Tax Complexity and Firm Tax Evasion: A Cross-Country Investigation

, ,

, ,  ,

,

Abstract

1. Introduction

2. Literature Review

3. Data and Sample

3.1. Measuring Tax Evasion

3.2. Measuring Tax Complexity

3.3. Control Variables

3.4. Sample Selection

4. Econometric Model

5. Results

5.1. Baseline Results

5.2. Endogeneity Concerns

5.3. Robustness Test

5.4. Additional Analysis

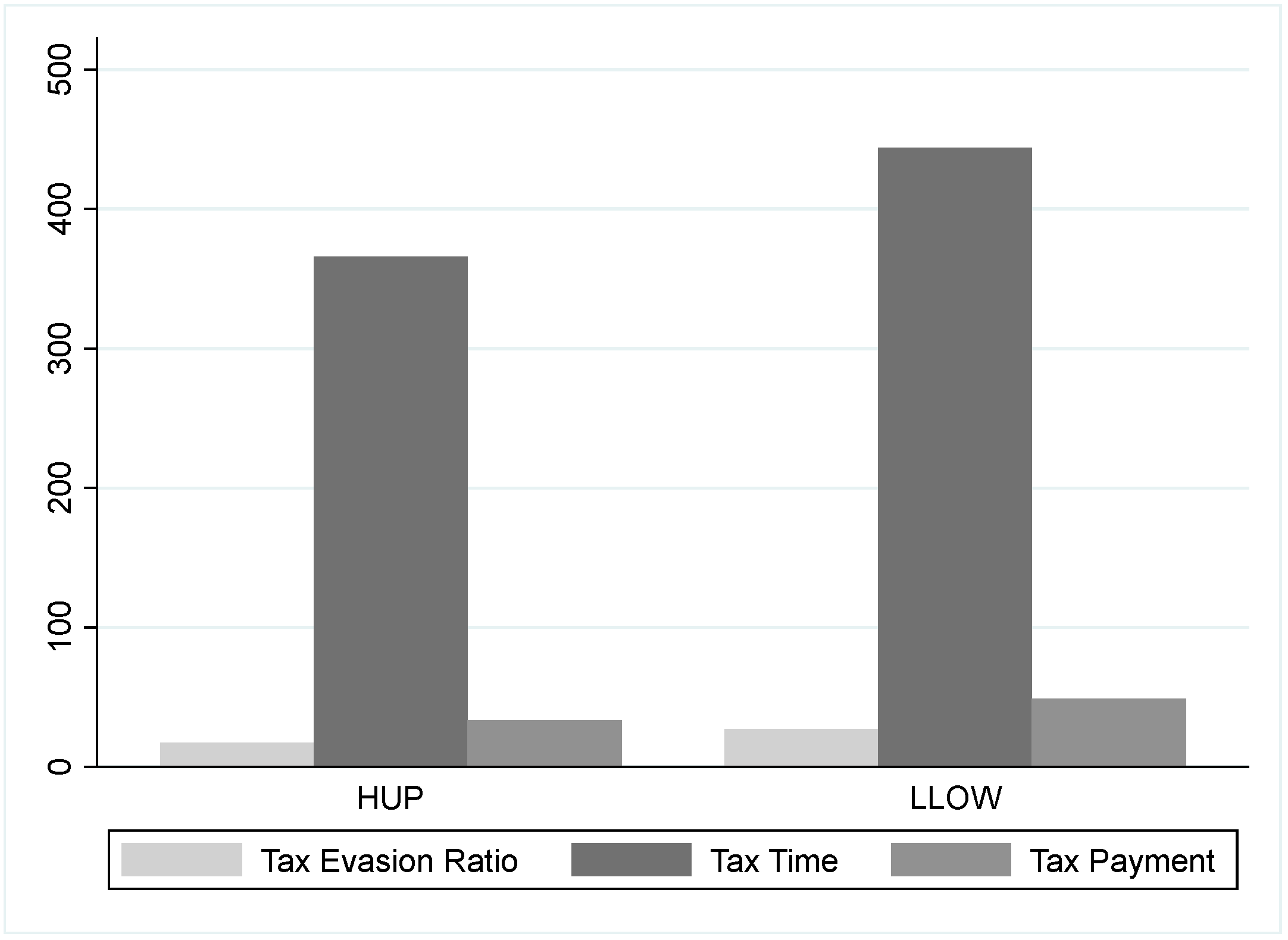

5.4.1. Country Heterogeneity Analysis

5.4.2. Industry Heterogeneity Analysis

5.4.3. Spatial Analysis

6. Conclusions

Author Contributions

Funding

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

| Variable | Definition | Database |

|---|---|---|

| Tax evasion ratio | Unreported sales tax. | WBES, the World Bank |

| Tax evasion dummy | The value is equal to one if the ratio of tax evasion is more than zero; otherwise, it is equal to zero. | WBES, the World Bank |

| Log of tax time | Log of the duration required for tax preparation and payment. | WBDB, the World Bank |

| Log of tax payment | Log of the aggregate quantity of taxes paid by firms, including the use of electronic filing methods. | WBDB, the World Bank |

| Log of GDP | Log of real GDP per capita, which is measured in terms of 2015 USD. | WDI, the World Bank |

| Inflation | The yearly growth rate of the ratio between the GDP measured in current local currency and the GDP measured in constant local currency. | WDI, the World Bank |

| Unemployment | The proportion of the labour force that is actively seeking employment but currently without a job. | WDI, the World Bank |

| Agriculture | The contribution of agriculture, forestry, and fisheries to the GDP in terms of value added. | WDI, the World Bank |

| Tax burden | The tax liability imposed by the governing authorities. A higher value (0–1) implies a heavier tax burden and vice versa. | Index of Economic Freedom, the Heritage Foundation |

| Age | The percentage of the population in the age range of 15 to 24 who are engaged in economic activities. | Population Estimates and Projections, the World Bank |

| Gender | The percentage of female labour. | Gender Statistics, the World Bank |

| Voice and accountability | The perceptions of the public participation level in government selection. A higher value (−2.5–2.5) implies a better institutional quality. | WGI, the World Bank |

| Political stability | The perceptions on the probability of encountering political instability and politically motivated violence. A higher value (−2.5–2.5) implies a better institutional quality. | WGI, the World Bank |

| Government effectiveness | The perceptions pertain to several aspects of public services. A higher value (−2.5–2.5) implies a better institutional quality. | WGI, the World Bank |

| Regulatory quality | The perceptions on the government’s capacity to effectively devise and execute well-founded policies and regulations that facilitate and advance the growth of the private sector. A higher value (−2.5–2.5) implies a better institutional quality. | WGI, the World Bank |

| Rule of law | The perceptions of the degree to which individuals exhibit trust and compliance with societal norms. A higher value (−2.5–2.5) implies a better institutional quality. | WGI, the World Bank |

| Control of corruption | The perceptions on the degree to which public authority is used for personal benefit. A higher value (−2.5–2.5) implies a better institutional quality. | WGI, the World Bank |

References

- Abdixhiku, Lumir, Geoff Pugh, and Iraj Hashi. 2018. Business tax evasion in transition economies: A cross-country panel investigation. European Journal of Comparative Economics 15: 11–36. [Google Scholar]

- Acemoglu, Daron, and Simon Johnson. 2005. Unbundling institutions. Journal of Political Economy 113: 949–95. [Google Scholar] [CrossRef]

- Acosta-Ormaechea, Santiago, Sergio Sola, and Jiae Yoo. 2019. Tax composition and growth: A broad cross-country perspective. German Economic Review 20: e70–e106. [Google Scholar] [CrossRef]

- Ahamed, M. Mostak. 2016. Does inclusive financial development matter for firms’ tax evasion? Evidence from developing countries. Economics Letters 149: 15–9. [Google Scholar] [CrossRef]

- Aldrich, John H., and Forrest D. Nelson. 1984. Linear Probability, Logit, and Probit Models. Newbury Park: Sage Publications. [Google Scholar]

