1. Introduction

The insurance industry related to life insurance and pension plans is facing a number of risks. Longevity risk is one of the most important risks faced by annuity providers, in which participants are promised a benefit throughout their retirement. When people live longer than expected, an increase in longevity risk is observed. Although most of the international demographic trends indicate a steady increase in life expectancy, there are other schools of thought that argue for potential opposite trends due to unknown diseases or other medical reasons (e.g., malnutrition, obesity, etc.).

Despite the fears that these reasons would reverse these trends, life expectancy in developed countries has grown steadily, by approximately 2.5 years per decade.

Kisser et al. (

2012) show that an increase in life expectancy by one year in the USA raises pension liabilities by 3% to 4%, which is a substantial economic magnitude.

Jones (

2013) explains how longevity risk can affect most in the whole of society—for example, the governments who have to provide retirement benefits to individuals through pensions and healthcare, the corporate sponsors who provide retirement benefits and health insurance obligations to former employees and individuals who do not rely on governments or corporate sponsors to fund retirement.

In this spirit, actuaries seek solutions through the development of some financial instruments that can offer tools against longevity risk. Traditionally, reinsurance can serve as a hedging tool but sometimes is rather expensive. Securitization can substitute classic reinsurance by transferring risk to third parties.

Blake and Burrows (

2001) suggested the use of longevity bonds, issued by the governments, with coupon payments proportional to the population surviving to particular ages. The annuity providers would then make payments for a longer period if annuitants lived longer, but in that case, they would also receive a greater offsetting coupon payment on their survivor bonds asset positions. For a further discussion on the securitization process, we refer to

Cowley and Cummins (

2005).

There is rich literature with various papers on managing longevity risk, including securitization or other hedging techniques. Among others,

Lin and Cox (

2005) made a remarkable contribution that highlights the main aspects of longevity risk securitization. In their paper, the authors illustrate how insurers can use mortality-based securities to manage longevity risk. They argue that mortality-based securitization has the same structure as the catastrophe risk bonds, but differs in the way that deviations in mortality forecasts may occur gradually over a long period. Moreover,

Blake et al. (

2006) examined various ways in which an insurer can manage longevity risk, focusing on the use of mortality-linked securities to manage their exposure.

Thomsen and Andersen (

2007) observed an imbalance between supply and demand for longevity products explained by the fact that many insurers are interested in hedging their longevity risks, in the absence of investors who want to benefit from an unexpected rise in mortality. Nevertheless,

Hari et al. (

2008) analyzed the importance of longevity risk for the solvency of annuity portfolios, and focused on the risk that results from uncertainty in the remaining lifetime of a member of a pension plan. They also distinguish two types of longevity risk, the micro-longevity risk that results from non-systematic deviations from a member’s expected remaining lifetime, and the macro-longevity risk that is due to the change in survival probabilities over time.

Furthermore,

Yang and Huang (

2009) investigated the interplay between asset allocation and longevity risk for defined contribution pension plans, while

Barrieu et al. (

2012) explored the key risk management challenges for both financial and insurance industries. To make the longevity risk market operational in an efficient and transparent way,

De Jong and Ferris (

2019) and

Lin et al. (

2022) proposed the so-called survival–mortality bond, which is a long-term conventional government bond that incorporates a survivorship part and a mortality part. For an extensive review on recent developments related to longevity risk and capital markets, we refer to

Blake and Cairns (

2021).

An essential step in the process of longevity risk securitization is the selection of the mortality projection model. An appropriate mortality model must be able to handle the mortality patterns of the given data and produce reliable forecasts for building projected life tables. Different modeling approaches have been developed so far.

Lin and Cox (

2005) used the model of

Renshaw et al. (

1996) to predict the future mortality improvements needed to price longevity risk securities for US data. One of the most prominent modeling approaches is also the

Lee and Carter (

1992) model, which is widely used by many researchers.

Denuit et al. (

2007) applied the original Lee–Carter model on Belgian mortality data in order to price a longevity bond;

Levantesi et al. (

2008) used the

Brouhns et al. (

2002) extension of the Lee–Carter model in a similar study for the Italian population, while

Kim and Choi (

2011) and

Lorson and Wagner (

2014) priced a longevity bond using the mortality projections of the Lee–Carter model for German and Australian data, respectively.

A critical issue that may appear when fitting a mortality model is the limited data availability, which may affect the existing modeling methods that inevitably base their forecasts on population datasets of limited periods of observations. This paper contributes to the literature in two ways. Firstly, it incorporates a recently developed modeling framework, particularly designed to project mortality rates for datasets, with limited experience for the mortality evolution of a specific age, but extensive experience for the entire fitted range of ages. Secondly, our projected life tables are used to price a longevity bond with the Wang transform for the mortality data of Greece, a country with limited publicly available data.

The remainder of this paper is organized as follows.

Section 2 presents the mortality modeling approach under the credibility regression framework with three extrapolation methods to construct projected life tables.

Section 3 describes the mathematical structure and the necessary transactions for pricing longevity bonds with the Wang transform.

Section 4 applies the whole pricing process to Greek data, and

Section 5 concludes the paper.

2. Mortality Projection under the Credibility Regression Framework

In this section, we review the credibility regression mortality framework, presented as a special case of a more general model in

Bozikas and Pitselis (

2019). Credibility theory includes various estimation techniques, traditionally used in non-life insurance. More specifically, credibility regression was introduced by

Hachemeister (

1975) to estimate the trend in automobile bodily injury claims for various states in the USA.

