Fuzzy Stochastic Automation Model for Decision Support in the Process Inter-Budgetary Regulation

Abstract

1. Introduction

2. Literature Review

2.1. Research Areas on the Concept of Tight Budget Constraints

2.2. Analysis of Recent Research in the Field of Automatic Simulation of Inter-Budgetary Relations

3. Materials and Methods

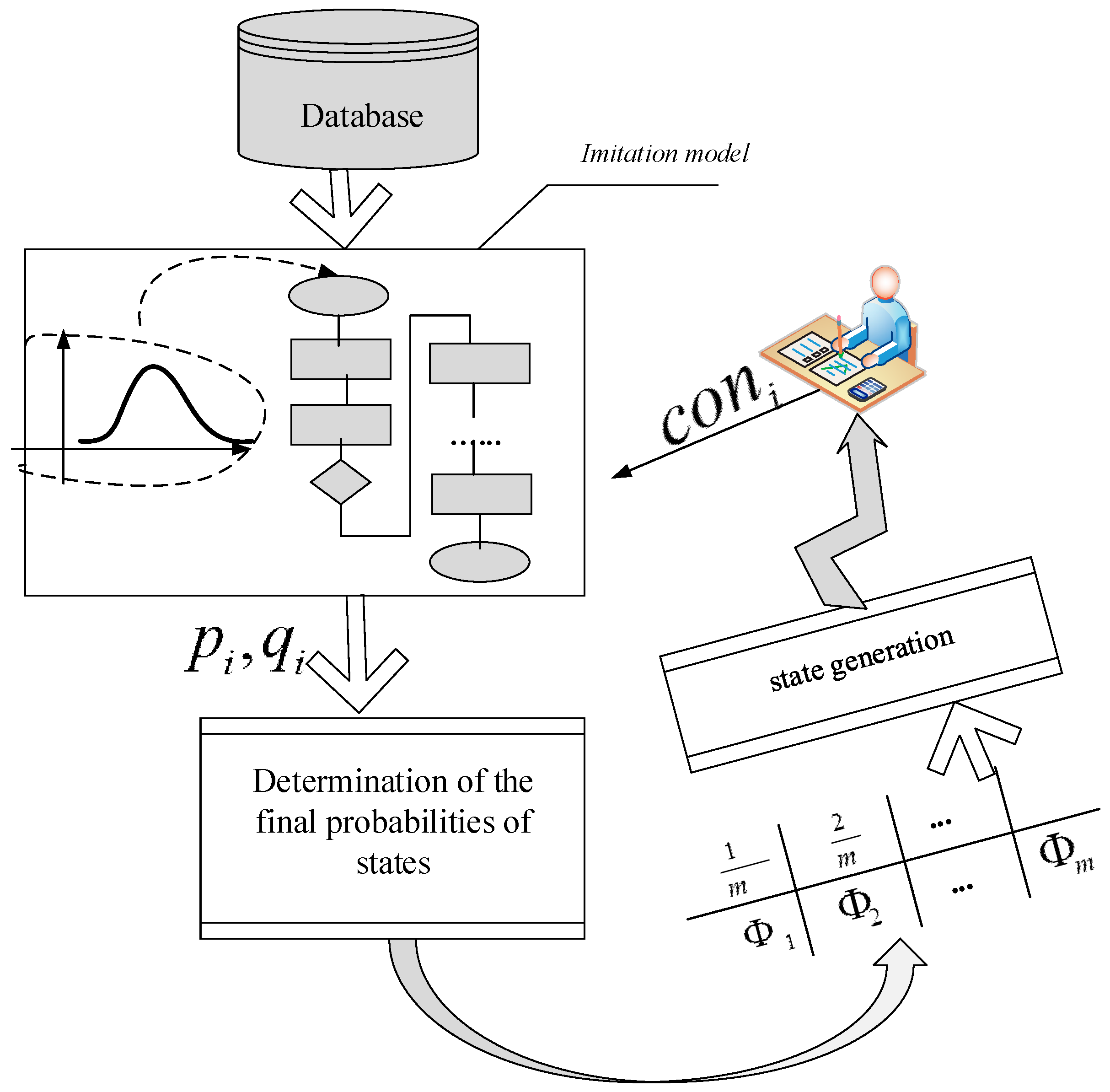

3.1. Concept and Tools

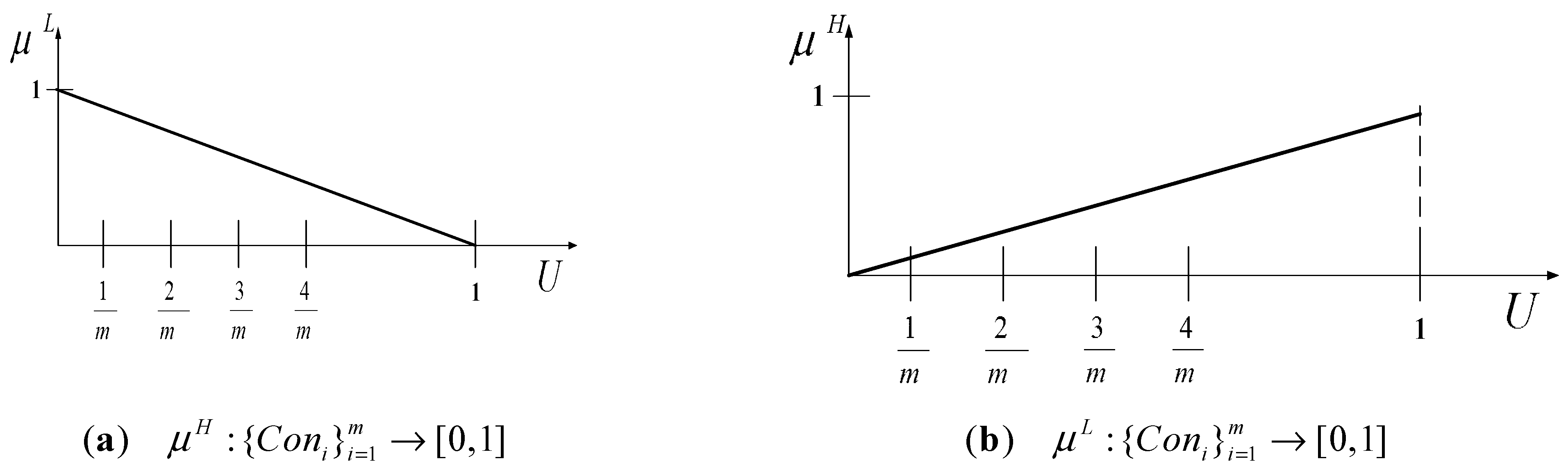

3.2. Synthesis of Automatic and Fuzzy-Multiple Approaches in the Decision Support Model

3.3. Theorems about the Appropriateness of Behavior of Fuzzy Automata

4. Computer Implementation and Experimental Results

4.1. Information Technology to Support Decision-Making in the Shared Distribution of Tax Revenues

4.2. Discussion of Results

5. Conclusions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Luczak, A.; Just, M. A Complex MCDM Procedure for the Assessment of Economic Development of Units at Different Government Levels. Mathematics 2020, 8, 1067. [Google Scholar] [CrossRef]

