Evaluation of Outsourcing Development in the Service Sector

and

and

Abstract

1. Introduction

2. Literature Review and Statistical Data Analysis

2.1. Literature Review

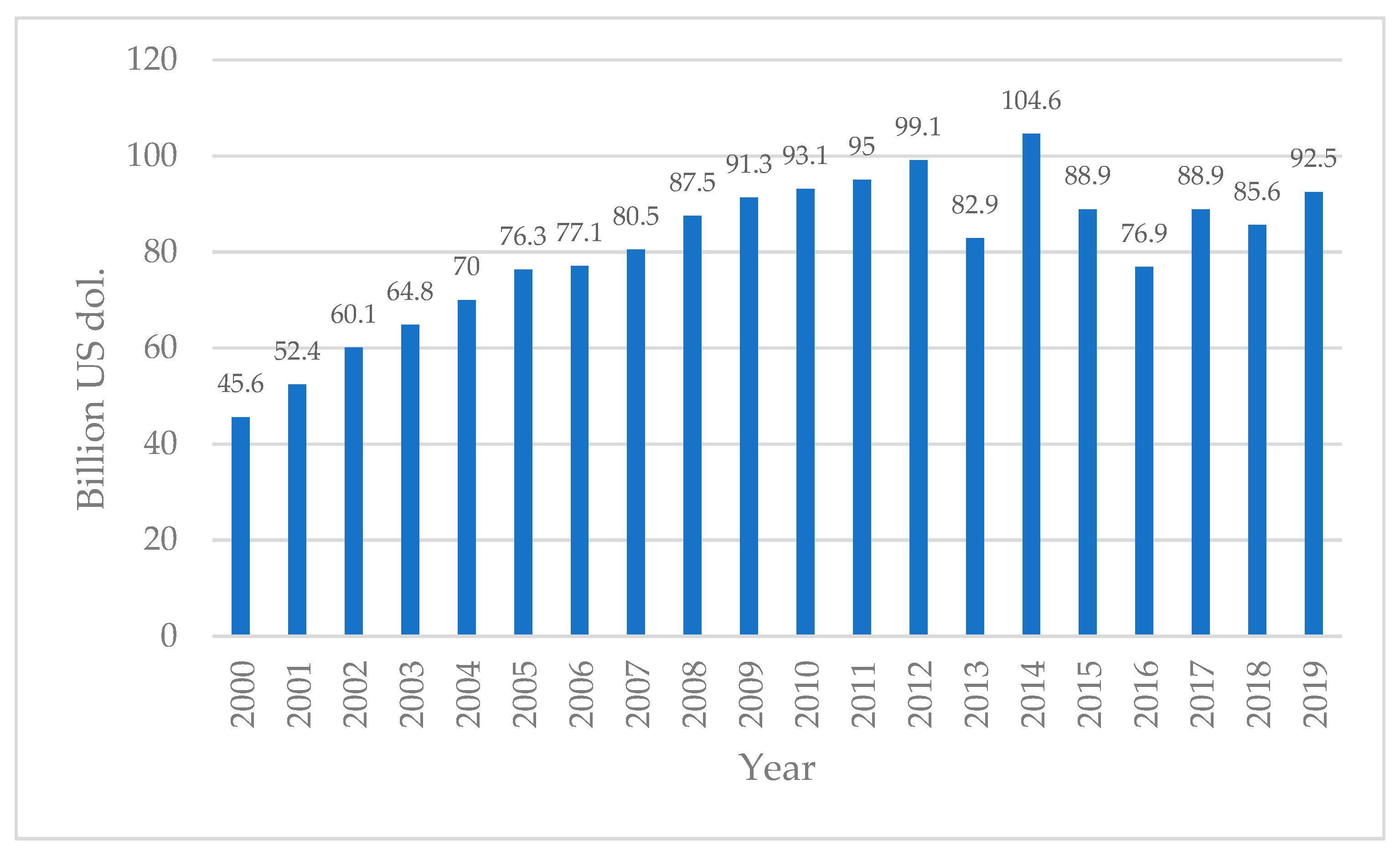

2.2. Statistical Data Analysis

3. Methodology

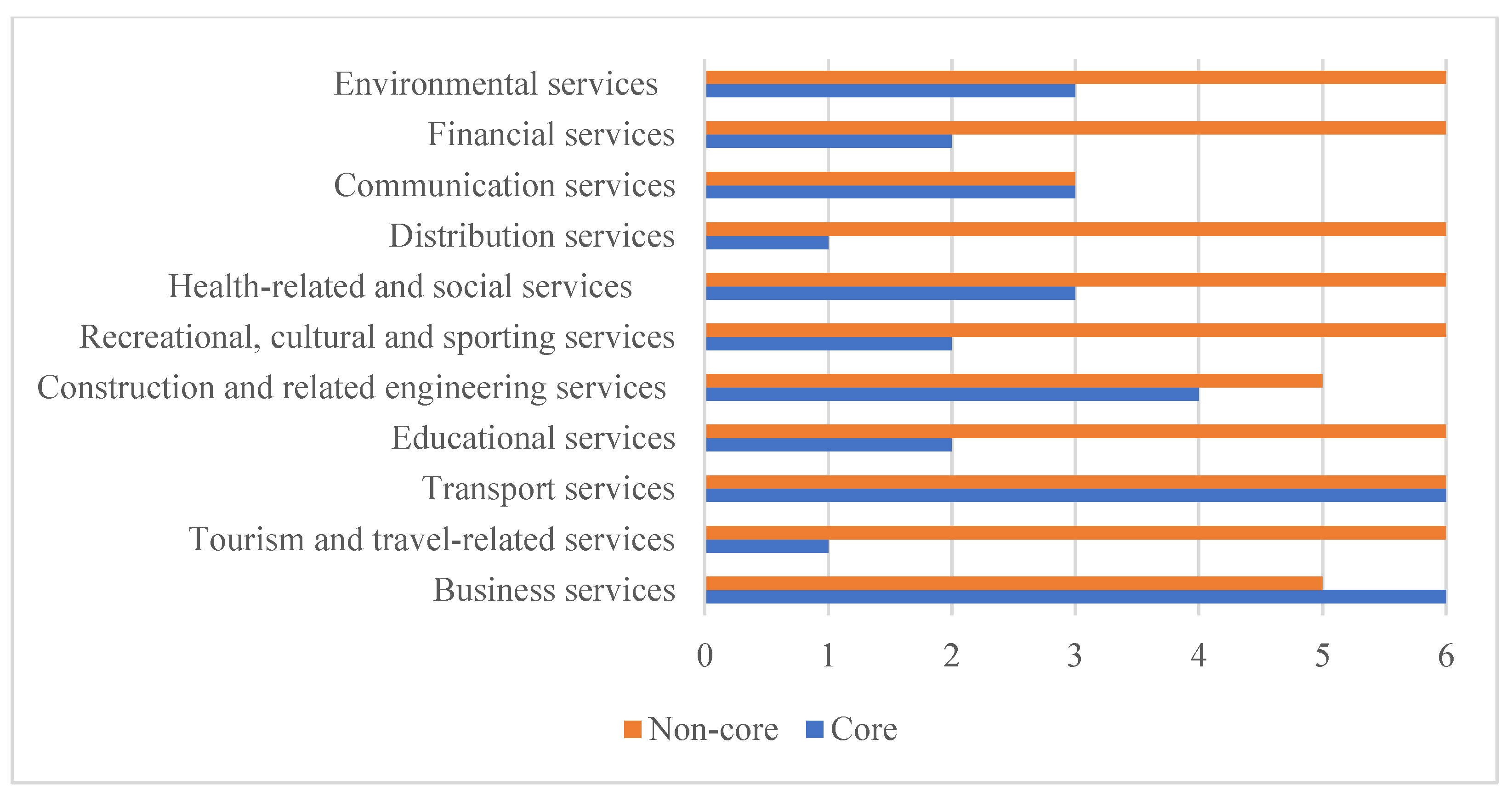

