Modeling of the Bitcoin Volatility through Key Financial Environment Variables: An Application of Conditional Correlation MGARCH Models

Abstract

1. Introduction

2. Literature Review

3. Materials and Methods

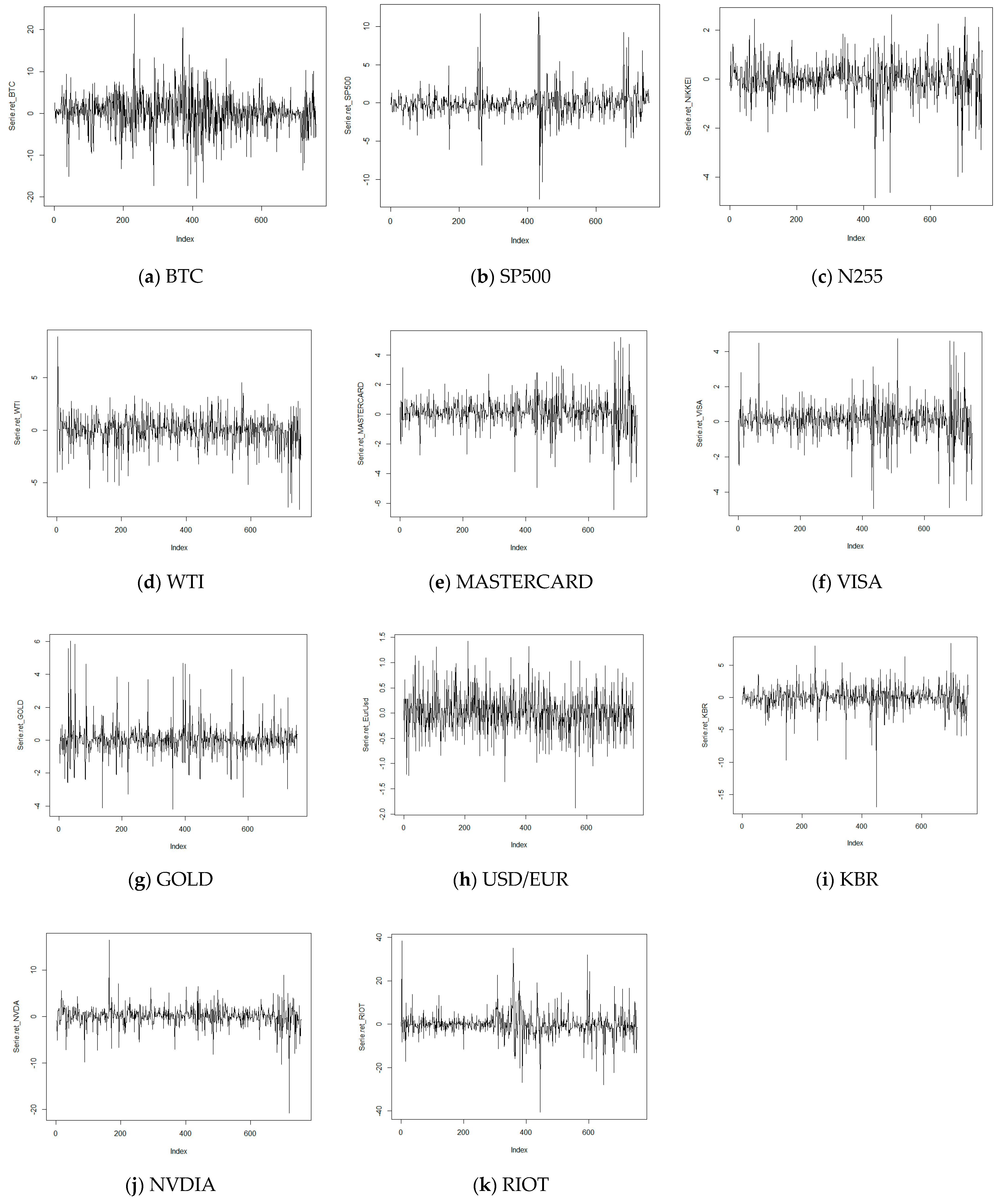

3.1. Data and Variables

3.2. Methodology

4. Results

5. Discussion

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

Appendix A

{kind=link}

| BTC | SP500 | GOLD | WTI | RIOT | NIKKEI | USD/EUR | KBR | VISA | MAST | NVDA | |

| BTC | 1.000 | ||||||||||

| SP500 | −0.0539 | 1.000 | |||||||||

| GOLD | 0.0105 | 0.0049 | 1.000 | ||||||||

| WTI | 0.0282 | −0.1040 | 0.0033 | 1.000 | |||||||

| RIOT | 0.0689 * | −0.1962 | −0.0246 | 0.0470 | 1.000 | ||||||

| NIKKEI | −0.0262 | −0.1066 | −0.0955 | 0.1180 | 0.0282 | 1.000 | |||||

| USD/EUR | −0.0113 | −0.0793 | 0.2145 | 0.0607 | 0.0553 | −0.0239 | 1.000 | ||||

| KBR | 0.0783 ** | −0.0375 | −0.0549 | 0.0078 | 01158 | 0.0576 | 0.0323 | 1.000 | |||

| VISA | 0.0831 ** | −0.5938 | −0.0162 | 0.0337 | 0.1544 | 0.0946 | 0.0404 | −0.0060 | 1.000 | ||

| MAST | 0.0578 | −0.5660 | −0.0030 | 0.0566 | 0.1911 | 0.0994 | 0.0519 | −0.0204 | 0.8842 | 1.000 | |

| NVDA | 0.0977 ** | −0.4458 | −0.0356 | 0.0179 | 0.1445 | 0.0607 | −0.0725 | −0.0038 | 0.5121 | 0.5121 | 1.000 |

References

- Nakamato, S. Bitcoin: A Peer-toPeer Electronic Cash System. Bitcoin 2009, 4, 1–9. [Google Scholar]

- Weber, B. Bitcoin and the legitimacy crisis of money. Camb. J. Econ. 2015, 40, 17–41. [Google Scholar] [CrossRef]

- Bouri, E.; Gupta, R.; Tiwari, A.K.; Roubaud, D. Does Bitcoin hedge global uncertainty? Evidence from wavelet-based quantile-in-quantile regressions. Financ. Res. Lett. 2017, 23, 87–95. [Google Scholar] [CrossRef]