- Huggins, R.; Morgan, B.; Williams, N. Regions as Enterprising Places: Governance, Policy and Development, Enterprising Places: Leadership and Governance Networks (Contemporary Issues in Entrepreneurship Research; Emerald Group Publishing Limited: Bingley, UK, 2014; Volume 3, pp. 1–28. [Google Scholar] [CrossRef]

- Plešivčák, M.; Buček, J. In the centre, but still on the periphery: Is there any room for development of socio-economically deprived region in Slovakia? Int. J. Soc. Econ. 2017, 44, 1539–1558. [Google Scholar] [CrossRef]

- Popkova, E.G.; Bogoviz, A.V. Modeling Regional Economic Growth in Russia; Sergi, B.S., Ed.; Tech, Smart Cities, and Regional Development in Contemporary Russia; Emerald Publishing Limited: Bingley, UK, 2019; pp. 119–150. [Google Scholar] [CrossRef]

- Brachert, M.; Dettmann, E.; Titze, M. The regional effects of a place-based policy–Causal evidence from Germany. Reg. Sci. Urban Econ. 2019, 79, 103483. [Google Scholar] [CrossRef]

- Achten, S.; Lessmann, C. Spatial inequality, geography and economic activity. World Dev. 2020, 136, 105114. [Google Scholar] [CrossRef]

