Wealth Status and Health Insurance Enrollment in India: An Empirical Analysis

Abstract

1. Introduction

2. Materials and Methods

2.1. Data

2.2. Description of the Variables

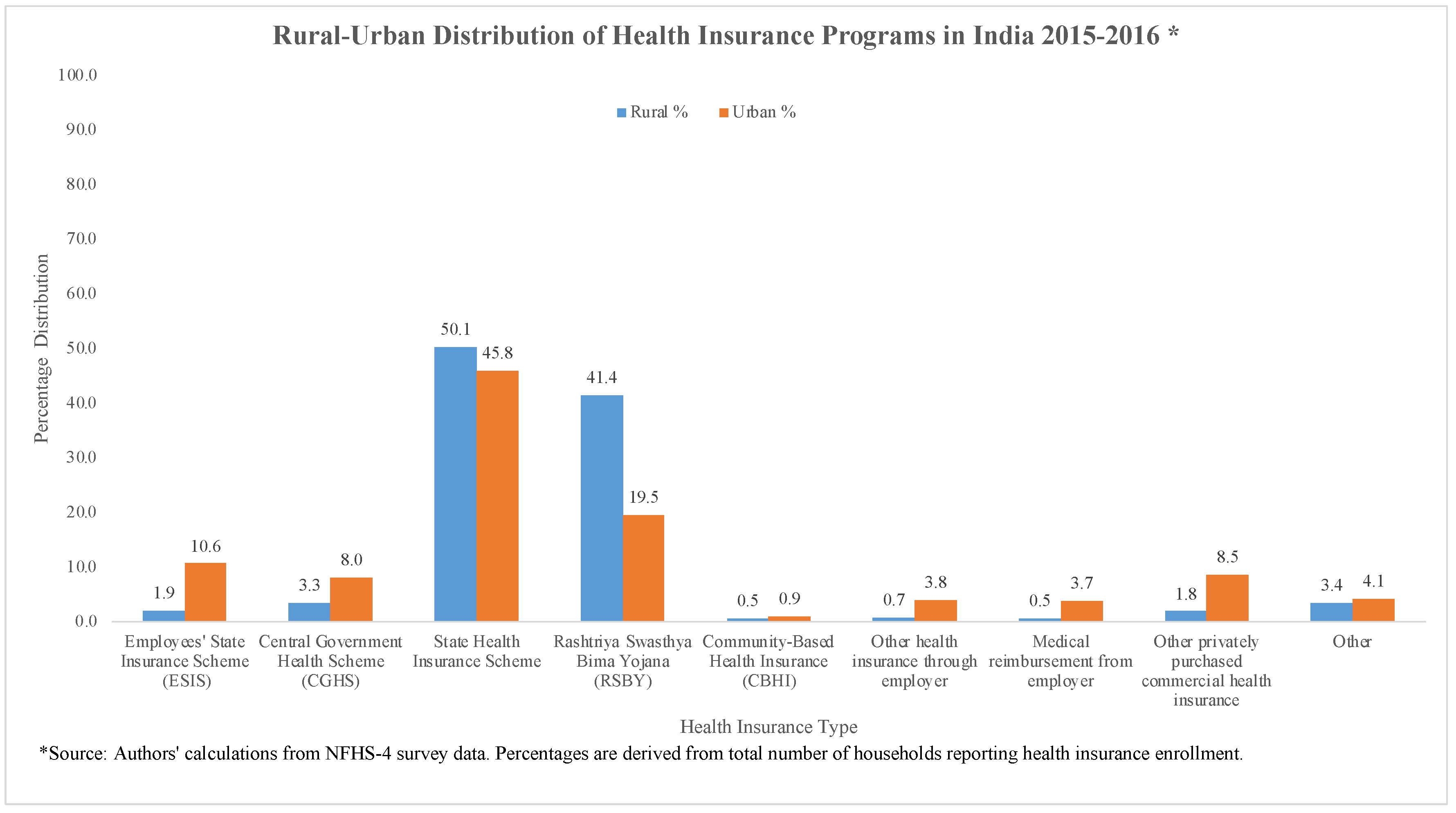

2.2.1. Health Insurance Enrollment

2.2.2. Explanatory Variables

2.3. Empirical Strategy

3. Results

3.1. Determinants of HI Enrollment

3.1.1. Role of Household Wealth

3.1.2. Role of Media

3.1.3. Role of Dependency Variables

3.1.4. Role of Caste

3.1.5. Role of Other Control Variables

3.2. Determinants of HI Enrollment by Schemes

3.2.1. Role of Household Wealth

3.2.2. Role of Media

3.2.3. Role of Dependency Variables

3.2.4. Role of Caste

3.2.5. Role of Other Control Variables

4. Discussion

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

| Variable Abbreviation | Definition |

|---|---|

| HI | Dummy variable for any usual member in the household has health insurance (0 = not enrolled, 1 = enrolled in HI). |

| HI Type | 0 = No-insurance, 1 = Employer-based, 2 = Publicly funded HI, 3 = Private HI, 4 = Other |

| Household Asset | 0 = Low Asset, 1 = Medium Asset, 2 = High Asset |

| Newspaper | Dummy variable for reading newspaper (0 = does not read newspaper, 1 = read newspaper) |

| Radio | Dummy variable for listening to radio (0 = does not listen radio, 1 = listen radio) |

| Television | Dummy variable for watching TV (0 = does not want TV, 1 = watch TV) |

| # Above 60 | Number of members in HH above age 60 years |

| # between 0 and 5 | Number of members in HH between ages 0 and 5 years |

| # between 6 and 15 | Number of members in HH between ages 6 and 15 years |

| SC | Dummy for Scheduled Caste (0 = non-SC, 1 = SC) |

| ST | Dummy for Scheduled Tribe (0 = non-ST, 1 = ST) |

| OBC | Dummy for Other Backward Caste (0 = non-OBC, 1 = OBC) |

| Hindu | Dummy for Hindu (0 = non-Hindu, 1 = Hindu) |

| Muslim | Dummy for Muslim (0 = non-Muslim, 1 = Muslim) |

| Female-headed HH | Dummy for female-headed household (0 = Male-headed, 1 = Female-headed) |

| HH head’s Age | Age of the household head in years |

| HH head’s education | No. of years of education of household head (Education in years) |

| Agriculture: Male | Dummy for any married man in the household works in the agricultural sector (0 = does not work in agriculture, 1 = work in agriculture) |

| Non-Agriculture: Male | Dummy for any married man in the household works in the non-agricultural sector (0 = does not work in non-agriculture, 1 = work in non-agriculture) |

| Agriculture: Female | Dummy for any woman (aged 15–49 years) in the household works in the agricultural sector (0 = does not work in agriculture, 1 = work in agriculture) |

| Non-Agriculture: Female | Dummy for any woman (aged 15–49 years) in the household works in the non-agricultural sector (0 = does not work in non-agriculture, 1 = work in non-agriculture) |

| Region | Dummy for Urban area (0 = Rural, 1 = Urban) |

| State | State dummies (0 = Karnataka, 1 = Resident of state) |

Appendix B

| ||

|---|---|---|

| Chakravarti and Shankar [15] | Our Study | |

| Household Asset Variables | ||

| Medium Asset | (+) *** in urban, rural, and overall samples | (−) |

| High Asset | (+) *** in urban, rural, and overall samples | (+) * in overall sample |

| Media Exposure Variables | ||

| Newspaper | (+) ** in urban, rural, and overall samples | (+) * in urban and overall samples |

| Radio | (+) ** in urban and overall samples | (+/−) |

| Television | (+) ** in urban, rural, and overall samples | (+) *** in rural and overall samples |

| Dependency Variables | ||

| High Asset * # above 60 | (+/−) | (−) |

| # above 60 | (+/−) | (+) ** in urban, rural, and overall samples |

| # between 0 and 5 | (+/−) | (−) *** in urban and overall samples |

| # between 6 and 15 | (+) | (+) * in rural sample |

| Caste | ||

| SC | (−) | (+) *** in rural and overall samples |

| ST | (+/−) | (+) *** in rural and overall samples |

| OBC | (+/−) | (+/−) |

| SC * Medium Asset | (+) * in rural and overall samples | (+/−) |

| SC * High Asset | (+) * in rural and overall samples | (−) ** in overall sample |

| ST * Medium Asset | (+/−) | (+) |

| ST * High Asset | (−) * in overall | (−) ** in overall sample |

| OBC * Medium Asset | (+) | (+) |

| OBC * High Asset | (−) | (−) ** in overall sample |

| Control Variables | ||

| Hindu | (+) *** in urban, rural, and overall samples | (+) * in rural sample |

| Muslim | (−) ** in urban and overall samples | (−) * in urban sample |

| Female-headed HH | (+/−) | (−) |

| HH head’s age | (+) *** in urban, rural, and overall samples | (+) *** in urban, rural, and overall samples |

| HH head’s education | (+) *** in urban, rural, and overall samples | (+) * in urban sample |

| Agriculture: Male | (+) * in overall sample | (+/−) |

| Non-Agriculture: Male | (+) *** in urban and overall samples | (+) |

| Agriculture: Female | (+) ** in rural and overall samples | (+) *** in rural and overall samples |

| Non-Agriculture: Female | (+) * in rural | (+) *** in urban, rural, and overall samples |

| Region | (+) * | (−) *** |

| ||

| Outcome 1: Public HI | ||

| Chakravarti and Shankar [15] | Our Study | |

| Household Asset Variables | ||

| Medium Asset | (+) *** in urban, rural, and overall samples | (−) |

| High Asset | (+) *** in urban, rural, and overall samples | (−) |

| Media Exposure Variables | ||

| Newspaper | (+/−) | (+) |

| Radio | (+/−) | (−) |

| Television | (+) * in rural | (+) *** in rural and overall samples |

| Dependency Variables | ||

| High Asset * # above 60 | (+/−) | (−) |

| # above 60 | (−) | (+) * in rural and overall samples |

| # between 0 and 5 | (−) * in urban | (−) *** in urban and overall sample |

| # between 6 and 15 | (+/−) | (+) ** in rural and overall samples |

| Caste | ||

| SC | (−) | (+) ** in rural and overall samples |

| ST | (+) | (+) * in rural |

| OBC | (−) * in urban | (+/−) |

| SC * Medium Asset | (+) * in overall | (+/−) |

| SC * High Asset | (+) *** in rural and overall samples | (+/−) |

| ST * Medium Asset | (+/−) | (+) |

| ST * High Asset | (−) | (+/−) |

| OBC * Medium Asset | (+) | (+) |

| OBC * High Asset | (+) | (+) |

| Control Variables | ||

| Hindu | (+) *** in urban, rural, and overall samples | (+) * in rural |

| Muslim | (−) | (+/−) |

| Female-headed HH | (−) | (−) |

| HH head’s age | (+) *** in urban, rural, and overall samples | (+) *** in rural and overall samples |

| HH head’s education | (+) *** in urban, rural, and overall samples | (−) * in overall |

| Agriculture: Male | (−) | (−) |

| Non-Agriculture: Male | (+) * in urban and overall samples | (+) |

| Agriculture: Female | (+) | (+) *** in rural and overall samples |

| Non-Agriculture: Female | (+/−) | (+) *** in rural and overall samples |

| Region | (+) ** | (−) *** |

| Outcome 2: CBHI | ||

| Chakravarti and Shankar [15] | Our Study | |

| Household Asset Variables | ||

| Medium Asset | (+) * in rural | (+) *** in urban |

| High Asset | (+) | (+) *** in urban |

| Media Exposure Variables | ||

| Newspaper | (+) * in urban | (+) |

| Radio | (+/−) | (−) *** in rural |

| Television | (+) *** rural and overall samples | (−) |

| Dependency Variables | ||

| High Asset * # above 60 | (+/−) | (+/−) |

| # above 60 | (+/−) | (+/−) |

| # between 0 and 5 | (+/−) | (+/−) |

| # between 6 and 15 | (+/−) | (+/−) |

| Caste | ||

| SC | (−) | (+) *** in urban |

| ST | (−) | (−) |

| OBC | (+/−) | (+) *** in urban |

| SC * Medium Asset | (+/−) | (−) *** in urban |

| SC * High Asset | (−) *** in rural | (−) *** in urban |

| ST * Medium Asset | (−) | (+) * in rural and overall samples |

| ST * High Asset | (+/−) | (−) *** in rural |

| OBC * Medium Asset | (+) | (−) *** in urban, (+) * in rural samples |

| OBC * High Asset | (+) | (−) *** in urban |

| Control Variables | ||

| Hindu | (+) * in overall | (−) |

| Muslim | (−) | (−) ** in urban |

| Female-headed HH | (+/−) | (+) |

| HH head’s age | (+) | (+) *** rural and overall samples |

| HH head’s education | (+) *** in urban, rural, and overall samples | (+/−) |

| Agriculture: Male | (+) * in overall | (+) |

| Non-Agriculture: Male | (+/−) | (+/−) |

| Agriculture: Female | (+) | (+/−) |

| Non-Agriculture: Female | (+) *** in rural and overall samples | (+/−) |

| Region | (−) | (+) |

| Outcome 3: Private HI | ||

| Chakravarti and Shankar [15] | Our Study | |

| Household Asset Variables | ||

| Medium Asset | (+) *** in urban, rural, and overall samples | (+) *** in urban, rural, and overall samples |

