1. Introduction

The flare-up of inflation, which has recently hit the international economy, and in particular the European one, has made it necessary for non-life insurance companies to check on the adequacy of methods and models currently in use for reserve valuations and the associated risks. This paper considers possible ways to incorporate the effects of unexpectedly high economic inflation in the estimates of the non-life claim reserves and the corresponding solvency capital requirements as imposed by Solvency II, the reserve SCR.

As is well-known, non-life insurance claims are exposed to both

general (or

economic) inflation, andto

superimposed inflation. The first component is related to the trend of the overall level of prices, and is measured by the percentage changes of some consumer price index (CPI). The superimposed inflation is an additional component determined by the changes in costs of goods and services that have a specific impact on the line of business considered. A popular method to derive the historical

total claims inflation (general plus superimposed) by claims data is the

separation method developed by

Taylor (

1977). Further methods were proposed thereafter to detect claims inflation and, more generally, calendar year effects in claims data. A relevant advance came from the age–period–cohort models defined in

Kuang et al. (

2008) and their subsequent developments. In the present paper, however, we only consider general inflation which, of course, is estimated directly on economic data. We think that referring to economic inflation is a useful exercise to tackle the more complex (and somewhat elusive) problem of total claims inflation, since the two are necessarily correlated. For an empirical study of superimposed inflation in some lines of business, see

Bohnert et al. (

2016).

In the recent historical period, characterized by low and stable economic inflation rates, the problem of incorporating inflation in the estimates of future claims losses has typically been approached with so-called

implicit, or

unmodeled,

inflation methods, which are assumed to automatically project past inflation into the estimate of future claim payments. In particular, the chain-ladder (CL), probably the most popular among the claims reserving methods, is usually applied to triangle of past claim payments expressed at historical costs, i.e., to data which has not been adjusted for past inflation. This is motivated by the generally accepted opinion that the CL applied to unadjusted data projects a weighted average of past claims inflation into the future. As discussed and illustrated by

Brydon and Verral (

2009), this may not be true. However, this approach with unmodeled inflation can be considered acceptable if future inflation is expected to be roughly the same as in the past (see, e.g.,

Taylor 2000). In this situation, the uncertainty of the estimate, and in particular the reserve SCR, is measured using stochastic CL models applied to unadjusted data, which produce estimates of

technical risk (claims development uncertainty, enriched, perhaps implicitly, with an inflation risk component).

Motivated by the “structural break” evident in the time-series of consumer price indices around mid-2021, in this paper, we will analyze possible alternative approaches to the use of stochastic CL models, which can be considered suitable for incorporating in the claims reserve estimates, and in the corresponding SCR, the effects of an explicit general inflation, which is not a reproduction of historical experience, but is consistent with current expectations on trend and variability. These approaches necessarily start from a “non-classical” application of the CL as a projection method, which consists of using as input data a triangle of claim payments expressed at current costs (i.e., in current money value), which is obtained escalating the payments observed in past years by the corresponding realized inflation. In order to incorporate the inflation effects into the predicted paid losses, the use of an appropriate stochastic model for economic inflation is therefore required. So, these methods with explicit inflation can be referred to as modeled inflation methods.

Two possible approaches to the problem will be considered. The first one, referred to as actuarial approach, simply considers a probability distribution suitable to describe the stochastic dynamics of the CPI, without including in the reserve estimates an inflation risk premium, as would be required in an approach genuinely market-consistent. A market approach will then be proposed, where risk premia are properly taken into account using a stochastic market model for nominal and real interest rates.

In both approaches, it will be assumed that a specific stochastic claims reserving model based on the CL has been adopted, to be applied preferably according to the one-year uncertainty point of view adopted in Solvency II (alternative wordings are Clams Development Result: CDR, Year-End Expectation: YEE, and re-reserving). Among the most popular stochastic CL models, one can consider Mack’s Distribution-Free Chain Ladder (DFCL) model or its variants (e.g., the Merz and Wüthrich model) and the Over-dispersed Poisson (ODP) model. In any case, our aim is to extend the model chosen, in its bootstrap-simulated version, to incorporate explicitly a stochastic model for economic inflation.

In this paper, we use a simplified inflation model, since we assume that the future expected inflation rates are deterministic. As a consequence of this assumption, in the reserve SCR estimate (under one-year view), the risk of the inflation rate is not considered in full, since the component due to the uncertainty on its future expectation is missing. So, a natural extension of this paper is to consider a model in which the expected inflation rate is also stochastic. A three-factor Gaussian model with these characteristics has recently been proposed (

Moriconi 2023). For an approach that directly models the claims inflation rate using a mean-reverting time series model of Vasicek type (see, e.g.,

D’Arcy and Au 2008;

Bohnert et al. 2016).

The present paper is organized as follows. In

Section 2, we briefly introduce notations and basic definitions. In

Section 3, we provide a formal representation of the features common to traditional stochastic CL methods with unmodeled inflation. In

Section 4, the actuarial approach to claims reserving with modeled inflation is presented and a simple stochastic model for the general price index model is proposed. The market approach is presented in

Section 5, where we preliminarily provide the fundamental results of a two-factor stochastic model for nominal and real interest rates. In

Section 6, we provide an example of application of the different approaches to market data as of 30 December 2022. The estimate of the inflation component of the two-factor model is obtained from time series data and observed prices of inflation-linked swaps, and the nominal interest rate component, specified as the Vasicek-Hull and White model, is estimated and calibrated to ECB and EIOPA data. A comparison of numerical results obtained from different approaches using the estimated model is provided. Details of the two-factor model are provided, and some methodological issues are discussed in

Appendix A,

Appendix B and

Appendix C.

2. Notation and Basic Definitions

We assume that the reader is familiar with the CL technique and with at least one of the stochastic CL models found in the literature, applied through bootstrap simulation. Thus, we simply introduce the basic notations and limit the details of the actuarial models in a minimal form. We are at time I (which we assume to be a year-end). The claim payments are organized by accident year and development year , and are arranged in a matrix of cells . Then, claim payments have been observed for years, and we assume that incurred claims are settled in years. Calendar years (the matrix “diagonals”) are indexed by , hence the cells with provide the triangle of observed payments (“past triangle”, “upper triangle”) and the cells with provide the “future triangle”, or “lower triangle”, . We denote by the incremental payments in cell and, in general, our aim is to derive the joint probability distribution of , i.e., the payments in the future calendar years , using the data .

