The Dynamic Connectedness between Risk and Return in the Fintech Market of India: Evidence Using the GARCH-M Approach

Abstract

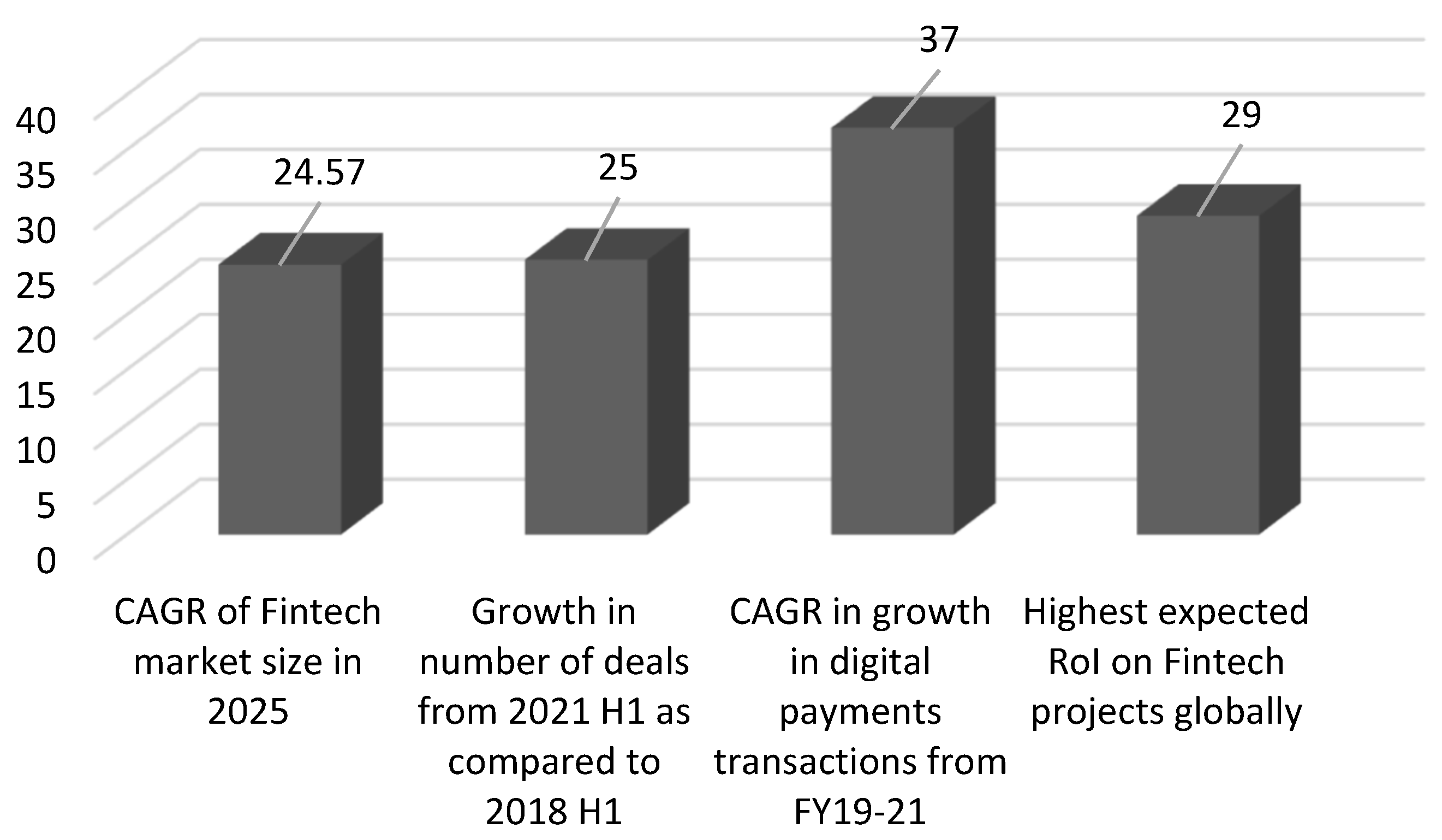

1. Introduction

2. Literature Review

3. Methodology

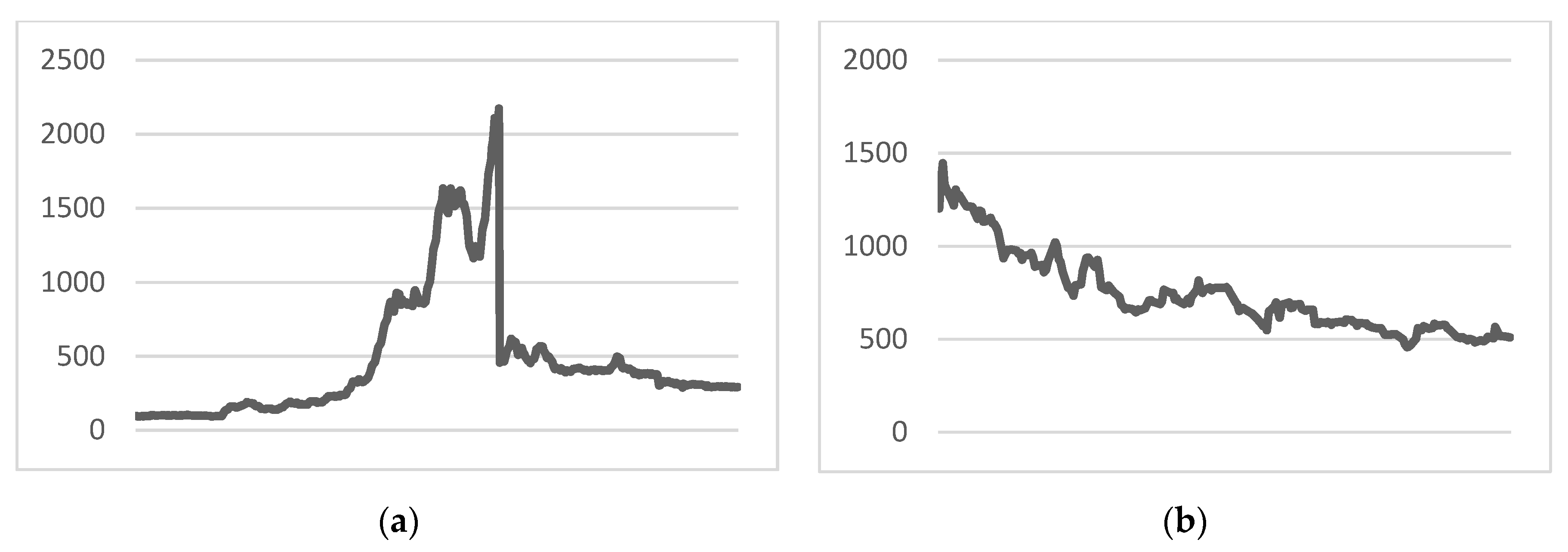

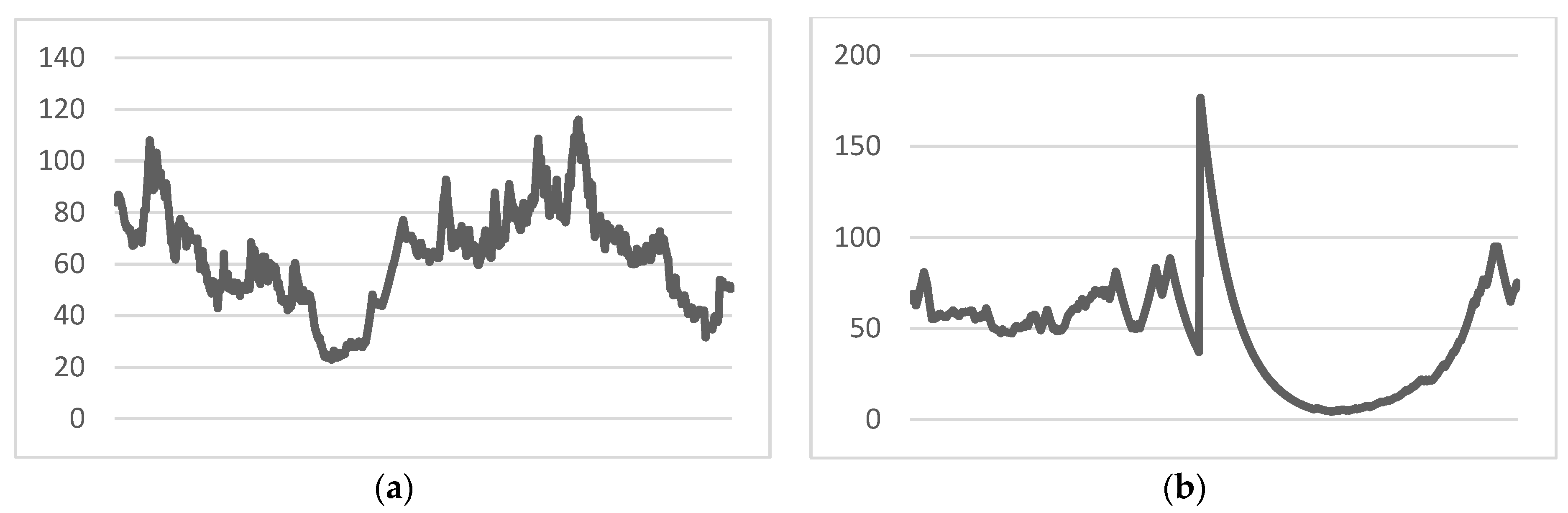

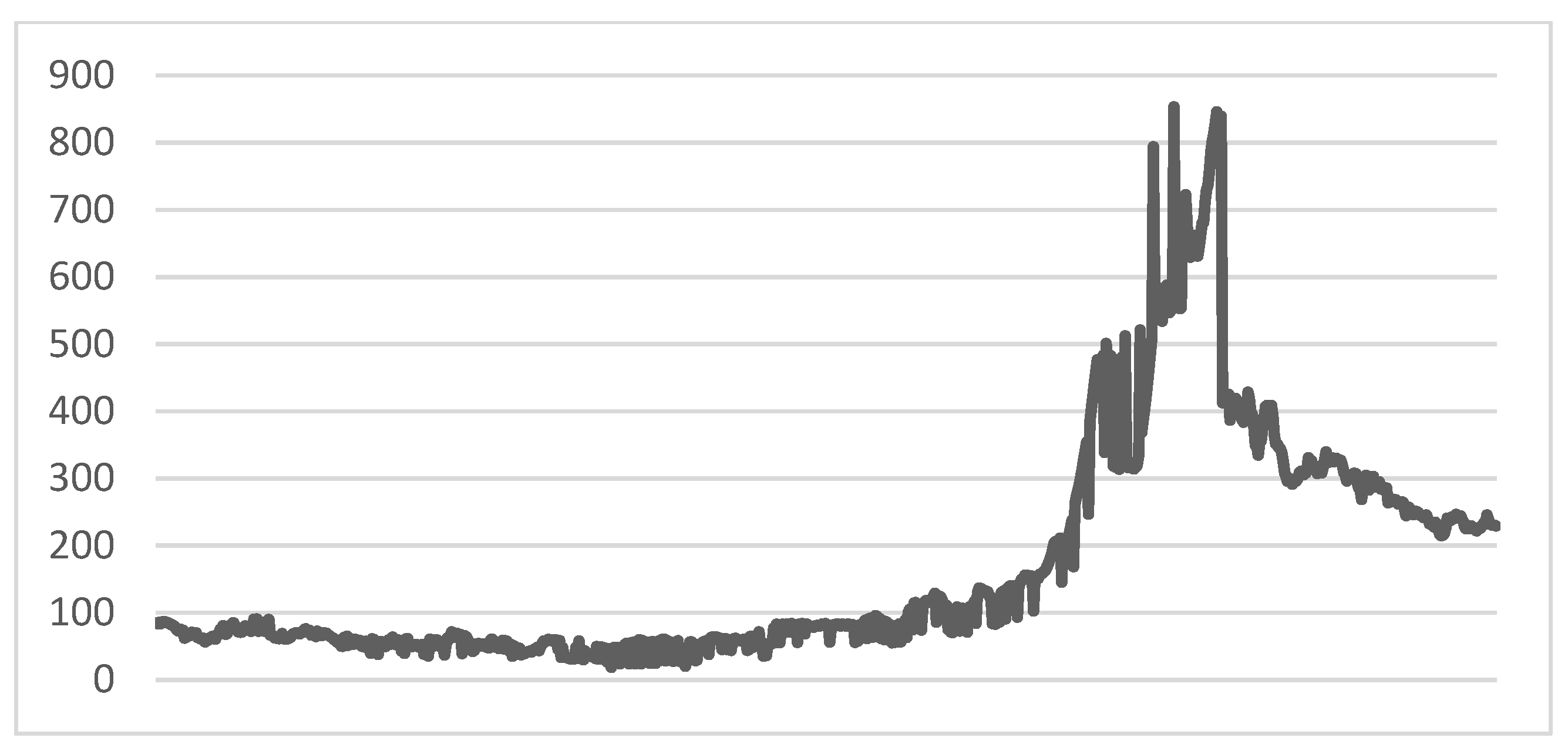

3.1. Sample

3.2. Model

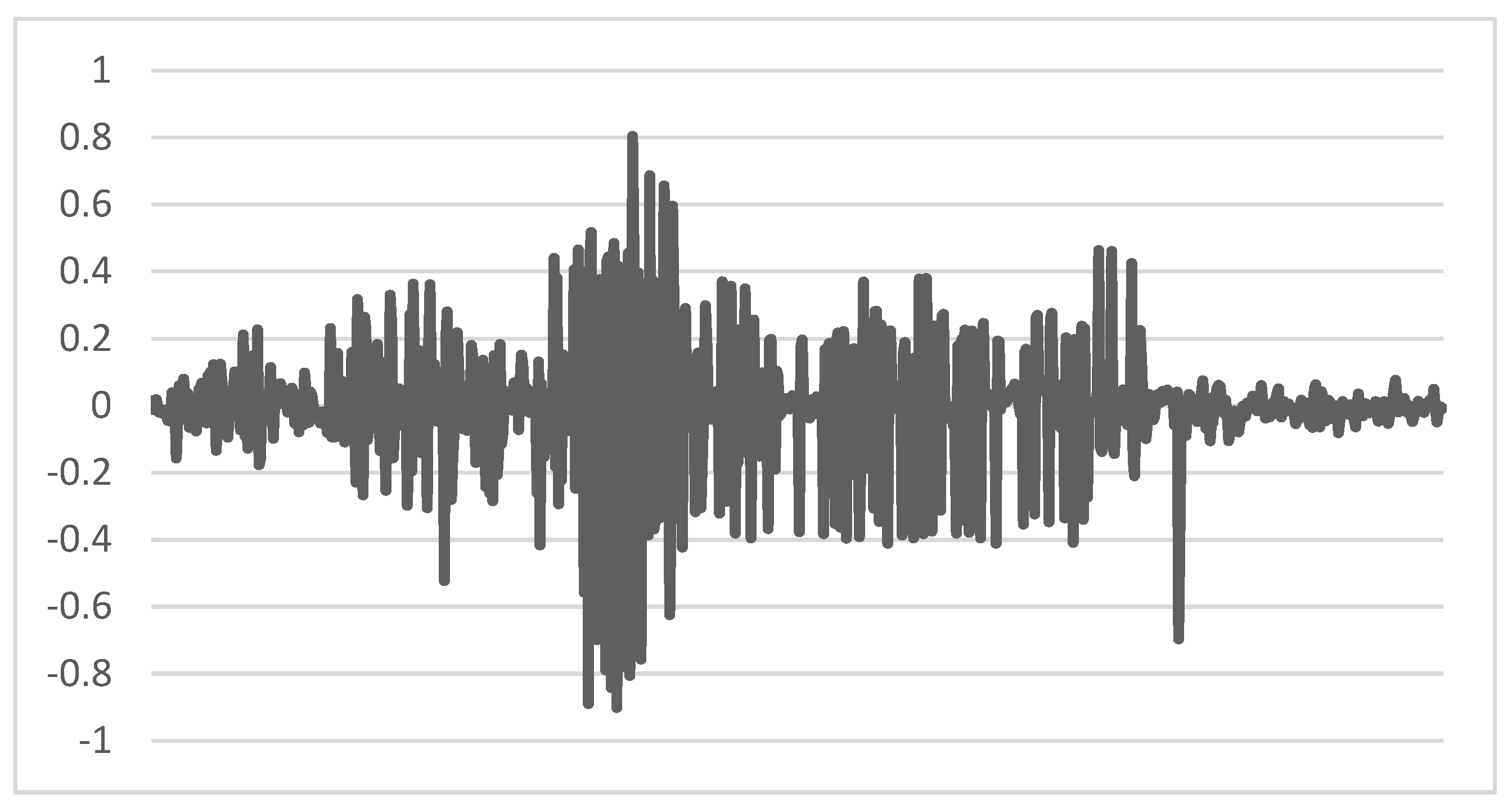

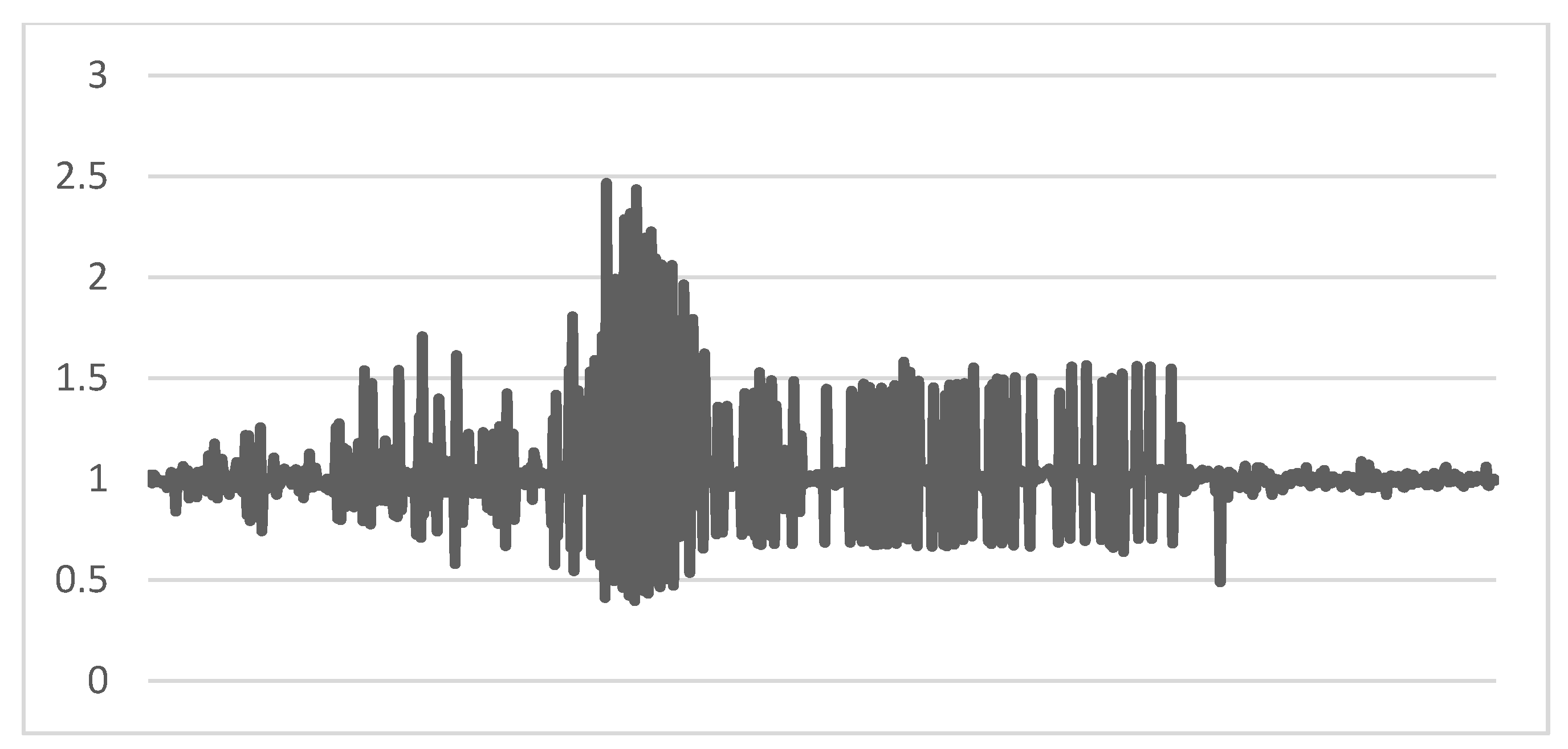

4. Results

5. Discussion

6. Concluding Remarks

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

References

- Agrawal, Vivek. 2021. “History of Fintech”. FINTICA. August 28. Available online: https://www.fintica.com/history-of-fintech/ (accessed on 12 September 2022).