| High Asset | (+) *** in urban, rural, and overall samples | (+) *** in urban, rural, and overall samples |

| Media Exposure Variables | ||

| Newspaper | (+) *** in urban, rural, and overall samples | (+) * in urban and overall samples |

| Radio | (+) *** in urban and overall samples | (+) |

| Television | (+) *** in urban, rural, and overall samples | (+) * in urban |

| Dependency Variables | ||

| High Asset * # above 60 | (+/−) | (+/−) |

| # above 60 | (+) * in overall | (+/−) |

| # between 0 and 5 | (−) | (−) |

| # between 6 and 15 | (+/−) | (−) |

| Caste | ||

| SC | (+/−) | (+) ** in urban |

| ST | (+/−) | (+/−) |

| OBC | (+) | (+) *** in urban, rural, and overall samples |

| SC * Medium Asset | (+/−) | (−) *** in urban |

| SC * High Asset | (+/−) | (−) *** in urban |

| ST * Medium Asset | (+/−) | (+) |

| ST * High Asset | (−) * in overall | (−) * in urban and overall samples |

| OBC * Medium Asset | (−) * in urban | (−) * in urban |

| OBC * High Asset | (−) ** in urban and overall samples | (−) * in urban and overall samples |

| Control Variables | ||

| Hindu | (+) | (+) |

| Muslim | (−) ** in urban and overall | (−) |

| Female-headed HH | (+/−) | (−) |

| HH head’s age | (+) ** in rural and overall samples | (+/−) |

| HH head’s education | (+) *** in urban, rural, and overall samples | (+) *** in urban, rural, and overall samples |

| Agriculture: Male | (+) | (+/−) |

| Non-Agriculture: Male | (+) ** in urban and overall samples | (+) * in urban and overall samples |

| Agriculture: Female | (+) ** in overall | (+/−) |

| Non-Agriculture: Female | (+) | (+) |

| Region | (+) ** | (+) * |

| Outcome 4: Other | ||

| Chakravarti and Shankar [15] | Our Study | |

| Household Asset Variables | ||

| Medium Asset | (+) | (−) |

| High Asset | (+) | (+/−) |

| Media Exposure Variables | ||

| Newspaper | (+) * in overall | (+) * in rural and overall samples |

| Radio | (+) * in overall | (+/−) |

| Television | (+) | (+) |

| Dependency Variables | ||

| High Asset * # above 60 | (+) | (+) |

| # above 60 | (−) | (+) * in rural and overall samples |

| # between 0 and 5 | (+) | (+/−) |

| # between 6 and 15 | (+) | (+) |

| Caste | ||

| SC | (−) | (+) |

| ST | (−) | (+) |

| OBC | (−) | (+) |

| SC * Medium Asset | (+) | (−) * in overall |

| SC * High Asset | (+) | (−) * in overall |

| ST * Medium Asset | (−) | (−) |

| ST * High Asset | (+) | (+/−) |

| OBC * Medium Asset | (+) | (−) |

| OBC * High Asset | (+) | (+/−) |

| Control Variables | ||

| Hindu | (+/−) | (−) * in overall |

| Muslim | (−) | (−) ** in overall |

| Female-headed HH | (+/−) | (+) |

| HH head’s age | (+) | (+) ** in overall |

| HH head’s education | (+) * in rural and overall samples | (+) * in rural |

| Agriculture: Male | (+) | (+/−) |

| Non-Agriculture: Male | (+/−) | (+) |

| Agriculture: Female | (+) | (+) |

| Non-Agriculture: Female | (+) | (+) |

| Region | (−) ** | (−) |

Appendix C

| Outcome 1: Public H.I. | ||||||

|---|---|---|---|---|---|---|

| Urban | Rural | Combined | ||||

| RRR | p-Value † | RRR | p-Value † | RRR | p-Value † | |

| Household Asset Variables | ||||||

| Medium Asset | 0.579 | 0.096 | 1.002 | 0.989 | 0.925 | 0.469 |

| High Asset | 0.608 | 0.114 | 0.824 | 0.131 | 0.876 | 0.243 |

| Media Exposure Variables | ||||||

| Newspaper | 1.044 | 0.480 | 1.009 | 0.828 | 1.02 | 0.552 |

| Radio | 0.983 | 0.840 | 0.971 | 0.547 | 0.973 | 0.554 |

| Television | 1.172 | 0.196 | 1.217 | 0.000 *** | 1.242 | 0.000 *** |

| Dependency Variables | ||||||

| Highest Asset * # above 60 years | 0.871 | 0.273 | 0.992 | 0.926 | 0.943 | 0.420 |

| # above 60 years | 1.127 | 0.190 | 1.087 | 0.018 * | 1.085 | 0.019 * |

| # between 0 and 5 years | 0.844 | 0.000 *** | 0.971 | 0.131 | 0.933 | 0.000 *** |

| # between 6 and 15 years | 1.013 | 0.642 | 1.038 | 0.006 ** | 1.029 * | 0.026 |

| Caste | ||||||

| SC | 0.755 | 0.381 | 1.426 | 0.000 *** | 1.328 ** | 0.005 |

| ST | 0.794 | 0.490 | 1.255 | 0.024 * | 1.191 | 0.078 |

| OBC | 0.827 | 0.574 | 1.071 | 0.468 | 1.046 | 0.635 |

| SC * Medium Asset | 1.489 | 0.266 | 0.949 | 0.697 | 0.961 | 0.751 |

| SC * High Asset | 1.484 | 0.265 | 1.008 | 0.963 | 0.921 | 0.578 |

| ST * Medium Asset | 1.51 | 0.341 | 1.043 | 0.811 | 1.062 | 0.705 |

| ST * High Asset | 1.819 | 0.110 | 0.836 | 0.377 | 1.066 | 0.709 |

| OBC * Medium Asset | 1.519 | 0.251 | 1.016 | 0.897 | 1.092 | 0.453 |

| OBC * High Asset | 1.254 | 0.515 | 1.138 | 0.341 | 0.996 | 0.973 |

| Control Variables | ||||||

| Hindu | 0.906 | 0.434 | 1.315 | 0.005 ** | 1.128 | 0.116 |

| Muslim | 0.855 | 0.297 | 1.195 | 0.157 | 1.063 | 0.530 |

| Female-headed HH | 0.891 | 0.190 | 0.97 | 0.536 | 0.937 | 0.146 |

| HH head’s age | 1.027 | 0.192 | 1.098 | 0.000 *** | 1.073 | 0.000 *** |

| Age square | 1.000 | 0.346 | 0.999 | 0.000 *** | 0.999 | 0.000 *** |

| HH head’s education | 0.993 | 0.288 | 0.993 | 0.101 | 0.992 * | 0.044 |

| Agriculture: Male | 0.953 | 0.764 | 0.988 | 0.858 | 0.986 | 0.824 |

| Non-Agriculture: Male | 1.05 | 0.681 | 1.034 | 0.608 | 1.04 | 0.493 |

| Agriculture: Female | 1.08 | 0.554 | 1.208 | 0.000 *** | 1.201 | 0.000 *** |

| Non-Agriculture: Female | 1.119 | 0.080 | 1.187 | 0.000 *** | 1.165 | 0.000 *** |

| Region | NA | NA | NA | NA | 0.718 | 0.000 *** |

| Outcome 2: CBHI | ||||||

| Urban | Rural | Combined | ||||

| RRR | p-Value † | RRR | p-Value † | RRR | p-Value † | |

| Household Asset Variables | ||||||

| Medium Asset | NA | NA | 0.238 | 0.188 | 0.322 | 0.210 |

| High Asset | NA | NA | 0.482 | 0.296 | 1.029 | 0.967 |

| Media Exposure Variables | ||||||

| Newspaper | NA | NA | 1.648 | 0.210 | 1.831 | 0.076 |

| Radio | NA | NA | 0.093 | 0.000 *** | 0.606 | 0.222 |

| Television | NA | NA | 0.825 | 0.668 | 0.547 | 0.135 |

| Dependency Variables | ||||||

| Highest Asset * # above 60 years | NA | NA | 1.97 | 0.307 | 0.893 | 0.844 |

| # above 60 years | NA | NA | 0.917 | 0.816 | 0.904 | 0.751 |

| # between 0 and 5 years | NA | NA | 1.147 | 0.340 | 1.228 | 0.138 |

| # between 6 and 15 years | NA | NA | 0.901 | 0.507 | 0.958 | 0.728 |

| Caste | ||||||

| SC | NA | NA | 0.41 | 0.235 | 0.419 | 0.243 |

| ST | NA | NA | 0.117 | 0.077 | 0.117 | 0.070 |

| OBC | NA | NA | 0.336 | 0.133 | 0.496 | 0.342 |

| SC * Medium Asset | NA | NA | 1.854 | 0.703 | 6.429 | 0.168 |

| SC * High Asset | NA | NA | 3.984 | 0.219 | 1.279 | 0.803 |

| ST * Medium Asset | NA | NA | 73.767 | 0.017 * | 39.558 | 0.033 * |

| ST * High Asset | NA | NA | 0.003 | 0.000 *** | 11.838 | 0.071 |

| OBC * Medium Asset | NA | NA | 12.383 | 0.048 * | 7.16 | 0.062 |

| OBC * High Asset | NA | NA | 2.811 | 0.297 | 1.791 | 0.492 |

| Control Variables | ||||||

| Hindu | NA | NA | 0.864 | 0.773 | 0.869 | 0.819 |

| Muslim | NA | NA | 0.486 | 0.380 | 0.334 | 0.193 |

| Female-headed HH | NA | NA | 1.486 | 0.489 | 1.127 | 0.793 |

| HH head’s age | NA | NA | 1.165 | 0.182 | 1.296 | 0.017 * |

| Age square | NA | NA | 0.998 | 0.189 | 0.998 * | 0.026 |

| HH head’s education | NA | NA | 1.009 | 0.847 | 1.035 | 0.331 |

| Agriculture: Male | NA | NA | 2.478 | 0.066 | 1.558 | 0.277 |

| Non-Agriculture: Male | NA | NA | 1.18 | 0.738 | 0.769 | 0.519 |

| Agriculture: Female | NA | NA | 0.566 | 0.251 | 0.584 | 0.219 |

| Non-Agriculture: Female | NA | NA | 0.291 | 0.098 | 1.083 | 0.835 |

| Region | NA | NA | NA | NA | 1.324 | 0.436 |

| Outcome 3: Private H.I. | ||||||

| Urban | Rural | Combined | ||||

| RRR | p-Value † | RRR | p-Value † | RRR | p-Value † | |

| Household Asset Variables | ||||||

| Medium Asset | 293,78.175 | 0.000 *** | 4.261 | 0.005 ** | 3.514 | 0.010 * |

| High Asset | 260,436.027 | 0.000 *** | 11.322 | 0.000 *** | 18.110 | 0.000 *** |

| Media Exposure Variables | ||||||

| Newspaper | 1.471 | 0.026 * | 1.32 | 0.083 | 1.428 | 0.003 *** |

| Radio | 1.229 | 0.179 | 1.169 | 0.405 | 1.178 | 0.184 |

| Television | 3.455 | 0.020 * | 0.909 | 0.727 | 1.488 | 0.083 |

| Dependency Variables | ||||||

| Highest Asset * # above 60 years | 0.946 | 0.821 | 1.23 | 0.437 | 1.062 | 0.728 |