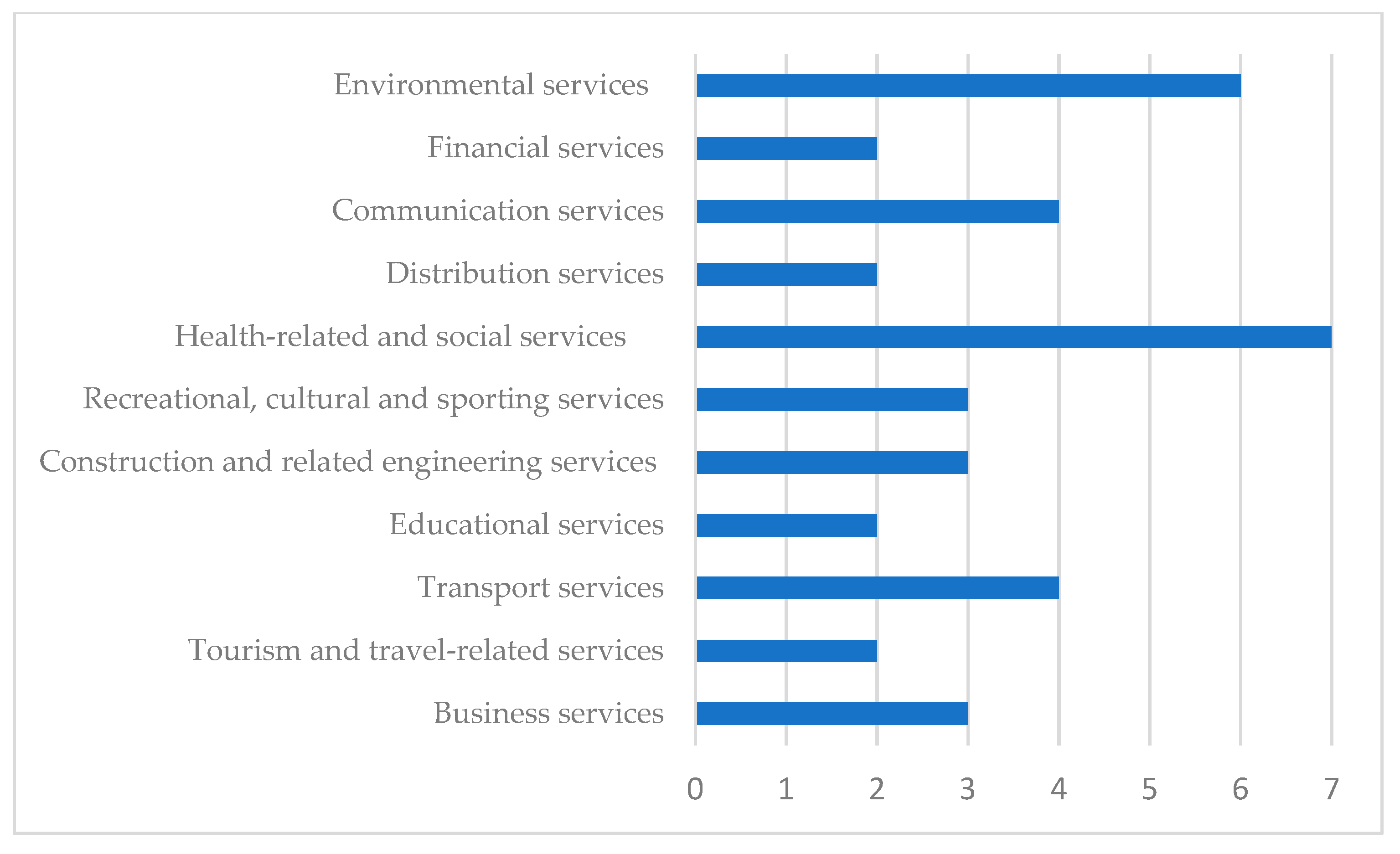

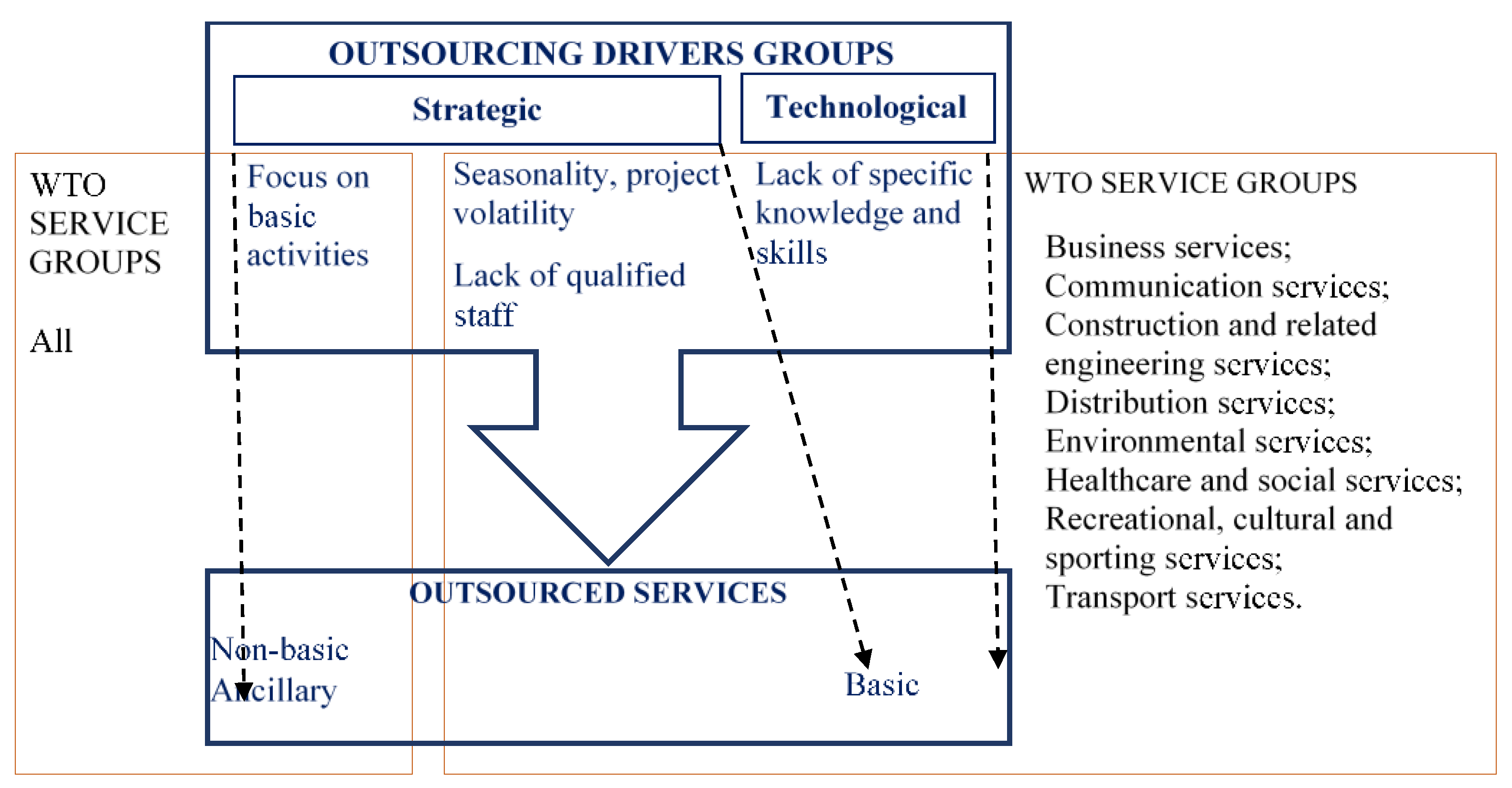

4. Results

5. Conclusions

Author Contributions

Funding

Conflicts of Interest

References

- Amendolagine, Vito, Rosa Capolupo, and Giovanni Ferri. 2014. Innovativeness, offshoring and black economy decisions. Evidence from Italian manufacturing firms. International Business Review 23: 1153–66. [Google Scholar] [CrossRef]

- Assaf, Sadi, Mohammad A. Hassanain, Abdul-Mohsen Al-Hammad, and Ahmed Al-Nehmi. 2011. Factors affecting outsourcing decisions of maintenance services in Saudi Arabian universities. Property Management 29: 195–212. [Google Scholar] [CrossRef]

