Oil Volatility Uncertainty: Impact on Fundamental Macroeconomics and the Stock Index

Abstract

1. Introduction

2. Literature Review

2.1. The Relationship between Crude Oil Price Changes and Macroeconomic Variables

2.2. Applications of GARCH Models

3. Methodology

3.1. The GARCH(1,1) Models

3.2. MS-GARCH Model

3.3. ARDL Model

3.4. The Evaluation Criteria

4. Data Description

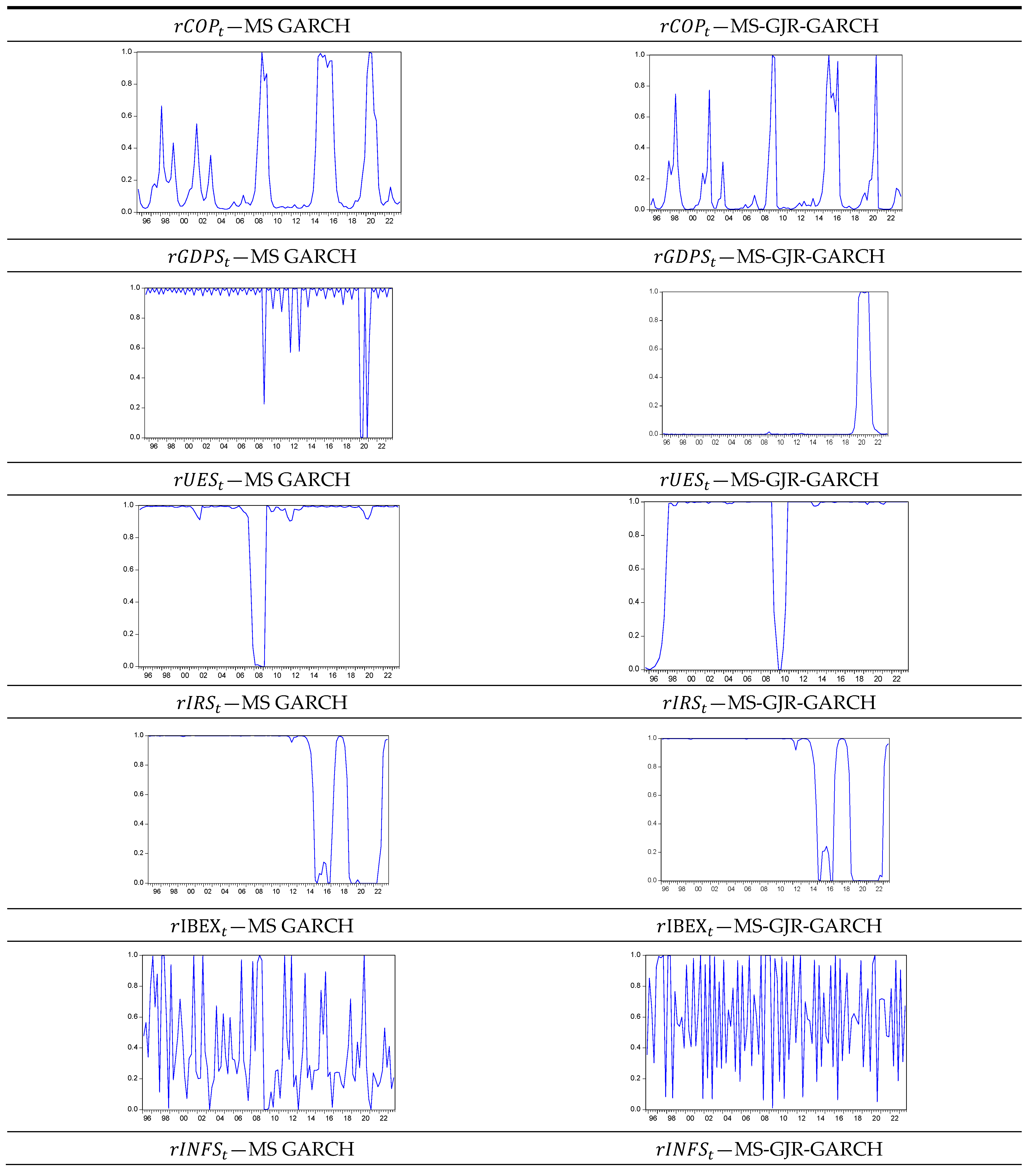

5. Empirical Results

6. Conclusions

Funding

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Agnolucci, Paolo. 2009. Volatility in crude oil futures: A comparison of the predictive ability of GARCH and implied volatility models. Energy Economics 31: 316–21. [Google Scholar] [CrossRef]

- Ahsanullah, Mohammad, B. M. Golam Kibria, and Mohammad Shakil. 2014. Student’s t Distribution. In Normal and Student’s t Distributions and Their Applications. Paris: Atlantis Press, pp. 51–62. [Google Scholar] [CrossRef]

- Aktan, Bora, Renata Korsakienė, and Rasa Smaliukiene. 2010. Time-varying volatility modelling of Baltic stock markets. Journal of Business Economics and Management 11: 511–32. [Google Scholar] [CrossRef]

