2142.7404 | 2.6973 | −0.1008 | −3.9589 | 6.0779 | 5.6189 | −2.7768 |

| 117 | 861.3342 | 2496.6658 | 1954.9159 | −186.0828 | 5.8465 | 0.3535 | −2.5223 | 2.5265 | 6.4763 | 0.8487 |

| 118 | 58.9066 | 144.0934 | 477.5511 | −195.2330 | 4.8868 | 0.8878 | −2.6918 | 0.0013 | 5.5744 | −1.3490 |

| 119 | 1145.9901 | 2631.0099 | 2560.8575 | 11,719.1110 | 5.2564 | −0.1897 | −2.9741 | −3.1537 | 7.1807 | −1.2400 |

| 120 | 325.9018 | −259.9018 | 515.4729 | −192.3633 | 2.6554 | −0.0412 | −3.9518 | 0.4701 | 4.2991 | −1.1967 |

| 121 | 421.1450 | −302.1450 | 961.2311 | −898.9849 | 3.1993 | 0.4183 | −3.5518 | 3.7867 | 4.5332 | −0.4463 |

| 122 | −273.6192 | 369.6192 | −545.7965 | 571.5556 | 3.4488 | 0.1512 | −3.5588 | 4.8356 | 3.8694 | 0.0806 |

| 123 | 567.1229 | −544.1229 | 1344.4224 | −1091.8022 | 5.1192 | 0.3324 | −2.8206 | 3.1090 | 5.6538 | 0.7656 |

| 124 | 525.7816 | −507.7816 | 530.5266 | −499.4813 | 5.2159 | −0.3159 | −3.0405 | 3.1624 | 5.4430 | −0.1430 |

| 125 | 505.0980 | −51.0980 | 848.9980 | 1879.8723 | 5.4272 | −1.7481 | −3.5273 | 0.4627 | 5.7696 | 2.6501 |

| 126 | 105.7261 | 364.2739 | −48.0290 | 3936.3558 | 5.5651 | 0.6755 | −2.5061 | 3.9772 | 3.8959 | 4.3025 |

| 127 | 466.6245 | −290.6245 | 1329.5232 | −1124.1959 | 2.6650 | −0.6962 | −4.2091 | 5.3563 | 5.1591 | −1.2529 |

| 128 | 617.6935 | −573.6935 | 1105.0236 | −944.0564 | 3.9123 | 0.2572 | −3.3318 | 1.2126 | 4.9083 | −1.5237 |

| 129 | 542.7019 | 4611.2981 | 1272.0711 | 1616.2775 | 4.6135 | −1.1044 | −3.5950 | −3.5300 | 5.8403 | −1.2867 |

| 130 | 957.3152 | −289.3152 | 2094.2042 | −975.1130 | 4.4293 | 0.3268 | −3.0979 | 1.2283 | 5.4568 | 0.3951 |

| 131 | 101.8632 | −58.8632 | 1007.8094 | −608.6876 | 6.1741 | 1.2953 | −2.0162 | 2.4998 | 6.0738 | −2.1988 |

| 132 | 1252.6979 | −838.6979 | 3090.7022 | −2692.7676 | 4.8484 | 0.2627 | −2.9564 | −0.7231 | 7.5148 | −1.6036 |

| 133 | 379.4899 | 34.5101 | 386.2206 | 1625.0652 | 4.4128 | −2.2867 | −4.1464 | 2.6062 | 4.3474 | 2.4994 |

| 134 | 816.4930 | 2887.5070 | 179.7704 | 4943.5477 | 4.8903 | 1.0772 | −2.6150 | −0.4153 | 4.8250 | 2.4147 |

| 135 | 741.4089 | −550.4089 | 2156.0721 | −2111.5693 | 4.8557 | −1.1634 | −3.5220 | 0.1736 | 5.6242 | 0.3098 |

| 136 | 574.6556 | −480.6556 | 1761.1885 | −1579.5213 | 4.8415 | −2.2541 | −3.9625 | 3.3930 | 4.8173 | 0.0639 |

| 137 | 1640.0858 | 621.9142 | 2066.5937 | −415.1708 | 4.2048 | −0.0421 | −3.3344 | 3.7062 | 7.0625 | 0.3561 |

| 138 | 384.3835 | −363.3835 | 1231.1255 | −1196.8168 | 4.9977 | −1.6227 | −3.6485 | 3.0808 | 6.6686 | −2.7103 |

| 139 | 850.0265 | −821.0265 | 2489.8287 | −2435.1313 | 4.3185 | −0.5471 | −3.4905 | 3.9641 | 6.8928 | −0.9786 |

| 140 | 468.8703 | −440.8703 | 538.2755 | −468.0800 | 5.8406 | 1.3816 | −2.1147 | 4.4144 | 5.1554 | 2.8165 |

| 141 | 1053.7496 | −134.7496 | 2581.8556 | −2216.5767 | 5.2523 | −0.0627 | −2.9250 | −0.4783 | 6.4885 | 0.9353 |

| 142 | 412.3537 | −273.3537 | 950.9342 | 307.3503 | 2.6650 | 0.5231 | −3.7230 | 1.3745 | 4.1001 | −0.7733 |

| 143 | 320.2542 | −121.2542 | 143.9051 | −129.6988 | 1.4567 | 0.9845 | −4.0208 | 4.9152 | 3.4006 | −1.2536 |

| 144 | 797.6335 | −694.6335 | 2080.1409 | −1173.1426 | 6.7741 | −0.0144 | −2.2991 | 4.0263 | 7.3081 | 1.2110 |

| 145 | 505.5336 | −382.5336 | 1146.8861 | −935.9998 | 5.7922 | 0.9331 | −2.3128 | −0.1570 | 5.6626 | 0.8869 |

| 146 | 981.5285 | −795.5285 | 2020.3191 | −1615.3777 | 6.0471 | 1.1421 | −2.1279 | 8.7116 | 7.0300 | 0.8349 |

| 147 | −49.4561 | 245.4561 | −391.0747 | 621.9621 | 3.4797 | −0.8050 | −3.9277 | 2.5498 | 3.7981 | −2.0149 |

| 148 | 437.7307 | −172.7307 | 784.3168 | −407.4934 | 3.6608 | −0.4282 | −3.7053 | 2.0474 | 4.6208 | −0.5976 |

| 149 | 627.0237 | 170.9763 | 1850.1446 | −1252.8601 | 3.9296 | 0.5778 | −3.1970 | 2.4600 | 5.5820 | −2.6123 |

| 150 | 354.4497 | −311.4497 | 676.1894 | −436.2025 | 4.2165 | −0.0498 | −3.3329 | 3.4482 | 5.4949 | 1.1908 |

| 151 | 1207.2293 | −1160.2293 | 3171.9089 | −2996.0714 | 6.5279 | −0.6719 | −2.6594 | 7.2437 | 7.6503 | 0.3180 |

| 152 | 632.5845 | −551.5845 | 1859.3084 | −1609.4283 | 2.5888 | 0.6576 | −3.6998 | −0.6498 | 5.5035 | −2.4020 |

| 153 | 431.2340 | −218.2340 | 1389.4170 | 303.6980 | 3.4236 | 0.6304 | −3.3778 | 5.3074 | 4.7684 | −1.2009 |

| 154 | 734.8808 | −530.8808 | 1673.1824 | −869.5662 | 5.5029 | 0.0833 | −2.7670 | −1.6184 | 6.5621 | −0.5162 |

| 155 | 1001.8981 | −531.8981 | 2196.0992 | −1820.6150 | 6.4107 | 1.1028 | −1.9986 | 2.1636 | 7.3038 | 1.1557 |

| 156 | 767.8319 | −670.8319 | 2240.8475 | −2135.5631 | 1.8537 | 0.6463 | −3.9973 | 2.7014 | 5.7144 | −2.5674 |

| 157 | 919.7612 | −890.7612 | 2526.6768 | −2472.4976 | 4.8344 | −0.7158 | −3.3520 | 3.7810 | 7.2380 | −1.6787 |

| 158 | 268.8538 | 5.1462 | 1362.6444 | −974.7106 | 2.8889 | 0.8853 | −3.4894 | −1.2277 | 3.7457 | −0.6812 |

| 159 | 613.8385 | 2256.1615 | 1114.3249 | 278.7212 | 4.9620 | −0.5409 | −3.2315 | 0.1684 | 5.7476 | 2.4103 |

| 160 | 848.7126 | −611.7126 | 2164.0740 | −1432.2581 | 6.3787 | 1.0638 | −2.0269 | 3.3510 | 7.0321 | 1.8797 |

| 161 | 835.9006 | −110.9006 | 1270.4199 | −726.3390 | 5.0439 | 0.0149 | −2.9772 | 2.1657 | 5.6008 | 0.8698 |

| 162 | 952.0725 | −574.0725 | 1893.7428 | −1132.7409 | 3.6934 | −0.4341 | −3.6946 | −1.0542 | 6.0318 | 0.8941 |

| 163 | 1125.9117 | −995.9117 | 3107.5916 | −2690.3760 | 7.2448 | 0.9608 | −1.7227 | 2.1586 | 7.6835 | 0.5969 |

| 164 | 472.7708 | 1194.2292 | 1991.7360 | 886.9379 | 5.5475 | −0.2236 | −2.8715 | 0.6621 | 5.9560 | 0.4155 |

| 165 | 958.7020 | 3775.2980 | 3449.8599 | 17,922.7224 | 4.8914 | 1.3451 | −2.5077 | −3.2206 | 7.0397 | −1.5774 |

