This section presents the models and compares the results with those obtained from models in which a loss state is only possible during the second period. We present two different settings, one for the case where the insurance decision and the saving decision are separable, the other for the case where the individual integrates the decision for saving when purchasing insurance.

2.1. Optimal Insurance

First, we analyze the optimal level of insurance in the absence of endogenous saving. The model presented in this section corresponds to situations where an individual either forgoes her choice of saving or saves/borrows but does not integrate this into her decision-making process of insuring the risk.

Assume that a representative individual is endowed with W in both the current and the future periods and also faces the risk of losing l in both periods. The distributions of such losses in these two periods are independent to each other. The possibilities of loss during the current and the future periods are, respectively, and . As we assume only two states of the world are possible, and are the possibilities that no loss occurs in the respective periods. For simplicity, we assume both the subjective time discount rate and the rate of gross risk-free return are equal to one.

In this environment, the individual chooses at the current period the insurance coverage,

, to maximize expected utility over the two periods:

where

denotes the insurance premium, and

, the proportional loading (

in the case of a marginally fair premium).

To examine the effects of incorporating risks in both periods, we compare the optimal demand for insurance with that of a two-period model in which a loss state is only possible during the second period. This benchmark model is given as:

where

is the probability of losses during the second period, and

is the size of such loss. These specifications ensure that the expected losses, as well as the maximum possible losses over the two periods are the same between the two models. We acknowledge that it is a bit odd to assume

, but notice that

, so if we keep loss severity fixed and only vary the probabilities (i.e.,

and

), we not only eliminate half of the possibilities by constraining them as

, but also have a different maximum possible loss.

The following numerical example may help to illustrate the impact of different timings of risks.

