The Analytical Solution for the Black-Scholes Equation with Two Assets in the Liouville-Caputo Fractional Derivative Sense

, , and

, , and

Abstract

1. Introduction

- C is the call option depending on the underlying stock prices at time ,

- is the dividend yield on the ith underlying stock,

- is the correlation between the ith and jth underlying stock prices,

- T is the expiration date,

- r is the risk-free interest rate to expiration,

- is the volatility of the ith underlying stock,

- is the strike price of the ith underlying stock,

- is a coefficient so that all risky asset prices are at the same level.

2. Mathematical Model

3. Basic Ideas of Time Fractional Black-Scholes Model with LHPM

3.1. A Solution of Time Fractional Black-Scholes Model by LHPM

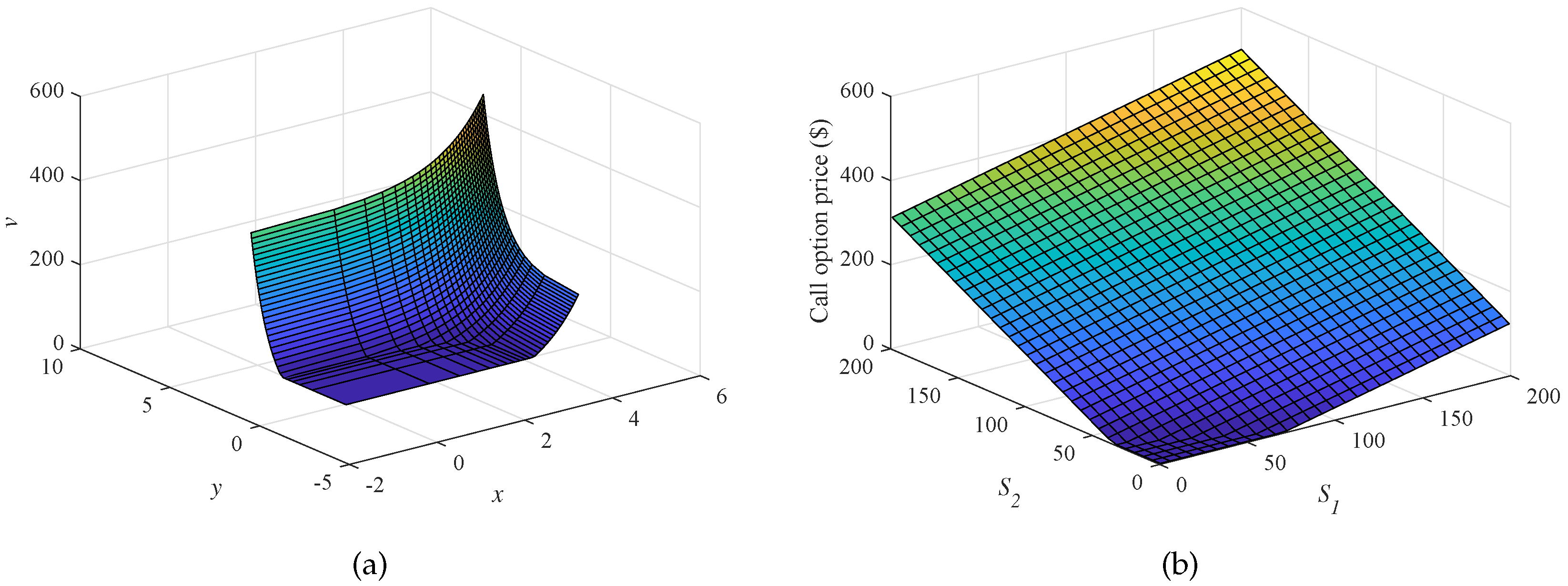

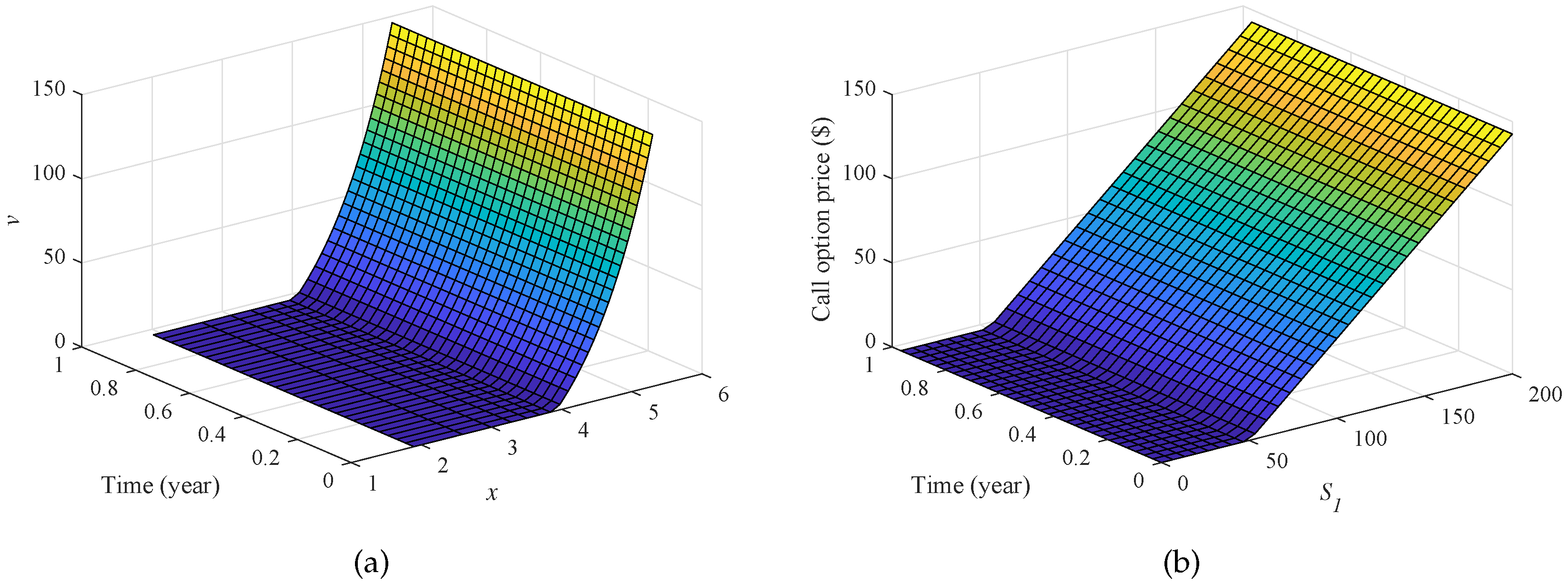

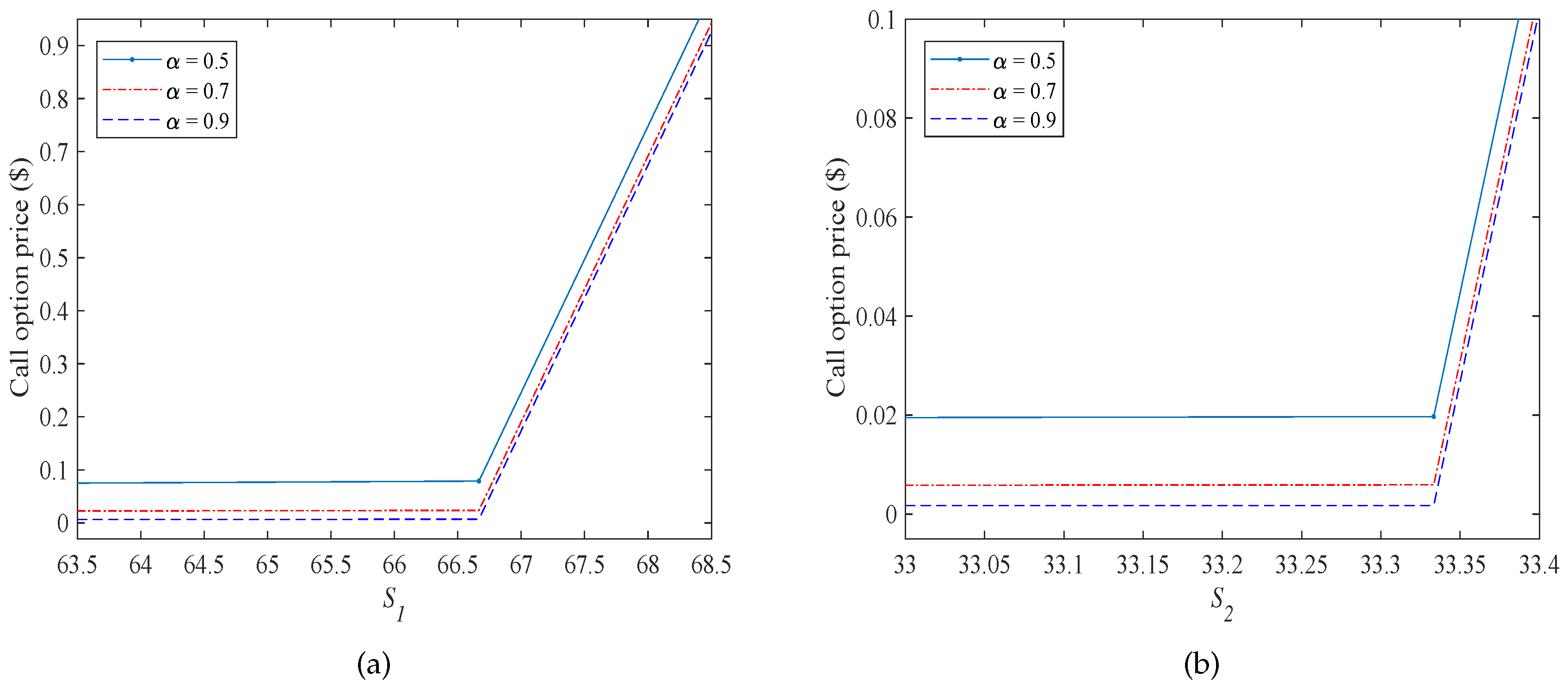

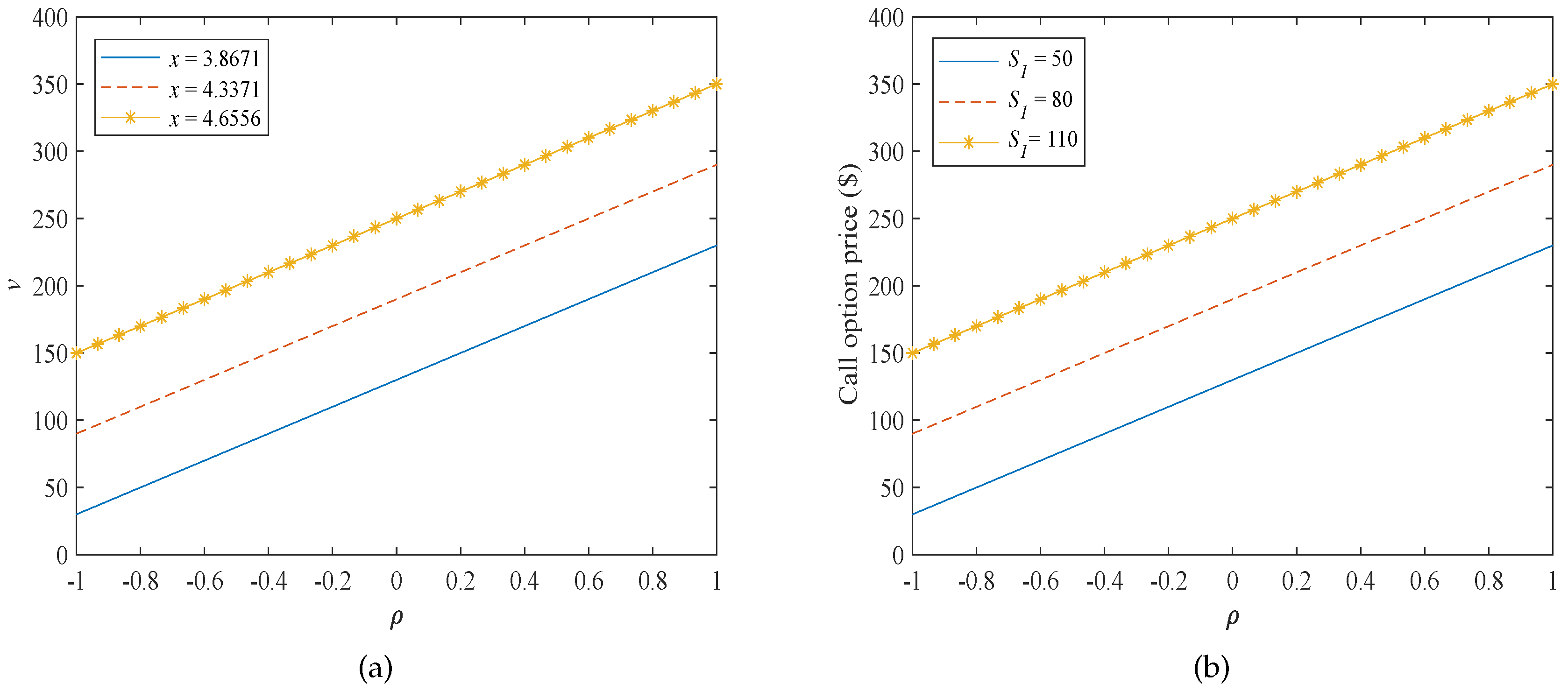

4. Numerical Examples

5. Conclusions

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

References

- Corzo, T.; Prat, M.; Vaquero, E. Behavioral Finance in Joseph de la Vega’s Confusion de Confusiones. J. Behav. Financ. 2014, 15, 341–350. [Google Scholar] [CrossRef]