- Alfaro, Laura, Alan Auerbach, Mauricio Cárdenas, Takatoshi Ito, Sebnem Kalemli-Özcan, and Justin Sandefur. 2021. Doing Business: External Panel Review: Final Report. Washington, DC: World Bank. [Google Scholar]

- Allam, Amir, Tantawy Moussa, Mona Abdelhady, and Ahmed Yamen. 2023. National culture and tax evasion: The role of the institutional environment quality. Journal of International Accounting, Auditing and Taxation 52: 100559. [Google Scholar] [CrossRef]

- Allingham, Michael G., and Agnar Sandmo. 1972. Income tax evasion: A theoretical analysis. Journal of Public Economics 1: 323–38. [Google Scholar] [CrossRef]

- Alm, James, Ali Enami, and Michael McKee. 2020. Who responds? Disentangling the effects of audits on individual tax compliance behavior. Atlantic Economic Journal 48: 147–59. [Google Scholar] [CrossRef]

- Alm, James, and Chandler McClellan. 2012. Tax morale and tax compliance from the firm’s perspective. Kyklos 65: 1–17. [Google Scholar] [CrossRef]

- Alm, James. 2012. Measuring, explaining, and controlling tax evasion: Lessons from theory, experiments, and field studies. International Tax and Public Finance 19: 54–77. [Google Scholar] [CrossRef]

- Alon, Anna, and Amy M. Hageman. 2013. The impact of corruption on firm tax compliance in transition economies: Whom do you trust? Journal of Business Ethics 116: 479–94. [Google Scholar] [CrossRef]

- Andreoni, James, Brian Erard, and Jonathan Feinstein. 1998. Tax compliance. Journal of Economic Literature 36: 818–60. [Google Scholar]

- Angrist, Joshua D., and Alan B. Krueger. 2001. Instrumental variables and the search for identification: From supply and demand to natural experiments. Journal of Economic Perspectives 15: 69–85. [Google Scholar] [CrossRef]

- Angrist, Joshua D., and Jörn-Steffen Pischke. 2008. Mostly Harmless Econometrics. Pinceton: Princeton University Press. [Google Scholar]

- Annan, Betty, William Bekoe, and Edward Nketiah-Amponsah. 2014. Determinants of tax evasion in Ghana: 1970–2010. International Journal of Economic Sciences and Applied Research 6: 97–121. [Google Scholar]

- Anselin, Luc. 1988. Spatial Econometrics: Methods And Models. Dordrecht: Springer Science and Business Media. [Google Scholar]

- Antonakis, John, Samuel Bendahan, Philippe Jacquart, and Rafael Lalive. 2010. On making causal claims: A review and recommendations. The Leadership Quarterly 21: 1086–120. [Google Scholar] [CrossRef]

- Arias, Roberto J. 2005. A Note on Indirect Tax Evasion. Buenos Aires: Asociacion Argentina de Economia Politica. [Google Scholar]

- Arif, Imtiaz, and Amna Sohail Rawat. 2018. Corruption, governance, and tax revenue: Evidence from EAGLE countries. Journal of Transnational Management 23: 119–33. [Google Scholar] [CrossRef]

- Avi-Yonah, Reuven S. 2004. International tax as tax law. Tax Law Review 57: 483. [Google Scholar]

- Awasthi, Rajul, and Nihal Bayraktar. 2015. Can tax simplification help lower tax corruption? Eurasian Economic Review 5: 297–330. [Google Scholar] [CrossRef]

- Ayyagari, Meghana, Asli Demirgüç-Kunt, and Vojislav Maksimovic. 2008. How well do institutional theories explain firms’ perceptions of property rights? The Review of Financial Studies 21: 1833–871. [Google Scholar]

- Baldry, Jonathan C. 1987. Income tax evasion and the tax schedule: Some experimental results. Public Finance=Finances Publiques 42: 357–83. [Google Scholar]

- Barber, Brad M., and Terrance Odean. 2001. Boys will be boys: Gender, overconfidence, and common stock investment. The Quarterly Journal of Economics 116: 261–92. [Google Scholar] [CrossRef]

- Baron, Jonathan, and Ilana Ritov. 2004. Omission bias, individual differences, and normality. Organizational Behavior and Human Decision Processes 94: 74–85. [Google Scholar] [CrossRef]

- Barrios, Salvador, Diego d’Andria, and Maria Gesualdo. 2020. Reducing tax compliance costs through corporate tax base harmonization in the European Union. Journal of International Accounting, Auditing and Taxation 41: 100355. [Google Scholar] [CrossRef]

- Barth, Erling, and Tone Ognedal. 2018. Tax evasion in firms. Labour 32: 23–44. [Google Scholar] [CrossRef]

- Barth, James R., Chen Lin, Ping Lin, and Frank M. Song. 2009. Corruption in bank lending to firms: Cross-country micro evidence on the beneficial role of competition and information sharing. Journal of Financial Economics 91: 361–88. [Google Scholar] [CrossRef]

- Basu, Kaushik. 2018. The ease of doing business comes with trade-offs. Brookings Institution. March 12. Available online: https://www.brookings.edu/opinions/the-ease-of-doing-business-comes-with-trade-offs/ (accessed on 14 April 2024).

- Beck, Thorsten, Asli Demirgüç-Kunt, and Vojislav Maksimovic. 2005. Financial and legal constraints to growth: Does firm size matter? The Journal of Finance 60: 137–77. [Google Scholar] [CrossRef]

- Beck, Thorsten, Chen Lin, and Yue Ma. 2014. Why do firms evade taxes? The role of information sharing and financial sector outreach. The Journal of Finance 68: 763–817. [Google Scholar] [CrossRef]

- Becker, Gary S. 1968. Crime and punishment: An economic approach. Journal of Political Economy 76: 169–217. [Google Scholar] [CrossRef]

- Bellemare, Charles, Marvin Deversi, and Florian Englmaier. 2019. Complexity and Distributive Fairness Interact in Affecting Compliance Behavior. CESifo Working Paper 7899. Munich: CESifo. [Google Scholar]

- Bergolo, Marcelo, Rodrigo Ceni, Guillermo Cruces, Matias Giaccobasso, and Ricardo Perez-Truglia. 2023. Tax audits as scarecrows: Evidence from a large-scale field experiment. American Economic Journal: Economic Policy 15: 110–53. [Google Scholar] [CrossRef]

- Berkel, Hanna, Christian Estmann, and John Rand. 2022. Local governance quality and law compliance: The case of Mozambican firms. World Development 157: 105942. [Google Scholar] [CrossRef]

- Besley, Timothy, and Torsten Persson. 2014. Why do developing countries tax so little? Journal of Economic Perspectives 28: 99–120. [Google Scholar] [CrossRef]

- Bittencourt, Manoel, Rangan Gupta, and Lardo Stander. 2014. Tax evasion, financial development and inflation: Theory and empirical evidence. Journal of Banking & Finance 41: 194–208. [Google Scholar]

- Blaufus, Kay, Frank Hechtner, and Janine K. Jarzembski. 2019. The income tax compliance costs of private households: Empirical evidence from Germany. Public Finance Review 47: 925–66. [Google Scholar] [CrossRef]

- Blesse, Sebastian. 2023. Do your tax problems make tax evasion seem more justifiable? Evidence from a survey experiment. European Journal of Political Economy 78: 102365. [Google Scholar] [CrossRef]

- Bliss, Chester I. 1934a. The method of probits. Science 79: 38–9. [Google Scholar] [CrossRef] [PubMed]

- Bliss, Chester I. 1934b. The method of probits—A correction. Science 79: 409–10. [Google Scholar] [CrossRef] [PubMed]

- Boame, Attah. 2009. Individual Tax Compliance: A Time-Series Regression Using Canadian Data, 1987–2003. Paper presented at International Conference on Institutional Taxation Analysis, London, UK, Septermber 21–22. [Google Scholar]

- Borrego, Ana Clara, Cidalia Maria Mota Lopes, and Carlos Ferreira. 2016. Tax complexity indices and their relation with tax noncompliance: Empirical evidence from the Portuguese tax professionals. Tékhne 14: 20–30. [Google Scholar] [CrossRef]