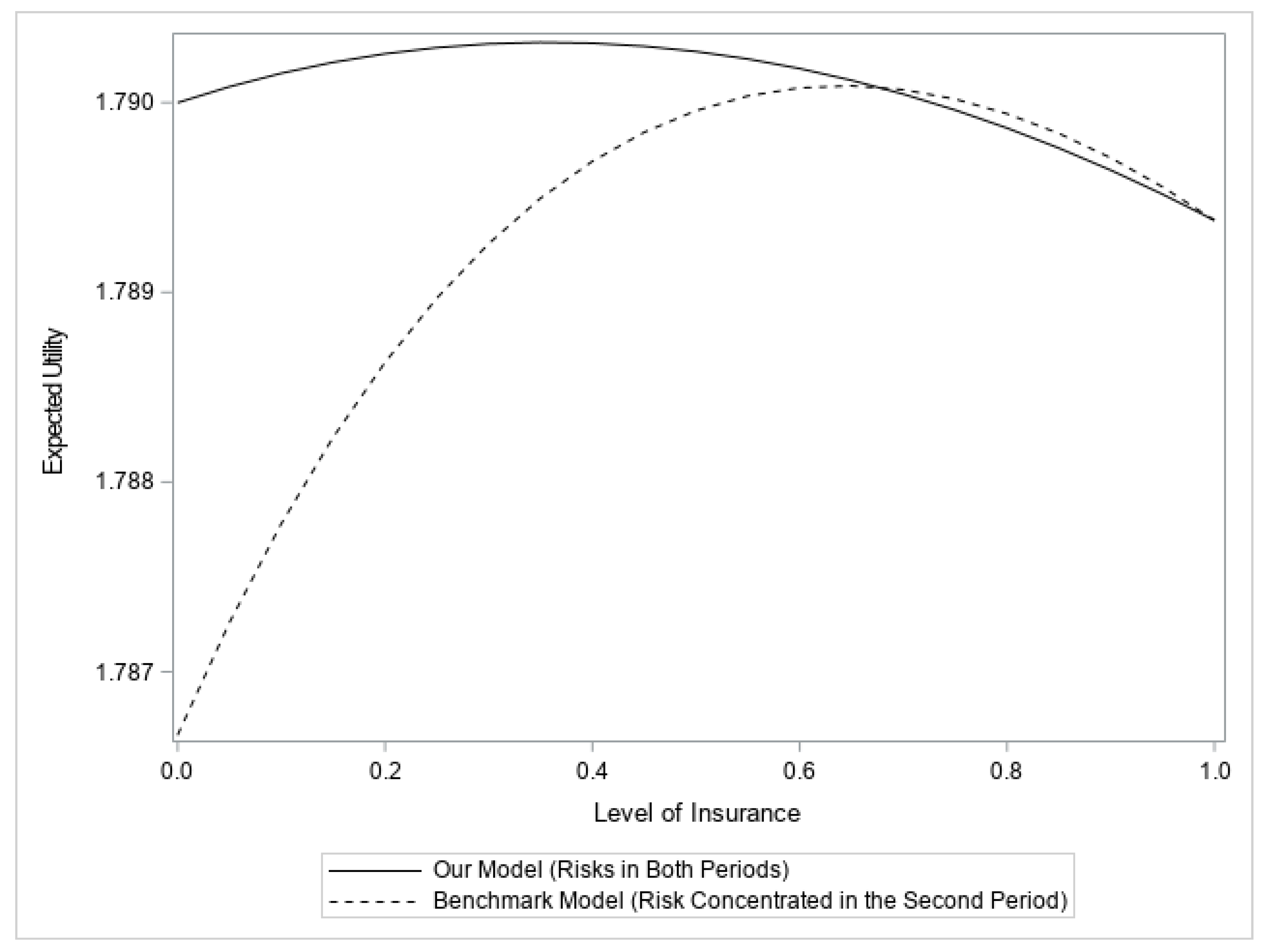

Figure 1 provides a direct impression of the differences between the two models. Though both the maximum possible loss and the expected loss of our model are the same as those of the benchmark model, our model not only has a higher maximum expected utility, its optimal level of insurance is also different from that of the benchmark model.

Next, we will formally compare the optimal insurance of our model and that of the benchmark model. It is straightforward to show that the second-order conditions are satisfied for both models as long as the individual is risk-averse (). Hence, the optimal levels of insurance in each setting can be characterized by the respective first-order conditions. With this in mind, we derive the following propositions:

For a zero loading, , we have:

Proposition 1. a. A risk-averse individual demands less than full insurance.

b. When , the decision maker demands less insurance coverage than when risk is concentrated in the second period.

c. Otherwise, the decision maker purchases less/equal/more insurance when , where is an endogenously determined threshold.

It is noteworthy that the level of consumption at the no-loss state in the second period is not permutable. Insurance decreases the consumption gaps between the respective loss and the no-loss states in both the current and the future periods. However, the cost of purchasing insurance in the first period increases the consumption gap between the no-loss state in the first period and the no-loss state in the second period, as well as the gap between the loss state in the first period and the no-loss state in the second period. Therefore, insurance is an imperfect way of smoothing consumption over time in this model. The individual purchases less than full insurance even when the insurance premium is actuarially fair, which implies Mossin’s Theorem is violated. Given the optimal level of insurance for the benchmark model, when the sum of the probabilities of losses for the two periods is larger than one in our model, the marginal cost of purchasing insurance is always greater than the expected marginal benefit, suggesting a decrease in the demand of insurance. Otherwise, the decision maker purchases less insurance than when risk is concentrated in the second period if the sum of the probabilities of losses is larger than a threshold and vice versa.

Let us now consider the case when there is a positive premium loading, i.e., . Let denote the optimal insurance coverage when risk is concentrated in the second period, we have:

Proposition 2. a. Compared to the optimal level of insurance when the price is actuarially fair, when , a decision maker always demands less insurance; when , a non-decreasing absolute prudence is the sufficient but not necessary condition for an individual to demand less insurance;

b. When or , the optimal demand for insurance is lower than that when risk is concentrated in the second period;

c. Otherwise, the optimal demand for insurance is lower/equal/higher when , where is an endogenously determined threshold.

Unlike

Mossin’s Theorem, the individual does not purchase full insurance with an actuarially fair premium. More importantly, the decision maker might purchase more insurance when the premium becomes unfair. Given the optimal level of insurance when the price is actuarially fair, a positive loading on the insurance premium increases the marginal cost of purchasing insurance, as well as the marginal benefits of insuring in both periods. If the probabilities of losses are large enough, the increases in the marginal cost always outweigh the increases in marginal benefit for the loss state in the first period, resulting in a lower demand for insurance. On the other hand, if the probabilities are small, a non-decreasing absolute prudence

1 ensures the increases in marginal cost are more than the increases in marginal benefits for the loss states in both periods. This is important because standard risk aversion requires decreasing absolute prudence (

Kimball (

1993)), implying that it is possible for an average decision maker to purchase more insurance when the price becomes unfair.

When individuals make insurance decisions, they face several uncertainties. First, they do not know whether the losses will occur or not over the two periods. Second, they do not know how many losses will occur. Lastly, when a loss occurs, they are uncertain whether it will happen during the first period or the second one. Therefore, the individuals need to take into account all the uncertainties during the decision-making process.

Propositions 1 and 2 summarize such effects. Besides the deviation from Mossin’s Theorem, it is also interesting to observe that when the cost of insurance is within a certain range, whether the decision maker demands more or less insurance than when risk is concentrated in the second period depends on whether the price is lower or higher than a threshold. Notice that a higher cost of insurance does not necessarily mean a larger premium loading; it can also mean the risk is greater, in the sense that the sum of the probabilities of losses for the two periods is larger.