| 166 | 1062.6934 | −971.6934 | 2044.7632 | −1655.1719 | 2.0447 | −0.4360 | −4.3527 | −4.2728 | 5.0810 | −0.5032 |

| 167 | 664.0992 | 1237.9008 | 1885.3246 | −532.3949 | 6.4902 | −0.3538 | −2.5476 | −1.7913 | 6.4222 | 1.1005 |

| 168 | 727.6856 | −659.6856 | 1251.1728 | −817.9138 | 6.1919 | 1.0303 | −2.1147 | −5.9305 | 5.8912 | 3.2755 |

| 169 | 558.5586 | −450.5586 | 1342.2520 | −820.3912 | 5.9741 | −1.7279 | −3.3012 | −5.7427 | 5.7445 | 2.8709 |

| 170 | 623.4588 | −278.4588 | 1088.8957 | 359.6700 | 3.3224 | 0.5582 | −3.4469 | −10.1501 | 4.7751 | −1.5662 |

| 171 | 758.7580 | −499.7580 | 2174.3994 | −2104.5115 | 3.3841 | 1.1492 | −3.1867 | −0.7964 | 6.2942 | −2.6053 |

| 172 | 1027.4720 | 2894.5280 | 2775.5467 | −1049.8610 | 6.2990 | 0.4307 | −2.3111 | −8.5210 | 7.1817 | 0.3588 |

| 173 | 10.0673 | 183.9327 | 363.4542 | −110.5142 | 5.8294 | 0.5474 | −2.4518 | −4.6822 | 5.7331 | −1.1361 |

| 174 | 1342.5768 | 2811.4232 | 3495.4431 | 11,192.3004 | 5.4906 | 0.1888 | −2.7298 | −8.0906 | 7.6548 | −1.2273 |

| 175 | 421.8690 | −356.8690 | 1143.6858 | −873.3859 | 2.7659 | 0.0508 | −3.8711 | −3.1045 | 4.3688 | −1.1824 |

| 176 | 601.7665 | −497.7665 | 1060.8185 | −1003.6147 | 3.0687 | 0.4796 | −3.5794 | −3.7446 | 5.2867 | −0.4534 |

| 177 | 309.9527 | −217.9527 | 419.4815 | −394.7895 | 4.1078 | 0.8922 | −3.0007 | −2.7561 | 4.9027 | 1.1358 |

| 178 | 950.6490 | −927.6490 | 2078.9672 | −1833.5362 | 4.8343 | −0.2306 | −3.1586 | −2.6206 | 6.1448 | 0.3080 |

| 179 | 730.4836 | −712.4836 | 661.8090 | −631.1581 | 5.7293 | −0.8818 | −3.0615 | −2.5346 | 5.8626 | 0.6374 |

| 180 | 524.0082 | −73.0082 | 1511.6599 | 1118.6579 | 5.3439 | −0.0733 | −2.8928 | −6.0323 | 5.8921 | 1.6317 |

| 181 | 104.3187 | 333.6813 | 254.7594 | 3591.6545 | 5.9228 | 0.3139 | −2.5076 | −1.8055 | 4.1920 | 4.2485 |

| 182 | 449.2219 | −278.2219 | 754.8781 | −566.0434 | 4.1893 | −1.6461 | −3.9801 | −6.1732 | 5.3308 | −0.0468 |

| 183 | 634.8819 | −589.8819 | 1400.7719 | −1245.7590 | 3.4424 | 0.7462 | −3.3241 | −4.5527 | 5.2803 | −2.3660 |

| 184 | 574.7761 | 4640.2239 | 1545.0108 | 1084.1510 | 4.7118 | −0.9303 | −3.4864 | −10.0385 | 6.0712 | −1.3653 |

| 185 | 980.7250 | −267.7250 | 2207.3175 | −1148.8937 | 4.4218 | −0.4643 | −3.4163 | 1.4257 | 5.6718 | −0.0159 |

| 186 | 470.3106 | −427.3106 | 1147.0881 | −721.1985 | 6.1885 | 0.6865 | −2.2531 | −2.8773 | 6.1827 | −1.3911 |

| 187 | 1262.7405 | −836.7405 | 3431.5731 | −3024.4722 | 4.8424 | 0.5723 | −2.8354 | −6.7093 | 7.0168 | −1.1144 |

| 188 | 323.2984 | 90.7016 | 372.4051 | 1520.1690 | 4.9163 | −2.9343 | −4.2039 | −5.3933 | 4.7835 | 2.3415 |

| 189 | 740.1004 | 3013.8996 | 94.4189 | 4945.6888 | 4.8704 | 1.5227 | −2.4452 | −6.5064 | 4.7477 | 2.5173 |

| 190 | 824.0553 | −645.0553 | 2341.6947 | −2297.9975 | 5.0007 | −1.7661 | −3.7045 | −3.3285 | 6.0077 | 0.0416 |

| 191 | 598.4461 | −504.4461 | 1846.8102 | −1675.7279 | 4.8230 | −1.7572 | −3.7718 | −3.2651 | 5.1177 | −0.7756 |

| 192 | 1757.9704 | 560.0296 | 3154.2534 | −1516.3579 | 4.9027 | −1.9298 | −3.8088 | 1.5670 | 7.4879 | 0.5121 |

| 193 | 870.0694 | −852.0694 | 2039.1291 | −2005.5112 | 4.7237 | −0.9904 | −3.5056 | 3.0572 | 6.7296 | −1.9296 |

| 194 | 869.0247 | −842.0247 | 2451.7501 | −2395.2032 | 4.6516 | −0.3928 | −3.2961 | −3.9854 | 6.9905 | −1.1552 |

| 195 | 511.3141 | −482.3141 | 306.6891 | −233.3361 | 5.9055 | 1.4660 | −2.0552 | −1.3648 | 5.3889 | 2.6397 |

| 196 | 1134.9336 | −207.9336 | 2484.6914 | −2147.6839 | 4.8919 | −0.1766 | −3.1142 | −3.0728 | 6.4870 | 0.8115 |

| 197 | 655.6299 | −515.6299 | 1799.4553 | −723.2920 | 2.5149 | 0.2660 | −3.8853 | −0.5838 | 5.1189 | −1.9733 |

| 198 | 530.4277 | −338.4277 | 552.6710 | −539.3580 | 1.9187 | 0.8929 | −3.8731 | −5.3625 | 3.6020 | −0.4136 |

| 199 | 888.7154 | −785.7154 | 2198.9987 | −1286.4982 | 6.7721 | −0.2147 | −2.3798 | −1.3236 | 7.4929 | 0.8186 |

| 200 | 145.5856 | −23.5856 | 357.2969 | −147.0973 | 5.9019 | 1.8608 | −1.8992 | −2.1345 | 5.1566 | 0.9450 |

| 201 | 1096.4768 | −910.4768 | 2720.1027 | −2357.9044 | 6.3696 | 0.1637 | −2.3894 | −0.2252 | 7.3212 | 0.9121 |

| 202 | 214.9676 | −15.9676 | 91.0444 | 114.2233 | 3.8503 | −0.8366 | −3.7925 | −4.5401 | 4.4447 | −2.2193 |

| 203 | 584.3196 | −316.3196 | 1491.8706 | −1130.3812 | 3.6693 | −0.1804 | −3.6031 | −2.1299 | 4.9970 | −0.8172 |

| 204 | 761.1296 | 20.8704 | 2461.6271 | −1865.0092 | 4.2568 | 0.6048 | −3.0559 | −3.8930 | 6.0680 | −2.5055 |

| 205 | 508.1199 | −465.1199 | 611.8938 | −383.3545 | 4.1888 | −0.1156 | −3.3702 | −2.4694 | 5.6514 | 1.2023 |

| 206 | 1281.0201 | −1234.0201 | 3658.0520 | −3513.6407 | 6.8455 | −0.7380 | −2.5591 | 3.5900 | 7.8516 | 0.5397 |

| 207 | 413.0221 | −332.0221 | 1523.2166 | −1273.7048 | 2.9635 | 0.4827 | −3.6201 | −5.6889 | 5.5189 | −2.5189 |

| 208 | 277.0542 | −64.0542 | 1653.7460 | −165.4243 | 3.7459 | 0.6141 | −3.2558 | −0.7457 | 4.9203 | −1.0011 |

| 209 | 1030.5755 | −823.5755 | 1857.4852 | −1154.1175 | 5.8241 | 0.3188 | −2.5450 | −8.7189 | 7.0700 | 0.5532 |

| 210 | 1054.2914 | −595.2914 | 2750.3769 | −2405.0914 | 6.7729 | 0.9902 | −1.8991 | −8.9251 | 7.5803 | 1.2731 |

| 211 | 732.0948 | −639.0948 | 2774.2420 | −2669.0697 | 1.5390 | 0.4013 | −4.2205 | −1.2478 | 5.5317 | −3.2631 |

| 212 | 783.0058 | −756.0058 | 2395.7792 | −2342.1896 | 5.2605 | −0.6494 | −3.1557 | −5.1411 | 6.9786 | −1.5393 |

| 213 | 183.1656 | 80.8344 | 590.9739 | −255.5319 | 2.7398 | 0.1593 | −3.8382 | −5.8967 | 3.2121 | −0.5084 |

| 214 | 708.8498 | 2002.1502 | 1412.8730 | −131.3883 | 4.4471 | −0.3945 | −3.3784 | −6.8895 | 5.5877 | 2.4470 |

| 215 | 892.1540 | −656.1540 | 2263.8983 | −1511.7491 | 6.6203 | 0.8425 | −2.0188 | −0.8006 | 7.1987 | 1.7101 |