- Ahmi, Aidi, Afiruddin Tapa, and Ahmad Husni Hamzah. 2020. Mapping of Financial Technology (FinTech) Research: A Bibliometric Analysis. International Journal of Advanced Science and Technology 29: 379–92. [Google Scholar]

- Aielli, Gian Piero. 2013. Dynamic Conditional Correlation: On Properties and Estimation. Journal of Business & Economic Statistics 31: 282–99. [Google Scholar] [CrossRef]

- Al Nawayseh, Mohammad K. 2020. Fintech in COVID-19 and beyond: What Factors Are Affecting Customers’ Choice of Fintech Applications? Journal of Open Innovation: Technology, Market, and Complexity 6: 1–15. [Google Scholar] [CrossRef]

- Alam, Azhar, Ririn Tri Ratnasari, Chabibatul Mua’awanah, and Raisa Aribatul Hamidah. 2022. Generation Z Perceptions in Paying Zakat, Infaq, and Sadaqah Using Fintech: A Comparative Study of Indonesia and Malaysia. Investment Management and Financial Innovations 19: 320–30. [Google Scholar] [CrossRef]

- Al-Emadi, Khalid Ahmed, Zorah Abu Kassim, and Anjum Razzaque. 2021. User Friendly and User Satisfaction Model Aligned With FinTech. In Advances in Finance, Accounting, and Economics. Edited by Yousif Abdullatif Albastaki, Anjum Razzaque and Adel M. Sarea. Bahrain: IGI Global, pp. 291–301. [Google Scholar] [CrossRef]

- Algoquant Fintech Limited. n.d. Available online: https://www.algoquantfintech.com/ (accessed on 6 October 2022).

- Al-Homaidi, Eissa A., Ebrahim Mohammed Al-Matari, Mosab I. Tabash, Amgad S. D. Khaled, and Nabil Ahmed M. Senan. 2021. The Influence of Corporate Governance Characteristics on Profitability of Indian Firms: An Empirical Investigation of Firms Listed on Bombay Stock Exchange. Investment Management and Financial Innovations 18: 114–25. [Google Scholar] [CrossRef]

- Arslanian, Henri, and Fabrice Fischer. 2019. The Rise of Fintech. In The Future of Finance. Cham: Palgrave Macmillan, pp. 25–56. [Google Scholar] [CrossRef]

- Asmarani, Saraya Cita, and Chandra Wijaya. 2020. Effects of Fintech on Stock Return: Evidence from Retail Banks Listed in Indonesia Stock Exchange. The Journal of Asian Finance, Economics and Business 7: 95–104. [Google Scholar] [CrossRef]

- Beaulieu, Marie-Claude, Marie-Hélène Gagnon, and Lynda Khalaf. 2009. A Cross-section Analysis of Financial Market Integration in North America Using a Four Factor Model. International Journal of Managerial Finance 5: 248–67. [Google Scholar] [CrossRef]

- Berdjane, Belkacem, and Serguei Pergamenshchikov. 2016. Sequential δ-Optimal Consumption and Investment for Stochastic Volatility Markets with Unknown Parameters. Theory of Probability & Its Applications 60: 533–60. [Google Scholar] [CrossRef]

