1. Introduction

The financial derivatives market is very old. Recent data from the Bank for International Settlements show that the total (notional) amount of outstanding contracts in the derivatives market was approximately USD 610 trillion in the first half of 2021. According to Bloomberg, the current global GDP is USD 84.75 trillion. As the value of financial derivatives is dependent on the value of the underlying financial asset, the pricing of these instruments is not immediate. The price of the underlying asset must be modeled using mathematics and statistics, and then the value of the derivative must be determined. The paper focuses on the pricing of call financial options.

According to [

1], mathematical tools for efficient and accurate pricing of financial derivatives are provided by the development and evolution of option pricing models. The study of the theory begins with the Black–Scholes (BS) model [

2].

As Hull [

3] mentions, the Black–Scholes–Merton (BSM) PDE must satisfy the condition that the stock price on which it depends is not paying a dividend. For the model to yield a fair price, there must be no arbitrage opportunities, so the option replication portfolio must earn the risk-free rate.

In Hull [

3], it is assumed that the option price will be determined at any point in time

. If the maturity of the option is denoted as

T, then the option will be priced to maturity, such that

.

In the BS model, the stock price behaves as a geometric Brownian movement, so that the evolution of the value of the asset, denoted by

S, in continuous time is given by

Assuming there are no arbitrage opportunities, the expected return on the stock, , is equal to the risk-free interest rate and the variation of the instrument, , which depends on the stochastic part, dz.

In accordance with Hull [

3], a replication portfolio is assembled consisting of stocks and options. Under the assumption of risk neutrality, the return on the portfolio is the risk-free rate. The BS equation for the option value,

V, is defined as follows and depends on

S and

t:

The significance of the BS model lies not only in the pricing of an option based on certain assumptions, but also in the influence it has had on the history and development of the option pricing model. It is a fundamental approach for future research and a response to the complexity of financial markets.

Corresponding to this, Nthiwa et al. [

4] note that the traditional Black, Scholes, and Merton (BSM) model [

2,

5] assumes that the underlying asset returns are normally distributed. However, empirical studies show that asset returns have higher peaks and broader and more asymmetric tails than normal distributions. This has been shown to be the case in the determination of the market value of the contracts. The result has been inaccurate values that have been the cause of significant losses to financial institutions.

Other research has chosen to improve option pricing by introducing fractional or conformable derivatives into the BS partial differential equation.

As Sawangton et al. [

6] definitively show, fractional calculus can explain complicated incidents in real situations to a greater extent than traditional calculus. To extend the scope of financial theory, the fractional calculus of financial markets has been applied to the BS model. Meng et al. [

7] used this model to price a call option for a foreign exchange bank in China, and their results showed that the fractional BS model is better than the traditional model in explaining the effect of market mechanisms. However, as Zhao and Lou [

8] noted, fractional calculus is a powerful tool for modeling nonlinear systems. Khalil proposed another type of local fractional derivative called a conformable derivative (CFD), which has properties that coincide with Newton’s derivative, making it easier to solve fractional derivatives. They confidently generalized the definition of the CFD by the Linear Extendable General Derivative (LEGD) to the general Conformal Fractional Derivative (GCFD). They clearly show that the Khalil [

9] conformable derivative is a special case of the GCFD. Considering the work of Zhao and Lou, we decided to apply in this research the generalized conformable derivatives since, as proved in the previous study [

10], they show a clear advantage in the valuation of stock options applying Khalil’s conformable derivative, and therefore we expect that by using them we will obtain better approximations and fewer errors.

In the article [

10], we incorporated the Khalil [

9] conformable derivative in the BSM [

2,

5] partial differential equation in the underlying parameter by changing the variable such that

. We obtained the following Black–Scholes (BS)-compliant partial differential equation:

This is different from the work of Wyss [

11] and Zhang et al. [

12], who included the fractional derivatives in the partial differential BS equation with the aim of proposing different ways of numerically solving the time-fractional BS models, and of Yavuz and Ozdemir [

13], who propose using conformable derivatives but over the life of the option contract until it expires. In the same way, they perform numerical solutions seeking convergence to the proposed equations.

In this work, we present a BS equation with generalized conformal derivatives in the variable

S, which extends previous work in [

10]. In this study, the parameters

and

r are constant, which makes implementation straightforward. We present its closed analytical solution in terms of the classical solution of the BS equation by a change of variable. We also show that, for European option pricing, the mean squared error (MSE) is much smaller with the selected conformable functions than the MSE in the results presented in [

10].

It is very important to emphasize that, in both the previous research and the present work, we propose closed analytical solutions of the conformable BS equations, unlike other studies that use fractional derivatives or conformal derivatives. This allows our results to be practically implemented for professional, academic, and research purposes.

In this research, we conduct an empirical comparison of ten models: the traditional BSM model, the Heston model [

14] and the modified BSM model [

10], and the newly proposed general conformable seven-model BSM.