- Aladwani, Jassim. 2023. Wavelet Coherence and Continuous Wavelet Transform—Implementation and Application to the Relationship between Exchange Rate and Oil Price for Importing and Exporting Countries. International Journal of Energy Economics and Policy 13: 531–41. [Google Scholar] [CrossRef]

- Aloui, Chaker, Besma Hkiri, and Larisa Yarovaya. 2015. On the effects of oil price uncertainty on stock returns in major oil-importing countries: Evidence from quantile regression. Journal of Quantitative Economics 13: 95–115. [Google Scholar]

- Álvarez, Luis J., and Alberto Urtasun. 2013. Variation in the cyclical sensitivity of Spanish inflation. In Economic Bulletin. Madrid: Banco de España, July–August. [Google Scholar]

- Ardia, David, Keven Bluteau, Kris Boudt, Leopoldo Catania, and Denis-Alexandre Trottier. 2019. Markov-switching GARCH models in R: The MSGARCH package. Journal of Statistical Software 91: 1–38. [Google Scholar] [CrossRef]

- Babatunde, S. Omotosho. 2019. Oil Price Shocks, Fuel Subsidies and Macroeconomic (In)stability in Nigeria. CBN Journal of Applied Statistics 10: 2. [Google Scholar] [CrossRef] [PubMed]

- Baillie, Richard, and Tim Bellerslev. 2003. A multivariate generalized ARCH approach to modeling risk. Journal of International Money and Finance 22: 625–49. [Google Scholar]

- Barrios, Salvador, and Diego Rodríguez-Palenzuela. 2015. Understanding the oil price–macroeconomy relationship: The role of asymmetries for US real GDP. Energy Economics 52: 77–93. [Google Scholar]

- Baumeister, Christiane, and Lutz Kilian. 2016. Forty Years of Oil Price Fluctuations: Why the Price of Oil May Still Surprise Us. Journal of Economic Perspectives 30: 139–60. [Google Scholar] [CrossRef]

- Bauwens, Luc, Sébastien Laurent, and Jeroen V. K. Rombouts. 2006. Multivariate GARCH models: A survey. Journal of Applied Econometrics 21: 79–109. [Google Scholar] [CrossRef]

- Becken, Susanne, and James Lennox. 2012. Implications of a long-term increase in oil prices for tourism. Tourism Management 33: 133–42. [Google Scholar] [CrossRef]

- Bergareche, Juan Carpizo. 2019. Regional and Local Energy Taxation: Problems and Possible Solutions. Studies on the Spanish Economy. Madrid: FEDEA, p. 21. [Google Scholar]

- Bialkowski, Jedrzej. 2004. Modelling returns on stock indices for western and central European stock exchanges—A Markov switching approach. South-Eastern Europe Journal of Economics 2: 81–100. Available online: http://www.asecu.gr/Seeje/issue03/bialkowski.pdf (accessed on 12 February 2024).

- Bollerslev, Tim. 1986. Generalized autoregressive conditional heteroskedasticity. Journal of Econometrics 31: 307–27. [Google Scholar] [CrossRef]

- Braun, M., Michael Kvasnicka, and M. Schmidt. 2019. Movin’up to the east side: Oil and gas extraction and intraregional migration in Russia. Journal of Development Economics 139: 165–86. [Google Scholar]

- Brown, Stephen P. A., and Mine K. Yücel. 2002. Energy Prices and Aggregate Economic Activity: An Interpretative Survey. Quarterly Review of Economics and Finance 42: 193–208. [Google Scholar] [CrossRef]

- Burbridge, John, and Alan Harrison. 1984. Testing for the effects of oil price rises using vector autoregressions. International Economic Review 25: 459–84. [Google Scholar] [CrossRef]

- Cai, Jun. 1994. A Markov Model of Switching-Regime ARCH. Journal of Business & Economic Statistics 12: 309–16. [Google Scholar]

- Camarero, Mariam, Josep Lluís Carrion-i-Silvestre, and Cecilio Tamarit. 2006. The relationship between oil prices, stock prices, and inflation: Evidence from Spain. International Journal of Finance & Economics 11: 175–88. [Google Scholar]

- Cantavella-Jordá, Manuel. 2020. Fluctuations of Oil Prices and Gross Domestic Product in Spain. International Journal of Energy Economics and Policy 10: 57–63. Available online: https://www.econjournals.com/index.php/ijeep/article/view/8806 (accessed on 23 December 2023).

