Abstract

This study analyzes how sectoral stock volatility in the GCC region responds to global financial uncertainty shocks originating from the U.S. (CBOE VIX), Europe (VSTOXX-50), Bitcoin investors’ Sentiment Indices (BSI), and disaggregated global Financial Stress Indicators (FSI) by using both the “Frequency” and “Time” domain TVP-VAR based connectivity approaches. The “Time” and “Frequency” domain TVP-VAR results indicate that the Energy, Financials, Materials and REIT sectors experience the highest shock spillover from the U.S. and European equity market uncertainty (VIX and VSTOXX-50) for the overall and long-term investment horizons. Whereas, all the five disaggregated global financial stress indicators and BSI transmit higher shocks spillovers towards the sectoral stock conditional volatility of Energy and Materials sectors for the overall and long-term investment horizons. Furthermore, the “Frequency” domain TVP-VAR approach shows that overall shocks spillovers are higher in long-term and intensified during the COVID-19 period. The Energy, Materials, and REIT sectors’ high sensitivity to U.S.VIX and Euro.VSTOXX-50 shocks calls for sector-specific hedging—such as sectors remain least susceptibility to long-term U.S. and European equity risk shocks such as Utility. Over the long-term and overall investment horizons, the Energy and Material sectors’ position as the main shock recipient from all five global financial stress components and the BSI underscores its role as a volatility hub. Policymakers should enforce stress tests and capital buffers for energy and material focused firms, while proactive liquidity management and commodity hedging are vital during global financial stress and BSI spikes to limit funding and operational risks.

1. Introduction

The GCC financial systems experienced spillover effects during the 2008 global downturn despite limited exposure to subprime mortgages (Espinoza et al., 2013). B. Chen and Sun (2024) also classified that optimal portfolio divarication by including asset classes with imperfect correlation characteristics can improve portfolio optimization. The global credit market disruptions and funding restrictions also lead towards the financial asset devaluation and cause financial structural imbalances within the GCC financial system. Furthermore, GCC financial system is also exposed to the spillover of shocks from the U.S. and European financial systems because of the increased emerging economies’ financial integration with the developed financial systems The spread of contagion has intensified due to financial globalization. The domestic macroeconomic and financial variables, including trade and policy issues, influence the volatility of external shocks in developing countries (Shi & Wang, 2023). Through capital flows, financial openness can intensify these shocks. For example, Endri et al. (2024) discovered that, with the exception of China, Indonesia’s equities market had good short-term integration but weak long-term integration with significant partners. Oil volatility, geopolitical risk, trade policy uncertainty, and oil shock decomposition have been the primary subjects of research on GCC financial systems. External factors such as global Financial Stress Indicators (FSI), Bitcoin sentiment (BSI), European uncertainty (VSTOXX-50), and U.S. market uncertainty (VIX) have received less attention.

The stronger worldwide financial integration makes a persuasively strong motivation factor to explore the shock propagation from European and U.S. implied stock volatility (VSTOXX-50 and VIX) in both the temporal and frequency domains. Cross-border market turbulence swiftly erodes investor sentiment, slows growth, and erodes resilience. About 20% of worldwide output, energy consumption, and foreign investment, 10% of commerce, and one-third of international stock capitalization are all attributed to the United States. Likewise, the EU-GCC cooperation accounts for more than 50% of worldwide foreign direct investment, 17.5% of global commerce, and 20% of global GDP (European Commission, 2022). In 2024, the EU was the second-biggest trading accomplice of the GCC, accounting for 7.9% of GCC exports, 15.7% of imports, and 11.7% of goods trade (European Commission, 2025). With the help of €180 billion in EU investment stock, commerce reached €174 billion two years prior (European Union External Action Service, 2021). The volatility spillovers across border are further amplified within the EU by close trade, capital, and inflation ties (Baele, 2005).

One of the motivational factor for exploring the shock transmission from the global Financial Stress Indicators (FSI) towards the GCC sectoral stock volatility lies in the fact that credit constraints increase borrowing expenses, limit financing, and increase default risks, which exacerbate macroeconomic instability and worse stock performance (Gilchrist et al., 2009). Investors demand greater risk premiums and move to safer assets during times of stress, which lowers liquidity and stock prices (Tronzano, 2020). Lack of funding restricts company operations, exacerbates shocks to commodity prices, particularly in metals, and reduces profitability. Clustering of volatility exacerbates uncertainty, depresses mood, and puts pressure on stock prices. The GCC is still quite vulnerable to global financial crisis because of its reliance on hydrocarbons and fixed currency rates.

The motivational factor for exploring the shock absorption capability of GCC sectoral stock volatility from the Bitcoin investors’ fear and greed sentiment indices (BSI) is the region’s increasing interest in digital assets. The first cryptocurrency was authorized by Bahrain’s Sharia Review Board in 2021, and Ripple teamed up with Saudi Arabia’s National Commercial Bank to provide blockchain-based remittances. Bitcoin was considered possibly acceptable as “customary currency” in early discussions about Islamic banking (Mensi et al., 2020). Investors in the UAE made around $200 million from cryptocurrencies in 2023, which reflects this acceptability (Bandyopadhyay, 2024). While Bahrain’s central bank extended its 2019 digital asset laws by piloting JPMorgan’s block chain, Oman recognized Bitcoin under Islamic law and started $1.1 billion in mining activities to enhance variety (Zupan, 2021). Gambling, alcohol, and tobacco are among the prohibited businesses that cannot be included in investments in Islamic finance (Hasan et al., 2021). Similar to this, using cryptocurrencies is permissible as long as it is morally upright and devoid of fraud or speculation. Thus, this study investigates the relationship between volatility in GCC Islamic equities sectors and investor emotion toward Bitcoin, namely fear (loss aversion) and greed (profit-seeking). By making three original contributions to the body of existing literature, the current study enhances academic debate.

Firstly, previous research has mainly analyzed the predictive power of investor sentiment—such as cryptocurrency fear and greed indices—for forecasting crypto prices (Güler, 2023). Bouteska et al. (2022) showed that adding sentiment measures enhances return forecast accuracy. Ali et al. (2024) examined Sharia-compliant Bitcoin–equity links, while W. M. A. Ahmed (2021a) analyzed Bitcoin’s asymmetric volatility relative to Islamic stocks. Other works explored return interconnectedness between Bitcoin and developed markets like the U.S. (Nguyen, 2022) and G7 (L. Xu & Kinkyo, 2023). However, no study has yet assessed how Bitcoin investor fear (selling pressure) and greed (buying optimism) sentiment shocks transmit to GCC sectoral stock volatility across overall, short-, and long-term horizons.

Secondly, existing research mainly explores how shocks from U.S. economic conditions (Smales, 2020), trade policies, and climate policy uncertainties (Tedeschi et al., 2024) affect developed markets, with limited focus on how U.S. (VIX) and European (VSTOXX-50) uncertainties influence GCC sectoral volatility. Prior studies examined volatility transmission among the equity returns of U.S. and China (B. Chen & Sun, 2024), G20 (Naeem et al., 2024), and G7 (Lang et al., 2024), finding stronger interconnectedness during crises such as COVID-19, Brexit, and recessions. More recent work has addressed country-specific contexts for equity market shock transmission—e.g., Shen et al. (2022) on Chinese sectors and Iqbal et al. (2022) on European markets, showing how asset allocation can adjust to transmission patterns. Extending this logic, if U.S. or European instability disproportionately impacts certain GCC sectors, investors could mitigate risk through portfolio reallocation. However, no study has yet examined how shocks from the U.S. VIX and VSTOXX-50 transmit to GCC sectoral stock volatility across different frequency bands.

Thirdly, this study is the first to analyze how shocks from disaggregated global Financial Stress Indicators (FSI)—including “Credit” disruptions, “Equity Valuation,” “Funding” constraints, shifts to “Safe Assets,” and “Volatility” in global commodity, stock, and forex markets—affect GCC sectoral stock volatility. It employs a Time- and Frequency-domain TVP-VAR connectedness framework (Antonakakis et al., 2020; Chatziantoniou et al., 2023) to assess shock transmission across short-, medium-, and long-term horizons. Previous research has mainly used aggregated FSI to study spillovers in U.S., European, and developed markets (see Lang et al., 2024; He et al., 2021). An exception, Cipollini and Mikaliunaite (2020) examined European FSI and macroeconomic uncertainty but not sectoral effects in the GCC. No prior study has explored how disaggregated FSI shape GCC volatility. Stronger FSI spillovers can erode investor confidence, shift sentiment, and influence trading and investment strategies. The findings offer policymakers insights to anticipate and mitigate external shocks, supporting fiscal and monetary stability during global stress.