Over the last century, empirical mortality data have shown a downward trend in each age. Particularly in higher ages, mortality rates have been significantly improving over the last few decades due to many factors, such as the dynamics of the human race, the improvement of living conditions, medical advances, etc. This fact led us to seek a model structure that will be able to capture these improvement trends and describe the mortality evolution over time, even if our available data are of a limited size. The credibility regression framework will be used to construct projected life tables for datasets with limited experience for the mortality evolution of a specific age, but extensive experience for the entire fitted age range.

2.1. Notation and Assumptions

We denote by the observed number of deaths at age in year and by the average population aged during year (also known as exposure to risk), while the age-specific mortality rates are obtained by the ratio . Let us consider that corresponds to consecutive integer ages ( in total) and corresponds to consecutive calendar years ( in total). Then, for each age , we define a regression model , where is the response vector of log-transformed mortality rates, is the design matrix, is the vector of coefficients and is the vector of model error, with and , where is a fixed diagonal matrix of known regression weights.

To implement the credibility regression framework, we assume that response variable

is characterized by an

vector of risk parameters

, associated with age

. The design matrix

includes an intercept and a slope parameter, which integrates the linear trend of mortality decline over calendar years

1. Therefore, the pair that describes mortality evolution in age

under the credibility regression framework is

.

To proceed with the parameter estimation procedure, it is further assumed that the pairs , , , are independent and are independent and identically distributed. The conditional expectation is , where is a fixed design matrix and is an regression coefficients vector, and the conditional variance is . Note that in some cases, the use of appropriate regression weights may improve the model fit. Otherwise, one can simply consider that , where is the identity matrix.

2.2. Credibility Estimation

Before proceeding to the credibility estimation, we first define the parameters of the proposed model (also known as structural parameters). The overall mean and variance of regression coefficients are given by and , respectively, and the expected variance by .

The least squares estimator of the regression coefficients

can be derived by

, the covariance matrix by

, and its expected value by

. Then, the credibility estimator

of

for the proposed model is given by:

where

is the estimator of credibility weight (also known as credibility factor). We use the following optimal estimators (with minimum variance within the class of unbiased estimators) for the structural parameters:

Note that the estimators of

and

are calculated iteratively, imposing

after each iteration. Fore more details on the estimation procedure, we refer to

De Vylder (

1978,

1996),

Goovaerts et al. (

1990), and

Bozikas and Pitselis (

2019).

2.3. Constructing Projected Life Tables

Given the available mortality rates

, the aim is to obtain the credibility mortality estimates for

years ahead

where

denotes the design matrix of future periods, i.e., for calendar years

. First, we derive the one-year-ahead credibility mortality estimates by

or equivalently by

Then, we can obtain the projected mortality rates

for

years ahead using the following projection methods:

(a) Standard Projection Method (SPM): Similar to (

3), the credibility estimates of future mortality rates for

are given by

, where the vector

is estimated by (

1). Hence, under this method, future mortality estimates are based on the data of the initial fitting span

. Two additional methods can be applied in practice to derive future mortality rates over a given forecasting horizon

. The numerical results in

Bozikas and Pitselis (

2019) justify that the following methods can be efficiently implemented in actuarial practice.

(b) Moving Projection Method (MPM): Assume that the derived one-year-ahead mortality rate is added in the response variable, while the first observed rate is simultaneously excluded from it. Thus, the fitting span shifts by one year to become , keeping a constant fitting length, to estimate . By repeating the same procedure, we can consecutively obtain .

(c) Extended Projection Method (EPM): Now, we assume that the one-year-ahead mortality rate is added in the response variable, but now is not excluded, so that the fitting year span is extended by one year to . Hence, after each step, the response variable is extended by one year to obtain .

Both MPM and EPM (also known as dynamic forecasting methods in time series contexts) extend the use of Equation (

3) to a forecasting horizon of h-years ahead. Note that under the MPM, future estimates are based on the mortality experience of more recent calendar years, while under the EPM, the whole experience is accounted for when estimating future mortality.

Remark 1. There are cases where the uncertainty in mortality forecasts is of interest. This uncertainty may be expressed with prediction intervals. In such a case, the prediction intervals for the mortality forecasts can be obtained by the upper and lower bounds of in credibility Formula (2). However, in this paper, we use the point projections obtained from each projection method. Once mortality projections are obtained, we can obtain any quantity of interest, which is essential for the construction of a projected life table. Specifically, the one-year probability of death for an annuitant aged

in year

is derived from the identity

by assuming a constant force of mortality over each integer age

and calendar year

, while the corresponding one-year survival probability is given by

. Then, the projected

t-year survival probability for an annuitant aged

in year

can be obtained as follows

while its complement

will be

4. Numerical Illustration

In this section, we illustrate longevity bond pricing using the projected life tables, constructed under the credibility framework. We use the data of the general population of Greece, obtained by the

Human Mortality Database (

2022), where the official Greek data are publicly available for a relatively short period of mortality observations (1981–2019), compared to the datasets of other developed countries. Similar data limitations are often the case when dealing with insurance datasets. The credibility modeling framework aims to capture underlying data trends, particularly when there is limited mortality experience from a specific age, and extensive experience from the entire age range. Credibility regression methods can, of course, be used on larger datasets as well.

