1. Introduction

Technology and globalization have interconnected market forces across various industries and geographical borders. This implies that the occurrences within a particular economic system can potentially impact other economic activities that are not directly related, sometimes referred to as spillover effects. Over the course of recent decades, the regions of the Middle East and Asia have experienced a series of significant occurrences that have had far-reaching implications for global energy production as well as distribution. The primary objective of this study is to examine the presence, direction, and attributes of spillover effects on oil stock returns in Asian OPEC+ nations. The intention is to offer significant information to investors, resource managers, regulators, and market participants.

Against the backdrop of an intensifying worldwide economic downturn, there was a notable upswing in investment within the energy industry, with a growth rate of 8% observed in 2022, culminating in a cumulative sum of USD 2.4 trillion. According to the 2023 report published by the International Energy Agency [

1], it is anticipated that this particular investment will experience a further increase of 17%, reaching a total of USD 2.8 trillion in 2023. This development would establish it as the most substantial recorded capital investment thus far. The energy sector has not experienced a significant decrease in investor confidence despite the presence of several factors such as high prices, increasing expenses, economic uncertainty, concerns over energy security, and imperatives related to climate policy [

2]. The integrated oil and gas business is a sector that has garnered significant international interest. The market under consideration has a notable degree of volatility, rendering it one of the most unpredictable and unstable markets on a global scale. It possesses a substantial market capitalization and offers considerable anticipated returns for shareholders and investors. However, the rapid expansion of both external and internal shocks to the industry in recent times has generated considerable conjecture. There is a growing public concern regarding potential disruptions to the oil supply, as shareholders express concerns regarding the potential consequences of such disruptions on their financial returns in both the short and long term.

The phenomenon of spillover effects in energy markets, specifically with regard to the returns of oil, has received considerable scholarly interest. Spillover effects manifest when disturbances originating in a specific segment of the global economy disseminate and exert an influence on other geographical areas or financial markets. Within the framework of oil markets, these shocks can materialize in the form of rapid price swings, delays in supply, or geopolitical tensions. The widespread nature of spillover effects in financial markets has been underlined in studies conducted by [

3]. These studies shed light on the interconnectedness of global financial markets, illustrating how events occurring in a particular country or region can have reverberating impacts on a global scale. Spillover effects frequently arise as a result of the interdependence of energy markets, whereby disparities in supply and demand within a particular region can significantly influence global oil prices. The oil price shocks that occurred throughout the 1970s, such as the OPEC oil embargo, served as a notable illustration of the extensive implications resulting from disturbances within the oil market. The preceding shocks resulted in notable economic consequences, affecting not only states involved in oil production but also those reliant on oil imports. In the latter, escalating energy expenses had a role in exacerbating inflationary forces and precipitating economic contractions [

4].

Furthermore, the examination of risk and returns has undergone significant development and increased intricacy due to the extensive integration of technology [

5,

6]. The spread of news and updates related to regional occurrences such as geopolitical incidents, natural disasters, and worldwide disruptions can cause disruptions in economic markets, hence prompting market participants to react in a corresponding manner. The shifts in the supply and demand dynamics of local crude oil markets have been observed, as noted by [

7]. In the present context, the term “spillover” pertains to the influence imposed by non-oil-related occurrences, such as geopolitical events and natural disasters, on the oil market. The energy market holds significant importance in global market dynamics as it plays a crucial role in both industrial development and home sustenance. The research conducted by [

8] demonstrates that oil markets display bidirectional spillover transmission characteristics, which are also heightened by significant occurrences such as the recent global COVID-19 epidemic. Moreover, it has been observed that significant geopolitical risk shocks in the oil market have been linked to Russia. Consequently, there exists a responsibility for investors and scholars to assess the potential impact of these unrelated occurrences on market prices and returns [

9]. An effective initial step involves comprehending the extent of impacts exhibited by certain areas or nations, exemplified by the Asian members of OPEC+.