- Bildirici, Melike E. 2022. Chaos Structure and Contagion Behavior between COVID-19, and the Returns of Prices of Precious Metals and Oil: MS-GARCH-MLP Copula. Nonlinear Dynamics, Psychology, and Life Sciences 26: 209–30. [Google Scholar]

- Black, Fischer, and Myron Scholes. 1973. The Pricing of Options and Corporate Liabilities. Journal of Political Economy 81: 637–57. [Google Scholar] [CrossRef]

- Bollerslev, Tim. 1986. Generalized Autoregressive Conditional Heteroskedasticity. Journal of Econometrics 31: 307–27. [Google Scholar] [CrossRef]

- Bollerslev, Tim, and Robert F. Engle. 1993. Common Persistence in Conditional Variances. Econometrica 61: 167. [Google Scholar] [CrossRef]

- BSE. 2022. India Stock Exchange. Available online: https://www.bseindia.com/ (accessed on 15 September 2022).

- Cardenas, Juan Camilo, and Jeffrey Carpenter. 2008. Behavioural Development Economics: Lessons from Field Labs in the Developing World. The Journal of Development Studies 44: 311–38. [Google Scholar] [CrossRef]

- Cha, Baekin, and Yan-leung Cheung. 1998. The Impact of the U.S. and the Japanese Equity Markets on the Emerging Asia-Pacific Equity Markets. Asia-Pacific Financial Markets 5: 191–209. [Google Scholar] [CrossRef]

- Chang, Kuo-Ping. 2019. Behavioral Economics Versus Traditional Economics: Are They Very Different? SSRN Scholarly Paper ID 3350088. Rochester: Social Science Research Network. [Google Scholar] [CrossRef]

- Chen, Gong-meng, Michael Firth, and Oliver Meng Rui. 2002. Stock Market Linkages: Evidence from Latin America. Journal of Banking & Finance 26: 1113–41. [Google Scholar] [CrossRef]

- Chen, Ming-Hsiang, and Woo Gon Kim. 2006. The Long-Run Equilibrium Relationship Between Economic Activity and Hospitality Stock Prices. The Journal of Hospitality Financial Management 14: 1–15. [Google Scholar] [CrossRef]

- Cheng, Ing-Haw. 2020. Volatility Markets Underreacted to the Early Stages of the COVID-19 Pandemic. Edited by Jeffrey Pontiff. The Review of Asset Pricing Studies 10: 635–68. [Google Scholar] [CrossRef]

- Chishti, Susanne, and Janos Barberis. 2016. The Fin Tech Book: The Financial Technology Handbook for Investors, Entrepreneurs and Visionaries. Hoboken: Wiley. [Google Scholar]

- Da Fonseca, José, and Yahua Xu. 2019. Variance and Skew Risk Premiums for the Volatility Market: The VIX Evidence. Journal of Futures Markets 39: 302–21. [Google Scholar] [CrossRef]

- David, Dharish, Miyana Yoshino, and Joseph Pablo Varun. 2022. Developing FinTech Ecosystems for Voluntary Carbon Markets Through Nature-Based Solutions: Opportunities and Barriers in ASEAN. In Green Digital Finance and Sustainable Development Goals. Edited by Farhad Taghizadeh-Hesary and Suk Hyun. Economics, Law, and Institutions in Asia Pacific. Singapore: Springer Nature, pp. 111–42. [Google Scholar] [CrossRef]

- De Almeida, Daniel, Luiz K. Hotta, and Esther Ruiz. 2018. MGARCH Models: Trade-off between Feasibility and Flexibility. International Journal of Forecasting 34: 45–63. [Google Scholar] [CrossRef]

- Elangovan, Rajesh, Francis Gnanasekar Irudayasamy, and Satyanarayana Parayitam. 2021. Testing the Market Efficiency in Indian Stock Market: Evidencefrom Bombay Stock Exchangebroad Market Indices. Journal of Economics, Finance and Administrative Science. [Google Scholar] [CrossRef]

- Engle, Robert. 2002. Dynamic Conditional Correlation: A Simple Class of Multivariate Generalized Autoregressive Conditional Heteroskedasticity Models. Journal of Business & Economic Statistics 20: 339–50. [Google Scholar]

- EY. 2022. How Is the Fintech Sector in India Poised for Exponential Growth? Available online: https://www.ey.com/en_in/financial-services/how-is-the-fintech-sector-in-india-poised-for-exponential-growth (accessed on 9 September 2022).

- Feyen, Erik, Jon Frost, Leonardo Gambacorta, Harish Natarajan, and Matthew Saal. 2021. Fintech and the Digital Transformation of Financial Services: Implications for Market Structure and Public Policy. BIS and World Bank Group. Available online: https://www.bis.org/publ/bppdf/bispap117.pdf (accessed on 27 August 2022).

- Fintech Insights. 2022. Performance of Public FinTechs Raises an Alarm: Is the FinTech Story Still Intact? Available online: https://www.rblt.com/fintech-insights/public-market-fintech-performance-raises-an-alarm-is-the-fintech-story-still-intact (accessed on 30 September 2022).

- Fouladi, Seyyed Hamed, and Hamidreza Amindavar. 2012. Blind Separation of Dependent Sources Using Multiwavelet Based on M-GARCH Model. Paper presented at IEEE 2012 11th International Conference on Information Science, Signal Processing and Their Applications (ISSPA), Montreal, QC, Canada, July 2–5; pp. 49–53. [Google Scholar] [CrossRef]

- Hinson, Robert, Robert Lensink, and Annika Mueller. 2019. Transforming Agribusiness in Developing Countries: SDGs and the Role of FinTech. Current Opinion in Environmental Sustainability 41: 1–9. [Google Scholar] [CrossRef]

- Horn, Matthias, Andreas Oehler, and Stefan Wendt. 2020. FinTech for Consumers and Retail Investors: Opportunities and Risks of Digital Payment and Investment Services. In Ecological, Societal, and Technological Risks and the Financial Sector. Edited by Thomas Walker, Dieter Gramlich, Mohammad Bitar and Pedram Fardnia. Palgrave Studies in Sustainable Business in Association with Future Earth. Cham: Springer International Publishing, pp. 309–27. [Google Scholar] [CrossRef]

- Invest India. 2022. Financial Services Sector in India|Fintech Industry in India. Available online: https://www.investindia.gov.in/sector/bfsi-fintech-financial-services (accessed on 27 September 2022).

