1. Introduction

It is well known that the standard deviation is not a good measure of risk because it penalizes upside deviation, as well as downside deviation. Additionally, it is also poor at measuring risk with asymmetric payoff profiles. The poor performance of the standard deviation will lead to poor performance of the Sharpe ratio, which establishes a relationship between the ratio of return versus volatility (

Kapsos et al. (

2014);

Guastaroba et al. (

2016)). A number of studies developed some theories that propose to circumvent the limitations. For example,

Homm and Pigorsch (

2012) develop an economic performance measure based on

Aumann and Serrano’s (

2008) index of riskiness. They prove that the proposed economic performance measure is consistent with first- and second-order stochastic dominance (SD).

Keating and Shadwick (

2002) propose to use the Omega ratio, the probability weighted ratio of gains versus losses to a prospect or the ratio of upside returns (good) relative to downside returns (bad), to replace the Sharpe ratio to measure the risk return performance of a prospect. Thus, the Omega ratio considers all moments, while the Sharpe ratio considers only the first two moments of the return distribution in the construction. According to

Caporin et al. (

2016),

Bellini et al. (

2017) and the references provided therein, the Omega ratios are strongly related to expectiles, which are a type of inverse of the Omega ratio and present interesting properties as risk measures.

Guastaroba et al. (

2016) discuss the advantages of using the Omega ratio further. Thus, the Omega ratio has been commonly used by academics and practitioners as noted by

Kapsos et al. (

2014) and the references therein.

It is well known that the SD theory can be used to examine whether the market is efficient, whether there is any arbitrage opportunity in the market, and whether there is any anomaly in the market (

Sriboonchitta et al. (

2009);

Levy (

2015)), and thus, academics are interested in checking whether there is any relationship between any risk measure with SD. The work from

Darsinos and Satchell (

2004) and others can be used to establish the relationship between the second-order SD (SSD) and the Omega ratio. By using two counterexamples, we first demonstrate that SSD and/or second-order risk-seeking SD (SRSD) alone for any two prospects is not sufficient to imply Omega ratio dominance (OD) and that the Omega ratio of one asset is always greater than that of the other one. We then extend the work of

Darsinos and Satchell (

2004) and others by proving that the preference of SSD (for risk averters) implies the preference of the corresponding Omega ratios are selected only when the return threshold is less than the mean of the higher return asset. On the other hand, the preference of SRSD (for risk seekers) implies the preference of the corresponding Omega ratios only when the return threshold is larger than the mean of the smaller return asset. Lastly, we develop the relationship between the first-order SD (FSD) and the Omega ratio in such a way that the preference of FSD for any investor with increasing utility functions does imply the preference of the corresponding Omega ratios for any return threshold.

Qiao and Wong (

2015) apply SD tests to examine the relationship between property size and property investment in the Hong Kong real estate market. They do not find any FSD relationship in their study.

Tsang et al. (

2016) extend their work to reexamine the relationship between property size and property investment in the same market. They suggest to analyze both rental and total yields and find the FSD relationship of rental yield in adjacent pairings of different housing classes in Hong Kong. Based on their analysis on both rental and total yields, they conclude that investing in a smaller house is better than a bigger house. We note that analyzing both rental and total yields is not sufficient to draw such a conclusion. To circumvent the limitation, we extend their work by applying the Omega ratio to examine the relationship between property size and property investment in the Hong Kong real estate market. In addition to analyzing the rental yield, we recommend analyzing the price yields of different houses. We find that a smaller house dominates a bigger house in terms of rental yield, and there is no dominance between smaller and bigger houses in price yield. Our findings lead us to conclude that regardless of whether the buyers are risk averse or risk seeking, they will not only achieve higher expected utility, but also obtain higher expected wealth when buying smaller properties. This implies that the Hong Kong real estate market is not efficient, and there are expected arbitrage opportunities and anomalies in the Hong Kong real estate market. Our findings are useful for real estate investors in their investment decision making and useful to policy makers in real estate for their policy making to make the real estate market become efficient.

The rest of this paper is organized as follows:

Section 2 presents the formal definitions of the SD rules and Omega ratios. We then show our main results about the consistency of Omega ratios with respect to the SD in

Section 3. In

Section 4, we discuss how to apply the theory developed in this paper to examine whether the market is efficient, whether there is any arbitrage opportunity in the market and whether there is any anomaly in the market. An illustration of the Hong Kong housing market is included in

Section 5. The final section offers our conclusion.