The remainder of the paper is organized as follows. Section 2 reviews the literature and theoretical background. Section 3 describes the data and methodology. Section 4 presents the results and their economic implications. Robustness checks and sensitivity analyses are conducted in Section 5. Section 6 discusses the findings in light of theoretical rationality and practical implications. Finally, Section 7 concludes the paper, highlighting limitations and suggesting directions for future research.

2. Literature Review and Economic Rationality

The literature review provides a theoretical framework for investigating the interactions between conditional volatility in GCC equities and disaggregated financial stress indicators (FSI), Bitcoin sentiment indices (BSI), and implied volatility measures from the U.S. (VIX) and Euro (VSTOXX-50) equity markets. It also summarizes earlier empirical studies to draw attention towards the research gaps.

2.1. The Spillover of Shock Propagation Towards the GCC Sectoral Stock Conditional Volatility from Global Financial Stress Indicators (FSI)1

Taking insights from the contagion theoretical perspective, investors’ willingness to invest in “safe heaven” asset classes due to the “flight-to-quality” phenomenon explains the excessive shock transmission from the U.S. and European financial uncertainty towards the GCC financial system. Investors’ sentiments played a contributory factor in transmitting the uncertainty shocks from U.S. and European financial markets. With the increase in risk premium in the developed financial systems, investors become more willing to invest in safe-haven financial asset classes and disinvesting in riskier financial asset classes of the emerging economies. Therefore, behavioral financial perspective and “guilt by association bias” also stated that investors during the financial recession extrapolate bearish conditions in the developed financial systems to all other emerging financial markets and because of this generalization, the volatility shock spillovers towards the emerging financial system increases. Therefore, building upon the capital shift amid financial recession and volatility shock transmission mechanism, GCC sectoral stock conditional volatility series experienced heightened shocks from FSI.

The liquidity constraints and margin calls are generally due to the increased financial stress in developed financial systems, whereas institutional investors take into account the short-term positioning in unconnected and uncorrelated asset classes. Even in markets that were not immediately impacted by the initial shock, such forced reductions in leverage result in synchronized increases in unpredictability throughout financial systems (Rösch & Kaserer, 2013). This is conceptually consistent with the liquidity spiral model proposed by Brunnermeier and Pedersen (2009), which holds that systemic instability and broad asset sell-offs result from funding limitations exacerbated by drops in market liquidity. Therefore, investors’ inability and unwillingness to hold risky asset classes, funding constraints, illiquidity and credit market disruptions in the wake of economic crisis lead towards the higher shock transmission towards the conditional volatility of the GCC sectoral stock returns.

The combined impact of commodity price volatility and financial market fragility, which both heighten investor reluctance and speculative behavior, results in a higher transmission of shocks from global financial stress indicators (FSI) to GCC sectoral stocks (Bouri et al., 2023). Resource-dependent industries are disproportionately impacted by global energy market instability, which is caused by shifts in demand-supply dynamics and general macroeconomic uncertainty (Bakas & Triantafyllou, 2020). Through portfolio reallocations and the increasing financialization of the energy industry, elevated financial stress exacerbates the volatility of commodities prices. Due to the GCC economies’ reliance on hydrocarbon exports, negative shocks intensify changes in the price of gas and oil, reducing sectoral competitiveness and causing instability in non-energy sectors. Increased global stress usually makes people less willing to take risks, which leads them to move away from developing financial markets’ stocks and into safe-haven investments. Additionally, hedging strategies, restrictions on cross-border capital flows, and reduced market liquidity can all contribute to these dynamics (Cavallaro & Cutrini, 2019). Unfavorable international circumstances can lead to capital outflows, reduced holdings, and local equities sell-offs, all of which exacerbate market volatility (Pavabutr & Yan, 2007). Reduced foreign inflows and liquidity constraints hence cause equity market devaluation and conditional volatility to rise in GCC markets during times of global financial crisis.

The majority of the existing literature focuses on economies outside of the GCC region and considers how shocks are transmitted from aggregated financial stress indices to financial asset classes (C. Liang et al., 2023; Apostolakis et al., 2021a; Hoque et al., 2024; Ilesanmi & Tewari, 2020; Y. Xu et al., 2023; Y. Liu & Wang, 2024). Such an approach, however, ignores the variety of sources of financial stress and their perhaps unique effects. Asset prices may be impacted by disaggregated stress components in quite varied ways, including disruptions to the “credit” market, “liquidity” constraints, higher investment positioning towards “safe-haven” assets, drops in “equities valuations”, and increased “volatility” in the global commodities, equity, and foreign exchange markets. Moreover, their impacts may change throughout short-, medium-, and long-term timeframes, reflecting variations in the rate and durability of shock transmission.

Y. Liu and Wang (2024) analyzed whether the shock transmission from aggregated measure of financial stress towards sustainable stock remain homogenous across different quantiles. Overall findings suggested that financial stress consistently had a large effect on green assets at all quantile levels. The potential predictive efficacy of aggregated financial stress variables for returns on the Chinese stock market was examined by Y. Xu et al. (2023). Their results show that these indices are better at describing market fluctuations during an upward trend than during a downward one. Furthermore, Apostolakis et al. (2021a) investigated the relationships among stock market dynamics in the G7 nations, financial stress, and oil market uncertainty. Changes in the level of uncertainty around the oil market have a substantial impact on financial stress in these wealthy countries. Similarly, C. Liang et al. (2023) analyses the response of equity markets due to the fluctuations in the composite financial stress indices. During the COVID-19 pandemic, the FSI demonstrated a remarkable capacity to predict the long-term realized volatility of stock markets.

According to study findings reported by Singh and Singh (2016), increasing financial stress is more likely to cause capital outflows and less likely to cause capital inflows in the Indian and American financial systems. Using the quantile dependent VAR technique, Hoque et al. (2024) examined the extent to which financial stress influences conditional risk in U.S. sectoral equities across higher and lower quantiles. They found that when bullish volatility is high, sectoral stocks are more susceptible to financial stress shocks than when volatility is moderate or median. In a related study, Ilesanmi and Tewari (2020) evaluated the impact of financial stress on investment and economic output in South Africa using a VAR framework. Their empirical results indicate that economic growth and capital formation are negatively impacted by elevated financial stress.

2.2. The Spillover of Shock Propagation Towards the GCC Sectoral Stock Conditional Volatility from Bitcoin Investors’ Fear and Greed Sentiment Indices (BSI)2

The digital currency adoption in the Gulf Cooperation Council (GCC) has exploded, with the region’s cryptocurrency market estimated to be worth USD 744.3 million in 2024 and expected to grow at a compound annual growth rate of 16.8% to reach USD 3.49 billion by 2033 (IMARC Group, 2024). The realized gains highlight the level of regional involvement; in 2023, investors taking positioning in Bitcoin investments in the United Arab Emirates made around USD 204 million in bitcoin profits, while Saudi investors made even more, USD 351 million (The National, 2024). With almost 70% of actual investment profits in the United Arab Emirates coming from Bitcoin, Ethereum comes in second with 24% and XRP comes in third (Gulf Insider, 2024). Bitcoin is still the most popular digital asset. With about USD 34 billion in inflows between July 2023 and June 2024—a 42% annual increase—the United Arab Emirates (UAE) has become the primary hub for crypto-related activity among the member nations (Mining Grid, 2024). With over half a million traders participating daily, of whom about 72% have a clear preference for Bitcoin, investor activity in the area is also growing (Bitget Research, 2024).

The shock transmission from BSI to sectoral stocks is theoretically consistent with cross-asset contagion processes in the setting of portfolio rebalancing (Kodres & Pritsker, 2002). Due to perceived wealth effects, positive shocks in the Bitcoin market might cause reallocations into stocks, but negative shocks cause “flight-to-safety” reactions that lower investment in developing market stocks. Furthermore, digital currencies and Islamic financial instruments are both becoming more widely acknowledged as vehicles for hedging and diversification, which implies that Bitcoin sentiment may be able to spread peculiar shocks throughout the GCC through risk-management choices and reallocation. Behavioral finance theory also emphasizes how trading psychology increases the spread of disruptions unique to cryptocurrencies. Markets with different macroeconomic structures may become interconnected through sentiment-driven channels due to investor overreactions, herd behavior, and uncertainty aversion (W. M. A. Ahmed, 2021a). Furthermore, significant depreciation in the Bitcoin prices lead towards the heightened fear amongst bitcoin investors and this would lead towards the anxiety and loss of confidence in the Bitcoin market. Therefore, a shock in the BSI lead towards the higher GCC sectoral stock volatility.