- Investor’s Business Daily. 2022. Fintech Stocks to Buy: Acquirers Weather Market Rotation. Investor’s Business Daily. October 3. Available online: https://www.investors.com/news/technology/fintech-companies-to-buy-and-watch/ (accessed on 1 September 2022).

- Ionescu, Luminita. 2020. Digital Data Aggregation, Analysis, and Infrastructures in FinTech Operations. Review of Contemporary Philosophy 19: 92–98. [Google Scholar] [CrossRef]

- Janakiramanan, Sundaram, and Asjeet S. Lamba. 1998. An Empirical Examination of Linkages between Pacific-Basin Stock Markets. Journal of International Financial Markets, Institutions and Money 8: 155–73. [Google Scholar] [CrossRef]

- Kaur, Balijinder, Sood Kiran, Simon Grima, and Ramona Rupeika-Apoga. 2021. Digital Banking in Northern India: The Risks on Customer Satisfaction. Risks 9: 209. [Google Scholar] [CrossRef]

- Khan, Shahebaz Sarfaraz, Meer Mazhar Ali, and M. A. Imran Khan. 2022. Analyzing the Factors That Influence Capital Investment Decisions: A Case Study o f SME’s Listed on Bombay Stock Exchange. International Journal of Science and Research 11: 44–48. [Google Scholar] [CrossRef]

- Kroner, Kenneth F., and William D. Lastrapes. 1993. The Impact of Exchange Rate Volatility on International Trade: Reduced Form Estimates Using the GARCH-in-Mean Model. Journal of International Money and Finance 12: 298–318. [Google Scholar] [CrossRef]

- Kumar, Joseph John Allwyn, and Robiyanto Robiyanto. 2021. The Impact of Gold Price and Us Dollar Index: The Volatile Case of Shanghai Stock Exchange and Bombay Stock Exchange During the Crisis of COVID-19. Jurnal Keuangan Dan Perbankan 25: 508–31. [Google Scholar] [CrossRef]

- Laidroo, Laivi, Ekaterina Koroleva, Agata Kliber, Ramona Rupeika-Apoga, and Zana Grigaliuniene. 2021. Business Models of FinTechs—Difference in Similarity? Electronic Commerce Research and Applications 46: 101034. [Google Scholar] [CrossRef]

- Lee, David Kuo Chuen, and Ernie G. S. Teo. 2015. Emergence of Fintech and the Lasic Principles. SSRN Electronic Journal. [Google Scholar] [CrossRef]

- Li, Guozhong, Jian Sheng Dai, Eun-Mi Park, and Seong-Taek Park. 2017. A Study on the Service and Trend of Fintech Security Based on Text-Mining: Focused on the Data of Korean Online News. Journal of Computer Virology and Hacking Techniques 13: 249–55. [Google Scholar] [CrossRef]

- Morales, Lucía, Geraldine Gray, and Daniel Rajmil. 2022. Emerging Risks in the FinTech Industry—Insights from Data Science and Financial Econometrics Analysis. Economics, Management, and Financial Markets 17: 9. [Google Scholar] [CrossRef]

- Mubarak, Muhammad Faraz, and Monika Petraite. 2020. Industry 4.0 Technologies, Digital Trust and Technological Orientation: What Matters in Open Innovation? Technological Forecasting and Social Change 161: 120332. [Google Scholar] [CrossRef]

- Najeeb, Syed Faiq, Obiyathulla Bacha, and Mansur Masih. 2015. Does Heterogeneity in Investment Horizons Affect Portfolio Diversification? Some Insights Using M-GARCH-DCC and Wavelet Correlation Analysis. Emerging Markets Finance and Trade 51: 188–208. [Google Scholar] [CrossRef]

- Nayer, C. P. S. 1986. Can a traditional financial technology co-exist with modern financial technologies? Savings and Development 10: 31–58. [Google Scholar]

- Ng, Hs Raymond, and Kai-Pui Lam. 2006. How Does the Sample Size Affect GARCH Model? Paper presented at 9th Joint Conference on Information Sciences (JCIS 2006), Kaohsiung, Taiwan, October 8–11; pp. 3–6. [Google Scholar] [CrossRef]

- Niyogin Fintech Ltd. 2022. Available online: https://www.niyogin.com/ (accessed on 25 August 2022).

- Oehler, Andreas, Matthias Horn, and Stefan Wendt. 2021. Investor Characteristics and Their Impact on the Decision to Use a Robo-Advisor. Journal of Financial Services Research 62: 91–125. [Google Scholar] [CrossRef]

- Panda, Ajaya Kumar, and Swagatika Nanda. 2018. A GARCH Modelling of Volatility and M-GARCH Approach of Stock Market Linkages of North America. Global Business Review 19: 1538–53. [Google Scholar] [CrossRef]

- PitchBook. 2022a. PolicyBazaar Company Profile. Available online: https://pitchbook.com/profiles/company/54757-00 (accessed on 27 October 2022).

- PitchBook. 2022b. Polo Queen Industrial Company Profile. Available online: https://pitchbook.com/profiles/company/187485-67 (accessed on 27 October 2022).