2. Definitions of Stochastic Dominance and

Omega Ratios

We first define cumulative distribution functions (CDFs) for

X and

Y:

We define the second-order integral of

Z,

,

and define the second-order reverse integral,

, of

ZIf

Z is the return, then

is the CDF of the return up to

and

is the second-order integral of

Z up to

, that is the probability of the CDF of the return up to

, and

is the second-order reverse integral of

Z up to

, that is the reverse integration of the reverse CDF of the return up to

. We call

the

i-th-order integral of

Z, which will be used to define the SD theory for risk averters (see, for example,

Quirk and Saposnik (

1962)). On the other hand, we call

the

i-th-order reversed integral, which will be used to define the SD theory for risk seekers (see, for example,

Hammond (

1974)). Risk averters typically have a preference for assets with a lower probability of loss, while risk seekers have a preference for assets with a higher probability of gain. When choosing between two assets

X or

Y, risk averters will compare their corresponding

i-th order SD integrals

and

and choose

X if

is smaller, since it has a lower probability of loss. On the other hand, risk seekers will compare their corresponding

i-th order RSD integrals

and

and choose

X if

is larger since it has a higher probability of gain.

Following the definition of stochastic dominance (

Hanoch and Levy (

1969)), prospect

X first-order stochastically dominates prospect

Y:

which is denoted by

; prospect

X second-order stochastically dominates prospect

Y:

which is denoted by

. Here, FSD and SSD denote first- and second-order stochastic dominance, respectively.

Next, we follow

Levy (

2015) to define risk-seeking stochastic dominance (RSD)

1 for risk seekers. Prospect

X stochastically dominates prospect

Y in the sense of second-order risk seeking:

which is denoted by

. Here, SRSD denotes second-order RSD.

Quirk and Saposnik (

1962),

Hanoch and Levy (

1969),

Levy (

2015) and

Guo and Wong (

2016) have studied various properties of stochastic dominance (for risk averters), while

Hammond (

1974),

Meyer (

1977),

Stoyan and Daley (

1983),

Li and Wong (

1999),

Wong and Li (

1999),

Wong (

2007),

Levy (

2015) and

Guo and Wong (

2016) have developed additional properties of risk-seeking stochastic dominance for risk seekers. One important property for SD is that SSD and SRSD are equivalent to the expected-utility maximization for (second-order) risk-averse and risk-seeking investors, respectively, while FSD is equivalent to the expected-utility/wealth maximization for any investor with increasing utility functions.

We turn to define

as follows:

Here, is called the return threshold. For any investor, returns below (above) her/his return threshold are considered as losses (gains). Thus, the Omega ratio is the probability weighted ratio of gains to losses relative to a return threshold.

We state the following Omega ratio dominance (OD) rule by using the Omega ratio:

Definition 1. For any two prospects X and Y with Omega ratios, and , respectively, X is said to dominate Y by the Omega ratio or X is said to Omega ratio dominate Y, denote by: 3. Consistency Results

We will use the term “theorem” to state new results obtained in this paper and “proposition” to state some well-known results. Some academics may believe that the SSD is consistent with the Omega ratio because they assert the following:

where

is the Omega ratio for

X defined in (

7) or (

8). The above assertion is in

Darsinos and Satchell (

2004) and others. We first establish the following property to state that the argument in (

10) may not be correct:

Property 1. SSD alone is not sufficient to imply for any η.

Property 1 implies that the assertion made by

Darsinos and Satchell (

2004) and others may not be always correct. We construct the following example to support the argument stated in Property 1.

Example 1. Consider two prospects X and Y having the following distributions:Then, we get and and obtain the following:It follows that for all . That is, . However, for any , we have . Recalling the definition of , we can conclude that for any , and thus, the statement “ for any η” does not hold. To complement Property 1, we establish the following property:

Property 2. SRSD alone is not sufficient to imply for any η.

We construct the following example to support the argument stated in Property 2.

Example 2. Consider two prospects X and Y as follows:We have and and obtain the following:It follows that for all . This concludes that . However, for , we can get:That is, . In fact, for any , we have , and thus, the statement “ for any η” does not hold. Properties 1 and 2 tell us that SSD and SRSD alone are not sufficient to imply

for any

. Then, one may ask: what is the relationship between

and

when there is SSD or SRSD?

Guo et al. (

2016) and

Balder and Schweizer (

2017) provide an answer. In this paper, we restate their result to extend the work by

Darsinos and Satchell (

2004) and others by first deriving the relationship between SSD (for risk averters) and the Omega ratio:

Proposition 1. For any two returns X and Y with means and and Omega ratios and , respectively, if , then for any .