Building upon the behavioral financial theoretical approach, investor attitude played a contributory role as non-fundamental factor that impacts asset price. Abrupt sell-offs due to increased anxiety lead towards the volatility across inter-connected financial markets. Conversely, bitcoin investors’ fear and greed are frequently the driving forces behind speculating bubbles. Changes in shareholders’ attitude, as indicated by indices of fear and greed, are anticipated to result in equity markets’ shock spillovers because of Bitcoin’s substantial involvement in GCC investment portfolios and its impact on wealth effects. Thus, GCC sectoral stock conditional volatility’s shock spillover absorption capability may be exacerbated by both macroeconomic variables and shifts in investor sentiment brought on by cryptocurrencies. According to W. M. A. Ahmed (2021b), psychological makeup of investors is crucial in facilitating the introduction of shocks unique to Bitcoin into the stock market. Economies with different economic and structural characteristics may monetarily integrate through emotional channels. For example, BSI depreciation may have caused bitcoin investors to experience extreme emotional stress, which would erode their sense of security and raise their risk perceptions. This implies that the mood dynamics around Bitcoin may have a substantial impact on conditional volatility in GCC sectoral equities. This demonstrates how emotion contagion might have caused local financial systems to become unbalanced. Consequently, changes in attitudes toward Bitcoin have a direct impact on risk appetite throughout financial asset classes; severe pessimism leads to large liquidations, while excessive optimism encourages speculative accumulation. When cryptocurrency prices are unclear, investors tend to minimize their exposure to riskier assets, including GCC stocks, which makes conditional volatility in these markets worse (W. M. A. Ahmed, 2021b).

Interestingly, no research has examined the impact of Bitcoin investors’ fear and greed sentiment related shocks on the conditional volatility of GCC sectoral stocks from a variety of investment horizons, including lower- and higher-frequency bands. Aside from the aforementioned facts, previous empirical research has mostly focused on the spillover of shocks from Bitcoin returns to different financial asset classes (S. Li, 2022; P. Liu & Yuan, 2024; Guo & Zhong, 2025; Bazán-Palomino, 2023; Younis et al., 2025; Jia et al., 2024; Khalfaoui et al., 2023). However, little focus has been placed on investigating the shock transmission from Bitcoin Investor Sentiment Indices (BSI), specifically fear and greed measures, on equity market volatility. This distinction is crucial because, whereas sentiment-based shocks represent behavioral and psychological phenomena that can impact trading activity beyond basic valuation movements, return-based shocks capture changes induced by actual market performance.

In a comparable manner, P. Liu and Yuan (2024) used TVP-VAR domain shock spillover technique to evaluate Bitcoin’s hedging potential against foreign exchange and other financial asset classes. Their investigation found that Bitcoin served as an oasis of security investment during times of severe financial crises and decreased long-term investment risks in the currency and equities markets. Guo and Zhong (2025) investigated the relationships and shock spillovers between various cryptocurrencies and traditional financial asset classes for the purpose of investigating whether they enhance investment portfolios’ capacity to mitigate financial market risks. The empirical findings demonstrate the superior hedging capabilities of cryptocurrencies, especially with regard to stock market exposures. Using the VAR-BEK-GARCH (1,1) approach, S. Li (2022) examined the dynamic relationships between meme stock risks and cryptocurrencies. According to the findings, Bitcoin’s negative volatility shocks had a greater and more substantial effect on meme stocks.

More recently, the transmission of volatility shocks between Bitcoin and stocks markets was studied by Bazán-Palomino (2023) in Europe, the US, and Asia-Pacific. The findings indicated that although Bitcoin’s long-term influence on the majority of Asia-Pacific economies remained substantial, its influence gradually diminished in North America and a few European countries. Similar to this, Younis et al. (2025) examined whether GCC economies have more spillover effects from Bitcoin’s volatility using the Diebold and Yilmaz (2012) connection approach inside a GVAR framework. The results indicated that while Bitcoin-induced volatility spikes mostly traveled to Qatar, Kuwait, and Oman, both Saudi Arabia and the United States were the primary providers of shocks to all other markets, albeit with larger magnitude and intensity. Khalfaoui et al. (2023) analyzed the asymmetrical quantile-based interactions between returns on conventional (non-Sharia) and Sharia-compliant stocks in BRICS nations and cryptocurrencies. The results showed that different quantiles exhibited unique patterns of shock transmission, which intensify during times of severe market circumstances. Bazán-Palomino (2023) examined the transmission of volatility shocks between Bitcoin and stock markets using data from Europe, the US, and Asia-Pacific. In 2024, Jia et al. carried out a similar examination of the connections between Bitcoin and a number of financial asset classes. Significant relationships between Bitcoin and international stock markets were discovered by their analysis, suggesting that Bitcoin might be a helpful tool for foreign investors looking to diversify and hedge against risk.

2.3. The Spillover of Shock Transmission Towards the GCC Sectoral Stock Conditional Volatility from U.S. and European Financial Market Uncertainty (U.S. CBOE VIX and Euro VSTOXX-50)

According to Balli et al. (2021), economies that have weaker fiscal systems, high levels of financial openness, and close commercial ties to developed markets are more susceptible to the uncertainty that is transferred from U.S. markets. Compared to realized volatility or model-based measures, volatility indices like the VIX and VSTOXX integrate more thorough information and function as forward-looking assessments of market expectations. These impacts are strengthened by the United States’ worldwide position, which in 2017 constituted an integral position within the international portfolio assets and continued to be a major source of foreign direct investment (Balli et al., 2021). As a result, shocks that start in the U.S. and European markets have a greater impact on global equities systems, including the GCC’s (Smales, 2020). Therefore, from the perspective of behavioral finance, periods of increased global stress, especially during spikes in the level of uncertainty in the U.S. and European equities markets as indicated by the VIX and VSTOXX, often lead to extensive sell-offs by foreign investors (Yadav et al., 2023). Even in the absence of unfavorable regional shocks, this trend is true for GCC stocks. Herding behavior, which occurs when traders mimic the tactics of others in such situations, is a phenomenon that increases the transmission of volatility shocks from financial stress indicators (FSIs) such as VIX, VSTOXX, and others to GCC sectoral equities markets (Kirimhan et al., 2024). As part of larger risk management strategies, institutional investors also help by adjusting their international portfolios and usually reducing their exposure to GCC assets. This procedure increases the GCC’s absorption of external volatility.

Äijö (2008) assessed the degree of equity market integration by examining the term structure of implied volatility across German, Swiss, and Pan-European blue-chip companies represented by the VSTOXX-50. Y.-J. Zhang et al. (2017) looked more closely at the role that the VIX and VSTOXX, two volatility indexes used in the United States and Europe, play in causing disruptions to global commodities markets. A risk-neutral, model-free benchmark, the Chicago Board Options Exchange Volatility Index (VIX) gauges market expectations of stock price movements over a 30-day period (Wu et al., 2023). As a measure of investor mood, the VIX is an implied volatility indicator; high values are frequently linked to heightened pessimism and downward pressure on asset prices (B. Chen & Sun, 2022).

Increased volatility in the U.S. financial markets (CBOE VIX) or the European financial markets (VSTOXX-50) encourages foreign investors to reevaluate their expected risk-return trade-off in the context of risk premia adjustment. As GCC financial institutions expand their connections to global capital markets, these reevaluations are mirrored in shifts in regional equity risk premia. Another perspective is offered by the contagion mechanism, which shows how volatility disturbances initiated in developed financial system spread throughout the global financial system (Longstaff, 2010). This process is accelerated by international portfolio reconfiguration, which causes sell-offs in GCC markets as investors shift their funds from riskier assets like GCC stocks to more conventional safe havens like US Treasuries and precious metals. The fundamental tenets of the asset pricing theoretical approach emphasize that taking on systematic risk is outweighed by expected returns, which are often reflected by implied volatility indexes such as the VIX and VSTOXX-50 as well as more broad indications of established financial market uncertainty indicators. Strong evidence of volatility spillovers has been presented by empirical research employing conditional correlation frameworks and regime-switching models; shocks originating in the United States and Europe have a particularly significant impact on regional and global markets (Baele, 2005). Together, these findings imply that through interrelated pathways of risk repricing, contagion, and portfolio rebalancing, financial turmoil in the United States and Europe, exacerbated by global financial stress indicators, can considerably increase conditional volatility in GCC sectoral equities. For instance, the historical evidence supports the idea that systemic financial recessions, such as the subprime mortgage crisis of 2007, European debt crisis of 2012 and the failure of Lehman Brothers in 2008, quickly intensified into a global recession with significant cross-market effects. Similar to this, during periods of significant shocks, periods of intense stock market volatility usually have an impact on whole financial systems. According to Bekaert et al. (2005), contagion is theoretically defined as “excessive correlation,” which denotes atypical cross-market co-movements during crises.

