1. Introduction

Internal Auditing is an essential component that helps distribute resources as efficiently as possible. It is also beneficial for reducing corruption’s outward signs and achieving economic success (

Al-Taee and Flayyih 2023). Therefore, considered IA is a practice that safeguards resources against misuse, confirms the veracity of corporate data, and guarantees adherence to applicable laws and regulations. IA also aims to stop events from occurring in the bank on purpose or by accident; rather, choices should be created through the IA strategy, and “top management” refers to the data analyzed during auditing when making decisions (

Napitupulu 2020). Employee loyalty to the organization in accomplishing common goals is shown in OC. Employees will endeavor to be innovative and productive in carrying out their jobs with a high level of devotion (

Sumardjo and Supriadi 2023). Concerns about ethical behavior in the workplace are raised by unethical behavior in both public and private organizations (

Limpo and Junaidi 2023). To make choices that are in line with the demands and objectives of the bank, it is vital to have information that is consistent with the AIS characteristics of each current department. Meanwhile, the OC that each person possesses may be used to create accurate information. This is so that information generated by each employee’s performance may be measured against the OC evaluation (

Fauzi et al. 2023). Moreover, OC is a key factor that affects and defines audit consistency, where OC is at the heart of a bank’s operations and has an impact on both the performance as a whole as well as the caliber of its goods and services (

Aldegis 2018).

Moreover, IA must also confirm that all pertinent economic events are gathered by the AIS and the process of changing and translating financial data (

Al-Taee and Flayyih 2023). The dissemination of information has been accelerated by the advent of the big data era, the rise of the network economy, and advances in technology, while accounting computerization has gradually replaced the conventional manual bookkeeping system employed by banks, and the stage of computer information has officially begun (

Alqudah et al. 2023). The success or loss of bank operations throughout the bank expansion process, however, can be somewhat influenced by accounting information statistics (

Ye and Hu 2020). An AIS is a crucial instrument for managers looking to maintain a competitive edge. The AIS is sometimes thought of as one of the supportive information systems used in managerial tasks (

Jarah et al. 2023a). Therefore, the AIS used by banks must be of a high caliber (

Jarah and Almatarneh 2021). Every bank also needs an AIS that has been correctly created, is kept up to date, and enables the bank to conduct its purposes in order to keep the path of incoming and outgoing accounts. An information technology-based solution that aids in the control of a bank’s economic and financial activities is an AIS (

Jarah and Al Jarrah 2022). Although this method requires a lot of processes and procedures to facilitate IA operations, significant technological improvements have allowed banks to strategically use it. To do this, the bank’s management must be held accountable for enhancing employee performance, encouraging cooperation, and sharing information with the chain of command (

Jarah et al. 2023b).

Therefore, the significance of this study is derived from the significance of its dependent, independent, and mediator factors. In order to improve the efficiency of the AIS in Jordanian banks. Thus, this study will focus on IA and the cycle of raising the efficiency of the AIS in Jordanian banks using OC as a mediator. Accordingly, it is necessary to inform the administration of the value of IA and its contribution to improving the effectiveness of AIS in Jordanian banking. The departments responsible for banks have paid close attention to IA because it is regarded as a crucial component of comprehensive banking control and because of how important it is in preventing, repelling, and limiting risks and errors that banks may be exposed to daily. Therefore, IA is based on a group among the controls for the conduct of banks’ business to ensure mathematical accuracy. This research will also highlight the significance of the Jordanian banking sector’s challenges in implementing AIS. The findings can therefore provide a clear picture of how much Jordanian banks are aware of the value of IA and how it contributes to improving the effectiveness of the AIS.

This paper is organized in five sections at the end of this introduction.

Section 2 is the literature review of the study. The paper then proceeds to methodology in

Section 3, which includes research questions, research design in the study, research instruments, statistical analysis, data collection procedures, and participants;

Section 4 is the research results,

Section 5 is discussion; and

Section 6 includes the implications and limitations and future research and conclusions of this study.