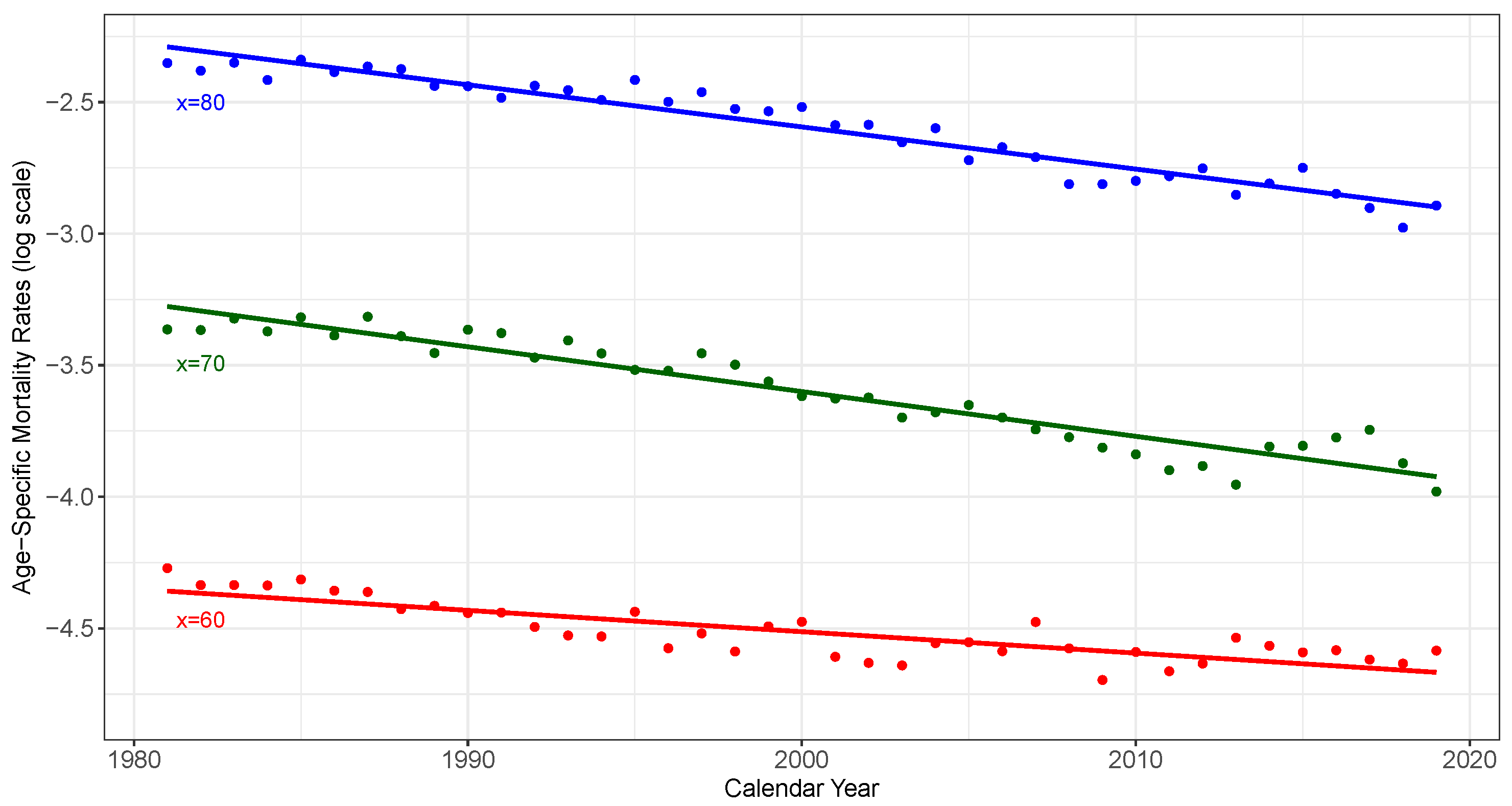

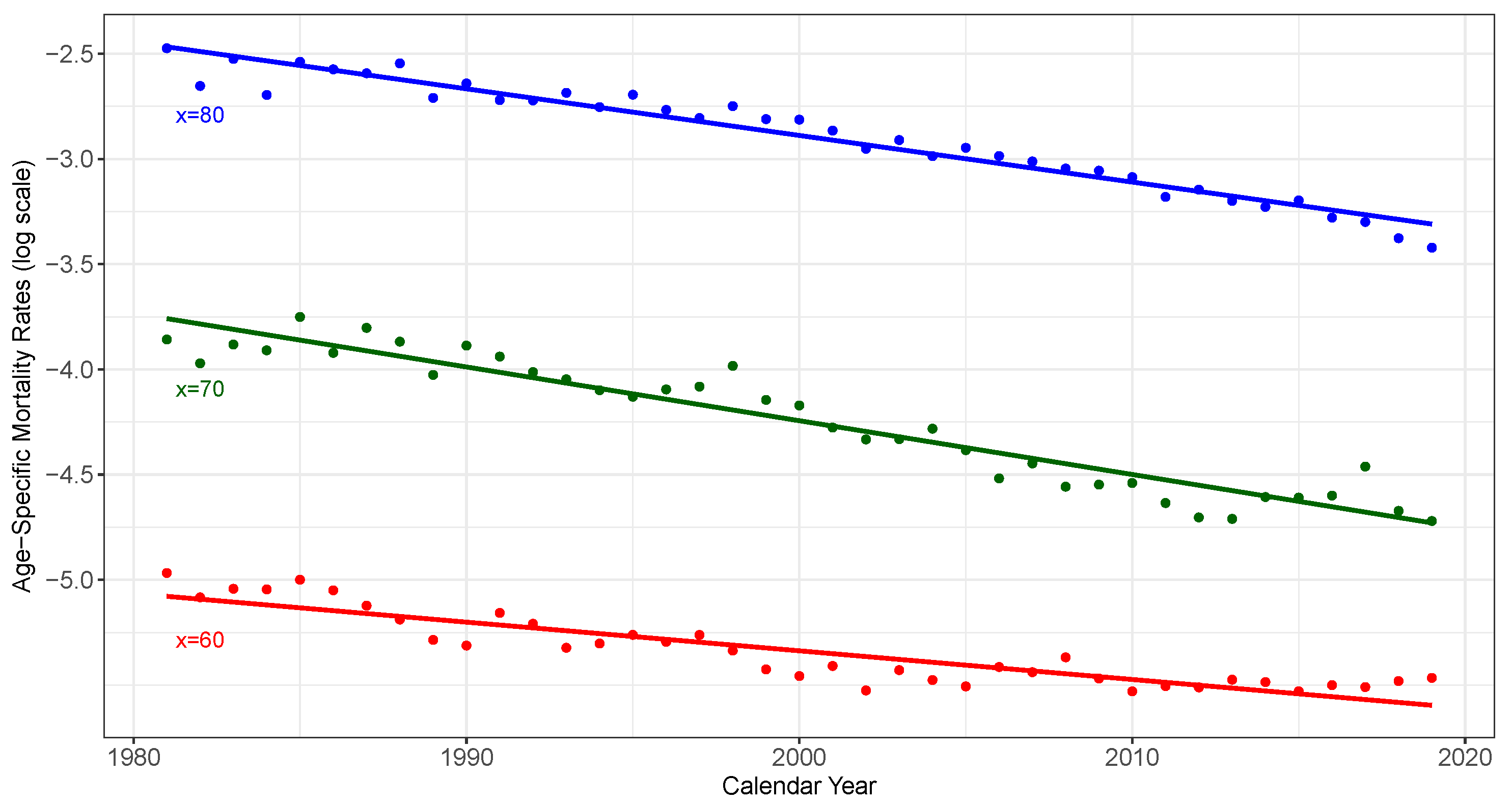

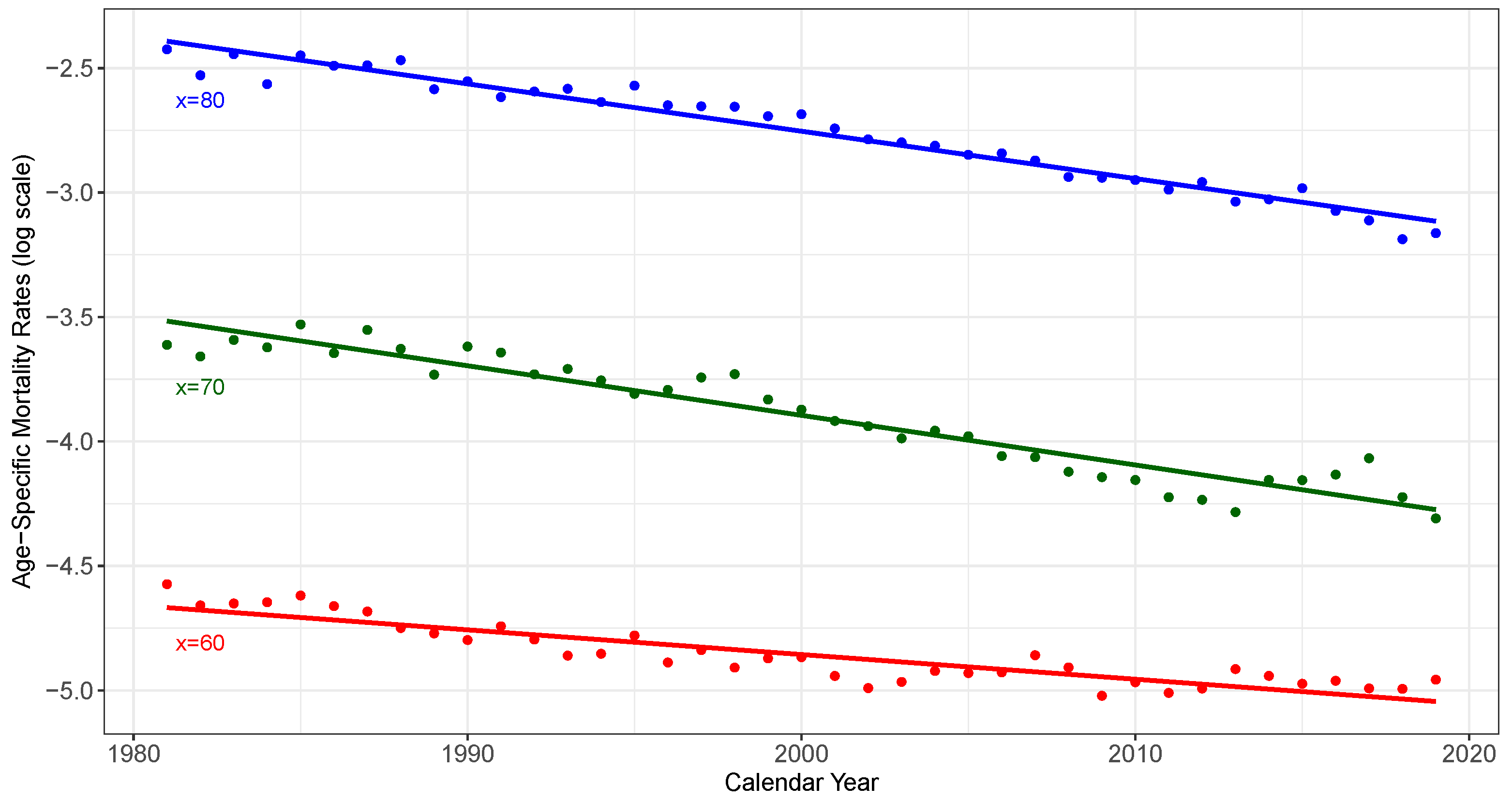

The Greek mortality rates for ages

over the period 1981–2019 are depicted for males in

Figure 2, for females in

Figure 3, and for the total population in

Figure 4. For both genders and the total population, we can easily observe a downward trend in age-specific mortality data per year.