The literature on the transmission of shocks from the implied volatility of the U.S. and European equity markets into the GCC financial system, however, is still noticeably lacking, especially when examined across a variety of frequency horizons. It is important to address this gap because doing so would help investors and policymakers create resilience plans for the sectors markets of the GCC in a variety of market scenarios. It will also improve our knowledge of cross-regional volatility links. For instance, previous research has predominantly concentrated on the ways in which trade, climate, and macroeconomic disruptions originating in the U.S. financial system cascade into financial asset classes (Tedeschi et al., 2024; D. Li et al., 2022). Much of this work has examined volatility and shock spillovers from international equity market disturbances to the African financial system (Dankwah et al., 2025), from the U.S. to the Asia–Pacific region (Cheng et al., 2024), among the G7 economies (Akhtaruzzaman et al., 2021b), between the U.S. and China (Y. Zhang & Mao, 2022), and from European sectoral equities to commodity-linked asset classes (Cheng et al., 2024).

In a related study, X. Chen et al. (2024) examined the transmission channels between the commodities and equity markets using Diebold and Yilmaz’s (2012) conventional connectedness model. It also examined the role of the VIX as a key determinant of the overall interdependence of the financial and commodity markets. The findings demonstrated that the moderating influence of the VIX on the connections between commodities and financial markets depends on the prevailing investment regime. Dankwah et al. (2025) investigated the transmission of shocks from global equities returns to developing markets in African nations using a connection paradigm based on Quantile Vector Auto-regression (QVAR). According to their results, there are better connections between the African financial system and traditional asset classes; however, the degree of these connections varies depending on the state of the stock market. Using the QVAR connection technique, Cheng et al. (2024) also examined asymmetric shock spillovers in the quantile domain among traditional asset classes in Asia, the US, and Europe. The findings showed that the Asian-Pacific financial system is more impacted by the returns of European and American equities, and that these impacts are more noticeable when the market is volatile. Additionally, using the framework of financial contagion theory, Akhtaruzzaman et al. (2021b) investigated the interdependencies between the financial markets of China and the G7. Their results showed that during the pandemic, correlations between financial-sector companies increased significantly, highlighting their crucial role in promoting the spread of market disruptions. Similarly, Y. Zhang and Mao (2022) used the spillover of shock methodology introduced by Diebold and Yilmaz (2012) to study shock propagation between developed and emerging equities markets, specifically the US and China. They found that the American financial system was more affected by Chinese shocks, a phenomenon exacerbated by the COVID-19 pandemic.

3. Data and Methodology

3.1. Data

This study investigates how shocks from BSI, U.S. and European financial markets’ uncertainty indices (CBOE VIX and VSTOXX-50) and FSIs influence the conditional volatility of GCC Islamic sectoral equities—specifically Industrials (IND), Health Care (HC), Real Estate (RE), Consumer Staples (CS), Financials (FIN), Energy (ENE), Telecommunication (TEL), Utilities (UTI) and Materials (MAT)—using daily data from 1 February 2018, to 1 January 2025. The Islamic sectoral stocks are taken into account because of the fact that Sharia-compliant financial system’s resilience during the 2008–09 financial crisis and its outperformance of conventional equity markets have strengthened investor demand for Sharia-compliant products, which prohibit interest and operate on profit-and-loss sharing principles. Whereas, the daily time series data on GCC sectoral stocks are incorporated from https://www.spglobal.com/en (accessed on 1 January 2025). U.S. equity market uncertainty conditions captured through the CBOE Volatility Index (VIX), representing S&P 500 volatility. Data on CBOE VIX and European VSTOXX-50 were sourced from the Federal Reserve Economic Data (https://fred.stlouisfed.org/ (accessed on 1 January 2025)) and www.investing.com (accessed on 1 January 2025) from 1 February 2018, to 1 January 2025. For the European market, the VSTOXX-50 index is employed to reflect anticipated volatility in Eurozone equities. While the VIX serves as a global equity market risk gauge, the VSTOXX specifically captures Eurozone equity market uncertainty (Sarwar, 2023).

To further assess the role of global financial stress, we incorporate disaggregated daily Financial Stress Index (FSI) measures—obtained from the U.S. Department of Treasury—which include “credit” market disruptions, “funding” pressures, equity, forex and commodity “volatility”, reduced “equity valuation” capacity, and a shift toward “safe-haven” assets. The daily data for the components of the Financial Stress Index (FSI) spanning the period from 1 February 2018, to 1 January 2025, were obtained from the U.S. Office of Financial Research’s publicly accessible database (available at https://www.financialresearch.gov/financial-stress-index/ (accessed on 1 January 2025)).

As an indication of global equity market risk, Dutta (2018) used the U.S. CBOE VIX in an ARDL modeling framework to examine the connection between the performance of U.S. energy sector stocks and the unpredictability of the global oil market. As a measure of investor emotion and expectations for future market circumstances, the VIX has been validated by Q. Zhang et al. (2024) as a crucial indicator of market uncertainty in the United States. Additionally, Sarwar (2023) demonstrated that the CBOE-VIX and its European equivalent, the VSTOXX-50, modify the dynamic conditional correlations between the financial markets of the United States and Europe and function as indicators of stock market uncertainty.

A popular tool for assessing the mood of the cryptocurrency market and predicting price patterns is the Bitcoin Fear and Greed Sentiment Index (BSI). It compiles metrics including price momentum, social media sentiment, market momentum, volatility, and Bitcoin dominance. DataStream provided daily data from 1 February 2018, until 1 January 2025 (https://www.lseg.com/en (accessed on 1 January 2025)). Similarly, Mokni et al. (2022) used a quantile regression framework to evaluate their capacity to predict Bitcoin returns during the COVID-19 crisis, while Gaies et al. (2023) employed them to predict Bitcoin price movements using daily observations from 2018 to 2020.

In order to create a harmonized dataset appropriate for thorough econometric analysis, daily records for sectoral stock conditional volatilities, stress indices, sentiment measures related to cryptocurrencies, and implied volatility indicators were methodically linked with their corresponding calendar dates using VLOOKUP. Previous studies have also looked at the transmission patterns connecting the VIX to different commodities asset classes and the spread of shocks from composite measures of financial stress indices to equities markets (Le et al., 2021). Additionally, a smaller body of research has examined the relationship between U.S. stock markets and mood indices measuring fear and greed among Bitcoin investors, using a similar data alignment approach to guarantee temporal consistency. This study used Excel’s VLOOKUP feature to combine and align data from a variety of sources, such as financial stress indicators (FSI), the CBOE VIX, VSTOXX-50, BSI, and GCC sectoral stocks. The rationale for this approach is rooted in the fundamental need in time-series econometrics that models such as the TVP-VAR employ uniformly synchronized datasets, in which every variable is denoted by an identical temporal index. Without such synchronization, the estimation of dynamic linkages and shock transmission mechanisms would be susceptible to distortion, since misaligned observations introduce spurious inconsistencies and compromise the reliability of the findings.

Following the 2008 global financial crisis, Islamic finance had a considerable expansion on a global scale, reaching a valuation of $2.19 trillion by 2018 (Raouf & Ahmed, 2022). Islamic banks played a crucial role in shaping the region’s financial environment, as seen by the over $490 billion in assets they held in the GCC alone by the middle of 2013 (Aliani et al., 2022). The current study uses a Student’s t-copula structure in conjunction with a univariate EGARCH (1,1) model to describe the daily dynamics of conditional volatility in Sharia-compliant sectoral stocks across GCC markets. With a combined market value of over $8 trillion, companies listed on GCC stock exchanges establish the area as a major contributor to the MSCI Emerging Markets Index (Al-Fayoumi et al., 2023). According to projections, the economies of the GCC are expected to grow at an annualized rate of around 7%, following development paths like to those seen in fast emerging countries like China and India (Bouri et al., 2023). The EGARCH (1,1) approach’s mean and variance equation can be expressed as

In the above Equation (1a), and are characterized as return series at a time t and conditional mean, respectively. Whereas, is the return innovation (shock). is the standardized error term, typically assumed with mean 0 and variance 1 (e.g., Normal or Student’s t). Furthermore, the variance equation of the EGARCH (1,1) can be written as

In the specified Equation (1b), ω represents the constant component that determines the unconditional or long-term average level of volatility. The coefficient β denotes the persistence parameter, reflecting the degree to which previous volatility continues to influence current conditional volatility (). A higher estimated value of β suggests that shocks to volatility dissipate more slowly, thereby enhancing persistence. The parameter α captures the magnitude effect, indicating the sensitivity of volatility to the size of market shocks (measured through absolute returns). A positive α suggests that larger shocks translate into heightened future volatility. The coefficient γ embodies the asymmetry, often referred to as the leverage effect, assessing whether negative innovations ( < 0) exert a different impact on volatility compared to positive ones of equal magnitude. When γ < 0, negative shocks intensify volatility more strongly than comparable positive shocks, whereas γ > 0 implies the reverse, with positive shocks exerting greater influence. In contrast, Bouri et al. (2023) employed models from the GARCH family to assess the conditional risk dynamics of sector-specific equities in the GCC region and to investigate how extreme shocks are transmitted between oil-related implied volatility and the volatility of GCC sectoral stock markets.