| # above 60 years | 1.227 | 0.248 | 0.905 | 0.555 | 1.061 | 0.625 |

| # between 0 and 5 years | 0.904 | 0.424 | 0.936 | 0.414 | 0.913 | 0.301 |

| # between 6 and 15 years | 0.95 | 0.448 | 0.946 | 0.422 | 0.945 | 0.269 |

| Caste | ||||||

| SC | 37,418.294 | 0.000 *** | 1.965 | 0.321 | 2.632 | 0.118 |

| ST | 0.965 | 0.905 | 1.192 | 0.775 | 1.738 | 0.365 |

| OBC | 39,774.466 | 0.000 *** | 2.724 | 0.045 * | 3.587 | 0.009 ** |

| SC * Medium Asset | 0.000 | 0.000 *** | 0.348 | 0.178 | 0.372 | 0.156 |

| SC * High Asset | 0.000 | 0.000 *** | 0.337 | 0.174 | 0.223 | 0.021 * |

| ST * Medium Asset | 2.75 | 0.126 | 1.245 | 0.725 | 1.131 | 0.842 |

| ST * High Asset | 0.216 | 0.001 ** | 0.578 | 0.473 | 0.159 | 0.007 ** |

| OBC * Medium Asset | 0.000 | 0.000 *** | 0.356 | 0.079 | 0.375 | 0.075 |

| OBC * High Asset | 0.000 | 0.000 *** | 0.387 | 0.084 | 0.150 | 0.000 *** |

| Control Variables | ||||||

| Hindu | 1.277 | 0.398 | 1.382 | 0.362 | 1.437 | 0.126 |

| Muslim | 0.637 | 0.238 | 0.792 | 0.584 | 0.733 | 0.312 |

| Female-headed HH | 0.872 | 0.493 | 0.737 | 0.150 | 0.839 | 0.252 |

| HH head’s age | 0.996 | 0.899 | 0.999 | 0.972 | 1.001 | 0.961 |

| Age square | 1.000 | 0.599 | 1.000 | 0.678 | 1.000 | 0.577 |

| HH head’s education | 1.143 | 0.000 *** | 1.073 | 0.000 *** | 1.124 | 0.000 *** |

| Agriculture: Male | 1.95 | 0.102 | 0.899 | 0.679 | 1.308 | 0.279 |

| Non-Agriculture: Male | 2.262 | 0.025 * | 1.328 | 0.259 | 1.753 | 0.011 * |

| Agriculture: Female | 1.074 | 0.902 | 0.991 | 0.970 | 1.005 | 0.981 |

| Non-Agriculture: Female | 1.058 | 0.678 | 1.412 | 0.063 | 1.12 | 0.318 |

| Region | NA | NA | NA | NA | 1.338 * | 0.017 |

| Outcome 4: Other | ||||||

| Urban | Rural | Combined | ||||

| RRR | p-Value † | RRR | p-Value † | RRR | p-Value † | |

| Household Asset Variables | ||||||

| Medium Asset | 147,995.624 | 0.000 *** | 0.723 | 0.262 | 0.786 | 0.371 |

| High Asset | 378,814.230 | 0.000 *** | 0.997 | 0.991 | 1.716 | 0.028 * |

| Media Exposure Variables | ||||||

| Newspaper | 1.777 | 0.004 ** | 1.186 | 0.069 | 1.333 | 0.001 *** |

| Radio | 0.962 | 0.835 | 1.189 | 0.157 | 1.099 | 0.405 |

| Television | 0.835 | 0.660 | 1.375 * | 0.014 | 1.299 * | 0.042 |

| Dependency Variables | ||||||

| Highest Asset * # above 60 years | 1.093 | 0.805 | 0.736 | 0.174 | 0.987 | 0.943 |

| # above 60 years | 1.519 | 0.096 | 1.269 | 0.003 ** | 1.344 | 0.000 *** |

| # between 0 and 5 years | 0.952 | 0.626 | 0.953 | 0.325 | 0.943 | 0.201 |

| # between 6 and 15 years | 0.988 | 0.865 | 1.029 | 0.381 | 1.011 | 0.729 |

| Caste | ||||||

| SC | 83,834.442 | 0.000 *** | 1.32 | 0.159 | 1.293 | 0.196 |

| ST | 56,029.248 | 0.000 *** | 1.221 | 0.297 | 1.431 | 0.068 |

| OBC | 120,729.780 | 0.000 | 0.966 | 0.861 | 1.056 | 0.791 |

| SC * Medium Asset | 0.000 | 0.000 *** | 0.841 | 0.619 | 0.791 | 0.464 |

| SC * High Asset | 0.000 | 0.000 *** | 1.338 | 0.450 | 0.683 | 0.207 |

| ST * Medium Asset | 0.000 | 0.000 *** | 1.112 | 0.777 | 0.874 | 0.700 |

| ST * High Asset | 0.000 | 0.000 *** | 1.058 | 0.892 | 0.522 | 0.093 |

| OBC * Medium Asset | 0.000 | 0.000 *** | 1.319 | 0.380 | 1.111 | 0.723 |

| OBC * High Asset | 0.000 | 0.000 *** | 1.489 | 0.231 | 0.724 | 0.235 |

| Control Variables | ||||||

| Hindu | 0.609 | 0.088 | 0.79 | 0.247 | 0.682 | 0.033 * |

| Muslim | 0.176 | 0.000 *** | 0.819 | 0.527 | 0.364 | 0.000 *** |

| Female-headed HH | 1.353 | 0.250 | 0.939 | 0.658 | 1.131 | 0.414 |

| HH head’s age | 1.161 | 0.000 *** | 1.077 | 0.003 ** | 1.103 | 0.000 *** |

| Age square | 0.999 | 0.000 *** | 0.999 | 0.007 ** | 0.999 | 0.000 *** |

| HH head’s education | 1.015 | 0.482 | 1.008 | 0.522 | 1.015 | 0.192 |

| Agriculture: Male | 1.483 | 0.244 | 1.142 | 0.369 | 1.239 | 0.121 |

| Non-Agriculture: Male | 1.381 | 0.361 | 1.04 | 0.779 | 1.135 | 0.344 |

| Agriculture: Female | 1.197 | 0.586 | 1.197 | 0.056 | 1.192 | 0.068 |

| Non-Agriculture: Female | 1.341 | 0.087 | 1.241 | 0.065 | 1.251 | 0.033 * |

| Region | NA | NA | NA | NA | 0.725 | 0.005 ** |

| Observations | 21,850 | 51,757 | 73,619 | |||

| Pseudo R-squared | 0.174 | 0.245 | 0.216 | |||

| Log pseudolikelihood | −176.329 | −269.794 | −452.478 | |||

Appendix D

| Urban | Rural | Combined | ||||

|---|---|---|---|---|---|---|

| Marginal Effects | p-Value † | Marginal Effects | p-Value † | Marginal Effects | p-Value † | |

| Household Asset Variables | ||||||

| Medium Asset | −0.089 | 0.071 | 0.006 | 0.697 | −0.013 | 0.421 |

| High Asset | −0.005 | 0.932 | 0.006 | 0.748 | 0.041 | 0.014 * |

| Media Exposure Variables | ||||||

| Newspaper | 0.022 * | 0.033 | 0.006 | 0.302 | 0.012 | −0.020 * |

| Radio | 0.004 | 0.784 | −0.001 | 0.927 | 0.000 | 0.95 |

| Television | 0.032 | 0.082 | 0.027 | 0.000 *** | 0.032 | 0.000 *** |

| Dependency Variables | ||||||

| Highest Asset * # above 60 years | −0.011 | 0.585 | −0.006 | 0.622 | −0.003 | 0.777 |

| # above 60 years | 0.028 | 0.043 * | 0.014 | 0.005 ** | 0.015 | 0.002 ** |

| # between 0 and 5 years | −0.027 | 0.000 *** | −0.005 | 0.053 | −0.012 | 0.000 *** |

| # between 6 and 15 years | −0.000 | 0.913 | 0.005 | 0.018 * | 0.003 | 0.189 |

| Caste | ||||||

| SC | −0.033 | 0.525 | 0.059 | 0.000 *** | 0.052 | 0.001 *** |

| ST | −0.035 | 0.509 | 0.039 | 0.006 ** | 0.037 | 0.014 * |

| OBC | −0.009 | 0.868 | 0.013 | 0.310 | 0.013 | 0.352 |

| SC * Medium Asset | 0.071 | 0.266 | −0.018 | 0.324 | −0.012 | 0.526 |

| SC * High Asset | 0.005 | 0.936 | −0.017 | 0.434 | −0.056 | 0.005 ** |

| ST * Medium Asset | 0.074 | 0.331 | 0.003 | 0.898 | 0.003 | 0.896 |

| ST * High Asset | 0.014 | 0.824 | −0.038 | 0.144 | −0.057 | 0.011 * |

| OBC * Medium Asset | 0.069 | 0.277 | −0.003 | 0.871 | 0.011 | −0.512 |

| OBC * High Asset | −0.038 | 0.487 | 0.006 | 0.757 | −0.050 | 0.003 ** |

| Control Variables | ||||||

| Hindu | −0.022 | 0.329 | 0.036 | 0.008 ** | 0.015 | 0.220 |

| Muslim | −0.053 * | 0.030 | 0.024 | 0.175 | -0.005 | 0.719 |

| Female-headed HH | −0.014 | 0.341 | −0.005 | 0.464 | -0.008 | 0.233 |

| HH head’s age | 0.006 | 0.018 * | 0.013 | 0.000 *** | 0.011 | 0.000 *** |

| Age square | −0.000 | 0.067 | −0.000 | 0.000 *** | -0.000 | 0.000 *** |

| HH head’s education | 0.003 | 0.022 * | −0.000 | 0.723 | 0.001 | 0.116 |

| Agriculture: Male | 0.021 | 0.332 | 0.002 | 0.809 | 0.008 | 0.363 |

| Non-Agriculture: Male | 0.037 | 0.022 * | 0.008 | 0.342 | 0.016 | 0.037 * |

| Agriculture: Female | 0.018 | 0.407 | 0.026 | 0.000 *** | 0.029 | 0.000 *** |

| Non-Agriculture: Female | 0.023 | 0.025 * | 0.030 | 0.000 *** | 0.028 | 0.000 *** |

| Region | NA | NA | NA | NA | -0.041 | 0.000 *** |

| Observations | 22,429 | 52,881 | 75,310 | |||

| Pseudo R-squared | 0.146 | 0.243 | 0.201 | |||

| Log pseudolikelihood | −14.002 | −23.021 | −37.392 | |||

Appendix E

| D1: Outcome 1: Public H.I. | ||||||

|---|---|---|---|---|---|---|

| Urban | Rural | Combined | ||||

| RRR | p-Value † | RRR | p-Value † | RRR | p-Value † | |

| Household Asset Variables | ||||||

| Medium Asset | 0.567 | 0.066 | 1.037 | 0.742 | 0.938 | 0.547 |

| High Asset | 0.585 | 0.069 | 0.867 | 0.25 | 0.88 | 0.251 |

| Media Exposure Variables | ||||||

| Newspaper | 1.036 | 0.559 | 1.005 | 0.891 | 1.016 | 0.642 |

| Radio | 0.983 | 0.836 | 0.965 | 0.478 | 0.971 | 0.516 |

| Television | 1.192 | 0.147 | 1.206 | 0.000 *** | 1.235 | 0.000 *** |

| Dependency Variables | ||||||

| Highest Asset * # above 60 years | 0.878 | 0.293 | 0.97 | 0.738 | 0.935 | 0.351 |

| # above 60 years | 1.112 | 0.245 | 1.085 * | 0.021 | 1.082 | 0.025 * |

| # between 0 and 5 years | 0.840 | 0.000 *** | 0.969 | 0.100 | 0.930 | 0.000 *** |

| # between 6 and 15 years | 1.008 | 0.779 | 1.039 | 0.004 ** | 1.028 * | 0.028 |