- Popova, Yelena. 2021. Economic Basis of Digital Banking Services Produced by FinTech Company in Smart City. Journal of Tourism and Services 12: 86–104. [Google Scholar] [CrossRef]

- Rupeika-Apoga, Ramona, and Eleftherios I. Thalassinos. 2020. Ideas for a Regulatory Definition of FinTech. International Journal of Economics and Business Administration VIII: 136–54. [Google Scholar] [CrossRef]

- Rupeika-Apoga, Ramona, and Stefan Wendt. 2022. FinTech Development and Regulatory Scrutiny: A Contradiction? The Case of Latvia. Risks 10: 167. [Google Scholar] [CrossRef]

- Scheicher, Martin. 2001. The Comovements of Stock Markets in Hungary, Poland and the Czech Republic. International Journal of Finance & Economics 6: 27–39. [Google Scholar] [CrossRef]

- Singh, Manvendra Pratap, Arpita Chakraborty, Mousumi Roy, and Avinash Tripathi. 2021. Developing SME Sustainability Disclosure Index for Bombay Stock Exchange (BSE) Listed Manufacturing SMEs in India. Environment, Development and Sustainability 23: 399–422. [Google Scholar] [CrossRef]

- Sotiropoulou, Georgia, Georgios Pampalakis, and Eleftherios P. Diamandis. 2009. Functional Roles of Human Kallikrein-Related Peptidases. Journal of Biological Chemistry 284: 32989–94. [Google Scholar] [CrossRef] [PubMed]

- Srivastava, Aman, Shikha Bhatia, and Prashant Gupta. 2015. Financial Crisis and Stock Market Integration: An Analysis of Select Economies. Global Business Review 16: 1127–42. [Google Scholar] [CrossRef]

- Statista. 2022. Fintech in India. Statista. Available online: https://www.statista.com/topics/5666/fintech-in-india/ (accessed on 15 August 2022).

- Tanda, Alessandra, and Cristiana-Maria Schena. 2019. FinTech, BigTech and Banks: Digitalisation and Its Impact on Banking Business Models. Palgrave Macmillan Studies in Banking and Financial Institutions. Cham: Palgrave Macmillan. [Google Scholar] [CrossRef]

- Varma, Parminder, Shivinder Nijjer, Kiran Sood, Simon Grima, and Ramona Rupeika-Apoga. 2022. Thematic Analysis of Financial Technology (Fintech) Influence on the Banking Industry. Risks 10: 186. [Google Scholar] [CrossRef]

- Vasenska, Ivanka, Preslav Dimitrov, Blagovesta Koyundzhiyska-Davidkova, Vladislav Krastev, Pavol Durana, and Ioulia Poulaki. 2021. Financial Transactions Using Fintech during the COVID-19 Crisis in Bulgaria. Risks 9: 48. [Google Scholar] [CrossRef]

- Wei, Shaobo, Dabao Xu, and Hua Liu. 2022. The Effects of Information Technology Capability and Knowledge Base on Digital Innovation: The Moderating Role of Institutional Environments. European Journal of Innovation Management 25: 720–40. [Google Scholar] [CrossRef]

- Wonglimpiyarat, Jarunee. 2018. Challenges and Dynamics of FinTech Crowd Funding: An Innovation System Approach. The Journal of High Technology Management Research 29: 98–108. [Google Scholar] [CrossRef]

- Wu, Wuqing, Dongliang Xu, Yue Zhao, and Xinhai Liu. 2020. Do Consumer Internet Behaviours Provide Incremental Information to Predict Credit Default Risk? Economic and Political Studies 8: 482–99. [Google Scholar] [CrossRef]

- Xu, Zhong, and Chuanwei Zou. 2022. Fintech: Frontier and Beyond, 1st ed. London: Routledge. [Google Scholar] [CrossRef]

- Zalan, Tatiana, and Elissar Toufaily. 2017. The Promise of Fintech in Emerging Markets: Not as Disruptive. Contemporary Economics 11: 415–430. Available online: https://papers.ssrn.com/abstract=3200954 (accessed on 18 September 2022).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| t-Statistic | Prob. | ||