For our illustration, we construct projected life tables under the credibility regression framework, using the observed mortality rates in Greece, for males, females, and the total population for years

and ages

(from a usual age of an annuitant up to the level of life expectancy in developed countries). The forecasting performance of each projection method, in comparison to other widely used mortality models, has been thoroughly evaluated in

Bozikas and Pitselis (

2019), where the MPM method had the best average forecasting performance, especially in pricing annuity and life insurance products.

Let us now consider an initial cohort of

= 10,000 annuitants in year

of an annuity provider that needs to be secured for

years on. The

value in Equation (

11) is an appropriate proxy for the market price of an annuity, sold to an annuitant at the age of

. To obtain this value

3, we use two representative life tables, developed by the Hellenic Actuarial Society (namely HAS2005 and HAS2012) for annuity products. The first life table is a sex-distinct table based on the mortality experience over the years 2000–2003 from individual insurance policies, while the second one, which is currently in use, is an updated version of HAS2005 developed on a unisex basis

4. To ensure the efficiency of these life tables in future computations, the assigned working group projected the annual mortality improvement coefficients based on the data from the Greek general population.

To obtain the corresponding market price of risk

under each projection method, we use the projected probability

in (

5) to solve Equation (

11) numerically. The annuity values, based on the HAS2005 life table, are 14.66 for a male and 17.36 for a female annuitant aged 65, while the corresponding value for the total population, based on the HAS2012 table, is 16.54. The discount factor is calculated with

for a period of

years to maturity.

For comparison purposes, we consider different interest rates varying from 1 to 3 percent to calculate the market price of risk values under each projection method, based on the annuities obtained from the HAS2005 (male and female population) and HAS2012 life tables (total population). The corresponding results are exhibited in

Table 1.

We observe that the average market price of risk with the selected interest rate

is

for males,

for females, and

for the total population, with the highest values per gender observed under the SPM projection method. Moreover, the overall average for males and females is

, slightly higher than the average value

, reported for other markets in the literature (see

Kim and Choi 2011;

Lorson and Wagner 2014). As

Denuit et al. (

2007) pointed out, the market price of risk is lower if a more conservative life table is used by the annuity provider.