- Borrego, Ana Clara, Ern Chen Loo, Cidaia Maria Mota Lopes, and Carlos Manuel S. Ferreira. 2015. Tax professionals’ perception of tax system complexity: Some preliminary empirical evidence from Portugal. eJTR 13: 338. [Google Scholar]

- Boyd, John H., and Abu M. Jalal. 2012. A new measure of financial development: Theory leads measurement. Journal of Development Economics 99: 341–57. [Google Scholar] [CrossRef]

- Calford, Evan M., and Gregory DeAngelo. 2023. Ambiguity and enforcement. Experimental Economics 26: 304–38. [Google Scholar] [CrossRef]

- Cameron, A. Colin, and Pravin K. Trivedi. 2005. Microeconometrics: Methods and Applications. Cambridge: Cambridge University Press. [Google Scholar]

- Cameron, A. Colin, and Pravin K. Trivedi. 2010. Microeconometrics Using Stata. College Station: Stata Press. [Google Scholar]

- Campbell, Katherine, and Duane Helleloid. 2016. Starbucks: Social responsibility and tax avoidance. Journal of Accounting Education 37: 38–60. [Google Scholar] [CrossRef]

- Carrillo, Paul, Dina Pomeranz, and Monica Singhal. 2017. Dodging the Taxman: Firm Misreporting and Limits to Tax Enforcement. American Economic Journal: Applied Economics 9: 144–64. [Google Scholar] [CrossRef]

- Chang, Juin-Jen, and Ching-Chong Lai. 2004. Collaborative tax evasion and social norms: Why deterrence does not work. Oxford Economic Papers 56: 334–68. [Google Scholar] [CrossRef]

- Charness, Gary, and Uri Gneezy. 2012. Strong evidence for gender differences in risk taking. Journal of Economic Behavior & Organization 83: 50–8. [Google Scholar]

- Chesher, Andrew, Dongwoo Kim, and Adam M. Rosen. 2023. IV methods for Tobit models. Journal of Econometrics 235: 1700–24. [Google Scholar] [CrossRef]

- Choo, C. Y. Lawrence, Miguel A. Fonseca, and Gareth D. Myles. 2016. Do students behave like real taxpayers in the lab? Evidence from a real effort tax compliance experiment. Journal of Economic Behavior & Organization 124: 102–14. [Google Scholar]

- Christians, Allison. 2014. Avoidance, evasion, and taxpayer morality. Washington University Journal of Law & Policy 44: 39. [Google Scholar]

- Ciziceno, Marco, and Pietro Pizzuto. 2022. Life satisfaction and tax morale: The role of trust in government and cultural orientation. Journal of Behavioral and Experimental Economics 97: 101824. [Google Scholar] [CrossRef]

- Clarke, Kevin A. 2009. Return of the phantom menace: Omitted variable bias in political research. Conflict Management and Peace Science 26: 46–66. [Google Scholar] [CrossRef]

- Clausing, Kimberly A. 2009. Corporate tax revenues in OECD countries. International Tax and Public Finance 14: 115–33. [Google Scholar] [CrossRef]

- Clotfelter, Charles T. 1983. Tax evasion and tax rates: An analysis of individual returns. The Review of Economics and Statistics, 363–73. [Google Scholar]

- Cobham, Alex, and Petr Janský. 2018. Global distribution of revenue loss from corporate tax avoidance: Re-estimation and country results. Journal of International Development 30: 206–32. [Google Scholar] [CrossRef]

- Cowell, Frank A. 1992. Tax evasion and inequity. Journal of Economic Psychology 13: 521–43. [Google Scholar] [CrossRef]

- Cowell, Frank A., and James P. F. Gordon. 1988. Unwillingness to pay: Tax evasion and public good provision. Journal of Public Economics 36: 305–21. [Google Scholar] [CrossRef]

- Crocker, Keith J., and Joel Slemrod. 2005. Corporate tax evasion with agency costs. Journal of Public Economics 89: 1593–610. [Google Scholar] [CrossRef]

- Cronqvist, Henrik, and Frank Yu. 2017. Shaped by their daughters: Executives, female socialization, and corporate social responsibility. Journal of Financial Economics 126: 543–562. [Google Scholar] [CrossRef]

- Croson, Rachel, and Uri Gneezy. 2009. Gender differences in preferences. Journal of Economic Literature 47: 448–74. [Google Scholar] [CrossRef]

- Cuccia, Andrew D. 1994. The economics of tax compliance: What do we know and where do we go? Journal of Accounting Literature 13: 81. [Google Scholar]

- Cuccia, Andrew D., and Gregory A. Carnes. 2001. A closer look at the relation between tax complexity and tax equity perceptions. Journal of Economic Psychology 22: 113–40. [Google Scholar] [CrossRef]

- Cummings, Ronald G., Jorge Martinez-Vazquez, Michael McKee, and Torgler Benno. 2005. Effects of Tax Morale on Tax Compliance: Experimental and Survey Evidence. CREMA Working Paper 2005-29. Melbourne: Crema Constructions. [Google Scholar]

- Damayanti, Theresia Woro, and Supramono Supramono. 2019. Women in control and tax compliance. Gender in Management 34: 444–64. [Google Scholar] [CrossRef]

- DeBacker, Jason, Bradley T. Heim, Anh Tran, and Alexander Yuskavage. 2018. Once bitten, twice shy? The lasting impact of enforcement on tax compliance. The Journal of Law and Economics 61: 1–35. [Google Scholar] [CrossRef]

- Demin, Alexander V. 2020. Certainty and Uncertainty in Tax Law: Do Opposites Attract? Laws 9: 30. [Google Scholar] [CrossRef]

- Dickson, Eric S., Sanford C. Gordon, and Gregory A. Huber. 2022. Identifying legitimacy: Experimental evidence on compliance with authority. Science Advances 8: eabj7377. [Google Scholar] [CrossRef] [PubMed]

- Djankov, Simeon, Rafael La Porta, Florencio Lopez-de-Silanes, and Andrei Shleifer. 2003. Courts. The Quarterly Journal of Economics 118: 453–517. [Google Scholar] [CrossRef]

- Djankov, Simeon, Tim Ganser, Caralee McLiesh, Rita Ramalho, and Andrei Shleifer. 2010. The effect of corporate taxes on investment and entrepreneurship. American Economic Journal: Macroeconomics 2: 31–64. [Google Scholar] [CrossRef]

- Doerrenberg, Philipp, and Andreas Peichl. 2013. Progressive taxation and tax morale. Public Choice 155: 293–316. [Google Scholar] [CrossRef]

- e Hassan, Ibn, Ahmed Naeem, and Sidra Gulzar. 2021. Voluntary tax compliance behavior of individual taxpayers in Pakistan. Financial Innovation 7: 1–23. [Google Scholar] [CrossRef]

- Eichfelder, Sebastian, and Frank Hechtner. 2018. Tax compliance costs: Cost burden and cost reliability. Public Finance Review 46: 764–92. [Google Scholar] [CrossRef]

- Elbra, Ainsley, and John Mikler. 2017. Paying a ‘fair share’: Multinational corporations’ perspectives on taxation. Global Policy 8: 181–90. [Google Scholar] [CrossRef]

- Elffers, Henk, Russell H. Weigel, and Dick J. Hessing. 1987. The consequences of different strategies for measuring tax evasion behavior. Journal of Economic Psychology 8: 311–37. [Google Scholar] [CrossRef]

- Elgin, Ceyhun, and Oguz Oztunali. 2014. Institutions, informal economy, and economic development. Emerging Markets Finance and Trade 50: 145–62. [Google Scholar] [CrossRef]

- Epaphra, Manamba, and John Massawe. 2017. Corruption, governance and tax revenues in Africa. Business and Economic Horizons 13: 439–67. [Google Scholar] [CrossRef]

- Feinstein, Jonathan S. 1991. An econometric analysis of income tax evasion and its detection. The RAND Journal of Economics, 14–35. [Google Scholar]