- Augustinaitis, Arūnas, Vitalija Rudzkienė, Rimantas Alfonsas Petrauskas, Ina Dagytė, Eugenija Martinaitytė, Edgaras Leichteris, Eglė Malinauskienė, Vanda Višnevska, and Ieva Žilionienė. 2009. Lietuvos Evaldžios Gairės: Ateities Įžvalgų Tyrimas: Monograph. Vilnius: Mykolas Romeris Unversity Publishing Centre. [Google Scholar]

- Baatartogtokh, Baljir, W. Scott Dunbar, and Dirk van Zyl. 2018. The state of outsourcing in the Canadian mining industry. Resources Policy 59: 184–91. [Google Scholar] [CrossRef]

- Bagieńska, Anna. 2016. The demand for professional knowledge as a key factor of the development of outsourcing of financial and accounting services in Poland. Business, Management and Education 14: 19–33. [Google Scholar] [CrossRef]

- Baytok, Ahmet, Huseyin Soybali Hasan, and Ozcan Zorlu. 2013. Outsourcing in Thermal Hotel Enterprises: The Case of Turkey. Business Management Dynamics 3: 1–14. [Google Scholar]

- Borodako, Krzysztof, Jadwiga Berbeka, and Michał Rudnicki. 2015. External and Internal Factors Motivating Outsourcing of Business Services by Meeting-Industry Companies: A Case Study in Krakow, Poland. Journal of Convention & Event Tourism 16: 93–115. [Google Scholar]

- Bush, Ashley A., Amrit Tiwana, and Hiroshi Tsuji. 2008. An empirical investigation of the drivers of software outsourcing decisions in Japanese organisations. Information and Software Technology 25: 499–510. [Google Scholar] [CrossRef]

- Canham, Stephen, and Robert T. Hamilton. 2013. SME internationalisation: Offshoring, “backshoring”, or staying at home in New Zealand. Strategic Outsourcing: An International Journal 6: 277–91. [Google Scholar] [CrossRef]

- Chen, Sim Siew, and Yee Seow Voon. 2016. Exploring Human Resource Outsourcing Trends in Malaysia. Procedia-Social and Behavioral Sciences 224: 491–98. [Google Scholar] [CrossRef][Green Version]

- Eggert, Andreas, Eva Böhm, and Christina Cramer. 2017. Business service outsourcing in manufacturing firms: An event study. Journal of Service Management 28. [Google Scholar] [CrossRef]

- Espino-Rodríguez, Tomás F., and Juan Carlos Ramírez-Fierro. 2017. Factors determining hotel activity outsourcing. An approach based on competitive advantage. International Journal of Contemporary Hospitality Management 29: 2006–26. [Google Scholar] [CrossRef]

- Eurostat Statistics Data. n.d. Available online: https://ec.europa.eu/eurostat/data/statistics-a-z/abc (accessed on 27 January 2021).

- Ferruzzi, Marcos Antonio, Mário Sacomano Neto, Eduardo Eugênio Spers, and Mateus Canniatti Ponchio. 2011. Reasons for outsourcing services in medium and large companies. Brazilian Business Review, Fucape Business School 8: 44–66. [Google Scholar] [CrossRef]

- Gaižauskienė, Inga, and Natalija Valavičienė. 2016. Socialinių Tyrimų Metodai: Kokybinis Interviu. Vilnius: Mykolo Romerio Universitetas, p. 392. [Google Scholar]

- Gbadegesin, Job Taiwo, and Theophilus Olugbenga Babatunde. 2015. Investigating expert‘s opinion on outsourcing decision in facilities management practice in public universities in Nigeria. Journal of Facilities Management 13: 27–41. [Google Scholar] [CrossRef]

- Gewald, Heiko, and Jens Dibbern. 2009. Risks and benefits of business process outsourcing: A study of transaction services in the German banking industry. Information & Management 46: 249–57. [Google Scholar]

- Ghausi, Nadjya. 2002. Trends in outsourced manufacturing—Reducing risk and maintaining flexibility when moving to an outsourced model. Assembly Automation 22: 21–25. [Google Scholar] [CrossRef]

- Grama, Ana, and Vasile-Daniel Păvăloaia. 2014. Outsourcing IT—The alternativ ve for a successful Romanian SME. Procedia Economics and Finance 15: 1404–12. [Google Scholar] [CrossRef]

- Hanafizadeh, Payam, and Ahad Zare Ravasan. 2018. An empirical analysis on outsourcing decision: The case of e-banking services. Journal of Enterprise Information Management 31: 146–72. [Google Scholar] [CrossRef]

- Hassanain, Mohammad A., Sadi Assaf, Abdul-Mohsen Al-Hammad, and Ahmed Al-Nehmi. 2015. A multicriteria decision making model for outsourcing maintenance services. Facilities 33: 229–44. [Google Scholar] [CrossRef]

- Abdul-Halim, Hasliza, and Norbani Che-Ha. 2010. HR outsourcing among Malaysian manufacturing companies. Business Strategy 11: 363–70. [Google Scholar] [CrossRef]

- Horgos, Daniel. 2007. International Outsourcing—Some Measurement Problems: An Empirical Analysis of Outsourcing Activities in Germany. Hamburg: Department of Economics, Helmut Schmidt University. [Google Scholar]

- Ikediashi, Dubem, and Onuwa Okwuashi. 2015. Significant factors influencing outsourcing decision for facilities management (FM) services: A study of Nigeria’s public hospitals. Property Management 33: 59–82. [Google Scholar] [CrossRef]