Once the

s are obtained, we can obtain the transformed probability values by (

9) and (

10) to calculate the expected value

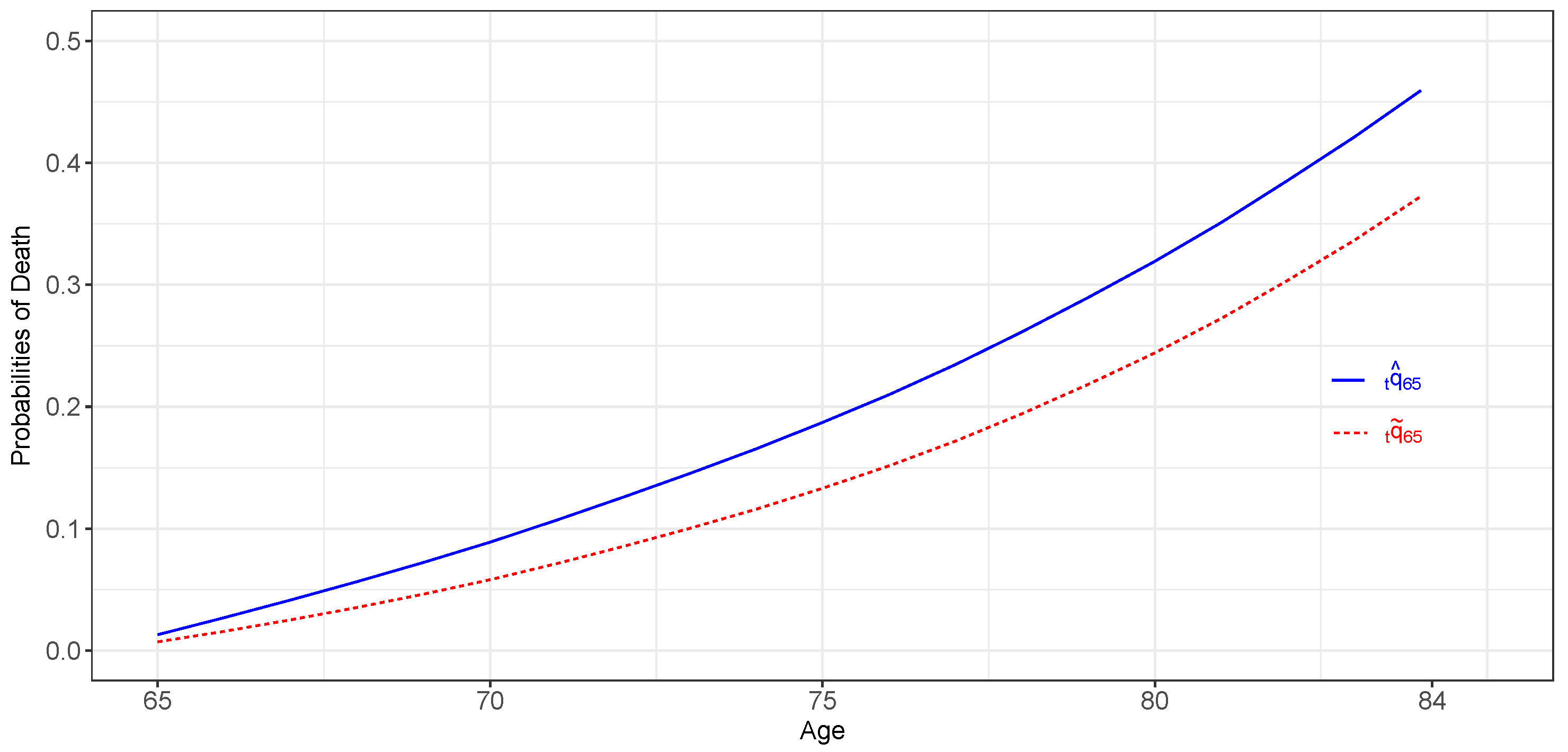

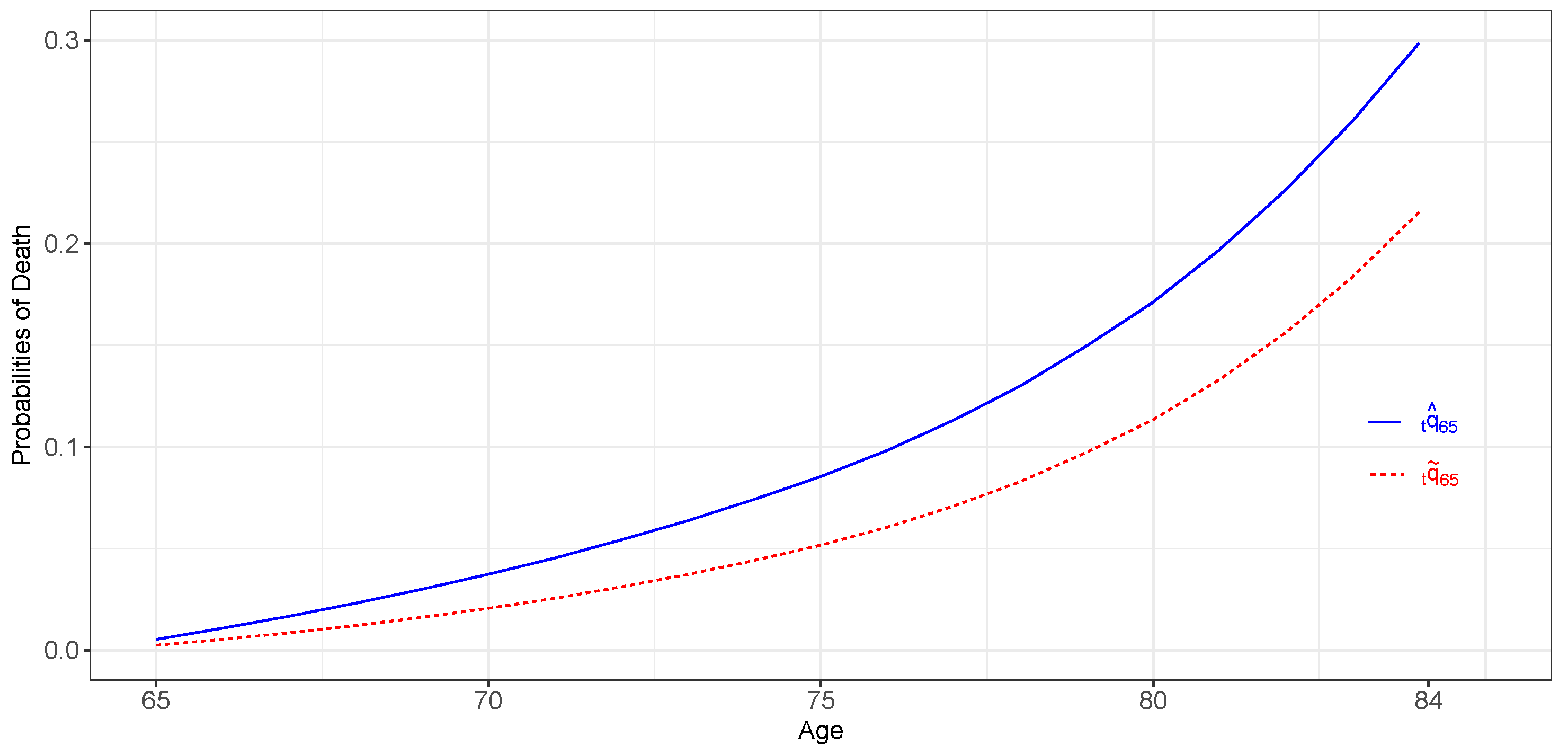

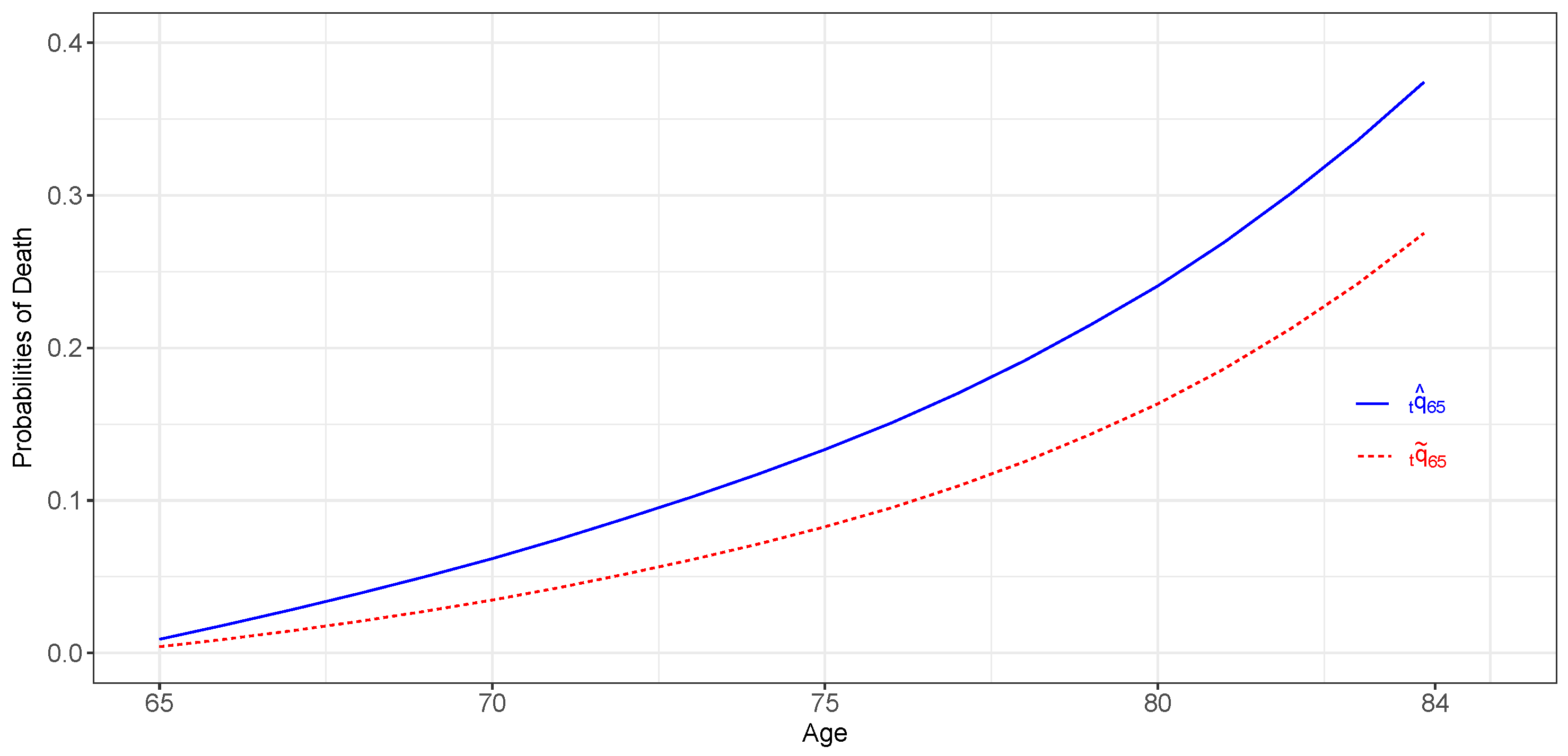

, needed for the calculation of the longevity bond price. The death probability

under the SPM method, which corresponds to a 65-year-old annuitant that will die before reaching age

, and the corresponding transformed probability

under the Wang transform are illustrated for Greek males in

Figure 5, for females in

Figure 6, and the total population in

Figure 7.

We observe that the transformed probabilities are lower than their credibility counterparts. The same behavior is also observed for the corresponding probabilities under the MPM and EPM methods (not displayed). This was also noted by

Levantesi et al. (

2010), explaining the fact that transformed probabilities should be lower because they incorporate longevity risk.