- Carrion-i-Silvestre, Lluis, and Dukpa Kim. 2000. The dynamic relationship between stock prices and inflation: Evidence from Spain. Journal of Macroeconomics 22: 331–51. [Google Scholar]

- Castro, César, Rebeca Jiménez-Rodríguez, Pilar Poncela, and Eva Senra. 2017. A new look at oil prices passes through into inflation: Evidence from disaggregated European data. Journal of Analytical and Institutional Economics 34: 55–82. [Google Scholar]

- Chen, Shiu-Sheng, and Hung-Chyn Chen. 2007. Oil prices and real exchange rates. Energy Economics 29: 390–404. [Google Scholar] [CrossRef]

- Cheratian, Iman, Mohammad Reza Farzanegan, and Saleh Goltabar. 2019. Oil Price Shocks and Unemployment Rate: New Evidence from the MENA Region. MAGKS Papers on Economics 201931. Marburg: Philipps-Universität Marburg. [Google Scholar]

- Chkili, Walid, and Duc Khuong Nguyen. 2017. Stock returns and oil price changes in France: A multiscale analysis using wavelets. Energy Economics 64: 568–77. [Google Scholar]

- Cologni, Alessandro, and Matteo Manera. 2008. Oil prices, inflation, and interest rates in a structural cointegrated VAR model for the G-7 countries. Energy Economics 30: 856–88. [Google Scholar] [CrossRef]

- Cunado, Juncal, and F. Perez de Gracia. 2005. Oil prices, economic activity, and inflation: Evidence for some Asian countries. Quarterly Review of Economics and Finance 45: 65–83. [Google Scholar] [CrossRef]

- Cunado, Juncal, and Fernando Pérez de Gracia. 2003. Do oil price shocks matter? Evidence for some European countries. Energy Economics 25: 137–54. [Google Scholar] [CrossRef]

- De Blas, Beatriz, and Katheryn Russ. 2015. The macroeconomic effects of oil price shocks in Spain: A SVAR approach. Energy Economics 51: 599–612. [Google Scholar]

- Del Rio, Pablo, and Jiménez Rodríguez-López. 2016. The relationship between oil price shocks and stock market: Evidence from Spain. International Journal of Energy Economics and Policy 6: 477–83. [Google Scholar]

- de Miguel, Carlos, Baltasar Manzano, and Jose M. Martin-Moreno. 2003. Oil price shocks and aggregate fluctuations. The Energy Journal 24: 47–61. [Google Scholar] [CrossRef]

- Engle, Robert F. 1982. Autoregressive Conditional Heteroscedasticity with Estimates of the Variance of United Kingdom Inflation. Econometrica 50: 987–1007. [Google Scholar] [CrossRef]

- Ewing, Bradley, and Mark A. Thompson. 2007. The impact of oil price shocks on the term structure of stock returns. The Quarterly Review of Economics and Finance 47: 582–95. [Google Scholar]

- Fahrmeir, Ludwig, Thomas Kneib, Stefan Lang, and Brian Marx. 2010. Regression: Models, Methods, and Applications. Berlin/Heidelberg: Springer. [Google Scholar]

- Fan, Ying, Yue-Jun Zhang, Hsien-Tang Tsai, and Yi-Ming Wei. 2008. Estimating ‘Value at Risk’ of crude oil price and its spillover effect using the GED-GARCH approach. Energy Economics 30: 3156–71. [Google Scholar] [CrossRef]

- Ferderer, J. Peter. 1996. Oil price volatility and the macroeconomy. Journal of Macroeconomics 18: 1–26. [Google Scholar] [CrossRef]

- Franses, Philip Hans, and Dick Van Dijk. 1996. Forecasting stock market volatility using (non-linear) Garch models. Journal of Forecasting 15: 229–335. [Google Scholar] [CrossRef]

- Frommel, Michael. 2010. Volatility regimes in Central and Eastern European countries’ exchange rates. Czech Journal of Economics and Finance 60: 2–21. Available online: https://journal.fsv.cuni.cz/storage/1177_1177_str_2 (accessed on 24 December 2023).

- Gelman, Andrew. 2004. Bayesian Data Analysis, 2nd ed. Boca Raton: Chapman and Hall/CRC. [Google Scholar]

- Gisser, Micha, and Thomas H. Goodwin. 1986. Crude oil and the macroeconomy: Tests of some popular notions. Journal of Money, Credit and Banking 18: 95–103. [Google Scholar] [CrossRef]

- Glosten, Lawrence R., Ravi Jagannathan, and David E. Runkle. 1993. On the Relation between the Expected Value and the Volatility of the Nominal Excess Return on Stocks. The Journal of Finance 48: 1779–801. [Google Scholar] [CrossRef]

- Gormus, N. Alper, and Ugur Soytas. 2020. Oil price shocks, stock market, and inflation in the Eurozone. Energy & Environment 31: 1353–75. [Google Scholar]

- Gómez-Loscos, Ana, Antonio Montañés, and M. Dolores Gadea. 2011. The Impact of Oil Shocks on The Spanish Economy. Occasional Papers 1914. Madrid: Bank of Spain. [Google Scholar]

- Guo, Hui, and Kevin L. Kliesen. 2005. Oil price volatility and U. S. macroeconomic activity. Review-Federal Reserve Bank of St. Louis 57: 669–83. [Google Scholar] [CrossRef]

- Güntner, Jochen H. F. 2014. How do oil producers respond to oil demand shocks? Energy Economics 44: 1–13. [Google Scholar] [CrossRef]

- Haas, Markus, Stefan Mittnik, and Marc S. Paolella. 2004. A new approach to Markov-switching GARCH models. Journal of Financial Econometrics 2: 493–530. [Google Scholar] [CrossRef]

- Haas, Markus, and Marc S. Paolella. 2012. Mixture and regime-switching GARCH models. In Handbook of Volatility Models and Their Applications. Edited by Luc Bauwens, Christian Hafner and Sebastien Laurent. Hoboken: John Wiley & Sons, pp. 71–102. [Google Scholar] [CrossRef]