For an illustration, we compare the degree of riskiness in our model with that of the benchmark model where risk is concentrated in the second period. In a two-period model with a zero time discounting rate, one can multiply all the probabilities by

. Then, without loss of generality, the wealth prospects are the same ones as in the setting of a single-period model. Therefore, we can use an illustration similar to the one in

Briys and Schlesinger (

1990). First, we compare the risks in the two models. Even though we construct our model so that the expected loss, as well as the probable maximum loss, are the same as those of a benchmark model, the risks, as defined in

Rothschild and Stiglitz (

1970), are different. Under the assumption of a zero time discounting rate, we can normalize the sum of the probabilities for the four states to one. Then, an individual’s wealth prospects over the two periods for both models can be illustrated as shown in

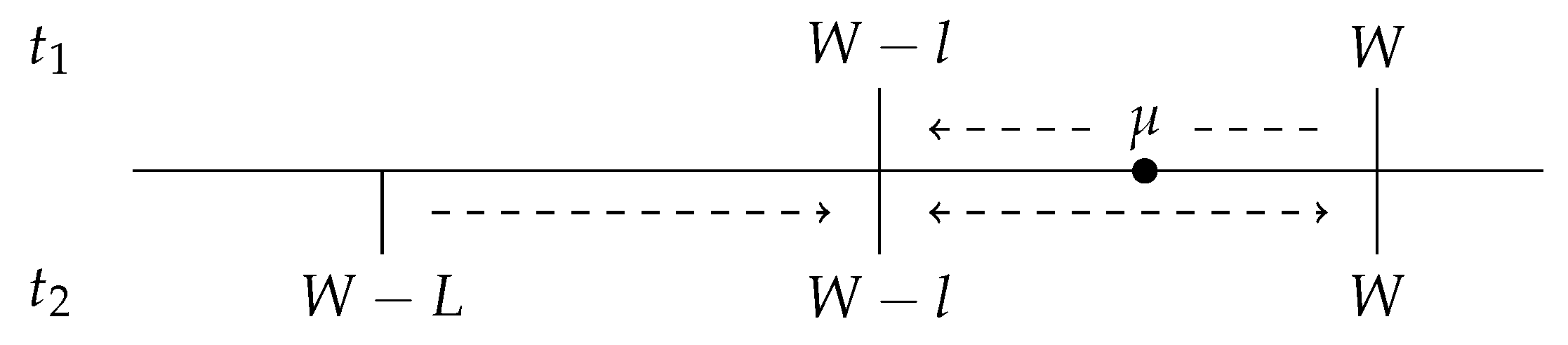

Figure 2.

For the benchmark model, the individual’s wealth is W plus a lottery between and W. For our model, the individual’s wealth is the sum of two lotteries between and W. By construction, these two models have the same expected wealth, , over the two periods. Essentially, from the benchmark model to our model, some of the probability mass () is shifted from W to during the first period, while in the second period the entire probability mass () is shifted from to and/or W. Moreover, some of the probability mass might shift from W to , resulting in a probability mass of at and a probability mass of at W. Ultimately, the two probability masses in the benchmark model, W and , are shifted to W and in our model. Such a shift is a mean-preserving contraction of the wealth distribution, representing a decrease in risk. Therefore, the situation faced by the decision maker in our model is less risky than the one faced in the benchmark model.