The Organization of the Petroleum Exporting Countries and its Allies (OPEC+) is a prominent international organization that aims to stabilize and regulate the global oil market. OPEC+ comprises both OPEC member countries and non-member countries. The main distinction between OPEC+ members and non-members relates to their formal membership status within the organization. OPEC member countries, including prominent oil producers such as Saudi Arabia, Iran, and Venezuela, have full voting rights and actively participate in decision-making processes. The member countries share the joint responsibility of managing oil production levels and implementing production quotas to regulate global oil supply and ensure price stability. Non-member countries of OPEC+ are typically prominent oil-producing nations that do not possess official membership within OPEC, yet have established collaborative alliances with the organization to effectively synchronize oil production plans. These countries are commonly referred to as “non-member OPEC+ countries” [

10]. Prominent countries outside the OPEC+ membership, such as Russia, Oman, Malaysia, and Kazakhstan, are part of the Asian OPEC+ members. While those who are not members of OPEC do not possess the power to vote in the organization’s decision-making processes, they actively engage in collaboration with OPEC member countries to collectively manage oil output and foster stability within the market. The inclusion of non-member countries inside the OPEC+ framework holds major implications. These countries frequently coordinate their oil production strategy with OPEC decisions, willingly agreeing to cuts or increases in production to ensure market stability.

Through collaboration with OPEC, non-members of the organization play a role in stabilizing the worldwide equilibrium between the supply and demand of oil. This collaborative effort has the potential to provide favorable outcomes in terms of oil prices and enhance market confidence. Yet, non-member countries within the OPEC+ framework encounter specific limitations and challenges. Non-members lack direct authority over OPEC’s decision-making processes and may not possess an equivalent level of influence compared to member nations. The absence of official membership may impose constraints on their capacity to influence policy and exert direct influence over crucial aspects pertaining to oil production quotas and pricing. Additionally, non-member countries have individual interests and priorities that may diverge from those of OPEC member countries. They face the challenge of balancing their domestic economic objectives, such as maximizing revenue from oil exports, while also contributing to the joint endeavors aimed at achieving stability within the worldwide oil market. Occasional conflicts or tensions may arise between non-members and OPEC member countries regarding production levels and market strategies. Extensive studies have been conducted on volatility spillover effects of OPEC oil prices and returns [

11,

12,

13]. Nevertheless, it is imperative to have a more profound comprehension of the intricacies inherent in non-member nations and their engagements with the OPEC+ alliance.

Several scholars have analyzed the volatility and movement of oil returns and prices, particularly in relation to significant risk events such as the financial crisis of 2007–2008 [

2], the uncertainty surrounding economic policies in the BRIC countries [

14], and declarations made by OPEC [

15]. Additional events that have been subject to research include the Gulf War of 1990–1991, the Iraq War of 2003, the occurrences of Hurricanes Rita and Katrina in late 2005, the Arab Spring of 2011, the ongoing COVID-19 pandemic, and the Russia–Ukraine conflicts from 2022 [

16]. These studies provide further evidence of the significance of spillover effects on market returns. The current geopolitical landscape has prompted a closer examination of the involvement of significant non-member countries of OPEC+ in the oil trade and financial benefits. This scrutiny is particularly relevant in light of the European sanctions and restrictions imposed on the industry. Given the ongoing challenges faced by OPEC in maintaining global energy pricing and supplies, as well as addressing the Russia–Ukraine crisis, it is pertinent to explore the potential impact of these external factors on the oil returns of non-member countries. Our research contributes to the literature on spillover in the oil market in three ways.