| Caste | ||||||

| SC | 0.746 | 0.329 | 1.452 | 0.000 *** | 1.334 | 0.004 ** |

| ST | 0.761 | 0.38 | 1.290 | 0.009 ** | 1.206 | 0.054 |

| OBC | 0.807 | 0.496 | 1.075 | 0.430 | 1.038 | 0.689 |

| SC * Medium Asset | 1.514 | 0.224 | 0.918 | 0.513 | 0.948 | 0.667 |

| SC * High Asset | 1.54 | 0.201 | 0.978 | 0.890 | 0.933 | 0.636 |

| ST * Medium Asset | 1.565 | 0.277 | 0.994 | 0.974 | 1.033 | 0.835 |

| ST * High Asset | 1.889 | 0.072 | 0.802 | 0.265 | 1.049 | 0.776 |

| OBC * Medium Asset | 1.545 | 0.206 | 0.987 | 0.917 | 1.079 | 0.505 |

| OBC * High Asset | 1.306 | 0.412 | 1.120 | 0.388 | 1.017 | 0.886 |

| Control Variables | ||||||

| Hindu | 0.896 | 0.385 | 1.328 | 0.003 ** | 1.130 | 0.108 |

| Muslim | 0.847 | 0.264 | 1.219 | 0.11 | 1.069 | 0.488 |

| Female-headed HH | 0.872 | 0.121 | 0.962 | 0.417 | 0.926 | 0.079 |

| HH head’s age | 1.028 | 0.175 | 1.098 | 0.000 *** | 1.073 | 0.000 *** |

| Age square | 1.000 | 0.338 | 0.999 | 0.000 *** | 0.999 | 0.000 *** |

| HH head’s education | 0.994 | 0.362 | 0.993 | 0.102 | 0.993 | 0.050 * |

| Agriculture: Male | 0.996 | 0.980 | 1.022 | 0.726 | 1.022 | 0.706 |

| Non-Agriculture: Male | 1.119 | 0.300 | 1.064 | 0.315 | 1.078 | 0.166 |

| Agriculture: Female | 1.100 | 0.459 | 1.194 | 0.000 *** | 1.192 | 0.000 *** |

| Non-Agriculture: Female | 1.116 | 0.085 | 1.198 | 0.000 *** | 1.170 | 0.000 *** |

| Region | NA | NA | NA | NA | 0.720 | 0.000 *** |

| D2: Outcome 2: CBHI | ||||||

| Urban | Rural | Combined | ||||

| RRR | p-Value † | RRR | p-Value † | RRR | p-Value † | |

| Household Asset Variables | ||||||

| Medium Asset | NA | NA | 0.262 | 0.226 | 0.343 | 0.239 |

| High Asset | NA | NA | 0.95 | 0.948 | 1.375 | 0.662 |

| Media Exposure Variables | ||||||

| Newspaper | NA | NA | 1.455 | 0.333 | 1.692 | 0.102 |

| Radio | NA | NA | 0.168 | 0.003 ** | 0.701 | 0.336 |

| Television | NA | NA | 0.808 | 0.604 | 0.549 | 0.107 |

| Dependency Variables | ||||||

| Highest Asset * # above 60 years | NA | NA | 1.058 | 0.937 | 0.715 | 0.575 |

| # above 60 years | NA | NA | 1.390 | 0.458 | 1.206 | 0.621 |

| # between 0 and 5 years | NA | NA | 1.104 | 0.487 | 1.171 | 0.267 |

| # between 6 and 15 years | NA | NA | 0.832 | 0.277 | 0.895 | 0.413 |

| Caste | ||||||

| SC | NA | NA | 0.423 | 0.250 | 0.439 | 0.269 |

| ST | NA | NA | 0.124 | 0.083 | 0.129 | 0.083 |

| OBC | NA | NA | 0.492 | 0.296 | 0.693 | 0.607 |

| SC * Medium Asset | NA | NA | 1.848 | 0.705 | 6.395 | 0.17 |

| SC * High Asset | NA | NA | 2.97 | 0.330 | 1.157 | 0.883 |

| ST * Medium Asset | NA | NA | 69.528 | 0.020 * | 37.178 | 0.035 * |

| ST * High Asset | NA | NA | 0.000 | 0.000 *** | 9.665 | 0.096 |

| OBC * Medium Asset | NA | NA | 8.592 | 0.085 | 5.256 | 0.109 |

| OBC * High Asset | NA | NA | 1.511 | 0.668 | 1.265 | 0.775 |

| Control Variables | ||||||

| Hindu | NA | NA | 0.973 | 0.957 | 0.919 | 0.889 |

| Muslim | NA | NA | 0.495 | 0.380 | 0.333 | 0.183 |

| Female-headed HH | NA | NA | 1.346 | 0.606 | 1.060 | 0.896 |

| HH head’s age | NA | NA | 1.125 | 0.218 | 1.230 | 0.020 * |

| Age square | NA | NA | 0.999 | 0.197 | 0.998 | 0.026 * |

| HH head’s education | NA | NA | 0.991 | 0.857 | 1.025 | 0.502 |

| Agriculture: Male | NA | NA | 1.156 | 0.850 | 1.057 | 0.907 |

| Non-Agriculture: Male | NA | NA | 0.565 | 0.450 | 0.532 | 0.136 |

| Agriculture: Female | NA | NA | 0.536 | 0.192 | 0.559 | 0.171 |

| Non-Agriculture: Female | NA | NA | 0.429 | 0.174 | 1.125 | 0.751 |

| Region | NA | NA | NA | NA | 1.213 | 0.587 |

| D3: Outcome 3: Private H.I. | ||||||

| Urban | Rural | Combined | ||||

| RRR | p-Value † | RRR | p-Value † | RRR | p-Value † | |

| Household Asset Variables | ||||||

| Medium Asset | 62,154.103 | 0.000 *** | 3.771 | 0.007 ** | 3.050 | 0.017 * |

| High Asset | 600,116.591 | 0.000 *** | 10.362 | 0.000 *** | 15.540 | 0.000 *** |

| Media Exposure Variables | ||||||

| Newspaper | 1.518 | 0.016 * | 1.207 | 0.273 | 1.416 | 0.004 ** |

| Radio | 1.223 | 0.195 | 1.146 | 0.456 | 1.166 | 0.218 |

| Television | 3.518 | 0.018 * | 0.981 | 0.944 | 1.538 | 0.057 |

| Dependency Variables | ||||||

| Highest Asset * # above 60 years | 0.960 | 0.868 | 1.125 | 0.656 | 1.047 | 0.791 |

| # above 60 years | 1.223 | 0.258 | 0.919 | 0.608 | 1.073 | 0.557 |

| # between 0 and 5 years | 0.921 | 0.502 | 0.944 | 0.471 | 0.929 | 0.385 |

| # between 6 and 15 years | 0.955 | 0.488 | 0.951 | 0.469 | 0.95 | 0.304 |

| Caste | ||||||

| SC | 85,166.207 | 0.000 *** | 1.613 | 0.471 | 2.173 | 0.197 |

| ST | 0.937 | 0.814 | 0.994 | 0.992 | 1.479 | 0.508 |

| OBC | 91,963.477 | 0.000 *** | 2.411 | 0.063 | 3.205 | 0.011 * |

| SC * Medium Asset | 0.000 | 0.000 *** | 0.394 | 0.226 | 0.433 | 0.219 |

| SC * High Asset | 0.000 | 0.000 *** | 0.386 | 0.223 | 0.268 | 0.037 * |

| ST * Medium Asset | 3.081 | 0.086 | 1.582 | 0.453 | 1.428 | 0.555 |

| ST * High Asset | 0.217 | 0.000 *** | 0.624 | 0.529 | 0.181 | 0.010 ** |

| OBC * Medium Asset | 0.000 | 0.000 *** | 0.371 | 0.079 | 0.418 | 0.097 |

| OBC * High Asset | 0.000 | 0.000 *** | 0.409 | 0.088 | 0.166 | 0.000 *** |

| Control Variables | ||||||

| Hindu | 1.269 | 0.401 | 1.379 | 0.351 | 1.430 | 0.123 |

| Muslim | 0.644 | 0.243 | 0.773 | 0.537 | 0.731 | 0.299 |

| Female-headed HH | 0.883 | 0.522 | 0.793 | 0.263 | 0.868 | 0.341 |

| HH head’s age | 0.999 | 0.958 | 0.995 | 0.855 | 1.002 | 0.940 |

| Age square | 1.000 | 0.664 | 1.000 | 0.570 | 1.000 | 0.613 |

| HH head’s education | 1.142 | 0.000 *** | 1.079 | 0.000 *** | 1.126 | 0.000 *** |

| Agriculture: Male | 2.016 | 0.067 | 0.801 | 0.370 | 1.273 | 0.305 |

| Non-Agriculture: Male | 2.413 | 0.007 ** | 1.212 | 0.419 | 1.743 | 0.006 ** |

| Agriculture: Female | 1.083 | 0.892 | 0.939 | 0.783 | 0.982 | 0.936 |

| Non-Agriculture: Female | 1.073 | 0.605 | 1.383 | 0.079 | 1.128 | 0.292 |

| Region | NA | NA | NA | NA | 1.298 | 0.032 * |

| D4: Outcome 4: Other | ||||||

| Urban | Rural | Combined | ||||

| RRR | p-Value † | RRR | p-Value † | RRR | p-Value † | |

| Household Asset Variables | ||||||

| Medium Asset | 394,358.683 | 0.000 *** | 0.903 | 0.786 | 1.039 | 0.917 |

| High Asset | 810,782.482 | 0.000 *** | 0.642 | 0.353 | 1.385 | 0.401 |

| Media Exposure Variables | ||||||

| Newspaper | 1.612 | 0.118 | 1.360 | 0.024 * | 1.437 | 0.008 ** |

| Radio | 0.93 | 0.776 | 1.067 | 0.717 | 0.947 | 0.738 |

| Television | 0.567 | 0.275 | 1.368 | 0.151 | 1.256 | 0.308 |

| Dependency Variables | ||||||

| Highest Asset * # above 60 years | 1.829 | 0.182 | 1.017 | 0.956 | 1.496 | 0.142 |

| # above 60 years | 1.317 | 0.323 | 1.338 | 0.011 * | 1.380 | 0.002 ** |

| # between 0 and 5 years | 0.814 | 0.173 | 1.003 | 0.966 | 0.920 | 0.235 |

| # between 6 and 15 years | 1.089 | 0.326 | 1.007 | 0.891 | 1.027 | 0.564 |

| Caste | ||||||

| SC | 270,681.356 | 0.000 *** | 1.692 | 0.067 | 1.675 | 0.085 |

| ST | 0.656 | 0.238 | 1.055 | 0.87 | 1.081 | 0.811 |

| OBC | 286,475.745 | 0.000 *** | 1.249 | 0.468 | 1.313 | 0.389 |

| SC * Medium Asset | 0.000 | 0.000 *** | 0.405 | 0.054 | 0.369 | 0.028 * |

| SC * High Asset | 0.000 | 0.000 *** | 1.573 | 0.382 | 0.305 | 0.007 ** |

| ST * Medium Asset | 0.977 | 0.983 | 0.804 | 0.683 | 0.750 | 0.574 |

| ST * High Asset | 1.344 | 0.691 | 1.181 | 0.778 | 0.793 | 0.739 |

| OBC * Medium Asset | 0.000 | 0.000 *** | 0.829 | 0.662 | 0.831 | 0.659 |

| OBC * High Asset | 0.000 | 0.000 *** | 1.082 | 0.872 | 0.477 | 0.063 |

| Control Variables | ||||||

| Hindu | 0.483 | 0.127 | 0.665 | 0.137 | 0.550 | 0.027 * |

| Muslim | 0.243 | 0.023 * | 0.691 | 0.405 | 0.403 | 0.021 * |

| Female-headed HH | 1.480 | 0.246 | 1.340 | 0.15 | 1.467 | 0.070 |

| HH head’s age | 1.201 | 0.001 ** | 1.07 | 0.079 | 1.101 | 0.003 ** |

| Age square | 0.998 | 0.001 *** | 0.999 | 0.108 | 0.999 | 0.003 ** |

| HH head’s education | 0.995 | 0.858 | 1.043 | 0.027 * | 1.022 | 0.253 |

| Agriculture: Male | 1.741 | 0.082 | 0.983 | 0.937 | 1.148 | 0.434 |

| Non-Agriculture: Male | 1.880 | 0.025 * | 1.206 | 0.352 | 1.423 | 0.024 * |

| Agriculture: Female | 1.332 | 0.562 | 1.072 | 0.65 | 1.108 | 0.505 |

| Non-Agriculture: Female | 1.305 | 0.358 | 1.019 | 0.929 | 1.113 | 0.588 |

| Region | NA | NA | NA | NA | 0.737 | 0.071 |

| Observations | 22,168 | 52,147 | 74,328 | |||

| Pseudo-R-squared | 0.184 | 0.249 | 0.223 | |||

| Log pseudolikelihood | −166.153 | −253.602 | −424.956 | |||

References

- Oxford Economics/Haver Analytics. Global Analysis of Health Insurance in India; Ernst & Young LLP: London, UK, 2016. [Google Scholar]