- Statista. Market Capitalization of Cryptocurrencies from 2013 to 2019. Available online: https://www.statista.com/statistics/730876/cryptocurrency-maket-value/ (accessed on 12 October 2020).

- Statista. Bitcoin Price Index from July 2012 to July 2020. Available online: https://www.statista.com/statistics/326707/bitcoin-price-index/ (accessed on 12 October 2020).

- Papadimitriou, T.; Gogas, P.; Gkatzoglou, F. The evolution of the cryptocurrencies market: A complex networks approach. J. Comput. Appl. Math. 2020, 376, 112831. [Google Scholar] [CrossRef]

- Baur, D.G.; Hong, K.H.; Lee, A.D. Bitcoin: Medium of exchange or speculative assets? J. Int. Financ. Mark. Inst. Money 2018, 54, 177–189. [Google Scholar] [CrossRef]

- Brauneis, A.; Mestel, R. Price discovery of cryptocurrencies: Bitcoin and beyond. Econ. Lett. 2018, 165, 58–61. [Google Scholar] [CrossRef]

- Swan, M. Blockchain: Blueprint for a New Economy; O’Reilly Media, Inc.: Newton, MA, USA, 2015; ISBN 978-1-4919-2044-2. [Google Scholar]

- Underwood, S. Blockchain beyond bitcoin. Commun. ACM 2016, 59, 15–17. [Google Scholar] [CrossRef]

- CoinMarketCap. Available online: https://coinmarketcap.com (accessed on 15 January 2021).

- Bitcoin Is Fiat Money, Too. Available online: https://www.economist.com/free-exchange/2017/09/22/bitcoin-is-fiat-money-too (accessed on 12 October 2020).

- Dorfman, J. Bitcoin Is An Asset, Not a Currency. Available online: https://www.forbes.com/sites/jeffreydorfman/2017/05/17/bitcoin-is-an-asset-not-a-currency/ (accessed on 12 October 2020).

