Risk Factor Disclosures in the US Airline Industry Following the COVID-19 Pandemic

Abstract

:1. Introduction

2. Literature Review

2.1. Risk Factors’ Disclosures

2.2. Risk Disclosure in the Aviation Industry

3. Methodology

3.1. Sample and Data Collection

3.2. Data Analysis

4. Findings

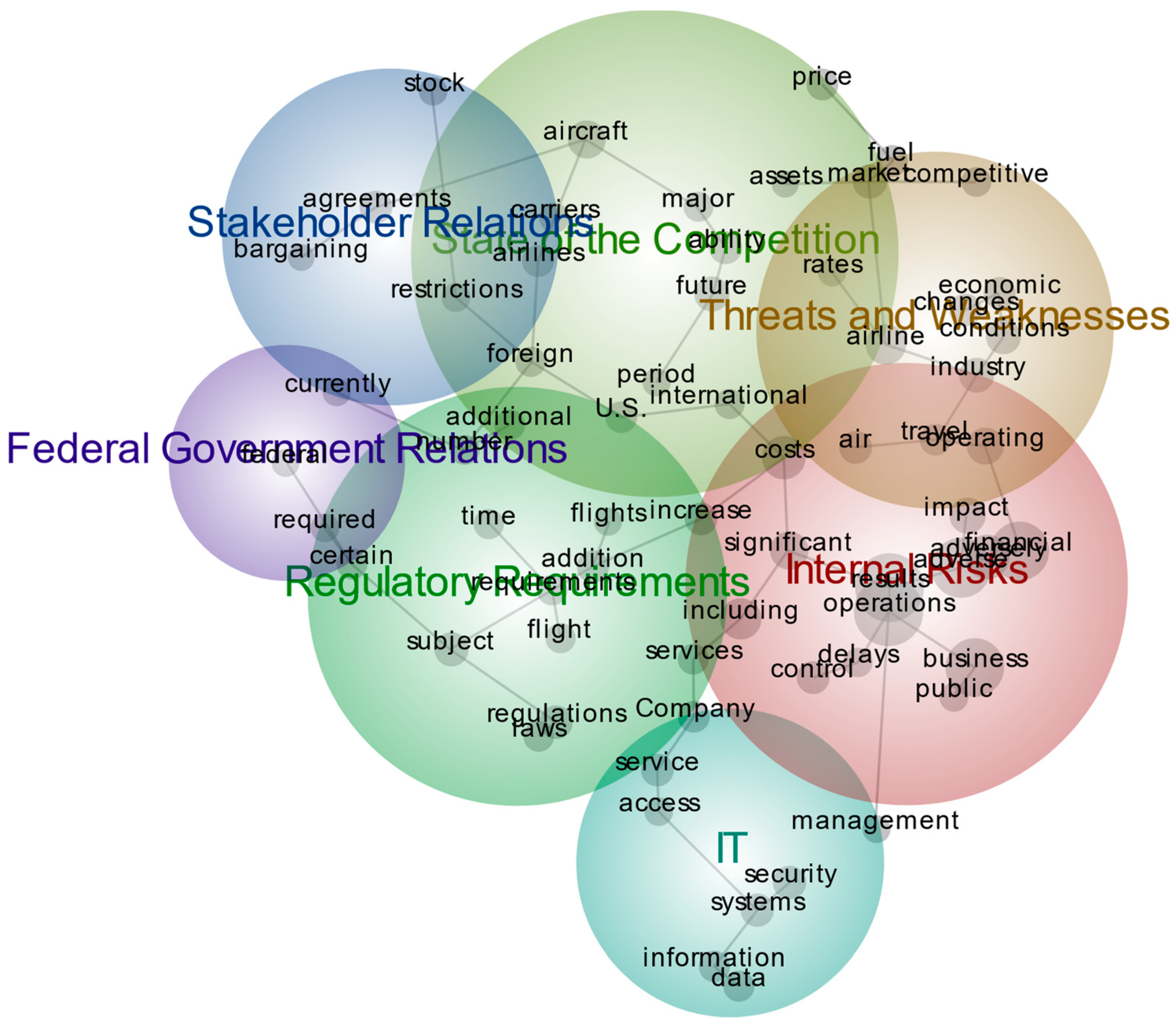

4.1. Main Concepts of the Years 2019 and 2020

4.2. Main Themes of the Year 2019

4.2.1. Internal Risks

4.2.2. State of the Competition

4.2.3. Threats and Weaknesses

4.2.4. Regulatory Requirements

4.2.5. IT

4.2.6. Stakeholder Relations

4.2.7. Federal Government Relations

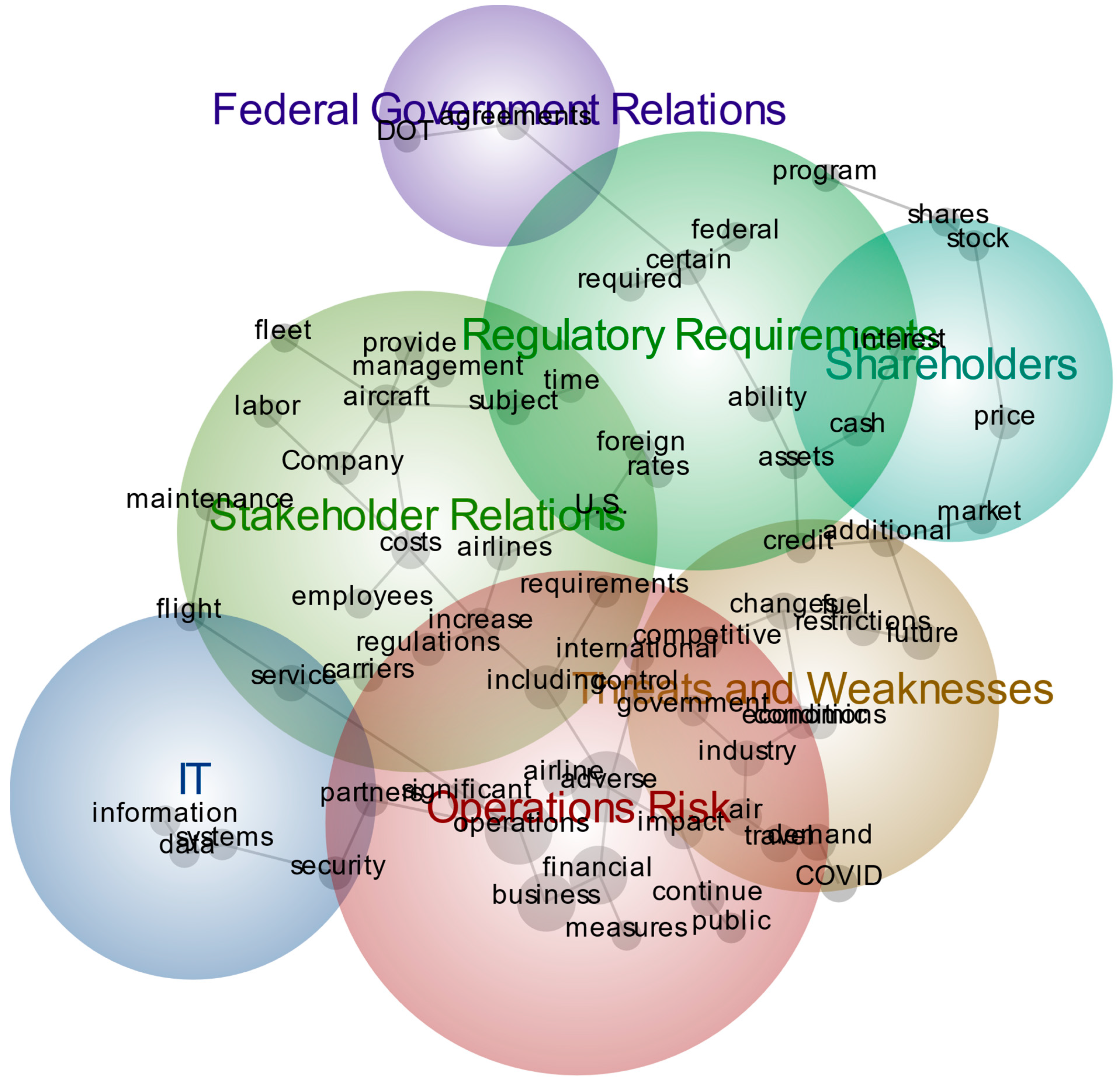

4.3. Main Themes of the Year 2020

4.3.1. Operations Risk

4.3.2. Stakeholder Relations

4.3.3. Threats and Weaknesses

4.3.4. Regulatory Requirements and Federal Government Relations

4.3.5. Shareholders

4.3.6. IT

5. Discussion

6. Conclusions

7. Contributions

8. Limitations and Future Research

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

| 1 | Federal Aviation Administration. |

| 2 | Transportation Security Administration. |

| 3 | Net Operating Losses. |

| 4 | AAR and Aviall are maintenance and other aviation services’ partners. |

| 5 | General Electric (engine supplier). |