Firstly, the study employs the Diebold–Yilmaz index, which offers an improved approach to investigating this phenomenon. The model quantifies the transmission of volatility or shocks between different markets or assets. It also measures the connectedness and interdependence of markets in terms of volatility rather than direct causality [

17]. Secondly, the study focuses its attention on Asian OPEC+ members, encompassing Russia, a prominent oil producer in the region in the context of recent geopolitical events. Finally, the study examines the collective impact of two major exogenous variables—geopolitical events [

18] and natural disasters [

19]—on the spillover effect in the oil market. In light of significant global events such as the earthquake in Turkey–Syria in 2023, the confrontation between Russia and Ukraine in 2022, the European heatwave in 2022, and the South Asian floods in 2020, these two factors have emerged as the most persistent components. These factors are considered to pose the most significant shocks to oil prices [

20,

21]. The outcomes of this study hold significant value for market participants as they seek to assess the spillover impact of these external influences. Consequently, this is expected to have an impact on the construction of portfolios and the implementation of hedging strategies within the financial industry. The purpose of this study is to examine the effects that spillovers of geopolitical events and natural disasters have on oil returns among Asian members of OPEC+. The study integrated data collected over a period of twenty years. However, it is important to note that certain noteworthy occurrences, such as geopolitical events, were examined with careful consideration of key factors before the data collection period, and these events might have had an impact on the credibility and validity of the study. The selection of the data period was primarily motivated by the limited accessibility of stock return data for a significant number of the oil businesses that were included in the analysis. The primary reason for this is that many companies recently became listed and hence lack historical stock data.

The foundation of financial decision making lies in the capacity to measure and evaluate risk and return, which are limited to tangible factors that can be precisely and conveniently quantified [

5,

22]. Still, the emergence of recent external market activities or environmental variables has become a notable concern for investors, as they possess the capacity to induce substantial fluctuations in risk, particularly within the oil market. The main focus of this study is to offer significant insights into the spillover impacts of crucial economic variables. This will ultimately contribute to increasing the accuracy and confidence of decision-making processes for investors operating within the oil market. Moreover, the study holds relevance for key actors in the oil industry, including managers, employees, and policymakers, as it provides an empirical basis for informed decision making during periods of significant global occurrences. Additionally, it facilitates comprehension of the potential consequences for the market. Furthermore, this research aims to establish a platform for academics to develop feasible econometric models capable of predicting or measuring the characteristics of spillover effects. This, in turn, would assist in making informed economic decisions at the individual, firm, and state levels. This study holds particular significance in light of the persistent shocks in the oil market that have been instigated by actions unrelated to the oil industry. Our study comprises five distinct sections. The introductory chapter offers a comprehensive examination of the study’s contextual framework and clearly defines the issue statement, research objectives, and significance. The second section provides an overview of relevant academic literature pertaining to the subject matter areas of geopolitical events and natural disasters that are the focus of this study. The next part provides a comprehensive discussion of the research methodology employed, which includes an examination of the research design, data collection techniques, research model implemented, data processing methods, analysis procedures, and ethical issues taken into account. The subsequent sections of this study clarify the findings and conclusions derived from the research and provide recommendations based on these outcomes.

3. Research Design

3.1. The Sample

The sample includes monthly data on three key variables: Oil Stock Returns, Geopolitical Risk Index (GRI), and Natural Disaster Index (NDI). The period of data collection is from 1 January 2000 to 1 March 2023.

3.1.1. Dependent Variable: Oil Stock Returns (NOPEC)

The study aimed to analyze the returns of publicly traded oil companies operating in non-member countries of the OPEC+ alliance. Since there was no existing return index specifically designed for these non-member OPEC+ countries, this study created one. The study focused on ten OPEC+ non-member countries: Azerbaijan, Bahrain, Brunei, Kazakhstan, Malaysia, Mexico, Oman, Russia, Sudan, and South Sudan. To construct the index, an extensive search was conducted using a Bloomberg terminal to gather monthly returns data for the period from 2000 to 2023. Initially, 61 publicly listed oil companies from the selected countries were identified. However, due to limited data availability for some recently listed companies, nine were excluded from the stock portfolio. Subsequently, 54 companies met the criteria for inclusion in the index, and they came from four countries: Kazakhstan, Oman, Malaysia, and Russia (

Table 1). The weights for these companies within the portfolio were assigned based on their market capitalization as of 29 May 2023. The market capitalization values were converted into USD using exchange rates obtained from Yahoo Finance on 28 May 2023. Since the data period for returns data varied across the companies, multiple data ranges were used to calculate weighted returns for different periods, ensuring the creation of a reliable index. The index created for this study is referred to as the “NOPEC Index,” indicating its purpose as a return index specifically designed for non-member OPEC+ countries (please see

Appendix A). The data and other relevant information for this index can be found in

Appendix B.