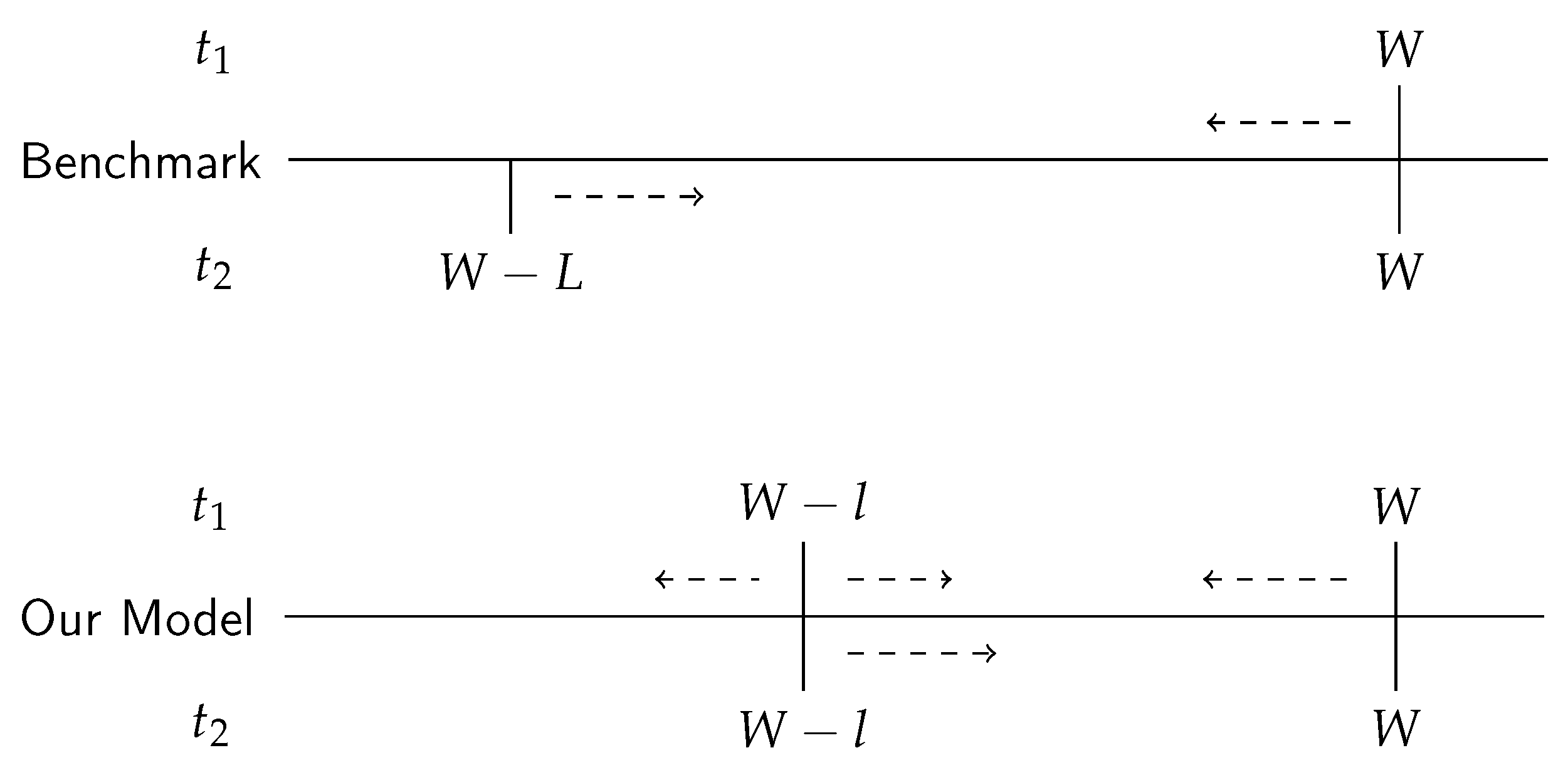

Now, consider the case of insurance. Again, we normalize the sums of probabilities to one, and the individual’s wealth prospects can be illustrated as in

Figure 3. Assuming the same level of insurance for both models, in the benchmark model, final wealth in the first period is reduced by

, while final wealth in the loss state in the second period is increased by

. In our model, final wealth in the no-loss state in the first period is reduced by

, while final wealth in the loss state in the second period is increased by

. As for the loss state in the first period, whether final wealth increases or decreases depends on the sign of

. Because the expected loss is the same for both models, the expected wealth over the two periods is also the same given the same loading factor

.

In our model, when , . It suggests that the effect of insurance causes both a (mean-preserving) spread and a (mean-preserving) contraction in the wealth distribution, so that it is less effective compared to its effects in the benchmark model, in which it always represents a (mean-preserving) contraction. Mean-preserving is achieved when the insurance price is actuarially fair. We have already illustrated that there is less risk in our model. Therefore, as shown in Propositions 1 and 2, when with or when with , the decision maker always demands less insurance coverage than when risk is concentrated in the second period.