- Thomas, T.K. Role of Health insurance in enabling universal health coverage in India: A critical review. Health Serv. Manag. Res. 2016, 29, 99–106. [Google Scholar] [CrossRef]

- Dror, I. Demystifying Micro Health Insurance Package Design-Choosing Healthplans All Together (Chat). Microfinanc. Insights 2007, 4, 17–19. [Google Scholar]

- Gumber, A.; Kulkarni, V. Health insurance for informal sector: Case study of Gujarat. Econ. Political Wkly. 2000, 35, 3607–3613. [Google Scholar]

- Binnendijk, E.; Dror, D.M.; Gerelle, E.; Koren, R. Estimating Willingness-to-Pay for health insurance among rural poor in India by reference to Engel’s law. Soc. Sci. Med. 2013, 76, 67–73. [Google Scholar] [CrossRef]

- Dhanaraj, S. Economic vulnerability to health shocks and coping strategies: Evidence from Andhra Pradesh, India. Health Policy Plan. 2016, 31, 749–758. [Google Scholar] [CrossRef]

- Kansra, P.; Gill, H.S. Role of Perceptions in Health Insurance Buying Behaviour of Workers Employed in Informal Sector of India. Glob. Bus. Rev. 2017, 18, 250–266. [Google Scholar] [CrossRef]

- Chakrabarti, A.; Shankar, A. Determinants of Health Insurance Penetration in India: An Empirical Analysis. Oxf. Dev. Stud. 2015, 43, 379–401. [Google Scholar] [CrossRef]

- Seshadri, T.; Mh, A.; Ganesh, G.; Kadammanavar, M.; Pati, M.; Elias, M.A. Implementing programmes as if social exclusion matters: Enrolment in a social health protection scheme. In Towards Equitable Coverage and More Inclusive Social Protection in Health; ITG Press: Antwerp, Belgium, 2014. [Google Scholar]

- Raza, W.; Van de Poel, E.; Panda, P. Analyses of Enrolment, Droput and Effectiveness of RSBY in Northern Rural INDIA; MPRA Paper 70081; University Library of Munich: Munich, Germany, 2016. [Google Scholar]

- Nandi, A.; Ashok, A.; Laxminarayan, R. The socioeconomic and institutional determinants of participation in India’s health insurance scheme for the poor. PLoS ONE 2013, 8, e66296. [Google Scholar] [CrossRef]

- Sun, C. An analysis of RSBY enrolment patterns: Preliminary evidence and lessons from the early experience. In India’s Health Insurance Scheme for the Poor: Evidence from the Early Experience of RSBY; Centre for Policy Research: New Delhi, India, 2011; pp. 84–116. [Google Scholar]

- Ghosh, S.; Datta-Gupta, N. Targeting and effects of rashtriya swasthya bima yojana on access to care and financial protection. Econ. Polit. Wkly. 2017, 52, 61–70. [Google Scholar]

- Ravi, S.; Ahluwalia, R.; Bergkvist, S. Health and Morbidity in India (2004–2014); 092016; Brookings Institution Indian Center: New Delhi, India, 2016. [Google Scholar]

- La Forgia, G.; Nagpal, S. Government-Sponsored Health Insurance in India: Are You Covered? World Bank Publications: Washington, DC, USA, 2012. [Google Scholar]

- Ghosh, S.; Mladovsky, P. Social exclusion and its effect on enrolment in Rashtriya Swasthya Bima Yojana in Maharashtra, India. In Health Inc-Towards Equitable Coverage and More Inclusive Social Protection in Health; ITG Press: Antwerp, Belgium, 2014. [Google Scholar]

- Rent, P.; Ghosh, S. Understanding the “Cash-Less” Nature of Government-Sponsored Health Insurance Schemes: Evidence From Rajiv Gandhi Jeevandayee Aarogya Yojana in Mumbai. Sage Open 2015, 5, 2158244015614607. [Google Scholar] [CrossRef]

- IIPS; Macro International. National Family Health Survey (NFHS-3), 2005–2006: India; International Institute for Population Sciences-IIPS/India, Macro International: Mumbai, India, 2007. [Google Scholar]

- IIPS; ICF. National Family Health Survey (NFHS-4), 2015–2016: India; International Institute for Population Sciences (IIPS), ICF: Mumbai, India, 2017. [Google Scholar]

- Keshri, V.R.; Ghosh, S. Health Insurance for Universal Health Coverage in India: A Critical Examination. Preprint 2019. [Google Scholar] [CrossRef]

- Raghavan, P. Modicare: The World’s Largest National Health Protection Scheme-The Economics Times. The Economic Times, 2 February 2018. [Google Scholar]

- National Health Agency. Pradhan Mantri Jan Arogya Yojna. PM-JAY-Ayushman Bharat. Available online: https://www.pmjay.gov.in/ (accessed on 12 February 2022).

- IIPS. Home Page-National Family Health Survey, India. Available online: http://rchiips.org/nfhs/ (accessed on 22 June 2022).

- DHS Program. Demographic and Health Surveys. Available online: https://dhsprogram.com (accessed on 19 April 2022).

- Ellis, R.P.; Alam, M.; Gupta, I. Health insurance in India: Prognosis and prospectus. Econ. Political Wkly. 2000, 35, 207–217. [Google Scholar]

- USAID. The DHS Program-Topics-Wealth Index. Available online: https://dhsprogram.com/topics/wealth-index/ (accessed on 28 June 2022).

- Bhat, R.; Jain, N. Factoring Affecting the Demand for Insurance in a Micro Health Insurance Scheme; IIMA: Ahmedabad, India, 2006. [Google Scholar]

- Wagstaff, A. Health Insurance for the Poor: Initial Impacts of Vietnam’s Health Care Fund for the Poor; The World Bank: Washington, DC, USA, 2007. [Google Scholar]

- Kamath, R.; Sanah, N.; Machado, L.M.; Sekaran, V.C. Determinants of enrolment and experiences of Rashtriya Swasthya Bima Yojana (RSBY) beneficiaries in Udupi district, India. Int. J. Med. Public Health 2014, 4, 82. [Google Scholar]

- StataCorp. In Stata Statistical Software: Release 15; StataCorp LLC.: College Station, TX, USA, 2017.

- Besley, T.; Hall, J.; Preston, I. The demand for private health insurance: Do waiting lists matter? J. Public Econ. 1999, 72, 155–181. [Google Scholar] [CrossRef]

- Cameron, A.C.; Trivedi, P.K.; Milne, F.; Piggott, J. A microeconometric model of the demand for health care and health insurance in Australia. Rev. Econ. Stud. 1988, 55, 85–106. [Google Scholar] [CrossRef]

- Propper, C. The demand for private health care in the UK. J. Health Econ. 2000, 19, 855–876. [Google Scholar] [CrossRef]

- Cameron, A.C.; Trivedi, P.K. The role of income and health risk in the choice of health insurance: Evidence from Australia. J. Public Econ. 1991, 45, 1–28. [Google Scholar] [CrossRef]

- Emmerson, C.; Frayne, C.; Goodman, A. Should private medical insurance be subsidised? Health Care UK 2001, 51, 49–65. [Google Scholar]

- Robinson, R. Religion, Socio-economic Backwardness & Discrimination: The Case of Indian Muslims. Indian J. Ind. Relat. 2008, 44, 194–200. [Google Scholar]

- Sachar, R.; Hamid, S.; Oommen, T.; Basith, M.; Basant, A. Social, economic and educational status of the Muslim community of India: A report. Dev. Econ. Work. Pap. 2006, 4, 22136. [Google Scholar]

- Ahlin, T.; Nichter, M.; Pillai, G. Health insurance in India: What do we know and why is ethnographic research needed. Anthropol. Med. 2016, 23, 102–124. [Google Scholar] [CrossRef] [PubMed]

- Garg, S.; Chowdhury, S.; Sundararaman, T. Utilisation and financial protection for hospital care under publicly funded health insurance in three states in Southern India. BMC Health Serv. Res. 2019, 19, 1004. [Google Scholar] [CrossRef] [PubMed]

- Sinha, R.K.; Chatterjee, K. Assessing Impact of India’s National Health Insurance Scheme (RSBY): Is There Any Evidence of Increased Health Care Utilisation? Int. J. Humanit. Soc. Sci. 2014, 4, 223–232. [Google Scholar]

- Azam, M. Does social health insurance reduce financial burden? Panel Data Evidence from India. World Dev. 2018, 102, 1–17. [Google Scholar] [CrossRef]

- Johnson, D.; Krishnaswamy, K. The Impact of RSBY on Hospital Utilization and Out-of-Pocket Health Expenditure. 2012. Available online: https://openknowledge.worldbank.org/server/api/core/bitstreams/3db2ecfd-00e2-52b3-8388-577ce0e392b6/content (accessed on 15 January 2023).

- Selvaraj, S.; Karan, A.K. Why publicly-financed health insurance schemes are ineffective in providing financial risk protection. Econ. Political Wkly. 2012, 47, 60–68. [Google Scholar]

- Karan, A.K.; Yip, W.C.M.; Mahal, A. Extending Health Insurance to the Poor in India: An Impact Evaluation of Rashtriya Swasthya Bima Yojana on Financial Risk Protection. 2015. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2702395 (accessed on 15 January 2023).

- Karan, A.; Yip, W.; Mahal, A. Extending health insurance to the poor in India: An impact evaluation of Rashtriya Swasthya Bima Yojana on out of pocket spending for healthcare. Soc. Sci. Med. 2017, 181, 83–92. [Google Scholar] [CrossRef]

- Ambade, P.; Rahman, T. Do National Health Insurance Programs for the Poor Improve the Relative Health Outcomes of the Poor? Evidence from India (25 September 2022). Available online: https://ssrn.com/abstract=4228939 (accessed on 15 January 2023).

- Ambade, M.; Sarwal, R.; Mor, N.; Kim, R.; Subramanian, S.V. Components of Out-of-Pocket Expenditure and Their Relative Contribution to Economic Burden of Diseases in India. JAMA Netw. Open 2022, 5, e2210040. [Google Scholar] [CrossRef]

- National Health Authority. About Pradhan Mantri Jan Arogya Yojana (PM-JAY). Available online: https://nha.gov.in/PM-JAY (accessed on 21 March 2022).

- Trivedi, M.; Saxena, A.; Shroff, Z.; Sharma, M. Experiences and challenges in accessing hospitalization in a government-funded health insurance scheme: Evidence from early implementation of Pradhan Mantri Jan Aarogya Yojana (PM-JAY) in India. PLoS ONE 2022, 17, e0266798. [Google Scholar] [CrossRef]

- Garg, S.; Bebarta, K.K.; Tripathi, N. Performance of India’s national publicly funded health insurance scheme, Pradhan Mantri Jan Arogaya Yojana (PMJAY), in improving access and financial protection for hospital care: Findings from household surveys in Chhattisgarh state. BMC Public Health 2020, 20, 949. [Google Scholar] [CrossRef]

- Subramanian, S.; Ambade, M.; Kumar, A.; Chi, H.; Joe, W.; Rajpal, S.; Kim, R. Progress on Sustainable Development Goal indicators in 707 districts of India: A quantitative mid-line assessment using the National Family Health Surveys, 2016 and 2021. Lancet Reg. Health-Southeast Asia 2023, 100155, 1–17. [Google Scholar] [CrossRef]

- Bose, M.; Banerjee, S. Equity in distribution of public subsidy for noncommunicable diseases among the elderly in India: An application of benefit incidence analysis. BMC Public Health 2019, 19, 1735. [Google Scholar] [CrossRef] [PubMed]

- Asaria, M.; Mazumdar, S.; Chowdhury, S.; Mazumdar, P.; Mukhopadhyay, A.; Gupta, I. Socioeconomic inequality in life expectancy in India. BMJ Glob. Health 2019, 4, e001445. [Google Scholar] [CrossRef] [PubMed]

- Oxfam India. Inequality Report 2021: India’s Unequal Healthcare Story; Oxfam India: New Delhi, India, 2021. [Google Scholar]

- Sabharwal, N.S. Caste, religion and malnutrition linkages. Econ. Political Wkly. 2011, 46, 16–18. [Google Scholar]

- Ramachandran, R.; Deshpande, A. The Impact of Caste: A Missing Link in the Literature on Stunting in India. IZA Discussion Paper No. 14173. 2021. Available online: https://ssrn.com/abstract=3803717 (accessed on 15 January 2023).