2. Literature Review

IA has emerged as a critical aspect in helping effective controls and risk management. In times of economic crisis, internal audits are one of the most powerful and quickest strategies to minimize operational expenses and offer the firm competitive benefits in the global market (

Jarah et al. 2022a). IA is a distinct activity that provides objective assurance and consulting services to improve and enhance an organization’s operations. IA helps banks achieve their objectives by utilizing a rigorous, disciplined approach to examine and enhance the efficacy of risk management and control (

Mulyani et al. 2019). One of the most crucial elements in helping a company create high-quality financial reporting is OC; this shows that strong OC may lead to timely, accurate, comparable, and trustworthy information. In light of this, it is anticipated that the installation of IA, AIS, and OC to the quality of financial reporting will enhance the performance of the business (

Setyaningsih et al. 2021). Additionally, IA activities assess the effectiveness of the practice, and the idea of IA frequently calls for management intervention reviews to handle situations that differ from those that were attained (

Van Dung 2020). According to

Rachman and Fitri (

2023) study, operational auditing and AIS have a considerable impact on sales performance, internal control has no bearing on sales performance. The findings of the study by

Wibowo et al. (

2023) demonstrate that the IA and the AIS combined have an influential positive on organizational performance.

IA is defined as a corporate function that tests and assesses bank operations as a service supplied to the bank (

Awuah et al. 2022). IA must thus guarantee that the AIS captures all crucial economic events and that summarizing and modifying financial data are error free. According to

Sagala (

2020), the AIS in the bank still faces a variety of risks during the course of operation. These risks are primarily from natural disasters, accidents, mistakes, dissatisfaction with the bank, or low quality of the staff, where these risk factors will affect the lack of accounting data tangibly, leading to data information errors, making it difficult to allocate resources reasonably, and causing irreparable losses to the bank (

Jarah et al. 2023b;

Liu 2023;

Jarah et al. 2022a).

Furthermore, the implementation of AIS is essential for the success of an organization since it enhances the collection, administration, and management of large amounts of organizational data. However, such systems frequently have malfunctions that result in serious operational issues and monetary losses (

Ayoub et al. 2020), while the inadequate implementation of IA was formerly the determining criterion for whether or not AIS qualified. Accordingly, AIS are necessary for effective business management and decision-making (

Alawaqleh 2021;

Jarah and Almatarneh 2021). IA is utilized to protect the bank against risk or lessen the consequences of risk incidents. In order to assure the accuracy of the bank’s financial statements, internal control must be built into the AIS (

Van Dung 2020). As a result, the major goal of IA is to assist the entity in managing risks in order to meet the entity’s goals while it is being constructed and to uphold the bank’s work ethics. Internal controls may also be defined as rules or guidelines intended to ensure the accomplishment of a certain goal (

Setyaningsih 2020). Moreover, the IA is a policy that protects assets from misappropriation, verifies bank information, ensures compliance with applicable rules and regulations, and prevents things from happening in the bank on purpose or by mistake (

Sagala 2020).

Therefore, the financial components of bank events are captured, processed, and reported using AIS, where the AIS keeps track of and reports on financial activity inside the bank as well as commercial transactions (

Mulyani et al. 2019). Therefore, the AIS has become more accessible to banks as technology has advanced. These systems are critical because they provide all levels of management with complete information that is used in the planning and control of operations inside banks (

Faisal et al. 2023). Furthermore, AISs deliver high-quality information to internal and external users, with a focus on six key areas: people, processes, data, software, information technology, and internal controls (

Ömer 2016). Moreover, with audits features in the accounting system, many frauds, irregularities, and mistakes may be avoided or monitored and addressed, where accounting information developments result in the development of information demands for interested parties as well as the necessity for quality procedures and performance in creating information (

Wahyuni et al. 2022). In a study by

Jarah et al. (

2023a), it was proven that the IA has an effect on the relationship between the AIS and the performance of Jordanian banks.

Wahyuni et al. (

2022) findings revealed that the AIS and IA had a partially good and substantial influence on internal control.

IA, on the other hand, is based on the plans, strategies, and metrics selected by a bank activity to protect its assets, verify the correctness and dependability of the data, enhance operating effectiveness, and ensure adherence to specified management standards (

Abed et al. 2022). It may be inferred that a bank’s subpar IA will have a significant impact on staff performance (

Amira and Permatasari 2022). However, independence and impartiality in IA are essential for the profession (

Lois et al. 2021). Similar to this, neutrality and presumptive doubt have evolved as the main perspectives of auditor professional skepticism, and IA should work to be fair in formulating its conclusions; there should be no prejudice on either side (

Silva et al. 2023). IA must also set up appropriate controls in accordance with the control profession and exercise the requisite professional care in their work, taking into account the amount of labor necessary to complete the assignment’s objectives (

Jarah et al. 2022b). According to

Sandag et al. (

2023), the effectiveness of the workforce, internal control systems, the quality of financial reports, and the function of AIS all have a positive and substantial impact on management performance.