In addition, we also study the relationship of second-order risk-seeking stochastic dominance and the corresponding Omega ratios. A dual result as stated in Theorem 1 is obtained. Finally, the relationship between first-order stochastic dominance and the Omega ratios is established in Corollary 2. Some simple examples (Examples 1 and 2) are presented to show that SSD or SRSD alone are not sufficient to imply for any .

Here, we provide a short proof

2 as follows: although it is true that if

, then

for any

. However, the sign of

and

can be negative. To be precise, for

,

. In this situation, we can get:

Furthermore, we note that:

Consequently, we cannot determine the sign of

Thus, we cannot determine the sign of

. However, for any

, we can have

, and thus, we have:

This implies that , and thus, the assertion of Proposition 1 holds. ☐

In the proof of Proposition 1, one could conclude that if

, then

for any

. However, for

, we cannot determine which one is larger if we are using SSD. However, one could consider employing the SD (RSD) theory for risk seeking (refer to Equation (

6)) in the study. By doing so, we establish the following theorem to state the relationship between the SRSD and Omega ratio:

Theorem 1. For any two returns X and Y with means and and Omega ratios and , respectively, if , then for any .

Here, we give a short proof as follows: assume that

. This is equivalent to

. Recall that

. This yields the following equation:

Further, we note that

implies

. Thus, for

, we obtain:

In other words, we can get

for any

, and thus, the assertion of Theorem 1 holds. ☐

We note that

Darsinos and Satchell (

2004) assert that SSD is consistent with the Omega ratio; that is, the relationship in Equation (

10) holds. However, we find that the consistency of SSD and the Omega ratio holds only when we restrict the range of return threshold, as stated in our Proposition 1 and Theorem 1. From Proposition 1 and Theorem 1, one could then derive the following theorem to state the relationship between the FSD and Omega ratio:

Theorem 2. If the SSD and SRSD hold, then the Omega ratio dominance also holds. In particular, this is the case when the FSD holds.

We give a short proof as follows: if

, by using the hierarchy property (

Levy (

1992,

1998,

2015);

Sriboonchitta et al. (

2009)), we obtain both

and

. From Proposition 1 and Theorem 1, we have

for any

and

. Since

, we have

for any

, and thus, the assertion of Theorem 2 holds. ☐

5. Illustration

Investment in property is important in both consumption and investment decisions (

Henderson and Ioannides (

1987)).

Ziering and McIntosh (

2000) argue that housing size is important in determining the risk and return of housing and conclude that the largest class of housing provides investors with the highest return and the greatest volatility. However,

Flavin and Nakagawa (

2008) document that investing in larger houses does not reduce risk, while

Kallberg et al. (

1996) show that smaller property offers impactful diversification benefits for investment portfolios with high return aspirations. On the other hand,

Cannon et al. (

2006) explain housing returns by volatility, price level and stock-market risk, and

Ghent and Owyang (

2010) investigate supply and demand to explain movements in the housing market.

The housing market in Hong Kong plays a very important role in the Hong Kong economy (

Haila (

2000)), and Hong Kong is one of the most expensive housing markets in the world in terms of both prices and rents (

Tsang et al. (

2016)).

Qiao and Wong (

2015) apply SD tests to examine the relationship between property size and property investment in the Hong Kong real estate market. They do not find any FSD relationship in their study.

Tsang et al. (

2016) extend their work to reexamine the relationship between property size and property investment in the same market and find the FSD relationship in rental yield in any adjacent pairing of the five well-defined housing classes in Hong Kong. In empirical studies, very few studies could discover the existence of any FSD relationship, and it is very important to obtain the FSD relationship (if there is any) because this information is very helpful to investors. For example, the findings from

Tsang et al. (

2016) imply that by shifting investing from the largest class of housing to the smallest class of housing, investors could obtain higher expected utility, as well as higher expected wealth from rental income.

In this paper, we extend their work by applying the Omega ratio to examine the relationship between property size and property investment in the Hong Kong real estate market. We recommend that analysts apply the Omega ratio to examine whether there is any FSD relationship between any pair of variables being studied because it is easier to obtain the Omega ratio. The Omega ratio could serve as a complementary tool for the FSD test, and thus, we recommend that analysts use both the Omega ratio and FSD test in their analysis. The existence of dominance from both the Omega ratio and FSD test could assert the existence of the FSD relationship between the variables being examined. In addition, our illustration could also serve our purpose to demonstrate whether the theory developed in this paper holds true.