- Jain, Ravi Kumar, and Ramachandran Natarajan. 2011. Factors influencing the outsourcing decisions: A study of the banking sector in India. Strategic Outsourcing: An International Journal 4: 294–322. [Google Scholar] [CrossRef]

- Johansson, Malin, Jan Olhager, Jussi Heikkilä, and Jan Stentoft. 2018. Offshoring versus backshoring: Empirically derived bundles of relocation drivers, and their relationship with benefits. Journal of Purchasing and Supply Management 25: 196–204. [Google Scholar] [CrossRef]

- Kaivo-Oja, Jari, Mikkel Stein Knudsen, and Theresa Lauraéus. 2018. Reimagining Finland as a manufacturing base: The nearshoring potential of Finland in an industry 4.0 perspective. Business, Management and Economics Engineering 16: 65–80. [Google Scholar] [CrossRef]

- Kavosi, Zahra, Hamed Rahimi, Saeideh Khanian, Payam Farhadi, and Erfan Kharazmi. 2018. Factors influencing decision making for health care services outsourcing: A review and Delphi study. Medical Journal of the Islamic Republic of Iran (MJIRI) 32: 56. [Google Scholar] [CrossRef]

- Kinkel, Steffen, and Spomenka Maloca. 2009. Drivers and antecedents of manufacturing offshoring and backshoring—A German perspective. Journal of Purchasing & Supply Management 15: 154–65. [Google Scholar] [CrossRef]

- Lahiri, Somnath, and Ben L. Kedia. 2011. Co-evolution of institutional and organisational factors in explaining offshore outsourcing. International Business Review 20: 252–63. [Google Scholar] [CrossRef]

- Lam, Terry, and Michael X. J. Han. 2005. A study of outsourcing strategy: A case involving the hotel industry in Shanghai, China. Hospitality Management 24: 41–56. [Google Scholar] [CrossRef] [PubMed]

- Lamminmaki, Dawne. 2011. An examination of factors motivating hotel outsourcing. International Journal of Hospitality Management 30: 963–73. [Google Scholar] [CrossRef]

- Lau, Kwok Hung, and Jianmei Zhang. 2006. Drivers and obstacles of outsourcing practices in China. International Journal of Physical Distribution & Logistics Management 36: 776–92. [Google Scholar] [CrossRef]

- Libby, Robert, and Roger K. Blashfield. 1987. Performance of a composite as a function of the number of judges. Organisational Behavior and Human Performance 21: 121–29. [Google Scholar] [CrossRef]

- Moon, Karen Ka-Leung, Fung-Yi Tam, Mei-Mei Lau, and Jimmy M. T. Chang. 2014. Production Outsourcing: Perspectives from Small and Medium-sized Enterprises. Research Journal of Textile and Apparel 18: 65–83. [Google Scholar] [CrossRef]

- Munjal, Surender, Ignacio Requejo, and Sumit K. Kundu. 2019. Offshore outsourcing and firm performance: Moderating effects of size, growth and slack resources. Journal of Business Research 103: 484–94. [Google Scholar] [CrossRef]

- Nordigården, Daniel, Jakob Rehme, Staffan Brege, Daniel Chicksand, and Helen Walker. 2014. Outsourcing decisions—The case of parallel production. International Journal of Operations & Production Management 34: 974–1002. [Google Scholar] [CrossRef]

- OECD. n.d. Stat Data and Metadata. Available online: https://stats.oecd.org/ (accessed on 27 November 2020).

- Roza, Marja, Frans A. J. Van den Bosch, and Henk W. Volberda. 2011. Offshoring strategy: Motives, functions, locations, and governance modes of small, medium-sized and large firms. International Business Review 20: 314–23. [Google Scholar] [CrossRef]

- Rupšienė, Liudmila. 2007. Kokybinių Tyrimų Duomenų Rinkimo Metodologija. Klaipėda: University of Klaipėda, p. 147. [Google Scholar]

- Sani, Azurin, Shahin Dezdar, and Sulaiman Ainin. 2013. Outsourcing patterns among Malaysian hotels. International Journal of Business and Social Science 4: 113–14. [Google Scholar]

- Sigala, Ioanna Falagara, and Tina Wakolbinger. 2019. Outsourcing of humanitarian logistics to commercial logistics service providers: An empirical investigation. Journal of Humanitarian Logistics and Supply Chain Management 9: 47–69. [Google Scholar] [CrossRef]

- Sinha, Paresha, Michèle E. M. Akoorie, Qiang Ding, and Qian Wu. 2011. What motivates manufacturing SMEs to outsource offshore in China?: Comparing the perspectives of SME manufacturers and their suppliers. Strategic Outsourcing: An International Journal 4: 67–88. [Google Scholar] [CrossRef]

- Slepniov, Dmitrij, and Brian Vejrum Waehrens. 2008. Offshore outsourcing of production: An exploratory study of process and effects in Danish companies. Strategic Outsourcing: An International Journal 1: 64–76. [Google Scholar] [CrossRef]

- Smuts, Hanlie, Paula Kotzé, Alta van der Merwe, and Marianne Loock. 2010. Information systems outsourcing issues in the communication technology sector. Paper presented at the IADIS International Conference Information Systems, Porto, Portugal, March 18–20; pp. 145–55. [Google Scholar]

- Sobinska, Malgorzata, and Leslie Willcocks. 2016. IT outsourcing management in Poland—Trends and performance. Strategic Outsourcing: An International Journal 9: 60–96. [Google Scholar] [CrossRef]

- Srivastava, Dabhana, and Ramkishen Rajan. 2006. Global outsourcing of services: Issue and implication. Harvard Asia Pacsific Review 9: 39–40. [Google Scholar]

- Suweero, Kittipong, Wutthipong Moungnoi, and Chotchai Charoenngam. 2017. Outsourcing decision factors of building operation and maintenance services in the commercial sector. Property Management 35: 254–74. [Google Scholar] [CrossRef]

- TPI: Information Service Group, Statista. 2020. Available online: https://www.statista.com/statistics/189788/global-outsourcing-market-size/ (accessed on 27 January 2021).