For any calendar year ℓ and claim payment with , it is convenient to define the CL operator , which provides the estimate of obtained by the CL algorithm applied to the claim payments observed up to year ℓ. The CL operator is additive; that is, for any with , .

We also denote by

the total incremental payments in the diagonal

ℓ:

The triangle

is a set of observed payments “at historical costs”, i.e., claims payment

is expressed in the money-value of calendar year

. If we know the past inflation, that is, the CPI level

observed on calendar years

, we can adjust the data for past inflation by the rescaling:

where the superscript

indicates that the claim payment is “at current costs”, i.e., expressed in the money-value of the current year

I. When it is necessary to distinguish, we will use the superscript

hc to indicate monetary amounts at historical costs.

4. Modeled Inflation with the Actuarial Approach

As we said, claims reserving methods with modeled inflation are applied to inflation-adjusted data triangles and, of course, require the specification of a model for future inflation. We first consider an approach that we will call “actuarial”, since it is a natural extension of the traditional approach described in the previous section. An approach of this type has been applied in a field study by

Cavastracci et al. (

2006).

4.1. The Actuarial Approach

In the actuarial approach with modeled general inflation, a stochastic model for the general price level is chosen, which is estimated on an observed time-series of the CPI, which best explains economic inflation. Moreover, in addition to the basic assumptions of the specific stochastic claims reserving model adopted, the following assumptions are made.

Economic inflation uncertainty is independent of technical uncertainty.

There is no interest rate risk, i.e., future interest rates are deterministic.

The future expected inflation rates are deterministic.

Risk premia are not taken into account in the valuation; in particular, an inflation risk premium is not included.

A further assumption, not necessary but sensible in the current situation, is that the expected values of future inflation rates are exogenously given (possibly taking into account the current market information) and not derived by estimates on historical data.

4.1.1. Reserve Estimate

Under the actuarial approach, the claims reserve estimate, i.e., the BE with explicit inflation, is given by:

where

, for

and

, is the

inflation repricing factor defined as:

Obviously,

denotes a conditional expectation given

, where

represents the relevant information available at time

t. Throughout this paper, we use this simplified notation for expectations, since the meaning of

will be clear from the context.

This expression for the reserve highlights the important role played by inflation expectations in claims reserving with explicit inflation. Given the regulatory value of the reserve estimates, these expectations must reduce the degree of subjectivity as much as possible to achieve a sufficient level of consensus. This can be performed in several nonmutually exclusive ways: by specifying a stochastic inflation model that can be estimated on observational data, by using publicly stated expectations from economic research centers or public institutions and, normally to a lesser extent, by observing current prices of inflation-linked products traded on the market. A simple inflation model suitable for our purposes will be presented in

Section 4.2. As we shall see, by including this model in an appropriate two-factor market model, it will be possible to derive inflation expectations from the observation of market prices. This will provide the expectations in (

4) with the level of objectivity provided by the market consistency.

If we adjust for past inflation but not for future inflation, that is, if we do not apply the inflation repricing factors

, we obtain the reserve estimate:

It is usually expected that, with positive historical inflation, , but as we shall see, this is not necessarily true.

4.1.2. Predictive Distribution under Long-Term View

The predictive distribution under the long-term view is obtained as:

where the future diagonal sums

are bootstrap-simulated as in the implicit inflation case, and the future values of the price index are simulated according to the stochastic model chosen for the

process.

Under unbiasedness of the bootstrap simulation, we obtain:

since

.

4.1.3. Predictive Distribution under One-Year View

The predictive distribution under the one-year view is given by:

where:

Here, the CL operator is applied to the original triangle augmented with the next simulated diagonal

, where the claim payments are still at time

I costs, i.e., are

not inflated. The stochastic inflation factor

is applied instead. The inflation repricing factors

are expectation taken at time

. However, under the assumption of deterministic expected inflation, as with deterministic discount factors, they are equal to the current forward factors, that is:

So, expression (

5) is written as:

Also in this case, since

, the unbiasedness of the bootstrap simulation provides:

The empirical distributions DUO and YEO obtained with the actuarial approach are used for reserve risk and capital requirement calculations, exactly as in the case with unmodeled inflation illustrated in

Section 3.

4.2. A Simple Model for the Price Index

For the stochastic inflation model, we choose the diffusion dynamics described by the

stochastic differential equation (SDE):

where

is a standard Brownian motion, or Wiener process, and the functions

and

are the

drift and the

diffusion coefficient, respectively, of

process. For these coefficients, we choose the simple specification:

where

is the

volatility parameter (a positive constant) and the

function is the

expected instantaneous inflation rate at time

t. In fact, since

, we have:

As stated in the basic assumptions, we take

as a deterministic function. Hence,

is a geometric Brownian motion with time dependent drift and the corresponding SDE for

:

defines a model with deterministic expected inflation.

For

, let us consider the logarithm of the price ratio

:

Using Ito’s lemma, it is easily shown that the SDE (

7) implies that

is normal, with mean:

and variance:

Hence, at time

t, the ratio

is a lognormal random variable which can be simulated as:

with

standard normal. In

Section 4.1.1, the

inflation repricing factor on the time interval

as been defined as:

Since

, by the normality of

we have:

hence:

Often, inflation expectations at time

t for future years

, are communicated through the forward annual expected rates:

For the moment, we leave open the question of how to specify the function

. Typically, a parametric form is assumed and, in stable market conditions, the parameters are estimated on a time-series of observed prices. In the current market situation, it is not appropriate to make the estimate of

completely dependent on historical experience, and it is necessary to use some exogenous information. For example, at time

I the

for

, could be provided by regulatory institutions such as EIOPA or ECB as survey-based forecasting or “planned” inflation rates. Or, the repricing factors

could be directly derived from the market by observing current prices of inflation-linked securities. Expression (

8) provides, for

:

Therefore, if the

or the

are exogenously given (suggested by institutions or derived by the market), only the estimate of

is required to implement the model. In the example of application presented in

Section 6, we will follow the second path, deriving the

factors by observed market prices. To do this correctly, however, we need the market model, which will be presented in the next section.