The rest of the paper has the following structure. In

Section 2, we look at previous studies on fractional models for the solution of the partial differential equations associated with Black, Scholes, and Merton (BSM) [

2,

5]. In

Section 3, the paper explains the conformable derivatives, introduces them into the Black and Scholes PDE, and we provide seven generalized conformable solutions. In

Section 4, we solve the BSM equation in a manner similar to the traditional equation, and we also introduce the Heston model. In the empirical analysis, we analyze the accuracy of seven generalized models for pricing European options expiring in November 2023 on the Mexican Derivatives Market (MexDer). We also decided to test the seven conformable models, as well as the traditional Heston model, on six foreign options contracts expiring in 2024; three were contracts on stocks listed on the New York Stock Exchange (NYSE) and three were contracts on shares listed on the London Stock Exchange (LSE). We also decided to compare the seven conformable models to the modified BSM model proposed by Morales et al. [

10]. For this purpose, we use a sample of domestic equity contracts that were listed on the MexDer in 2021. We also decided to test the seven generalized conformable models on 10 out-sampled stock call option contracts to test their effectiveness. These out-samples were arbitrarily selected from a variety of stock exchanges around the world. In all cases, we find that the seven generalized conformable models best approximate the fair price of the option. In addition to the MSE results, we tested the positivity and stability of the results. We did this for a sample of six trading options on the London and New York stock markets. We plotted the values of the option contracts yielded by each of the seven generalized conformable models, the values of the contracts obtained by applying the traditional Heston model; and the market value of the contracts; we only plotted for each maturity the first strike price of each of the six contracts. We present this empirical analysis in

Section 5. Finally, we present our conclusions in

Section 6.

2. Previous Models and Methods

The [

1] BS model is important not just as a method for determining the value of an option based on certain assumptions, but also for the influence it has had on the history and development of option pricing models. A basic approach for future research was established, taking into account the complexity of financial markets.

The true complexity and unpredictability of market volatility is well captured by coarse-grained models of volatility. These models overcome some major limitations of traditional stochastic volatility models. Another notable advance has been the application of machine learning (ML) techniques to option pricing. Techniques such as neural networks and deep learning are now used to navigate the complex dynamics of financial markets. These algorithms have become powerful tools for real-time financial analysis and decision making because of their ability to learn from large numbers of historical market data and to adapt dynamically to new market conditions [

1].

The ability to solve complex option pricing models has been greatly enhanced by the development of sophisticated numerical methods. Innovations in Monte Carlo simulation, finite difference methods, and tree-based approaches have enhanced the tools available to deal with the increasing sophistication of today’s financial models. These advances improve the efficiency and accuracy of option pricing calculations. They also make it easier to deal with more complex models. Taken together, these advances represent a significant evolution in the modeling of financial markets. They provide a deeper understanding of market dynamics and give financial professionals more robust tools for option valuation and risk management. Through the use of these innovative approaches, the financial industry is better equipped to navigate the complexities of today’s markets and make more informed decisions based on sophisticated analysis [

1].

It is important to note that all of these technological advances are not accessible to all companies, including some financial institutions, and even less so to small and medium companies that want to implement hedging instruments, particularly options. As a result, researchers are still in search of alternatives that can be replicated without the high cost of specialized personnel and computer costs. It is for this reason that various modifications of the BSM equation continue to be proposed and studied.

In view of this concern about modification of the BS equation, various researchers have incorporated fractional derivatives into the partial differential equation of BSM, as in the cases of Zhang et al. [

12], Sugandha et al. [

15], and Zhang et al. [

16]. These fractional models are generalizations of the traditional option valuation pricing model.

The fractional BS model has received increased attention due to notable contributions such as those of Wyss [

11] and Cartea et al. [

17]. These authors definitively explain that fractional derivatives, as quasi-differential operators, have non-local properties. As a result, these models serve as a powerful tool for describing non-locality and LTM properties

For its part, Song and Wang [

18] suggest that the option price

is determined by the Black–Scholes time-factor equation, which is expressed as follows:

where

and

.

Using the implicit finite difference technique, Song and Wang [

18] solve the equation numerically.

Zhang et al. [

16] highlight the non-local properties of the fractional derivative, as well as the identification of fractal features in financial markets, which paved the way for the introduction and rapid development of fractional calculus in finance.

They also point out that the fractional Black–Scholes equation, in contrast to the traditional model, provides a better representation of market behavior by incorporating long-run dependence, heavy-tailed and leptokurtic distributions, and multifractality.

Interest in fractional differential equations has increased in recent years, according to Yang and Xu [

19]. Due to the non-locality of fractional derivatives, researchers point out that fractional derivatives are a powerful tool for the description of effects with memory. Tarasov [

20] mentions that fractional integral differential equations have been widely used to describe a variety of classes of economic processes with power-law memory and spatial non-locality. According to Aguilar et al. [

21], there is a strong link between fractional diffusion equations and stochastic processes (fractional Brownian motion, Lévy flight, and so on), making them very promising for modeling various financial applications. In fact, they have already been used in strong financial problems such as the modeling of financial markets [

22,

23,

24,

25].