3.1.2. Independent Variables

Geopolitical Risk Index (GRI)

The Geopolitical Risk Index serves as a crucial metric for quantifying the impact of geopolitical events. This index offers a comprehensive and measurable assessment of geopolitical risks. Specifically, the seminal study [

39] is widely acknowledged for its meticulous analysis and rigorous methodology in capturing and quantifying these risks. Their index encompasses various indicators, such as political instability, conflicts, policy uncertainty, and diplomatic tensions, thereby providing a holistic evaluation of geopolitical risks. In addition to the overall Geopolitical Risk index, Caldara and Iacoviello also developed two sub-indexes called geopolitical threats and acts (GPRT and GPRA). The GPRT sub-index comprised words associated with categories 1 to 5, which encompassed war, peace, nuclear, and terrorism threats, as well as military buildups. On the other hand, the GPRA sub-index included words related to categories 6 to 8, representing the beginning of war, the escalation of war, and terrorism acts. Notably, the GRI facilitates standardized measurements, enabling comparisons across different times and countries. For this study, a recent iteration of the GRI from [

39], which incorporated broader search criteria, was used. The data were acquired from an accessible dedicated site (refer to the provided site:

https://www.matteoiacoviello.com/gpr.htm, accessed on 17 March 2023) and subsequently processed and organized to ensure consistency and compatibility with the research objectives. This included identifying relevant periods and aligning the dataset with other variables utilized in the study. Notably, the GRI facilitates standardized measurements, enabling comparisons across different times and countries. This characteristic ensures the data’s reliability and validity when evaluating the geopolitical event factor within the context of spillover analysis in the oil market.

Natural Disaster Index (NDI)

The Natural Disaster Index employed in this study serves to assess the economic ramifications of natural disasters, encompassing both the financial costs and the human toll incurred. The primary data source utilized for constructing this index is the publicly available EMDAT database (refer to

https://www.emdat.be), which records occurrences of natural disasters and provides information on mortality, morbidity, and financial losses. Ref. [

68] proposed an approach to creating the Natural Disaster Index which was adopted in this study. The methodology employed by [

68] is founded on the World Health Organization’s calculation of the DALYs (disability-adjusted life years) lost through injuries and diseases (WHO 2013). Like the DALYs approach, the measurement framework utilizes life years as the unit of analysis. However, whereas DALYs focus solely on the health-related impacts of diseases, Noy’s measurement framework seeks to encompass the broader effects of calamities on human well-being, considering infrastructure and capital destruction. For the study, the index was adapted to a monthly format and recreated on the most recent EMDAT database available up until 1 April 2023.

3.2. The Diebold–Yilmaz Model

This study’s goal is to investigate and quantify the transmission of volatility, including its direction and intensity. We decided to use the approach first suggested by [

29] to achieve this. The Diebold–Yilmaz (DY-2012) model allows bilateral volatility spillovers, in contrast to the Spillover Asymmetric Multiplicative Error (SAMEM) model introduced by [

69], which necessitates predetermined directions in volatility. Additionally, the DY-2012 model enables us to assess the magnitude of spillovers by constructing an index for volatility transmissions. This feature facilitates meaningful comparisons across different variable sets and model configurations. Lastly, ref. [