| 216 | 1148.2591 | −405.2591 | 1893.3962 | −1393.7141 | 4.8005 | 0.1067 | −3.0377 | −1.7438 | 6.1249 | 1.3803 |

| 217 | 1158.2142 | −787.2142 | 2312.3086 | −1592.2105 | 4.4404 | −0.4040 | −3.3848 | −1.7064 | 6.6627 | 0.3191 |

| 218 | 1228.8664 | −1098.8664 | 2913.8990 | −2556.6805 | 6.7935 | 1.1039 | −1.8455 | −3.3716 | 7.6055 | 0.5227 |

| 219 | 781.2840 | 885.7160 | 2322.6674 | 434.2329 | 5.5607 | 0.3217 | −2.6489 | −10.1118 | 6.8432 | −0.8726 |

| 220 | 959.3801 | 3143.6199 | 3380.6825 | 17,513.0630 | 5.1239 | 0.5320 | −2.7392 | −11.7525 | 7.3812 | −2.2725 |

| 221 | 1115.5037 | −1024.5037 | 2017.0918 | −1525.5993 | 1.5798 | 0.7138 | −4.0796 | −0.4749 | 4.4082 | −0.6101 |

| 222 | 926.0551 | 975.9449 | 1943.5231 | −311.5171 | 5.6887 | −1.3705 | −3.2725 | −2.9045 | 6.3145 | 1.0037 |

| 223 | 1219.2642 | −1151.2642 | 2126.4402 | −1649.3582 | 5.2393 | 0.6866 | −2.6315 | −3.2862 | 5.9178 | 2.9217 |

| 224 | 666.3840 | −558.3840 | 1151.9832 | −552.9564 | 6.1308 | −2.1308 | −3.3993 | −2.1223 | 6.0271 | 2.4993 |

| 225 | 912.4096 | −567.4096 | 1390.5064 | 218.4749 | 2.7617 | 1.2205 | −3.4065 | −1.0139 | 4.9655 | −1.5601 |

| 226 | 621.8992 | −362.8992 | 1719.3569 | −1639.0896 | 2.9044 | 0.0086 | −3.8327 | −0.2599 | 5.6445 | −2.1662 |

| 227 | 1006.2113 | 2915.7887 | 2771.9115 | −700.0846 | 5.9106 | −0.1459 | −2.6958 | −1.8274 | 7.1406 | −0.1112 |

| 228 | 557.8372 | −363.8372 | 1221.5747 | −904.5162 | 5.2611 | −0.4442 | −3.0737 | −4.4443 | 6.2745 | −1.0914 |

| 229 | 1285.9756 | 2868.0244 | 3072.7276 | 14,661.4033 | 5.6035 | −0.1616 | −2.8245 | −3.0763 | 7.5183 | −0.8051 |

| 230 | 503.6747 | −438.6747 | 681.6681 | −367.3458 | 3.0456 | −0.6639 | −4.0445 | −2.7879 | 4.2953 | −0.2023 |

| 231 | 888.1194 | −784.1194 | 1794.9750 | −1727.1372 | 2.8060 | 0.0318 | −3.8627 | 0.9798 | 5.6518 | −1.4626 |

| 232 | 470.1443 | −378.1443 | 349.4053 | −321.7848 | 3.9980 | 0.4835 | −3.2074 | 1.5425 | 5.0321 | 1.1944 |

| 233 | 1104.4658 | −1081.4658 | 2053.1676 | −1770.6337 | 5.0566 | −0.5142 | −3.1831 | −2.6848 | 6.5264 | 0.5402 |

| 234 | 722.3520 | −704.3520 | 1137.7297 | −1101.4669 | 5.2563 | −0.1220 | −2.9471 | 0.5942 | 5.6849 | 0.8524 |

| 235 | 729.0355 | −278.0355 | 1307.5277 | 1629.9451 | 5.3583 | −0.1083 | −2.9010 | −3.5778 | 6.2904 | 1.1455 |

| 236 | 361.2792 | 76.7208 | 297.2191 | 3925.8971 | 5.3042 | 0.7551 | −2.5784 | −1.1312 | 4.4396 | 3.6197 |

| 237 | 533.8466 | −362.8466 | 1195.0617 | −978.8213 | 4.4665 | −0.9978 | −3.6111 | −3.8215 | 5.6392 | −0.1154 |

| 238 | 804.9002 | −759.9002 | 1500.1387 | −1317.8571 | 3.6419 | 0.2376 | −3.4474 | −3.3264 | 5.4777 | −1.9356 |

| 239 | 901.3082 | 4313.6918 | 2219.1234 | 921.4782 | 4.7277 | −0.8011 | −3.4286 | −6.3821 | 6.3989 | −1.7567 |

| 240 | 969.4231 | −256.4231 | 1239.9670 | −53.8740 | 4.7703 | −0.3649 | −3.2377 | −2.6924 | 5.7850 | −0.3255 |

| 241 | 289.4693 | −246.4693 | 1041.7522 | −543.1929 | 5.8754 | 0.8704 | −2.3047 | 0.3805 | 6.2822 | −1.6721 |

| 242 | 1365.2783 | −939.2783 | 3465.7381 | −2984.1470 | 4.9178 | −0.3687 | −3.1805 | −0.7421 | 7.0713 | −0.0313 |

| 243 | 460.7369 | −46.7369 | 988.9260 | 1110.9528 | 5.1729 | −3.2979 | −4.2465 | −2.9814 | 5.2862 | 1.3745 |

| 244 | 811.2145 | 2942.7855 | 157.7346 | 4779.6882 | 4.8665 | 2.1070 | −2.2139 | −5.4028 | 4.6344 | 2.0559 |

| 245 | 829.5364 | −650.5364 | 2739.3990 | −2694.1553 | 6.0295 | −1.7271 | −3.2788 | −2.1099 | 6.6991 | −0.2108 |

| 246 | 818.5377 | −724.5377 | 2422.5255 | −2231.7113 | 5.0402 | −1.8510 | −3.7226 | −0.3733 | 5.4753 | −0.6935 |

| 247 | 1658.3290 | 659.6710 | 2509.1721 | −710.6276 | 5.0293 | −2.6439 | −4.0431 | 3.4039 | 7.0472 | 1.0996 |

| 248 | 738.9701 | −720.9701 | 2640.9173 | −2601.9855 | 4.8100 | −0.9433 | −3.4525 | 2.7173 | 6.6978 | −1.7644 |

| 249 | 816.1794 | −789.1794 | 2254.2713 | −2188.8355 | 4.4006 | −0.5272 | −3.4498 | 2.4474 | 6.8838 | −1.1370 |

| 250 | 733.8969 | −704.8969 | 1160.1920 | −1073.4806 | 5.9217 | 1.3482 | −2.0957 | 2.9821 | 6.0697 | 1.9303 |

| 251 | 1456.9610 | −529.9610 | 2702.2236 | −2329.5220 | 4.5065 | −0.1922 | −3.2740 | −3.1226 | 6.8106 | 0.6179 |

| 252 | 907.8267 | −767.8267 | 2036.3910 | −743.3537 | 2.1205 | 1.4372 | −3.5757 | −0.2265 | 5.1851 | −2.4008 |

| 253 | 731.4857 | −539.4857 | −250.8989 | 265.9969 | 1.5826 | 1.3139 | −3.8393 | 0.3822 | 4.0687 | −1.3669 |

| 254 | 997.4641 | −894.4641 | 2309.2309 | −1318.9849 | 6.7313 | −0.3274 | −2.4410 | −0.1733 | 7.8162 | 0.4338 |

| 255 | 364.3307 | −242.3307 | 973.9638 | −726.3453 | 5.8609 | 1.6553 | −1.9975 | −2.9461 | 5.9795 | −0.5041 |

| 256 | 1286.5939 | −1100.5939 | 2588.2322 | −2105.7952 | 6.5547 | 0.0739 | −2.3514 | 11.4365 | 7.9456 | 0.3973 |

| 257 | 331.8499 | −132.8499 | 694.5950 | −469.8906 | 3.1048 | −0.6798 | −4.0272 | 1.4193 | 4.1353 | −2.1603 |

| 258 | 628.1121 | −360.1121 | 1473.7015 | −1080.0893 | 3.4896 | −0.7277 | −3.8929 | −2.5712 | 4.8985 | −1.2062 |

| 259 | 742.3919 | 39.6081 | 2165.5600 | −1491.5146 | 3.1518 | 0.6525 | −3.4773 | 1.5947 | 5.2676 | −2.5564 |

| 260 | 689.2796 | −646.2796 | 785.0013 | −534.8978 | 3.7567 | 0.0033 | −3.4950 | 0.6684 | 5.8637 | 1.1496 |

| 261 | 1282.0912 | −1235.0912 | 3374.2752 | −3194.7044 | 6.6407 | −0.2475 | −2.4452 | 6.5397 | 7.7995 | 0.5564 |

| 262 | 420.5460 | −339.5460 | 1669.4686 | −1385.3822 | 2.9332 | 0.3334 | −3.6917 | −3.4133 | 5.3901 | −2.6234 |

| 263 | 357.3876 | −144.3876 | 1841.0687 | −65.2700 | 3.8555 | −0.4332 | −3.6297 | 4.3497 | 4.6129 | 0.0316 |

| 264 | 1229.2552 | −1022.2552 | 2108.7358 | −1275.1946 | 5.3228 | −0.2978 | −2.9907 | 0.5450 | 7.1425 | 0.3325 |

| 265 | 1285.6237 | −826.6237 | 2710.0041 | −2313.0123 | 6.0650 | 1.1515 | −2.1170 | 1.1883 | 7.7617 | 0.8363 |