In order to readdress the issue studied by

Tsang et al. (

2016), we first use the same rental yield data used in

Tsang et al. (

2016) to compare monthly property-market rental yields in private domestic units of five different housing classes from January 1999–December 2013 in Hong Kong. The data are obtained from the Rating and Valuation Department of the Hong Kong SAR. The monthly rental yields for each class are calculated by dividing the average rent within the class by the average sale price for houses in the class for that month. Private domestic units are defined as independent dwellings with separate cooking facilities and bathrooms (and/or lavatories). They are sub-divided into five classes by reference to floor area: Class A salable area less than 40 m

; Class B salable area of 40–69.9 m

; Class C salable area of 70–99.9 m

; Class D salable area of 100–159.9 m

; and Class E salable area of 160 m

or above.

To analyze the rental yield and to illustrate Theorem 2, we set

A = rental yield of Class A and

E = rental yield of Class E and present the summary statistics of the rental yields for Classes

A and

E in

Table 1.

We first test the following hypotheses:

for rental yield. The result of the

t-test in

Table 1 concludes that the mean rental yield of

A is significantly higher than that of

E. Thereafter, we test the following hypotheses:

for rental yield. The result of the

F-test in

Table 1 does not reject that the variances of the rental yields of both

A and

E are the same. Applying the mean-variance rule for risk averters

Markowitz (

1952) that

A is better than

E if

,

and there is at least one strictly inequality, we conclude that risk averters prefer Property

A to Property

E based on rental yield. On the other hand, if we apply the mean-variance rule for risk seekers (

Wong (

2006,

2007);

Guo et al. (

2017)) that

A is better than

E provided that

,

and there is at least one strict inequality, we conclude that risk seekers prefer Property

A to Property

E based on rental yield under the condition that

A and

E belong to the same location-scale family or the same linear combination of location-scale families

Wong (

2006,

2007). Nonetheless, this conclusion cannot imply the existence of the first-order SD relationship between Properties

A and

E based on rental yield if

A and

E do not belong to the same location-scale family or the same linear combination of location-scale families. To circumvent the limitation, this paper recommends that academics and practitioners use the Omega ratio rule as discussed in this paper. Thus, we turn to applying the Omega ratio rule to analyze whether there is any first-order SD relationship between Properties

A and

E based on rental yield.