| 6 | Alaska Air Group’s wholly owned subsidiaries. |

| 7 | American Airlines Group. |

References

- Abraham, Santhosh, and Philip J. Shrives. 2014. Improving the relevance of risk factor disclosure in corporate annual reports. The British Accounting Review 46: 91–107. [Google Scholar] [CrossRef]

- Akhigbe, Aigbe, and Anna D. Martin. 2008. Influence of disclosure and governance on the risk of US financial services firms following Sarbanes-Oxley. Journal of Banking & Finance 32: 2124–35. [Google Scholar] [CrossRef]

- Albers, Sascha, and Volker Rundshagen. 2020. European airlines′ strategic responses to the COVID-19 pandemic (January–May, 2020). Journal of Air Transport Management 87: 101863–101863. [Google Scholar] [CrossRef] [PubMed]

- Arasli, Huseyin, Mehmet Saydam, and Hasan Kilic. 2020. Cruise Travelers’ Service Perceptions: A Critical Content Analysis. Sustainability 12: 6702. [Google Scholar] [CrossRef]

- Atems, Bebonchu, and Jules Yimga. 2021. Quantifying the impact of the COVID-19 pandemic on US airline stock prices. Journal of Air Transport Management 97: 102141. [Google Scholar] [CrossRef]

- Bae, Wonmi, and Junwook Chi. 2021. Content Analysis of Passengers’ Perceptions of Airport Service Quality: The Case of Honolulu International Airport. Journal of Risk and Financial Management 15: 5. [Google Scholar] [CrossRef]

- Bao, Yang, and Anindya Datta. 2014. Simultaneously Discovering and Quantifying Risk Types from Textual Risk Disclosures. Management Science 60: 1371–91. [Google Scholar] [CrossRef]

- Beretta, Sergio, and Saverio Bozzolan. 2004. A framework for the analysis of firm risk communication. The International Journal of Accounting 39: 265–88. [Google Scholar] [CrossRef]

- Berghöfer, Britta, and Brian Lucey. 2014. Fuel hedging, operational hedging and risk exposure—Evidence from the global airline industry. International Review of Financial Analysis 34: 124–39. [Google Scholar] [CrossRef]

- Brown, Richard S., and William A. Kline. 2020. Exogenous shocks and managerial preparedness: A study of U.S. airlines’ environmental scanning before the onset of the COVID-19 pandemic. Journal of Air Transport Management 89: 101899. [Google Scholar] [CrossRef]

- Budd, Lucy, Stephen Ison, and Nena Adrienne. 2020. European airline response to the COVID-19 pandemic—Contraction, consolidation and future considerations for airline business and management. Research in Transportation Business & Management 37: 100578. [Google Scholar] [CrossRef]