- Trushchenko, Irina V., Marina V. Samoshkina, and Evgenia V. Vikulina. 2021. Assessing the Expediency of Using Outsourcing in Various Economic Sectors: A Review of the Existing Approaches. In Frontier Information Technology and Systems Research in Cooperative Economics. Studies in Systems, Decision and Control. Edited by Aleksei V. Bogoviz, Alexander E. Suglobov, Alexandr N. Maloletko, Olga V. Kaurova and Svetlana V. Lobova. Cham: Springer, vol. 316. [Google Scholar] [CrossRef]

- Varajão, João, Maria Manuela Cruz-Cunha, and Maria da Glória Fraga. 2017. IT/IS Outsourcing in Large Companies—Motivations and Risks. Procedia Computer Science 121: 1047–61. [Google Scholar] [CrossRef]

- Wallo, Andreas, and Henrik Kock. 2018. HR outsourcing in small and medium-sized enterprises. Exploring the role of human resource intermediaries. Personnel Review 47: 1003–18. [Google Scholar] [CrossRef]

- Wan, Chin-Sheng, and Allan Yen-Lun Su. 2010. Exploring the Factors Affecting Hotel Outsourcing in Taiwan. Asia Pacific Journal of Tourism Research 15: 95–107. [Google Scholar] [CrossRef]

- World Trade Organisation (WTO). n.d. Trade and Tariff Data. Available online: https://www.wto.org/english/res_e/statis_e/statis_e.htm (accessed on 20 November 2020).

- World Bank: World Development Report. 2020. Available online: https://www.worldbank.org/en/publication/wdr2020 (accessed on 27 November 2020).

- World Trade Report. 2019. The Future of Services Trade. Available online: https://www.wto.org/english/res_e/booksp_e/00_wtr19_e.pdf (accessed on 27 January 2021).

- Zhang, Yan, Emily Ma, and Hailin Qu. 2018. Transaction Cost and Resources Based Views on Hotels’ Outsourcing Mechanism: An Empirical Study in China. Journal of Hospitality Marketing & Management 27: 583–600. [Google Scholar] [CrossRef]

- Žydžiūnaitė, Vilma, and Stanislav Sabaliauskas. 2017. Kokybiniai Tyrimai. Principai ir Metodai. Vilnius: Vaga, p. 385. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Groups of Outsourcing Drivers | Services Analyzed and the Author of the Research | ||||||||

|---|---|---|---|---|---|---|---|---|---|

| Accommodation Services | Financial Services | Healthcare Services | Educational Services | Commercial Services | |||||

| Espino-Rodríguez and Ramírez-Fierro (2017) | Hanafizadeh and Ravasan (2018) | Gewald and Dibbern (2009) | Kavosi et al. (2018) | Ikediashi and Okwuashi (2015) | Gbadegesin and Babatunde (2015) | Hassanain et al. (2015) | Assaf et al. (2011) | Suweero et al. (2017) | |

| Tactical | + | ||||||||

| Strategic | + | + | + | + | + | + | + | ||

| Material | + | ||||||||

| Non-material | + | ||||||||

| Economic | + | + | + | + | + | + | + | ||

| Basic activity | + | ||||||||

| Specialised resources | + | ||||||||

| Quality improvement | + | + | + | + | + | + | + | ||

| Managerial | + | + | + | + | + | ||||

| Technological | + | + | + | + | + | ||||

| Innovation | + | ||||||||

| Time | + | ||||||||

| Social | + | ||||||||

| Functional | + | + | + | + | |||||

| Expert | WTO Service Sector and Its Sub-Sector | Position | Size of Enterprise (Number of Employees) | Expert | WTO Service Sector and Its Sub-Sector | Position | Size of Enterprise (Number of Employees) |