- Fishburn, Geoffrey. 1981. Tax evasion and inflation. Australian Economic Papers 20: 325–32. [Google Scholar] [CrossRef]

- Fjeldstad, Odd-Helge, and Bertil Tungodden. 2003. Fiscal corruption: A vice or a virtue? World Development 31: 1459–467. [Google Scholar] [CrossRef]

- Forest, Adam, and Steven M. Sheffrin. 2002. Complexity and compliance: An empirical investigation. National Tax Journal 55: 75–88. [Google Scholar] [CrossRef]

- Foucault, Martial, Thierry Madies, and Sonia Paty. 2008. Public spending interactions and local politics. Empirical evidence from French municipalities. Public Choice 137: 57–80. [Google Scholar] [CrossRef]

- Frecknall-Hughes, Jane, Katharina Gangl, Eva Hofmann, Barbara Hartl, and Erich Kirchler. 2023. The influence of tax authorities on the employment of tax practitioners: Empirical evidence from a survey and interview study. Journal of Economic Psychology 97: 102629. [Google Scholar] [CrossRef]

- Gordon, John Steele. 2000. The Great Game: The Emergence of Wall Street as a World Power: 1653–2000. New York: Scibner. [Google Scholar]

- Guan, Jing, Hongjian Cheng, Kenneth A. Bollen, D. Roland Thomas, and Liqun Wang. 2019. Instrumental variable estimation in ordinal probit models with mismeasured predictors. Canadian Journal of Statistics 47: 653–67. [Google Scholar] [CrossRef]

- Hanlon, Michelle, Edward L. Maydew, and Jacob R. Thornock. 2015. Taking the long way home: US tax evasion and offshore investments in US equity and debt markets. The Journal of Finance 70: 257–87. [Google Scholar] [CrossRef]

- Hasseldine, John, Kevin Holland, and Pernill van der Rijt. 2011. The market for corporate tax knowledge. Critical Perspectives on Accounting 22: 39–52. [Google Scholar] [CrossRef]

- Henderson, J. Vernon, Tanner Regan, and Anthony J. Venables. 2016. Building the City: Sunk Capital, Sequencing, and Institutional Frictions. CEPR Discussion Paper No. 11211. Paris and London: CEPR Press. [Google Scholar]

- Hofmann, Eva, Katharina Gangl, Erich Kirchler, and Jennifer Stark. 2014. Enhancing Tax Compliance through Coercive and Legitimate Power of Tax Authorities by Concurrently Diminishing or Facilitating Trust in Tax Authorities. Law & Policy 36: 290–313. [Google Scholar]

- Hofmann, Eva, Martin Voracek, Christine Bock, and Erich Kirchler. 2017. Tax compliance across sociodemographic categories: Meta-analyses of survey studies in 111 countries. Journal of Economic Psychology 62: 63–71. [Google Scholar] [CrossRef]

- Hokamp, Sascha. 2014. Dynamics of tax evasion with back auditing, social norm updating, and public goods provision–An agent-based simulation. Journal of Economic Psychology 40: 187–99. [Google Scholar] [CrossRef]

- Hoppe, Thomas, Deborah Schanz, Susann Sturm, and Caren Sureth-Sloane. 2023. The tax complexity index—A survey-based country measure of tax code and framework complexity. European Accounting Review 32: 239–73. [Google Scholar] [CrossRef]

- Imam, Patrick Amir, and Davina Jacobs. 2014. Effect of corruption on tax revenues in the Middle East. Review of Middle East Economics and Finance 10: 1–24. [Google Scholar] [CrossRef]

- Islam, Azharul, Md. Harun Ur Rashid, Syed Zabid Hossain, and Rubayyat Hashmi. 2020. Public policies and tax evasion: Evidence from SAARC countries. Heliyon 6: e05449. [Google Scholar] [CrossRef] [PubMed]

- Ivanyna, Maksym, Alexandros Moumouras, and Peter Rangazas. 2016. The culture of corruption, tax evasion, and economic growth. Economic Inquiry 54: 520–42. [Google Scholar] [CrossRef]

- Iyer, Govind S., Philip M. J. Reckers, and Debra L. Sanders. 2010. A field experiment to explore the effects of detection and penalties communications and framing among Washington State retail firms. Advances in Accounting 26: 236–45. [Google Scholar] [CrossRef]

- Jensen, Anders. 2022. Employment structure and the rise of the modern tax system. American Economic Review 112: 213–34. [Google Scholar] [CrossRef]

- Johnson, Simon, Daniel Kaufmann, John McMillan, and Christoper Woodruff. 2000. Why do firms hide? Bribes and unofficial activity after communism. Journal of Public Economics 76: 495–520. [Google Scholar] [CrossRef]

- Joulfaian, David. 2000. Corporate income tax evasion and managerial preferences. Review of Economics and Statistics 82: 698–701. [Google Scholar] [CrossRef]

- Joulfaian, David. 2009. Bribes and business tax evasion. European Journal of Comparative Economics 6: 227–44. [Google Scholar]

- Karlsson, Maria, and Thomas Laitila. 2014. Finite mixture modeling of censored regression models. Statistical Papers 55: 627–42. [Google Scholar] [CrossRef]

- Kaufmann, Daniel, Aart Kraay, and Massimo Mastruzzi. 2011. The worldwide governance indicators: Methodology and analytical issues1. Hague Journal on the Rule of Law 3: 220–46. [Google Scholar] [CrossRef]

- Kaulu, Byrne. 2022. Determinants of tax evasion intention using the theory of planned behavior and the mediation role of taxpayer egoism. Fudan Journal of the Humanities and Social Sciences 15: 63–87. [Google Scholar] [CrossRef]

- Kelejian, Harry H., and Ingmar R. Prucha. 1999. A generalized moments estimator for the autoregressive parameter in a spatial model. International Economic Review 40: 509–33. [Google Scholar] [CrossRef]

- Kennedy, Edward H., Jacqueline A. Mauro, Michael J. Daniels, Natalie Burns, and Dylan S. Small. 2019. Handling missing data in instrumental variable methods for causal inference. Annual Review of Statistics and Its Application 6: 125–48. [Google Scholar]

- Kennedy, Peter. 2008. A Guide to Econometrics. Malden: John Wiley & Sons. [Google Scholar]

- Khan, Safi Ullah. 2023. The firm-level employment impact of COVID-19: International evidence from World Bank Group’s Enterprise Surveys. Eastern European Economics 61: 457–90. [Google Scholar] [CrossRef]

- Khujamkulov, Ismoil, and Sohrab Abizadeh. 2023. Trends in tax revenues of transition economies: An empirical approach. Empirical Economics 64: 833–68. [Google Scholar] [CrossRef]

- Kirchler, Erich, Apolonia Niemirowski, and Alexander Wearing. 2006. Shared subjective views, intent to cooperate and tax compliance: Similarities between Australian taxpayers and tax officers. Journal of Economic Psychology 27: 502–17. [Google Scholar] [CrossRef]

- Kirchler, Erich, Erik Hoelzl, and Ingrid Wahl. 2008. Enforced versus voluntary tax compliance: The “slippery slope” framework. Journal of Economic Psychology 29: 210–25. [Google Scholar] [CrossRef]

- Klepper, Steven, Mark Mazur, and Daniel Nagin. 1991. Expert intermediaries and legal compliance: The case of tax preparers. The Journal of Law and Economics 34: 205–29. [Google Scholar] [CrossRef]

- Kleven, Henrik Jacobsen, Martin B. Knudsen, Claus Thustrup Kreiner, Søren Pedersen, and Emmanuel Saez. 2011. Unwilling or unable to cheat? Evidence from a tax audit experiment in Denmark. Econometrica 79: 651–92. [Google Scholar]

- Kogler, Christoph, Jerome Olsen, Martin Müller, and Erich Kirchler. 2022. Information processing in tax decisions: A MouselabWEB study on the deterrence model of income tax evasion. Journal of Behavioral Decision Making 35: e2272. [Google Scholar] [CrossRef]