- UN Women. Turning Promises into Action: Gender Equality in the 2030 Agenda for Sustainable Development; UN Women: New York, NY, USA, 2018. [Google Scholar]

- Bora, J.K.; Raushan, R.; Lutz, W. The persistent influence of caste on under-five mortality: Factors that explain the caste-based gap in high focus Indian states. bioRxiv 2019. [Google Scholar] [CrossRef]

- Bang, A.; Chatterjee, M.; Dasgupta, J.; Garg, A.; Jain, Y.; Kumar, A.S.; Mor, N.; Paul, V.; Pradhan, P.; Rao, M.G. High Level Expert Group Report on Universal Health Coverage for India; Planning Commission of India: New Delhi, India, 2011. [Google Scholar]

- Acharya, S.S. Health Disparity and Health Equity in India Understanding the Difference and the Pathways Towards Policy. CASTE Glob. J. Soc. Exclusion 2022, 3, 211–222. [Google Scholar] [CrossRef]

- Nandi, S.; Schneider, H. Using an equity-based framework for evaluating publicly funded health insurance programmes as an instrument of UHC in Chhattisgarh State, India. Health Res. Policy Syst. 2020, 18, 50. [Google Scholar] [CrossRef]

| Inception Year | Central or State | Scheme | Eligibility Criteria |

|---|---|---|---|

| 1948 | Central Govt. | Employee State Insurance Scheme (ESIS) | Blue-collar workers |

| 1954 | Central Govt. | Central Government Health Scheme (CGHS) | Govt. employees |

| 2008 | Central Govt. | Rashitriya Swasthya Bima Yojana (RSBY) renamed/revamped Pradhan Mantri Jan Arogya Yojana (PM-JAY) in 2018 | Below Poverty Level (BPL) households working in the unorganized sector. In PM-JAY, they are identified by inclusion, deprivation, and occupational criteria of the Socio Economic Caste Census 2011 (SECC 2011). |

| 2016 | Assam | Atal Amrit Abhiyan/PM-JAY (in 2018) | Similar to PM-JAY |

| 2015 | Andaman and Nicobar Island | Andaman and Nicobar Island Scheme for Health Insurance (merged with PM-JAY in 2019) | Similar to PM-JAY |

| 2007 | Andhra Pradesh | Arogyashree Scheme (YSR Arogyasri Scheme after 2017) | State residents with an annual income below INR 500,000. Households with white ration card issued under National Food Security Act 2013. |

| 2014 | Arunachal Pradesh | The Arunachal Pradesh Chief Minister’s Universal Health Insurance Scheme (merged with PM-JAY in 2018) | Similar to PM-JAY |

| 2013 | Chhattisgarh | Mukhya Mantri Swasthya Bima Yojana (merged with PM-JAY and other programs in 2019) | Similar to PM-JAY |

| 2013 | Dadra and Nagar Haveli, Daman and Diu | Sanjeevani Swasthya Bima Yojana | Family listed in state BPL list |

| 2016 | Goa | Deen Dayal Swasthya Seva Yojana | All households |

| 2012 | Gujarat | Mukhya Mantri Amrutam Yojana | Household listed in state BPL list |

| 2016 | Himachal Pradesh | Mukhya Mantri State Health Care Scheme (merged with PM-JAY under the name Mukhya Mantri Himachal Health Care Scheme (HIMCARE) since 2019). | Similar to PM-JAY |

| 2017 | Jharkhand | Mukhya Mantri Swasthya Bima Yojana (merged with PM-JAY in 2018) | Similar to PM-JAY |

| 2018 | Karnataka | Ayushman Bharat-Aarogya Karnataka | Eligible households defined under National Food Security Act 2013 and beneficiaries for all ongoing schemes (Yashaswi Health Insurance Scheme 2003 and Vajpayee Arogyashree Scheme 2009). For non-beneficiaries, “co-payment” system is available. |

| 2008 | Kerala | Comprehensive Health Insurance Scheme (CHIS) and CHIS Plus (merged with PM-JAY in 2020 to form Karunya Arogya Suraksha Padhathi (KASP)) | Similar to PM-JAY |

| 2012 | Maharashtra | Rajiv Gandhi Jeevandayee Aarogya Yojana, renamed Mahatma Jyotiba Phule Jan Aarogya Yojana in 2017 | Eligible households defined under National Food Security Act 2013 having yellow and white ration cards. |

| 2012 | Meghalaya | Megha Health Insurance Scheme (merged with PM-JAY in 2019) | All residents except govt. employees |

| 2013 | Odisha | Biju Swasthya Kalyan Yojana | Eligible households defined under National Food Security Act 2013 |

| 2016 | Puducherry | Puducherry Medical Relief Society Scheme (merged with PM-JAY in 2019)/state scheme | All residents except govt. employees |

| 2015 | Punjab | Bhagat Puran Singh Health Insurance Scheme (implemented PM-JAY in 2019) | Similar to PM-JAY |

| 2015 | Rajasthan | Bhamashah Health Insurance Scheme/Mukhya Mantri Chiranjeevi Swasthya Bima Yojana | All residents (no premium for socioeconomically weaker families identified under Socio Economic Caste Census 2011 (SECC 2011)). |

| 2012 | Tamil Nadu | Chief Minister Comprehensive Health Insurance Scheme | Family annual income below INR 120,000 |

| 2007 | Telangana | Arogyashree Scheme | BPL families identified in state list |

| 200 | Tripura | RSBY/PM-JAY | Similar to PM-JAY |

| 2016 | Uttarakhand | Mukhya Mantri Swasthya Bima Yojana | All residents except govt. employees and pensioners |

| 2017 | West Bengal | Swasthya Sathi | Similar to PM-JAY |

| A. Health Insurance | |||||||

|---|---|---|---|---|---|---|---|

| Total, N = 598,252 | Has No HI, N = 425,778 | Has HI, N = 172,474 | p-Value | ||||

| Household Asset Variables (n = 598,252) | <0.001 | ||||||

| High Asset | 31.424 | 30.676 | 33.269 | ||||

| Medium Asset | 23.801 | 22.622 | 26.713 | ||||

| Low Asset | 44.775 | 46.702 | 40.018 | ||||

| Media Exposure Variables (n = 482,158) | |||||||

| Newspaper | 44.247 | 42.706 | 48.046 | <0.001 | |||

| Radio | 18.141 | 18.033 | 18.408 | 0.14 | |||

| Television | 78.155 | 74.688 | 86.699 | <0.001 | |||

| Dependency Variables (n = 598,252) | |||||||

| Prop. of # above 60 | 0.392 (0.647) | 0.390 (0.649) | 0.397 (0.642) | <0.001 | |||

| Prop. of # between 0 to 5 | 0.512 (0.831) | 0.551 (0.860) | 0.416 (0.746) | <0.001 | |||

| Prop. of # between 6 to 15 | 0.925 (1.156) | 0.974 (1.195) | 0.804 (1.045) | <0.001 | |||

| Caste (n = 571,188) | |||||||

| SC | 21.592 | 20.962 | 23.126 | <0.001 | |||

| ST | 9.642 | 9.388 | 10.259 | <0.001 | |||

| OBC | 44.241 | 43.305 | 46.518 | <0.001 | |||

| Control Variables | |||||||

| Hindu (n = 598,252) | 81.383 | 80.020 | 84.746 | <0.001 | |||

| Muslim (n = 598,252) | 12.568 | 14.105 | 8.772 | <0.001 | |||

| Sex of Household Head (n = 598,252) | 0.003 | ||||||

| Female | 14.636 | 14.777 | 14.290 | ||||

| Male | 85.364 | 85.223 | 85.710 | ||||

| HH head’s age (n = 598,168) | 48.415 (14.024) | 48.017 (14.291) | 49.398 (13.292) | <0.001 | |||

| HH head’s education (n = 595,856) | 6.044 (5.208) | 6.042 (5.172) | 6.048 (5.294) | 0.5 | |||

| Male: Agriculture (n = 78,207) | 34.268 | 33.335 | 36.387 | <0.001 | |||

| Male: Non-Agriculture (n = 78,207) | 65.562 | 66.273 | 63.949 | 0.001 | |||

| Female: Agriculture (n = 82,550) | 18.203 | 16.848 | 21.313 | <0.001 | |||

| Female: Non-Agriculture (n = 82,550) | 18.511 | 16.954 | 22.082 | <0.001 | |||

| Region (n = 598,252) | 0.054 | ||||||

| Rural | 65.163 | 64.951 | 65.686 | ||||

| Urban | 34.837 | 35.049 | 34.314 | ||||

| B. Health Insurance Products | |||||||

| Total, N = 591,378 | Has no HI, N = 425,778 | Has Public HI, N = 148,369 | Has CBHI, N = 809 | Has Private HI, N = 10,823 | Has Other HI, N = 5599 | p-Value | |

| Household Asset Variables (n = 591,378) | <0.001 | ||||||

| High Asset | 31.256 | 30.676 | 28.511 | 49.026 | 83.453 | 44.596 | |

| Low Asset | 44.895 | 46.702 | 43.142 | 25.893 | 5.764 | 32.284 | |

| Medium Asset | 23.850 | 22.622 | 28.347 | 25.081 | 10.782 | 23.120 | |

| Media Exposure Variables (n = 476,354) | |||||||

| Newspaper | 44.092 | 42.706 | 44.989 | 60.154 | 79.834 | 56.352 | <0.001 |

| Radio | 18.072 | 18.033 | 17.201 | 24.765 | 29.021 | 22.643 | <0.001 |

| Television | 78.016 | 74.688 | 85.894 | 88.524 | 95.996 | 86.723 | <0.001 |

| Dependency Variables (n = 591,378) | |||||||

| Prop. of # above 60 | 0.392 (0.647) | 0.390 (0.649) | 0.390 (0.634) | 0.406 (0.663) | 0.448 (0.696) | 0.496 (0.715) | <0.001 |

| Prop. of # between 0 and 5 | 0.513 (0.832) | 0.551 (0.860) | 0.419 (0.749) | 0.452 (0.764) | 0.362 (0.672) | 0.448 (0.786) | <0.001 |

| Prop. of # between 6 and 15 | 0.927 (1.158) | 0.974 (1.195) | 0.815 (1.053) | 0.792 (0.997) | 0.655 (0.913) | 0.829 (1.074) | <0.001 |

| Caste (n = 564,457) | |||||||

| SC | 21.628 | 20.962 | 24.453 | 16.541 | 10.737 | 18.083 | <0.001 |

| ST | 9.589 | 9.388 | 10.669 | 6.224 | 2.972 | 9.077 | <0.001 |

| OBC | 44.178 | 43.305 | 47.368 | 45.225 | 36.136 | 40.158 | <0.001 |

| Control Variables | |||||||

| Hindu (n = 591,378) | 81.295 | 80.020 | 84.507 | 83.381 | 84.298 | 86.979 | <0.001 |

| Muslim (n = 591,378) | 12.654 | 14.105 | 9.189 | 9.281 | 6.632 | 6.236 | <0.001 |

| HH Head’s Sex (n = 591,378) | <0.001 | ||||||

| Female | 14.673 | 14.777 | 14.803 | 12.565 | 9.764 | 13.082 | |

| Male | 85.327 | 85.223 | 85.197 | 87.435 | 90.236 | 86.918 | |

| HH head’s age (n = 591,3778) | 48.403 (14.037) | 48.017 (14.291) | 49.286 (13.296) | 49.731 (13.175) | 50.461 (13.395) | 50.183 (13.399) | <0.001 |

| HH head’s education (n = 589,002) | 6.027 (5.200) | 6.042 (5.172) | 5.535 (5.068) | 8.002 (5.693) | 11.302 (4.866) | 7.426 (5.310) | <0.001 |

