The study uses descriptive statistics, a method which is suitable for research that attempts to describe events from one point to another, and this method is mostly used in studies that are attempting to understand a certain phenomenon over a certain period of time. This research investigates factors that influence the individual investors’ investment behaviours for mutual fund investments. Factorial information was chosen from past studies to focus this research on investigating the perceptions of the investors’ investment behaviour towards mutual fund investment. A quantitative research method is the widely used approach, and it is a method that uses numerical data as the input for the research, using statistical methods to analyse the data (

Creswell 2009). This study examines the relationship between independent and dependent variables in order to understand the influences of these factors on the investors’ investment behaviours for unit trusts. Therefore, this research is more suited to a quantitative research method, as it could help the study to accurately examine and express the relationship in numerical form for better understanding. The respondents in this study are individual investors aged between 25 to 60 years. The sample size designed for this study is 250 participants. This research uses the non-probability sampling method, which is a convenient sampling technique allowing the researcher to select and choose participants at the best convenience of the researcher. For convenience sampling, a sample size between 200 to 500 respondents is preferred as it would indicate more a reliable sample and prove the validity of the results (

Churchill 1991). The convenience sampling method was used in this study because of the advantages of it being the least expensive and least time-consuming (

Malhotra 2004;

Park and Sullivan 2009;

Sekaran and Bougie 2016). This helps us to reduce the time spent on the selection of participants. Primary data collection is used in this study, and hence the data collection instrument used in this study is a survey questionnaire. The survey questions were adopted from past research studies and consists of close-ended questions which allow the researcher to convert the data into numerical values to apply statistical methods to analyse the data (

Dodge 1985). The survey questionnaire contains two sections. The first section provides the demographic profile which examines the personal backgrounds of participants, such as gender, age, income, occupation, and others. The second section of the survey questionnaire examines the agreement level of respondents toward some aspects as well as the investment behaviour for unit trust investments. A copy of the final questionnaire is appended as

Appendix A. The measurement scale used in this research study is the five Likert scale, and the reason for the use of five Likert scale is that it copes with the adoption of close-ended survey questions, as well as assisting researcher to later convert options into numerical values with SPSS software.

3.1. Data analysis and Findings

There were a total of 250 participants chosen for this research study, and there were sufficient amounts of survey questionnaires distributed to these 250 participants. The survey resulted in a total of 202 responses, indicating a total response rate of 80.8%. The reliability test was performed by using the Cronbach’s Alpha test, and this was to examine the internal consistency among the data collected in this research. In order to determine whether the data are reliable, the results produced from the Cronbach’s Alpha needed to be above 0.7 to show that the data is reliable (

Sekaran and Bougie 2016). There were five variables included in this research, where four are independent variables while one is a dependent variable. Each variable contains an equal number of five items. The Cronbach’s Alpha obtained for variables in terms of financial status, risk taking behaviour, investment revenue, source of investment information, and investment behaviour are 0.709, 0.717, 0.742, 0.773, and 0.739, respectively.

Table 1 provides the results that the measurement variables that are above and higher than 0.7, showing that the data collected in this research are reliable in nature to ensure the reliability of the research findings.

The validity test is to determine whether the instrument obtained the correct answers for the questions. The result of KMO and Barlett’s should be higher or above 0.6 to show that the data collected are valid for the study (

Pallant 2013).

Table 2, presented below, shows the validity test of KMO and Barlett’s for the data collected in this study. The KMO and Barlett’s results obtained for financial status, risk taking behaviour, investment revenue, source of investment information, and investment behaviour are 0.687, 0.792, 0.771, 0.707, and 0.642, respectively, and all are significant as shown in

Table 2. The results obtained are higher than the required 0.6 to show that data collected in this research are valid.