- Fernández-Villaverde, J.; Sanches, D.R. On the Economics of Digital Currencies; Working Paper No. 18-7; Federal Reserve Bank of Philadelphia: Philadelphia, PA, USA, 2018. [Google Scholar] [CrossRef]

- Hazlett, P.K.; Luther, W.J. Is bitcoin money? And what that means. Q. Rev. Econ. Financ. 2020, 77, 144–149. [Google Scholar] [CrossRef]

- Glaser, F.; Zimmermann, K.; Haferkorn, M.; Weber, M.C.; Siering, M. Bitcoin—Asset or currency? Revealing users’ hidden intentions. In Proceedings of the ECIS 2014 Proceedings—22nd Europe Conference Information Systems, Tel Aviv, Israel, 9–11 June 2014. [Google Scholar]

- Yermack, D. Is Bitcoin a Real Currency? An Economic Appraisal. In Handbook of Digital Currency: Bitcoin, Innovation, Financial Instruments, and Big Data; Elsevier: Amsterdam, The Netherlands, 2015; pp. 31–43. ISBN 9780128023518. [Google Scholar] [CrossRef]

- Baek, C.; Elbeck, M. Bitcoins as an investment or speculative vehicle? A first look. Appl. Econ. Lett. 2015, 22, 30–34. [Google Scholar] [CrossRef]

- White, R.; Marinakis, Y.; Islam, N.; Walsh, S. Is Bitcoin a currency, a technology-based product, or something else? Technol. Forecast. Soc. Chang. 2020, 151, 119877. [Google Scholar] [CrossRef]

- Bouri, E.; Shahzad, S.J.H.; Roubaud, D.; Kristoufek, L.; Lucey, B. Bitcoin, gold, and commodities as safe havens for stocks: New insight through wavelet analysis. Q. Rev. Econ. Financ. 2020, 77, 156–164. [Google Scholar] [CrossRef]

- Dyhrberg, A.H.; Foley, S.; Svec, J. How investible is Bitcoin? Analyzing the liquidity and transaction costs of Bitcoin markets. Econ. Lett. 2018, 171, 140–143. [Google Scholar] [CrossRef]

- Koutmos, D. Liquidity uncertainty and Bitcoin’s market microstructure. Econ. Lett. 2018, 172, 97–101. [Google Scholar] [CrossRef]

- Scharnowski, S. Understanding Bitcoin liquidity. Financ. Res. Lett. 2020, 101477. [Google Scholar] [CrossRef]

- Urquhart, A. The inefficiency of Bitcoin. Econ. Lett. 2016, 148, 80–82. [Google Scholar] [CrossRef]

- Nadarajah, S.; Chu, J. On the inefficiency of Bitcoin. Econ. Lett. 2017, 150, 6–9. [Google Scholar] [CrossRef]

- Tiwari, A.K.; Jana, R.K.; Das, D.; Roubaud, D. Informational efficiency of Bitcoin—An extension. Econ. Lett. 2018, 163, 106–109. [Google Scholar] [CrossRef]

- Cheah, E.T.; Mishra, T.; Parhi, M.; Zhang, Z. Long Memory Interdependency and Inefficiency in Bitcoin Markets. Econ. Lett. 2018, 167, 18–25. [Google Scholar] [CrossRef]

- Kristoufek, L. On Bitcoin markets (in)efficiency and its evolution. Phys. A Stat. Mech. Its Appl. 2018, 503, 257–262. [Google Scholar] [CrossRef]

- Nan, Z.; Kaizoji, T. Market efficiency of the bitcoin exchange rate: Weak and semi-strong form tests with the spot, futures and forward foreign exchange rates. Int. Rev. Financ. Anal. 2019, 64, 273–281. [Google Scholar] [CrossRef]

- Yu, M. Forecasting Bitcoin volatility: The role of leverage effect and uncertainty. Phys. A Stat. Mech. Its Appl. 2019, 533, 120707. [Google Scholar] [CrossRef]

- Zhang, H.; Li, S. Forecasting volatility in financial markets. Key Eng. Mater. 2010, 439–440, 679–682. [Google Scholar] [CrossRef]

- McAleer, M.; Medeiros, M.C. Realized volatility: A review. Econom. Rev. 2008, 27, 10–45. [Google Scholar] [CrossRef]

- Balcilar, M.; Bouri, E.; Gupta, R.; Roubaud, D. Can volume predict Bitcoin returns and volatility? A quantiles-based approach. Econ. Model. 2017, 64, 74–81. [Google Scholar] [CrossRef]

- Bariviera, A.F. The inefficiency of bitcoin revisited: A dynamic approach. arXiv 2017, arXiv:1709.08090. [Google Scholar] [CrossRef]