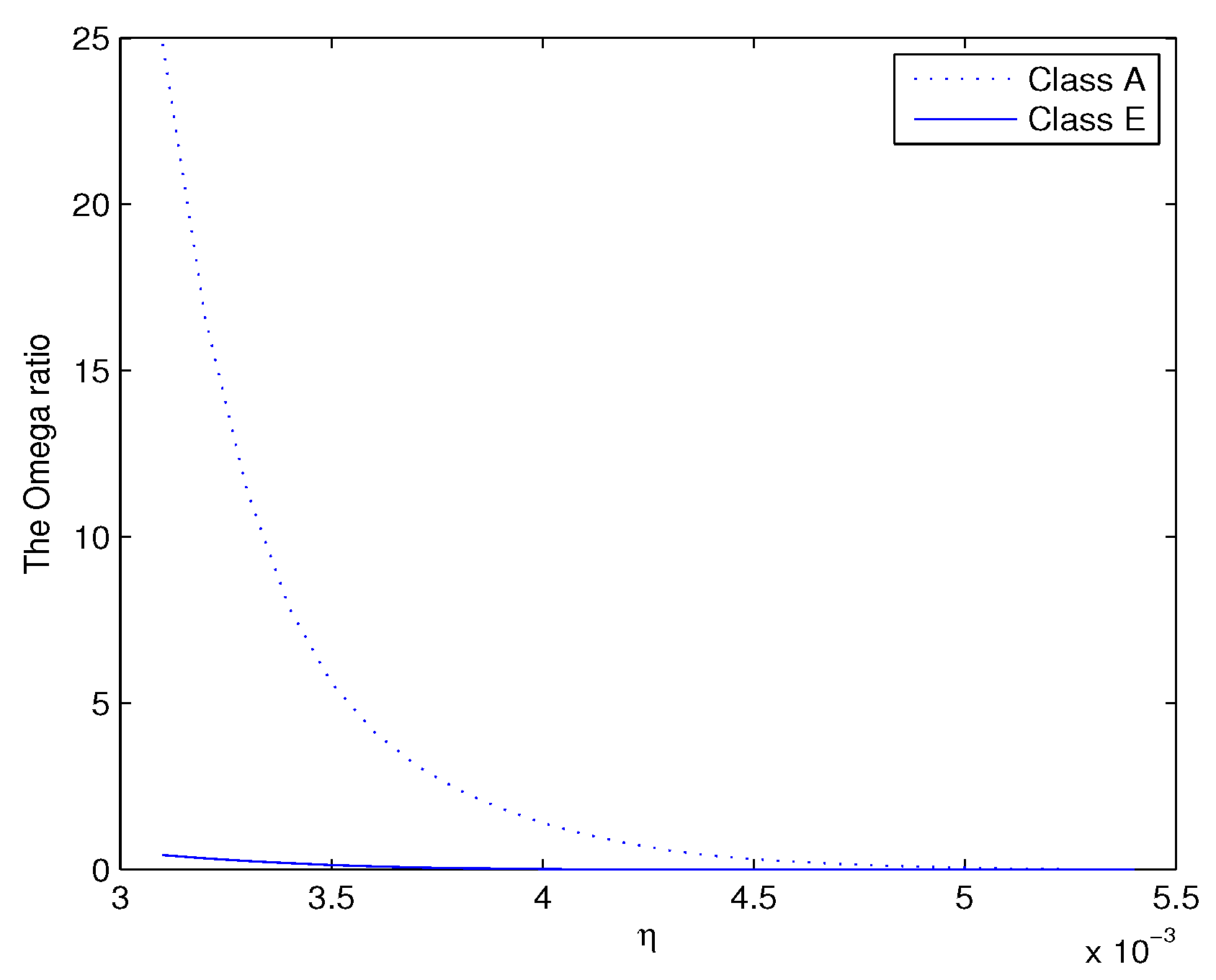

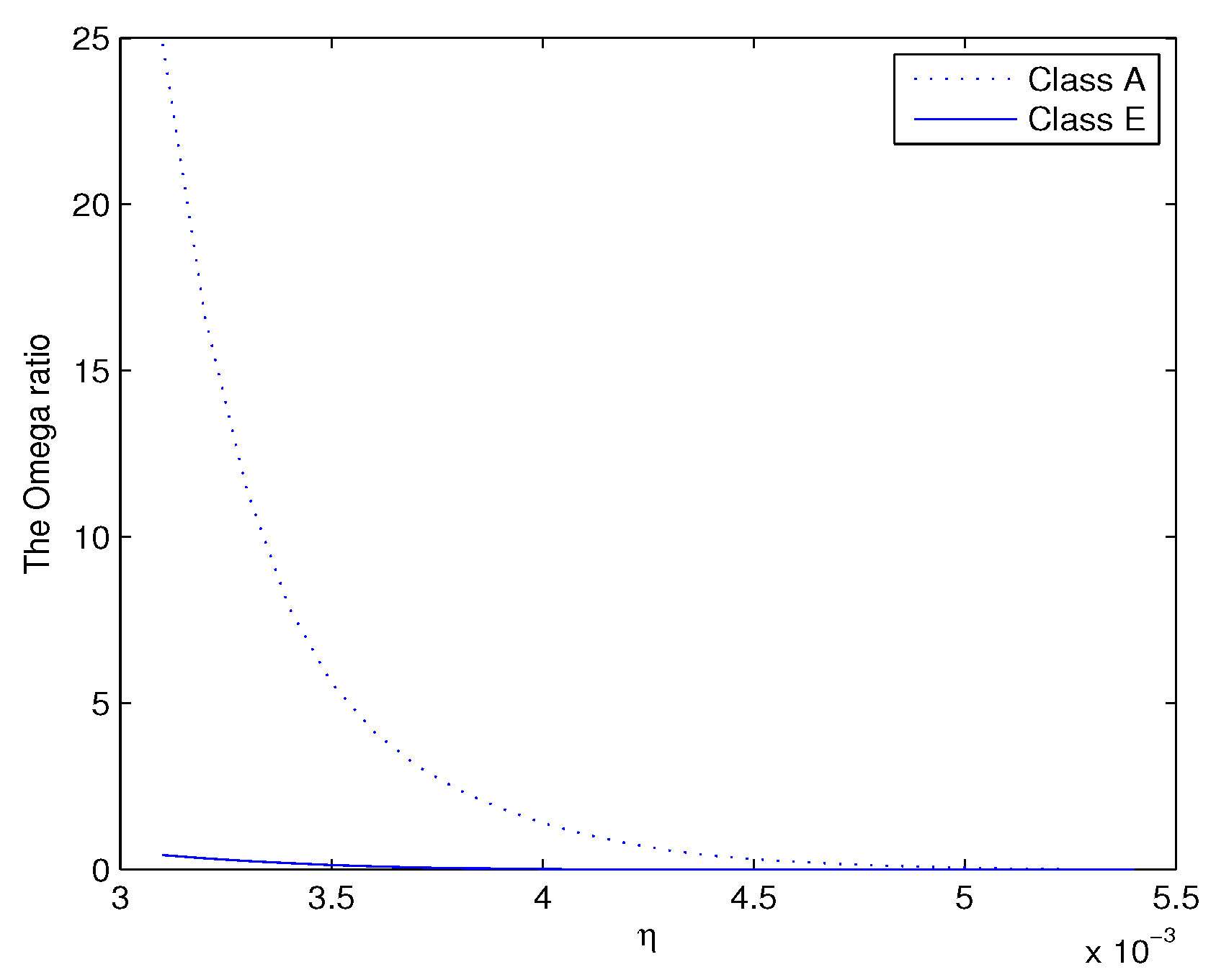

We note that for the existence of the Omega ratio, we need

with

. To satisfy this condition, we choose

. In addition, the term

should not be too small. If not, the Omega ratios will be very large. Thus, in this illustration, we set