3.2. Methodology3

3.2.1. The “Time” Domain Connectivity Approach Based upon the TVP-VAR Method by Antonakakis et al. (2020)

This study adopts the Time-Varying Parameter Vector Autoregressive (TVP-VAR) framework with a 20-step-ahead forecasting horizon to examine the spillover dynamics of shocks originating from U.S. and European financial market uncertainty—captured through the VIX and VSTOXX-50 indices—as well as from disaggregated Financial Stress Indicators (FSIs) and Bitcoin Investors’ Fear and Greed Sentiment Index (BSI) in predicting the 20-day-ahead conditional volatility of GCC sectoral equities. Within the existing body of research, Chatziantoniou and Gabauer (2021) investigated the dynamic transmission of shocks between interest rate swaps and monetary policy uncertainty by employing a similar 20-step-ahead predictive horizon coupled with a 200-day rolling window. The same forecasting horizon was used by Balcilar et al. (2021) to investigate the processes of shock transmission between the commodities market and oil futures prices using the TVP-VAR approach. Furthermore, Antonakakis et al. (2020), who looked at the changing interdependencies within foreign currency markets, used a methodological approach that is consistent with the 200-day rolling timeframe chosen for this research.

In order to ensure steady and effective parameter evolution across time, the Time-Varying Parameter Vector Autoregressive (TVP-VAR) model is estimated using a Bayesian framework and informative shrinkage priors. In particular, the model uses a “BayesPrior” specification, which assumes that the variance–covariance matrix and the coefficients follow random walk processes with innovations that are normally distributed. The hyper-parameters = 0.99 and = 0.96 determine the degree of smoothness in these time-varying parameters. The autoregressive coefficients have greater persistence when is larger, suggesting that they develop gradually and represent slow structural changes in the data. In contrast, the error covariance matrix’s adaptability is controlled by , which permits a considerable amount of flexibility in volatility dynamics. By avoiding overfitting and guaranteeing that parameter modifications maintain their economic significance, this Bayesian prior structure successfully strikes a compromise between model flexibility and parsimony. These previous arrangements have been frequently utilized in the empirical literature (e.g., Koop & Korobilis, 2014; Antonakakis et al., 2020) for modeling dynamic spillovers and uncertainty transmission across financial markets because they provide a dependable way of capturing changing interdependencies while maintaining numerical stability in estimation.

The connectivity technique of Diebold and Yilmaz (2012) is extremely susceptible to the arbitrary choice of the rolling-window dimensions, whereas the TVP-VAR methodology employs a multivariate variant of the conventional Kalman filter for estimating parameter values. Consequently, providing flexibility without the chance of losing observations when dealing with small datasets (Harvey et al., 1992). Furthermore, according to Balcilar et al. (2021), the spillover index estimated through the TVP-VAR connectivity approach show a high degree of robustness against outliers. This technique combines the methodology of Koop and Korobilis (2014) with the connection concept of Diebold and Yilmaz (2012). We use a TVP-VAR model with a lag order of 1 that was chosen using the Bayesian Information Criterion (BIC).

Let and represent K × K matrices, while , , and are K × 1 vectors. Although is a × matrix, both vec () and are vectors. Over time, the parameters () change, affecting the relationships among the series. The matrices of the variance-covariance and also vary over time (Balcilar et al., 2021). The Wold representation theorem is employed to transform the TVP-VAR model into a TVP-VMA model. The equation is presented, with = as the initial condition. Here, represents a vector of white noise shocks with a symmetric yet non-orthogonal time-varying covariance matrix () = . Consequently, the forecast error for H steps can be expressed as follows:

with error co-variance matrix as:

The framework is built upon the “H-step” ahead “generalized forecast error variance decomposition” (GFEVD) approach developed by Koop et al. (1996) and Pesaran and Shin (1998). The (scaled) GFEVD, denoted as , signifies the impact of a disruption in variable j on variable i, formally defined as:

In the scenario described, where is a K × 1 vector mostly zeros with a single one at the position, and denotes the reduction in error variance of variable i due to shocks in variable j over an H-step interval. Diebold and Yilmaz (2012) proposed a normalization approach to address the issue that does not equal 1. This involves dividing each value by the sum of its respective row, yielding the generalized spillover table . The key to spillover summary metrics is this table, which captures directional “FROM” connectivity (impact of other variables j on i) and “TO” connectivity (how shocks in i affect j). These spillovers can be expressed as:

The “NET” directional spillovers can be estimated as

Antonakakis et al. (2020) characterize the total connectedness indices (TCI) as the aggregate proportion of forecast error variance decomposition arising from the shock transmissions throughout the entire VAR network. This can be expressed as

In addition to the quantitative representation of TCI described earlier, another measure known as the “net pairwise dynamic connectedness” can be defined as: .

3.2.2. The “Frequency” Domain TVP-VAR Approach by Chatziantoniou et al. (2023)

From the overall transmission of shocks from the global uncertainty factors towards the GCC sectoral stock volatility, we now shift our focus to examining the interconnectedness in the frequency domain, specifically investigating the transmission of the short- and long-term shocks across the variables. This analysis employs the (Stiassny, 1996) spectral decomposition method, facilitating an exploration of interconnection as elucidated by Chatziantoniou et al. (2023). Chatziantoniou et al. (2023) examine the spectral density of variable at frequency ω using the equation , where “i” represents the imaginary unit (√−1) and ω denotes the frequency. The Fourier transformation of the TVP-VMA (∞∞) model is employed to define the spectral density in this context

Spectral density is included in the framework of the GFEVD incorporating frequency analysis. Normalizing the frequency-based GFEVD is crucial, and the methods employed here are similar to those used in the temporal analysis. The following is one way to express this normalization:

“” in this context indicates the spectral component of the variable associated with a shock in the variable at the certain frequency ‘ω.’ This metric represents the correlation at a specific frequency. To explore connections across the diverse time periods encompassing multiple frequencies, we aggregate all frequencies within a designated interval ‘d’ represented as (a, b), where ‘a’ and ‘b’ fall within the range (−π, π) with ‘a’ being less than ‘b’. Thus, expressing this as d = (a, b): a, b ∈ (−π, π), a < b encapsulates this concept effectively.

Hence, the directional spillover of shocks, i.e., TO, FROM and NPDC can be written as , and , respectively. However, the total connectedness indices (TCI) can be written as . Moreover, the NET spillover of shocks can be written as = .

All these measures provide particular information about the assigned frequency range, but none provides an exhaustive analysis of the total effect at all frequencies. In order to overcome this constraint, Baruník and Křehlík (2018) provide an approach wherein the impact of measurements for every frequency band ‘d’ is proportionately weighed in relation to the whole system. As stated by Chatziantoniou et al. (2023), the weighing, represented as Γ(d), is calculated by dividing the total number of variables ‘N’ in the system by the combined value of all “” values inside the frequency band.

Consequently, the directional transmission (TO), reception (FROM), and NET spillover of shocks can be expressed as and , respectively. Additionally, the total connectedness indices (TCI) can be written as . The net spillover of shocks can be reformulated as: . Finally, the directional “TO”, “FROM”, “NET” as well as ‘Total Connectedness Indices” and “Net Pairwise Directional Connectedness” (NPDC) in the frequency domain based on TVP-VAR can be articulated as

Furthermore, in the present study, the endogeneity issue is mitigated both econometrically and conceptually due to the following reasons. First, as the wavelet framework separates co-movements and causality patterns at different scales rather than depending on a single aggregated time-series process, this time–frequency decomposition naturally overcomes simultaneity bias. The framework lessens the possibility that estimated spillovers are caused by current shocks or feedback loops by distinguishing low-frequency (long-term) cycles reflecting structural interdependence from high-frequency (short-term) co-movements, which are usually dominated by market noise and instantaneous reactions (Chatziantoniou et al., 2023). In order to mitigate reverse causality, the model captures directional transmission instead of contemporaneous correlation. The transmission of shocks from Bitcoin to equity markets, for example, was examined by Khalfaoui et al. (2022) using a VAR-based connectivity approach. They found no evidence of simultaneity bias or reverse causality, indicating that endogeneity problems were not a significant worry in their model. By using a time-varying parameter VAR (TVP-VAR) connectivity framework, Shahbaz et al. (2024) also observed how financial stress shocks spread to industrial metals. Additionally, their results supported the directional and time-dependent characteristics of spillovers, which naturally reduces the likelihood of endogenous feedback effects.