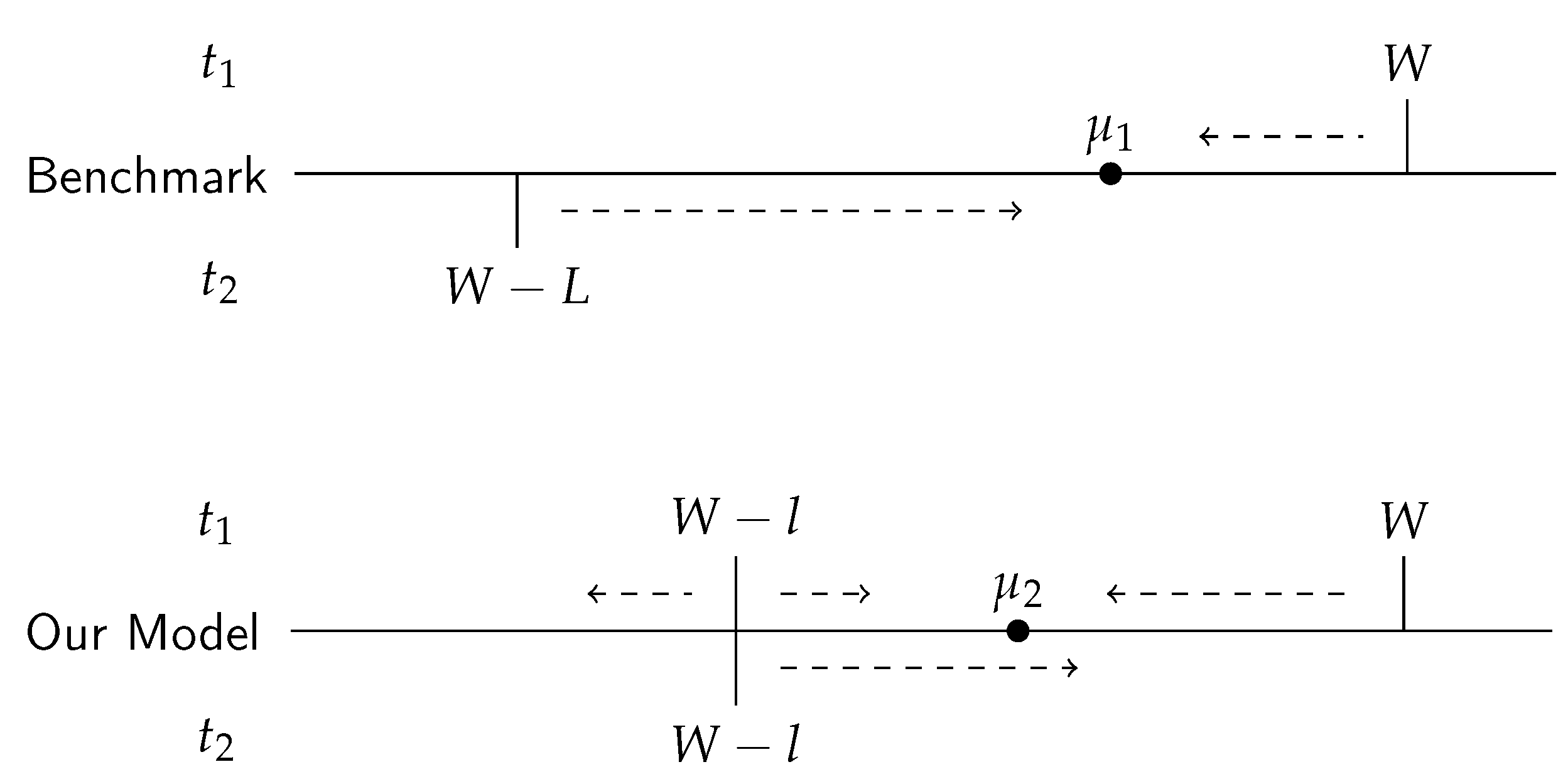

On the other hand, if we focus on the states that are affected by the choice of insurance and normalize the sums of these probabilities to one, we can illustrate the individual’s wealth prospects as in

Figure 4.

and are the expected levels of wealth given a loss state occurs in the second period for the benchmark model and our model, respectively. Consider the case when . We have and . Thus, the optimal level of insurance for the benchmark model is , and the two probability masses of W and are shifted to . In our model, insurance cannot equate the levels of wealth for all three states to .

We have shown that when the decision maker always demands less insurance compared to that in the benchmark model. If , things are not quite straightforward. Applying to the model, we have , , and , where , , and are the levels of wealth for the three states. Increasing the level of insurance will move the probability mass of closer to while moving further from it. We know an increase in insurance will move the probability mass of to the left, but because when , whether the probability mass will move closer or further from remains endogenously determined. Therefore, even though the insured risk is less risky in our model and the insurance itself might not be as effective, the decision maker could still demand more insurance.

2.2. Optimal Insurance and Optimal Saving

In the previous model, we exclude the possibility of saving in order to focus our inquiry on the case when the decisions for saving do not play a role in the determination of optimal insurance. Here, we examine the situation when the decisions for insurance and saving are made jointly.

In addition to consuming and purchasing insurance, individuals also decide how much they want to save or borrow at Period 1. We denote by

S the individual’s savings. Note that

S stands for saving for

, and borrowing for

. The individual’s objective function then changes to:

When endogenous saving can be used to achieve consumption smoothing, the second-period wealth in the no-loss state is affected by the individual’s decisions. Mossin’s Theorem can be proved with this model:

Lemma 1. With endogenous saving, an individual purchases full insurance if and only if the premium is actuarially fair.

This is reminiscent of the Separation Theorem obtained by

Dionne and Eeckhoudt (

1984), in which endogenous saving is described implicitly. In addition, our finding extends

Mossin’s Theorem to a two-period setting in which both periods are subject to the risk of loss. With a zero premium loading, full insurance (

) equates the consumption level of the loss state and that of the respective no-loss state in each period. The corresponding saving choice,

, equates the levels of consumption in

and

.