17] use a framework for generalized Vector Autoregression that does not rely on the order of the variables. This construction encompasses four categories of spillovers: directional, total, net, and net pairwise spillovers. These categories depict the level of connectedness or relationship among variables. The setup of the spillover indexes involves the utilization of a covariance-stationary VAR(p). According to this, we can express:

where function

is a vector of return/volatility series of dimensions N × 1,

represents an

matrix of parameters,

is a vector of disturbances that are dispersed independently and identically, and

is the variance matrix of the error vector

. The moving average form appears as follows:

where

is considered to be recursive.

presents a matrix of

dimensions, for

for

. The moving average’s coefficients in Equation (2) provide the framework for comprehending the dynamic procedure needed to calculate spillover indices. Prior to presenting the representations for the indices, it is essential to consider the following factors:

In forecasting , own variance shares represent the fractions of H-step-ahead error variances, which result from shocks to , for

The fractions of the H-step-ahead error variances in forecasting that derive from shocks to are known as cross variance shares or spillovers, for , such that .

The H-step-ahead forecast error variance decompositions, indicated by

, are stated as follows using the generalized VAR framework of KPSS:

where

represents the standard deviation of

for the

th equation and where the selection vector is

, with 1 as the

th element and 0 otherwise. The discrepancy arises from the fact that the combined contributions of the variance of the forecast error do not amount to a total of one, where is

. Diebold and Yilmaz (2012) employed a normalization technique whereby each item of the variance decomposition matrix was divided by the total of its respective row. As shown by

, the normalized KPSS H-step-ahead forecast error variance decompositions are written as follows:

where

and

by construction. Taking these factors into account, the total spillover index is represented as:

In summary, Equation (5) quantifies the extent of spillover contributions resulting from shocks in variables from to , for .

Table 2 presents related work and literature contributions of spillovers using the Diebold and Yilmaz model. Other similar studies also employed a GARCH model.

3.3. Preliminary Analysis

The preliminary analysis involved descriptive statistics and unit root tests for 279 observations. As an initial step, we use data transformation to account for the disparity in scale between returns and the other indexes, considering our focus on measuring spillover effects on returns rather than prices. It is essential to acknowledge the inherent differences in scale between these variables. Returns are expressed as percentage changes between consecutive periods, while indexes are represented in absolute terms. Consequently, the divergent scales can hinder direct comparisons. Moreover, the NDI and GRI had high values. To address this challenge, we utilize the natural logarithm of the indexes.