- Katsiampa, P. Volatility estimation for Bitcoin: A comparison of GARCH models. Econ. Lett. 2017, 158, 3–6. [Google Scholar] [CrossRef]

- Bollerslev, T. Generalized autoregressive conditional heteroskedasticity. J. Econom. 1986, 31, 307–327. [Google Scholar] [CrossRef]

- Engle, R.F. Autoregressive Conditional Heteroscedasticity with Estimates of the Variance of United Kingdom Inflation. Econometrica 1982, 50, 987. [Google Scholar] [CrossRef]

- Dyhrberg, A.H. Bitcoin, gold and the dollar—A GARCH volatility analysis. Financ. Res. Lett. 2016, 16, 85–92. [Google Scholar] [CrossRef]

- Manganelli, S.; Engle, R. Value at Risk Models in Finance. Available online: https://www.ecb.europa.eu/pub/pdf/scpwps/ecbwp075.pdf (accessed on 18 November 2020).

- Ardia, D.; Bluteau, K.; Rüede, M. Regime changes in Bitcoin GARCH volatility dynamics. Financ. Res. Lett. 2019, 29, 266–271. [Google Scholar] [CrossRef]

- Gronwald, M. Is Bitcoin a Commodity? On price jumps, demand shocks, and certainty of supply. J. Int. Money Financ. 2019, 97, 86–92. [Google Scholar] [CrossRef]

- Hung, J.C.; Liu, H.C.; Yang, J.J. Improving the realized GARCH’s volatility forecast for Bitcoin with jump-robust estimators. N. Am. J. Econ. Financ. 2020, 52, 101165. [Google Scholar] [CrossRef]

- Trucíos, C. Forecasting Bitcoin risk measures: A robust approach. Int. J. Forecast. 2019, 35, 836–847. [Google Scholar] [CrossRef]

- López-Cabarcos, M.Á.; Pérez-Pico, A.M.; Piñeiro-Chousa, J.; Šević, A. Bitcoin volatility, stock market and investor sentiment. Are they connected? Financ. Res. Lett. 2020, 38, 101399. [Google Scholar] [CrossRef]

- Chan, W.H.; Le, M.; Wu, Y.W. Holding Bitcoin longer: The dynamic hedging abilities of Bitcoin. Q. Rev. Econ. Financ. 2019, 71, 107–113. [Google Scholar] [CrossRef]

- Kumar, A.S.; Anandarao, S. Volatility spillover in crypto-currency markets: Some evidences from GARCH and wavelet analysis. Phys. A Stat. Mech. Its Appl. 2019, 524, 448–458. [Google Scholar] [CrossRef]

- Guesmi, K.; Saadi, S.; Abid, I.; Ftiti, Z. Portfolio diversification with virtual currency: Evidence from bitcoin. Int. Rev. Financ. Anal. 2019, 63, 431–437. [Google Scholar] [CrossRef]

- Kyriazis, Ν.A.; Daskalou, K.; Arampatzis, M.; Prassa, P.; Papaioannou, E. Estimating the volatility of cryptocurrencies during bearish markets by employing GARCH models. Heliyon 2019, 5, e02239. [Google Scholar] [CrossRef]

- Engle, R.F.; Lilien, D.M.; Robins, R.P. Estimating Time Varying Risk Premia in the Term Structure: The Arch-M Model. Econometrica 1987, 55, 391. [Google Scholar] [CrossRef]

- Engle, R. Dynamic conditional correlation: A simple class of multivariate generalized autoregressive conditional heteroskedasticity models. J. Bus. Econ. Stat. 2002, 20, 339–350. [Google Scholar] [CrossRef]

- Tse, Y.K.; Tsui, A.K.C. A multivariate generalized autoregressive conditional heteroscedasticity model with time-varying correlations. J. Bus. Econ. Stat. 2002, 20, 351–362. [Google Scholar] [CrossRef]

- Ali, O.; Ally, M.; Clutterbuck; Dwivedi, Y. The state of play of blockchain technology in the financial services sector: A systematic literature review. Int. J. Inf. Manag. 2020, 54, 102199. [Google Scholar] [CrossRef]

- Ma, J.; Gans, J.S.; Tourky, R. Market Structure in Bitcoin Mining; National Bureau of Economic Research: Cambridge, MA, USA, 2018. [Google Scholar] [CrossRef]

- Luther, W.J.; Salter, A.W. Bitcoin and the bailout. Q. Rev. Econ. Financ. 2017, 66, 50–56. [Google Scholar] [CrossRef]

- Hui, C.H.; Lo, C.F.; Chau, P.H.; Wong, A. Does Bitcoin behave as a currency?: A standard monetary model approach. Int. Rev. Financ. Anal. 2020, 70, 101518. [Google Scholar] [CrossRef]

- IFRS-IFRIC. Holdings of Cryptocurrencies—June 2019. Available online: https://cdn.ifrs.org/-/media/feature/supporting-implementation/agenda-decisions/holdings-of-cryptocurrencies-june-2019.pdf (accessed on 18 November 2020).