- Korndörfer, Martin, Ivar Krumpal, and Stefan C. Schmukle. 2014. Measuring and explaining tax evasion: Improving self-reports using the crosswise model. Journal of Economic Psychology 45: 18–32. [Google Scholar] [CrossRef]

- Krause, Kate. 2000. Tax complexity: Problem or opportunity? Public Finance Review 28: 395–414. [Google Scholar] [CrossRef]

- Krumpal, Ivar. 2013. Determinants of social desirability bias in sensitive surveys: A literature review. Quality & Quantity 47: 2025–47. [Google Scholar]

- Kuncoro, Haryo. 2023. Inflation and its uncertainty: Evidence from Indonesia and the Philippines. Global Journal of Emerging Market Economies 16: 09749101221149873. [Google Scholar] [CrossRef]

- Lambsdorff, Johann Graf. 2007. The Institutional Economics of Corruption and Reform: Theory, Evidence and Policy. Cambridge: Cambridge University Press. [Google Scholar]

- Lawless, Martina. 2013. Do complicated tax systems prevent foreign direct investment? Economica 80: 1–22. [Google Scholar] [CrossRef]

- Li, Wanfu, Jeffrey A. Pittman, and Zi-Tian Wang. 2019. The determinants and consequences of tax audits: Some evidence from China. The Journal of the American Taxation Association 41: 91–122. [Google Scholar] [CrossRef]

- Liu, Jingping. 2022. The abolition of agricultural taxes and the transformation of clientelism in the countryside of post-Mao China. The Journal of Peasant Studies 49: 585–603. [Google Scholar] [CrossRef]

- Liu, Yongzheng, and Haibo Feng. 2015. Tax structure and corruption: Cross-country evidence. Public Choice 162: 57–78. [Google Scholar] [CrossRef]

- Machen, Ronald C., Matthew T. Jones, George P. Varghese, and Emily L. Stark. 2021. Investigation of Data Irregularities in Doing Business 2018 and Doing Business 2020. Washington, DC: Wilmer Cutler Pickering Hale and Dorr. [Google Scholar]

- Madzharova, Boryana. 2013. The effect of low corporate tax rate on payroll tax evasion. In Critical Issues in Taxation and Development. Edited by Clemens Fuest and George R. Zodrow. Cambridge: The MIT Press, pp. 109–44. [Google Scholar]

- Mason, Paul D., Steven Utke, and Brian M. Williams. 2020. Why pay our fair share? How perceived influence over laws affects tax evasion. The Journal of the American Taxation Association 42: 133–56. [Google Scholar] [CrossRef]

- Mathieu, Laurence, Catherine Waddams Price, and Francis Antwi. 2010. The distribution of UK personal income tax compliance costs. Applied Economics 42: 351–68. [Google Scholar] [CrossRef]

- Matsa, David A., and Amalia R. Miller. 2013. A female style in corporate leadership? evidence from quotas. American Economic Journal: Applied Economics 5: 136–69. [Google Scholar] [CrossRef]

- Mawejje, Joseph. 2019. The oil discovery in Uganda’s Albertine region: Local expectations, involvement, and impacts. The Extractive Industries and Society 6: 129–35. [Google Scholar] [CrossRef]

- Mintz, Jack. 2004. Corporate tax harmonization in Europe: It’s all about compliance. International Tax and Public Finance 11: 221–34. [Google Scholar] [CrossRef]

- Moore, Mick, and Wilson Prichard. 2020. How can governments of low-income countries collect more tax revenue? In The Politics of Domestic Resource Mobilization for Social Development. Edited by Katja Hujo. Cambridge: Palgrave Macmillan, pp. 109–38. [Google Scholar]

- Moshirian, Fariborz. 2011. The global financial crisis and the evolution of markets, institutions and regulation. Journal of Banking & Finance 35: 502–11. [Google Scholar]

- Murphy, Kristina. 2004. Aggressive tax planning: Differentiating those playing the game from those who don’t. Journal of Economic Psychology 25: 307–29. [Google Scholar] [CrossRef]

- Musimenta, Doreen. 2020. Knowledge requirements, tax complexity, compliance costs and tax compliance in Uganda. Cogent Business & Management 7: 1812220. [Google Scholar]

- Nagac, K. 2015. Tax system and informal economy: A cross-country analysis. Applied Economics 47: 1775–787. [Google Scholar] [CrossRef]

- Neck, Reinhard, Jens Uwe Wächter, and Friedrich Schneider. 2012. Tax avoidance versus tax evasion: On some determinants of the shadow economy. International Tax and Public Finance 19: 104–17. [Google Scholar] [CrossRef]

- Nicodème, Gaëtan. 2009. On recent developments in fighting harmful tax practices. National Tax Journal 62: 755–71. [Google Scholar] [CrossRef]

- Nur-Tegin, Kanybek D. 2008. Determinants of business tax compliance. The BE Journal of Economic Analysis & Policy 8: 1683. [Google Scholar]

- Olsen, Robert A., and Constance M. Cox. 2001. The influence of gender on the perception and response to investment risk: The case of professional investors. The Journal of Psychology and Financial Markets 2: 29–36. [Google Scholar] [CrossRef]

- Onu, Diana, Lynne Oats, Erich Kirchler, and Andre Julian Hartmann. 2019. Gaming the system: An investigation of small business owners’ attitudes to tax avoidance, tax planning, and tax evasion. Games 10: 46. [Google Scholar] [CrossRef]

- Otusanya, Olatunde Julius. 2011. The role of multinational companies in tax evasion and tax avoidance: The case of Nigeria. Critical Perspectives on Accounting 22: 316–32. [Google Scholar] [CrossRef]

- Owusu, Godfred Matthew Yaw, Rita Amoah Bekoe, and Rockson Mintah. 2023. Predictors of tax compliance intentions among self-employed individuals: The role of trust, perceived tax complexity and antecedent-based intervention strategies. Small Enterprise Research 30: 49–70. [Google Scholar] [CrossRef]

- Pau, Caroline, Adrian Sawyer, and Andrew Maples. 2007. Complexity of New Zealand’s tax laws: An empirical study. Australian Tax Forum 22: 59. [Google Scholar]

- Petrongolo, Barbara, and Maddalena Ronchi. 2020. Gender gaps and the structure of local labor markets. Labour Economics 64: 101819. [Google Scholar] [CrossRef]

- Pissarides, Christopher A., and Guglielmo Weber. 1989. An expenditure-based estimate of Britain’s black economy. Journal of Public Economics 39: 17–32. [Google Scholar] [CrossRef]

- Pommerehne, Werner W., and Hannelore Weck-Hannemann. 1996. Tax rates, tax administration and income tax evasion in Switzerland. Public Choice 88: 161–70. [Google Scholar] [CrossRef]

- Rice, Eric M. 1992. The corporate tax gap: Evidence on tax compliance by small corporations. In Why People Pay Taxes. Edited by Joel Slemrod. Ann Arbor: The University of Michigan Press, pp. 125–62. [Google Scholar]

- Richardson, Grant. 2006. Determinants of tax evasion: A cross-country investigation. Journal of International Accounting, Auditing and Taxation 15: 150–169. [Google Scholar] [CrossRef]

- Riedel, Nadine. 2018. Quantifying international tax avoidance: A review of the academic literature. Review of Economics 69: 169–81. [Google Scholar] [CrossRef]

- Ritsema, Christina M., Deborah W. Thomas, and Gary D. Ferrier. 2003. Economic and behavioral determinants of tax compliance: Evidence from the 1997 Arkansas Tax Penalty Amnesty Program. Presented at the 2003 IRS Research Conference, Washington, DC, USA, June. [Google Scholar]

- Sakurai, Yuka, and Valerie Braithwaite. 2001. Taxpayers’ Perceptions of the Ideal Tax Adviser: Playing Safe or Saving Dollars? Centre for Tax System Integrity Working Paper No. 5. Available online: https://openresearch-repository.anu.edu.au/handle/1885/154896 (accessed on 10 March 2024).