Based on [

21], one of the first applications of fractional derivatives in finance was through fractional Brownian motion, which allows the incorporation of long-term autocorrelations typically observed in finance, in volatility modeling, and even in option pricing. In accordance [

21,

26,

27], in volatility modeling [

28] and even for the pricing of more complex options, such as American options [

29], double barrier options [

30] as well as currency options [

31]. Most of the analysis for the resolution of the Black–Scholes model was carried out through the application of fractional derivatives.

Now, to help the reader understand why we use generalized conformable derivatives in this study, we will briefly discuss the properties of non-integer derivatives, such as conformable and fractional derivatives.

Fractional derivatives depend on the history of the function. This means that to evaluate the derivative at a given point in time, information about the entire past evolution of the function is required. On the other hand, conformable derivatives are local. This makes them easier to compute and more practical to use for certain types of problems. Fractional derivatives act as non-local operators and have memory; see for example [

32].

Khalil et al. [

9] introduced conformable derivatives in their seminal work. It should also be noted that conformable derivatives have a clear advantage: differential equations expressed in conformable derivatives are often simpler and more easily solved than the same equations expressed in fractional derivatives.

In addition, the conformable derivative does not affect the linearity of the derivative itself or the equations in which it is used, and the conformable derivative facilitates the introduction of more parameters into the equations.

Conformable derivatives satisfy many of the basic properties of ordinary derivatives, such as product, quotient, and chain rules [

9,

32,

33]. This facilitates their use in problems where a direct generalization of differential calculus is the goal. This similarity with classic calculus has made the conformable derivative applicable in physics [

34,

35,

36], engineering [

37,

38], and other sciences.

3. Inclusion of Generalized Conformable Derivatives in the Underlying Asset

After the definition of the conformable derivative given by Khalil [

9], Zhao et al. and Anderson et al. [

8,

36] introduced a generalization based on the Gâteux differential of classical order and its linear extension.

Let us consider two topologically convex vector spaces

X and

Y, respectively. Let

f be a differentiable function on

X, and let

, such that for some set of differentiable functions

:

where

is a parameter.

In particular, the authors gave a geometric and physical interpretation for the extended Gâteux differential as a modification in direction and magnitude of the classical velocity, where the GCD for a function

, for all

and

is defined as:

If

f is differentiable, then we have

where

is a differentiable continuous real function that satisfies the following conditions:

The above holds if , takes the form of the derivative of the first order and is independent of the order of the fraction .

On the other hand, the conformable derivative corresponds to Khalil’s definition: if

[

9].

In this context, the following result is especially important. It is to be found in [

8]. It relates the conformable derivative of the order alpha to the classical derivative.

Additionally, Theorem [2.1] states in [

8] that if a function

has a generalized conformable derivative of order

,

and

f is also differentiable, then

In order to study this equation by means of the conformable derivative, we will assume that the derivatives are taken in the variable

S. We replace the operator

by

in BS Equation (

2). As in [

36], we will now show that the generalized conformal derivative (8) can be expressed as an integer derivative by changing the variable. In this section of the paper, we use

u to denote the variable change determined by the function

for convenience. In the rest of this paper we will use

to denote the above variable change

After the determination of the first derivative, the second derivative of

, including the partial differential equation of BS, is as follows.

This is the proof that the second generalized conformable derivative is transformed into a second-order integral derivative with the same variable changed.

The first and second generalized conformal derivatives corresponding to Equations (8) and (10) are substituted into BS Equation (

2) to replace the first- and second-order integer derivatives, respectively, to obtain the expression shown below:

Explicitly, in the form of generalized conformable derivatives, we obtain

This is the Generalized Conformable Black–Scholes (GCBS) equation. To our knowledge, this is the first time that the BS equation has been obtained using the GCBS derivatives. It is clear that the transformation only affects the variable S.

Notice that this last GCBS equation with a change of variable is transformed into a BS equation of integer order in the variable .

To find the solution of this GCBS equation, we observe that, by changing the variable

, the same solution of the equation of BS (2) is the solution of Equation (

18), but replacing the variable

S with the new variable

, in a way analogous to what was done in [

36]. To obtain this solution, we first use the Cauchy–Euler method and the variable separation method. Consider a solution of the form

.

If we substitute this solution

into the GCBS equation and divide by

, we obtain:

Now that we have applied the change of variable, we obtain the following ordinary differential equation of integer order in the new variable

In the general case, as has already been shown, we can assert that the generalized conformable derivative, when applied to differentiable functions, is in fact equivalent to a change of the variable, namely

, where

is a sufficiently smooth function with

, and is also an injective function in the variable

. Equation (

20) is an ordinary differential equation with variable coefficients. Its solutions are new ways of working with the BS equation. They are modified by generalized conformable derivatives. They will be the subject of study in later sections.