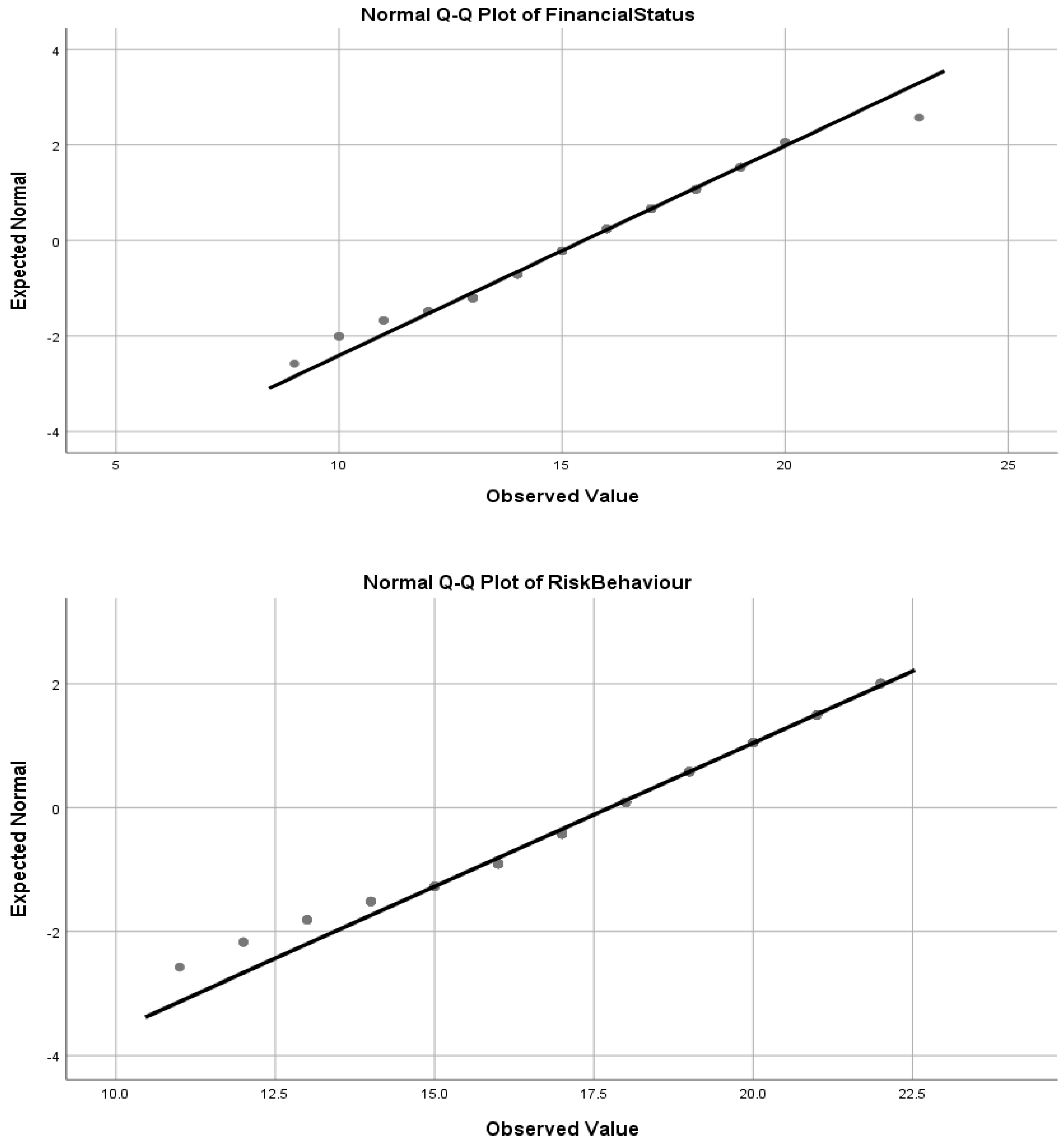

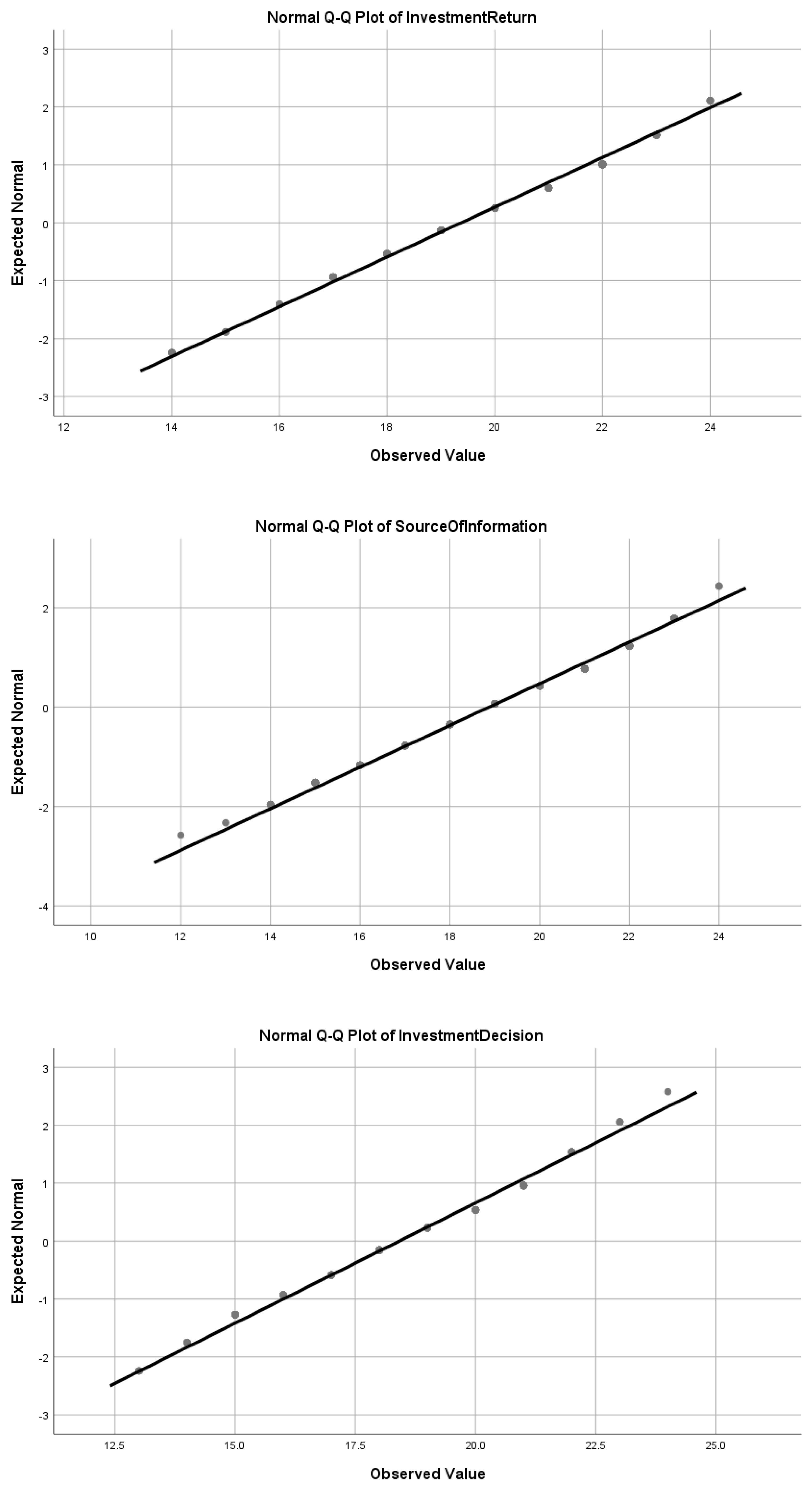

A normality test was conducted to determine whether the data collected are normally distributed or non-normally distributed. Data that are normally distributed indicated that there is consistency of the data collected, and in other words there are minimal amounts of mistakes or errors contained in the data. The Q-Q plot pairs up corresponding quantiles from the samples, and in this case, it is between independent and dependent variables that determine whether the sample data collected are normally distributed by inspecting the scatterplot. If they are normally distributed, the points in the scatterplot should lie close to the line (

Doyle 2010). In order to examine the normality of the data for this study, the graphic method of a normal Q-Q plot was used, and the results are presented in

Figure 2.

Based on the observation of the above normal Q-Q plots, it is observed that data collected under each variable in this study are normally distributed. This was shown on plots in all graphs that they are mostly on the centred line, and plots are closely distributed to the line to show they are normally distributed rather than abnormal distributions. Hence, the data collected in this research are normally distributed to ensure its data quality.

The demographic profile of participants is essentially important for this study. According to

Creswell (

2009), the demographic profile of participants could help a researcher to determine the behaviours and thoughts of participants, and with the linking of the related demographic profile, it helps to explain the behaviours of the participants in their investment behaviour. For instance, income level will determine the risk-taking behaviour of participants. Gender is one of the important aspects to be investigated. Many psychologists have concluded that there are biological differences between male and female in their behaviours, as well as in decision-making processes (

Ngun et al. 2011). The female individuals tend to be picky and they undergo a long decision-making process to make their decisions as they consider various factors to make decisions. Whereas, male individuals tend to be easy going, and spend less time on making decisions, at the same time there are also other factors taken into consideration in arriving at a decision.

Table 3 shows the percentage of male and female participants involved in this study. Male participants in this research account for 43.1%, while female participants are at 56.9%. This was done after studies indicated that females are better at investments compared to males (

Cannivet 2018;

Collinson 2018). Despite, the fact that there are more female participants, the findings of this research could fairly represent the investment behaviours of both gender groups of investors. Age is another important personal feature that needs to be investigated in this study. Age has the tendency to change individuals’ thought and thinking and tends to show different behaviours. The reason for the change in behaviour of individuals at different age levels can be attributed to their knowledge and experiences acquired, and this will eventually lead to variation in behaviour and thinking patterns.