- Cabedo, J.David, and José Miguel Tirado. 2004. The disclosure of risk in financial statements. Accounting Forum 28: 181–200. [Google Scholar] [CrossRef]

- Callaway, Ewen, David Cyranoski, Smriti Mallapaty, Emma Stoye, and Jeff Tollefson. 2020. Coronavirus by the Numbers. Nature 579: 482–83. Available online: https://www.nature.com/articles/d41586-020-00758-2 (accessed on 1 November 2022). [CrossRef] [PubMed]

- Campbell, John L., Hsinchun Chen, Dan S. Dhaliwal, Hsin-Min Lu, and Logan B. Steele. 2014. The information content of mandatory risk factor disclosures in corporate filings. Review of Accounting Studies 19: 396–455. [Google Scholar] [CrossRef]

- Elshandidy, Tamer, Philip J. Shrives, Matt Bamber, and Santhosh Abraham. 2018. Risk reporting: A review of the literature and implications for future research. Journal of Accounting Literature 40: 54–82. [Google Scholar] [CrossRef]

- Gao, Lei, Thomas G. Calderon, and Fengchun Tang. 2020. Public companies’ cybersecurity risk disclosures. International Journal of Accounting Information Systems 38: 100468. [Google Scholar] [CrossRef]

- Global Industry Analysts. 2021. Global Airlines Industry. ReportLinker. Available online: https://www.reportlinker.com/p05817569/Global-Airlines-Industry.html?utm_source=GNW (accessed on 1 November 2022).

- Gong, Stephen X. H., Michael Firth, and Kevin Cullinane. 2006. The information content of earnings releases by global airlines. Journal of Air Transport Management 12: 82–91. [Google Scholar] [CrossRef]

- Gössling, Stefan, Daniel Scott, and C. Michael Hall. 2021. Pandemics, tourism and global change: A rapid assessment of COVID-19. Journal of Sustainable Tourism 29: 1–20. [Google Scholar] [CrossRef]

- Hanlon, Pat. 1999. Global Airlines: Competition in a Transnational Industry. Oxford: Butterworth-Heinemann. [Google Scholar]

- Hannigan, Thomas J., Robert D. Hamilton III, and Ram Mudambi. 2015. Competition and competitiveness in the US airline industry. Competitiveness Review 25: 134–55. [Google Scholar] [CrossRef]

- Hao, Yu, Hanyu Bai, and Shiwei Sun. 2021. How does COVID-19 affect tourism in terms of people’s willingness to travel? Empirical evidence from China. Tourism Review 76: 892–909. [Google Scholar] [CrossRef]

- Hassan, Mostafa Kamal. 2009. UAE corporations-specific characteristics and level of risk disclosure. Managerial Auditing Journal 24: 668–87. [Google Scholar] [CrossRef]

- Hogan, Karen M. 2020. A global comparison of corporate value adjustments to news of cyber-attacks. Journal of Governance and Regulation 9: 34–44. [Google Scholar] [CrossRef]

- Indulska, Marta, Dirk S. Hovorka, and Jan Recker. 2012. Quantitative approaches to content analysis: Identifying conceptual drift across publication outlets. European Journal of Information Systems 21: 49–69. [Google Scholar] [CrossRef]

- Kang, Helen, and Sidney J. Gray. 2019. Country-specific risks and geographic disclosure aggregation: Voluntary disclosure behaviour by British multinationals. The British Accounting Review 51: 259–76. [Google Scholar] [CrossRef]

- Kim, Dongwook, and Sungbum Kim. 2017. Sustainable Supply Chain Based on News Articles and Sustainability Reports: Text Mining with Leximancer and DICTION. Sustainability 9: 1008. [Google Scholar] [CrossRef]

- Kravet, Todd, and Volkan Muslu. 2013. Textual risk disclosures and investors’ risk perceptions. Review of Accounting Studies 18: 1088–122. [Google Scholar] [CrossRef]