. Furthermore, for

, we have

. Thus, we set the upper-bound for

as

. We exhibit the plot in

Figure 1.

From the figure, it is clear that

for any

. We skip displaying plots of other pairs of variables because all the plots draw the same conclusion. We find that Class A dominates Classes B, C, D and E, Class B dominates Classes C, D and E, Class C dominates Classes D and E and Class D dominates Class E, by using the Omega ratio rule. We summarize the results of the Omega ratio dominance in

Table 2. The results in the table are read based on row versus column. For example, the cell in Row A and Column B tells us that Class A dominates Class B by the Omega ratio and is denoted by OD, while the cell in Row B and Column A means that Class B does not dominate Class A by the Omega ratio, as denoted by ND.

To check whether a smaller house (any house in the group with the smaller size) is better than a bigger house (any house in the group with the bigger size), only comparing their rental yields is not good enough.

Tsang et al. (

2016) suggest analyzing both rental and total yields. Based on their analysis on both rental and total yields, they conclude that investing in a smaller house is better than a bigger house. We note that analyzing both rental and total yields is not sufficient to draw such a conclusion. We explain the reasons as follows:

Tsang et al. (

2016) find that (a) the smaller house dominates the bigger house in terms of rental yield, and (c) there is no dominance between the smaller and bigger houses in total yield where total yield = rental yield + price yield. Under (a) and (c), it is possible that (b’) the bigger house dominates the smaller house in terms of the price yield, and thus, under (a), (b’) and (c), we cannot conclude that the smaller house is a better investment than the bigger house. To circumvent the limitation, in addition to analyzing the rental yield, we recommend analyzing the price yield as follows: We set

A = price yield of Class A and

E = price yield of Class E and present the summary statistics of the price yields for Classes

A and

E in

Table 3.

We first test the null hypothesis

that

versus the alternative hypothesis

that

as shown in (

17) for the price yield. The result of the

t-test in

Table 3 does not reject that the mean price yields for

A and

E are the same. Thereafter, we test the null hypothesis

that

versus the alternative hypothesis

that

as shown in (

18) for the price yield. The result of the

F-test in

Table 3 concludes that the variance of the price yield of

A is significantly smaller that that of

E. Thus, applying the mean-variance rules, we can conclude that risk averters prefer to invest in

A rather than

E, but risk seekers are indifferent between

A and

E. Nonetheless, this conclusion cannot imply any first-order SD relationship between Properties

A and

E based on the price yield. In this paper, we recommend that academics and practitioners use the Omega ratio rule as discussed in this paper.