- Hamilton, James D. 1983. Oil and the Macroeconomy since World War II. Journal of Political Economy 91: 228–48. [Google Scholar] [CrossRef]

- Hamilton, James D. 1988. Rational expectations econometric analysis of changes in regime: An investigation of the term structure of interest rates. Journal of Economic Dynamics and Control 12: 385–423. [Google Scholar] [CrossRef]

- Hamilton, James D. 1994. Time Series Analysis. Princeton: Princeton University Press. [Google Scholar]

- Hamilton, James D. 2008. Oil and the Macroeconomy. In The New Palgrave Dictionary of Economics: Palgrave Macmillan. Edited by Steven N. Durlauf and Lawrence E. Blume. London: Palgrave Macmillan. [Google Scholar]

- Hooker, Mark A. 1996. What Happened to the Oil Price-Macroeconomy Relationship? Journal of Monetary Economics 38: 195–213. [Google Scholar] [CrossRef]

- Hou, Aijun, and Sandy Suardi. 2012. A nonparametric GARCH model of crude oil price return volatility. Energy Economics 34: 618–26. [Google Scholar] [CrossRef]

- Huang, Bwo-Nung, M. J. Hwang, and Hsiao-Ping Peng. 2005. The asymmetry of the impact of oil price shocks on economic activities: An application of the multivariate threshold model. Energy Economics 27: 455–76. [Google Scholar] [CrossRef]

- Hung, Jui-Cheng, Ming-Chih Lee, and Hung-Chun Liu. 2008. Estimation of Value-at-Risk for Energy Commodities via Fat-Tailed GARCH Models. Energy Economics 30: 1173–91. [Google Scholar] [CrossRef]

- Huntington, Hillard G. 2007. Oil shocks and real U.S. income. The Energy Journal 28: 31–46. [Google Scholar] [CrossRef]

- IEA. 2020. World Energy Outlook 2020. Paris: IEA, Licence: CC BY 4.0. Available online: https://www.iea.org/reports/world-energy-outlook-2020 (accessed on 14 January 2024).

- IMF (International Monetary Fund). 2016. World Economic Outlook: Too Slow for Too Long. Washington, DC: International Monetary Fund. [Google Scholar]

- Jimenez-Rodriguez, Rebeca. 2009. Oil price shocks and real GDP growth: Testing for non-linearity. The Energy Journal 30: 1–23. [Google Scholar] [CrossRef]

- Jimenez-Rodriguez, Rebeca, and Marcelo Sanchez. 2005. Oil price shocks and real GDP growth: Empirical evidence for some OECD countries. Applied Economics 37: 201–28. [Google Scholar] [CrossRef]

- Kang, Sang Hoon, Sang-Mok Kang, and Seong-Min Yoon. 2009. Forecasting volatility of crude oil markets. Energy Economics 31: 119–25. [Google Scholar] [CrossRef]

- Kanjilal, Kakali, and Sajal Ghosh. 2017. Dynamics of crude oil and gold price post 2008 global financial crisis—New evidence from threshold vector error-correction model. Resources Policy 52: 358–65. [Google Scholar] [CrossRef]

- Katsampoxakis, Ioannis, Apostolos Christopoulos, Petros Kalantonis, and Vasileios Nastas. 2022. Crude oil price shocks and European stock markets during the COVID-19 period. Energies 15: 4090. [Google Scholar] [CrossRef]

- Kilian, Lutz. 2009. Not all oil price shocks are alike: Disentangling demand and supply shocks in the crude oil market. American Economic Review 99: 1053–69. [Google Scholar] [CrossRef]

- Kilian, Lutz, and Robert Vigfusson. 2011. Are the Responses of the U.S. Economy Asymmetric in Energy Price Increases and Decreases? Quantitative Economics 2: 419–53. [Google Scholar] [CrossRef]

- Kitous, Alban, Bert Saveyn, Kimon Keramidas, Toon Vandyck, Luis Rey Los Santos, and Krzysztof Wojtowicz. 2016. Impact of Low Oil Prices on Oil Exporting Countries. EUR 27909. Luxembourg: Publications Office of the European Union, JRC101562. [Google Scholar]

- Klaassen, Franc. 2002. Improving GARCH volatility forecasts with regime-switching GARCH. International Journal of Forecasting 27: 363–94. [Google Scholar]

- Koirala, Niraj Prasad, and Xiaohan Ma. 2020. Oil price uncertainty and U.S. employment growth. Energy Economics 91: 104910. [Google Scholar] [CrossRef]

- Lamoureux, Christopher G., and William D. Lastrapes. 1990. Heteroskedasticity in Stock Return Data: Volume versus GARCH Effects. Journal of Finance 45: 221–29. [Google Scholar]

- Lardic, Sandrine, and Valerie Mignon. 2006. The impact of oil prices on GDP in European countries: An empirical investigation based on asymmetrical cointegration. Energy Policy 34: 3910–15. [Google Scholar] [CrossRef]