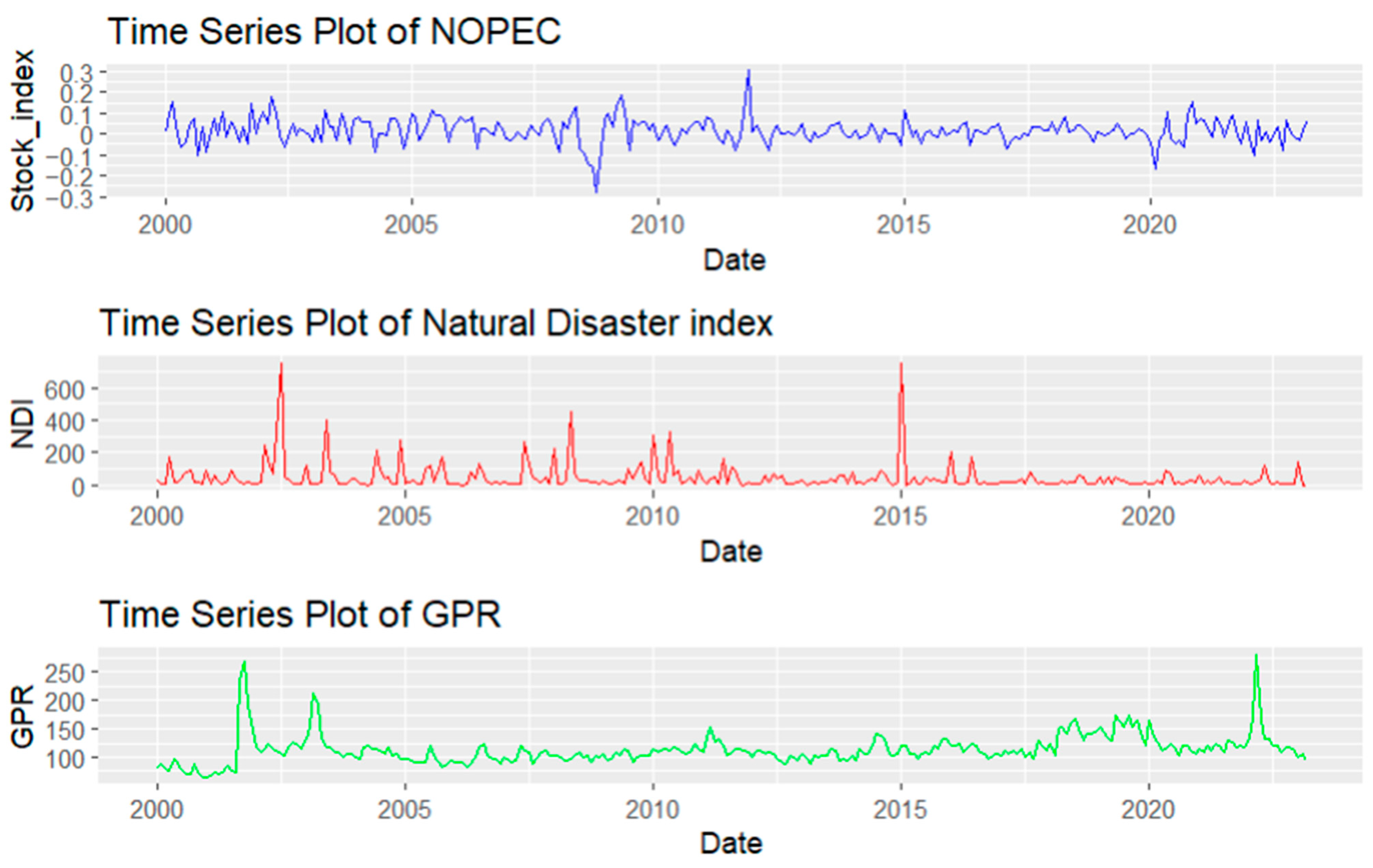

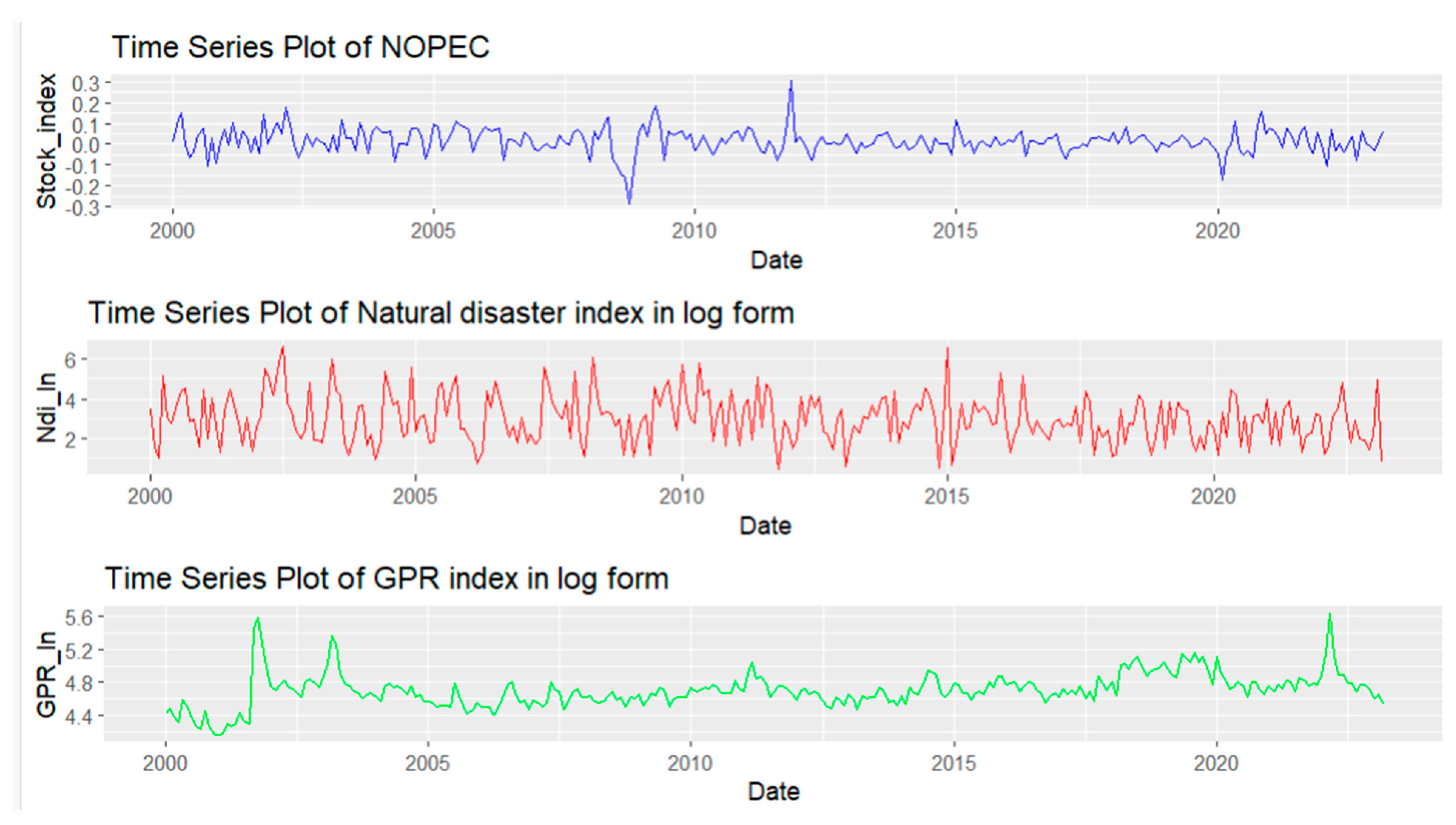

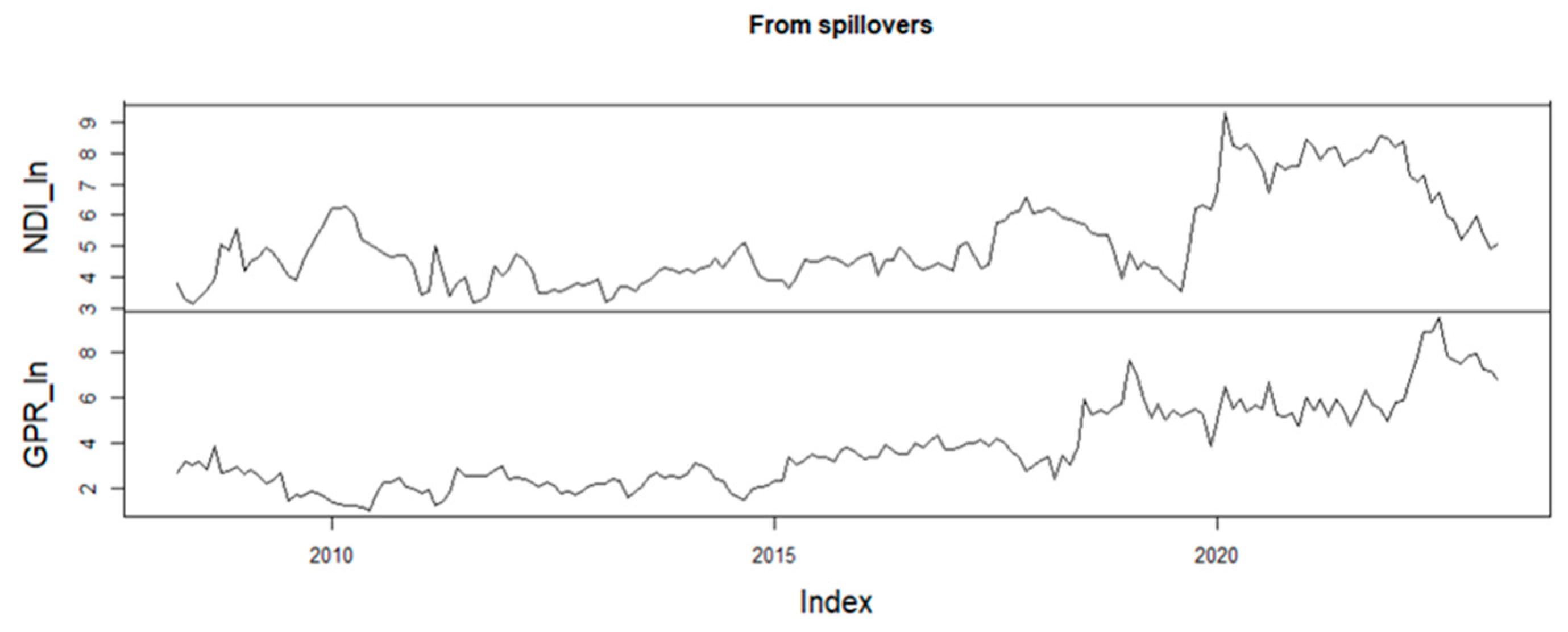

Employing the natural logarithm facilitates a transformation of the absolute index values into a scale that is more conducive to comparisons with returns. Specifically, the natural logarithm of an index provides a metric of the continuous growth rate of the index, rendering it more comparable to returns. This transformation enables a more accurate measurement of the degree of connectedness between different returns and indexes. The accompanying plots (

Figure 1 and

Figure 2) depict the data before and after the logarithmic transformation, illustrating the impact of this adjustment.

Stock_Index: 2008–2009 (Great Recession), 2011 (Libyan war), 2020 (COVID-19).