- Hussain Shahzad, S.J.; Bouri, E.; Roubaud, D.; Kristoufek, L. Safe haven, hedge and diversification for G7 stock markets: Gold versus bitcoin. Econ. Model. 2020, 87, 212–224. [Google Scholar] [CrossRef]

- Selgin, G. Synthetic commodity money. J. Financ. Stab. 2015, 17, 92–99. [Google Scholar] [CrossRef]

- Smales, L.A. Bitcoin as a safe haven: Is it even worth considering? Financ. Res. Lett. 2019, 30, 385–393. [Google Scholar] [CrossRef]

- Baur, D.G.; Lucey, B.M. Is gold a hedge or a safe haven? An analysis of stocks, bonds and gold. Financ. Rev. 2010, 45, 217–229. [Google Scholar] [CrossRef]

- Urquhart, A.; Zhang, H. Is Bitcoin a hedge or safe haven for currencies? An intraday analysis. Int. Rev. Financ. Anal. 2019, 63, 49–57. [Google Scholar] [CrossRef]

- Wang, G.; Tang, Y.; Xie, C.; Chen, S. Is bitcoin a safe haven or a hedging asset? Evidence from China. J. Manag. Sci. Eng. 2019, 4, 173–188. [Google Scholar] [CrossRef]

- Dyhrberg, A.H. Hedging capabilities of bitcoin. Is it the virtual gold? Financ. Res. Lett. 2016, 16, 139–144. [Google Scholar] [CrossRef]

- Selmi, R.; Mensi, W.; Hammoudeh, S.; Bouoiyour, J. Is Bitcoin a hedge, a safe haven or a diversifier for oil price movements? A comparison with gold. Energy Econ. 2018, 74, 787–801. [Google Scholar] [CrossRef]

- Brière, M.; Oosterlinck, K.; Szafarz, A. Virtual currency, tangible return: Portfolio diversification with bitcoin. J. Asset Manag. 2015, 16, 365–373. [Google Scholar] [CrossRef]

- Bouri, E.; Molnár, P.; Azzi, G.; Roubaud, D.; Hagfors, L.I. On the hedge and safe haven properties of Bitcoin: Is it really more than a diversifier? Financ. Res. Lett. 2017, 20, 192–198. [Google Scholar] [CrossRef]

- Bouri, E.; Jalkh, N.; Molnár, P.; Roubaud, D. Bitcoin for energy commodities before and after the December 2013 crash: Diversifier, hedge or safe haven? Appl. Econ. 2017, 49, 5063–5073. [Google Scholar] [CrossRef]

- Conlon, T.; Corbet, S.; McGee, R.J. Are cryptocurrencies a safe haven for equity markets? An international perspective from the COVID-19 pandemic. Res. Int. Bus. Financ. 2020, 54, 101248. [Google Scholar] [CrossRef]

- Ghabri, Y.; Guesmi, K.; Zantour, A. Bitcoin and liquidity risk diversification. Financ. Res. Lett. 2020, 101679. [Google Scholar] [CrossRef]

- Yang, R.; Yu, L.; Zhao, Y.; Yu, H.; Xu, G.; Wu, Y.; Liu, Z. Big data analytics for financial Market volatility forecast based on support vector machine. Int. J. Inf. Manag. 2020, 50, 452–462. [Google Scholar] [CrossRef]

- Andersen, T.G.; Bollerslev, T. Answering the Skeptics: Yes, Standard Volatility Models do Provide Accurate Forecasts. Int. Econ. Rev. (Philadelphia) 1998, 39, 885. [Google Scholar] [CrossRef]

- Gao, C.T.; Zhou, X.H. Forecasting VaR and ES using dynamic conditional score models and skew Student distribution. Econ. Model. 2016, 53, 216–223. [Google Scholar] [CrossRef]