- Lajili, Kaouthar, and Daniel Zéghal. 2009. A Content Analysis of Risk Management Disclosures in Canadian Annual Reports. Canadian Journal of Administrative Sciences/Revue Canadienne Des Sciences de L’administration 22: 125–42. [Google Scholar] [CrossRef]

- Lemon, Laura, and Jameson Hayes. 2020. Enhancing Trustworthiness of Qualitative Findings: Using Leximancer for Qualitative Data Analysis Triangulation. The Qualitative Report 25: 604–14. [Google Scholar] [CrossRef]

- Leximancer. 2021. Leximancer User Guide: Vol. Release 4. Available online: https://static1.squarespace.com/static/5e26633cfcf7d67bbd350a7f/t/60682893c386f915f4b05e43/1617438916753/Leximancer+User+Guide+4.5.pdf (accessed on 1 November 2022).

- Linsley, Philip M., and Philip J. Shrives. 2006. Risk reporting: A study of risk disclosures in the annual reports of UK companies. The British Accounting Review 38: 387–404. [Google Scholar] [CrossRef]

- Lobo, Gerald J., Wei Z. Siqueira, Kinsun Tam, and Jian Zhou. 2019. Does SEC FRR No. 48 disclosure communicate risk management effectiveness? Journal of Accounting and Public Policy 38: 106696. [Google Scholar] [CrossRef]

- Maneenop, Sakkakom, and Suntichai Kotcharin. 2020. The impacts of COVID-19 on the global airline industry: An event study approach. Journal of Air Transport Management 89: 101920–101920. [Google Scholar] [CrossRef] [PubMed]

- Martin, Nigel J., and John L. Rice. 2007. Profiling Enterprise Risks in Large Computer Companies Using the Leximancer Software Tool. Risk Management 9: 188–206. [Google Scholar] [CrossRef]

- Miihkinen, Antti. 2012. What Drives Quality of Firm Risk Disclosure? The International Journal of Accounting 47: 437–68. [Google Scholar] [CrossRef]

- Nelson, Karen K., and Adam C. Pritchard. 2007. Litigation Risk and Voluntary Disclosure: The Use of Meaningful Cautionary Language. Paper presented at 2nd Annual Conference on Empirical Legal Studies Paper, New York, NY, USA, November 9–10. [Google Scholar]

- Ong, Faith, Oscar Vorobjovas-Pinta, and Clifford Lewis. 2020. LGBTIQ + identities in tourism and leisure research: A systematic qualitative literature review. Journal of Sustainable Tourism 30: 1476–99. [Google Scholar] [CrossRef]

- OSHA. 2021. SIC Manual. Available online: https://www.osha.gov/sic-manual/4512 (accessed on 28 September 2021).

- Penela, Daniela, and Rogério M. Serrasqueiro. 2019. Identification of risk factors in the hospitality industry: Evidence from risk factor disclosure. Tourism Management Perspectives 32: 100578. [Google Scholar] [CrossRef]

- Probohudono, Agung Nur, Kelly Anh Vu, and Tyara Mayang Mustika. 2014. Risk reporting practices by the aviation industry. Corporate Ownership and Control 12: 438–49. [Google Scholar] [CrossRef]

- Schuster, Peter, and Vincent O’Connell. 2006. The Trend toward Voluntary Corporate Disclosures. Management Accounting Quarterly 7: 1–9. Available online: https://www.imanet.org/insights-and-trends/management-accounting-quarterly/maq-index/2006/winter-2006?ssopc=1 (accessed on 28 September 2021).

- Securities and Exchange Commission (SEC). 2005. Securities Exchange Commission Final Rule, Release Number 33-8591. Available online: https://www.sec.gov/rules/final/33-8591.pdf (accessed on 1 November 2022).

- Securities and Exchange Commission (SEC). 2016. Business and Financial Disclosure Required by Regulation S-K. Available online: https://www.sec.gov/rules/concept/2016/33-10064.pdf (accessed on 1 November 2022).

- Securities and Exchange Commission (SEC). 2018. Commission Statement and Guidance on Public Company Cybersecurity Disclosures. Available online: https://www.sec.gov/rules/interp/2018/33-10459.pdf (accessed on 25 June 2018).