Nevertheless, IA is a system that has access to organizational structure oversight as well as all mutually followed processes and ways to maintain the general stability of the bank’s assets from a variety of angles, where IA contributes significantly to the development of AIS (

Alawaqleh 2021). When using an AIS, IA can aid in preventing fraud and errors. Assume that better IA is needed for the AIS. Because IA aims to offer accuracy, the information system will be less helpful in situations when there is a reasonably significant risk of fraud occurring and harming both internal and external parties (

Putra 2023). IA also has a substantial influence on the comparability of AIS and the truthfulness of financial statement disclosure by limiting the extent, frequency, and proportion of related party transactions, particularly aberrant connected party dealings. IA, which can distinguish between different forms of related party transactions, is thus critical to the performance of corporate governance (

Ningrum et al. 2022). The study by

Irfan and Hamimi (

2023) discovered that the AIS impacts the quality of financial reporting, and internal control influences financial reporting. OC strengthens the impact of AIS on the quality of financial reporting, and OC strengthens the influence of internal control on financial reporting. According to

Amira and Permatasari (

2022), AISs positively and insignificantly impact employee performance, and internal control positively and significantly impacts AISs.

In order to achieve bank goals, the bank must therefore enhance its IA and AIS (

Hailat et al. 2023). Additionally, poor IA implementation will significantly lower the quality of the bank’s financial reports, as the financial data introduced must be of grade and be a base for evaluation. IA is also part of a framework used as a bank or organization-wide operational guideline approach to identify, assess, and share any corporate occurrences (

Rachman 2021;

Sastrawan et al. 2020). An AIS is a system that gathers and maintains data relevant to the bank’s activities, converts the data into meaningful information, shows plans, and delivers the required controls to protect the bank’s assets (

Jarah et al. 2023a). The research by

Wirdiansyah and Munandar (

2022) revealed that the payroll AIS was functioning properly and was able to boost the efficacy of the bank’s IA.

Syahputra (

2022) research indicates that internal control has no influence on information quality. According to

Li et al. (

2022), internal control quality helps accounting information comparability. The stronger the constraining impact of aberrant related party transactions adversely connected to AIS comparability, the higher the quality of internal control.

As a consequence, the auditor’s performance is the result of the auditor’s labor or accomplishment based on the obligations or responsibilities he obtains in the form of auditing activities in an organization or corporation (

Hazaea and Zhu 2022). Thus, auditor performance is determined by an improvement in auditor competence, the use of technology and an awareness of AIS, as well as OC (

Pura 2017). According to the findings of

Saputro (

2022) study, the AIS and internal control have an effect on the quality of financial reports. The findings of the study by

Dewi et al. (

2021) show that there is an influence of IA on accounting information technology. According to the findings of

Alawaqleh (

2021), internal control has an influence on employee performance and AIS. According to the findings of this study, the AIS plays a crucial role in the link between internal control and performance. The study by

Yusuf and Kanji (

2020) found that IA and AIS have a positive effect on internal control. The study by

Limpo and Junaidi (

2023) found that ethical and empowered leaders had a positive impact on employee job satisfaction, which also connected the predictor variables to employee job performance and OC.

Internal auditors may therefore assist management in carrying out control operations of the bank activities since they can efficiently create information required by managers to fulfill defined bank goals (

Wonoseto et al. 2022). Internal audit checks are performed by bank personnel who are not involved in the bank’s business activities and who record the bank’s financial statements. Internal auditors may help the bank achieve efficiency, effectiveness, and compliance when carrying out business activities (

Yusuf and Kanji 2020).

Napitupulu’s (

2020) research showed that the efficacy of IA has little influence on the AIS in rural banks. Accountants’ and auditors’ experience may improve decision-making (

Almaliki et al. 2019). According to

Ayoub et al. (

2020), the study’s findings show that organizational cultural qualities have a major effect on the internal control components of AIS, and hence such systems can be more prosperous in organizations that have supportive organizational cultural features. The findings of this study (

Jarah and Almatarneh 2021) showed that the AIS offers financial information with a highly predictive capacity that benefits system users. Additionally, the findings showed that an accurate grasp of OC resulted in an improvement in work quality.