- Conrad, C.; Custovic, A.; Ghysels, E. Long- and Short-Term Cryptocurrency Volatility Components: A GARCH-MIDAS Analysis. J. Risk Financ. Manag. 2018, 11, 23. [Google Scholar] [CrossRef]

- Bollerslev, T. Modelling the Coherence in Short-Run Nominal Exchange Rates: A Multivariate Generalized Arch Model. Rev. Econ. Stat. 1990, 72, 498. [Google Scholar] [CrossRef]

- Chan, F.; Lim, C.; McAleer, M. Modelling multivariate international tourism demand and volatility. Tour. Manag. 2005, 26, 459–471. [Google Scholar] [CrossRef]

- Gardebroek, C.; Hernandez, M.A. Do energy prices stimulate food price volatility? Examining volatility transmission between US oil, ethanol and corn markets. Energy Econ. 2013, 40, 119–129. [Google Scholar] [CrossRef]

- Garcia-Jorcano, L.; Benito, S. Studying the properties of the Bitcoin as a diversifying and hedging asset through a copula analysis: Constant and time-varying. Res. Int. Bus. Financ. 2020, 54, 101300. [Google Scholar] [CrossRef]

- Kwon, J.H. Tail behavior of Bitcoin, the dollar, gold and the stock market index. J. Int. Financ. Mark. Inst. Money 2020, 67, 101202. [Google Scholar] [CrossRef]

- Engle, R. Estimates of the Variance of US Inflation Base on the ARCH Model; University of California, San Diego Discussion Paper; University of California: San Diego, CA, USA, 1980; pp. 80–114. [Google Scholar]

- De Almeida, D.; Hotta, L.K.; Ruiz, E. MGARCH models: Trade-off between feasibility and flexibility. Int. J. Forecast. 2018, 34, 45–63. [Google Scholar] [CrossRef]

- Orskaug, E. Multivariate DCC-GARCH Model -With Various Error Distributions. Master’s Thesis, Institutt for Matematiske Fag, Norges Teknisk-Naturvitenskapelige Universitet, Trondheim, Norway, June 2009. [Google Scholar]

- Jarjour, R.; Chan, K.S. Dynamic conditional angular correlation. J. Econom. 2020, 216, 137–150. [Google Scholar] [CrossRef]

- Lanza, A.; Manera, M.; McAleer, M. Modeling dynamic conditional correlations in WTI oil forward and futures returns. Financ. Res. Lett. 2006, 3, 114–132. [Google Scholar] [CrossRef]

- Diebold, F.X.; Mariano, R.S. Comparing predictive accuracy. J. Bus. Econ. Stat. 2002, 20, 134–144. [Google Scholar] [CrossRef]

| Variable | N | Mean | Std. Dev | Min | Max |

|---|---|---|---|---|---|

| BTC | 757 | 55,660.54 | 3787.380 | 750.600 | 19,1870.00 |

| SP500 | 757 | 11.623 | 3.615 | 7.800 | 22.120 |

| RIOT | 757 | 6.554 | 5.889 | 1.350 | 38.600 |

| N225 | 757 | 21,179.261 | 1556.405 | 18,240.500 | 24,270.620 |

| WTI | 757 | 57.727 | 8.748 | 42.530 | 76.410 |

| GOLD | 757 | 1308.948 | 550.06 | 1134.550 | 1425.900 |

| USD/EUR | 757 | 1.151 | 0.55 | 10.39 | 1.251 |

| KBR | 757 | 17.479 | 20.52 | 13.630 | 21.910 |

| VISA | 757 | 113.281 | 20.901 | 75.430 | 150.790 |

| MAST | 757 | 156.609 | 36.897 | 10.180 | 223.770 |

| NVDA | 757 | 186.919 | 57.649 | 87.640 | 289.360 |

| CCC-MGARCH | DCC-MGARCH | VCC-MGARCH | |||||||

|---|---|---|---|---|---|---|---|---|---|

| Correlation | Coef. | Std. Error | z | Coef. | Std. Error | z | Coef. | Std. Error | z |