| Male: Agriculture (n = 77,166) | 34.195 | 33.335 | 38.136 | 39.225 | 12.287 | 34.219 | <0.001 |

| Male: Non-Agriculture (n = 77,166) | 65.629 | 66.273 | 62.169 | 60.702 | 88.122 | 67.039 | <0.001 |

| Female: Agriculture (n = 81,464) | 18.181 | 16.848 | 22.713 | 9.075 | 5.030 | 21.959 | <0.001 |

| Female: Non-Agriculture (n = 81,464) | 18.420 | 16.954 | 21.733 | 19.247 | 25.613 | 19.598 | <0.001 |

| Region (n = 591,378) | <0.001 | ||||||

| Rural | 65.234 | 64.951 | 69.206 | 52.477 | 25.144 | 60.862 | |

| Urban | 34.766 | 35.049 | 30.794 | 47.523 | 74.856 | 39.138 | |

| Health Insurance Enrollment | Health Insurance Choices | |||

|---|---|---|---|---|

| Chakravarti and Shankar [15] | Our Study | Chakravarti and Shankar [15] | Our Study | |

| Household Asset Variables | ||||

| Medium Asset | Positive effect | No effect | Positive effect on public and private HI | Positive effect on private HI |

| High Asset | Positive effect | Positive effect (overall) | Positive effect on public and private HI | Positive effect on private HI |

| Media Exposure Variables | ||||

| Newspaper | Positive effect | Positive effect (urban and overall) | Positive effect on CBHI (urban) and private HI | Positive effect on private HI (urban and overall) |

| Radio | Positive effect (urban and overall) | No effect | Positive effect on private HI (urban and overall sample) | Negative effect on CBHI (rural) |

| Television | Positive effect | No change | Positive effect on all types of HI | Positive effect on public HI (rural and overall) and private HI (urban) |

| Dependency Variables | ||||

| High Asset * # above 60 | No effect | No change | No effect | No change |

| # above 60 | No effect | Positive effect | Positive effect on private HI (overall) | Positive effect on public HI (rural and overall) |

| # between 0 and 5 | No effect | Negative effect (urban and overall) | Negative effect on public HI (urban) | No change |

| # between 6 and 15 | No effect | Positive effect (rural) | No effect | Positive effect on public HI (rural and overall) |

| Caste | ||||

| SC | No effect | Positive effect (rural and overall) | No effect | Positive effect on public HI (rural and overall), CBHI (urban), and private HI (urban) |

| ST | No effect | Positive effect (rural and overall) | No effect | Positive effect on public HI (rural) |

| OBC | No effect | No change | Negative effect on public HI (urban) | Positive effect on CBHI (urban) and private HI. |

| SC * Medium Asset | Positive effect (rural and overall) | No effect | Positive effect on public HI (overall) | Negative effect on CBHI and private HI (urban) |

| SC * High Asset | Positive effect (rural and overall) | Negative effect (overall) | Positive effect on public HI (rural and overall), Negative on CBHI (rural) | Negative effect on CBHI and private HI (urban) |

| ST * Medium Asset | No effect | No change | No effect | Positive effect on CBHI (rural and overall) |

| ST * High Asset | Negative effect (overall) | No change | Negative effect on private HI (overall) | Negative effect on CBHI (rural) and private HI (urban and overall) |

| OBC * Medium Asset | No effect | No change | Negative effect on private HI (urban) | Negative effect on CBHI and private HI (urban) and positive effect on CBHI (rural) |

| OBC * High Asset | No effect | Negative effect (overall) | Negative effect on private HI (urban and overall) | Negative effect on public HI (urban) and private HI (urban and overall) |

| Control Variables | ||||

| Hindu | Positive effect | Positive effect (rural) | Positive effect on public HI and CBHI (overall) | Positive effect on public HI (rural) |

| Muslim | Negative effect (urban and overall) | No change | Negative effect on private HI (urban and overall) | Negative effect on CBHI (urban) |

| Female-headed HH | No effect | No change | No effect | No change |

| HH head’s age | Positive effect | No change | Positive effect on public and private HI | Positive effect on public HI and CBHI (rural and overall) |

| HH head’s education | Positive effect | Positive effect (urban) | Positive effect | Negative effect on public HI (overall), positive effect private HI |

| Agriculture: Male | Positive effect (overall) | No effect | Positive effect on CBHI (overall) | No effect |

| Non-Agriculture: Male | Positive effect (urban and overall) | No effect | Positive effect on public and private HI (urban and overall) | Positive effect on private HI (urban and overall) |

| Agriculture: Female | Positive effect (rural and overall) | No change | Positive effect on private HI (overall) | Positive effect on public HI (rural and overall) |

| Non-Agriculture: Female | Positive effect (rural) | Positive effect | Positive effect on CBHI (rural and overall) | Positive effect on public HI (rural and overall) |

| Region | Positive effect | Negative effect | Positive effect on public and private HI | Negative effect on public HI and positive effect on private HI |

| Urban | Rural | Combined | ||||

|---|---|---|---|---|---|---|

| Marginal Effects | p-Value † | Marginal Effects | p-Value † | Marginal Effects | p-Value † | |

| Household Asset Variables | ||||||

| Medium Asset | −0.085 | 0.110 | −0.001 | 0.961 | −0.016 | 0.305 |

| High Asset | 0.001 | 0.988 | −0.002 | 0.904 | 0.040 * | 0.019 |

| Media Exposure Variables | ||||||

| Newspaper | 0.022 * | 0.033 | 0.006 | 0.316 | 0.012 * | 0.024 |

| Radio | 0.005 | 0.727 | −0.000188 | 0.979 | 0.001 | 0.874 |

| Television | 0.031 | 0.098 | 0.028 *** | 0.000 | 0.032 *** | 0.000 |

| Dependency Variables | ||||||

| High Asset * # above 60 | −0.013 | 0.499 | −0.002 | 0.845 | −0.002 | 0.833 |

| # above 60 | 0.030 * | 0.032 | 0.013 ** | 0.006 | 0.015 ** | 0.002 |

| # between 0 and 5 | −0.027 *** | 0.000 | −0.005 | 0.075 | −0.012 *** | 0.000 |

| # between 6 and 15 | −0.001 | 0.899 | 0.005 * | 0.018 | 0.002 | 0.206 |

| Caste | ||||||

| SC | −0.032 | 0.568 | 0.055 *** | 0.000 | 0.050 ** | 0.001 |

| ST | −0.028 | 0.623 | 0.034 * | 0.018 | 0.034 * | 0.027 |

| OBC | −0.006 | 0.918 | 0.011 | 0.416 | 0.012 | 0.401 |

| SC * Medium Asset | 0.064 | 0.335 | −0.010 | 0.579 | −0.008 | 0.679 |

| SC * High Asset | 0.0004251 | 0.995 | −0.011 | 0.613 | −0.056 ** | 0.006 |

| ST * Medium Asset | 0.064 | 0.421 | 0.008 | 0.734 | 0.006 | 0.808 |

| ST * High Asset | 0.008 | 0.906 | −0.031 | 0.241 | −0.054 * | 0.019 |

| OBC * Medium Asset | 0.062 | 0.351 | 0.004 | 0.802 | 0.015 | 0.389 |

| OBC * High Asset | −0.044 | 0.460 | 0.013 | 0.503 | −0.049 ** | 0.003 |

| Control Variables | ||||||

| Hindu | −0.019 | 0.400 | 0.035 * | 0.010 | 0.015 | 0.210 |

| Muslim | −0.053 * | 0.036 | 0.022 | 0.220 | −0.006 | 0.675 |

| Female-headed HH | −0.010 | 0.470 | −0.005 | 0.472 | −0.007 | 0.294 |

| HH head’s age | 0.006 * | 0.024 | 0.013 *** | 0.000 | 0.011 *** | 0.000 |

| Age square | −0.000047 | 0.079 | −0.0001142 *** | 0.000 | −0.000092 *** | 0.000 |

| HH head’s education | 0.003 * | 0.031 | −0.00026 | 0.673 | 0.001 | 0.144 |

| Agriculture: Male | 0.014 | 0.529 | −0.002 | 0.854 | 0.003 | 0.756 |

| Non-Agriculture: Male | 0.028 | 0.130 | 0.005 | 0.603 | 0.011 | 0.181 |

| Agriculture: Female | 0.016 | 0.477 | 0.027 *** | 0.000 | 0.030 *** | 0.000 |

| Non-Agriculture: Female | 0.024 * | 0.023 | 0.028 *** | 0.000 | 0.028 *** | 0.000 |

| Region | N.A. | N.A. | N.A. | N.A. | −0.041 *** | 0.000 |

| No. of observations | 21850 | 51769 | 73619 | |||

| Pseudo R square | 0.1451 | 0.2448 | 0.2019 | |||

| Log pseudolikelihood | −13.6521 | −22.4992 | −36.5230 | |||

| A. Outcome 1: Public H.I. | ||||||

|---|---|---|---|---|---|---|

| Urban | Rural | Combined | ||||

| RRR | p-Value † | RRR | p-Value † | RRR | p-Value † | |

| Household Asset Variables | ||||||

| Medium Asset | 0.577 | 0.094 | 0.998 | 0.985 | 0.921 | 0.446 |

| High Asset | 0.610 | 0.117 | 0.841 | 0.169 | 0.886 | 0.283 |

| Media Exposure Variables | ||||||

| Newspaper | 1.042 | 0.503 | 1.002 | 0.969 | 1.014 | 0.673 |

| Radio | 0.988 | 0.884 | 0.967 | 0.500 | 0.974 | 0.562 |

| Television | 1.182 | 0.175 | 1.214 *** | 0.000 | 1.241 *** | 0.000 |

| Dependency Variables | ||||||

| Highest Asset * # above 60 | 0.866 | 0.254 | 0.987 | 0.883 | 0.935 | 0.359 |

| # above 60 | 1.121 | 0.213 | 1.085 * | 0.021 | 1.082 * | 0.025 |

| # between 0 and 5 | 0.844 *** | 0.000 | 0.971 | 0.129 | 0.932 *** | 0.000 |

| # between 6 and 15 | 1.013 | 0.643 | 1.039 ** | 0.005 | 1.029 * | 0.022 |

| Caste | ||||||

| SC | 0.752 | 0.376 | 1.416 ** | 0.001 | 1.319 ** | 0.006 |

| ST | 0.790 | 0.481 | 1.250 * | 0.027 | 1.185 | 0.087 |

| OBC | 0.824 | 0.567 | 1.062 | 0.524 | 1.038 | 0.696 |

| SC * Medium Asset | 1.496 | 0.261 | 0.962 | 0.772 | 0.972 | 0.824 |

| SC * High Asset | 1.493 | 0.257 | 1.008 | 0.960 | 0.930 | 0.623 |

| ST * Medium Asset | 1.519 | 0.334 | 1.043 | 0.812 | 1.065 | 0.691 |

| ST * High Asset | 1.818 | 0.111 | 0.826 | 0.342 | 1.062 | 0.724 |

| OBC * Medium Asset | 1.521 | 0.249 | 1.027 | 0.828 | 1.102 | 0.405 |

| OBC * High Asset | 1.261 | 0.504 | 1.156 | 0.279 | 1.013 | 0.917 |

| Control Variables | ||||||

| Hindu | 0.918 | 0.501 | 1.323 ** | 0.004 | 1.140 | 0.088 |

| Muslim | 0.865 | 0.335 | 1.197 | 0.154 | 1.070 | 0.486 |

| Female-headed HH | 0.887 | 0.175 | 0.965 | 0.467 | 0.932 | 0.113 |

| HH head’s age | 1.026 | 0.207 | 1.099 *** | 0.000 | 1.073 *** | 0.000 |

| Age square | 1.000 | 0.369 | 0.999 *** | 0.000 | 0.999 *** | 0.000 |

| HH head’s education | 0.992 | 0.284 | 0.993 | 0.091 | 0.992 * | 0.036 |

| Agriculture: Male | 0.967 | 0.838 | 0.992 | 0.906 | 0.994 | 0.918 |

| Non-Agriculture: Male | 1.066 | 0.595 | 1.038 | 0.571 | 1.047 | 0.425 |

| Agriculture: Female | 1.085 | 0.532 | 1.203 *** | 0.000 | 1.197 *** | 0.000 |

| Non-Agriculture: Female | 1.122 | 0.075 | 1.189 *** | 0.000 | 1.168 *** | 0.000 |