Remark 2. As we have already pointed out, the choice of a deterministic function is for simplicity sake, but involves, in principle, an underestimate of the inflation uncertainty. To circumvent this issue a more complex model should be used where the expected inflation is also stochastic. This is equivalent in this framework to also include a SDE for . An appropriate version of the trivariate model proposed by Cox et al. (1985) could be used. A similar model was applied to the Italian bond market (Moriconi 1995). Recently, a three-factor Gaussian model suitable for claims reserving applications has been proposed in Moriconi (2023). 4.3. Possible Weaknesses of the Actuarial Approach

A possible criticism to the actuarial approach concerns the assumption of absence of inflation risk premium. The claims reserve estimate is obtained as the expected value (from a distribution that contains technical uncertainty and inflation uncertainty) discounted at nominal rates. Therefore, it actually is a BE in the technical sense of Solvency II, as it does not include a risk premium either for technical or for inflation uncertainty. The absence of the technical risk premium in non-life best estimates is acknowledged in Solvency II, given that technical risk is unhedgeable. In this framework, this shortcoming is taken into account when computing the “technical provisions” by adding a specific “risk margin” to the BE, derived by the corresponding SCR figure. However, given the existence of a market of inflation-linked securities, general inflation uncertainty is to be considered hedgeable under suitable conditions (the most obvious is that these securities are linked to the same inflation index used for reserve estimates). Therefore, the technical provisions with explicit inflation should include a specific market risk premium. It can be noted, however, that the same criticism could be made to the approach with implicit inflation, hitherto commonly used without this type of concerns.

Remark 3. A related issue which we do not consider here, but which may be of some interest, is that, in principle, a non-life insurer could also consider the possibility of actually implementing a hedging strategy by holding on the asset side an appropriate portfolio of inflation-indexed securities.

The assumption of deterministic interest rates is an obvious simplification of the reality which, however, has the cost of rule out a source of uncertainty in the derivation of the one-year loss distribution. This assumption can be accepted as an approximation, because we take the expected inflation rates also as deterministic. Indeed, deterministic interest rates would be inconsistent with a model for the price index where is stochastic (this is a consequence of the so-called Fisher effect, which will be illustrated in the next section).

In conclusion, the actuarial approach provides a simplified solution to the problem of incorporating explicit inflation in the claims reserve estimate and, in particular, in the estimation of the reserve SCR under the one-year view. Whether the resulting approximations are acceptable from a practical point of view it can only be correctly appreciated by making a comparison with the results of a more complex market model. In

Section 6, we will provide a numerical example that is useful to illustrate this issue.

Remark 4. Another possible weakness of the actuarial approach could concern the time-series estimate of inflation volatility. This “backward looking” estimate could be considered unreliable, given the structural break occurred recently on market data. If real (i.e., inflation-linked) derivatives were quoted on an efficient bond market, one could derive an estimate of implied volatility for the inflation by calibrating an appropriate stochastic model for nominal and real interest rates on a cross section of prices of these derivatives. We will not develop this topic further here.

5. The Market Approach

In what we will call the “market approach”, in addition to the basic assumptions of the specific claims reserving model adopted, the usual assumptions hold of perfection and absence of risk-free arbitrage opportunities for the nominal and real bond market, which is populated by risk averse agents. Also in this case, moreover, the assumption of deterministic expected inflation is made.

It is worth noting that models of this type are usually developed with the aim of deriving no-arbitrage prices of complex securities, as inflation-linked derivatives. For our applications, it is sufficient to derive the expression of the nominal and real discount factors, and we will not need to push the use of our pricing model further.

5.1. The Fundamental Results of the Market Model

In

Appendix A, a simple bivariate stochastic model for nominal and real interest rates is presented. We summarize here the two main results obtained, which will be used in the calculation schemes for the claims reserve and the reserve risk with explicit inflation. The first result is a kind of

stochastic Fisher effect, expressed by the relation:

where:

is the market nominal risk-free discount factor on the time period ;

is the market real risk-free discount factor on ;

is the risk-neutralinflation discount factor on .

One point worth noting is that the discount factors in expression (

13) are provided by the model as a function of a risk factor whose stochastic dynamics is specified. This allows their future values to be simulated.

The second basic result concerns the form of inflation discount factor, which is given by:

where

is defined in (

9) and has the form in (

10).

We add some details and comments below.

Nominal Discount Factor

As we said in

Section 3.1 (and as it is required by the no-arbitrage assumption), the nominal discount factor

is the price (in euros) observed at time

t on the market of a ZCB which pays with certainty at maturity

T a nominal unit (1 euro). It is assumed here that the form of a parametric function for

is determined in a market model. For simplicity, we choose a univariate model, described by the SDE:

where

is the instantaneous nominal interest rate. Once the form of the functions

and

is specified, the probability distribution of

, for

, remains identified. These

natural probabilities are also referred to as

real-world probability measures. In order to derive the arbitrage-free price of securities depending on

, a third function,

, the

market price of interest rate risk, must also be specified. Using the

hedging argument, the fundamental tool for no-arbitrage pricing in perfect markets, a new probability measure

is obtained, defined by the functions

and

. This probability measure, referred to as the

(interest rate) risk-neutral measure, provides a probability distribution, which is properly adjusted to take into account the interest rate risk premium prevailing at time

t in the market. This distribution has the fundamental property that any security price can be derived as a discounted expectation taken with respect to

. In particular, through the functions

and

, the discount factor

can be expressed as an explicit (deterministic) function of

, and the stochastic evolution of future discount factors is driven by the

natural dynamics (

14). For the moment, we can proceed by deferring the specification of the functions

to the application example presented in

Section 6, where we will choose a Vasicek model for

(see

Section 6.3.1).

Real Discount Factor

The real discount factor

is the price observed at time

t on the market of a ZCB which pays with certainty at maturity

T a real unit; that is, a unit of the basket of goods and services chosen to define the CPI

(the “reference basket”). The price

is also expressed in real units. The form of the

function depends on the form of

by relation (

13) then, ultimately,

also depends on

.