In the following, we present seven generalized fitting functions that were obtained by the test-and-error method from a set of fitting functions in order to obtain the best results in the empirical analysis of the values of corporate stock options. Based on the examples of Zhao et al. [

35], this set of fitting functions was constructed. Seven of the fitting functions and the corresponding changes of the variables

for the generalized conformable derivative are presented in the following equations:

The parameters , a, and b in the presented conformable functions are free to adjust and have no specific interpretation. Conformable functions are free to adapt and do not need to be interpreted in a specific way. Note that most properties of the GCFD are consistent with classical derivation. For example, the chain rule is verified:

It is known that the classical integer order derivative and Khalil’s conformable derivative are special cases. For solving conformable differential equations of fractional order, conformable derivatives can be used. These derivatives are local operators because they do not store memory. This approach provides a solid foundation for differential equations and an alternative for modeling and improving approximations [

35,

36,

39,

40,

41,

42,

43,

44]

5. Empirical Analysis

In this research, we performed a broader empirical analysis with the aim of testing the effectiveness of solving the Black, Scholes, and Merton partial differential equation by applying generalized conformable derivatives in the value of the underlying asset, and we proposed seven functions. Moreover, we compared the results of the seven generalized conformable models with the Heston model, the traditional BSM model, and the model from recent research called the modified BSM model [

10]. For three different data samples, there was a comparison of the results of the evaluation of 10 models.

Specifically, 16 European financial call option contracts on Mexican non-financial companies listed on the Mexican Stock Exchange were included in our sample. We also analyzed six European financial call option contracts on three English stocks listed on the London Stock Exchange (LSE) and three US stocks listed on the New York Stock Exchange (NYSE). We also tested this new proposal for the 16 financial option contracts that were analyzed in the previous study: contracts on Mexican non-financial stocks that were listed on 30 November 2021 [

10].

For each of the options, both domestic and international, we considered five strike prices and four expiration dates. We collected share price data for each company and used the 28-day Treasury bill yield as our domestic risk-free rate. We used London Interbank Offered Rates for international option contracts. For these calculations, we used the daily implied volatility of the financial option contracts, the risk-free interest rate, the price at which each company’s stock was trading at the time the option contract was issued, and the respective strike prices.

To have more power to test the effectiveness of the seven generalized conformable models, we decided to apply them to companies out-sample the base sample; for this, we searched on the web for the stocks with the highest marketability, and then in the Bloomberg Anywhere database we searched for which companies had issued call options on their stocks. We took 10 call contracts issued in April 2025 on the out-sample stocks; this amount was slightly more than 20% of the contracts in the base sample, considering that we analyzed 38 contracts in the base sample.

After searching the Bloomberg Anywhere database, our out-sample consisted of options on the following stocks: Iberdrola (Spain), Inditex (Spain), BMW (Germany), Volkswagen (Germany), Johnson and Johnson (U.S.A.), Procter and Gamble (U.S.A.), Eli Lilly (Global Markets), Tesla (Global Markets), Novo Nordisk (Global Markets), and United Health (Global Markets).

We took for each contract four maturities, five or six strike prices, the implied volatility of every maturity and strike price of each and every contract, the risk-free interest rates, the value of the underlying asset at the time of each expiration, and the market value of each contract.

In contrast to the base sample, the maturities of each contract were different: we took maturities of 3 days, 9 days, 17 days, and 24 days, and, for the Global Corporate Stocks contracts, the maturities ranged from 3 days to 486 days.

However, for each contract, we only evaluated four maturities at a time. In some cases, the maturities were very short. In particular, for the contracts of the Spanish and German companies, the maturities ranged from 3 days to only 17 days, while, for the Global Market companies, the maturities ranged from 3 days to 486 days.

In addition to the results of the MSE, we tested the positivity and stability of the results for the sample of the six options whose shares were traded in the London and New York stock markets. We plotted the values of the option contracts yielded by each of the seven generalized conformable models, the values of the contracts obtained by applying the traditional Heston model, and the market value of the contracts. As mentioned above, we considered the European call options on the shares of Associated British London Foods, Burberry London, Pearson London, Ford, NVIDIA and Pfizer. For each one, we applied the aforementioned models for their five strike prices and their maturities at 37, 128, 191, and 247 days. However, to analyze positivity and stability, we only plotted for each maturity one of the strike prices of each of the six contracts. This approach preserves the parsimoniousness of the empirical analysis.

It is very important to note that all models in this study were applied only to European equity call options. We did not use any other type of underlying asset.

All of the above information was obtained from the Bloomberg Anywhere data base. Only the names of the Mexican companies that issued call option contracts in 2021 and 2023 were provided by the Mexican Derivatives Market (MexDer) website.

Table 1 lists the names of the 16 companies whose shares were listed on the Mexican Stock Exchange on 30 November 2023.

Table 2 lists the six companies whose shares were listed in the options markets on 2 February 2024. Finally,

Table 3 lists the names of the companies analyzed in the previous study.

Table 4 provides basic information on the selected companies, including their GICS classification (using only industry and sector), share price, strike price range, and implied market volatility.

We computed the prices of the contracts with the seven generalized conformable models. In all cases, we obtained a mean square error in the order of twentieths of a decimal point of the market price. These seven generalized fitting models are even better than the one proposed in the previous study [

10]. They are therefore better than the traditional Black, Scholes, and Merton model.