| BTC-RIOT | 0.715586 | 0.354285 | 20.2 ** | 0.61279 | 0.408964 | 1.50 * | 0.772695 | 0.386975 | 20.0 ** |

| BTC-VISA | 0.789188 | 0.362937 | 2.17 ** | 0.702872 | 0.413236 | 1.70 ** | 0.809611 | 0.390046 | 20.8 ** |

| BTC-MAST | 0.63838 | 0.363874 | 1.75 * | 0.602087 | 0.412589 | 1.46 | 0.65487 | 0.389324 | 1.68 * |

| BTC-NVDA | 0.95818 | 0.364196 | 2.63 ** | 0.817696 | 0.413916 | 1.98 ** | 0.1004301 | 0.389384 | 2.58 ** |

| BTC-KBR | 0.812567 | 0.364059 | 2.23 ** | 0.707863 | 0.404163 | 1.75 * | 0.814958 | 0.384864 | 2.12 ** |

| BTC-SP500 | −0.370483 | 0.365215 | −10.1 | −0.315056 | 0.382983 | −0.82 | −0.405142 | 0.406624 | −1.00 |

| BTC-N225 | −0.136106 | 0.366807 | −0.37 | −0.105618 | 0.402157 | −0.26 | −0.080927 | 0.391535 | −0.21 |

| BTC-GOLD | −0.038485 | 0.365867 | −0.11 | −0.165848 | 0.441296 | −0.38 | −0.084389 | 0.410253 | −0.21 |

| BTC-WTI | 0.298558 | 0.365755 | 0.82 | 0.414276 | 0.434215 | 0.95 | 0.330555 | 0.416259 | 0.79 |

| BTC- USD/EUR | −0.1387 | 0.365587 | −0.38 | −0.17052 | 0.432998 | −0.39 | −0.113251 | 0.399557 | −0.28 |

| GARCH(1,1) | Estimate | Std. Error | t Value | Pr (>|t|) |

|---|---|---|---|---|

| μ | 0.22286 | 0.165905 | 1.3433 | 0.1792 |

| ar1 | −0.91074 | 0.38117 | −23.8934 | 0.000 |

| ma1 | 0.89966 | 0.3891 | 23.1218 | 0.000 |

| ω | 0.82175 | 0.396971 | 20.7 | 0.384 |

| α1 | 0.12374 | 0.36023 | 3.435 | 0.006 |

| β1 | 0.84611 | 0.40622 | 20.8287 | 0.000 |

| Log-Likelihood | −2178.159 | |||

| AIC | 5.7782 | |||

| BIC | 5.7923 | |||

| CCC-MGARCH | DCC-MGARCH | VCC-MGARCH | |||||||

|---|---|---|---|---|---|---|---|---|---|

| Coef. | Std. Error | z | Coef. | Std. Error | z | Coef. | Std. Error | z | |

| BTC | |||||||||

| ARCH L1 | 0.1157219 | 0.242308 | 4.78 ** | 0.1179887 | 0.243649 | 4.84 ** | 0.1154838 | 0.242022 | 4.77 ** |

| GARCH L1 | 0.8579689 | 0.277337 | 30.94 ** | 0.8558714 | 0.276567 | 30.95 ** | 0.8584539 | 0.277092 | 30.98 ** |

| cons | 0.7202004 | 0.2369002 | 30.4 ** | 0.7228328 | 0.2353516 | 30.7 ** | 0.7145526 | 0.2358767 | 30.3 ** |

| RIOT | |||||||||

| ARCH L1 | 0.618105 | 0.138402 | 4.47 ** | 0.615976 | 0.136573 | 4.51 ** | 0.620191 | 0.139318 | 4.45 ** |

| GARCH L1 | 0.9315316 | 0.130029 | 71.64 ** | 0.9323184 | 0.127162 | 73.32 ** | 0.9315534 | 0.130415 | 71.43 ** |

| cons | 0.3609495 | 0.1241317 | 2.91 ** | 0.3533077 | 0.1220651 | 2.89 ** | 0.36499 | 0.1257836 | 2.90 ** |

| VISA | |||||||||

| ARCH L1 | 0.2196341 | 0.455961 | 4.82 ** | 0.2412854 | 0.455877 | 5.29 ** | 0.2123614 | 0.457027 | 4.65 ** |

| GARCH L1 | 0.2783623 | 0.88319 | 3.15 ** | 0.2479007 | 0.738845 | 3.36 ** | 0.3088241 | 0.1003738 | 30.8 ** |

| cons | 0.4284671 | 0.676298 | 6.34 ** | 0.4447715 | 0.600111 | 7.41 ** | 0.4074951 | 0.751599 | 5.42 ** |