- Muinelo-Gallo, L.; Roca-Sagalés, O. Joint determinants of fiscal policy, income inequality and economic growth. Econ. Model. 2013, 30, 814–824. [Google Scholar] [CrossRef]

- Foroni, C.; Furlanetto, F.; Lepetit, A. Labor Supply Factors and Economic Fluctuations; International Economic Review; Department of Economics, University of Pennsylvania and Osaka University Institute of Social and Economic Research Association: Philadelphia, PA, USA, 2018; Volume 59, pp. 1491–1510. [Google Scholar]

- Remington, T.F. Why is interregional inequality in Russia and China not falling? Communist Post-Communist Stud. 2015, 48, 1–13. [Google Scholar] [CrossRef]

- Yusupov, K.N.; Toktamysheva, Y.S.; Yangirov, A.V.; Akhunov, R.R. Growth based on the dynamics of gross domestic product. Econ. Reg. 2019, 15, 151–163. [Google Scholar] [CrossRef]

- Yushkov, A. Fiscal decentralization and regional economic growth: Theory, empirics, and the Russian experience. Russ. J. Econ. 2015, 1, 404–418. [Google Scholar] [CrossRef]

- Nayden, S.N.; Belousova, A.V. Methodological tools for assessing well-being population: Interregional comparison. Econ. Reg. 2018, 14, 53–68. [Google Scholar] [CrossRef]

- Kuklin, A.A.; Naydenov, A.S.; Nikulina, N.L.; Tarasyeva, T.V. Transformation of theoretical and methodological approaches and methodological diagnostic tools the state of the individual and the territory of residence. Part 1. From common to alternative approaches to diagnostic. Background. Econ. Reg. 2014, 39, 22–36. [Google Scholar]

- Todes, A.; Turok, I. Spatial inequalities and policies in South Africa: Place-based or people-centred? Prog. Plan. 2018, 123, 1–31. [Google Scholar] [CrossRef]

- Kennedy, T.; Smyth, R.; Valadkhani, A.; Chen, G. Does income inequality hinder economic growth? New evidence using Australian taxation statistics. Econ. Model. 2017, 65, 119–128. [Google Scholar] [CrossRef]

- Venturini, F. The unintended composition effect of the subnational government fiscal rules: The case of Italian municipalities. Eur. J. Political Econ. 2020, 63, 101874. [Google Scholar] [CrossRef]

- Oates, W.E.; Schwab, R.M. Economic Competition among Jurisdictions: Efficiency Enhancing or Distortion Inducing? J. Public Econ. 1988, 35, 333–354. [Google Scholar] [CrossRef]

- Oates, W. An Essay on Fiscal Federalism. J. Econ. Lit. 1999, 37, 1120–1149. [Google Scholar] [CrossRef]

- Gross, T. Dynamic optimal fiscal policy in a transfer union. Rev. Econ. Dyn. 2020. [Google Scholar] [CrossRef]

- Arin, K.P.; Braunfels, E.; Doppelhofer, G. Revisiting the growth effects of fiscal policy: A Bayesian model averaging approach. J. Macroecon. 2019, 62, 103158. [Google Scholar] [CrossRef]

- Dweck, E.; Vianna, M.T.; da Cruz Barbosa, A. Discussing the role of fiscal policy in a demand-led agent-based growth model. Economia 2020, 21, 185–208. [Google Scholar] [CrossRef]

- Woller, G.M.; Phillips, K. Fiscal Decentralization and LDC Ecomomic Growth: An Empirical Investigation. J. Dev. Stud. 1998, 34, 139–148. [Google Scholar] [CrossRef]

- Tsybatov, V.A. Economic growth as the most important factor in reducing the energy intensity of the gross regional product. Econ. Reg. 2020, 16, 739–753. [Google Scholar] [CrossRef]

- Tejado, I.; Pérez, E.; Valério, D. Fractional Derivatives for Economic Growth Modelling of the Group of Twenty: Application to Prediction. Mathematics 2020, 8, 50. [Google Scholar] [CrossRef]

- Jia, J.; Ding, S.; Liu, Y. Decentralization, incentives, and local tax enforcement. J. Urban Econ. 2020, 115, 103225. [Google Scholar] [CrossRef]