On the other hand, even though the levels of consumption across periods/states can still be equalized, a positive premium loading causes insurance (or sacrificing saving/increasing borrowing to fund insurance purchase) to generate a cost of lower aggregate consumption over time. Therefore, it is not optimal to purchase full coverage. In conclusion, Mossin’s Theorem is restored for the model with both insurance and endogenous saving.

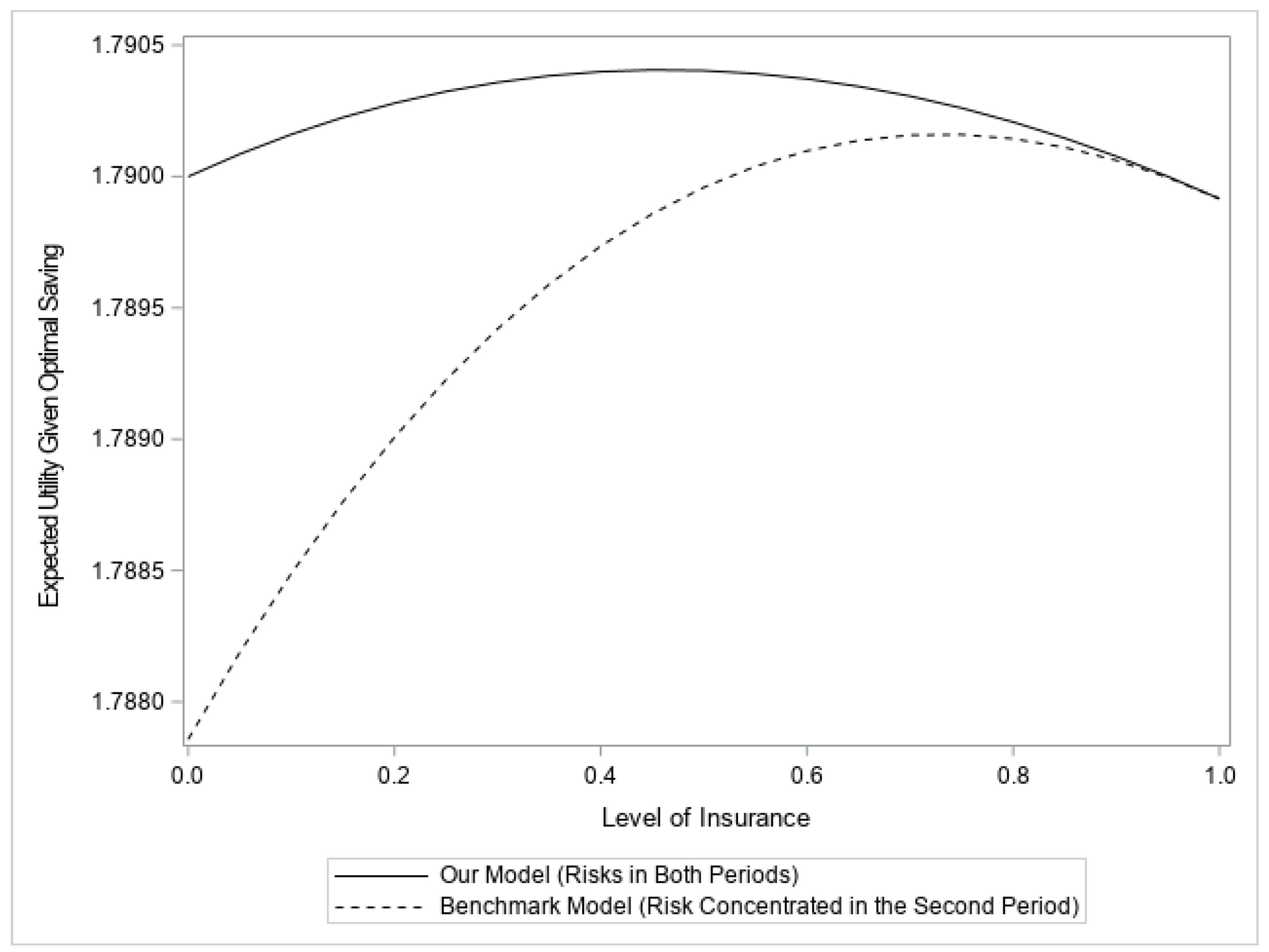

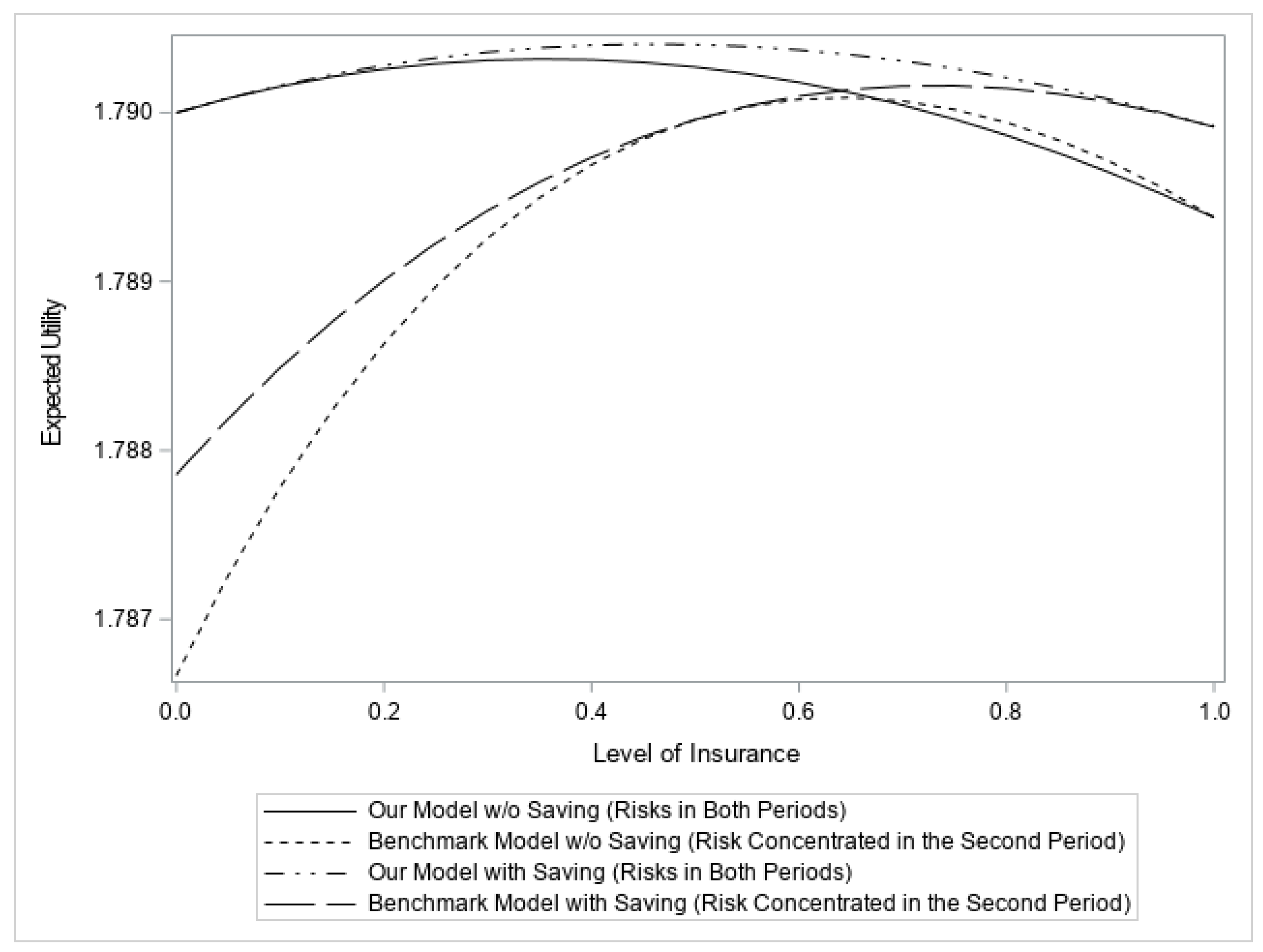

Figure 5 illustrates the differences between our model and the benchmark model with the presence of endogenous saving. The expected utilities are calculated with the optimal levels of saving given different levels of insurance. Even when the decision maker can shift wealth between periods, the different timings of losses still have a profound effect on the optimal demand for insurance. When compared with

Figure 12, we notice that the presence of endogenous saving increases both the maximum expected utilities and the optimal levels of insurance for both models, but the difference between the two optimal insurance levels still persists.

As discussed in

Hofmann and Peter (

2016), because both insurance and saving are endogenous, the saving choice that is optimal for one level of insurance is typically not optimal for other levels of insurance. Thus, we cannot directly plug the first-order condition of one model into that of the other model and check the sign. Therefore, comparing the optimal choice of insurance with that of the benchmark model in which risk is concentrated in the second period seems difficult. Fortunately, using the method proposed by

Gollier (

2004), we are still able to investigate the effects of having risks in both periods. The results are summarized in the following proposition:

Proposition 3. When , the optimal demand for insurance is lower/equal/higher than that when risk is concentrated in the second period, where is an endogenously determined threshold.