Pura (

2017) discovered that auditor competence, information technology, knowledge of AIS, and OC all had a substantial favorable influence on auditor performance.

Almaliki et al.’s (

2019) findings revealed that all of the AIS parameters studied had a substantial impact on IA effectiveness. Therefore, upon the illustration of the previous results and the gap in the studies, the researchers studied the results related to the role of IA in improving the AIS in Jordanian Banks by using OC as a mediator factor, where the banks can use financial statements to acquire a better understanding of their financial situation and operating performance.

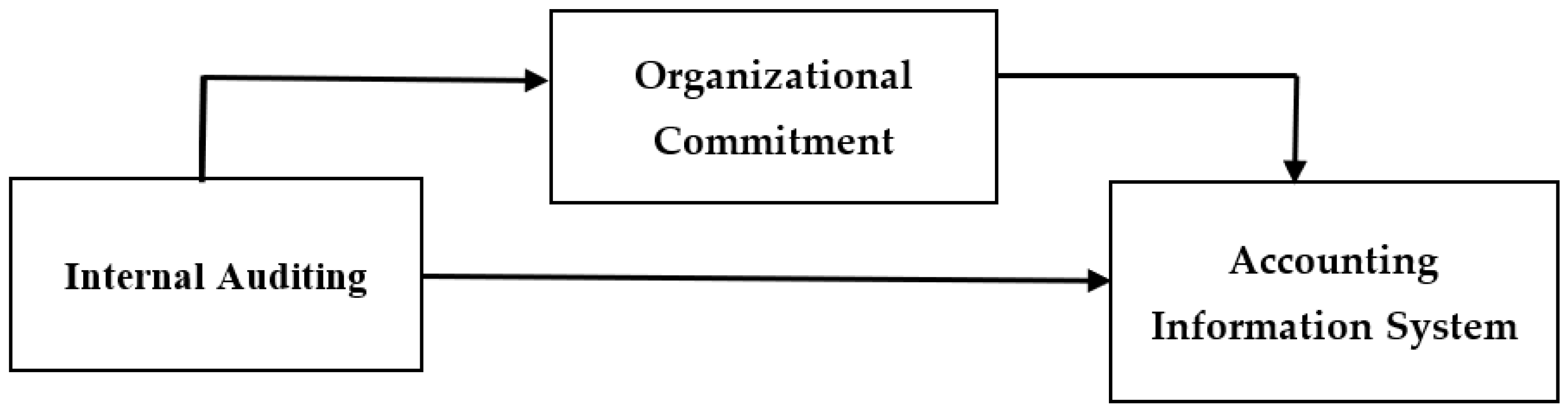

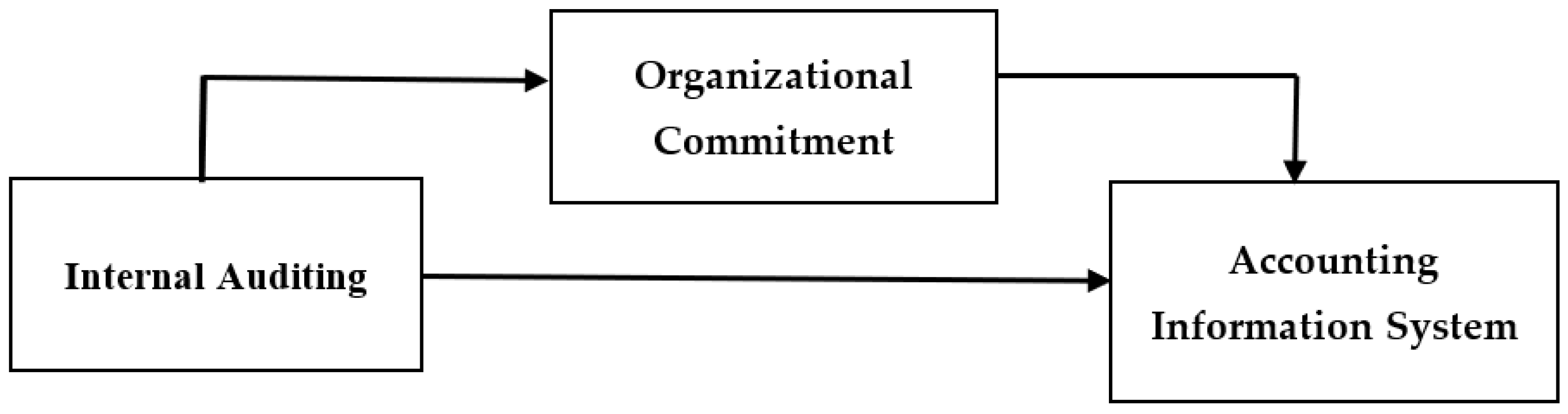

Based on the above literature review, the researchers developed the conceptual framework as shown in

Figure 1.