| 266 | 471.9769 | −378.9769 | 2412.7288 | −2297.8587 | 2.7155 | 1.4967 | −3.3148 | −2.8353 | 5.6217 | −3.0679 |

| 267 | 816.0655 | −789.0655 | 2139.0329 | −2077.5068 | 4.5360 | −0.7162 | −3.4712 | −1.7288 | 6.7885 | −1.8956 |

| 268 | 324.1251 | −60.1251 | 1270.1676 | −850.2212 | 2.0986 | 0.3373 | −4.0229 | −2.3590 | 3.5602 | −0.8935 |

| 269 | 848.8677 | 1862.1323 | 1571.4536 | −146.1770 | 4.3309 | 0.1894 | −3.1919 | −3.6807 | 5.7866 | 1.8663 |

| 270 | 985.9124 | −749.9124 | 2376.5150 | −1563.6481 | 6.5149 | 0.6933 | −2.1203 | 0.1857 | 7.5011 | 1.4236 |

| 271 | 1220.4578 | −477.4578 | 2212.3077 | −1706.3260 | 5.1282 | −0.1371 | −3.0042 | −4.7613 | 6.2930 | 1.5654 |

| 272 | 1187.3204 | −816.3204 | 2493.8017 | −1680.7735 | 3.2996 | −0.7038 | −3.9592 | 0.4793 | 6.1456 | 0.7906 |

| 273 | 1267.9883 | −1137.9883 | 3077.3716 | −2671.9039 | 7.0205 | 0.5836 | −1.9624 | 2.2926 | 7.9718 | 0.5282 |

| 274 | 1003.5070 | 663.4930 | 2762.5154 | 424.3443 | 5.5003 | 0.6938 | −2.5246 | −5.4607 | 7.0477 | −0.2128 |

| 275 | 1133.6456 | 2969.3544 | 3473.6297 | 19,523.8706 | 5.6163 | 0.1950 | −2.6772 | −7.5012 | 7.5084 | −1.1656 |

| 276 | 1140.0177 | −1049.0177 | 2380.8006 | −1889.3081 | 1.5878 | 0.8898 | −4.0063 | −0.5483 | 4.4990 | −0.5899 |

| 277 | 670.6594 | 1231.3406 | 1883.0665 | −251.0605 | 6.5920 | −0.8120 | −2.6897 | −3.4873 | 6.4242 | 0.4958 |

| 278 | 1013.8753 | −945.8753 | 1534.9497 | −1057.8678 | 5.3197 | 0.4611 | −2.6894 | −3.2283 | 5.7831 | 3.1058 |

| 279 | 662.5581 | −554.5581 | 1720.5095 | −1121.4828 | 5.8683 | −0.4215 | −2.8225 | −2.6991 | 5.7383 | 2.3922 |

| 280 | 866.4770 | −521.4770 | 1171.0121 | 437.9692 | 3.2211 | 0.9673 | −3.3242 | −1.0961 | 4.8316 | −0.9766 |

| 281 | 572.6354 | −313.6354 | 1877.8379 | −1797.5706 | 3.3855 | −0.6189 | −3.8910 | −0.2016 | 5.9699 | −2.5600 |

| 282 | 1154.7931 | 2767.2069 | 3105.7536 | −1033.9266 | 5.8136 | 0.4396 | −2.5011 | −2.0221 | 7.1413 | −0.2806 |

| 283 | 658.5666 | −464.5666 | 1443.3692 | −1126.3107 | 4.6432 | 0.4315 | −2.9709 | −4.5471 | 6.2983 | −1.9347 |

| 284 | 1423.0522 | 2730.9478 | 3734.4679 | 13,999.6630 | 5.4601 | 0.1506 | −2.7572 | −3.1436 | 7.6839 | −1.1704 |

| 285 | 507.1595 | −442.1595 | 1398.8047 | −1084.4823 | 2.8161 | 0.5784 | −3.6407 | −3.1916 | 4.1074 | −0.6074 |

| 286 | 924.7529 | −820.7529 | 1877.5529 | −1809.7151 | 4.0230 | 0.1588 | −3.3268 | 0.4440 | 6.4165 | −1.6286 |

| 287 | 348.5751 | −256.5751 | 1204.0089 | −1176.3884 | 4.0425 | 0.6658 | −3.1169 | 1.4521 | 4.9323 | 1.3656 |

| 288 | 945.0308 | −922.0308 | 1995.8869 | −1713.3529 | 6.1275 | −0.4949 | −2.7484 | −3.1195 | 6.9460 | 0.5234 |

| 289 | 794.3239 | −776.3239 | 1162.9685 | −1126.7057 | 6.1037 | 0.1993 | −2.4812 | 0.1283 | 5.7840 | 0.9736 |

| 290 | 585.6957 | −134.6957 | 1433.8686 | 1503.6042 | 5.8491 | −0.8390 | −2.9966 | −3.4821 | 6.2938 | 0.7567 |

| 291 | 252.6750 | 185.3250 | 251.0435 | 3972.0727 | 5.7950 | 1.0505 | −2.2649 | −1.4447 | 4.5009 | 3.3378 |

| 292 | 562.4055 | −391.4055 | 448.9213 | −232.6809 | 4.2649 | −1.2226 | −3.7812 | −3.6514 | 5.2577 | −0.2999 |

| 293 | 765.3357 | −720.3357 | 1416.7989 | −1234.5173 | 4.2946 | 0.2690 | −3.1746 | −3.5992 | 5.6516 | −1.6155 |

| 294 | 1029.1262 | 4185.8738 | 2415.5144 | 725.0872 | 5.1567 | −0.6901 | −3.2133 | −6.5974 | 6.7367 | −1.5589 |

| 295 | 999.6145 | −286.6145 | 1805.6580 | −619.5650 | 4.8117 | −0.6636 | −3.3403 | −2.5898 | 5.8256 | −0.1713 |

| 296 | 508.2797 | −465.2797 | 1569.5370 | −1070.9777 | 6.0338 | 0.9832 | −2.1966 | 0.2724 | 6.0606 | −1.4165 |

| 297 | 1429.9848 | −1003.9848 | 3525.3835 | −3043.7923 | 4.9982 | 0.6762 | −2.7318 | −1.1907 | 7.0872 | 0.2616 |

| 298 | 534.5751 | −120.5751 | 1021.5132 | 1078.3655 | 5.4042 | −3.2663 | −4.1417 | −3.0862 | 5.1621 | 2.0563 |

| 299 | 791.3000 | 2962.7000 | −14.7000 | 4952.1227 | 4.8297 | 1.6748 | −2.4009 | −5.2158 | 4.3827 | 2.1082 |

| 300 | 919.6271 | −740.6271 | 2593.1536 | −2547.9100 | 5.3421 | −1.1114 | −3.3073 | −2.0813 | 6.3814 | −0.3029 |

| 301 | 935.9100 | −841.9100 | 2282.7490 | −2091.9348 | 4.8735 | −1.5168 | −3.6558 | −0.4401 | 5.7019 | −0.7842 |

| 302 | 1521.9452 | 796.0548 | 2058.0311 | −259.4866 | 5.1369 | −2.8660 | −4.0887 | 3.4496 | 6.4969 | 1.1662 |

| 303 | 910.6914 | −892.6914 | 2614.0482 | −2575.1164 | 5.0451 | −0.4260 | −3.1525 | 2.4173 | 6.6563 | −1.3706 |

| 304 | 911.4966 | −884.4966 | 2374.1070 | −2308.6712 | 4.5376 | 0.6139 | −2.9403 | 1.9378 | 7.1394 | −1.6848 |

| 305 | 640.1449 | −611.1449 | 477.9226 | −391.2111 | 5.4383 | 0.8694 | −2.4793 | 3.3656 | 5.4043 | 2.3393 |

| 306 | 1379.0786 | −452.0786 | 2727.0338 | −2354.3321 | 4.1284 | 0.3382 | −3.2133 | −3.1833 | 6.3851 | 0.3260 |

| 307 | 778.6827 | −638.6827 | 1903.2700 | −610.2327 | 2.3624 | 0.9154 | −3.6873 | −0.1149 | 5.1559 | −2.2961 |

| 308 | 504.3446 | −312.3446 | 182.0085 | −166.9104 | 1.8120 | 1.3810 | −3.7211 | 0.2640 | 3.5046 | −1.2239 |

| 309 | 1016.9491 | −913.9491 | 2642.3744 | −1652.1284 | 6.9386 | −0.0765 | −2.2583 | −0.3560 | 7.8015 | 0.4054 |

| 310 | 184.5967 | −62.5967 | 903.1924 | −655.5740 | 5.2810 | 2.1556 | −2.0292 | −2.9144 | 5.0257 | −0.6877 |

| 311 | 1319.2631 | −1133.2631 | 2981.4559 | −2499.0189 | 6.1413 | 0.6769 | −2.2758 | 11.3609 | 7.8010 | −0.3010 |

| 312 | 693.1938 | −494.1938 | 877.6593 | −652.9549 | 2.5930 | 0.4768 | −3.7702 | 1.1622 | 4.2265 | −1.6618 |

| 313 | 771.2069 | −503.2069 | 1454.4554 | −1060.8432 | 3.5321 | −0.7285 | −3.8763 | −2.5878 | 5.3645 | −1.3464 |

| 314 | 899.5969 | −117.5969 | 1679.0247 | −1004.9793 | 3.1325 | 1.0700 | −3.3186 | 1.4359 | 4.9509 | −2.4193 |

| 315 | 534.1591 | −491.1591 | 596.9042 | −346.8007 | 4.0130 | 0.5999 | −3.1550 | 0.3284 | 5.4485 | 1.2289 |