We estimated the general conformable parameters

and the

parameter by optimizing the price adjustment, i.e., by solving the problem.

where

is the price of the call predicted by the general BSM conformable parameters

, and

, and

is the market price.

The MSE (mean square error) was calculated by taking the difference between the value of the financial options obtained with the seven conforming models and the market value of each contract, using the five prices in the entire sample, including, of course, the contracts of the 10 out-sampled options.

In the case of the domestic options contracts listed in 2023, it was observed that the models that provided the best possible adjustments were (21d), (21f), and (21b) for the 17-day contracts. In general, the model (21h) performed a good approximation, except for the company Fomento Económico Mexicano, whose MSE was 2.14 × , while for the company Grupo Aeroportuario del Sureste the MSE of the model (21d) was 7.03 × , both of which were the largest errors. The results of the analysis for contracts with a maturity of 122 days showed that the models with the best fit were again (21b), (21d), and (21f), preceded by model (21n) with an MSE of 6.81 × for Grupo Aeroportuario del Sureste. In the case of the contract with a maturity of 213 days, the models with the best fit were (21b), (21d), and (21f). The other models showed oscillations that were not consistent with the volatility of the companies. However, we highlight that the MSE did not exceed the value of 8.33 × . Finally, for the contract with a maturity of 304 days, we can highlight that again the models that offered the best possible fit were (21b), (21d), and (21f). We also highlight the case of Fomento Económico Mexicano with an MSE of 2.10 × with model (21h).