Inflation Discount Factor

The risk-neutral inflation discount factor

is the reciprocal of the

risk-neutral inflation repricing factor, which is defined as:

where the expectation is taken with respect to the risk-neutral probability measure

. This is the expectation of the price ratio

of the reference basket, calculated according to the

(price index) risk-neutral distribution, i.e., the probability distribution, which is adjusted to take into account the

inflation risk premium prevailing at time

t in the market. The function

also remains defined within a specified stochastic model for the price

. For the

dynamics, we choose the specification (

7) already used for the actuarial approach, and we assume that the

process and the

process are stochastically independent. However, in order to derive the risk-neutral measure

, we must also specify the form of the function

, the

market price of inflation risk. On the basis of considerations of a technical nature, also supported by arguments of general economic equilibrium, the form is chosen:

Since

and

, one has

. Therefore, the risk-neutral dynamics of

is expressed by the SDE:

where

. The SDE (

17) implies:

hence

is the expected instantaneous inflation rate in the risk-neutral world. As in

Section 4.2, we can derive the risk-neutral version of expression (

10), which is given by:

Correspondingly, the risk-neutral version of the forward annual expected rates

defined in (

11) is given by:

As will be seen, Expression (

16) of the inflation risk premium has important effects on the numerical valuations. However, before that, it is fundamental from a methodological point of view. In fact, given that

can be estimated on market data, it is possible to derive natural expectations on future inflation from the risk-neutral expectations observed on the market, as shown by (

18) and (

19). This is a rather unusual circumstance in financial modeling, given that additional assumptions, often ad hoc or based on judgment, are usually needed to derive natural expectations prevailing in the market. An analysis of natural inflation expectations and inflation risk premia leveraging inflation-linked securities and survey-based forecasting has recently been proposed in

Cecchetti et al. (

2022), where a multivariate stochastic model is used.

Remark 5. It is important to emphasize that relation (13) is obtained under the assumption that the price process and the process of the nominal rate are independent. This independence assumption is also crucial to justify the form (16) for the inflation risk premium. As shown in Cox et al. (1985), in a general equilibrium model (with the appropriate assumptions), the market risk premium for a given risk factor is equal to the covariance of changes in the risk factor with percentage changes in the investor optimally allocated wealth (the value of the so-called “market portfolio”). See Moriconi (2023) for an extensive use of this result. Expression (16) derives by this general equilibrium property if the assumption of independence between real and nominal quantities is made. This independence assumption was also referred to as separability property by Richard (1978), since it allows, more generally, to use the inflation component and the interest rate component of the two-factor model separately. See Appendix A.3 for more details. With the choice (

17), relation (

13) can be expressed in terms of returns over finite time periods

:

or also in terms of instantaneous returns (the limits as

of the corresponding finite periods returns):

where

is the

instantaneous real interest rate. These relations express the Fisher effect, instead of in multiplicative form, in the classic additive form: the nominal interest rate is the sum of the real interest rate and the expected rate of inflation.

Remark 6. The inflation repricing factor given by (18), and the corresponding inflation discount factor , are deterministic since, for , is known at time t. This is a consequence of the assumption of deterministic expected inflation rate. In a model where is stochastic, and are unpredictable at time t. 5.2. Claims Reserving with the Market Approach

Using the results of the two-factor model, we can formulate a fully market-consistent version of the actuarial approach to stochastic claims reserving, which we will call “market approach”. As we shall see, the main new features are (i) the different way of applying expected inflation in the calculation of reserves, and (ii) the simulation of future discount factors instead of the use of forward discount factors in the construction of the YEO distribution.

5.2.1. Reserve Estimate

Under the market approach, the claims reserve estimate is given by:

Since

, comparing with (

3), the inequality holds:

So, the reserve estimate with the market approach is lower than the estimate obtained with the actuarial approach due to the inclusion of the inflation risk premia. However, since for typical values of

, the factors

are only slightly lower than 1, the difference between the two reserve estimates is usually very small.

Equivalently to (

20), by the Fisher relation, one can discount the CL projections directly with the real interest rates:

This expression directly shows that in a fully market-consistent valuation subjective expectations of inflation are irrelevant. Technically, the reserve in (

21) can be interpreted as the cost of purchasing a portfolio containing real ZCBs, which are priced

, in the quantity

.

5.2.2. Predictive Distribution under Long-Term View

The predictive distribution under the long-term view is obtained as:

Since, compared with the actuarial approach, the stochastic factors

are here replaced by the deterministic factors

, we expect a lower variance of this simulated distribution.

Under unbiasedness of the bootstrap simulation, we obtain:

5.2.3. Predictive Distribution under One-Year View

The predictive distribution under the short-term view is given by as:

where:

The simulation of the future nominal discount factors is carried out using the interest rate component of the two-factor model. As illustrated in

Section 5.1, this model allows the discount factor

to be expressed as a known function

of the instantaneous interest rate

. Once the functions

and

have been specified, the probability distribution of future values of

is known and

can be simulated as

. As already mentioned, in the application example, we will choose

and

in the Vasicek form. Furthermore, in order to have a perfect fitting of

to the EIOPA term structure, we shall apply Vasicek’s model in the extended form provided by Hull and White.

Remark 7. As , by the Fisher relation, the residual reserves (23) can also be expressed using the real discount factors: It should be noted that for the YEO distribution, even though the simulation procedure is unbiased, the inequality holds:

In fact, one has, for

:

but, under interest rate uncertainty, the expectation of future interest rates does not coincide with current forward rates, hence:

However, in this kind of application, the difference between the present value of the sample mean

and the reserve

may be immaterial, and is often absorbed in the Monte Carlo error.

5.3. On the Use of a Model with Stochastic Expected Inflation

To conclude the theoretical framework, let us add some general considerations about the eventual use of a model with stochastic expected inflation. A first observation is that in a framework with enhanced economic meaning, the actuarial approach seems to have no more place. Because of the Fisher relation, in fact, keeping it would be equivalent to accepting an approximation in which nominal interest rates are deterministic while real interest rates are stochastic, which seems hard to justify.

Turning to consider the market approach, the expression (

21) for the reserve would still apply and expressions (

22) and (

23) would be written as, respectively:

and:

These expressions are formally identical to the corresponding versions with deterministic expected inflation, the only difference being that the real discount factor is now the product of two factors that are both stochastic. If even in the model with stochastic expected inflation the discount factors are perfectly fitted to market data, the numerical value of the reserve

and that of the elements of the DUO distribution should remain the same. For the residual reserves in the YEO distribution, however, we should expect some differences, due to the different estimates of the parameters in the two models. In particular, it should be the case that the variability of

is greater than the variability of

with

deterministic (recall that we do not directly observe

, but the factors

and

separately). Ultimately, then, in a model with stochastic expected inflation nothing should change for the DUOs (both in the mean and the CV), while for the YEOs, there should be an additional increase in the CV, and then in the SCR.

6. An Example of Application

We provide a numerical example of application of both the actuarial and the market approach considering a triangle of incremental payments in the

Motor Third Party Liability (MTPL) line of a large Italian insurance company. The triangle is observed at the end of 2022 (time

I), and includes 22 accident years, from 2001 to 2022. For confidentiality purposes, the figures are scaled with a constant in order to provide a CL reserve equal to 100,000 (say, Euros)

1.