Secondly, from a theoretical standpoint, endogeneity is not a major issue in the current TVP-VAR methodological approach. This is because of the fact that the flow of uncertainty and sentiment-driven shocks follows an asymmetric and unidirectional pattern, impending from global indicators like the BSI and FSI as well as prominent financial systems, mainly the U.S. and European markets, toward relatively emerging or regionally integrated markets like those in the GCC. In the global volatility network, GCC equities markets mostly act as price takers due to their lower market size and relative lack of financial openness (Alotaibi & Mishra, 2015). The GCC is positioned as a net receiver or absorber of such disruptions, as evidenced by Haddad et al. (2020), who show that shocks that originate in advanced economies are conveyed to developing markets with higher power and persistence. Similarly, a unidirectional spillover from aggregated global financial stress indices toward stock returns across a variety of economies is documented by Soltani and Abbes (2025). Furthermore, Alotaibi and Mishra (2015) underlined that the main factors influencing GCC stock returns are the shocks from the United States and Saudi Arabia. Thus, from an economic perspective, it is still unlikely that shifts in GCC sectoral volatility would have a significant feedback effect on global benchmarks such as the VIX, VSTOXX-50, or BSI.

Thirdly, the empirical findings from earlier research also show how resilient the TVP-VAR-based connectedness technique is in identifying shock propagation processes across financial asset classes (Kapar et al., 2024) without introducing problems with endogeneity. The unidirectional and time-dependent spillover effects that are repeatedly shown in these research suggest that the TVP-VAR paradigm places inherent limitations on the emergence of simultaneity or feedback problems. Overall, we show that the VAR and TVP-VAR connectivity methods provide a robust and robust way to describe dynamic interdependencies in financial and commodities market evaluations while efficiently preventing endogeneity issues. Furthermore, the time-varying parameter vector autoregressive (TVP-VAR) approach utilized in this study proficiently handles possible dynamic endogeneity by allowing model parameters to vary uninterruptedly over time. The TVP-VAR configuration, in divergence to conventional static VAR or OLS stipulations, accounts for structural breakdowns, regime transitions, and shifts in market subtleties by capturing the evolutionary nature of interlinkages among variables (Balcilar et al., 2021). The TVP-VAR model, a well-liked econometric technique for proving directional spillovers and reducing simultaneity bias, identifies time-varying lead-lag correlations by integrating each series’ lagged interactions with its own and other variables’ prior values.

4. Results

4.1. Descriptive Statistics

Table 1a presents a summary of key descriptive statistics associated to various uncertainty indicators, including indicators of financial stress, market volatility indices for the European financial system (VSTOXX-50) and United States (CBOE-VIX), as well as the sentiment index reflecting Bitcoin investors’ fear and greed levels. On the other hand, the conditional volatility descriptive data for the different GCC stock market sectors are shown in Table 1b. The “Volatility” component, which represents volatile fluctuations in the stock, foreign currency, and commodity markets, has the most variability among the five examined global financial stress indicators, with a standard deviation of 1.183. Standard deviations of 0.50 and 0.40 are comparatively high for the “Credit” stress indicator, which represents market tension from expanding spreads, and the “Equity Valuation” component, which indicates investors’ risk aversion. The CBOE-VIX and VSTOXX-50 indexes have average values of 19.88 and 20.24, respectively, with standard deviations of 7.61 and 7.82, according to Table 1a. These numbers exceed those linked to the Financial Stress Index (FSI). Significant excess kurtosis is seen in both the European and American uncertainty indicators (VSTOXX-50 and VIX), indicating leptokurtic distributions with extreme values. This statistical data suggests that industrialized economies are experiencing increasingly frequent and severe bouts of market volatility, which might have an impact on financially linked nations like the GCC. Furthermore, with a standard deviation of 21.97, the Bitcoin Fear and Greed Sentiment Index exhibits a significant amount of unpredictability. This broad range suggests that although times of anxiety tend to cause panic selling and sharp drops in asset values, times of increased investor confidence frequently result in speculative spikes and overpriced markets.

Table 1.

(a). Descriptive statistics for the global uncertainty factors. (b) Descriptive statistics for the GCC sectoral stock conditional volatility.

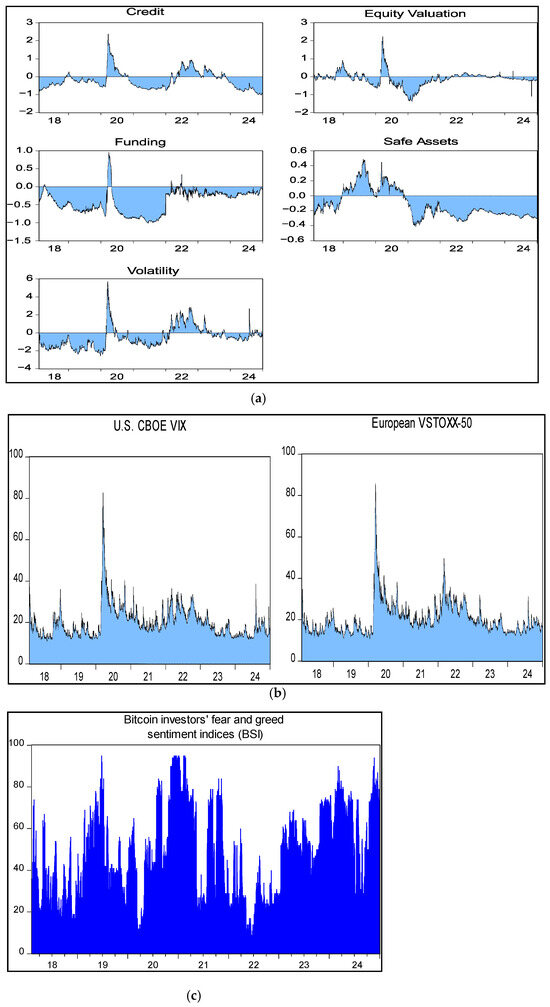

The disaggregated measures of financial distress indicators reveal a pronounced escalation, as illustrated in Figure 1a–c. The onset of the COVID-19 pandemic, among various economic disruptions, triggered breakdowns in supply-chain networks, limitations on mobility, and a decline in domestic household expenditure. Consequently, apprehensions regarding corporate sustainability and the direction of the post-crisis economic rebound intensified (Kapar et al., 2024). This heightened ambiguity prompted market participants to re-evaluate asset risks and valuations, thereby amplifying turbulence across international financial systems (Rahman et al., 2021). Specifically, Figure 1b highlights a substantial surge in the VSTOXX-50 index during 2020 and 2021. The CBOE-VIX and VSTOXX-50 indices show a significant increase in market uncertainty in both the U.S. and European stock markets during the COVID-19 pandemic. Strict lockdowns and economic limitations imposed throughout Europe in reaction to the epidemic are mostly to blame for this increase. Major European market indexes, such as the UK’s FTSE 100, France’s CAC 40, and Germany’s DAX, also had significant corrections at this time. Furthermore, while new trade agreements and regulatory reforms altered Europe’s financial landscape and affected overall equities performance, the end of Brexit at the end of 2020 added more layers of uncertainty. The attitude of Bitcoin investors also declined throughout the epidemic, as seen in Figure 1c, with anxiety levels increasing as sentiment indexes declined. Additionally, this encourages us to investigate the time-varying shock spillovers across various frequency wavelengths between the GCC financial system and FSI, BSI, and U.S. and European financial market uncertainty (VIX, VSTOXX-50) during COVID-19.

Figure 1.

(a): Graphical representation of the disaggregated global financial stress indicators (FSI). (b): U.S. and European financial market uncertainty indices. (c): The Bitcoin investors’ fear and greed Sentiment Indices (BSI).

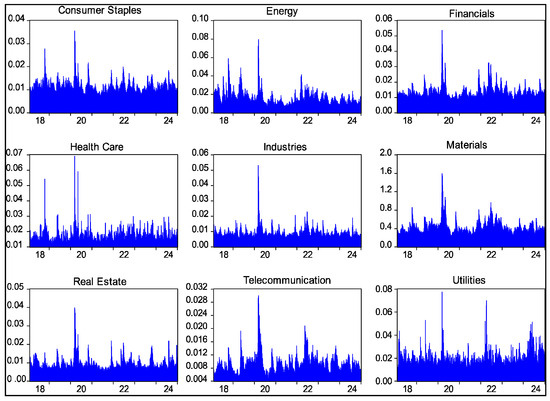

Table 1b presents the performance metrics for GCC sectoral equities, showing that Energy and Utility sectors recorded the highest average conditional volatility of 0.0162 and 0.0196, respectively, followed by Health Care (0.0167), Industries (0.092) and Financials (0.0135). The Energy sector exhibited the largest standard deviation of conditional volatility (0.0074), with Utility (0.0065) and Materials (0.1447) also displaying relatively high variability, reflecting greater return instability and elevated uncertainty. As illustrated in Figure 2, volatility levels across most GCC sectors intensified during distinct phases, notably in 2018–2019, throughout the COVID-19 pandemic, and in the post-pandemic period (2021–2022). The transnational portfolio modifications, cross-market capital flows, and shifts in investor sentiment are some of the ways that external shocks can spread across emerging economies like the GCC. Furthermore, during the COVID-19 epidemic, the conditional volatility across GCC stock sectors was increasing concurrently with global uncertainty indices like the VIX, VSTOXX-50, and the Bitcoin Sentiment Index (BSI) (see Figure 1a–c and Figure 2). This tendency makes sense given the complex linkages that characterize the contemporary global financial system (Voronkova, 2004). In big, sophisticated economies like the US or Europe, the effects of greater uncertainty often cut across national borders. Increased investor fear and a general flight from riskier assets were the causes of the sharp spikes in volatility that were seen during the pandemic (Akhtaruzzaman et al., 2021a). These moves probably had an impact on GCC stock markets as investors sought safety, causing local players to respond to both domestic and international turmoil, which in turn amplified sectoral performance changes. The idea of volatility spillover, which postulates that shocks originating in dominant financial centers can easily impact markets that differ geographically and structurally, is consistent with the apparent co-movement between GCC market volatility and key global uncertainty measures (Yousaf et al., 2022).