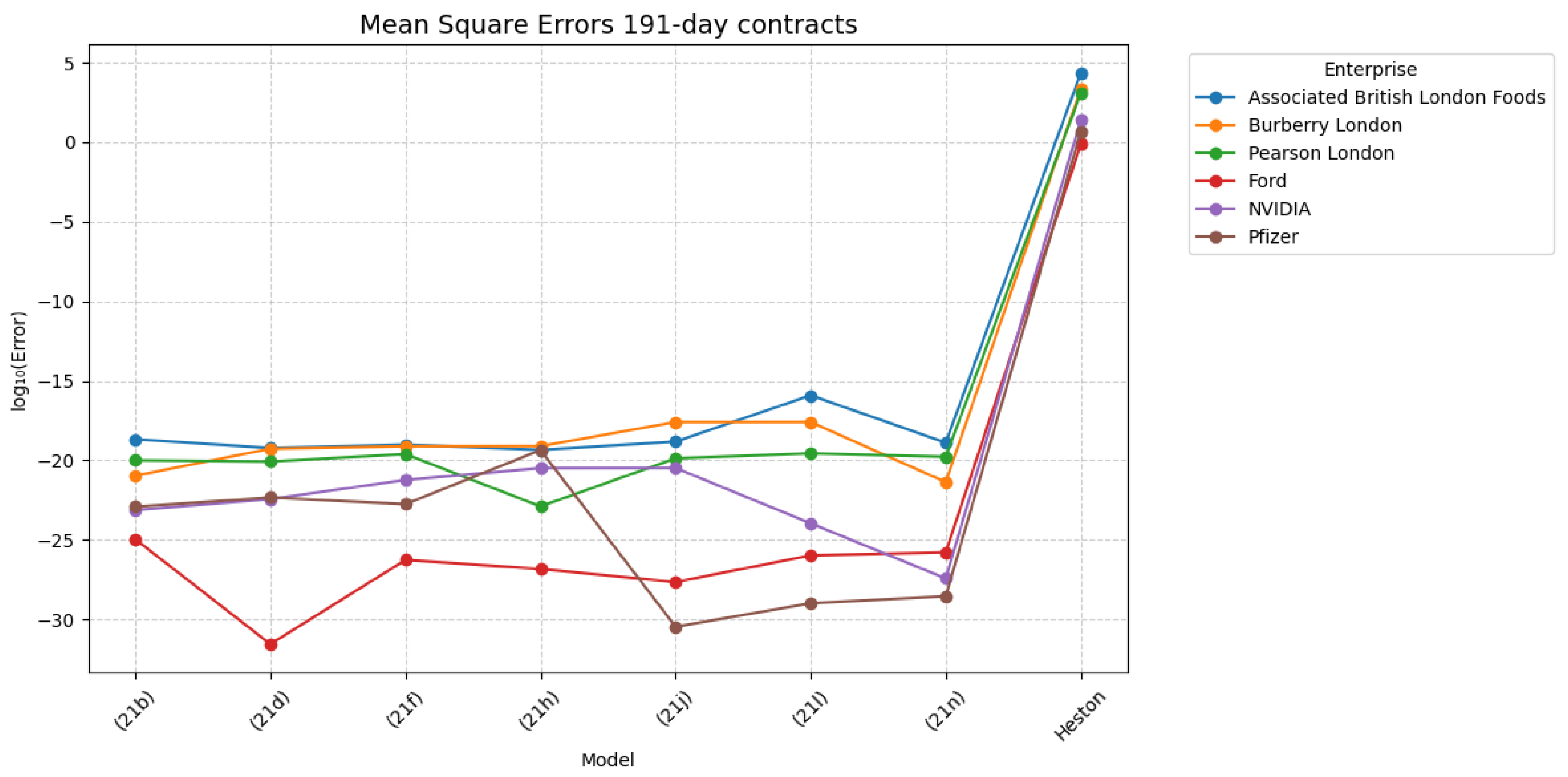

The analysis we have carried out on European call option contracts based on the shares of three UK and three US companies listed in 2024 highlights the following points. For contracts with a maturity of 37 days, the approximation provided by the seven models is very good for options on US stocks. For the 128-day contracts, we observe that the approximation provided by all the models is remarkably good, except for Burberry London with model (21j), which has an MSE of 2.51 × . For the 191-day contracts, the best models for the six companies are (21h) and (21n). The MSE of model (21l) stands out for Ford with a value of 3.19 × . In the case of the contracts with a maturity of 247 days, the seven models in their generality perform a very good approximation with MSEs below 4 × , except again for Burberry London, in which case the MSE of the model (21j) is 2.59 × .

We applied the models proposed in this study to the research option contracts of Morales et al. [

10], published in 2021, in order to test their effectiveness and superiority. In order to do this, we made use of the information provided by this paper. The results we have obtained are as follows. The best approximation models for 17-day European call contracts are (21j) and (21n), followed by (21d) with an MSE of 2.39 ×

. Note that the average MSE is 3.0 ×

for the seven generalized fitting models. These results exceed those obtained with the modified BSM model [

10]. All generalized conformable models come close to the market value of the option in the case of 45-day contracts. The models (21f) and (21h) for the Fomento Económico Mexicano have the largest errors, 9.75 ×

and 1.77 ×

, respectively. For 136-day contracts, all of the seven general models have an MSE of less than 3.5 ×

. Models (21j), (21n), and (21l) are the best approximating models. Grupo Bimbo has the highest MSE with the model (21b). It is equal to 3.27 ×

. Furthermore, contracts with a maturity of 227 days behave very similarly to those with a maturity of 136 days, with an MSE lower than 6.1 ×

. However, (21j), (21f), and (21n) are the most appropriate. Note that Grupo Aeroportuario del Centro Norte with model (21h) is the only outlier. It has an MSE of 6.04 ×

.

Table 5 shows the average of the value obtained by the errors in the seven general conforming MSEs. All four maturities are summarized in this table. As can be seen, the errors obtained using the conformable BSM are much smaller for all the companies studied. This is certainly a consequence of the flexibility provided by the conformable parameters

and the resulting non-linear local approximation to the option value that is implicit in the CBSM model.

In general, the MSEs of the seven generalized conformable models provide a good approximation according to the results presented in

Table 5. However, as can be seen, (21b), (21d), and (21f) give the lowest MSEs.

Analyzing the alphas of the Mexican 2023 options, we can see that they behave very similarly for the four maturities. Contrary to Morales et al. [

10], the alphas of the general conformable model (21b) are lower. This is because this study does not present time-varying parameters. The highest alphas are obtained by the general conformable models (21f), (21n), and (21l), with a value of 0.99. On the other hand, the general conformable model (21h) shows strong oscillations. Grupo Aeroportuario Centro del Norte, Grupo México, and Grupo Aeroportuario del Sureste have the lowest values. For the four maturities, the US and London options have very similar values. For the general conformable model (21b), the London firms have alphas of 0.61. Those of the US firms are 0.01. The exception is NVIDIA, which reaches a value of 0.4. It is noteworthy that, for the other models, the alphas of the London companies are 0.99, while for the US companies there is a sharp decrease, especially for the general conformable model (21h) with an average value of 0.001 and for the general conformable model (21j), with a value of 0.2.

The following figures (

Figure 1,

Figure 2 and

Figure 3) show plots of base sample alphas only. On the abscissa axis are the names of the general conformable models. On the ordinate axis are the values of the alphas. The names of the individual companies are in the box within the graph.

On the other hand, the parameters of the Heston diffusion process were obtained in the Excel program with the log maximum likelihood model using stock price series of each of the six companies for the period 2 February 2014–5 February 2025. The results are presented below (

Table 6 and

Table 7).

The p-value for the logarithmic maximum likelihood distribution function was less than 0.05 for all companies. This is considered a chi square with 6 parameters of freedom.

Heston [

14] confirms that the correlation parameter

positively affects the skewness of spot returns. As the spot price rises, a positive correlation spreads out the right tail of the probability density, resulting in higher variance. On the other hand, the left tail has a lower variance and does not have a spread. We can confirm this by looking at the cases of NVIDIA and Ford in particular. They have higher variance in the long run.

The degree of volatility is controlled by the parameter. If is zero, the volatility is deterministic and the continuously compounded returns of the spot price will have a normal distribution. On the other hand, will increase the kurtosis of the returns of the stock price.