| MAST | |||||||||

| ARCH L1 | 0.3144456 | 0.591334 | 5.32 ** | 0.3315486 | 0.602443 | 5.50 ** | 0.3104572 | 0.600185 | 5.17 ** |

| GARCH L1 | 0.1140479 | 0.496595 | 2.30 ** | 0.1119515 | 0.462801 | 2.42 ** | 0.131731 | 0.595819 | 2.21 ** |

| cons | 0.6212404 | 0.59697 | 10.41 ** | 0.6232054 | 0.584486 | 10.66 ** | 0.6099208 | 0.651673 | 9.36 ** |

| NVD | |||||||||

| ARCH L1 | 0.4120287 | 0.1044437 | 3.94 ** | 0.4164346 | 0.1016261 | 4.10 ** | 0.751948 | 0.377091 | 1.99 ** |

| GARCH L1 | −0.304007 | 0.156859 | −1.94* | −0.269155 | 0.172217 | −1.56* | 0.6948316 | 0.13216 | 5.26 ** |

| cons | 3.545683 | 0.270191 | 13.12 ** | 3.4860.43 | 0.2649787 | 13.16 ** | 10.76436 | 0.4879063 | 2.21 ** |

| KBR | |||||||||

| ARCH L1 | 0.084833 | 0.038641 | 2.20 ** | 0.08407 | 0.040724 | 20.6 ** | 0.084996 | 0.038168 | 2.23 ** |

| GARCH L1 | −0.9208836 | 0.456257 | −20.18 ** | −0.9213761 | 0.459383 | −20.6 ** | −0.9220857 | 0.443027 | −20.81 ** |

| cons | 5.710.864 | 0.3275781 | 17.43 ** | 5.743225 | 0.3296634 | 17.42 ** | 5.716813 | 0.3262242 | 17.52 ** |

| Adjustment | λ1 | 0.164511 | 0.063529 | 2.59 ** | 0.055529 | 0.033387 | 1.66 ** | ||

| λ2 | 0.8429994 | 0.538045 | 15.67 ** | 0.9058289 | 0.389035 | 23.28 ** | |||

| AIC | 18015.13 | 18005.96 | 18021.19 | ||||||

| BIC | 18167.86 | 18167.94 | 18183.17 | ||||||

| Model | Test Statistics | Difference | p-Value | |

| CCC vs. DCC | 0.7051 | 0.02441 | 0.4807 | |

| CCC vs. VCC | 1.102 | 0.07035 | 0.2706 | |

| DCC vs. VCC | 0.7097 | 0.04594 | 0.4779 | |

| CCC vs. GARCH | 0.7233 | 0.02033 | 0.9423 | |

| DCC vs. GARCH | 0.157 | 0.04473 | 0.8752 | |

| VCC vs. GARCH | 0.3099 | 0.09067 | 0.7566 | |

| CCC-MGARCH | DCC-MGARCH | VCC-MGARCH | GARCH(1,1) | |

| MAE % | 3.2900344 | 3.2901131 | 3.2899625 | 3.2899992 |

| MAPE % | 0.18185568 | 0.18077208 | 0.18045294 | 0.18531575 |

| RMSE | 4.6804338 | 4.6805512 | 4.680403 | 4.6812991 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Cebrián-Hernández, Á.; Jiménez-Rodríguez, E. Modeling of the Bitcoin Volatility through Key Financial Environment Variables: An Application of Conditional Correlation MGARCH Models. Mathematics 2021, 9, 267. https://doi.org/10.3390/math9030267

Cebrián-Hernández Á, Jiménez-Rodríguez E. Modeling of the Bitcoin Volatility through Key Financial Environment Variables: An Application of Conditional Correlation MGARCH Models. Mathematics. 2021; 9(3):267. https://doi.org/10.3390/math9030267

Chicago/Turabian StyleCebrián-Hernández, Ángeles, and Enrique Jiménez-Rodríguez. 2021. "Modeling of the Bitcoin Volatility through Key Financial Environment Variables: An Application of Conditional Correlation MGARCH Models" Mathematics 9, no. 3: 267. https://doi.org/10.3390/math9030267

APA StyleCebrián-Hernández, Á., & Jiménez-Rodríguez, E. (2021). Modeling of the Bitcoin Volatility through Key Financial Environment Variables: An Application of Conditional Correlation MGARCH Models. Mathematics, 9(3), 267. https://doi.org/10.3390/math9030267