- Osborne, M.F.M. Brownian motion in the stock market. Oper. Res. 1959, 7, 145–173. [Google Scholar] [CrossRef]

- Black, F.; Scholes, M. The pricing of options and corporate liabilities. J. Political Ecol. 1973, 81, 637–654. [Google Scholar] [CrossRef]

- Cen, Z.; Le, A. A robust finite difference scheme for pricing american put options with singularity-separating method. Numer. Algorithms 2010, 53, 497–510. [Google Scholar] [CrossRef]

- Cen, Z.; Le, A. A robust and accurate finite difference method for a generalized Black—Scholes equation. J. Comput. Appl. Math. 2011, 235, 2728–2733. [Google Scholar] [CrossRef]

- Kleinert, K.; Korbel, J. Option pricing beyond Black–Scholes based on double-fractional diffusion. J. Phys. A 2016, 449, 200–214. [Google Scholar] [CrossRef]

- Vazquez, C. An upwind numerical approach for an American and European option pricing model. Appl. Math. Comput. 1998, 97, 273–286. [Google Scholar] [CrossRef]

- Marcozzi, M.D.; Choi, S.; Chen, C.S. On the use of boundary conditions for variational formulations arising in financial mathematics. Appl. Math. Comput. 2001, 124, 197–214. [Google Scholar] [CrossRef]