The models for the pricing of call options on the above stocks were programmed in Python with the characteristic functions after the calculation of the volatility parameters [

48]. We use the Heston model for the pricing of call option contracts, and for each contract we use five strike prices and five expiration dates for 37 days, 128 days, 191 days, and 247 days. The results obtained using the Heston model for the 37-day contracts show the highest mean square errors for options on the shares of Associated British London Foods, Burberry London, and Pearson London, whose values are 6.20 ×

, 2.00 ×

, and 1.71 ×

, respectively. For the MSE of options contracts on US firms, the approximation is better, with an average value of 2.15 ×

.

For the 128-day, 191-day, and 247-day contracts, the results are quite similar. The average value of Heston’s MSE for the London firms is 8.57 × . For the three US firms, the average error is 1.02 × . These results are not comparable with the results for the firms with the seven generalized conformable models. The average MSE for these is 3.04 × .

To facilitate the reader’s comparison of the MSEs, it is important to note that these calculations are presented in

Figure 4,

Figure 5,

Figure 6 and

Figure 7, as the base 10 logarithm was applied to the MSEs because it was difficult to show the performance of each model for each company due to the very small amount.

The plots show that the generalized conformable BSM model is much more accurate than the classical alternatives.

In addition to the graphs, we present a table showing the differences between the MSE results obtained by subtracting the stock option values obtained by applying the seven generalized conformable models and the Heston model from the market value of these contracts.

From the results shown in

Table 8, the significant difference between the fits of the seven generalized conformable models and the Heston model can be deduced. As can be seen, the errors of the generalized conformable models reach 8.73 ×

. The Heston model does not perform badly. However, the magnitude of its average MSE reaches 2.74 ×

.

Notably, the generalized conformable models have a tendency to slightly underestimate the market value. The Heston model, on the other hand, tends to overestimate the market value. For all six sample firms, this is true.

The results of the seven generalized conformable models for the sample companies are not uniformly consistent on average, as shown in

Table 8. However, it is agreed that, according to the seven generalized conformable models, including the Heston model, the contract on the shares of Associated British London Foods shows that this is the firm with the highest average MSE. For the contract on the shares of Burberry London, the (21f) model is the best fit. For the contract on the shares of Pearson, the (21h) model is the best fit. For the contract on the shares of Ford, the (21j) model is the best fit; and, for the contract on the shares of NVIDIA, the (21l) model is the best fit. In addition, in the case of Pfizer, the seven generalized conformable models and the Heston model agree that it has the lowest average MSE among the six companies in the sample.

For the out-sample contracts, we calculated the MSEs for each parameter as for the base sample contracts. We chose to present only the cumulative average of MSEs.

The performance of the MSEs of the seven generalized fitting models is excellent. The average values are in the range 7.22 × to 3.7813 × . For the two Spanish companies, the best-fitting model is (21f) with an MSE of the order of × , while the worst-fitting model is (21h) with an MSE of 7.9907 × for Iberdrola. In the case of Inditex, the model with the highest MSE is (21b) with a value of 2.20265 × . For German companies, the best approximating model is (21l) with an average MSE of 2.26 × . The least efficient model with an average MSE of 5.79 × is (21h) for these contracts. For U.S. firm contracts, the results are mixed: for Johnson and Johnson, the best approximation is provided by model (21l), while, for Procter and Gamble, the lowest MSE is provided by model (21f), and the highest MSE is 2.1254 × for model (21h). In the case of the Global Market Stock contracts, the model that happens to provide the lowest MSE is model (21d) with an average error of 5.84 × , and the highest MSE for the four contracts is model (21h).

As can be seen, there is consistency in the model that performs slightly less efficiently (21h) compared with the seven generalized conformable models, but all the generalized fitting models show excellent fits. The fair value of the options on the 10 stocks is very near to the values generated by the seven models. It is worth noting, however, that the traditional BSM, the Heston model, and the modified BSM are again far outperformed by the MSE of the seven conformable models. The results of these tests can be seen in

Table 9 and

Figure 8.

Figure 9 shows the average cumulative alphas of the 10 out-of-sample contracts, and it can be seen that the alphas with values close to 0.99 for the 10 contracts are homogeneous for model (21f), which has no direct relationship with the MSE. The second model that also gives alphas in the range of 0.7 to 0.97 is model (21d), which is not one of the best approximations of the market value. The third model is model (21l), which gives alphas in the range of 0.3 to 0.97 for the 10 contracts. The lowest alphas are found in model (21h). In this case, it is the model that offers the best approximations to the market values of the options. There is no single contract that has the highest or lowest alphas for all models and all contracts.

The figures below clearly show the option values derived from the seven generalized conformable models, the Heston model, and the market value of the six contracts of the three London firms and the three US firms. The abscissa axis shows the names of the firms, and the ordinate axis shows the values of the models and the market value of the firms. The model name is shown in a box within the figure in different colors to indicate the line to which each model belongs. It is important to note again that we decided to plot one of the strike prices for each expiry date for the six option contracts on Associated British London Foods, Burberry London, Pearson London, Ford, NVIDIA, and Pfizer to verify the positivity and stability of the results.