Endogenous saving helps individuals achieve better consumption smoothing and changes the optimal level of insurance. Individuals purchase full insurance with an actuarially fair price. When there is a positive premium loading, comparing the optimal demand for insurance with that of the benchmark model in which risk is concentrated in the second period shows that the decision maker demands less insurance when the cost of insurance is higher than a threshold and vice versa. Again, a higher cost of insurance can be the result of either a larger premium loading or a larger sum of the probabilities of losses for the two periods or both.

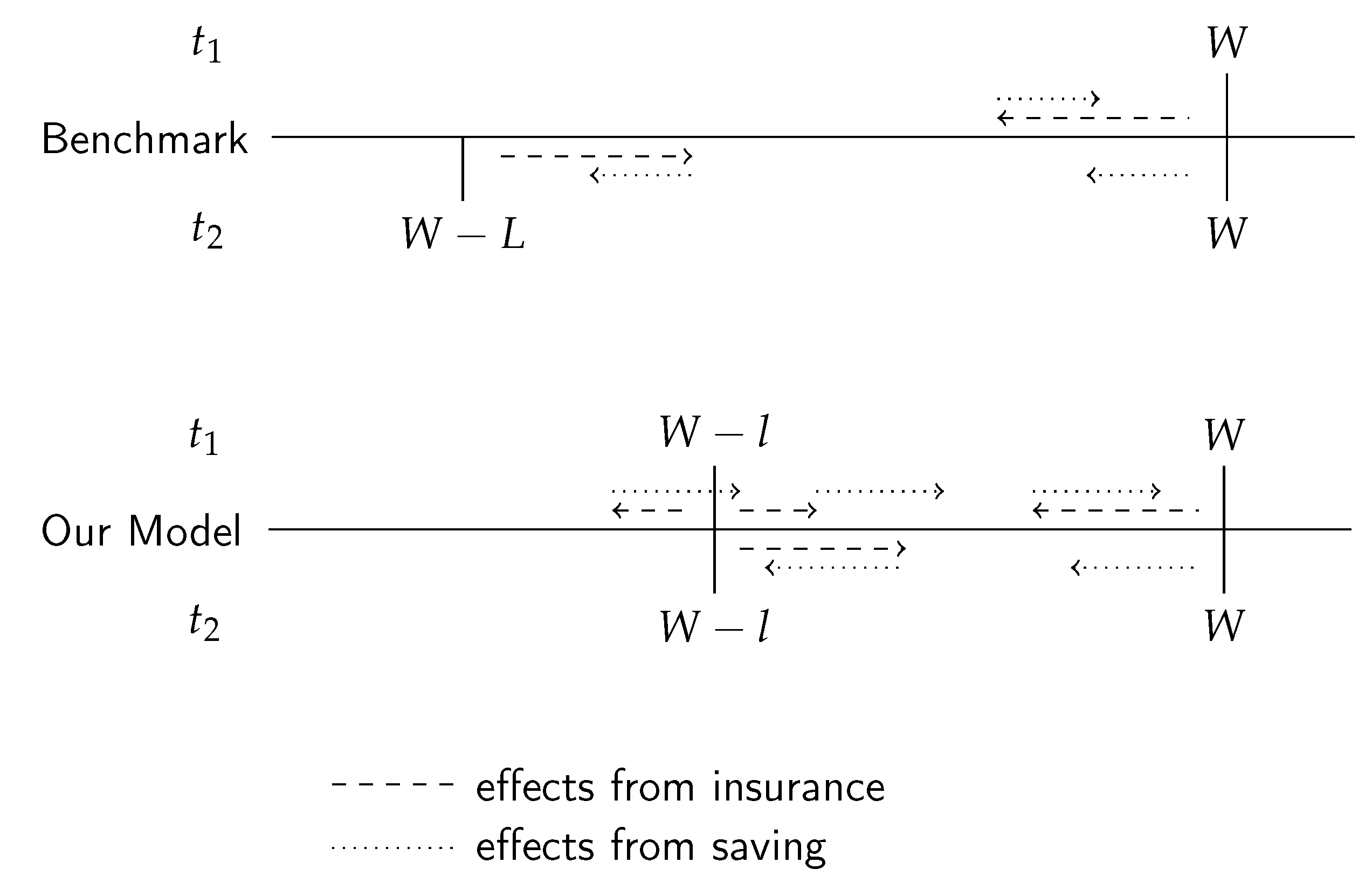

As for the effects on riskiness, when taking into account endogenous saving, the decision maker can move wealth between periods. If the endowments are the same in both periods, we have shown that the individual will borrow in the first period. The individual’s wealth prospects are illustrated in

Figure 6.

As can be seen from

Figure 6, in each model, borrowing moves some of the wealth from the second period to the first one. Thus, even though insurance might still cause a spread in the wealth distribution, this effect can be “fixed” by borrowing from the future. Therefore, whether the decision maker purchases more or less insurance than one would if risk is concentrated in the second period is now determined endogenously, as we shown in Proposition 3.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}