- Vom Lehn, C. Understanding the decline in the U.S. labor share: Evidence from occupational tasks. Eur. Econ. Rev. 2018, 108, 191–220. [Google Scholar] [CrossRef]

- Holm-Hadulla, F. Fiscal equalization and the tax structure. Reg. Sci. Urban Econ. 2020, 81, 103519. [Google Scholar] [CrossRef]

- Alexeev, M.; Kurlyandskaya, G. Fiscal federalism and incentives in a Russian region. J. Comp. Econ. 2003, 31, 20–33. [Google Scholar] [CrossRef]

- Rizzo, L. Local government responsiveness to federal transfers: Theory and evidence. Int. Tax Public Financ. 2008, 15, 316–337. [Google Scholar] [CrossRef]

- Baretti, C.; Huber, B.; Lichtblau, K. A tax on tax revenue: The incentive effects of equalizing transfers: Evidence from Germany. Int. Tax Public Financ. 2002, 9, 631–649. [Google Scholar] [CrossRef]

- Buettner, T.; Krause, M. Fiscal equalization as a driver of tax increases: Empirical evidence from Germany. Int. Tax Public Financ. 2020, 1–23. [Google Scholar] [CrossRef]

- Besley, T.J.; Rosen, H.S. Vertical externalities in tax setting: Evidence from gasoline and cigarettes. J. Public Econ. 1998, 70, 383–398. [Google Scholar] [CrossRef]

- Ferraresi, M.; Galmarini, U.; Rizzo, L.; Zanardi, A. Switch toward tax centralization in Italy: A wake-up for the local political budget cycle. Int. Tax Public Financ. 2019, 26, 872–898. [Google Scholar] [CrossRef]

- Bertero, E.; Rondi, L. Financial pressure and the behaviour of public enterprises under soft and hard budget constraints: Evidence from Italian panel data. J. Public Econ. 2000, 75, 73–98. [Google Scholar] [CrossRef]

- Berger, M.; Sommersguter-Reichmann, M.; Czypionka, T. Determinants of soft budget constraints: How public debt affects hospital performance in Austria. Soc. Sci. Med. 2020, 249, 112855. [Google Scholar] [CrossRef] [PubMed]

- Toyofuku, K. Stability or restructuring? Macroeconomic dynamics under soft budget constraints problems. Econ. Syst. 2013, 37, 625–649. [Google Scholar] [CrossRef]

- Miyazaki, T. Intergovernmental fiscal transfers and tax efforts: Regression-discontinuity analysis for Japanese local governments. Reg. Sci. Urban Econ. 2020, 84, 103554. [Google Scholar] [CrossRef]

- Han, L.; Kung, J.K.-S. Fiscal incentives and policy choices of local governments: Evidence from China. J. Dev. Econ. 2015, 116, 89–104. [Google Scholar] [CrossRef]

- Tsetlin, M.L. Research on the Theory of Automata and Modeling of Biological Systems; Nauka, G.L., Ed.; Fiz.—Mat. lit.: Moscow, Russia, 1969; 316p. [Google Scholar]

- Zadeh, L.A. The Concept of a Linguistic Variable and Its Application to Making Approximate Decisions; Mir: Moscow, Russia, 1976; 165p. [Google Scholar]

- Bird, R.M.; Rodriguez, E.R. Decentralization and poverty alleviation. International Experience and the case of the Phillippines. Public Adm. Dev. 1999, 19, 299–319. [Google Scholar] [CrossRef]

- Lindbeck, A. Fiscal Policy as a Tool of Economic Stabilization—Comments on the OECD Report. Kyklos 1970, 23, 7–32. [Google Scholar] [CrossRef]

- Aaron, H.; McGuire, M. Public Goods and Income Distribution. Econometrics. J. Econom. Soc. 1970, 38, 907–920. [Google Scholar] [CrossRef]

- Snyder, V.V. Measurement of Economic Stabilization 1955–65. Am. Econ. Rev. 1970, 60, 924–933. [Google Scholar]

- Green, K.V. Some institutional considerations in federal-state budgetary relations. Public Choice 1970, 9, 1–18. [Google Scholar] [CrossRef]

- Schwallie, D. A Theory of Intergovernmental Grants and their Effect on Aggregate Grantor-Recipient Spending. Public Financ. Q. 1987, 5, 322–338. [Google Scholar] [CrossRef]