- Securities and Exchange Commission (SEC). 2021. SEC.gov|About EDGAR. Available online: https://www.sec.gov/edgar/about (accessed on 1 November 2022).

- Shivaani, M. V., and Nishant Agarwal. 2020. Does competitive position of a firm affect the quality of risk disclosure? Pacific-Basin Finance Journal 61: 101317. [Google Scholar] [CrossRef]

- Smith, Andrew E., and Michael S. Humphreys. 2006. Evaluation of unsupervised semantic mapping of natural language with Leximancer concept mapping. Behavior Research Methods 38: 262–79. [Google Scholar] [CrossRef]

- Sobieralski, Joseph B. 2020. COVID-19 and airline employment: Insights from historical uncertainty shocks to the industry. Transportation Research Interdisciplinary Perspectives 5: 100123–100123. [Google Scholar] [CrossRef]

- Spry, Damien, and Tim Dwyer. 2017. Representations of Australia in South Korean online news: A qualitative and quantitative approach utilizing Leximancer and Korean keywords in context. Quality & Quantity 51: 1045–64. [Google Scholar] [CrossRef]

- Suk, Minho, and Wonjoon Kim. 2021. COVID-19 and the airline industry: Crisis management and resilience. Tourism Review 76: 984–98. [Google Scholar] [CrossRef]

- Teeroovengadum, Viraiyan, Boopen Seetanah, Eric Bindah, Arshad Pooloo, and Isven Veerasawmy. 2021. Minimising perceived travel risk in the aftermath of the COVID-19 pandemic to boost travel and tourism. Tourism Review 76: 910–28. [Google Scholar] [CrossRef]

- Tisdell, Clement A. 2020. Economic, social and political issues raised by the COVID-19 pandemic. Economic Analysis and Policy 68: 17–28. [Google Scholar] [CrossRef]

- TSA. 2021. TSA Checkpoint Travel Numbers. Available online: https://www.tsa.gov/coronavirus/passenger-throughput (accessed on 6 October 2021).

- Tseng, Chi, Bihu Wu, Alastair M. Morrison, Jingru Zhang, and Ying-Chen Chen. 2015. Travel blogs on China as a destination image formation agent: A qualitative analysis using Leximancer. Tourism Management 46: 347–58. [Google Scholar] [CrossRef]

- Vyychytilova, Jana, Orkhan Nadirov, Drahomira Pavelkova, and Martin Mikeska. 2020. Risk Reporting Practices of Listed Companies: Cross- Country Empirical Evidence from the Auto Industry. Journal of Competitiveness 12: 161–79. [Google Scholar] [CrossRef]

- Wang, Yinghui, Bin Li, Guowen Li, Xiaoqian Zhu, and Jianping Li. 2019. Risk factors identification and evolution analysis from textual risk disclosures for insurance industry. Procedia Computer Science 162: 25–32. [Google Scholar] [CrossRef]

- Wilk, Violetta, Geoffrey Soutar, and Paul Harrigan. 2019. Tackling social media data analysis. Qualitative Market Research: An International Journal 22: 94–113. [Google Scholar] [CrossRef]

- Wilk, Violetta, Helen Cripps, Alexandru Capatina, Adrian Micu, and Angela-Eliza Micu. 2021. The state of #digitalentrepreneurship: A big data Leximancer analysis of social media activity. International Entrepreneurship and Management Journal 17: 1899–916. [Google Scholar] [CrossRef]

- World Bank. 2021. Air Transport Passengers Carried. Available online: https://data.worldbank.org/indicator/IS.AIR.PSGR?most_recent_value_desc=true (accessed on 28 September 2021).

- WTO. 2020. 100% of Global Destinations Now Have COVID-19 Travel Restrictions, UNWTO Reports|UNWTO. Available online: https://www.unwto.org/news/covid-19-travel-restrictions (accessed on 7 October 2021).