|---|---|---|---|---|---|---|---|

| A1 | I B | Head | 50–249 | A33 | VI L | Director | 50–249 |

| A2 | I B | Director | 10–19 | A34 | VII M | Director | 1–9 |

| A3 | I B | Head | 10–19 | A35 | VII M | Head | 250 and < |

| A4 | I B | Head | 10–19 | A36 | VII M | Director | 20–49 |

| A5 | I B | Director | 20–49 | A37 | VII M | Director | 50–249 |

| A6 | I B | Director | 1–9 | A38 | VII M | Head | 50–249 |

| A7 | II C | Director | 50–249 | A39 | VII M | Director | 50–249 |

| A8 | II D | Director | 1–9 | A40 | VIII N | Director | 1–9 |

| A9 | II E | Head | 250 and > | A41 | VIII N | Head | 20–49 |

| A10 | III F | Director | 10–19 | A42 | VIII O | Director | 50–249 |

| A11 | III F | Director | 50–249 | A43 | VIII O | Director | 50–249 |

| A12 | III F | Director | 50–249 | A44 | VIII O | Director | 50–249 |

| A13 | III F | Director | 50–249 | A45 | VIII O | Director | 50–249 |

| A14 | III F | Director | 10–19 | A46 | IX P | Director | 50–249 |

| A15 | III F | Director | 20–49 | A47 | IX R | Director | 1–9 |

| A16 | IV G | Director | 10–19 | A48 | IX P | Director | 50–249 |

| A17 | IV H | Head | 50–249 | A49 | IX P | Head | 10–19 |

| A18 | IV G | Director | 20–49 | A50 | IX P | Director | 50–249 |

| A19 | IV G | Director | 10–19 | A51 | IX P | Director | 50–249 |

| A20 | IV G | Director | 1–9 | A52 | X S | Head | 250 and < |

| A21 | IV H | Head | 1–9 | A53 | X S | Director | 1–9 |

| A22 | V I | Director | 50–249 | A54 | X T | Head | 250 and < |

| A23 | V I | Director | 50–249 | A55 | X U | Director | 1–9 |

| A24 | V J | Vice-dean | 250 and > | A56 | X T | Director | 1–9 |

| A25 | V J | Professor | 250 and > | A57 | X T | Director | 20–49 |

| A26 | V J | Professor | 250 and > | A58 | XI Z | Director | 50–249 |

| A27 | V J | Head | 250 and > | A59 | XI Z | Director | 20–49 |

| A28 | VI K | Director | 1–9 | A60 | XI Z | Director | 50–249 |

| A29 | VI K | Director | 1–9 | A61 | XI Z | Director | 50–249 |

| A30 | VI K | Director | 50–249 | A62 | XI Z | Director | 20–49 |

| A31 | VI K | Director | 50–249 | A63 | XI Z | Director | 20–49 |

| A32 | VI K | Director | 20–49 |

| Drivers’ Groups | Core Services | Non-Core Services | |||

|---|---|---|---|---|---|

| Frequency of Naming Outsourcing Drivers | Average of Significance of Outsourcing Drivers | Frequency of Naming Outsourcing Drivers | Average of Significance of Outsourcing Drivers | ||

| Drivers | |||||

| Economic | Reduction of general costs | 19 | 3.9 | 58 | 4.5 |

| Exchanging fixed costs for variable | 2 | 3.5 | 2 | 5 | |

| Lack of capital | 1 | 3 | 0 | 0 | |

| Strategic | Flexibility | 2 | 4.5 | 9 | 4 |

| Specialisation of the outsourced service provider in the field | 7 | 4.3 | 38 | 4.4 | |

| Focus on basic activities | 1 | 4 | 22 | 4.8 | |

| Lack of constant need (seasonality/project volatility) | 21 | 4.7 | 22 | 4 | |

| Lack of staff qualified in the field | 9 | 4.1 | 7 | 4.6 | |

| Contingency management | 6 | 3.7 | 2 | 5 | |

| Quick adaptation to changing needs | 3 | 5 | 1 | 4 | |

| Risk-distribution | 0 | 0 | 1 | 5 | |

| Technological | Demand for specific knowledge/skills | 8 | 4.5 | 13 | 4.3 |

| Demand for specific machinery | 7 | 2.9 | 6 | 4.5 | |

| Managerial | Reduction of administrative load | 5 | 2.6 | 18 | 4.4 |

| Time-saving | 3 | 4 | 11 | 4.4 | |

| Quality | Quality improvement | 4 | 4 | 2 | 5 |

| Others | Positive experience of others | 0 | 0 | 2 | 4 |

| Location of service provision | 0 | 0 | 4 | 4.25 | |

| Outsourcing Drivers Group | Service Sector by WTO | ||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Environmental Services | Financial Services | Communication Services | Distribution Services | Health Related and Social Services | Recreational, Cultural and Sporting Services | Construction and Related Engineering Services | Educational Services | Transport Services | Tourism and Travel Related Services | Business Services | KW p-Value | ||||||||||||||

| Mean | SN | Mean | SN | Mean | SN | Mean | SN | Mean | SN | Mean | SN | Mean | SN | Mean | SN | Mean | SN | Mean | SN | Mean | SN | ||||

| Outsourced activities | Core | E | 0.56 | 0.86 | 0.17 | 0.41 | 0.89 | 0.84 | 0.28 | 0.68 | 0.28 | 0.68 | 0.28 | 0.68 | 0.39 | 0.49 | 0.00 | 0.00 | 0.94 | 1.06 | 0.28 | 0.68 | 1.17 | 0.62 | 0.086 |

| S | 0.29 | 0.32 | 0.17 | 0.27 | 1.00 | 0.33 | 0.10 | 0.26 | 0.31 | 0.34 | 0.31 | 0.52 | 0.60 | 0.64 | 0.00 | 0.00 | 0.98 | 0.27 | 0.00 | 0.00 | 1.21 | 0.81 | 0.000 | ||

| M | 0.33 | 0.82 | 0.00 | 0.00 | 0.50 | 0.87 | 0.00 | 0.00 | 0.17 | 0.41 | 0.00 | 0.00 | 0.42 | 1.02 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.92 | 0.92 | 0.020 | ||

| T | 0.00 | 0.00 | 0.00 | 0.00 | 1.00 | 1.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.42 | 1.02 | 1.67 | 1.54 | 0.75 | 1.17 | 0.25 | 0.42 | 0.42 | 1.02 | 0.75 | 1.17 | 0.049 | ||

| Q | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.50 | 1.22 | 0.67 | 1.63 | 1.50 | 2.35 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.246 | ||