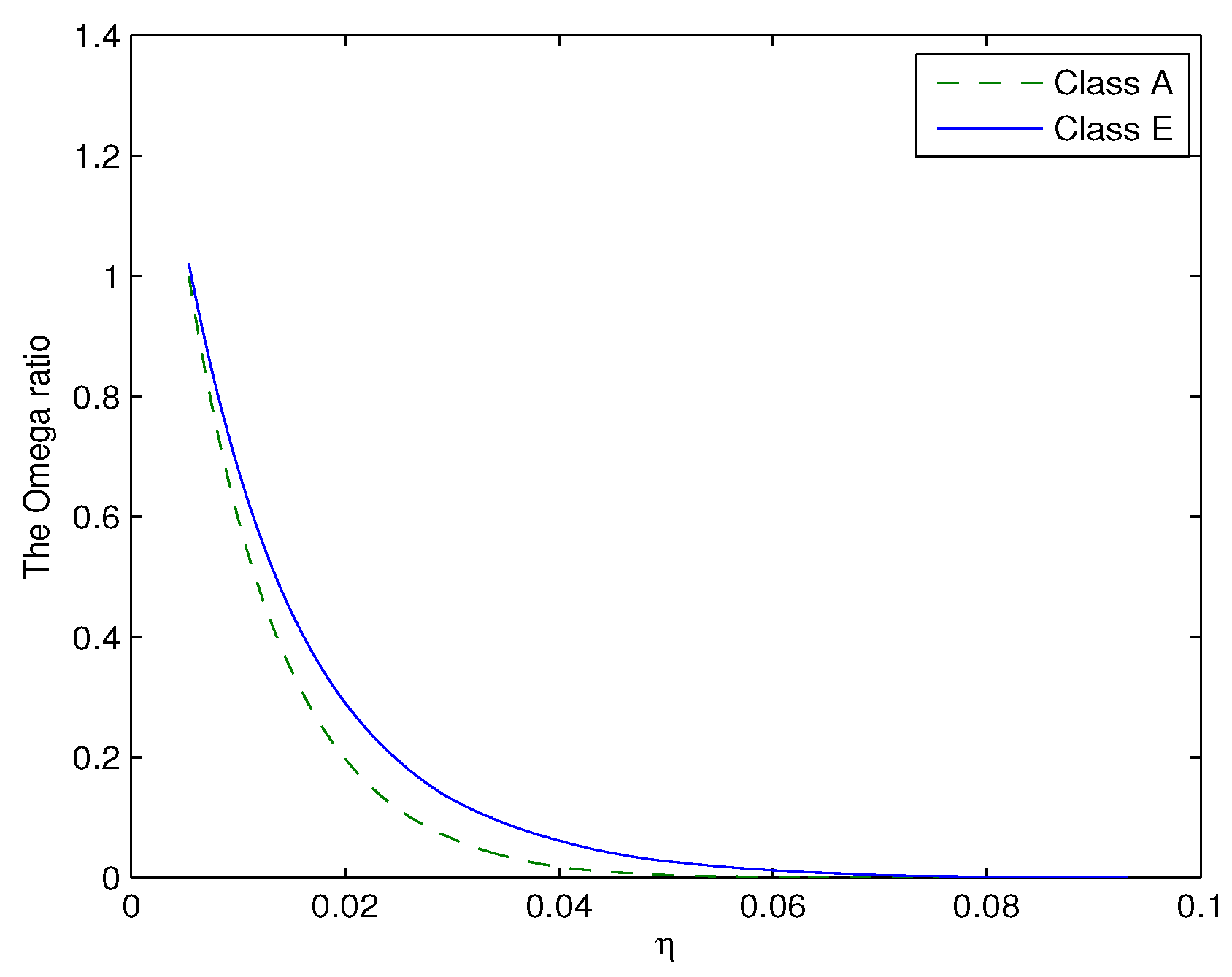

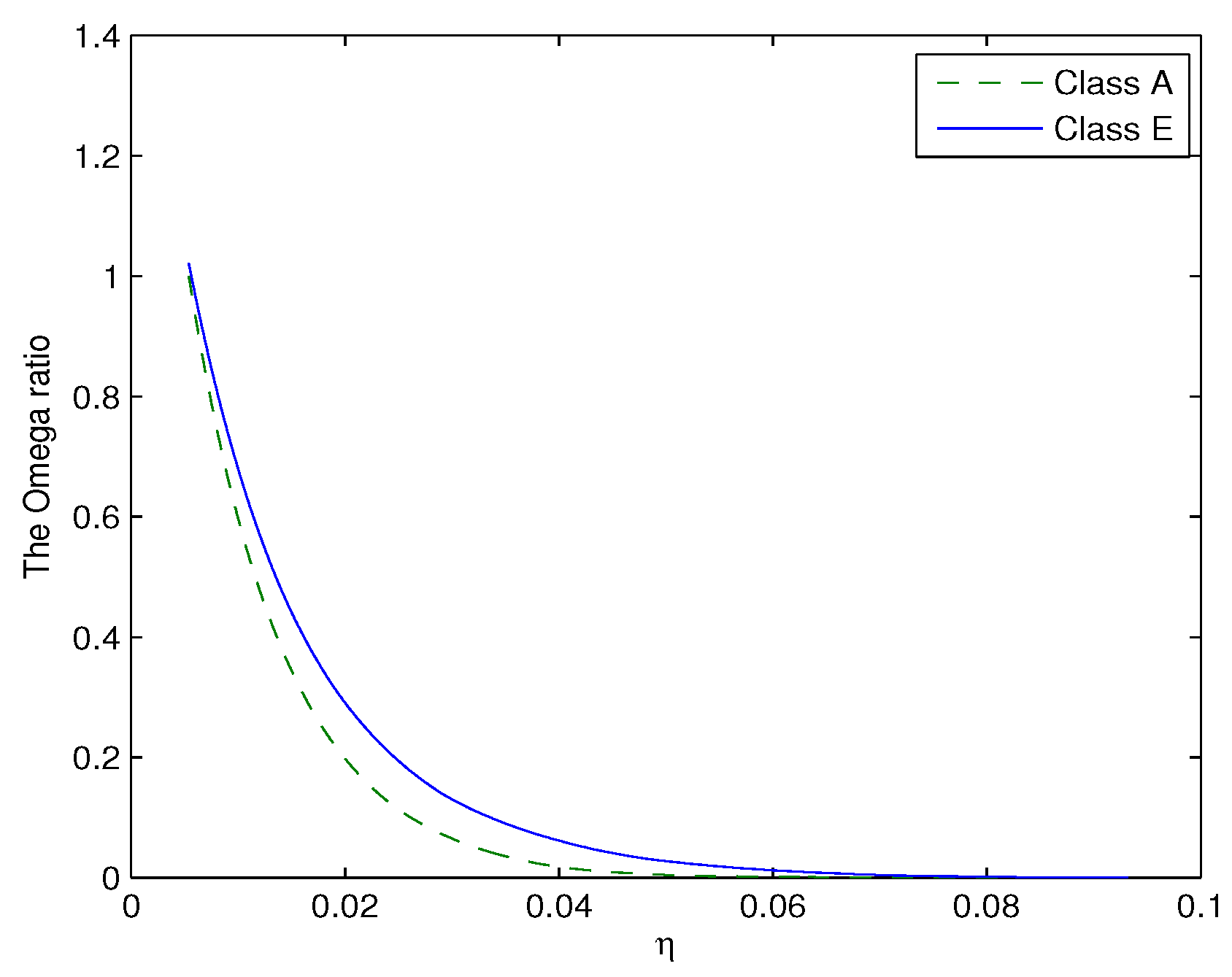

Continuing with our analysis in the rental yield, we find that when

,

is smaller than

, while when

,

is larger. Thus, there is no OD relationship between

A and

E. To illustrate our results empirically, we set

. The related results are exhibited in

Figure 2. From this figure, it is clear that the Omega ratio of Class E is larger than that of Class A. For the Omega ratio dominance, different from the analysis for the rent yields, there is no dominance relationship between A and E in terms of the price yield by using the Omega ratio, and thus, we conclude that there is no FSD relationship between A and E in terms of the price yield.

Tsang et al. (

2016) find that Class A SSD dominates Class E in terms of total yield. We conduct the Omega ratio test analysis for this issue. Our findings are consistent with

Tsang et al. (

2016). Since using both rental yield and price yield could draw the conclusion that investing in the smaller house is better than the bigger house, we skip reporting the OD results for the total yield.

Recall that

Tsang et al. (

2016) have shown that (a) the smaller house dominates the bigger house in terms of rental yield and (c) there is no dominance between smaller and bigger houses in total yield. Under (a) and (c), it is possible that (b’) the bigger house dominates the smaller house in terms of the price yield.

In this paper, we find that (a) the smaller house dominates the bigger house in terms of rental yield, and (b) there is no dominance between smaller and bigger houses in price yield. We note that total yield = rental yield + price yield. Findings (a) and (b) can get either (c) that the smaller house dominates the bigger house in terms of total yield or (c’) there is no dominance between