- Saptono, Prianto Budi, and Gustofan Mahmud. 2022. Institutional environment and tax performance: Empirical evidence from developing economies. Public Sector Economics 46: 207–37. [Google Scholar] [CrossRef]

- Saw, Kathryn, and Adrian Sawyer. 2010. Complexity of New Zealand’s income tax legislation: The final installment. Australian Tax Forum 25: 213. [Google Scholar]

- Schneider, Friedrich, Andreas Buehn, and Claudio E. Montenegro. 2010. New estimates for the shadow economies all over the world. International Economic Journal 24: 443–61. [Google Scholar] [CrossRef]

- Shuai, Xiaobing, and Christine Chmura. 2013. The effect of state corporate income tax rate cuts on job creation. Business Economics 48: 183–93. [Google Scholar] [CrossRef]

- Slemrod, Joel, Marsha Blumenthal, and Charles Christian. 2001. Taxpayer response to an increased probability of audit: Evidence from a controlled experiment in Minnesota. Journal of Public Economics 79: 455–83. [Google Scholar] [CrossRef]

- Slemrod, Joel. 2007. Cheating ourselves: The economics of tax evasion. Journal of Economic Perspectives 21: 25–48. [Google Scholar] [CrossRef]

- Slemrod, Joel. 2019. Tax compliance and enforcement. Journal of Economic Literature 57: 904–54. [Google Scholar] [CrossRef]

- Stein, Sarah E. 2019. Auditor industry specialization and accounting estimates: Evidence from asset impairments. Auditing: A Journal of Practice & Theory 38: 207–34. [Google Scholar]

- Taing, Heang Boong, and Yongjin Chang. 2020. Determinants of tax compliance intention: Focus on the theory of planned behavior. International Journal of Public Administration 44: 62–73. [Google Scholar] [CrossRef]

- Tan, Lin Mei, and Adrian J. Sawyer. 2003. A synopsis of taxpayer compliance studies: Overseas vis-a-vis New Zealand. New Zealand Journal of Taxation Law and Policy 9: 431–54. [Google Scholar]

- Tanzi, Vito, and Parthasarathi Shome. 1993. A primer on tax evasion. IMF Economic Review 40: 807–28. [Google Scholar] [CrossRef]

- Tanzi, Vito. 1980. Inflation and the Personal Income Tax. Cambridge: Cambirdge University Press. [Google Scholar]

- Tanzi, Vito. 2018. Corruption, complexity and tax evasion. Ekonomicheskaya Politika/Economic Policy 13: 36–53. [Google Scholar]

- Tobin, James. 1958. Estimation of relationships for limited dependent variables. Econometrica: Journal of the Econometric Society 26: 24–36. [Google Scholar]

- Torgler, Benno, and Friedrich Schneider. 2007. Shadow Economy, Tax Morale, Governance and Institutional Quality: A Panel Analyisis. Berkeley Program in Law and Economics, Working Paper Series. Available online: https://www.iza.org/publications/dp/2563/shadow-economy-tax-morale-governance-and-institutional-quality-a-panel-analysis (accessed on 12 March 2024).

- Torgler, Benno, and Friedrich Schneider. 2009. The impact of tax morale and institutional quality on the shadow economy. Journal of Economic Psychology 30: 228–45. [Google Scholar] [CrossRef]

- Torgler, Benno, and Neven T. Valev. 2006. Corruption and age. Journal of Bioeconomics 8: 133–45. [Google Scholar] [CrossRef]

- Torgler, Benno. 2011. Tax Morale and Compliance: Review of Evidence and Case Studies for Europe. World Bank Policy Research Working Paper 5922. Available online: https://elibrary.worldbank.org/doi/abs/10.1596/1813-9450-5922 (accessed on 12 March 2024).

- Tørsløv, Thomas, Ludvig Wier, and Gabriel Zucman. 2023. The missing profits of nations. The Review of Economic Studies 90: 1499–534. [Google Scholar] [CrossRef]

- Tourangeau, Roger, and Ting Yan. 2007. Sensitive questions in surveys. Psychological Bulletin 133: 859. [Google Scholar] [CrossRef]

- Tran-Nam, Binh, and Chris Evans. 2014. Towards the development of a tax system complexity index. Fiscal Studies 35: 341–70. [Google Scholar] [CrossRef]

- Treisman, Daniel. 2007. What have we learned about the causes of corruption from ten years of cross-national empirical research? Annual Review of Empirical Science 10: 211–44. [Google Scholar] [CrossRef]

- United Nations. 2008. Industrial Classification of All Economic Activities (ISIC), Rev.4. New York: United Nations. [Google Scholar]

- van’t Riet, Maarten, and Arjan Lejour. 2018. Optimal tax routing: Network analysis of FDI diversion. International Tax and Public Finance 25: 1321–71. [Google Scholar] [CrossRef]

- White, Halbert. 1980. Using least squares to approximate unknown regression functions. International Economic Review 21: 149–70. [Google Scholar] [CrossRef]

- Williams, Brian. 2016. Financial Accounting Standards, audit Profession Development, and Firm-Level Tax Evasion. Indiana University Working Paper. Available online: https://scholarsbank.uoregon.edu/xmlui/handle/1794/19699 (accessed on 11 March 2024).

- Wilms, Rafael, E. Mäthner, Lothar Winnen, and Ralf Lanwehr. 2021. Omitted variable bias: A threat to estimating causal relationships. Methods in Psychology 5: 100075. [Google Scholar] [CrossRef]

- Wooldridge, Jeffrey M. 2008. Instrumental variables estimation of the average treatment effect in the correlated random coefficient model. In Modelling and Evaluating Treatment Effects in Econometrics. Edited by Daniel L. Millimet, Jeffrey A. Smith and Edward J. Vytlacil. Amsterdam: Emerald Group Publishing Limited, pp. 93–116. [Google Scholar]

- Wooldridge, Jeffrey M. 2010. Econometric Analysis of Cross Section and Panel Data. Cambridge: MIT Press. [Google Scholar]

- Xiao, Zumian, Juanhe Gao, Zongshu Wang, Zhichao Yin, and Lijin Xiang. 2022. Power shortage and firm productivity: Evidence from the World Bank Enterprise Survey. Energy 247: 123479. [Google Scholar] [CrossRef]

- Yamen, Ahmed, Amir Allam, Ahmed Bani-Mustafa, and Ali Uyar. 2018. Impact of institutional environment quality on tax evasion: A comparative investigation of old versus new EU members. Journal of International Accounting, Auditing and Taxation 32: 17–29. [Google Scholar] [CrossRef]

- Yang, Weixin, Xiu Zheng, and Yunpeng Yang. 2024. Impact of environmental regulation on export technological complexity of high-tech industries in Chinese manufacturing. Economies 12: 50. [Google Scholar] [CrossRef]

- Yitzhaki, Shlomo. 1974. A note on income tax evasion: A theoretical analysis. Journal of Public Economics 3: 201–2. [Google Scholar] [CrossRef]

| Number of Firms | Number of Countries | |

|---|---|---|

| Confidential WBES database for the 2002 to 2023 survey period | 252,834 | 164 |

| Missing data on tax evasion ratio | (180,019) | (58) |

| Countries with inconsistent rankings for two measures of tax evasion (the absolute value of the discrepancy between the two ranks exceeds 70) | (458) | (3) |