The stochastic CL model chosen for our applications is the ODP model introduced by

Renshaw and Verral (

1998), in the boostrapped version proposed by

England and Verral (

2002). This ODP Bootstrap model was applied according to the one-year view. In the ODP simulations, the process error component was obtained by sampling from a gamma distribution.

6.1. Results with the Unmodeled Inflation Approach

Before applying the modeled inflation approaches, we provide the results of a classical estimation with implicit inflation using the deterministic CL to derive the reserve estimate and the ODP Bootstrap model to produce the simulated YEO distribution. For comparison, the simulated DUO distribution is also produced.

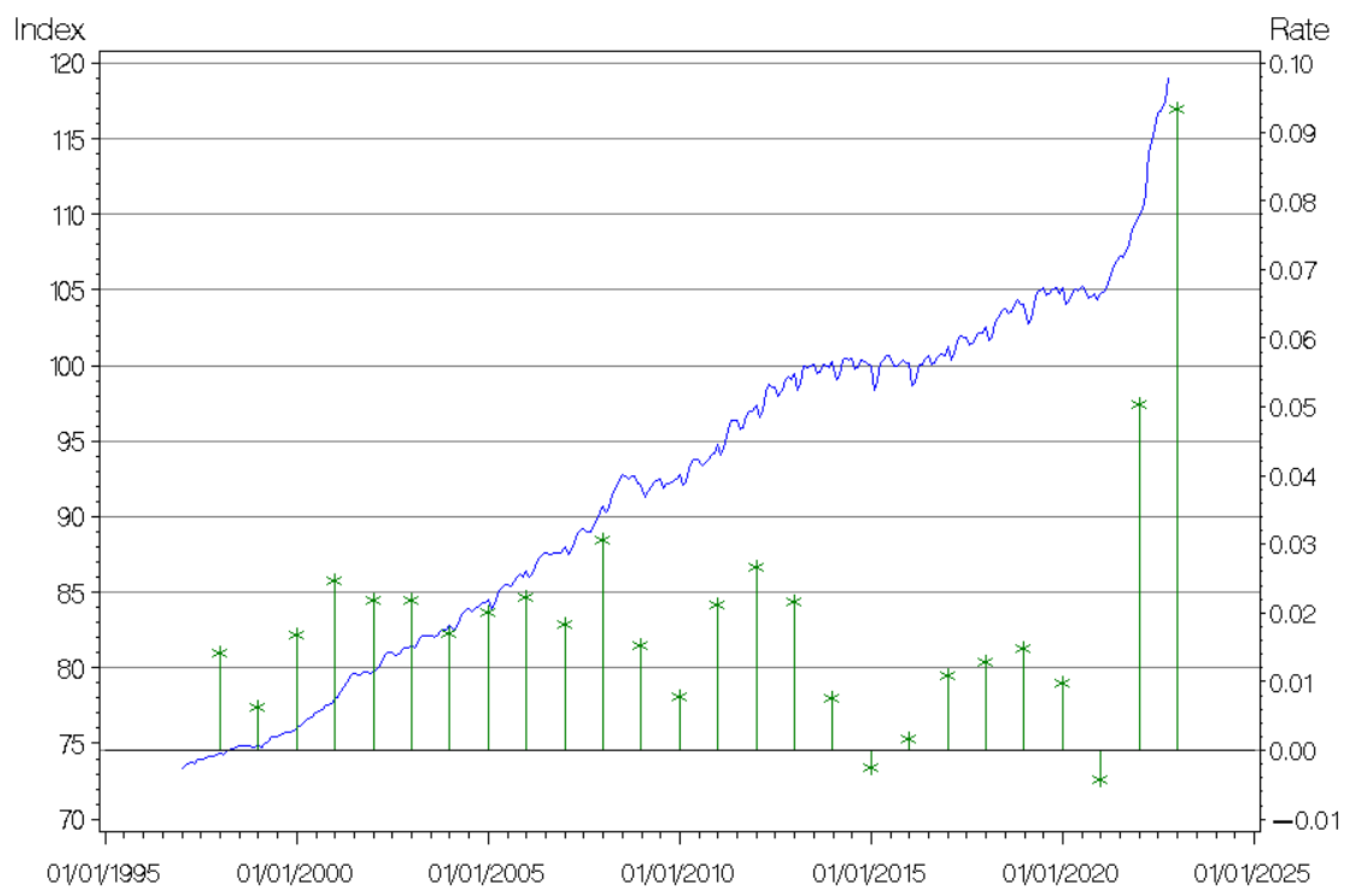

For discounting, we used the nominal risk-free discount factors

provided by EIOPA at

(including

volatility adjustment, VA). The corresponding log-returns are reported in

Figure 1 (blue line) for maturities

years (we need to discount future cash-flows for

years).

Applying the deterministic CL with unmodeled inflation, we obtain the following estimates:

| - Undiscounted reserve with implicit inflation | 100,000 |

| - Discounted reserve with implicit inflation (BE): | 91,091 |

The ODP Bootstrap with 100,000 simulations provides:

| - DUO sample mean: | 91,300 |

| - DUO Std | 4431 |

| - DUO CV | 4.85% |

| - YEO sample mean: | 94,227 |

| - YEO Std | 3658 |

| - YEO CV | 3.88% |

| - percentile of YEO | 104,301 |

| - Solvency Capital Requirement | 10,075 |

| - Present value of YEO sample mean: | 91,158 |

As can be seen, discounting produces a BE that is about

lower than the undiscounted reserve. Comparing the mean of the DUO and the discounted mean of the YEO with the BE

provided by the CL, it can be seen that the bootstrap simulation procedure is roughly unbiased. The coefficient of variation (CV) of the PDF is about

, and the reserve SCR is

of the BE. For comparative purposes, many of these figures are also reported in the second column of

Table 1.

By partial executions of the simulation procedure, one finds that the CV with only the estimation error is

and the CV with only the process error is

. Obviously, the overall CV benefits from the diversification effect due to the independence. This CV decomposition is illustrated in the first section of

Table 2.

It is worth noting that the YEO distribution (the “PDF”) has an excess-kurtosis (with respect to the normal distribution) (we find and for the estimation error and the process error stand-alone component, respectively). If we consider the moment-fitted lognormal distribution (i.e., the lognormal distribution with same mean and variance of the YEO), we obtain . Thus, the probability distribution describing the claims development uncertainty provided by the ODP Bootstrap is more fat-tailed than the fitted lognormal. Correspondingly, the “SCR ratio” SCR/Std is for the PDF and for the fitted lognormal.