| O | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 1.000 | ||

| Outsourcing Drivers | Service Sector by WTO | ||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Environmental Services | Financial Services | Communication Services | Distribution Services | Health Related and Social Services | Recreational, Cultural and Sporting Services | Construction and Related Engineering Services | Educational Services | Transport Services | Tourism and Travel Related Services | Business Services | KW p-Value | ||||||||||||||

| Mean | SN | Mean | SN | Mean | SN | Mean | SN | Mean | SN | Mean | SN | Mean | SN | Mean | SN | Mean | SN | Mean | SN | Mean | SN | ||||

| Outsourced activities | Core | Reduction of overall costs | 1.67 | 2.58 | 0.50 | 1.22 | 2.67 | 2.52 | 0.83 | 2.04 | 0.83 | 2.04 | 0.83 | 2.04 | 1.17 | 1.47 | 0.00 | 0.00 | 1.83 | 2.48 | 0.83 | 2.04 | 2.83 | 2.32 | 0.323 |

| Change of fixed costs to variable | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.50 | 1.22 | 0.00 | 0.00 | 0.67 | 1.63 | 0.567 | ||

| Lack of capital | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.50 | 1.22 | 0.00 | 0.00 | 0.00 | 0.00 | 0.485 | ||

| Flexibility | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.83 | 2.04 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.67 | 1.63 | 0.567 | ||

| Specialization of service provider | 0.83 | 2.04 | 0.50 | 1.22 | 1.33 | 2.31 | 0.00 | 0.00 | 0.00 | 0.00 | 1.67 | 2.58 | 0.83 | 2.04 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.50 | 1.22 | 0.524 | ||

| Concentration | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.67 | 1.63 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.485 | ||

| Absence of constant demand (seasonality or project volatility) | 1.50 | 2.35 | 0.00 | 0.00 | 3.33 | 2.89 | 0.83 | 2.04 | 0.50 | 1.22 | 0.00 | 0.00 | 3.33 | 2.58 | 0.00 | 0.00 | 4.00 | 2.00 | 0.00 | 0.00 | 4.50 | 0.84 | 0.000 | ||

| Lack of staff with certain qualifications | 0.00 | 0.00 | 0.00 | 0.00 | 1.67 | 2.89 | 0.00 | 0.00 | 1.17 | 2.04 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 1.83 | 2.14 | 0.00 | 0.00 | 2.33 | 2.58 | 0.017 | ||

| Control unplanned situations | 0.00 | 0.00 | 0.83 | 2.04 | 0.00 | 0.00 | 0.00 | 0.00 | 0.83 | 2.04 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 1.17 | 1.60 | 0.00 | 0.00 | 0.83 | 2.04 | 0.124 | ||

| Rapid adaptation to changing needs | 0.00 | 0.00 | 0.00 | 0.00 | 1.67 | 2.89 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.83 | 2.04 | 0.00 | 0.00 | 0.83 | 2.04 | 0.330 | ||

| Risk sharing | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 1.000 | ||

| Reducing administrative burdens | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.83 | 2.04 | 1.50 | 2.35 | 1.50 | 2.35 | 0.00 | 0.00 | 0.83 | 2.04 | 1.50 | 2.35 | 0.329 | ||

| Time saving | 0.00 | 0.00 | 0.00 | 0.00 | 2.00 | 2.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 1.83 | 2.04 | 0.00 | 0.00 | 0.50 | 0.84 | 0.00 | 0.00 | 0.00 | 0.00 | 0.002 | ||

| Need for specific knowledge/skills | 0.67 | 1.63 | 0.00 | 0.00 | 1.00 | 1.73 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 1.00 | 1.10 | 0.022 | ||

| Need for specific technique | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.33 | 0.82 | 0.00 | 0.00 | 0.83 | 2.04 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.83 | 2.04 | 0.653 | ||

| Quality Improvement | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.50 | 1.22 | 0.67 | 1.63 | 1.50 | 2.35 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.246 | ||

| Positive experience of others | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 1.000 | ||

| Service location | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 1.000 | ||

| Drivers | Service Groups | ||||||

|---|---|---|---|---|---|---|---|

| Business Services | Construction and Related Services | Communication Services | Transport Services | Healthcare and Related Services | Educational Services | Tourism and Travel Related Services | |

| Lack of constant demand | + | + | + | ||||

| Lack of staff with certain qualifications | + | + | + | + | |||

| Need for specific knowledge/skills | + | + | + | + | |||

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Dudė, U.; Žitkienė, R.; Jurevičienė, D.; Skvarciany, V.; Lapinskaite, I. Evaluation of Outsourcing Development in the Service Sector. Economies 2021, 9, 44. https://doi.org/10.3390/economies9020044

Dudė U, Žitkienė R, Jurevičienė D, Skvarciany V, Lapinskaite I. Evaluation of Outsourcing Development in the Service Sector. Economies. 2021; 9(2):44. https://doi.org/10.3390/economies9020044

Chicago/Turabian StyleDudė, Ugnė, Rima Žitkienė, Daiva Jurevičienė, Viktorija Skvarciany, and Indre Lapinskaite. 2021. "Evaluation of Outsourcing Development in the Service Sector" Economies 9, no. 2: 44. https://doi.org/10.3390/economies9020044

APA StyleDudė, U., Žitkienė, R., Jurevičienė, D., Skvarciany, V., & Lapinskaite, I. (2021). Evaluation of Outsourcing Development in the Service Sector. Economies, 9(2), 44. https://doi.org/10.3390/economies9020044