- Yashodha, Yasmin, Baharom Abdul Hamid, and Muzaffar Shah Habibullah. 2017. Financial Risk Exposures of the Airlines Industry: Evidence from Cathay Pacific and China Airlines. International Journal of Business and Society 17: 221–24. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

| Company | HQ | 2019 Report Date | 2020 Report Date |

|---|---|---|---|

| ALASKA AIR GROUP, INC. | Washington | 12 February 2020 | 26 February 2021 |

| Allegiant Travel CO | Nevada | 27 February 2020 | 1 March 2021 |

| AMERICAN AIRLINES, INC. | Texas | 19 February 2020 | 17 February 2021 |

| DELTA AIRLINES, INC. | Georgia | 3 February 2020 | 2 February 2021 |

| HAWAIIAN HOLDINGS INC | Hawaii | 12 February 2020 | 1 February 2021 |

| JETBLUE AIRWAYS CORP | New York | 18 February 2020 | 2 March 2021 |

| MESA AIR GROUP INC | Arizona | 17 December 2019 | 14 December 2020 |

| SKYWEST INC | Utah | 18 February 2020 | 22 February 2021 |

| SOUTHWEST AIRLINES CO | Texas | 4 February 2020 | 8 February 2021 |

| Spirit Airlines, Inc. | Florida | 16 April 2020 | 10 February 2021 |

| UNITED AIRLINES, INC. | Illinois | 25 February 2020 | 1 March 2021 |

| Nr. | Concept | Count | Relevance | Nr. | Concept | Count | Relevance |

|---|---|---|---|---|---|---|---|

| 1 | results | 1042 | 100% | 34 | certain | 156 | 15% |

| 2 | operations | 1035 | 99% | 35 | additional | 143 | 14% |

| 3 | adverse | 792 | 76% | 36 | economic | 141 | 14% |

| 4 | business | 775 | 74% | 37 | information | 140 | 13% |

| 5 | financial | 754 | 72% | 38 | U.S. | 138 | 13% |

| 6 | costs | 455 | 44% | 39 | data | 135 | 13% |

| 7 | adversely | 409 | 39% | 40 | services | 133 | 13% |

| 8 | aircraft | 381 | 37% | 41 | carriers | 131 | 13% |

| 9 | including | 369 | 35% | 42 | travel | 129 | 12% |

| 10 | airline | 362 | 35% | 43 | stock | 127 | 12% |

| 11 | significant | 314 | 30% | 44 | requirements | 126 | 12% |

| 12 | operating | 270 | 26% | 45 | time | 126 | 12% |

| 13 | future | 257 | 25% | 46 | flight | 116 | 11% |

| 14 | impact | 232 | 22% | 47 | laws | 115 | 11% |

| 15 | agreements | 226 | 22% | 48 | competitive | 113 | 11% |

| 16 | market | 224 | 21% | 49 | major | 112 | 11% |

| 17 | subject | 223 | 21% | 50 | number | 111 | 11% |

| 18 | conditions | 212 | 20% | 51 | foreign | 110 | 11% |

| 19 | industry | 212 | 20% | 52 | international | 102 | 10% |

| 20 | ability | 204 | 20% | 53 | required | 100 | 10% |

| 21 | systems | 194 | 19% | 54 | restrictions | 95 | 9% |

| 22 | regulations | 191 | 18% | 55 | public | 87 | 8% |

| 23 | service | 190 | 18% | 56 | currently | 80 | 8% |

| 24 | security | 183 | 18% | 57 | delays | 79 | 8% |

| 25 | control | 182 | 17% | 58 | access | 74 | 7% |

| 26 | increase | 181 | 17% | 59 | flights | 67 | 6% |

| 27 | addition | 176 | 17% | 60 | federal | 67 | 6% |

| 28 | airlines | 174 | 17% | 61 | period | 66 | 6% |

| 29 | changes | 172 | 17% | 62 | rates | 62 | 6% |

| 30 | price | 169 | 16% | 63 | management | 61 | 6% |