In order to apply the methods with modeled inflation, we have to complete the specification of the bivariate model and proceed to the estimation of the relevant parameters. As already noted, the separability property of the model allows us to consider the inflation component separately, which is sufficient for a market-consistent application of the actuarial approach, and the interest rate component, which is instead required for a full market approach, that includes the interest rate risk. We then proceed considering first the application of the actuarial approach.

6.2. Application of the Actuarial Approach

6.2.1. Inflation Model Estimate

The inflation component of the two-factor model allows us to derive from market data not only an estimate of CPI volatility, but also an estimate of the prevailing expectations on future inflation.

Volatility Estimate

As the reference CPI

, we use the Harmonized Index of Consumer Prices (HICP), which is compiled by Eurostat and the euro-area national statistical institutes and is published at the end of each month. The HICP monthly time-series, as well as the annual inflation rates computed at each year-end, are reported in

Figure 2.

We use the monthly time-series

, where

is the set of month-end dates in [January 2005, December 2022]. The corresponding time-series of monthly log-returns (

):

is derived and an estimate of

is obtained computing the sample variance of this time-series. Taking the square root, the following volatility estimate, on annual basis, is obtained:

The estimated annual drift of the price process is

. However, we do not take this historical drift as the expectation of future inflation.

Expected Inflation by ZCIIS

We derive market expectations of future inflation by the

Zero-Coupon Inflation-Indexed Swaps (ZCIIS) observed at the valuation date. On each trading day

t, the ZCIIS rate

(the

swap rate) is quoted on the market for time-to-maturity

years. By simple, model independent, arbitrage arguments (see

Appendix C), the relation is found to hold:

Hence,

provides, by relation (

13), the inflation discount factor

prevailing in the market at time

t for time-to-maturity

.

The inflation log-returns

observed at the valuation date are represented in

Figure 1 by a continuous green line. As a usual market practice, rates for the missing maturities were obtained by linear interpolation of quoted swap rates. In the figure, the curve of real log-returns obtained by the Fisher relation is also reported (red line). For further illustration, we also calculated, according (

19), the risk-neutral market expectations

of the future annual inflation rates. These expected inflation rates for

up to 25 years are represented by green dots joined by a dotted line in

Figure 1 (the “jumps” between years 15 and 16 and years 20 and 21 in the

sequence are due to the linear interpolation of the quoted swap rates).

For our purposes, two points are particularly relevant.

As shown in

Section 5.1, Expression (

15), the inflation repricing factors observed on the market at time

t provides the risk-neutral expectation of the corresponding inflation factors. That is:

The corresponding

factors will be directly used when implementing expressions (

20), (

22) and (

23) in the market approach.

- 2.

Since the market price of inflation risk is known in our model, the natural market expectations are immediately derived, by (

18), as:

which also gives

. The corresponding

factors are used in expressions (

3) and (

6) in the actuarial approach. As concerning the simulation of future levels of the price index, required to derive the DUO and YEO distributions in the actuarial approach and the YEO distribution in the market approach, these can be obtained by the first expression in (

12).

Innovation in the Inflation Process

Since we estimated

, the one year expected inflation returns

are practically equal to (about 3 basis points higher than) their risk-neutral counterparts reported in

Figure 1. Comparing these

values with the drift coefficient

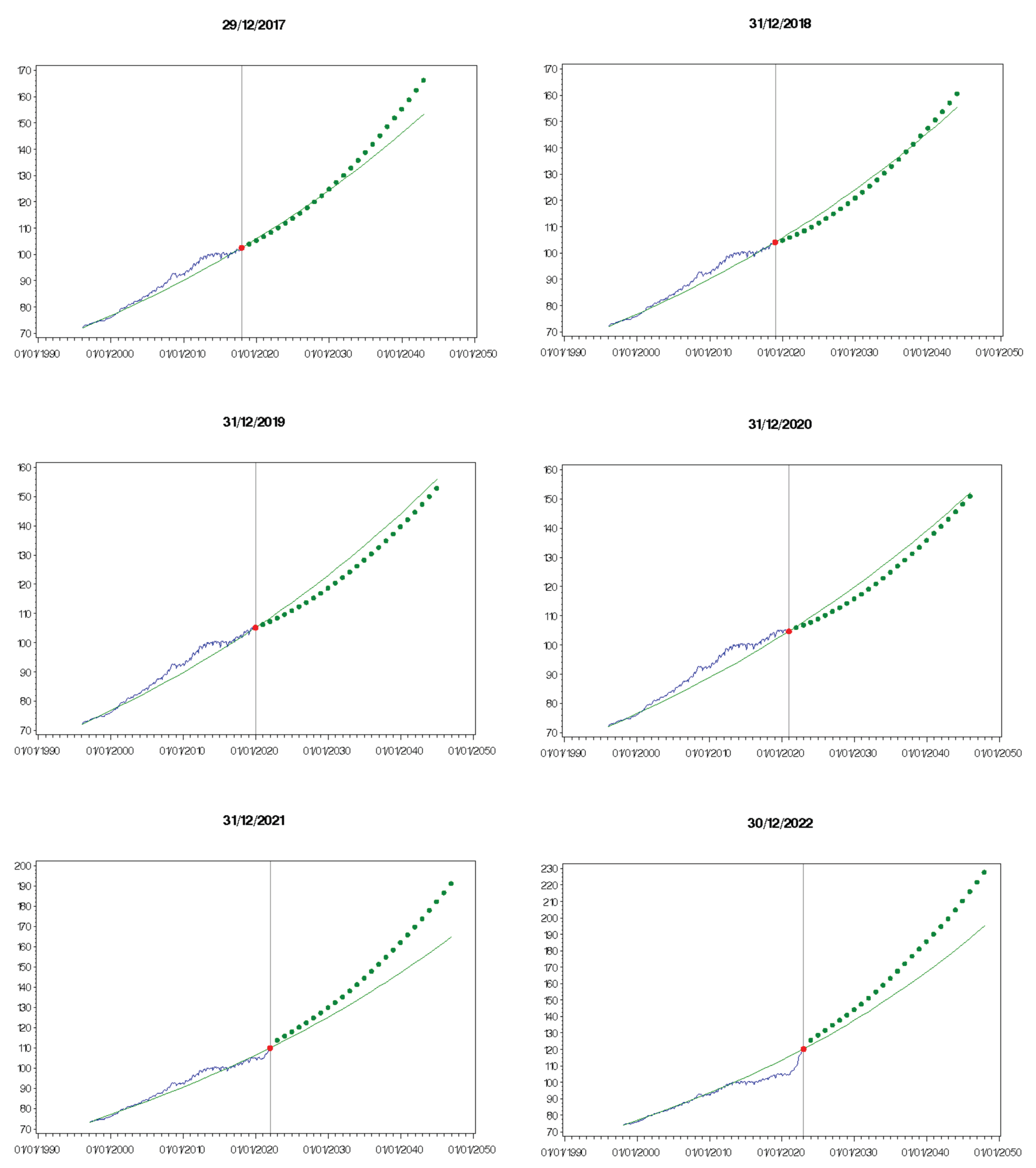

estimated on the observed HICP time-series evolution, one finds that at the valuation date the expectations of future inflation rates are consistently greater than those observed in the past. This “innovation effect” in the inflation process can be illustrated as in the last graph in