| 316 | 1304.9273 | −1257.9273 | 3277.6254 | −3098.0546 | 6.8051 | −1.2169 | −2.7661 | 6.8606 | 7.8581 | 0.4191 |

| 317 | 560.9506 | −479.9506 | 1781.1512 | −1497.0648 | 3.1969 | 0.1781 | −3.6485 | −3.4565 | 5.5613 | −2.1863 |

| 318 | 358.4625 | −145.4625 | 1839.8832 | −64.0844 | 3.8556 | −0.4356 | −3.6306 | 4.3506 | 4.6123 | 0.0277 |

| 319 | 1231.3459 | −1024.3459 | 1669.6136 | −836.0724 | 6.3464 | −0.8201 | −2.7908 | 0.3451 | 7.8390 | −0.4969 |

| 320 | 1105.5497 | −646.5497 | 2835.9983 | −2439.0064 | 6.5617 | 1.2597 | −1.8758 | 0.9472 | 7.5913 | 0.5873 |

| 321 | 790.1959 | −697.1959 | 2343.4596 | −2228.5895 | 3.2014 | 1.3820 | −3.1668 | −2.9833 | 5.8473 | −1.9584 |

| 322 | 840.0349 | −813.0349 | 2441.5782 | −2380.0520 | 4.8102 | −0.5395 | −3.2914 | −1.9085 | 6.7661 | −1.8939 |

| 323 | 507.7302 | −243.7302 | 1539.1219 | −1119.1755 | 2.8341 | 1.1958 | −3.3874 | −2.9944 | 3.7476 | −0.0935 |

| 324 | 831.5757 | 1879.4243 | 1804.0855 | −378.8090 | 4.6605 | −0.3480 | −3.2747 | −3.5978 | 5.8447 | 2.2022 |

| 325 | 953.4211 | −717.4211 | 2382.5877 | −1569.7207 | 6.7041 | 0.8691 | −1.9748 | 0.0402 | 7.2097 | 1.6626 |

| 326 | 1161.8996 | −418.8996 | 2269.4337 | −1763.4519 | 5.0935 | −0.0044 | −2.9651 | −4.8004 | 5.9994 | 1.3868 |

| 327 | 1147.8397 | −776.8397 | 2175.1083 | −1362.0801 | 4.1516 | −1.7213 | −4.0251 | 0.5452 | 5.8946 | 0.0295 |

| 328 | 1178.3826 | −1048.3826 | 2851.9926 | −2446.5249 | 6.0110 | 1.8461 | −1.8616 | 2.1917 | 7.4739 | 0.1690 |

| 329 | 1058.5042 | 608.4958 | 2848.5497 | 338.3100 | 5.4294 | 0.4040 | −2.6684 | −5.3169 | 6.9157 | −1.0586 |

| 330 | 1042.0847 | 3060.9153 | 3727.2900 | 19,270.2102 | 5.9385 | 0.1668 | −2.5600 | −7.6184 | 7.3934 | −1.8828 |

References

- Abakah, Emmanuel Joel Aikins, Aviral Kumar Tiwari, Imhotep Paul Alagidede, and Shawkat Hammoudeh. 2023. Nonlinearity in the causality and systemic risk spillover between the OPEC oil and GCC equity markets: A pre- and post-financial crisis analysis. Empirical Economics 65: 1–77. [Google Scholar] [CrossRef]

- Abdel Fattah, Fadi Abdel Muniem, Khalid Abed Dahleez, Abdul Hakim H. M. Mohamed, Mohammad Khaleel Okour, and Abrar Mohammed Mubarak AL Alawi. 2022. Public health awareness: Knowledge, attitude and behaviours of the public on health risks during COVID-19 pandemic in sultanate of Oman. Global Knowledge Memory and Communication 71: 27–51. [Google Scholar] [CrossRef]

- Abdelwahed, Nadia Abdelhamid Abdelmegeed, and Bahadur Ali Soomro. 2023. The COVID-19 Crises: The Threats, Uncertainties and Risks in Entrepreneurial Development. Risks 11: 89. [Google Scholar] [CrossRef]

- Abdi, Yaghoub, Xiaoni Li, and Xavier Càmara-Turull. 2023. Firm value in the airline industry: Perspectives on the impact of sustainability and COVID-19. Humanities and Social Sciences Communications 10: 294. [Google Scholar] [CrossRef]

- Abdullah, Dahlan, S. Susilo, Ansari Saleh Ahmar, R. Rusli, and Rahmat Hidayat. 2022. The application of K-means clustering for province clustering in Indonesia of the risk of the COVID-19 pandemic based on COVID-19 data. Qual Quant 56: 1283–91. [Google Scholar] [CrossRef]

- Attaran, Mohsen. 2023. The impact of 5G on the evolution of intelligent automation and industry digitization. Journal of Ambient Intelligence and Humanized Computing 14: 5977–93. [Google Scholar] [CrossRef]

- Busco, Carolina, Felipe González, and Michelle Aránguiz. 2023. Factors that favor or hinder the acquisition of a digital culture in large organizations in Chile. Frontiers in Psychology 14: 1153031. [Google Scholar] [CrossRef]

- Chow, Gregory C. 1960. Tests of Equality Between Sets of Coefficients in Two Linear Regressions. Econometrica 28: 591–605. [Google Scholar] [CrossRef]

- Cui, Yong, Saba Fazal Firdousi, Ayesha Afzal, Minahil Awais, and Zubair Akram. 2022. The influence of big data analytic capabilities building and education on business model innovation. Frontiers in Psychology 13: 999944. [Google Scholar] [CrossRef]

- Davidson, Russell, and James G. MacKinnon. 1993. Estimation and inference in econometrics. Econometric Theory 11: 631–35. [Google Scholar] [CrossRef]

- De Gooijer, Jan G., and Rob J. Hyndman. 2006. 25 Tears of Time Series Forecasting. International Journal of Forecasting Twenty Five Years of Forecasting 22: 443–73. [Google Scholar] [CrossRef]

- Dohale, Vishwas, Priyanka Verma, Angappa Gunasekaran, and Priya Ambilkar. 2023. COVID-19 and supply chain risk mitigation: A case study from India. The International Journal of Logistics Management 34: 417–42. [Google Scholar] [CrossRef]

- Erer, Deniz, Elif Erer, and Selim Güngör. 2023. The aggregate and sectoral time-varying market efficiency during crisis periods in Turkey: A comparative analysis with COVID-19 outbreak and the global financial crisis. Financial Innovation 9: 80. [Google Scholar] [CrossRef] [PubMed]

- Fortunato, Francesca, Roberto Lillini, Domenico Martinelli, Giuseppina Iannelli, Leonardo Ascatigno, Georgia Casanova, Pier Luigi Lopalco, and Rosa Prato. 2023. Association of socio-economic deprivation with COVID-19 incidence and fatality during the first wave of the pandemic in Italy: Lessons learned from a local register-based study. International Journal of Health Geographics 22: 10. [Google Scholar] [CrossRef]

- Fortune. 2023. Global 500. Available online: https://fortune.com/ranking/global500/2022/search/?fg500_industry=Telecommunications (accessed on 6 June 2023).

- Garcia, Ronald, and Andrew Lumsdaine. 2005. MultiArray: A C++ library for generic programming with arrays. Software Practice and Experience 35: 159–88. [Google Scholar] [CrossRef]

- Hean, Oudom, and Nattanicha Chairassamee. 2023. The effects of the COVID-19 pandemic on U.S. entrepreneurship. Letters in Spatial and Resource Sciences 16: 1. [Google Scholar] [CrossRef] [PubMed]

- Hohenstein, Nils-Ole. 2022. Supply chain risk management in the COVID-19 pandemic: Strategies and empirical lessons for improving global logistics service providers’ performance. The International Journal of Logistics Management 33: 1336–65. [Google Scholar] [CrossRef]

- IMD. 2023. World Competitiveness Online. Available online: https://www.imd.org/centers/wcc/world-competitiveness-center/rankings/world-competitiveness-ranking/ (accessed on 6 June 2023).

- Inshakova, Agnessa O., Anastasia A. Sozinova, and Tatiana N. Litvinova. 2021. Corporate Fight against the COVID-19 Risks Based on Technologies of Industry 4.0 as a New Direction of Social Responsibility. Risks 9: 212. [Google Scholar] [CrossRef]

- Kanamura, Takashi. 2023. An impact assessment of the COVID-19 pandemic on Japanese and US hotel stocks. Financial Innovation 9: 87. [Google Scholar] [CrossRef]

- Kolchin, Sergey, Nadezda Glubokova, Mikhail Gordienko, Galina Semenova, and Milyausha Khalilova. 2023. Financial Risk Management of the Russian Economy during the COVID-19 Pandemic. Risks 11: 74. [Google Scholar] [CrossRef]

- Kukoyi, Patricia Omega, Fredrick Simpeh, Oluseyi Julius Adebowale, and Justus Ngala Agumba. 2022. Managing the risk and challenges of COVID-19 on construction sites in Lagos, Nigeria. Journal of Engineering Design and Technology 20: 99–144. [Google Scholar] [CrossRef]

- Leung, Wilson K. S., Man Kit Chang, Man Lai Cheung, and Si Shi. 2023. VR tourism experiences and tourist behavior intention in COVID-19: An experience economy and mood management perspective. Information Technology & People 36: 1095–125. [Google Scholar] [CrossRef]

- Litvinova, Tatiana N. 2022. Risks of Entrepreneurship amid the COVID-19 Crisis. Risks 10: 163. [Google Scholar] [CrossRef]