NDI_ln: 2003 (Iran Bam Earthquake, China floods and Korea Maemi Typhoon), 2004 (Sumatra Earthquake, Indian Ocean Tsunami), 2005 (Hurricanes Katerina and Wilma), 2007(Windstorm and floods in Bangladesh and China, Japan Earthquake), 2008 (Cyclone Nargis in Myanmar and Sichuan Earthquake in China), 2010 (Haiti Earthquake and Russian Summer Heatwave), 2015 (Nepal Earthquake) (EMDAT Database).

GRI_ln: 2001 (9/11 terrorist attacks, Iraq war, London Bombings), 2011 (Military intervention in Libya), 2014/15 (Russia annexes Crimea), 2019/20 (US-North Korea tensions, US-Iran tensions), 2022 (Russia-Ukraine conflict) [

39].

We employ a unit root test for all the variables after log transformation, which further confirmed the stationarity of the return index at a 1% significance level for all test types except for KPSS, which shows that the stationarity might be trend stationary and not strict stationary. It was a similar case for natural disasters and geopolitical risk, even though these two were stationary at 5% using only the intercept for DF-GLS.

Table 3 displays the descriptive statistics for the variables included in the study. Notably, the average returns of oil stocks from the selected Asian OPEC+ member countries over the study period were positive. The GRI and NDI variables exhibited positive skewness, indicating a tendency towards higher values. The average values for the Geopolitical Risk Index and the Natural Disaster Index are also provided. Moreover, the kurtosis values for GRI and NOPEC exceed three, indicating a leptokurtic distribution. Similarly, the Jarque–Bera statistics revealed evidence of non-normality in the variables under investigation.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}