| 31 | air | 161 | 15% | 64 | bargaining | 44 | 4% |

| 32 | fuel | 161 | 15% | 65 | assets | 42 | 4% |

| 33 | Company | 157 | 15% |

| Nr. | Concept | Count | Relevance | Nr. | Concept | Count | Relevance |

|---|---|---|---|---|---|---|---|

| 1 | adverse | 1528 | 100% | 35 | airlines | 195 | 13% |

| 2 | operations | 1369 | 90% | 36 | fuel | 189 | 12% |

| 3 | business | 1049 | 69% | 37 | requirements | 183 | 12% |

| 4 | financial | 1035 | 68% | 38 | systems | 172 | 11% |

| 5 | including | 517 | 34% | 39 | economic | 167 | 11% |

| 6 | aircraft | 466 | 30% | 40 | U.S. | 162 | 11% |

| 7 | costs | 429 | 28% | 41 | cash | 158 | 10% |

| 8 | future | 395 | 26% | 42 | market | 154 | 10% |

| 9 | increase | 390 | 26% | 43 | information | 154 | 10% |

| 10 | impact | 382 | 25% | 44 | data | 152 | 10% |

| 11 | significant | 381 | 25% | 45 | carriers | 152 | 10% |

| 12 | airline | 358 | 23% | 46 | required | 149 | 10% |

| 13 | service | 347 | 23% | 47 | time | 145 | 9% |

| 14 | agreements | 338 | 22% | 48 | international | 143 | 9% |

| 15 | certain | 330 | 22% | 49 | competitive | 141 | 9% |

| 16 | COVID | 327 | 21% | 50 | public | 133 | 9% |

| 17 | changes | 312 | 20% | 51 | provide | 131 | 9% |

| 18 | travel | 307 | 20% | 52 | flight | 131 | 9% |

| 19 | additional | 298 | 20% | 53 | employees | 128 | 8% |

| 20 | ability | 295 | 19% | 54 | shares | 127 | 8% |

| 21 | air | 292 | 19% | 55 | government | 126 | 8% |

| 22 | demand | 282 | 18% | 56 | credit | 124 | 8% |

| 23 | Company | 274 | 18% | 57 | foreign | 122 | 8% |

| 24 | subject | 271 | 18% | 58 | federal | 120 | 8% |

| 25 | industry | 264 | 17% | 59 | measures | 110 | 7% |

| 26 | continue | 236 | 15% | 60 | labor | 109 | 7% |

| 27 | restrictions | 232 | 15% | 61 | maintenance | 106 | 7% |

| 28 | partners | 229 | 15% | 62 | fleet | 106 | 7% |

| 29 | stock | 222 | 15% | 63 | assets | 99 | 6% |

| 30 | security | 209 | 14% | 64 | rates | 86 | 6% |

| 31 | regulations | 206 | 13% | 65 | program | 79 | 5% |

| 32 | price | 206 | 13% | 66 | management | 78 | 5% |

| 33 | control | 204 | 13% | 67 | interest | 63 | 4% |

| 34 | conditions | 203 | 13% | 68 | DOT | 57 | 4% |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Penela, D.; Palma, M. Risk Factor Disclosures in the US Airline Industry Following the COVID-19 Pandemic. Risks 2023, 11, 34. https://doi.org/10.3390/risks11020034

Penela D, Palma M. Risk Factor Disclosures in the US Airline Industry Following the COVID-19 Pandemic. Risks. 2023; 11(2):34. https://doi.org/10.3390/risks11020034

Chicago/Turabian StylePenela, Daniela, and Miguel Palma. 2023. "Risk Factor Disclosures in the US Airline Industry Following the COVID-19 Pandemic" Risks 11, no. 2: 34. https://doi.org/10.3390/risks11020034

APA StylePenela, D., & Palma, M. (2023). Risk Factor Disclosures in the US Airline Industry Following the COVID-19 Pandemic. Risks, 11(2), 34. https://doi.org/10.3390/risks11020034