Figure 2.

The graphical representation of the GCC sectoral stock conditional volatility series.

4.2. The “Time” and “Frequency” Domain Shock Spillovers from Uncertainty Factors Towards the Equity Market Conditional Volatility

Table 2 reports the aggregated “time-domain” values of forecast error variances, capturing the overall spillover effects between GCC equity market conditional volatility and BSI, VIX, FSI, and VSTOXX-50. Table 3 presents the frequency-domain spillovers, revealing heterogeneous shock transmission patterns across low- and high-frequency bands, corresponding to long- and short-term investment horizons. Figure 2 provides a graphical representation of the time-varying spillover dynamics, illustrating both the aggregate (time-domain) effects and the frequency-specific transmission patterns for different investment periods (long- and short-term).

Table 2.

The time domain spillover of shocks from U.S. and European financial market risk, BSI and global financial stress indicators towards the GCC equity market volatility.

Table 3.

The frequency domain spillover of shocks from U.S. and European financial market risk, BSI and global financial stress indicators towards the GCC equity market volatility.

4.2.1. Shock Transmission from Disaggregated Financial Stress Indicators (FSI)

Table 2 indicates that the Energy sector within GCC equities absorbed the largest shock contributions, receiving 2.9%, 3%, 0.91%, 0.92%, and 2.96% from financial stress components related to “Credit” disruptions, declines in “Equity Valuation,” shifts toward “Safe Assets,” “Funding” constraints, and “Volatility,” respectively. Similarly, the Real Estate sector exhibited elevated sensitivity to shocks from “Credit” disruptions (1.74%), reduced “Equity Valuation” (3.18%), “Safe Asset” transitions (1.26%), and “Volatility” (3.23%). For the Telecommunication sector, financial stress indicators of “Credit” market disruptions, “Safe Asset” transitions, lower “Equity Valuation”, “Volatility” and “Funding” constraints also accounted for higher contributions of 1.25%, 1.22%, 4.2%, 2.64%, and 0.64% of error variances to conditional volatility, respectively, as compared with rest of the sectors. Additionally, fluctuations across international currency, commodity, and stock markets generated significant transmission effects, accounting for approximately 3.96% of disturbances within the financial industry and 4.75% within the materials industry.

In contrast to the prevalent trends in previous empirical research, the current findings on shock transmission from disaggregated Financial Stress Indicators (FSI) to GCC sectoral stock conditional volatility offer fresh perspectives. He et al. (2021) have expanded this study to European green and sustainable enterprises, demonstrating that investor risk aversion and liquidity limitations might have a negative impact on environmentally oriented industries through aggregate global stress indicators. Cipollini and Mikaliunaite (2020), on the other hand, provided a regional viewpoint by using monthly FSI at the European level to investigate the relationship between national financial stress situations and macroeconomic uncertainty in many European nations. According to their results, the spread of stress is frequently diverse and impacted by institutional and financial elements unique to each nation. As an illustration, Hippler and Hassan (2015) examined the connection between overall financial stress and US stock market performance, showing that times of elevated financial stress considerably raise systematic risk and reduce market efficiency. Therefore, previous research has mostly focused on how aggregate financial stress indicators, which are frequently built as composite indexes, explain volatility and contagion effects in advanced economies, generally ignoring disaggregated or channel-specific dynamics in developing markets.

Nevertheless, the existing literature is still lacking in a number of important areas in spite of these significant additions. To evaluate how each channel uniquely transmits shocks to various sectors, prior research has not broken down aggregated FSI into their constituent parts, such as disruptions in the “credit” market, distortions in “equity valuation”, “funding” constraints, shifts to “safe assets”, or “volatility” in global commodities and foreign exchange markets. Our understanding of how financial stress affects sectoral risk dynamics is hampered by this omission, especially in developing and resource-dependent GCC financial market, where structural characteristics like fixed exchange rate regimes, little financial diversification, and a reliance on hydrocarbon revenues may make a market more susceptible to global financial disruptions.

The empirical findings of this research article demonstrate a significant spillover influence from Financial Stress Indicators (FSI) to the conditional volatility of sectoral equities, which is consistent with earlier research on financial contagion and market instability. L. Chen et al. (2023) state that since investors are still unsure and risk averse, shocks that happen during periods of high market volatility tend to have more disruptive and long-lasting effects than those that happen during periods of financial stability. Financial pressure has a consistent negative effect on stock returns throughout the distribution, affecting both gains and losses, according to Y. Liu and Wang (2024). When taken as a whole, past studies demonstrate how financial stress affects risk dynamics and market behavior, serving as the main driver of volatility in developing financial systems. Furthermore, because positive stress shocks result in deteriorating fiscal balances and rising levels of government debt, Kasal (2023) found that increased financial stress frequently limits public financing conditions. This linkage highlights the wider macro-financial ramifications of stress-induced shocks by connecting financial instability to shifts in asset prices and systemic and fiscal vulnerabilities in developing countries. Similar to this, Fink and Schüler (2015) highlighted that changes in market dynamics might worsen during times of financial hardship because indirect channels—like credit restrictions, stricter borrowing requirements, and a lack of available capital—amplify the effects of shocks brought on by stress. Their research’s findings are in strong agreement with and support the findings of the current analysis.

Table 2 demonstrates that the cumulative proportion of forecast error variance—capturing the comprehensive transmission of disturbances across the variables (FSI, BSI, VIX, and VSTOXX-50) within the full TVP-VAR structure—is equivalent to 59.68% for the overall investment horizon. In contrast, Table 3 presents the spillover effects across frequency wavelengths, indicating that the total shock spillover—measured by the aggregated forecast error variance—is lower in the short term (19.35%) compared with the long term (40.33%). For example, in the short term, the conditional volatility of the Real Estate sector received the highest contributions of forecast error variance of 0.3%, 0.58%, 0.82%, 0.28%, and 0.59% from the financial stress components of “Credit,” “Equity Valuation,” “Safe Assets,” “Funding,” and “Volatility,” respectively. Furthermore, in the short-term, conditional volatility within the Telecommunication sector also received higher shocks of 0.3%, 0.75%, 0.76%, 0.25% and 0.85%, respectively, from these stress indicators. In the long term, these disaggregated financial stress indicators transmit larger shock contributions of 2.52%, 2.77%, 0.55%, 0.6%, and 2.61% to the conditional volatility of the Energy sector. Moreover, “Credit,” “Equity Valuation,” “Safe Assets,” “Funding,” and “Volatility” also transmitted higher contributions of shocks of 1.39%, 2.34%, 0.55%, 0.68% and 4.24% towards the conditional volatility of Material sector, respectively.

The intensified spillover effects from financial stress indicators to sectoral conditional volatility observed in this study are consistent with prior empirical research. In the same vein, the pronounced contagion patterns observed in this analysis are consistent with the work of Chau and Deesomsak (2014), who found that financial stress is an effective indicator of macroeconomic variability and functions as a precautionary signal for forthcoming financial turmoil. Additionally, the findings of Balcilar et al. (2023), who reported a strong and positive correlation between financial stress intensity and volatility transmission across developing equity markets, are supported by the stronger spillover links from different components of financial stress to conditional market risk. According to their findings, this relationship’s intensity tends to increase over longer time horizons and at times when there are significant market disturbances. According to C. Liang et al. (2023), composite indices of financial stress have a significant and long-lasting impact on the actual volatility of stock markets over time, particularly at times when there are significant global financial disruptions. All together, these similarities confirm that aggregate and disaggregated financial stress plays a crucial role in determining volatility behavior, with long-term effects on the resilience and stability of developing financial systems.