|---|---|---|---|

| Augmented Dickey–Fuller test statistic | 5.313794 | 0.0000 | |

| Test critical values: | 1% level | 3.437426 | |

| 5% level | 2.864553 | ||

| 10% level | 2.568427 | ||

| Variable | Coefficient | Std. Error | t-Statistic | Prob. |

|---|---|---|---|---|

| RETURN(−1) | −0.813562 | 0.153104 | −5.313794 | 0.0000 |

| D(RETURN(−1)) | −0.774386 | 0.149580 | −5.177083 | 0.0000 |

| D(RETURN(−2)) | −1.066055 | 0.146537 | −7.274982 | 0.0000 |

| D(RETURN(−3)) | −1.209492 | 0.143531 | −8.426708 | 0.0000 |

| D(RETURN(−4)) | −1.146063 | 0.139377 | −8.222740 | 0.0000 |

| D(RETURN(−5)) | −1.097207 | 0.132485 | −8.281762 | 0.0000 |

| D(RETURN(−6)) | −0.910645 | 0.121602 | −7.488740 | 0.0000 |

| D(RETURN(−7)) | −0.769113 | 0.106693 | −7.208654 | 0.0000 |

| D(RETURN(−8)) | −0.568617 | 0.086165 | −6.599186 | 0.0000 |

| D(RETURN(−9)) | −0.368982 | 0.061599 | −5.990065 | 0.0000 |

| D(RETURN(−10)) | −0.175751 | 0.033110 | −5.308097 | 0.0000 |

| C | 0.832868 | 0.156859 | 5.309644 | 0.0000 |

| R-squared | 0.762460 | Mean dependent var | 4.28 × 10−6 | |

| Adjusted R-squared | 0.759505 | S.D. dependent var | 0.391822 | |

| S.E. of regression | 0.192151 | Akaike info criterion | −0.447769 | |

| Sum squared resid | 32.63903 | Schwarz criterion | −0.383511 | |

| Log likelihood | 212.6005 | Hannan-Quinn criter. | −0.423217 | |

| F-statistic | 257.9532 | Durbin-Watson stat | 2.006463 | |

| Prob(F-statistic) | 0.000000 | |||

| Variable | Coefficient | Std. Error | t-Statistic | Prob. |

|---|---|---|---|---|

| C | 3.14 × 10−6 | 2.70 × 10−5 | 0.116343 | 0.9074 |

| AR(1) | −0.519600 | 0.017158 | −30.28302 | 0.0000 |

| MA(1) | −1.000000 | 7.329339 | −0.136438 | 0.8915 |

| SIGMASQ | 0.031587 | 0.005246 | 6.021269 | 0.0000 |

| R-squared | 0.760349 | Mean dependent var | 5.95 × 10−6 | |

| Adjusted R-squared | 0.759552 | S.D. dependent var | 0.363248 | |

| S.E. of regression | 0.178121 | Akaike info criterion | −0.599520 | |

| Sum squared resid | 28.61769 | Schwarz criterion | −0.578288 | |

| Log likelihood | 275.5827 | Hannan–Quinn criter. | −0.591412 | |

| F-statistic | 953.9377 | Durbin–Watson stat | 2.262986 | |

| Prob(F-statistic) | 0.000000 | |||

| Inverted AR Roots | −0.52 | |||

| Inverted MA Roots | 1.00 | |||

| F-statistic | 84.54389 | Prob. F(2,901) | 0.0000 | |

| Obs*R-squared | 142.8438 | Prob. Chi-Square(2) | 0.0000 | |

| Test Equation: | ||||

| Dependent Variable: RESID^2 | ||||

| Method: Least Squares | ||||

| Date: 22 September 2022 Time: 10:08 | ||||

| Sample (adjusted): 7 January 2019–21 September 2022 | ||||

| Included observations: 904 after adjustments | ||||

| Variable | Coefficient | Std. Error | t-Statistic | Prob. |

| C | 0.016113 | 0.002848 | 5.656841 | 0.0000 |

| RESID(−1)^2 | 0.185374 | 0.031721 | 5.843919 | 0.0000 |

| RESID(−2)^2 | 0.305616 | 0.031721 | 9.634534 | 0.0000 |

| R-squared | 0.158013 | Mean dependent var | 0.031656 | |

| Adjusted R-squared | 0.156144 | S.D. dependent var | 0.084311 | |

| S.E. of regression | 0.077449 | Akaike info criterion | −2.275074 | |

| Sum squared resid | 5.404552 | Schwarz criterion | −2.259122 | |

| Log likelihood | 1031.333 | Hannan–Quinn criter. | −2.268981 | |

| F-statistic | 84.54389 | Durbin–Watson stat | 2.064221 | |

| Prob(F-statistic) | 0.000000 | |||

| Variable | Coefficient | Std. Error | z-Statistic | Prob. |

|---|---|---|---|---|

| C | 0.000297 | 0.027199 | 0.010922 | 0.9913 |

| AR(1) | −0.309213 | 0.219286 | −1.410090 | 0.1585 |

| MA(1) | −0.305138 | 0.280940 | −1.086130 | 0.2774 |

| Variance Equation | ||||

| C | 0.131948 | 0.135561 | 0.973351 | 0.3304 |

| RESID(−1)^2 | 0.150000 | 0.176532 | 0.849704 | 0.3955 |

| GARCH(−1) | 0.600000 | 0.391528 | 1.532459 | 0.1254 |

| T-DIST. DOF | 19.87092 | 101.5485 | 0.195679 | 0.8449 |

| R-squared | 0.517457 | Mean dependent var | −2.67 × 10−5 | |

| Adjusted R-squared | 0.516387 | S.D. dependent var | 0.363448 | |

| S.E. of regression | 0.252750 | Akaike info criterion | 0.905366 | |

| Sum squared resid | 57.62205 | Schwarz criterion | 0.942554 | |

| Log likelihood | −402.6781 | Hannan–Quinn criter. | 0.919568 | |

| Durbin–Watson stat | 2.917639 | |||

| Inverted AR Roots | −0.31 | |||

| Inverted MA Roots | 0.31 | |||

| Variable | Coefficient | Std. Error | z-Statistic | Prob. |

|---|---|---|---|---|

| GARCH | 0.000555 | 0.000251 | 2.209806 | 0.0271 |

| C | −8.41 × 10−5 | 3.31 × 10−5 | −2.543014 | 0.0110 |

| AR(1) | −0.241525 | 0.035507 | −6.802208 | 0.0000 |

| MA(1) | −0.992338 | 0.004089 | −242.6798 | 0.0000 |

| Variance Equation | ||||

| C | 1.208346 | 0.644220 | 1.875674 | 0.0607 |

| RESID(−1)^2 | 1124.257 | 540.7955 | 2.078894 | 0.0376 |

| GARCH(−1) | 0.291233 | 0.033948 | 8.578811 | 0.0000 |

| T-DIST. DOF | 2.000462 | 0.000199 | 10,053.79 | 0.0000 |

| R-squared | 0.760140 | Mean dependent var | −2.67 × 10−5 | |

| Adjusted R-squared | 0.759341 | S.D. dependent var | 0.363448 | |

| S.E. of regression | 0.178297 | Akaike info criterion | −1.737947 | |

| Sum squared resid | 28.64252 | Schwarz criterion | −1.695446 | |

| Log likelihood | 794.4212 | Hannan–Quinn criter. | −1.721716 | |

| Durbin–Watson stat | 2.395802 | |||

| Inverted AR Roots | −0.24 | |||

| Inverted MA Roots | 0.99 | |||

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Bhatnagar, M.; Özen, E.; Taneja, S.; Grima, S.; Rupeika-Apoga, R. The Dynamic Connectedness between Risk and Return in the Fintech Market of India: Evidence Using the GARCH-M Approach. Risks 2022, 10, 209. https://doi.org/10.3390/risks10110209

Bhatnagar M, Özen E, Taneja S, Grima S, Rupeika-Apoga R. The Dynamic Connectedness between Risk and Return in the Fintech Market of India: Evidence Using the GARCH-M Approach. Risks. 2022; 10(11):209. https://doi.org/10.3390/risks10110209

Chicago/Turabian StyleBhatnagar, Mukul, Ercan Özen, Sanjay Taneja, Simon Grima, and Ramona Rupeika-Apoga. 2022. "The Dynamic Connectedness between Risk and Return in the Fintech Market of India: Evidence Using the GARCH-M Approach" Risks 10, no. 11: 209. https://doi.org/10.3390/risks10110209

APA StyleBhatnagar, M., Özen, E., Taneja, S., Grima, S., & Rupeika-Apoga, R. (2022). The Dynamic Connectedness between Risk and Return in the Fintech Market of India: Evidence Using the GARCH-M Approach. Risks, 10(11), 209. https://doi.org/10.3390/risks10110209