- Lee, Kiseok, Shawn Ni, and Ronald A. Ratti. 1995. Oil shocks and the macroeconomy: The role of price variability. The Energy Journal 16: 39–56. [Google Scholar] [CrossRef]

- Lescaroux, François, and Valérie Mignon. 2008. On the Influence of Oil Prices on Economic Activity and Other Macroeconomic and Financial Variables. Working Papers from CEPII research center. Paris: CEPII Research Center. [Google Scholar]

- Linne, Thomas. 2002. A Markov switching model of stock returns: An application to the emerging markets in Central and Eastern Europe. In East European Transition and EU Enlargement. Edited by Wojciech W. Charemza and Krystyna Strzała. Heidelberg: Physica, pp. 371–84. [Google Scholar] [CrossRef] [PubMed]

- Litzenberger, Robert H., and Nir Rabinowitz. 1995. Backwardation in oil futures markets: Theory and empirical evidence. The Journal of Finance 50: 1517–45. [Google Scholar] [CrossRef]

- Liu, Ming-Lei, Qiang Ji, and Ying Fan. 2013. How Does Oil Market Uncertainty Interact with Other Markets? An Empirical Analysis of Implied Volatility Index. Energy 55: 860–68. [Google Scholar] [CrossRef]

- Manera, Matteo, Chiara Longo, Anil Markandya, and Elisa Scarpa. 2007. Evaluating the Empirical Performance of Alternative Econometric Models for Oil Price Forecasting. FEEM Fondazione Eni Enrico Mattei Research Paper Series [Working Paper] (4), 1–49. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=958942# (accessed on 4 January 2024).

- Marcucci, Juri. 2005. Forecasting stock market volatility with regime-switching GARCH Models. Studies in Nonlinear Dynamics & Econometrics 9: 1–55. [Google Scholar] [CrossRef]

- Mohammadi, Hassan, and Lixian Su. 2010. International evidence on crude oil price dynamics: Applications of ARIMA-GARCH models. Energy Economics 32: 1001–1008. [Google Scholar]

- Mohd, Atif, Mustafa Raza Rabbani, Hana Bawazir, and Iqbal Thonse Hawaldar. 2022. Oil price changes and stock returns: Fresh evidence from oil exporting and oil importing countries. Cogent Economics & Finance 10: 2018163. [Google Scholar] [CrossRef]

- Moore, Tomoe, and Ping Wang. 2007. Volatility in stock returns for new EU member states: Markov regime switching model. International Review of Financial Analysis 16: 282–92. [Google Scholar] [CrossRef]

- Mork, Knut Anton, and Olstein Olsen. 1994. Macroeconomic responses to oil price increases and decreases in seven OECD countries. Energy Journal 15: 19–35. [Google Scholar] [CrossRef]

- Muşetescu, Radu-Cristian, George-Eduard Grigore, and Simona Nicolae. 2022. The Use of GARCH Autoregressive Models in Estimating and Forecasting the Crude Oil Volatility. European Journal of Interdisciplinary Studies 14: 13–38. [Google Scholar] [CrossRef]

- Nelson, Daniel B. 1991. Conditional heteroskedasticity in asset returns: A new approach. Econometrica 59: 347–70. [Google Scholar] [CrossRef]

- Ordóñez, Javier, Mercedes Monfort, and Juan Carlos Cuestas. 2019. Oil prices, unemployment, and the financial crisis in oil-importing countries: The case of Spain. Energy 181: 625–34. [Google Scholar] [CrossRef]

- Pérez-Quiros, Gabriel, and Allan Timmermann. 2000. Business conditions and asset returns. The Quarterly Journal of Economics 115: 161–201. [Google Scholar]

- Raihan, Tasneem. 2017. Performance of Markov-Switching GARCH Model Forecasting Inflation Uncertainty (MPRA Paper No. 82343). Available online: https://mpra.ub.uni-muenchen.de/82343/1/MPRA_paper_82343.pdf (accessed on 8 February 2021).

- Robays, Ine Van. 2012. Macroeconomic Uncertainty and the Impact of Oil Shocks. Working Paper Series, NO 1479. Available online: https://www.ecb.europa.eu/pub/pdf/scpwps/ecbwp1479.pdf (accessed on 15 February 2024).

- Rodríguez-Zúñiga, J., M. Sánchez, and D. León. 2019. Effects of oil price shocks on Spanish macroeconomic variables. International Journal of Energy Economics and Policy 9: 376–84. [Google Scholar]

- Rotta, Pedro Nielsen, and Pedro L. Valls Pereira. 2016. Analysis of contagion from the dynamic conditional correlation model with Markov Regime switching. Applied Economics 48: 2367–82. [Google Scholar] [CrossRef]

- Sadorsky, Perry. 1999. Oil price shocks and stock market activity. Energy Economics 21: 449–69. [Google Scholar] [CrossRef]

- Sekati, Boitumelo Nnoi Yolanda, Johannes Tshepiso Tsoku, Lebotsa Daniel Metsileng, and Damir Tokic. 2020. Modelling the oil price volatility and macroeconomic variables in South Africa using the symmetric and asymmetric GARCH models. Cogent Economics & Finance 8: 1792153. [Google Scholar]