Table 4 shows the distribution of respondents according to their respective age groups.

Table 4 displays the percentage of respondent’s behaviour and thinking pattern of the different age groups. Based on the data, most of the participants are predominantly in the age group of between 41 to 50 years, as they reflect 45.6% of the total participants in this study. This is followed by 37.6% of participants who are between the age of 31 to 40 years; 8.4% of participants are between 21 to 30 years old, 7.4% of participants are between 51 to 60 years old, and only 5% of the participants are above 61 years. This clearly indicated that the findings are representative of investors from all age groups. The status of the individual is also an important aspect in this study, as individuals who are single are less willing to make investment, as they only have sufficient funds for self-spending, and they do not have the affordability to make long-term financial planning. Individuals who are married have strong desires for investment, as they need to make more money with the limited funding in the future to support their realisation of their dreams and raise their children within their living expenses.

For the perspective of the employment status of participants in

Table 5, the majority of participants are employed, and they account for 57.3%. In addition, 20.3% of participants are self-employed which indicates that they are involved in businesses. Four and a half percent of participants are unemployed, while 14.4% of participants are students. Respondents who have retired and housewives are at 3.5%. Therefore, the findings of this study are also representative of participants at different employment status. Educational level refers to the knowledge that the individuals possess at certain level that influences their decisions. Respondents with a higher level of educational backgrounds are able to think logically and able to make informed decisions.

The results presented in

Table 6 show the distribution of respondents’ educational background. Based on the results, 29.7% of participants have graduated from high schools, referring to their highest qualification possessed. In addition, a vast majority of participants at 42.6% have bachelor degrees as their highest qualification. Eight point four percent of participants obtained their masters, while 3.0% of participants received their PhD. Finally, 16.3% of participants have other qualifications, such as professional certificates. Hence, participants involved in this research are well-educated, and this also ensures that the responses provided by participants are reliable.

Income level is the most important aspect in this study, as it reveals the financial status of the individual, and the ability to absorb risks in their investments. Individuals with a high income are able to invest large amounts in investment instruments compared to low income groups, whom are only able to afford low risks.

Table 7 shows the income distribution of participants involved in this research. Thirty-two-point-two percent of the respondents are in the category of earning monthly income of RM8001 to RM10,000. This is followed by respondents earning RM3000 and below comprising 26.7%. 23.8% of the participants receive a monthly income of between RM5001 to RM8000, and only 8.9% of participants are able to make a monthly income of above RM10,001. Nevertheless, all participants in this study are well salaried to support their investment activities.

3.6. Investment Behaviour

Investment behaviour is the process of consideration based on different factors to make the right investment decisions for specific investments. Investment behaviour can be influenced by a wide range of factors and forces, and these factors can be divided into personal characteristics, such as personality, self-motivation, and others. Thus, the behaviour of the investor can also be influenced by external factors and forces such as the general economic environment, stocks past performances, and other related factors.

Table 12 presents the mean scores for items included in the investment behaviour. The mean scores ranged from 3.44 to 3.88 and the mean scores of all the items shows that investors have the positive investment behaviour for unit trust.

Table 13 shows the results of Pearson correlation analysis. It shows that all independent variables have a positive but low level of correlation with the investment behaviours for unit trust.