Figure 3. In this graph, we directly provide the evolution of the HICP observed up to 30 December 2022 (blue line) and the expected HICP (green dots) derived by the ZCIIS quoted on the same date. The continuous green line represents the HICP evolution according to the lognormal model fitted to the observed prices (which, in this case, provided the previous estimates

and

). In

Figure 3, this exercise is repeated by taking as the valuation date

t the end of the years 2017–2021. At each date

t, a simple lognormal model (with constant drift coefficient

and volatility coefficient

) was fitted to the monthly time-series of HICP observed on the previous years. The

estimate was used to draw the corresponding exponential green line through the current HICP value (red dot), and the green dots represent the natural expectations at the valuation date of the HICP levels over the next 25 years. As explained, these HICP expectations are derived by the risk-neutral expectations provided by the ZCIIS observed at time

t, adjusted using the estimate

.

The graphs show a strong positive innovation effect (expected inflation higher than historical inflation, especially in the near future) in years 2021 and 2022. This indicates that modeled inflation approaches are more appropriate for the reserve estimate in these cases. One could also argue that methods with implicit inflation were acceptable in the previous four years.

In a numerical experiment on artificial triangles aimed to test the ability of implicit inflation CL to correctly project forward past inflation,

Brydon and Verral (

2009) detected important distortions in the projections when an inflationary shock is applied to the data triangle in the latest calendar years. In particular, they observe that (p. 296) “… if there is a large change in the calendar year effect for the latest calendar year, the 1-year forecasts implied by the CL method [with implicit inflation] should be treated with caution”. It should be argued that this kind of problem also affects triangles of real data observed in 2021 and in 2022 especially, given that, as shown in

Figure 2, the inflation rates observed in those years are significantly higher than in previous years.

Remark 8. Inflation risk strongly depends on the line of business considered; therefore, a general consumer price index like HICP cannot fully describe the claims inflation specific to the MTPL line. Some components of the index may be overweighted, while an important component of superimposed inflation may be not represented. For this reason, even the assumption, used in the market approach, that inflation risk is hedgeable may be accepted only as an approximation (partial hedging). However, we think that the results produced in this example may be of some interest, as they capture important aspects of the innovation effect and could be used as a reference point for further investigation.

6.2.2. Numerical Results of the Actuarial Approach

Using the previous estimates, we performed our claims reserving exercise with modeled inflation according to the actuarial approach. The chain-ladder based deterministic computations provided:

| - Undiscounted reserve with triangle at current costs | 100,087 |

| - Discounted reserve with triangle at current costs: | 91,391 |

| - Undiscounted reserve with modeled inflation: | 109,554 |

| - Discounted reserve with modeled inflation (BE): | 99,493 |

From these deterministic calculations, we see that, rather unusually, the inequality

considered in

Section 4.1.1 is not fulfilled in this case, since the undiscounted (discounted) reserve with inflation adjusted triangle is greater, albeit very slightly, than the undiscounted (discounted) reserve with the unadjusted triangle. Evidently, in this case, the reduction in development factors is more than offset by the increase in cumulative payments up to the last diagonal, probably due to the fact that, as illustrated in

Figure 2, the rate of inflation over the past year or two (over 9% in 2022 and

in 2021) is much higher than in all previous years. However, although the effect of rescaling the triangle at current costs is negligible, the application of expected inflation to future cash-flows leads to an increase in the BE of over 9% compared to the estimate with implicit inflation provided in

Section 6.1. This is clearly a consequence of the innovation effect illustrated in the last graph of

Figure 3.

As for the approach with unmodeled inflation, the ODP bootstrap algorithm was used to derive the distribution of the future insurance obligations. The ODP Bootstrap with 100,000 simulations provided the following results:

| - DUO sample mean: | 99,396 |

| - DUO Std | 5219 |

| - DUO CV | 5.25% |

| - YEO sample mean: | 102,827 |

| - YEO Std | 4542 |

| - YEO CV | 4.42% |

| - percentile of YEO | 115,386 |

| - Solvency Capital Requirement | 12,559 |

| - Present value of YEO sample mean: | 99,479 |

Also, in this case, the mean of the DUO and the discounted mean of the YEO are close to the BE

, which confirms the unbiasedness of the simulation procedure. The coefficient of variation of the PDF is

, and the reserve SCR is

of the BE. These figures should be compared with the corresponding figures provided by the implicit inflation approach, and show the increase in the reserve risk due to the modeled inflation uncertainty (

increase in SCR). These results are summarized in the third column of

Table 1,

Section 6.5.

It is important to point out that the increase in CV compared to the ODP with implicit inflation is not entirely due to stochastic inflation alone. Applying the ODP Boootstrap to the triangle at current costs without repricing for future inflation, one finds for the YEO distribution CV

. In this case, one also finds that the estimation error component stand-alone gives CV

, and the process error component stand-alone CV

. Taking account of the diversification effect due to the independence assumption between claims development risk and inflation risk, one finds that the CV component generated by the stochastic inflation stand-alone is

. This decomposition is summarized in the second section of

Table 2.

As concerning the kurtosis of the PDF with inflation uncertainty, we find and for the moment-fitted lognormal distribution we obtain . The corresponding SCR/Std ratios are and . Since, with the implicit inflation approach, the kurtosis of the PDF and of the moment-fitted lognormal is and , respectively, these figures seem to suggest that the inclusion of the inflation uncertainty reduces the kurtosis of the predictive distribution, bringing it closer to that of the corresponding lognormal distribution. This “push towards lognormality” should be a consequence of the fact that the inflation factors applied to the claim payments are lognormally distributed.