3. Methodology

3.1. Research Question

The importance of this study is derived from the relevance of the dependent, independent, and mediator variables of banking, which is considered to be one of the most important businesses for achieving growth and prosperity in bank sectors to increase the AIS’s effectiveness in Jordanian banks. The relevance of the difficulties that Jordanian banking has in implementing AIS will also be highlighted by this study.

Therefore, the purpose of this study is to investigate the relationship between IA and AIS in Jordanian banks, with a focus on the mediator role of OC. The study seeks to answer the following research questions:

3.2. Research Design

This study employed a quantitative research design to collect and analyze data. A cross-sectional survey method was used to collect data from a sample of employees who work in banks, including those who work in the internal audit department. The survey questionnaire was divided into three sections: the first collected demographic information, the second collected data on IA and AIS, and the third collected information on OC.

3.3. Research Instruments

Three instruments were used in this study. The independent variable (IV) in this study is IA, which includes 9 items developed by (

Al Matarneh 2011). The dependent variable (DV) is AIS, which includes 7 items developed by (

Jarah and Iskandar 2019), and the mediator variable (MD) is OC, which includes 7 items developed by (

Al-Fakeh et al. 2020)

3.4. Statistical Analysis

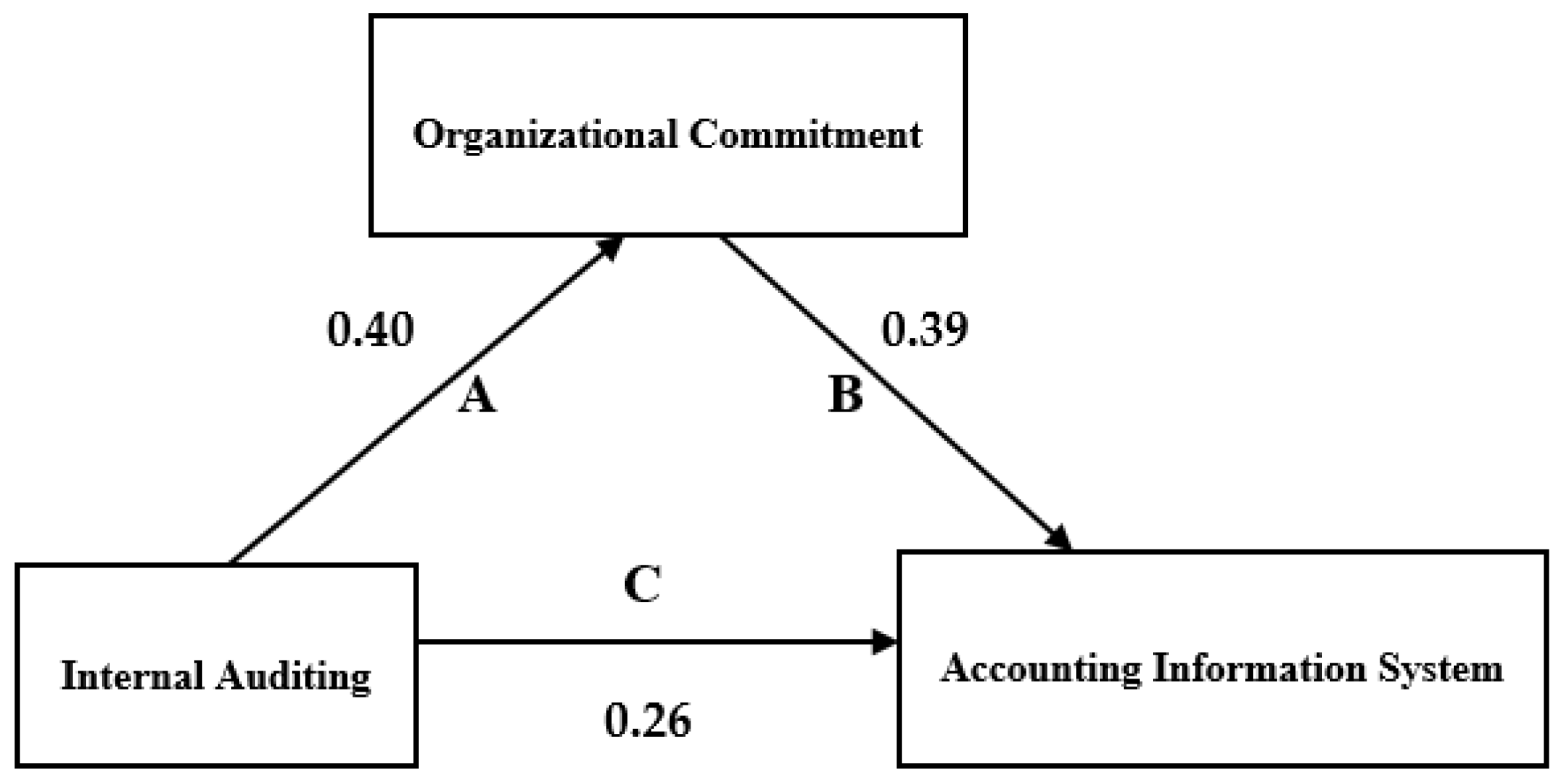

The collected data were analyzed using SPSS 26.0 and PROCESS V4.1. PROCESS V4.1 is used for evaluating direct and indirect effects in single and multiple mediator models (parallel and serial); it is frequently utilized in the social, business, and health sciences. Descriptive statistical methods, such as frequencies, percentages, means, and standard deviations, were employed to depict both the characteristics of the sample and the participants’ responses to the study items. Reliability analysis was conducted to ensure the internal consistency of the study instrument. The scale was corrected and adopted for a five-point Likert scale, where means below 2.33 were considered low, means between 2.34 and 3.66 were considered medium, and means between 3.67 and 5.00 were considered high.

The study utilized the PROCESS V4.1 macro for SPSS to test the mediator effect. Specifically, the nonparametric bootstrap method was used to test the significance level of the mediator effect.

3.5. Data Collection Procedures