| Only include one sample survey period of each country | (12,941) | |

| Missing data on tax complexity | (9684) | (11) |

| Missing data on control variables | (3686) | (9) |

| The final number of observations | 46,046 | 83 |

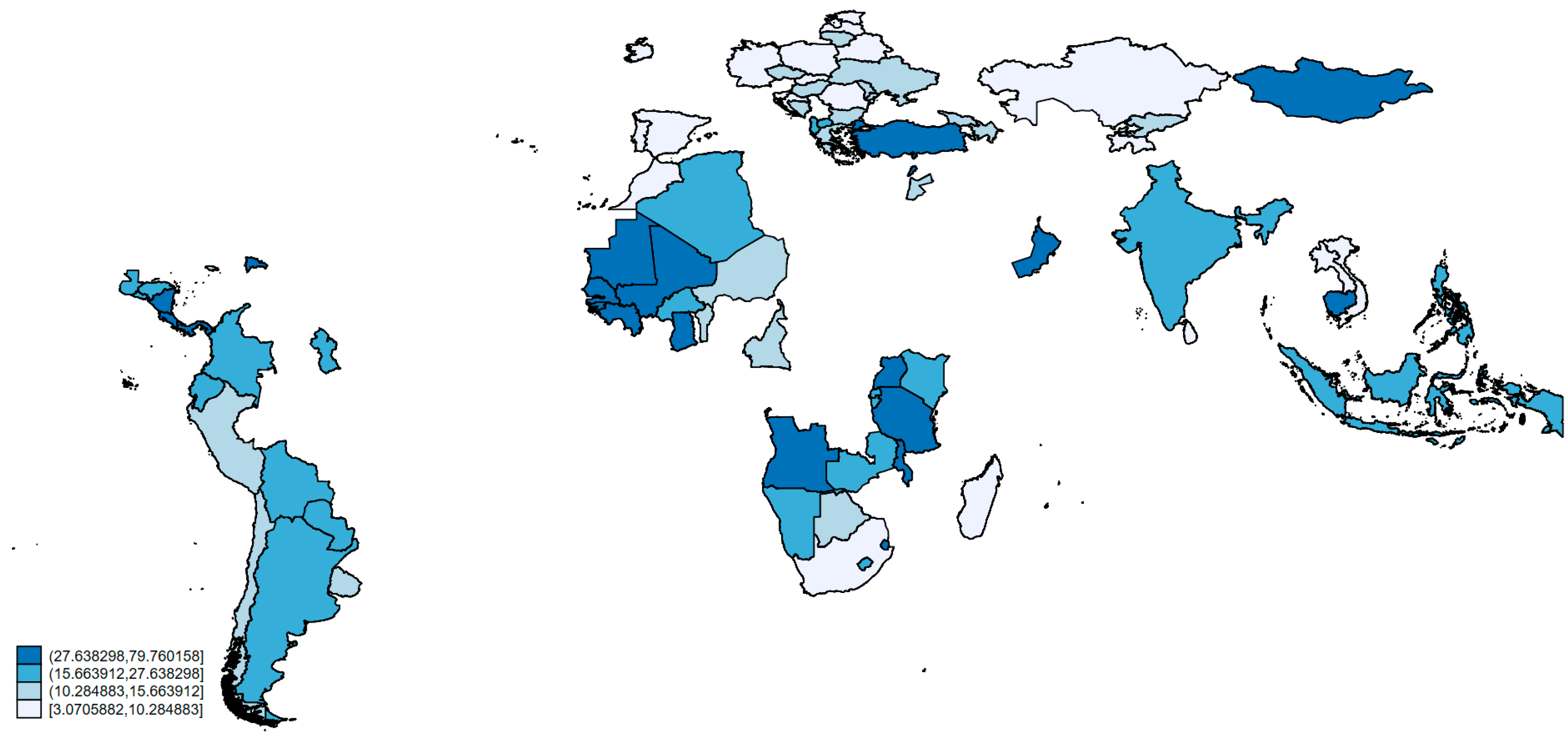

| Country | Number of Firms | Tax Evasion Ratio | Tax Time | Tax Payment | |

|---|---|---|---|---|---|

| 1 | Albania | 198 | 0.230 | 364 | 45 |

| 2 | Algeria | 188 | 0.276 | 451 | 39 |

| 3 | Angola | 118 | 0.794 | 284 | 31 |

| 4 | Argentina | 1894 | 0.175 | 453 | 62 |

| 5 | Azerbaijan | 349 | 0.139 | 756 | 37 |

| 6 | Belarus | 320 | 0.072 | 986.5 | 125 |

| 7 | Benin | 176 | 0.144 | 270 | 52 |

| 8 | Bolivia | 1104 | 0.202 | 1080 | 42 |

| 9 | Bosnia and Herzegovina | 195 | 0.118 | 368 | 55 |

| 10 | Botswana | 209 | 0.131 | 140 | 19 |

| 11 | Bulgaria | 290 | 0.135 | 598 | 29 |

| 12 | Burkina Faso | 131 | 0.219 | 270 | 45 |

| 13 | Burundi | 540 | 0.157 | 140 | 33 |

| 14 | Cambodia | 423 | 0.520 | 137 | 39 |

| 15 | Cameroon | 168 | 0.121 | 654 | 45 |

| 16 | Chile | 1862 | 0.132 | 316 | 8 |

| 17 | Colombia | 1840 | 0.171 | 456 | 70 |

| 18 | Costa Rica | 287 | 0.284 | 402 | 43 |

| 19 | Croatia | 211 | 0.075 | 232 | 40 |

| 20 | Czech Republic | 333 | 0.131 | 866 | 27 |

| 21 | Dominican Republic | 139 | 0.439 | 232 | 75 |

| 22 | Ecuador | 1212 | 0.264 | 600 | 8 |

| 23 | El Salvador | 1108 | 0.192 | 320 | 41 |

| 24 | Estonia | 170 | 0.031 | 81 | 7 |

| 25 | Eswatini | 584 | 0.579 | 116 | 33 |

| 26 | Georgia | 164 | 0.109 | 448 | 46 |

| 27 | Germany | 1192 | 0.057 | 196 | 12 |

| 28 | Ghana | 292 | 0.313 | 304 | 37 |

| 29 | Greece | 502 | 0.110 | 264 | 19 |

| 30 | Guatemala | 986 | 0.270 | 344 | 38 |

| 31 | Guinea | 426 | 0.643 | 416 | 57 |

| 32 | Guinea-Bissau | 41 | 0.280 | 218 | 46 |

| 33 | Guyana | 156 | 0.262 | 288 | 35 |

| 34 | Honduras | 726 | 0.157 | 424 | 58 |

| 35 | Hungary | 592 | 0.113 | 340 | 13 |

| 36 | India | 3869 | 0.269 | 252.88 | 60 |

| 37 | Indonesia | 713 | 0.269 | 266 | 51 |

| 38 | Ireland | 490 | 0.038 | 75 | 9 |

| 39 | Jamaica | 72 | 0.110 | 324 | 72 |

| 40 | Jordan | 415 | 0.126 | 136 | 26 |

| 41 | Kazakhstan | 568 | 0.066 | 261 | 7 |

| 42 | Kenya | 395 | 0.183 | 444 | 52 |

| 43 | Kyrgyz Republic | 197 | 0.146 | 222 | 76 |

| 44 | Lao PDR | 242 | 0.038 | 672 | 34 |

| 45 | Latvia | 194 | 0.071 | 280 | 29 |

| 46 | Lebanon | 292 | 0.344 | 180 | 20 |

| 47 | Lesotho | 48 | 0.171 | 564 | 33 |

| 48 | Lithuania | 172 | 0.103 | 166 | 11 |

| 49 | Madagascar | 286 | 0.065 | 400 | 27 |

| 50 | Malawi | 132 | 0.303 | 376 | 23 |

| 51 | Mali | 97 | 0.766 | 270 | 58 |

| 52 | Mauritania | 456 | 0.470 | 696 | 37 |

| 53 | Mauritius | 156 | 0.122 | 161 | 8 |

| 54 | Moldova | 321 | 0.105 | 234 | 53 |

| 55 | Mongolia | 160 | 0.364 | 204 | 41 |

| 56 | Morocco | 834 | 0.039 | 358 | 28 |

| 57 | Namibia | 644 | 0.254 | 339 | 37 |

| 58 | Nicaragua | 834 | 0.409 | 240 | 66 |

| 59 | Niger | 111 | 0.127 | 270 | 41 |

| 60 | North Macedonia | 182 | 0.235 | 192 | 43 |

| 61 | Oman | 284 | 0.287 | 52 | 15 |

| 62 | Panama | 1096 | 0.371 | 560 | 52 |

| 63 | Paraguay | 926 | 0.192 | 328 | 35 |

| 64 | Peru | 1242 | 0.106 | 424 | 9 |

| 65 | Philippines | 598 | 0.218 | 195 | 48 |

| 66 | Poland | 969 | 0.100 | 420 | 41 |

| 67 | Portugal | 502 | 0.082 | 328 | 7 |

| 68 | Romania | 577 | 0.066 | 192 | 108 |

| 69 | Rwanda | 420 | 0.189 | 168 | 25 |

| 70 | Senegal | 190 | 0.798 | 696 | 59 |

| 71 | Slovak Republic | 191 | 0.045 | 325 | 32 |

| 72 | Slovenia | 205 | 0.072 | 248 | 22 |

| 73 | South Africa | 562 | 0.091 | 346 | 12 |

| 74 | Spain | 600 | 0.037 | 298 | 8 |

| 75 | Sri Lanka | 355 | 0.076 | 262 | 58 |

| 76 | Tajikistan | 200 | 0.090 | 296 | 69 |

| 77 | Tanzania | 834 | 0.469 | 172 | 47 |

| 78 | Turkey | 1120 | 0.495 | 254 | 10 |

| 79 | Uganda | 1094 | 0.464 | 237 | 32 |

| 80 | Ukraine | 573 | 0.107 | 2085 | 147 |

| 81 | Uruguay | 736 | 0.147 | 304 | 55 |

| 82 | Vietnam | 1609 | 0.094 | 1050 | 32 |

| 83 | Zambia | 157 | 0.158 | 183 | 38 |

| Industry | Number of Firms | Tax Evasion Ratio | |

|---|---|---|---|

| 1 | Accounting and finance | 3 | 0.510 |

| 2 | Advertising and marketing | 501 | 0.086 |

| 3 | Agroindustry | 346 | 0.375 |

| 4 | Auto and auto components | 248 | 0.207 |