| Region | N.A. | N.A. | N.A. | N.A. | 0.715 *** | 0.000 |

| B. Outcome 2: CBHI | ||||||

| Urban | Rural | Combined | ||||

| RRR | p-Value † | RRR | p-Value † | RRR | p-Value † | |

| Household Asset Variables | ||||||

| Medium Asset | 414,263.200 *** | 0.000 | 0.237 | 0.187 | 0.322 | 0.209 |

| High Asset | 700,030.700 *** | 0.000 | 0.478 | 0.289 | 1.027 | 0.969 |

| Media Exposure Variables | ||||||

| Newspaper | 1.773 | 0.060 | 1.647 | 0.211 | 1.834 | 0.075 |

| Radio | 0.930 | 0.782 | 0.092 *** | 0.000 | 0.602 | 0.215 |

| Television | 0.544 | 0.256 | 0.823 | 0.664 | 0.545 | 0.132 |

| Dependency Variables | ||||||

| Highest Asset * # above 60 | 1.884 | 0.161 | 1.987 | 0.302 | 0.897 | 0.850 |

| # above 60 | 1.336 | 0.295 | 0.913 | 0.809 | 0.906 | 0.754 |

| # between 0 and 5 | 0.838 | 0.239 | 1.147 | 0.340 | 1.229 | 0.135 |

| # between 6 and 15 | 1.039 | 0.656 | 0.901 | 0.506 | 0.958 | 0.729 |

| Caste | ||||||

| SC | 263,280.000 *** | 0.000 | 0.409 | 0.234 | 0.418 | 0.241 |

| ST | 0.605 | 0.154 | 0.116 | 0.076 | 0.117 | 0.069 |

| OBC | 289,420.400 *** | 0.000 | 0.336 | 0.133 | 0.494 | 0.339 |

| SC * Medium Asset | 0.000003 *** | 0.000 | 1.851 | 0.704 | 6.389 | 0.169 |

| SC * High Asset | 0.000001 *** | 0.000 | 3.993 | 0.218 | 1.292 | 0.796 |

| ST * Medium Asset | 0.912 | 0.933 | 73.535 * | 0.017 | 39.110 * | 0.033 |

| ST * High Asset | 1.552 | 0.549 | 0.001 *** | 0.000 | 11.839 | 0.069 |

| OBC * Medium Asset | 0.000004 *** | 0.000 | 12.446 * | 0.048 | 7.178 | 0.062 |

| OBC * High Asset | 0.000002 *** | 0.000 | 2.810 | 0.297 | 1.788 | 0.493 |

| Control Variables | ||||||

| Hindu | 0.486 | 0.133 | 0.862 | 0.769 | 0.868 | 0.819 |

| Muslim | 0.173 ** | 0.004 | 0.485 | 0.378 | 0.333 | 0.191 |

| Female-headed HH | 1.539 | 0.202 | 1.491 | 0.487 | 1.135 | 0.781 |

| HH head’s age | 1.222 *** | 0.000 | 1.164 | 0.184 | 1.296 * | 0.016 |

| Age square | 0.998 *** | 0.000 | 0.998 | 0.190 | 0.998 * | 0.025 |

| HH head’s education | 0.995 | 0.877 | 1.009 | 0.833 | 1.036 | 0.324 |

| Agriculture: Male | 1.618 | 0.126 | 2.500 | 0.064 | 1.563 | 0.274 |

| Non-Agriculture: Male | 1.716 | 0.069 | 1.201 | 0.712 | 0.775 | 0.532 |

| Agriculture: Female | 1.331 | 0.566 | 0.564 | 0.248 | 0.583 | 0.218 |

| Non-Agriculture: Female | 1.329 | 0.326 | 0.290 | 0.098 | 1.089 | 0.824 |

| Region | N.A. | N.A. | N.A. | N.A. | 1.331 | 0.426 |

| C. Outcome 3: Private H.I. | ||||||

| Urban | Rural | Combined | ||||

| RRR | p-Value † | RRR | p-Value † | RRR | p-Value † | |

| Household Asset Variables | ||||||

| Medium Asset | 68654.040 *** | 0.000 | 4.246 ** | 0.005 | 3.509 * | 0.011 |

| High Asset | 616760.200 *** | 0.000 | 11.242 *** | 0.000 | 18.188 *** | 0.000 |

| Media Exposure Variables | ||||||

| Newspaper | 1.477 * | 0.025 | 1.322 | 0.082 | 1.433 ** | 0.003 |

| Radio | 1.229 | 0.189 | 1.166 | 0.411 | 1.172 | 0.209 |

| Television | 3.399 * | 0.021 | 0.909 | 0.726 | 1.476 | 0.089 |

| Dependency Variables | ||||||

| Highest Asset * # above 60 | 0.923 | 0.745 | 1.236 | 0.427 | 1.051 | 0.775 |

| # above 60 | 1.249 | 0.210 | 0.902 | 0.545 | 1.074 | 0.558 |

| # between 0 and 5 | 0.909 | 0.447 | 0.933 | 0.396 | 0.917 | 0.319 |

| # between 6 and 15 | 0.946 | 0.409 | 0.948 | 0.440 | 0.943 | 0.246 |

| Caste | ||||||

| SC | 86,983.790 *** | 0.000 | 1.945 | 0.328 | 2.624 | 0.120 |

| ST | 0.957 | 0.880 | 1.197 | 0.769 | 1.776 | 0.347 |

| OBC | 93,107.950 *** | 0.000 | 2.712 * | 0.046 | 3.609 ** | 0.008 |

| SC * Medium Asset | 0.000018 *** | 0.000 | 0.350 | 0.180 | 0.371 | 0.156 |

| SC * High Asset | 0.000007 *** | 0.000 | 0.341 | 0.179 | 0.221 * | 0.020 |

| ST * Medium Asset | 2.777 | 0.115 | 1.247 | 0.723 | 1.118 | 0.857 |

| ST * High Asset | 0.215 ** | 0.001 | 0.572 | 0.463 | 0.154 ** | 0.006 |

| OBC * Medium Asset | 0.00002 *** | 0.000 | 0.356 | 0.080 | 0.372 | 0.073 |

| OBC * High Asset | 0.000005 *** | 0.000 | 0.390 | 0.087 | 0.148 *** | 0.000 |

| Control Variables | ||||||

| Hindu | 1.275 | 0.396 | 1.392 | 0.352 | 1.439 | 0.121 |

| Muslim | 0.633 | 0.231 | 0.793 | 0.586 | 0.729 | 0.303 |

| Female-headedHH | 0.882 | 0.527 | 0.742 | 0.158 | 0.850 | 0.285 |

| HH head’s age | 0.997 | 0.909 | 0.998 | 0.946 | 1.001 | 0.951 |

| Age square | 1.000 | 0.611 | 1.000 | 0.659 | 1.000 | 0.598 |

| HH head’s education | 1.144 *** | 0.000 | 1.072 *** | 0.000 | 1.125 *** | 0.000 |

| Agriculture: Male | 1.922 | 0.107 | 0.891 | 0.654 | 1.296 | 0.293 |

| Non-Agriculture: Male | 2.271 * | 0.023 | 1.327 | 0.259 | 1.755 * | 0.011 |

| Agriculture: Female | 1.082 | 0.892 | 0.994 | 0.979 | 1.012 | 0.959 |

| Non-Agriculture: Female | 1.067 | 0.636 | 1.417 | 0.060 | 1.128 | 0.291 |

| Region | N.A. | N.A. | N.A. | N.A. | 1.349 * | 0.014 |

| D. Outcome 4: Others | ||||||

| Urban | Rural | Combined | ||||

| RRR | p-Value † | RRR | p-Value † | RRR | p-Value † | |

| Household Asset Variables | ||||||

| Medium Asset | N.A. | N.A. | 0.868 | 0.704 | 0.994 | 0.986 |

| High Asset | N.A. | N.A. | 0.620 | 0.316 | 1.185 | 0.653 |

| Media Exposure Variables | ||||||

| Newspaper | N.A. | N.A. | 1.333 * | 0.037 | 1.458 ** | 0.005 |

| Radio | N.A. | N.A. | 1.057 | 0.759 | 0.954 | 0.776 |

| Television | N.A. | N.A. | 1.383 | 0.137 | 1.251 | 0.320 |

| Dependency Variables | ||||||

| Highest Asset * # above 60 | N.A. | N.A. | 1.023 | 0.943 | 1.575 | 0.098 |

| # above 60 | N.A. | N.A. | 1.340 * | 0.010 | 1.375 ** | 0.002 |

| # between 0 and 5 | N.A. | N.A. | 1.009 | 0.903 | 0.934 | 0.324 |

| # between 6 and 15 | N.A. | N.A. | 1.006 | 0.895 | 1.006 | 0.889 |

| Caste | ||||||

| SC | N.A. | N.A. | 1.653 | 0.081 | 1.589 | 0.120 |

| ST | N.A. | N.A. | 1.014 | 0.965 | 1.016 | 0.962 |

| OBC | N.A. | N.A. | 1.211 | 0.531 | 1.248 | 0.480 |

| SC * Medium Asset | N.A. | N.A. | 0.418 | 0.062 | 0.379 * | 0.032 |

| SC * High Asset | N.A. | N.A. | 1.525 | 0.420 | 0.325 * | 0.010 |

| ST * Medium Asset | N.A. | N.A. | 0.675 | 0.472 | 0.651 | 0.417 |

| ST * High Asset | N.A. | N.A. | 1.207 | 0.750 | 0.884 | 0.859 |

| OBC * Medium Asset | N.A. | N.A. | 0.864 | 0.732 | 0.862 | 0.722 |

| OBC * High Asset | N.A. | N.A. | 1.109 | 0.833 | 0.528 | 0.108 |

| Control Variables | ||||||

| Hindu | N.A. | N.A. | 0.665 | 0.138 | 0.545 * | 0.025 |

| Muslim | N.A. | N.A. | 0.691 | 0.404 | 0.331 ** | 0.004 |

| Female-headed HH | N.A. | N.A. | 1.335 | 0.158 | 1.499 | 0.056 |

| HH head’s age | N.A. | N.A. | 1.068 | 0.088 | 1.105 ** | 0.002 |

| Age square | N.A. | N.A. | 0.999 | 0.119 | 0.999 ** | 0.003 |

| HH head’s education | N.A. | N.A. | 1.043 * | 0.025 | 1.024 | 0.217 |

| Agriculture: Male | N.A. | N.A. | 0.945 | 0.806 | 1.067 | 0.725 |

| Non-Agriculture: Male | N.A. | N.A. | 1.157 | 0.487 | 1.306 | 0.103 |

| Agriculture: Female | N.A. | N.A. | 1.057 | 0.723 | 1.103 | 0.530 |

| Non-Agriculture: Female | N.A. | N.A. | 1.007 | 0.972 | 1.124 | 0.555 |

| Region | N.A. | N.A. | N.A. | N.A. | 0.746 | 0.090 |

| No. of observations | 21,592 | 51,506 | 72,660 | |||

| Pseudo R square | 0.183 | 0.251 | 0.224 | |||

| Log pseudolikelihood | −162.217 | −247.842 | −415.239 | |||

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Ambade, P.N.; Gerald, J.; Rahman, T. Wealth Status and Health Insurance Enrollment in India: An Empirical Analysis. Healthcare 2023, 11, 1343. https://doi.org/10.3390/healthcare11091343

Ambade PN, Gerald J, Rahman T. Wealth Status and Health Insurance Enrollment in India: An Empirical Analysis. Healthcare. 2023; 11(9):1343. https://doi.org/10.3390/healthcare11091343

Chicago/Turabian StyleAmbade, Preshit Nemdas, Joe Gerald, and Tauhidur Rahman. 2023. "Wealth Status and Health Insurance Enrollment in India: An Empirical Analysis" Healthcare 11, no. 9: 1343. https://doi.org/10.3390/healthcare11091343

APA StyleAmbade, P. N., Gerald, J., & Rahman, T. (2023). Wealth Status and Health Insurance Enrollment in India: An Empirical Analysis. Healthcare, 11(9), 1343. https://doi.org/10.3390/healthcare11091343