- Kim, J.; Kim, T.; Jo, J.; Choi, Y.; Lee, S.; Hwang, H.; Yoo, M.; Jeong, D. A practical finite difference method for the three-dimensional Black–Scholes equation. Eur. J. Oper. Res. 2016, 252, 183–190. [Google Scholar] [CrossRef]

- Lesmana, D.C.; Wang, S. An upwind finite difference method for a nonlinear Black–Scholes equation governing European option valuation under transaction costs. J. Appl. Math. Comput. 2013, 219, 8811–8828. [Google Scholar] [CrossRef]

- Song, L.; Wang, W. Solution of the fractional Black–Scholes option pricing model by finite difference method. Abstr. Appl. Anal. 2013, 1–10. [Google Scholar] [CrossRef]

- Phaochoo, P.; Luadsong, A.; Aschariyaphotha, N. The meshless local Petrov–Galerkin based on moving kriging interpolation for solving fractional Black–Scholes model. J. King Saud Univ.-Sci. 2016, 28, 111–117. [Google Scholar] [CrossRef]

- Yoon, J.H. Mellin Transform Method for European Option Pricing with Hull-White Stochastic Interest Rate. J. Appl. Math. 2014, 2014, 759562. [Google Scholar] [CrossRef]

- He, J.H. Homotopy perturbation method for bifurcation of nonlinear problems. Int. J. Nonlinear Sci. Numer. Simul. 2005, 6, 207–208. [Google Scholar] [CrossRef]

- He, J.H. Homotopy perturbation technique. Comput. Methods Appl. Mech. Eng. 1999, 178, 257–262. [Google Scholar] [CrossRef]

- Trachoo, K.; Sawangtong, W.; Sawangtong, P. Laplace Transform Homotopy Perturbation Method for the Two Dimensional Black Scholes Model with European Call Option. Math. Comput. Appl. 2017, 22, 23. [Google Scholar] [CrossRef]

- Safdari-Vaighani, A.; Heryudono, A.; Larsson, E. A Radial Basis Function Partition of Unity Collocation Method for Convection–Diffusion Equations Arising in Financial Applications. J. Sci. Comput. 2015, 64, 341–367. [Google Scholar] [CrossRef]

- Shcherbakov, V.; Larsson, E. Radial basis function partition of unity methods for pricing vanilla basket options. Comput. Math. Appl. 2016, 71, 185–200. [Google Scholar] [CrossRef]

- Cavoretto, R.; Rossi, A.D.; Perracchione, E. Optimal Selection of Local Approximants in RBF-PU Interpolation. Download PDF J. Sci. Comput. 2018, 74, 1–22. [Google Scholar] [CrossRef]

- Cavoretto, R.; Schneider, T.; Zulian, P. OPENCL Based Parallel Algorithm for RBF-PUM Interpolation. J. Sci. Comput. 2018, 74, 267–289. [Google Scholar] [CrossRef]

- Bastian-Pinto, C.L. Modeling generic mean reversion processes with a symmetrical binomial lattice applications to real options. Procedia Comput. Sci. 2015, 55, 764–773. [Google Scholar] [CrossRef]

- Cox, J.C.; Ross, S. Rubinstein M. Option pricing: A simplified approach. J. Financ. Econ. 1949, 7, 229–263. [Google Scholar] [CrossRef]

- Glazyrina, A.; Melnikov, A. Bernstein’s inequalities and their extensions for getting the Black–Scholes option pricing formula. J. Stat. Probab. Lett. 2016, 111, 86–92. [Google Scholar] [CrossRef]

- Bjork, T.; Hult, H. A note on Wick products and the fractional Black–Scholes model. Financ. Stoch. 2005, 9, 197–209. [Google Scholar] [CrossRef]

- Kumar, S.; Kumar, D.; Singh, J. Numerical computation of fractional Black–Scholes equation arising in financial market. Egypt. J. Basic Appl. Sci. 2014, 1, 177–183. [Google Scholar] [CrossRef]