- Serletis, Apostolos, and John Elder. 2011. Introduction To Oil Price Shocks. Macroeconomic Dynamics 15: 327–36. [Google Scholar] [CrossRef]

- Szczygielski, Jan Jakub, and Chimwemwe Chipeta. 2023. Properties of returns and variance and implications for time series modeling: Evidence from South Africa. Modern Finance 1: 35–55. [Google Scholar] [CrossRef]

- Tiwari, Aviral Kumar, Arif Billah Dar, and Niyati Bhanja. 2013. Oil price and exchange rates: A wavelet based analysis for India. Economic Modelling 31: 414–22. [Google Scholar] [CrossRef]

- Topan, Ligia, César Castro, Miguel Jerez, and Andrés Barge-Gil. 2020. Oil price pass-through into inflation in Spain at national and regional level. Journal of the Spanish Economic Association 11: 561–83. [Google Scholar] [CrossRef] [PubMed]

- Tuna, Vedat Ender, Gülfen Tuna, and Nurcan Kostak. 2021. The effect of oil market shocks on the stock markets: Time-varying asymmetric causal relationship for conventional and Islamic stock markets. Energy Reports 7: 2759–74. [Google Scholar] [CrossRef]

- van Eyden, Renee, Mamothoana Difeto, Rangan Gupta, and Mark Wohar. 2019. Oil price volatility and economic growth: Evidence from advanced economies using more than a century’s data. Applied Energy 233–34: 612–21. [Google Scholar] [CrossRef]

- Van Robays, Ine. 2016. Macroeconomic Uncertainty and Oil Price Volatility. Oxford Bulletin of Economics and Statistics 78: 671–93. [Google Scholar] [CrossRef]

- Wacuka Ng’ang’a, Faith, and Meleah Oleche. 2022. Modelling and Forecasting of Crude Oil Price Volatility Comparative Analysis of Volatility Models. Journal of Financial Risk Management 11: 154–87. [Google Scholar] [CrossRef]

- Wang, Jun, Huopo Pan, and Fajiang Liu. 2012. Forecasting Crude Oil Price and Stock Price by Jump Stochastic Time Effective Neural Network Model. Journal of Applied Mathematics 2012: 646475. [Google Scholar] [CrossRef]

- Wang, Yudong, and Chongfeng Wu. 2012. Forecasting energy market volatility using GARCH models: Can multivariate models beat univariate models? Energy Economics 34: 2167–81. [Google Scholar] [CrossRef]

- Westfall, Peter. 2014. Adequacy of normal approximation for the t distribution using formal and informal tests. Statistics in Medicine 33: 659–74. [Google Scholar]

- Zagaglia, Paolo. 2010. Macroeconomic factors and oil futures prices: A data-rich model. Energy Economics 32: 409–17. [Google Scholar] [CrossRef]

- Zakoian, Jean-Michel. 1994. Threshold heteroskedastic models. Journal of Economic Dynamics and Control 18: 931–55. [Google Scholar] [CrossRef]

- Zhang, Hai-Ying, Qiang Ji, and Ying Fan. 2015. What drives the formation of global oil trade patterns? Energy Economics 49: 639–48. [Google Scholar] [CrossRef]

- Zhang, Yue-Jun, and Jing Wang. 2015. Exploring the WTI crude oil price bubble process using the Markov regime switching model. Physica A: Statistical Mechanics and its Applications 421: 377–87. [Google Scholar] [CrossRef]

- Zhang, Qin, and Jin Boon Wong. 2023. The influence of oil price uncertainty on stock liquidity. Futures Markets 43: 141–67. [Google Scholar] [CrossRef]

- Zhang, Yue-Jun, and Lu Zhang. 2015. Interpreting the crude oil price movements: Evidence from the Markov regime switching model. Applied Energy 143: 96–109. [Google Scholar] [CrossRef]

- Živkov, Dejan, and Jasmina Đurašković. 2021. How does oil price uncertainty affect output in the Central and Eastern European economies?—The Bayesian-based approaches. Central and Eastern European Economies 31: 39–54. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

| Coeff. | ||||||

|---|---|---|---|---|---|---|

| Linear GARCH model | ||||||

| 0.0008 * | 0.0003 *** | 0.0001 *** | 0.0029 * | 0.0010 | 0.0041 | |

| 0.2980 * | 0.4600 *** | 0.2239 * | 0.1712 *** | 0.0157 | 0.1063 | |

| 0.4400 | 0.3340 *** | 0.7516 *** | 0.7560 | 0.8440 * | 0.7760 | |

| 4.5001 ** | 5.6134 ** | 7.8480 ** | 3.7255 ** | 5.7716 ** | 11.6300 ** | |

| + | 0.7380 | 0.7940 | 0.9755 | 0.9272 | 0.8597 | 0.8823 |

| 53.6581 | 143.5620 | 119.083 | 81.8467 | 114.7021 | 86.0331 | |

| 0.0534 | 0.0357 | 0.0765 | 0.0730 | 0.0840 | 0.1059 | |

| Non-linear GJR-GARCH model | ||||||

| 0.0013 * | 0.0004 *** | 0.0003 *** | 0.0026 *** | 0.0029 ** | 0.0045 * | |

| 0.1316 * | 0.1887 ** | 0.1778 *** | 0.1950 *** | 0.2380 * | 0.1334 *** | |

| 0.7646 * | 0.8323 *** | 0.6120 * | 0.2591 *** | 0.4213 * | 0.1407 ** | |

| 0.2433 *** | 0.3878 *** | 0.5017 *** | 0.6071 *** | 0.5199 *** | 0.7221 *** | |