- Loughran, Tim, and Bill McDonald. 2023. Management disclosure of risk factors and COVID-19. Financial Innovation 9: 53. [Google Scholar] [CrossRef]

- McMillan, Michael. 2014. Data Structures and Algorithms with JavaScript. Sebastopol: O’Reilly Media, pp. 30–32. [Google Scholar]

- Metwally, Abdelmoneim Bahyeldin Mohamed, and Ahmed Diab. 2023. An institutional analysis of the risk management process during the COVID-19 pandemic: Evidence from an emerging market. Journal of Accounting & Organizational Change 19: 40–62. [Google Scholar] [CrossRef]

- Mezghani, Taicir, Fatma Ben Hamadou, and Mouna Boujelbène Abbes. 2021. The dynamic network connectedness and hedging strategies across stock markets and commodities: COVID-19 pandemic effect. Asia-Pacific Journal of Business Administration 13: 520–52. [Google Scholar] [CrossRef]

- Moreno Ramírez, Denise, Shannon Gutenkunst, Jenna Honan, Maia Ingram, Carolina Quijada, Marvin Chaires, Sam J. Sneed, Flor Sandoval, Rachel Spitz, Scott Carvajal, and et al. 2022. Thinking on your feet: Beauty and auto small businesses maneuver the risks of the COVID-19 pandemic. Frontiers in Public Health 10: 921704. [Google Scholar] [CrossRef] [PubMed]

- Ngo, Vu Minh, Hiep Cong Pham, and Huan Huu Nguyen. 2023. Drivers of digital supply chain transformation in SMEs and large enterprises—A case of COVID-19 disruption risk. International Journal of Emerging Markets 18: 1355–77. [Google Scholar] [CrossRef]

- Phang, Soon-Yeow, Christofer Adrian, Mukesh Garg, Anh Viet Pham, and Cameron Truong. 2023. COVID-19 pandemic resilience: An analysis of firm valuation and disclosure of sustainability practices of listed firms. Managerial Auditing Journal 38: 85–128. [Google Scholar] [CrossRef]

- Popkova, Elena G., and Bruno S. Sergi. 2021. Dataset Modelling of the Financial Risk Management of Social Entrepreneurship in Emerging Economies. Risks 9: 211. [Google Scholar] [CrossRef]

- Salami, Babatunde A., Saheed O. Ajayi, and Adekunle S. Oyegoke. 2022. Coping with the Covid-19 pandemic: An exploration of the strategies adopted by construction firms. Journal of Engineering, Design and Technology 20: 159–82. [Google Scholar] [CrossRef]

- Sozinova, Anastasiya A., and Elena G. Popkova. 2023. Dataset Analysis of Pandemic Risks and Risk Management Prospects Based on Management and Marketing in Conditions of COVID-19 Recession. Risks 11: 37. [Google Scholar] [CrossRef]

- Tan, Xiaoyu, Shiqun Ma, Xuetong Wang, Chao Feng, and Lijin Xiang. 2022. The impact of the COVID-19 pandemic on the global dynamic spillover of financial market risk. Frontiers in Public Health 10: 963620. [Google Scholar] [CrossRef] [PubMed]

- Tang, Hongfei, Kangzhen Xie, and Xiaoqing Eleanor Xu. 2023. COVID-19 Pandemic and Bond ETF Valuation Discount. Journal of Fixed Income 32: 83–155. [Google Scholar] [CrossRef]

- Tingey-Holyoak, Joanne Louise, and John Dean Pisaniello. 2021. The need for accounting-integrated data streams for scenario-based planning in primary production: Responding to COVID-19 and other crises. Sustainability Accounting Management and Policy Journal 12: 898–912. [Google Scholar] [CrossRef]

- Türk, Abdullah. 2022. Digital leadership role in developing business strategy suitable for digital transformation. Frontiers in Psychology 13: 1066180. [Google Scholar] [CrossRef]

- Velayutham, Ajantha, Asheq Razaur Rahman, Anil Narayan, and Michael Wang. 2021. Pandemic turned into pandemonium: The effect on supply chains and the role of accounting information. Accounting Auditing & Accountability Journal 34: 1404–15. [Google Scholar] [CrossRef]

- Vogl, Markus. 2022. Quantitative modelling frontiers: A literature review on the evolution in financial and risk modelling after the financial crisis (2008–2019). SN Business & Economics 2: 183. [Google Scholar] [CrossRef]

- World Bank. 2023. GDP Growth (Annual %). Available online: https://data.worldbank.org/indicator/NY.GDP.MKTP.KD.ZG?view=chart (accessed on 1 August 2023).

- Yamen, Ahmed Emadeldin. 2021. Tax evasion, corruption and COVID-19 health risk exposure: A cross country analysis. Journal of Financial Crime 28: 995–1007. [Google Scholar] [CrossRef]

- Yelikbayev, Kuanysh, and Inna Andronova. 2022. The Interaction of the EEU Member States and Risks of Their Mutual Trade during the COVID-19 Pandemic: Implications for the Management of Corporate Social Responsibility. Risks 10: 27. [Google Scholar] [CrossRef]

- Yeşildağ, Eser. 2019. Financial Risks and Derivative Use of Non-financial Companies in Turkey. Frontiers in Applied Mathematics and Statistics 5: 64. [Google Scholar] [CrossRef]

- Yuan, Duanyang, Jingwei Yue, Xuefeng Xiong, Yibi Jiang, Peng Zan, and Chunyong Li. 2023. A regression method for EEG-based cross-dataset fatigue detection. Frontiers in Physiology 14: 1196919. [Google Scholar] [CrossRef] [PubMed]

- Zhou, Haiyang, and Shuping Li. 2022. Effect of COVID-19 on risk spillover between fintech and traditional financial industries. Frontiers in Public Health 10: 979808. [Google Scholar] [CrossRef] [PubMed]

| Research Question (RQ) | Research Task | Research Method | Sample |

|---|---|---|---|

| RQ1: What is the level of risks for companies during the COVID-19 crisis (in 2020): higher or lower than the pre-crisis level (2019)? | Task 1: to measure risks for companies during the COVID-19 crisis and to determine the features of risks in developed and developing countries | Method of horizontal analysis | Sample 1: “Global 500” (Fortune 2023) in 2019–2022 with division into developed and developing countries (rank, revenue, and profits) Sample 2: The top 55 most competitive digital economies of the world (IMD 2023) in 2017–2022 (listed domestic companies and connected statistics) |

| RQ2: Which countries experienced the highest risks for companies during the COVID-19 crisis: developed or developing nations? | |||

| RQ3: What are the consequences of risks for companies during the COVID-19 crisis for the economy: increase or reduction in crisis phenomena in the economy? | Task 2: to determine cause-and-effect relationships between the change and digital management of risks for companies during the COVID-19 crisis Task 3: to determine the potential for digital management of risks for companies under the conditions of a crisis of a non-economic nature via the example of the COVID-19 pandemic | Method of regression analysis | Sample 2: The top 55 most competitive digital economies of the world (IMD 2023) in 2017–2022 (econometric modelling of the connection between listed domestic companies and alternative measures of risk management and potential implications for the economy) |

| RQ4: How (and with what measures) can we manage risks under the conditions of a crisis of a non-economic nature given the experience of the COVID-19 crisis: measures of state or corporate management? | Method of foresight, method of trend analysis |

| Year | Digital/Technological Skills | Use of Big Data and Analytics | Digital Transformation in Companies | Mobile Broadband Subscribers | Protectionism | Health Infrastructure | Listed Domestic Companies | Gross Domestic Product (GDP) | Tax Evasion | Exports of Goods—Growth | Government Budget Surplus/Deficit (%) |

|---|---|---|---|---|---|---|---|---|---|---|---|

| 2017 | 6.96 | 4.90 | 5.99 | 46.09 | 5.81 | 5.67 | 720.04 | 1334.21 | 4.43 | 12.62 | −1.55 |

| 2018 | 6.88 | 4.85 | 5.95 | 55.60 | 5.94 | 5.66 | 713.07 | 1421.45 | 4.51 | 11.83 | −0.88 |

| 2019 | 6.87 | 5.00 | 5.58 | 63.21 | 5.76 | 5.67 | 722.93 | 1441.75 | 4.65 | −2.93 | −1.19 |

| 2020 | 6.95 | 5.15 | 5.70 | 69.80 | 5.78 | 5.91 | 727.16 | 1396.19 | 4.77 | −7.66 | −7.01 |

| 2021 | 6.84 | 5.05 | 5.68 | 76.06 | 5.44 | 5.92 | - | 1582.30 | 4.54 | 28.48 | −4.13 |

| 2022 | 6.69 | 5.25 | 5.82 | - | 5.55 | 5.83 | - | - | 4.86 | - | - |

| 2018/ 2017 | 0.99 | 0.99 | 0.99 | 1.21 | 1.02 | 1.00 | 0.99 | 1.07 | 1.02 | 0.94 | 0.56 |

| 2019/ 2018 | 1.00 | 1.03 | 0.94 | 1.14 | 0.97 | 1.00 | 1.01 | 1.01 | 1.03 | −0.25 | 1.36 |

| 2020/ 2019 | 1.01 | 1.03 | 1.02 | 1.10 | 1.00 | 1.04 | 1.01 | 0.97 | 1.03 | 2.61 | 5.88 |

| 2021/ 2020 | 0.98 | 0.98 | 1.00 | 1.09 | 0.94 | 1.00 | - | 1.13 | 0.95 | −3.72 | 0.59 |