- Meng, L.; Wang, M. Comparison of Black–Scholes Formula with Fractional Black–Scholes Formula in the Foreign Exchange Option Market with Changing Volatility. Asia-Pac. Financ. Mark. 2010, 17, 99–111. [Google Scholar] [CrossRef]

- Misirana, M.; Lub, Z.; Teo, K.L. Fractional black-scholes models: complete mle with application to fractional option pricing. In Proceedings of the International Conference on Optimization and Control 2010, Guiyang, China, 18–23 July 2010; pp. 573–588. [Google Scholar]

- Mehrdoust, F.; Najafi, A.R. Pricing European Options under Fractional Black–Scholes Model with a Weak Payoff Function. Comput. Econ. 2017. [Google Scholar] [CrossRef]

- Jumarie, G. Derivation and solutions of some fractional Black–Scholes equations in coarse-grained space and time. Application to Merton’s optimal portfolio. Comput. Math. Appl. 2010, 59, 1142–1164. [Google Scholar] [CrossRef]

- Liu, H.K.; Chang, J.J. A closed-form approximation for the fractional Black–Scholes model with transaction costs. Comput. Math. Appl. 2013, 65, 1719–1726. [Google Scholar] [CrossRef]

- Zhang, H.; Liu, F.; Turner, I.; Yang, Q. Numerical solution of the time fractional Black–Scholes model governing European options. Comput. Math. Appl. 2016, 71, 1772–1783. [Google Scholar] [CrossRef]

- Contreras, M.; Llanquihuén, A.; Villena, M. On the Solution of the Multi-Asset Black-Scholes Model: Correlations, Eigenvalues and Geometry. J. Math. Financ. 2016, 6, 562–579. [Google Scholar] [CrossRef]

- Miller, K.S.; Ross, B. An Introduction Fractional Calculus Functional Differential Equations; Johan Willey and Sons Inc.: New York, NY, USA, 2003. [Google Scholar]

- Baholian, E.; Azizi, A.; Saeidian, J. Some notes on using the homotopy perturbation method for solving time-dependent differential equations. Math. Comput. Model. 2009, 50, 213–224. [Google Scholar] [CrossRef]

- Mathai, A.M.; Haubold, H.J. Mathematical Methods in the Applied Sciences; Springer: New York, NY, USA, 2008. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Parameters | Value |

|---|---|

| strike price, K (dollars) | 70 |

| risk-free interest rate (per year), r | |

| maturity time, T (year) | 1 |

| volatility of the underlying first assets (per year), | |

| volatility of the underlying second assets (per year), | |

| correlation, | 0.5 |

| 2 | |

| 1 |

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Sawangtong, P.; Trachoo, K.; Sawangtong, W.; Wiwattanapataphee, B. The Analytical Solution for the Black-Scholes Equation with Two Assets in the Liouville-Caputo Fractional Derivative Sense. Mathematics 2018, 6, 129. https://doi.org/10.3390/math6080129

Sawangtong P, Trachoo K, Sawangtong W, Wiwattanapataphee B. The Analytical Solution for the Black-Scholes Equation with Two Assets in the Liouville-Caputo Fractional Derivative Sense. Mathematics. 2018; 6(8):129. https://doi.org/10.3390/math6080129

Chicago/Turabian StyleSawangtong, Panumart, Kamonchat Trachoo, Wannika Sawangtong, and Benchawan Wiwattanapataphee. 2018. "The Analytical Solution for the Black-Scholes Equation with Two Assets in the Liouville-Caputo Fractional Derivative Sense" Mathematics 6, no. 8: 129. https://doi.org/10.3390/math6080129

APA StyleSawangtong, P., Trachoo, K., Sawangtong, W., & Wiwattanapataphee, B. (2018). The Analytical Solution for the Black-Scholes Equation with Two Assets in the Liouville-Caputo Fractional Derivative Sense. Mathematics, 6(8), 129. https://doi.org/10.3390/math6080129