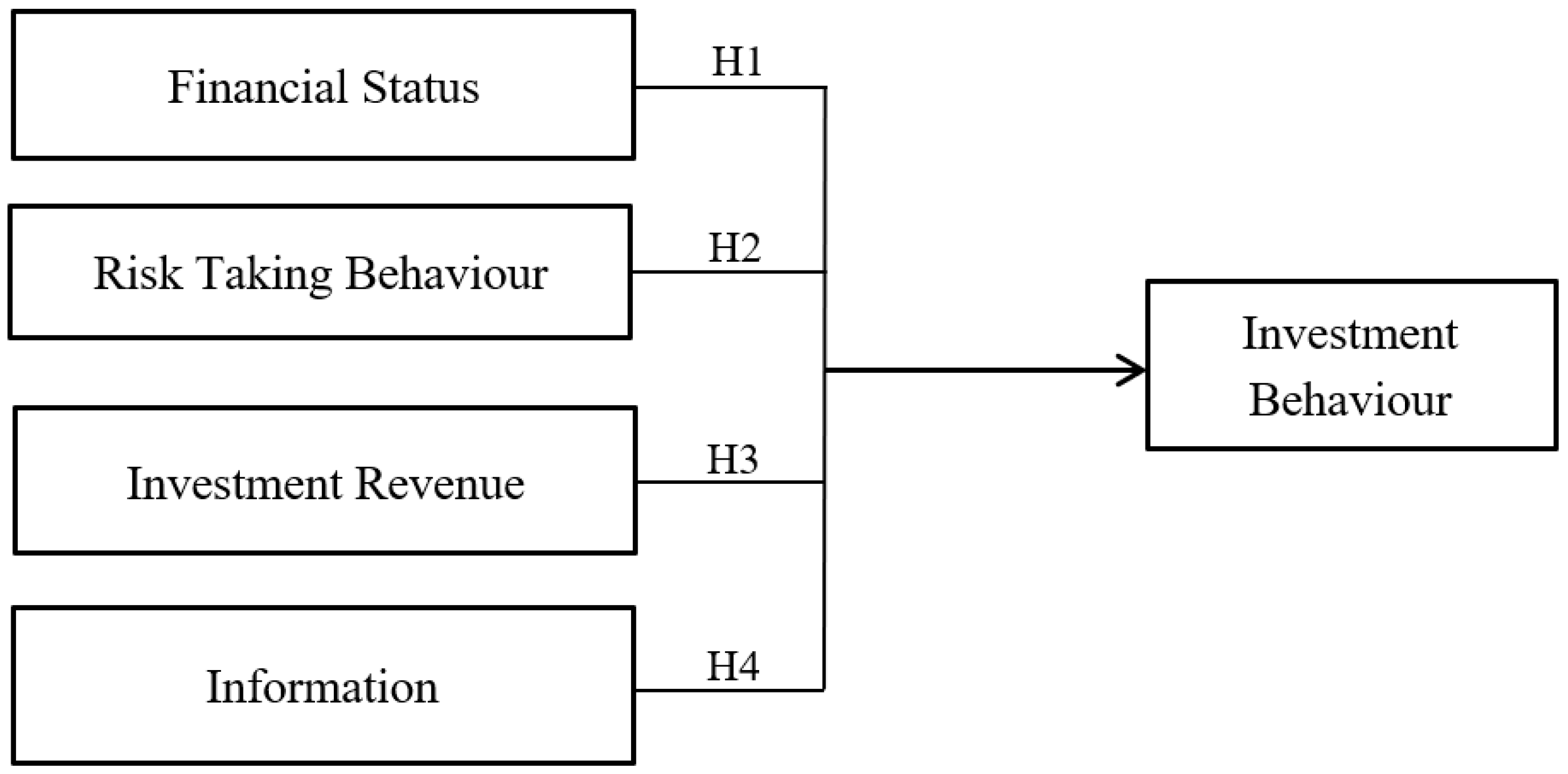

Table 14 shows that all the factors have R values lesser than 0.2 to barely show the significant positive correlation. Multiple regression analysis is also employed in this research. Multiple regression analysis in this research helps to assess whether there exists a statistical relationship between each of these factors and the investors’ investment behaviours for mutual fund. There are two results to be looked at in the multiple regression analysis. First, the R square value shows that the total effects given by independent variables in this research on the dependent variable, and it represents the percentage of change that dependent variable that will be affected. On the other hand, the significance value helps to assess the relationship between each independent variable and dependent variable, to gauge whether there is the statistical relationship in between. When the significance value is less than 0.05, there is the statistical relationship in between or vice versa. Most importantly, the significance value is also used to determine whether the research hypothesis will be accepted or rejected. Risk behaviour has the strongest relationship among all, followed by the source of information, financial status and investment return. Pearson correlation analysis shows that there is a positive relationship between the variables of the study and investment decisions. According to

Table 13 results, financial status and sources of information were found to be significantly related to investment decision. Therefore hypothesis 1 and 4 are accepted in this study.

The R square value shows that the total effects from independent variables of financial status, risk-taking behaviour, source of information, and investment revenue or return on the investment behaviour at 14.4%. This shows the low level of relationship between these factors to the investment behaviours. Looking at the significance value, this shows that investment revenue or return found to have no statistical relationship with the investment behaviour, as the significance value is 0.110 that is higher than 0.05. From

Table 15, it shows that financial status, risk behaviour and source of investment information have significant values of less than 0.05 which explains that they have a statistical relationship with the investment behaviour for unit trusts. However, investment revenue is statistically insignificant based on the results, and therefore, hypothesis three is rejected, while hypothesis one, two, and four are accepted.

{kind=link}

{kind=link}

{kind=link}