smaller and bigger houses in terms of the total yield. No matter under (a), (b) and (c) or under (a), (b) and (c’) (actually, we find (c’) in our paper), we conclude that regardless of whether the buyers are risk averse or risk seeking, they will not only achieve higher expected utility, but also obtain higher expected wealth when buying smaller properties. This implies that the Hong Kong real estate market is not efficient, and there are expected arbitrage opportunities and anomalies in the Hong Kong real estate market. Our findings are useful for real estate investors and policy makers in real estate for their policy making to make the real estate market become efficient.

Last, we note that though our paper finds that there exists “expected arbitrage opportunity” in the Hong Kong real estate market, however, it is very difficult, if not impossible, to short sell a property in Hong Kong. Thus, it is not easy to explore this “expected arbitrage opportunity”. Nonetheless, if an investor would like to buy a big house to stay in Hong Kong and sell it a couple years later, then, she/he may consider buying a few smaller houses with the same amount of funds in total, rent out all the smaller houses she/he bought, rent a bigger house for her/him to stay and sell all the properties she/he bought as her/his plan a couple of years later. In this way, she/he will get positive net rental income each month (since the rental yield of the smaller house OD dominates that of the bigger house), while the price yield has no difference when she/he sells the big house or the small houses (since there is OD dominance between smaller and bigger houses in terms of price yield). Thus, when she/he sells all her/his properties, she/he still gets net profit by the rental rental if she/he chooses to buy small houses.

{kind=link}

{kind=link}