- Romer, T.; Rosenthal, H. An Institutional Theory of the Effect of Intergovernmental Grants. Natl. Tax. J. 1980, 33, 451–458. [Google Scholar]

- Qian, Y.; Roland, G. Federalism and the Soft Budget Constraint. Am. Econ. Rev. 1998, 88, 1143–1161. [Google Scholar] [CrossRef]

- Qian, Y.Y.; Xu, C.G. Why China’s Economic Reforms Differ: The M-Form Hierarchy and Entry. Expansion of the Nonstate Sector. Econ. Transit. 1993, 1, 135–170. [Google Scholar] [CrossRef]

- Rodden, J.; Eskeland, G.S.; Litvack, J. Fiscal Decentralization and the Challenge of Hard Budge Constraints; The MIT Press: Cambridge, MA, USA; London, UK, 2003; 476p. [Google Scholar]

- Rodden, J. The Fiscal Federalism Dilemma: Grants and Fiscal Performance Around the World. Am. J. Political Sci. 2002, 46, 670–687. [Google Scholar] [CrossRef]

- Rodden, J. Comparative federalism and decentralization: On meaning and measurement. Comp. Politics 2004, 36, 481–500. [Google Scholar] [CrossRef]

- Rodden, J. Federalism and Bailouts in Brazil Fiscal Decentralization and the Challenge of Hard Budge Constraints; The MIT Press: Cambridge, MA, USA; London, UK, 2003; pp. 213–248. [Google Scholar]

- Rodden, J. The Dilemma of Fiscal Federalism: Grants and Fiscal Performance Around the World. Am. J. Political Sci. 2002, 46, 670–687. [Google Scholar] [CrossRef]

- Eyraud, L.; Lusinyan, L. Vertical fiscal imbalances and fiscal performance in advanced economies. J. Monet. Econ. 2013, 60, 571–587. [Google Scholar] [CrossRef]

- Hindricks, J.; Lockwood, B. Decentralization and Electoral Accountability: Incentives, Separation and Voter Welfare. Eur. J. Political Econ. 2009, 25, 385–397. [Google Scholar] [CrossRef]

- Chulkov, D. Innovation in centralized organizations: Examining evidence from Soviet Russia. J. Econ. Stud. 2014, 41. [Google Scholar] [CrossRef]

- Hopland, A.O. Can game theory explain poor maintenance of regional government facilities? Facilities 2015, 33. [Google Scholar] [CrossRef]

- Bethlendi, A.; Lentner, C.; Nagy, L. The issue of sustainability in a highly centrally regulated fiscal model of local governments: An empirical study. Acc. Res. J. 2020. [Google Scholar] [CrossRef]

- Rattsø, J. Vertical imbalance and fiscal behavior in the welfare state: Norway. In Fiscal Decentralization and the Problem of Hard Budget Constraints; MIT Press: Cambridge, MA, USA, 2003; pp. 133–160. [Google Scholar]

- Yilmaz, S.; Beris, Y.; Serrano-Bertet, R. The relationship between local government discretion and accountability in the decentralization process. Dev. Policy Rev. 2010, 28, 259–293. [Google Scholar] [CrossRef]

- Poterba, J.M. Balanced Budget Rules and Fiscal Policy: Evidence from the States. Natl. Tax J. 1995, 48, 329–336. [Google Scholar]

- Moesen, W.; Cauwenberge, P. The Status of the Budget Constraint, Federalism and the Relative Size of Government: A Bureaucracy Approach. Public Choice 2000, 104, 207–224. [Google Scholar] [CrossRef]

- Maskin, E.S. Recent Theoretical Work on the Soft Budget Constraint. Am. Econ. Rev. Am. Econ. Assoc. 1999, 89, 421–425. [Google Scholar] [CrossRef]

- Tanzi, V. Fiscal Federalism and Decentralization: A Review of Some Effeciency and Macroeconomic Aspects. In Annual World Bank Conference on Development Economics; Bruno, M., Pleskovic, B., Eds.; World Bank: Washington, DC, USA, 1996; pp. 295–316. [Google Scholar]

- Sewell, D. The Dangers of Decentralization According to Prud’homme: Some Further Aspects. World Bank Res. Obs. 1996, 11, 143–150. [Google Scholar] [CrossRef]