6.3. Application of the Market Approach

6.3.1. Specification of the Nominal Interest Rate Model

We chose perhaps the simplest univariate diffusion model for interest rates, proposed by

Vasicek (

1977) as a special case of an Ornstein–Uhlenbeck process. The real-world dynamics (

14) of the model is described by the SDE:

Then, we have a mean reverting drift

and a constant diffusion coefficient

. By (

24), given

, the conditional (natural) probability distribution of

, for

, is normal, with mean and variance determined by

and

; that is, by the parameters

and

. The mean is:

and the variance is:

For the market price of risk, we choose the form

, where

is the risk premium parameter (this is the form chosen by Cox, Ingersoll and Ross for their “mean-reverting square-root process” in Cox et al. (1985), where the choice is justified by general equilibrium arguments). Then, the risk-adjusted drift is given by:

The risk-neutral distribution of

is still normal, with mean and variance given, respectively, by (

25) and (

26) with

and

replaced by their risk-adjusted counterparts.

By the hedging argument, one finds that the nominal discount factor in

t for maturity

has the explicit form:

with:

It is worth noting that, by (

27), for

and

the random variable

has lognormal conditional distribution, given

.

Remark 9. Vasicek’s model has been criticized in the past for allowing nominal interest rates to be negative. Ironically, since around 2016, when a period of negative nominal interest rates set in, this feature has become one of its main strengths. However, the assumption of a constant diffusion coefficient remains a weakness of the model, since it is empirically observed that in periods of higher interest rates these, generally, also have higher volatility. That is, the symmetry of the distribution is an oversimplified assumption.

6.3.2. Estimation of the Interest Rate Model

Natural Parameters

In order to estimate the natural parameters and of the Vasicek model, we consider the triple-A yield curves computed by the European Central Bank (ECB) on each trading day. These curves are obtained by interpolating the observed returns on triple-A bonds with different maturities using the Svensson model, a six-parameters smooth function (see the Technical Notes downloadable from the ECB website for details). Since we are only interested in the instantaneous nominal interest rate (the initial point of the yield curve), we use only the estimates of parameters and , since in the Svensson function .

We use the daily time-series

of parameters computed by ECB, where

is the set of all trading days in [01/01/2005, 30/12/2022]. A well-known result in the Ornstein–Uhlenbeck process theory is that, integrating the SDE (

24) after an appropriate exponential transformation, one obtains an equation corresponding, for a chosen time step

, to the first order autoregressive model:

with:

and where the error terms

are independent normal with zero mean and constant variance:

Using the time-series of market values

, the parameter estimates

and

are obtained by linear regression and the corresponding estimates of

and

are derived by relations (

29) and (

30).

This procedure provided the following estimates:

Risk-Neutral Parameters

In order to calibrate at the valuation date

t, the Vasicek ZCB pricing function given by (

27) and (

28), we first estimate the risk-neutral parameters

and

by a best-fitting procedure of the theoretical function

to the corresponding market term structure

(with VA) provided by EIOPA at time

t. To have maximum flexibility, the instantaneous interest rate

is also included in the estimate. The corresponding ordinary-least-squares problem can be written as follows:

where the

A and

B functions are given in (

28) and the volatility parameter is maintained at the value

estimated in the previous section (observe that times-to-maturity greater than 25 years are not used in the estimation).

This procedure, however, cannot provide a perfect fitting of the model term structure to the observed one, a property that is instead essential in Solvency II, where the discount factors prescribed by EIOPA are mandatory. To circumvent this problem, we use the extension of the Vasicek model provided by

Hull and White (

1990) here (see also

Brigo and Mercurio (

2007), pp. 142–47). Some details of this model can be found in

Appendix B. In the Hull and White (HW) model, the basic idea to obtain the perfect fitting is to allow the parameter

to be time-dependent. As a consequence, the estimates

and

provided by (

31) are not used, because they remain “absorbed” in the observed term structure (which is taken as given). For our purposes, the crucial result in the HW model is that the future discount factors

, for

and

, are obtained as:

where

is normal with mean zero and variance:

and where:

with:

For the risk-neutral parameter

the estimate

obtained by the best-fitting procedure (

31) is used, while for the natural mean-reversion parameter, the time-series estimate

derived the previous section is maintained.

Expression (

32), together with the normality of

, allows us to simulate the one-year discount factors

and

required in the market approach. As in the Vasicek model, these random variables are conditionally lognormal.

6.4. Numerical Results with the Market Approach

Deterministic computations with the market approach provided:

| - Undiscounted reserve with modeled inflation | 109,445 |

| - Discounted reserve with modeled inflation (BE): : | 99,402 |

Using ODP Bootstrap with 100,000 simulations we obtained:

| - DUO sample mean: | 99,304 |

| - DUO Std | 5101 |

| - DUO CV | 5.14% |

| - YEO sample mean: | 102,809 |

| - YEO Std | 4773 |

| - YEO CV | 4.64% |

| - percentile of YEO | 115,880 |

| - Solvency Capital Requirement | 13,071 |

| - Present value of YEO sample mean: | 99,461 |

The property

is verified, since we have

99,402 and

99,493. The difference is small, however, since the factors

are very close to 1. The theoretical difference, discussed at the end of

Section 5.2.3, between

and the present value of

cannot be checked, since it is lower than the simulation error, as expected.

As concerning the reserve risk, we observe first that, as anticipated in

Section 5.2.2, the CV of the DUO distribution is now lower than with the actuarial approach. This is not the case for the YEO distribution: the interest rate uncertainty applied to the reserve estimates in

produces an increase in the standard deviation of the YEO with respect to the actuarial approach (CV

). The reserve SCR is

of the BE. As with the inflation risk, the impact of the interest rate risk is partially hidden by diversification effects. Using again the independence assumptions, one finds that the CV component due to interest rate risk stand-alone is

. These results are also summarized in

Table 1 (fourth column) and

Table 2 (second block) in the next section.

Considering the kurtosis of the PDF, we find

, and for the moment-fitted lognormal distribution, we obtain

. The corresponding SCR/STD ratios are

and

. These figures seem to indicate a slight further push towards lognormality, which could be explained by the fact that the stochastic discount factors

given by (

32) are also lognormally distributed.

6.5. Concluding Summary Tables

The following comparison tables summarize the main results obtained with the three claims reserving approaches considered.

{kind=link}

{kind=link}

{kind=link}