As can be seen in

Figure 10,

Figure 11,

Figure 12 and

Figure 13, it is confirmed that all the values of the seven generalized conformable models, as well as the result of the traditional Heston model, are in the first quadrant of the Cartesian plane. This confirms that they are positive and stable.

Figure 10,

Figure 11,

Figure 12 and

Figure 13 confirm the positivity and stability of the results of the seven generalized conformable models. Once again, they confirm that the seven conformable models better fit the market value of option contracts compared with the traditional Heston model.

6. Conclusions

We derive a BS equation in terms of generalized conformable derivatives and show that this equation is transformable into a BS equation of integer order, with a change of the variable determined by the conformable function used in the generalized conformable derivatives. In addition, using the new variable determined by the seven conformable functions presented, we give their closed BS analytical solution.

We can conclude that the seven conformable models generally provided an excellent fit from the empirical analysis performed. For the 2023 contracts, the generalized conformable models with the best fit for each maturity were (21d) and (21f).

In performing the analysis for international firms, we decided to compare the results of the seven general conformable models with Heston’s model. Surprisingly, the conformable models generally provided extremely good fits for MSEs below 4.00 × .

As mentioned above, we chose to run the analysis on options contracts that were traded in 2021 in order to evaluate the fit of the seven fit models proposed in this study. It is not surprising to see that all of the seven conformable models also provided a higher level of fit than the modified BSM conformable model.

According to our analysis, it can be concluded that the seven general conformable models perform an excellent approximation to the market value of the options, with very small MSEs and, as we observe, surpassing the results of the Heston’s model, the BSM modified model [

10], and the traditional BS model.

We decided to apply the seven generalized conformable models to out-of-sample contracts to provide further evidence of their excellent approximation. For this purpose, we performed an Internet search for the companies that currently have the highest stock market bursatility. From the results obtained, we selected 20 companies, and then we searched in the Bloomberg Anywhere database for those companies that had issued European call options on their shares, and we were left with 10 companies: Iberdrola (Spain), Inditex (Spain), BMW (Germany), Volkswagen (Germany), Johnson and Johnson (USA), Procter and Gamble (USA.), Eli Lilly (Global Markets), Tesla (Global Markets), Novo Nordisk (Global Markets) and United Health (Global Markets).

Due to the heterogeneity of the listed companies, we found that some had contracts with maturities ranging from 3 days to 17 days. Each contract had five strike prices, as well as the share value, implied volatility, and risk-free rate at the time each contract was issued. Particularly in the case of equity contracts traded on global markets, they had maturities ranging from 3 days to 486 days, each with five strike prices, as well as the share value, implied volatility, and risk-free rate at the time of issuing each contract. From our sample, we selected only four maturities, and for those with few periods we took almost all the contracts; however, for the contracts with many maturities we arbitrarily selected, depending on the issues, the maturities at 3 days, 9 days, 38 days, 73 days, 168 days, 192 days, and 465 days, but emphasizing again that from these contracts we selected only four maturities. We applied the seven generalized conformable models to each out-sample contract and calculated the MSE for each parameter and maturity. The results obtained in the base sample were confirmed: all seven models provided excellent fits, with MSEs ranging from 3.76 × to 7.22 × . As in the base sample, there was no single model that consistently provided the best fit for all ten companies, but those that offered the best approximation were (21l), (21n), and (21f). Model (21h) had the “relatively lower” average cumulative errors. Despite this, the models offered better approximations of market value than the traditional BS, Heston, and modified BS models.

We also decided to verify the positivity and stability of the results of the seven generalized conforming models, as well as the traditional Heston model. To do this, we took a sample of European call contracts from six international companies: Associated British London Foods, Burberry London, Pearson London, Ford, NVIDIA, and Pfizer, taking into account that for the analysis we used their five strike prices and their expiration dates of 7, 128, 191, and 247 days. We plotted the option values obtained from the eight models. We also plotted the market value of the contract price. In order to maintain the parsimony of the empirical analysis, we plotted only one of the strike prices for each of the maturities. With all values in the first quadrant of the Cartesian plane, the results of the graphs confirmed positivity and stability. The excellent fit of the seven generalized conformal models was also verified.

We believe that our general conformable models represent a significant evolution in financial modeling, offering a deeper understanding of market dynamics and providing financial professionals with more robust tools for option pricing and risk management.

It is important to emphasize that the seven generalized conformable models always achieve the best possible fit. However, across all firms in the four samples, there is no consensus on a single model that stands out above the others. This result is to be expected. It is necessary to take into account the macroeconomic and microeconomic situation of the country, and the industry and sector of the companies, as well as the internal situation of each company. This is a very important issue for future research. The goal should be to find the model that is optimal in all cases.

Finally, it is really very important to emphasize that in the seven generalized conformable models we obtained closed analytical solutions of the Black–Scholes–Merton equation, as opposed to other investigations that use fractional or conformable derivatives to search for complex iterative numerical solutions that provide imprecise solutions.

,

,

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}