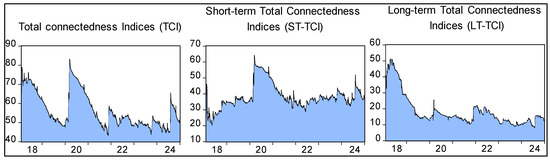

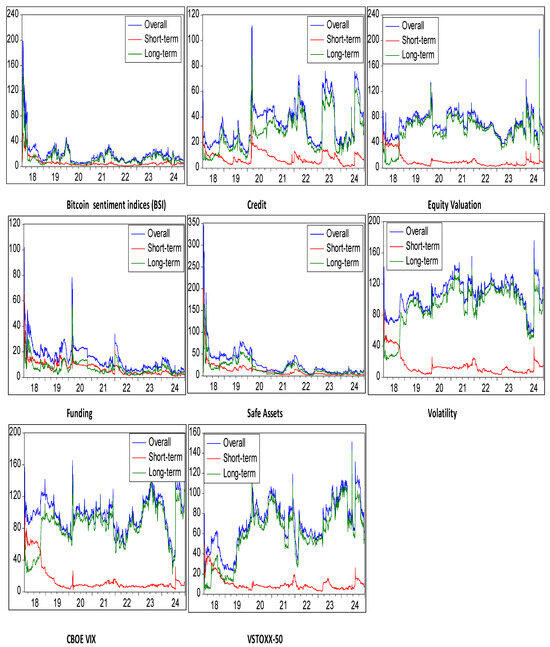

Figure 3 illustrates the total time-varying dynamic spillover effects between global uncertainty indicators (BSI, FSI, VIX, and VSTOXX-50) and the conditional volatility of GCC sectoral equities. The combined measures of overall spillovers in the time domain, as well as short- and long-term spillovers in the frequency domain, exhibit a notable rise during 2018 and 2019. Furthermore, pronounced increases in both aggregate and horizon-specific connectedness across these variables are also evident throughout 2020, between 2022 and 2023, and in the final quarters of 2023.

Figure 3.

Total Connectedness Indices for the overall, short- and long-term investment horizons.

Figure 4 presents the temporal and frequency-domain dynamics of amplified shock transmissions from financial stress indicators (FSI), such as global “Credit” disruptions, widening spreads due to “Funding” issue, decreased “equity valuations”, transition towards “Safe Assets” reflecting heightened risk aversion, and increased “volatility” in foreign exchange, commodity, and financial markets. These effects were most pronounced in 2018 and during the COVID-19 outbreak in late 2019. Intensified spillovers from FSI to GCC sectoral stock volatility were also evident in 2020 (during the COVID-19), between 2021 and 2022, and in the final quarter of 2023.

Figure 4.

Spillover of shocks from variable “” “TO” variable “” by utilizing the “Time” and “Frequency” domain TVP-VAR based connectedness approach.

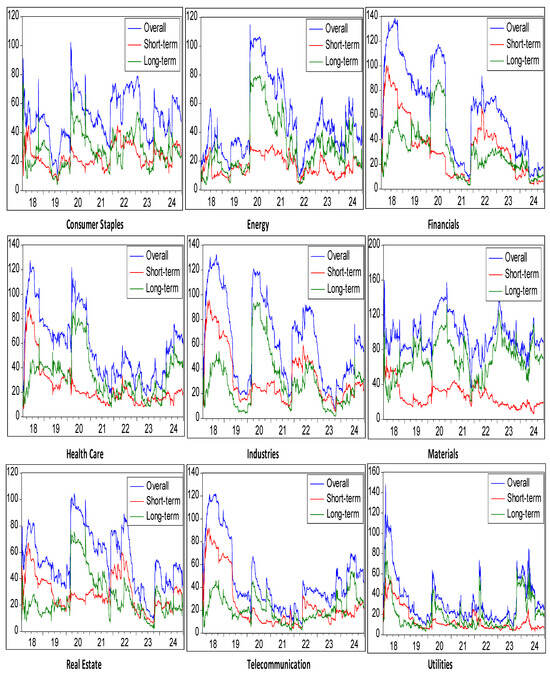

As shown in Figure 5, GCC sectoral stocks experienced elevated volatility shocks across 2018, 2019–2021 (during the COVID-19), and again between 2022 and 2023. Moreover, conditional volatility in GCC sectors recorded an additional surge in shock reception from FSI and other global uncertainty sources during the last quarter of 2023.

Figure 5.

Spillover of shocks “FROM” all other variables “j” to variable “i” by utilizing the “Time” and “Frequency” domain TVP-VAR based connectedness approach.

One of the justifications for the time-varying shock spillovers is the investors reaction to the uncertainty created by U.S. trade restrictions and their perceived implications for global economic growth; the increased financial stress shocks that influenced GCC sectoral stock volatility in 2018 were primarily caused by widening credit spreads and increasing global market turbulence (Santacreu, 2020). At the same time, Italy’s political unrest increased fiscal uncertainty throughout Europe, raising the rates on sovereign bonds and widening credit spreads in the Eurozone (The Economist, 2022; Schiantarelli et al., 2020). All of these changes reinforced financial contagion pathways from developed countries to GCC markets and indicated an increase in systemic risk. Similar economic strain was reawakened in 2019 due to the strident reduction of the Argentine peso, increasing inflationary pressures, and growing fears of a government breakdown (World Bank Group, 2018). These measures signaled growing susceptibilities in developing financial systems and augmented the spread of volatility from global financial stress indicators to the GCC’s equities markets. Subsequent to this, the COVID-19 pandemic in late 2019 further aggravated financial unsteadiness by causing a sharp worldwide economic decline, liquidity constraints, and a significant upsurge in credit spreads as governments and businesses sought for immediate sources of funding. The hostility over oil pricing between Russia and Saudi Arabia, which led to an extraordinary breakdown in crude oil values, undermined the energy industry and intensified the financial vulnerability of the GCC’s petroleum-based economic structure (Ma et al., 2021).

Furthermore, the global financial disruptions following the pandemic were compounded by the Evergrande debt turmoil in China, which heightened investors’ risk perception and exposed the structural fragility of over-leveraged property sectors (Altman et al., 2022). Given its trade interconnections and dependence on resource exports, the GCC region experienced a more pronounced impact from the ensuing financial tremors that rippled through worldwide equity markets, amplifying volatility transmission. These developments collectively diminished investor assurance, broadened sectoral exposure to risk, and escalated market instability across the GCC’s financial landscape. This demonstrates how the region’s susceptibility to worldwide financial stress is still impacted by foreign financial and geopolitical shocks. As a result, FSI showed more robust transmission patterns toward sectoral volatility in the GCC in 2021, signifying a time of increased market interdependence and fresh stress. Lastly, by distressing commodity supply chains, imposing harsh sanctions, and raising risks in the energy and geopolitical markets, the Russia-Ukraine conflict of 2022 further increased global unpredictability (Boubaker et al., 2022). In addition to increasing risk premiums and volatility across a number of asset sectors, these disruptions tightened global financial conditions.

4.2.2. Shock Transmission from U.S. VIX and European VSTOXX-50

Table 2 reveals that variations in the U.S. VIX produce significant expansions in the proportion of forecast error variance linked to sector-specific conditional volatility—amounting to 3.98% for the Financial sector, 3.48% for Energy, 4.88% for Materials, and 3.55% for Real Estate. In addition, the same table shows that shocks originating from the VSTOXX-50’s conditional volatility generate the largest spillover effects of 3.28%, 2.88%, 3.02%, and 2.87% on the Energy, Industrials, Materials, and Real Estate sectors, respectively. Meanwhile, Table 3 presents the pattern of shock transmission across different frequency domains, capturing both short- and long-term investment horizons. The findings indicate that volatility shocks from both the VIX and the VSTOXX-50 exert stronger and more persistent effects on the Energy, Financials, Materials, and Real Estate sectors over the long run compared to the short run. For instance, in the short term, the conditional volatility of Financials, Health Care, Industrials and Telecommunication sectors receives higher shock contributions of 0.96%, 1.04%, 1.16% and 1.28%, from the VIX, respectively, compared with the other GCC sectors. Similarly, these sectors receive higher short-term shocks of 0.73%, 0.62%, 0.94% and 0.72% from the VSTOXX-50, respectively (see Table 3). However, in the long term, the Energy, Financials, Material and Real Estate sectors experience the highest shock spillovers from both the VIX and the VSTOXX-50 compared with the other GCC sectors. For example, in the long term, the VIX transmits shocks of 2.87%, 3.02%, 4.15% and 2.78% to the conditional volatility of Energy, Financials, Material and Real Estate sectors, respectively. Similarly, these sectors receive the highest shock spillovers from the VSTOXX-50, with contributions of 2.77%, 2.05%, 2.68%, 2.25%, respectively, compared with the remaining GCC sectors.