- Mc Guire, M. A Method for Estimating the Effect of a Subsidy on the Receiver’s Resource Constraint: With an Application to U.S. Local Governments 1964–1971. J. Public Econ. 1978, 10, 25–44. [Google Scholar] [CrossRef]

- Robinson, C. Occupational Mobility, Occupation Distance, and Specific Human Capital. J. Hum. Resour. 2018, 53, 513–551. [Google Scholar] [CrossRef]

- Pommerehne, W.W. Quantitative Aspects of Federalism: A Study of Six Countries. The Political Economy of Fiscal Federalism. 1.exington, Mass: D.C. Heath. 1976, No 74, pp. 275–355. Available online: https://ideas.repec.org/p/zbw/kondp1/74.html (accessed on 30 December 2020).

- Jin, Y.; Rider, M. Does fiscal decentralization promote economic growth? n empirical approach to the study of China and India. J. Public Budgeting Acc. Financ. Manag. 2020. [Google Scholar] [CrossRef]

- Kornai, J. The Hungarian Reform Process: Visions, Hopes, and Reality. J. Econ. Lit. 1985, 24, 1687–1737. [Google Scholar]

- Kornai, J.; Maskin, E.; Roland, G. Understanding the soft budget constraint. J. Econ. Lit. 2003, 41, 1095–1136. [Google Scholar] [CrossRef]

- Bukhara, V.V.; Lavrov, A.M. Hard Budget Constraints: Theory and Problems of Russian Cities. Public Admin. Issues 2020, 1, 7–40. [Google Scholar]

- Streltsova, E.D. Application of stochastic automata for modeling complex systems with time-varying behavior. Izv. universities. Electromechanics 2002, 3, 76–78. [Google Scholar]

- Streltsova, E.D.; Fedy, V.S. Investigation of the expediency of behavior and asymptotic optimality of stochastic automata in random environments. Izv. universities. Electromechanics 2003, 3, 67–70. [Google Scholar]

- Streltsova, E.D.; Yakovenko, I.V. Support of Dicision-Making in Interbudgetary Regulation on the Basis of Simulation Modeling. In Proceedings of the International Science and Technology Conference “FarEastCon”, Vladivostok, Russia, 2–4 October 2018; pp. 165–172. [Google Scholar]

- Yakovenko, I.V. Model Construction <Simulation Model> ↔ <Stochastic Automaton> in the Decision Support System for Interbudgetary Regulation; Series: Economics and Law; Bulletin of the Udmurt University: Izhevsk, Russia, 2017; No. 3; pp. 73–80. [Google Scholar]

{kind=link}

{kind=link}

| Condition | ||

|---|---|---|

| The Final Probability | The Final Probability | |

| … | … | … |

| Final probabilities | 0.353 | 0.312 | 0.2 | 0.135 |

| Final probabilities | 0.049 | 0.05 | 0.35 | 0.551 |

| Subregion Devel | 0.25 | 0.5 | 0.75 | 1 | |

| 0.21 | 0.51 | 0.851 | 0.917 | ||

| 0.79 | 0.49 | 0.149 | 0.083 | ||

| Subregion Andevel | 0.25 | 0.5 | 0.75 | 1 | |

| 0.11 | 0.11 | 0.12 | 0.15 | ||

| 0.89 | 0.89 | 0.88 | 0.85 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2020 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Yakovenko, I. Fuzzy Stochastic Automation Model for Decision Support in the Process Inter-Budgetary Regulation. Mathematics 2021, 9, 67. https://doi.org/10.3390/math9010067

Yakovenko I. Fuzzy Stochastic Automation Model for Decision Support in the Process Inter-Budgetary Regulation. Mathematics. 2021; 9(1):67. https://doi.org/10.3390/math9010067

Chicago/Turabian StyleYakovenko, Irina. 2021. "Fuzzy Stochastic Automation Model for Decision Support in the Process Inter-Budgetary Regulation" Mathematics 9, no. 1: 67. https://doi.org/10.3390/math9010067

APA StyleYakovenko, I. (2021). Fuzzy Stochastic Automation Model for Decision Support in the Process Inter-Budgetary Regulation. Mathematics, 9(1), 67. https://doi.org/10.3390/math9010067