| 2022/ 2021 | 0.98 | 1.04 | 1.02 | - | 1.02 | 0.98 | - | - | 1.07 | - | - |

| Regression statistics | ||||||

| Multiple R | 0.2830 | |||||

| R-square | 0.0801 | |||||

| Adjusted R-square | 0.0630 | |||||

| Standard error | 1195.5137 | |||||

| Observations | 330 | |||||

| ANOVA | ||||||

| df | SS | MS | F | Significance F | ||

| Regression | 6 | 40,180,810.2300 | 6,696,801.7050 | 4.6855 | 0.0001 | |

| Residual | 323 | 461,648,735.7215 | 1,429,253.0518 | |||

| Total | 329 | 501,829,545.9515 | ||||

| Coefficients | Standard error | t-Stat | p-Value | Lower 95% | Upper 95% | |

| Constant | −647.6480 | 530.7913 | −1.2202 | 0.2233 | −1691.8927 | 396.5967 |

| DGT1 | −21.1858 | 101.3259 | −0.2091 | 0.8345 | −220.5278 | 178.1562 |

| DGT2 | −23.1690 | 135.9699 | −0.1704 | 0.8648 | −290.6675 | 244.3295 |

| DGT3 | 287.6776 | 149.7063 | 1.9216 | 0.0555 | −6.8449 | 582.2000 |

| DGT4 | 7.6846 | 3.3696 | 2.2806 | 0.0232 | 1.0555 | 14.3138 |

| GOV1 | −196.7826 | 68.0364 | −2.8923 | 0.0041 | −330.6331 | −62.9321 |

| GOV2 | 103.3040 | 48.6336 | 2.1241 | 0.0344 | 7.6254 | 198.9826 |

| Chow test | ||||||

| Before the pandemic (2019) | During the pandemic (2020) | |||||

| Coefficients | p-Value | Coefficients | p-Value | |||

| Constant | −471.2037 | 0.7195 | −803.4855 | 0.5851 | ||

| DGT1 | −23.7715 | 0.9273 | 93.8439 | 0.7575 | ||

| DGT2 | −190.0792 | 0.6732 | −33.9622 | 0.9432 | ||

| DGT3 | 365.7956 | 0.4432 | 77.4060 | 0.8743 | ||

| DGT4 | 10.5258 | 0.3183 | 14.5071 | 0.1725 | ||

| GOV1 | −190.3167 | 0.2885 | −151.6951 | 0.3714 | ||

| GOV2 | 122.9987 | 0.3465 | 80.5655 | 0.5496 | ||

| Coefficients | Values of the Coefficients | |

|---|---|---|

| Before the Pandemic (in 2019) | During the COVID-19 Pandemic and Crisis (in 2020) | |

| Constant | −471.2037 | −803.4855 |

| DGT1 | −23.7715 | 93.8439 |

| DGT2 | −190.0792 | −33.9622 |

| DGT3 | 365.7956 | 77.4060 |

| DGT4 | 10.5258 | 14.5071 |

| GOV1 | −190.3167 | −151.6951 |

| GOV2 | 122.9987 | 80.5655 |

| Level of significance (α) | 0.01 (1%) | |

| F-table at the level of significance α | 3.2036 At k1 = m = 6; k2 = n − m − 1 = 55 − 6 − 1 = 48 | |

| F-observed | 0.8011 | 0.7810 |

| Regression statistics | ||||||

| Multiple R | 0.6910 | |||||

| R-square | 0.4775 | |||||

| Adjusted R-square | 0.4661 | |||||

| Standard error | 2551.3779 | |||||

| Observations | 330 | |||||

| ANOVA | ||||||

| df | SS | MS | F | Significance F | ||

| Regression | 7 | 1,915,243,144.1090 | 273,606,163.4441 | 42.0316 | 6.746 × 10−42 | |

| Residual | 322 | 2,096,068,391.9956 | 6,509,529.1677 | |||

| Total | 329 | 4,011,311,536.1046 | ||||

| Coefficients | Standard error | t-Stat | p-Value | Lower 95% | Upper 95% | |

| Constant | −1984.6080 | 1135.3836 | −1.7480 | 0.0814 | −4218.3147 | 249.0987 |

| DGT1 | 386.1310 | 216.2569 | 1.7855 | 0.0751 | −39.3238 | 811.5859 |

| DGT2 | 993.0822 | 290.1901 | 3.4222 | 0.0007 | 422.1742 | 1563.9903 |

| DGT3 | −898.8861 | 321.3132 | −2.7975 | 0.0055 | −1531.0245 | −266.7478 |

| DGT4 | 7.0497 | 7.2489 | 0.9725 | 0.3315 | −7.2115 | 21.3108 |

| GOV1 | 12.1996 | 147.0666 | 0.0830 | 0.9339 | −277.1332 | 301.5324 |

| GOV2 | −150.2545 | 104.5127 | −1.4377 | 0.1515 | −355.8683 | 55.3594 |

| RISK | 1.8530 | 0.1187 | 15.6051 | 0.0000 | 1.6194 | 2.0867 |

| Chow test | ||||||

| Before the pandemic (2019) | During the pandemic (2020) | |||||

| Coefficients | p-Value | Coefficients | p-Value | |||

| Constant | −703.2492 | 0.7870 | −2029.0648 | 0.5085 | ||

| DGT1 | 287.4853 | 0.5782 | 411.8522 | 0.5152 | ||

| DGT2 | 1898.4237 | 0.0380 | 1427.2338 | 0.1539 | ||

| DGT3 | −1878.5130 | 0.0523 | −1447.6214 | 0.1587 | ||

| DGT4 | 18.7260 | 0.3749 | 11.9684 | 0.5921 | ||

| GOV1 | −118.6725 | 0.7400 | 135.9525 | 0.7012 | ||

| GOV2 | −131.6089 | 0.6134 | −243.5808 | 0.3866 | ||

| RISK | 1.9450 | 0.00000002 | 1.7591 | 0.0000004 | ||

| Coefficients | Values of the Coefficients | |

|---|---|---|

| Before the Pandemic (in 2019) | During the COVID-19 Pandemic and Crisis (in 2020) | |

| Constant | −703.2492 | −2029.0648 |

| DGT1 | 287.4853 | 411.8522 |

| DGT2 | 1898.4237 | 1427.2338 |

| DGT3 | −1878.5130 | −1447.6214 |

| DGT4 | 18.7260 | 11.9684 |

| GOV1 | −118.6725 | 135.9525 |

| GOV2 | −131.6089 | −243.5808 |

| RISK | 1.9450 | 1.7591 |

| Level of significance (α) | 0.000001 (0.0001%) | |

| F-table at the level of significance α | 8.5622 At k1 = m = 7; k2 = n − m − 1 = 55 − 7 − 1 = 47 | |

| F-observed | 7.9598 | 6.2082 |

| Regression statistics | ||||||

| Multiple R | 0.7878 | |||||

| R-square | 0.6206 | |||||

| Adjusted R-square | 0.6124 | |||||

| Standard error | 1.0104 | |||||

| Observations | 330 | |||||

| ANOVA | ||||||

| df | SS | MS | F | Significance F | ||

| Regression | 7 | 537.7296 | 76.8185 | 75.2517 | 5.292 × 10−64 | |

| Residual | 322 | 328.7042 | 1.0208 | |||

| Total | 329 | 866.4339 | ||||

| Coefficients | Standard error | t-Stat | p-Value | Lower 95% | Upper 95% | |

| Constant | −1.5057 | 0.4496 | −3.3489 | 0.0009 | −2.3903 | −0.6211 |

| DGT1 | −0.1706 | 0.0856 | −1.9917 | 0.0473 | −0.3390 | −0.0021 |

| DGT2 | 0.2690 | 0.1149 | 2.3407 | 0.0199 | 0.0429 | 0.4951 |

| DGT3 | 0.0961 | 0.1272 | 0.7550 | 0.4508 | −0.1543 | 0.3464 |

| DGT4 | 0.0134 | 0.0029 | 4.6538 | 4.77 × 10−6 | 0.0077 | 0.0190 |

| GOV1 | 0.6611 | 0.0582 | 11.3508 | 2.42 × 10−25 | 0.5465 | 0.7756 |

| GOV2 | 0.1229 | 0.0414 | 2.9686 | 0.0032 | 0.0414 | 0.2043 |

| RISK | 0.0001 | 0.0000 | 1.3221 | 0.1871 | 0.0000 | 0.0002 |

| Chow test | ||||||

| Before the pandemic (2019) | During the pandemic (2020) | |||||

| Coefficients | p-Value | Coefficients | p-Value | |||

| Constant | −1.5184 | 0.1420 | −1.3761 | 0.2388 | ||

| DGT1 | −0.2966 | 0.1482 | −0.1070 | 0.6548 | ||

| DGT2 | 0.2019 | 0.5661 | 0.1564 | 0.6769 | ||

| DGT3 | 0.3414 | 0.3618 | 0.0095 | 0.9804 | ||

| DGT4 | 0.0169 | 0.0448 | 0.0183 | 0.0344 | ||

| GOV1 | 0.6412 | 0.0000 | 0.7830 | 0.0000 | ||

| GOV2 | 0.0845 | 0.4101 | 0.0291 | 0.7839 | ||

| RISK | 0.0001 | 0.6040 | 0.0001 | 0.5248 | ||

| Coefficients | Values of the Coefficients | |

|---|---|---|

| Before the Pandemic (in 2019) | During the COVID-19 Pandemic and Crisis (in 2020) | |