| 4.7010 *** | 5.8810 * | 5.5539 ** | 3.9280 ** | 6.6822 ** | 10.4376 ** | |

| + | 0.7585 | 0.9931 | 0.9858 | 0.9343 | 0.9715 | 0.9304 |

| 61.2484 | 230.0170 | 192.8820 | 86.5688 | 124.9110 | 94.8700 | |

| 0.0554 | 0.0340 | 0.0535 | 0.0587 | 0.0663 | 0.1103 | |

| Coeff | ||||||

|---|---|---|---|---|---|---|

| Regime 1—low-volatility regime | ||||||

| 0.0264 ** | 0.0916 *** | 0.0451 | 0.0143 | 0.0120 ** | 1.3900 *** | |

| 0.2526 ** | 0.7640 *** | 0.8282 ** | 0.1451 *** | 0.2744 ** | 0.1846 *** | |

| 0.2321 *** | 0.3730 *** | 0.3020 *** | 0.6282 *** | 0.3050 ** | 0.7305 *** | |

| + | 0.4840 | 0.7369 | 0.9201 | 0.7729 | 0.0304 | 0.5461 |

| Regime 2—high-volatility regime | ||||||

| 0.0061 | 0.0121 *** | 0.0107 ** | 0.0125 ** | 0.0253 ** | 0.0040 *** | |

| 0.0538 *** | 0.1336 *** | 0.1994 ** | 0.4106 *** | 0.1474 *** | 0.1933 *** | |

| 0.3970 *** | 0.3781 *** | 0.3211 *** | 0.2670 *** | 0.2390 *** | 0.6620 *** | |

| + | 0.4507 | 0.2446 | 0.5205 | 0.6767 | 0.3864 | 0.8550 |

| 18.1892 *** | 17.937 *** | 14.7865 *** | 18.7617 *** | 13.5570 *** | 12.4000 *** | |

| 0.9213 *** | 0.9464 *** | 0.7780 *** | 0.9031 *** | 0.6610 *** | 0.9850 *** | |

| 0.0788 *** | 0.1879 ** | 0.0164 ** | 0.0244 *** | 0.4720 ** | 0.0307 | |

| 64.8973 | 249.1149 | 194.0167 | 75.3913 | 127.2704 | 90.4500 | |

| 0.0510 | 0.0743 | 0.0214 | 0.0628 | 0.02050 | 0.0560 | |

| 0.0110 | 0.0248 | 0.0223 | 0.0385 | 0.0412 | 0.0867 | |

| 0.0788 | 0.0621 | 0.1847 | 0.0904 | 0.3911 | 0.0154 | |

| 0.9212 | 0.9380 | 0.8154 | 0.9101 | 0.6101 | 0.9847 | |

| 3.5823 | 1.2312 | 4.4890 | 10.3117 | 1.8786 | 31.5954 | |

| 12.7035 | 17.6253 | 61.3103 | 41.1651 | 2.9471 | 66.3019 | |

| Coeff | ||||||

|---|---|---|---|---|---|---|

| Regime 1—low-volatility regime | ||||||

| 0.0019 *** | 0.0016 *** | 0.0020 *** | 0.0021 ** | 0.0028 * | 0.0016 *** | |

| 0.0061 *** | 0.2544 *** | 0.2967 *** | 0.2160 ** | 0.2770 * | 0.1315 *** | |

| 0.9653 *** | 0.1830 *** | 0.2538 ** | 0.2918 ** | 0.5871 * | 0.8983 ** | |

| 0.4515 *** | 0.4034 *** | 0.3861 ** | 0.4624 ** | 0.3310 *** | 0.3595 ** | |

| + | 0.9412 | 0.7494 | 0.8096 | 0.8239 | 0.8967 | 0.9401 |

| Regime 2—high-volatility regime | ||||||

| 0.0034 *** | 0.0011 *** | 0.0015 *** | 0.0010 | 0.0008 | 0.0002 *** | |

| 0.020 *** | 0.0874 *** | 0.1110 *** | 0.2576 *** | 0.2826 * | 0.1670 *** | |

| 0.8940 *** | 0.7604 *** | 0.8378 *** | 0.6164 *** | 0.7041 ** | 0.8842 *** | |

| 0.5031 *** | 0.3732 *** | 0.2701 *** | 0.2667 *** | 0.2427*** | 0.3610 *** | |

| + | 0.9700 | 0.8409 | 0.8003 | 0.8324 | 0.8784 | 0.9701 |

| 19.4941 *** | 18.9141 *** | 4.3156 *** | 6.6687 *** | 15.2694 *** | 15.5394 *** | |