In order to capture the opinions of the selected sample, the questionnaire was used as a technique of data collection. A self-administered questionnaire was selected as the survey instrument since it is a common method for gathering data for surveys and fits the nature of the current inquiry. In order to accomplish the goals of the study, the researchers employed the five-point Likert measures to create and enhance the questionnaire and gather data; the data were collected in the period between 2022 and 2023, and data collection took four months.

3.6. Participants

The study sample includes 214 employees who work in banks, including those who work in the internal audit department. A total of 193 questionnaires were completed and returned. A convenience sampling method was used to select the sample. A total of 193 individuals were surveyed, of whom 83 (43%) are male and 110 (57%) are female. In terms of age, the largest group was in the 18–34 age range, which makes up 57.5% of the sample. The 35–49 age group was the second largest group at 26.4%, followed by the 50–64 age group at 14%, and the 65 and over age group at 2.1%.

In terms of education, the most common level is a diploma, which is held by 44.6% of the sample. This is followed by a Bachelor’s degree at 34.2%, a Master’s degree at 11.9%, and a PhD at 9.3%. In terms of years of experience, the largest group has 10–15 years of experience, which accounts for 62.2% of the sample. The other three groups, less than 5 years, 5–10 years, and more than 15 years, make up 11.4%, 13%, and 13.5% of the sample, respectively.

Finally,

Table 1 shows information on the distribution of respondents across six different banks. The Jordan Kuwait Bank is the most common bank among the sample, with 25.9% of respondents using this bank. The Cairo Amman Bank is the second most common at 20.7%, followed by the Capital Bank of Jordan at 18.7%. The other three banks, Jordan Ahli Bank JAB, Jordan Islamic Bank for Finance and Investment, and Arab Jordan Investment Bank, have 16.1%, 10.4%, and 8.3% of respondents, respectively.

3.7. Validity

The questionnaire’s validity, including its content, was confirmed through peer review by the research supervisors’ members, who granted their approval. The questions were scrutinized to ensure their consistency with the content, and a sample of the questionnaire was used to test the definitions and eliminate any ambiguities for the research subjects.

3.8. Reliability Analysis

According to

Table 2, Cronbach’s alpha coefficient is acceptable for the goals of the study; Cronbach’s alpha reliability coefficient is acceptable if it exceeds 0.60 (

Sekaran and Bougie 2016).

{kind=link}

{kind=link}