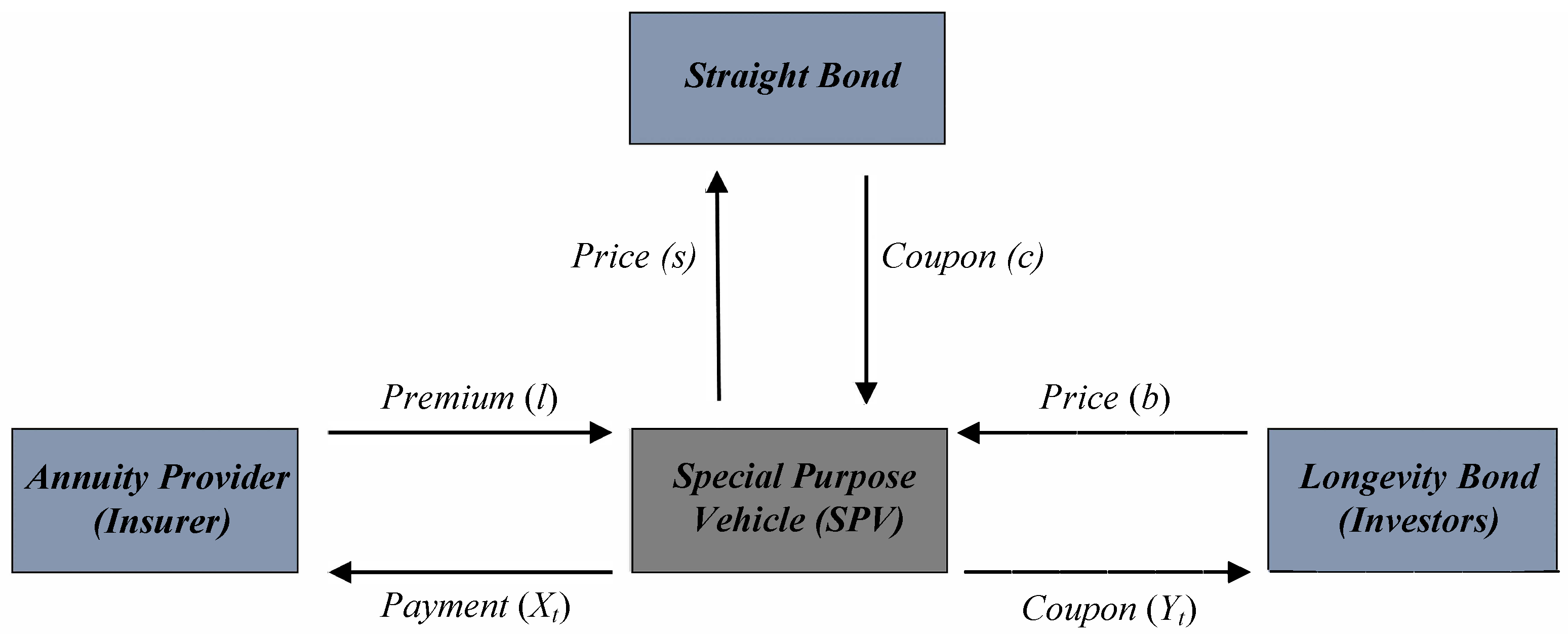

Based on our initial cohort of

= 10,000 annuitants, now, we assume that the SPV issues a longevity bond of face value 10,000,000 currency units with 4% coupon rate (

) and at the same time buys a straight bond of the same price and coupon. The SPV’s annual payment is 1000 currency units per annuitant who survives. If the number of annuitants who survive

exceeds the estimated number of survivors

, the annuity provider collects the excess from the SPV, up to the maximum amount of 1000c = 400,000, while the the total coupon received by the investors is given by the

(4,000,000

. The longevity bond pricing results for males, females, and the total population are presented concisely in

Table 2.

The pricing results indicate that the highest longevity bond price for a 65-year-old male annuitant from the initial cohort is given by the EPM method, while that for a female annuitant and an annuitant from the total population is given by the MPM method. This means that the premium paid by the annuity provider for a 20-year coverage for a male annuitant is lower under the EPM method (62.57), while the premium for a female and an annuitant from the total population is lower under the MPM method (33.26 and 64.32, respectively).

For the sake of comparison,

Table 3 provides the corresponding pricing results obtained by the well-known

Lee and Carter (

1992) mortality projection method. This method has been widely used in similar works for other markets—for example, see

Denuit et al. (

2007),

Kim and Choi (

2011) and

Lorson and Wagner (

2014). The results in

Table 3 indicate that, for both genders and the total population of Greece, the Lee–Carter method leads to a higher market price of risk and premium values than those obtained by the proposed methods (

Table 2).

In our application, the longevity bond price and the premium calculation are based on the mortality projections of the general population. This means that

and

do not refer to a specific insured population, but derive from an official public database. From an investor’s perspective, the use of a public source gives full access to the data, avoiding moral hazard, since annuity providers cannot manipulate their reported mortality data. On the other hand, the use of general population mortality data may lead to an imperfect hedge, which introduces basis risk. It is worth noting that the premium value could be lower if our projection methods were applied only to mortality data of the insured population. However, this is practically impossible in our case as there are only three available life tables

5 for the Greek insured population. Nevertheless, we think that a more active life annuity market could lead us to an even more representative price for the longevity bond.

5. Concluding Remarks

The increase in life expectancy raises serious concerns about the sustainability of the insurance industry. Longevity relates directly to the reserves of funds by creating additional costs for annuity providers.

In this paper, we exploited the credibility regression mortality framework to construct projected life tables with limited available data, and then we described how these projections can be incorporated to hedge longevity risk through the form of securitization. We demonstrated this process focusing on pricing a longevity bond using the available Greek data, obtained from a public source. To the best of our knowledge, such a study has not yet been conducted for Greek data; nevertheless, our findings look reasonable and conform with the international experience from similar studies.

Specifically, we used three methods under the credibility regression framework to construct projected life tables, and we described the process inherent to pricing a longevity bond. To obtain the transformed probabilities needed for the pricing process, we used the (one-parameter) Wang transform. Even if the Wang transform has been widely applied in the literature (see

Lin and Cox 2005,

Denuit et al. 2007,

Levantesi et al. 2008,

Kim and Choi 2011, and

Lorson and Wagner 2014) to price longevity risk for different populations, some authors have raised their concerns in regard to the relationship between transforms of different cohorts and terms to maturity, and their mutual coherence (see

Cairns et al. 2006). To resolve this issue,

Wang (

2002) proposed a two-parameter transform, using the cumulative distribution function of

distribution instead of the standard normal distribution, but this transform seemed to lack a sound economic interpretation.

An alternative option in pricing and hedging financial derivatives is the use of the martingale approach. However, as

Loisel and Serant (

2007) noted, the life insurance market is far from complete due to a lack of observed market prices. Thus, the choice of an explicit risk-neutral measure is a non-trivial task, and this is the reason that traditional pricing methods, involving the Wang transform, are sometimes preferred to other classical financial methods. Nevertheless, the consideration of other approaches (e.g., two-parameter Wang transform, risk-neutral approach), under the credibility mortality framework, has been left for future research.

Regarding some extensions of the longevity risk securitization process in the public sector, it should be mentioned that in the near past, actuaries disagreed on whether longevity bonds should be issued by the government and others suggested that it should have an auxiliary role in sharing longevity risk. Nowadays, many actuaries agree that government-issued longevity bonds or other securities should be reconsidered as a tool of sharing longevity risk fairly between generations, leading to more secure pension savings for social welfare improvements.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}