| 0.9252 *** | 0.9889 *** | 0.8932 *** | 0.8961 *** | 0.9057 *** | 0.980 *** | |

| 0.4531 *** | 0.2970 *** | 0.2012 | 0.0266 | 0.4323 *** | 0.1021 ** | |

| 397.3161 | 252.8515 | 137.6488 | 76.0090 | 132.0958 | 249.7012 | |

| 0.0751 | 0.0795 | 0.0519 | 0.0660 | 0.0634 | 0.0619 | |

| 0.0347 | 0.0826 | 0.0861 | 0.0753 | 0.0826 | 0.0819 | |

| 0.1205 | 0.0156 | 0.1180 | 0. 9035 | 0.1425 | 0.9781 | |

| 0.8801 | 0.9843 | 0.8812 | 0. 0965 | 0.8756 | 0.0211 | |

| 2.2074 | 3.3674 | 4.9720 | 9.6160 | 1.1012 | 48.6046 | |

| 14.5468 | 9.7710 | 9.3715 | 7.6871 | 1.6715 | 10.8039 | |

| MS-GARCH Model | ||||||

| 2024Q1 | 0.0346 | 0.0254 | 0.0041 | 0.0159 | 0.0255 | 0.0247 |

| 2024Q2 | 0.0366 | 0.0190 | 0.0039 | 0.0145 | 0.0265 | 0.0387 |

| 2024Q3 | 0.0323 | 0.0148 | 0.0022 | 0.0041 | 0.0286 | 0.0341 |

| 2024Q4 | 0.0321 | 0.0151 | 0.0016 | 0.0052 | 0.0308 | 0.0376 |

| 2025Q1 | 0.0316 | 0.0159 | 0.0013 | 0.0069 | 0.0372 | 0.0421 |

| MS-GJR-GARCH Model | ||||||

| 2024Q1 | 0.0368 | 0.0113 | 0.0069 | 0.0304 | 0.0234 | 0.0335 |

| 2024Q2 | 0.0318 | 0.0217 | 0.0057 | 0.0412 | 0.0217 | 0.0424 |

| 2024Q3 | 0.0331 | 0.0180 | 0.0095 | 0.0303 | 0.0249 | 0.0461 |

| 2024Q4 | 0.0315 | 0.0152 | 0.0064 | 0.0241 | 0.0250 | 0.0411 |

| 2025Q1 | 0.0286 | 0.0136 | 0.0049 | 0.0135 | 0.0254 | 0.0335 |

| Single-regime GARCH-type Models | ||||||

| Model | GARCH | GARCH | GJR-GARCH | GARCH | GARCH | GJR-GARCH |

| SIC | −0.7476 | −3.9610 | −3.1664 | −1.1975 | −1.8901 | 1.9498 |

| AIC | −0.8689 | −4.0822 | −3.2525 | −1.3423 | −2.0128 | 1.8042 |

| RMSE | 0.1556 | 0.0445 | 0.0550 | 0.2652 | 0.0850 | 1.2730 |

| MAPE | 0.1124 | 0.0380 | 0.0396 | 0.1455 | 0.0637 | 1.1208 |

| Double-regime GARCH-type Models | ||||||

| Model | MS-GARCH | MS-GARCH | MS-GJR-GARCH | MS-GARCH | MS-GARCH | MS-GJR-GARCH |

| SIC | −0.7970 | −4.0325 | −3.7340 | −1.2990 | −1.9774 | 1.7028 |

| AIC | −0.8952 | −4.1773 | −3.8871 | −1.4441 | −2.1221 | 1.6319 |

| RMSE | 0.1506 | 0.0411 | 0.0528 | 0.2556 | 0.0812 | 1.2545 |

| MAPE | 0.1102 | 0.0340 | 0.0350 | 0.1436 | 0.0613 | 1.1131 |

| Variables | Short-Term | Long-Term | ||

|---|---|---|---|---|

| Regime 1 | Regime 2 | Regime 1 | Regime 2 | |

| −0.4414 | −0.6423 | −2.1203 * | −1.3302 ** | |

| 0.0821 | 0.3439 | 0.8214 ** | 0.7955 ** | |

| −0.1160 | −0.3442 | −1.0810 ** | −1.2271 ** | |

| −0.0562 * | −0.2764 ** | −0.5438 * | −0.6101 * | |

| 0.0504 ** | 0.0614 ** | 1.6423 * | 2.0034 * | |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Aladwani, J. Oil Volatility Uncertainty: Impact on Fundamental Macroeconomics and the Stock Index. Economies 2024, 12, 140. https://doi.org/10.3390/economies12060140

Aladwani J. Oil Volatility Uncertainty: Impact on Fundamental Macroeconomics and the Stock Index. Economies. 2024; 12(6):140. https://doi.org/10.3390/economies12060140

Chicago/Turabian StyleAladwani, Jassim. 2024. "Oil Volatility Uncertainty: Impact on Fundamental Macroeconomics and the Stock Index" Economies 12, no. 6: 140. https://doi.org/10.3390/economies12060140

APA StyleAladwani, J. (2024). Oil Volatility Uncertainty: Impact on Fundamental Macroeconomics and the Stock Index. Economies, 12(6), 140. https://doi.org/10.3390/economies12060140