| Constant | −1.5184 | −1.3761 |

| DGT1 | −0.2966 | −0.1070 |

| DGT2 | 0.2019 | 0.1564 |

| DGT3 | 0.3414 | 0.0095 |

| DGT4 | 0.0169 | 0.0183 |

| GOV1 | 0.6412 | 0.7830 |

| GOV2 | 0.0845 | 0.0291 |

| RISK | 0.0001 | 0.0001 |

| Level of significance (α) | 0.0000000001 (0.00000001%) | |

| F-table at the level of significance α | 16.4298 At k1 = m = 7; k2 = n − m − 1 = 55 − 7 − 1 = 47 | |

| F-observed | 14.2800 | 14.3165 |

| Regression statistics | ||||||

| Multiple R | 0.1732 | |||||

| R-square | 0.0300 | |||||

| Adjusted R-square | 0.0270 | |||||

| Standard error | 3.6842 | |||||

| Observations | 330 | |||||

| ANOVA | ||||||

| df | SS | MS | F | Significance F | ||

| Regression | 1 | 137.7124 | 137.7124 | 10.1457 | 0.0016 | |

| Residual | 328 | 4452.1147 | 13.5735 | |||

| Total | 329 | 4589.8272 | ||||

| Coefficients | Standard error | t-Stat | p-Value | Lower 95% | Upper 95% | |

| Constant | −4.9940 | 0.6135 | −8.1404 | 8.3 × 10−15 | −6.2009 | −3.7872 |

| GOV2 | 0.3987 | 0.1252 | 3.1852 | 0.0016 | 0.1524 | 0.6449 |

| Chow test | ||||||

| Before the pandemic (2019) | During the pandemic (2020) | |||||

| Coefficients | p-Value | Coefficients | p-Value | |||

| Constant | −3.4038 | 0.0026 | −8.2518 | 0.0000002 | ||

| GOV2 | 0.4759 | 0.0342 | 0.2598 | 0.3483 | ||

| Coefficients | Values of the Coefficients | |

|---|---|---|

| Before the Pandemic (in 2019) | During the COVID-19 Pandemic and Crisis (in 2020) | |

| Constant | −3.4038 | −8.2518 |

| GOV2 | 0.4759 | 0.2598 |

| Level of significance (α) | 0.01 (1%) | |

| F-table at the level of significance α | 7.1386 At k1 = m = 1; k2 = n − m − 1 = 55 – 1 − 1 = 53 | |

| F-observed | 4.7260 | 0.8955 |

| Regression statistics | ||||||

| Multiple R | 0.5609 | |||||

| R-square | 0.3146 | |||||

| Adjusted R-square | 0.3062 | |||||

| Standard error | 1.6555 | |||||

| Observations | 330 | |||||

| ANOVA | ||||||

| df | SS | MS | F | Significance F | ||

| Regression | 4 | 408.8924 | 102.2231 | 37.2994 | 1.134 × 10−25 | |

| Residual | 325 | 890.6983 | 2.7406 | |||

| Total | 329 | 1299.5907 | ||||

| Coefficients | Standard error | t-Stat | p-Value | Lower 95% | Upper 95% | |

| Constant | −2.0686 | 0.7154 | −2.8916 | 0.0041 | −3.4760 | −0.6612 |

| DGT1 | 0.6197 | 0.1354 | 4.5758 | 6.76 × 10−6 | 0.3533 | 0.8861 |

| DGT2 | −0.0785 | 0.1882 | −0.4170 | 0.6769 | −0.4488 | 0.2918 |

| DGT3 | 0.3723 | 0.2047 | 1.8189 | 0.0699 | −0.0304 | 0.7751 |

| DGT4 | 0.0284 | 0.0044 | 6.5004 | 3.01 × 10−10 | 0.0198 | 0.0369 |

| Chow test | ||||||

| Before the pandemic (2019) | During the pandemic (2020) | |||||

| Coefficients | p-Value | Coefficients | p-Value | |||

| Constant | −1.5917 | 0.3690 | −2.0232 | 0.2983 | ||

| DGT1 | 0.5591 | 0.1195 | 0.7792 | 0.0553 | ||

| DGT2 | 0.3510 | 0.5722 | −0.4699 | 0.4683 | ||

| DGT3 | −0.1369 | 0.8367 | 0.5107 | 0.4419 | ||

| DGT4 | 0.0384 | 0.0064 | 0.0290 | 0.0386 | ||

| Coefficients | Values of the Coefficients | |

|---|---|---|

| Before the Pandemic (in 2019) | During the COVID-19 Pandemic and Crisis (in 2020) | |

| Constant | −1.5917 | −2.0232 |

| DGT1 | 0.5591 | 0.7792 |

| DGT2 | 0.3510 | −0.4699 |

| DGT3 | −0.1369 | 0.5107 |

| DGT4 | 0.0384 | 0.0290 |

| Level of significance (α) | 0.0001 (0.01%) | |

| F-table at the level of significance α | 7.3301 At k1 = m = 1; k2 = n − m − 1 = 55 − 1 − 1 = 53 | |

| F-observed | 5.7474 | 5.2092 |

| Correlation | DGT1 | DGT2 | DGT3 | DGT4 | GOV1 | GOV2 | RISK | ECON1 | ECON2 | GBD |

|---|---|---|---|---|---|---|---|---|---|---|

| DGT1 | 1.00 | 0.62 | 0.68 | 0.25 | 0.46 | 0.46 | 0.12 | 0.16 | 0.40 | 0.19 |

| DGT2 | 0.62 | 1.00 | 0.82 | 0.29 | 0.38 | 0.37 | 0.16 | 0.22 | 0.45 | 0.04 |

| DGT3 | 0.68 | 0.82 | 1.00 | 0.19 | 0.44 | 0.39 | 0.17 | 0.14 | 0.45 | 0.20 |

| DGT4 | 0.25 | 0.29 | 0.19 | 1.00 | 0.21 | 0.41 | 0.19 | 0.19 | 0.39 | −0.12 |

| GOV1 | 0.46 | 0.38 | 0.44 | 0.21 | 1.00 | 0.66 | 0.00 | 0.00 | 0.72 | 0.24 |

| GOV2 | 0.46 | 0.37 | 0.39 | 0.41 | 0.66 | 1.00 | 0.14 | 0.08 | 0.63 | 0.18 |

| RISK | 0.12 | 0.16 | 0.17 | 0.19 | 0.00 | 0.14 | 1.00 | 0.67 | 0.12 | −0.31 |

| ECON1 | 0.16 | 0.22 | 0.14 | 0.19 | 0.00 | 0.08 | 0.67 | 1.00 | 0.16 | −0.27 |

| ECON2 | −0.04 | 0.05 | 0.09 | 0.11 | −0.09 | −0.03 | −0.03 | −0.02 | 1.00 | 0.16 |

| GBD | 0.19 | 0.04 | 0.20 | −0.12 | 0.24 | 0.18 | −0.31 | −0.27 | 0.17 | 1.00 |

| Research Questions (RQs) | Answers in the Existing Literature | New Answers that Were Received in This Paper |

|---|---|---|

| RQ1: What is the level of risks for companies during the COVID-19 crisis (in 2020): higher or lower than the pre-crisis level (2019)? | Risks for companies were very high during the COVID-19 crisis (Moreno Ramírez et al. 2022; Tan et al. 2022; Zhou and Li 2022) | Risks for companies during the COVID-19 crisis increased slightly compared with those at the pre-crisis level |

| RQ2: Which countries experienced the highest risks for companies during the COVID-19 crisis: developed or developing nations? | Companies faced large risks during the COVID-19 crisis in developing countries (Abdullah et al. 2022; Dohale et al. 2023) | Companies faced large risks during the COVID-19 crisis in developed countries |

| RQ3: What are the consequences of risks for companies during the COVID-19 crisis for the economy: increase or reduction in crisis phenomena in the economy? | Due to the unpreparedness of companies for the COVID-19 crisis, the risks for them increased the economic decline (Mezghani et al. 2021; Yamen 2021) | Due to successful adaptation, the risk management of companies mitigated manifestations of the COVID-19 crisis in the economy |

| RQ4: How (and with what measures) can we manage risks under the conditions of a crisis of a non-economic nature given the experience of the COVID-19 crisis: measures of state or corporate management? | To reduce the risk burden on business during the COVID-19 crisis, there is a need for external (state) management with the help of standard measures of protectionism (Phang et al. 2023; Salami et al. 2022; Velayutham et al. 2021) and special measures of the development of healthcare infrastructure (Abdel Fattah et al. 2022) | Companies managed—independently and successfully (internal corporate management)—their risks during the COVID-19 crisis with the help of measures of the digitalisation of businesses |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Skryl, T.V.; Gerasimova, E.B.; Chutcheva, Y.V.; Golovin, S.V. Risks for Companies during the COVID-19 Crisis: Dataset Modelling and Management through Digitalisation. Risks 2023, 11, 157. https://doi.org/10.3390/risks11090157

Skryl TV, Gerasimova EB, Chutcheva YV, Golovin SV. Risks for Companies during the COVID-19 Crisis: Dataset Modelling and Management through Digitalisation. Risks. 2023; 11(9):157. https://doi.org/10.3390/risks11090157

Chicago/Turabian StyleSkryl, Tatiana V., Elena B. Gerasimova, Yuliya V. Chutcheva, and Sergey V. Golovin. 2023. "Risks for Companies during the COVID-19 Crisis: Dataset Modelling and Management through Digitalisation" Risks 11, no. 9: 157. https://doi.org/10.3390/risks11090157

APA StyleSkryl, T. V., Gerasimova, E. B., Chutcheva, Y. V., & Golovin, S. V. (2023). Risks for Companies during the COVID-19 Crisis: Dataset Modelling and Management through Digitalisation. Risks, 11(9), 157. https://doi.org/10.3390/risks11090157