| 5 | Beverages | 830 | 0.121 |

| 6 | Chemicals and pharmaceutics | 2558 | 0.167 |

| 7 | Construction | 2685 | 0.210 |

| 8 | Electronics | 482 | 0.135 |

| 9 | Food | 5312 | 0.225 |

| 10 | Garments | 4369 | 0.227 |

| 11 | Hotels and restaurants | 1595 | 0.299 |

| 12 | IT services | 1039 | 0.153 |

| 13 | Leather | 305 | 0.147 |

| 14 | Metals and machinery | 3420 | 0.186 |

| 15 | Mining and quarrying | 143 | 0.080 |

| 16 | Non-metallic and plastic materials | 1518 | 0.181 |

| 17 | Other manufacturing | 3546 | 0.216 |

| 18 | Other services | 2582 | 0.212 |

| 19 | Other transport equipment | 85 | 0.538 |

| 20 | Other unclassified | 269 | 0.283 |

| 21 | Paper | 650 | 0.146 |

| 22 | Real estate and rental services | 489 | 0.074 |

| 23 | Retail and wholesale trade | 8228 | 0.256 |

| 24 | Telecommunications | 106 | 0.056 |

| 25 | Textiles | 2340 | 0.205 |

| 26 | Transport | 739 | 0.111 |

| 27 | Wood and furniture | 1658 | 0.267 |

| Variables | Observations | Mean | Standard Deviation | Minimum | Maximum |

|---|---|---|---|---|---|

| Dependent Variables | |||||

| Tax evasion ratio | 46,046 | 0.214 | 0.317 | 0 | 1 |

| Tax evasion dummy | 46,046 | 0.456 | 0.498 | 0 | 1 |

| Independent Variables | |||||

| Log of tax time | 46,046 | 3.897 | 0.576 | 1.311 | 4.601 |

| Log of tax payment | 46,046 | 3.450 | 0.762 | 1.946 | 4.990 |

| Control Variables | |||||

| Log of GDP | 46,046 | 8.159 | 1.129 | 5.667 | 10.807 |

| Inflation | 46,046 | 8.663 | 10.356 | −2.273 | 100.608 |

| Unemployment | 46,046 | 8.078 | 6.081 | 0.774 | 37.25 |

| Agriculture | 46,046 | 11.597 | 8.182 | 0.727 | 42.260 |

| Tax burden | 46,046 | 75.713 | 8.905 | 52.4 | 98.5 |

| Age | 46,046 | 7.337 | 4.590 | 1.953 | 18.868 |

| Gender | 46,046 | 50.552 | 1.320 | 44.135 | 54.152 |

| Voice and accountability | 46,046 | 0.076 | 0.752 | −1.767 | 1.624 |

| Political stability | 46,046 | −0.331 | 0.827 | −2.095 | 1.300 |

| Government effectiveness | 46,046 | −0.115 | 0.674 | −1.296 | 1.736 |

| Regulatory quality | 46,046 | −0.030 | 0.728 | −1.454 | 1.516 |

| Rule of law | 46,046 | −0.167 | 0.746 | −1.405 | 1.664 |

| Control of corruption | 46,046 | −0.158 | 0.745 | −1.326 | 1.885 |

| Dependent Variables | Tax Evasion Ratio | Tax Evasion Dummy | ||||

|---|---|---|---|---|---|---|

| Models | Tobit | Probit | ||||

| Specifications | (1) | (2) | (3) | (4) | (5) | (6) |

| Log of tax time | 0.067 *** | 0.061 *** | 0.046 *** | 0.070 *** | 0.064 *** | 0.053 *** |

| (0.006) | (0.006) | (0.007) | (0.004) | (0.004) | (0.005) | |

| Log of tax payment | 0.042 *** | 0.077 *** | 0.080 *** | 0.052 *** | 0.063 *** | 0.059 *** |

| (0.005) | (0.005) | (0.006) | (0.004) | (0.004) | (0.004) | |

| Log of GDP | −0.026 *** | −0.102 *** | −0.197 *** | −0.046 *** | −0.070 *** | −0.127 *** |

| (0.006) | (0.007) | (0.009) | (0.005) | (0.006) | (0.007) | |

| Inflation | 0.004 *** | 0.004 *** | 0.004 *** | 0.003 *** | 0.003 *** | 0.004 *** |

| (0.0002) | (0.0003) | (0.0003) | (0.0002) | (0.0002) | (0.0002) | |

| Unemployment | 0.0017 *** | 0.0001 | −0.0006 | −0.001 *** | −0.001 ** | −0.001 ** |

| (0.0006) | (0.0006) | (0.0007) | (0.0005) | (0.0005) | (0.0005) | |

| Agriculture | 0.012 *** | 0.011 *** | 0.014 *** | 0.010 *** | 0.010 *** | 0.012 |

| (0.0008) | (0.0008) | (0.001) | (0.001) | (0.001) | (0.0008) | |

| Tax burden | −0.0002 | −0.002 *** | −0.002 *** | −0.001 ** | −0.001 *** | −0.001 *** |

| (0.0004) | (0.0004) | (0.0005) | (0.0003) | (0.0003) | (0.0004) | |

| Age | 0.032 *** | 0.041 *** | 0.009 *** | 0.015 *** | ||

| (0.001) | (0.002) | (0.001) | (0.001) | |||

| Gender | 0.006 ** | 0.046 *** | −0.007 *** | −0.021 *** | ||

| (0.003) | (0.004) | (0.002) | (0.003) | |||

| Voice and accountability | 0.079 *** | 0.061 *** | ||||

| (0.008) | (0.006) | |||||

| Political stability | −0.031 *** | −0.020 *** | ||||

| (0.006) | (0.005) | |||||

| Government effectiveness | −0.383 *** | −0.206 *** | ||||

| (0.018) | (0.014) | |||||

| Regulatory quality | 0.003 | −0.008 | ||||

| (0.014) | (0.011) | |||||

| Rule of law | 0.440 *** | 0.282 *** | ||||

| (0.193) | (0.015) | |||||

| Control of corruption | −0.196 *** | −0.157 *** | ||||

| (0.014) | (0.011) | |||||

| Observations | 46,046 | 46,046 | 46,046 | 46,046 | 46,046 | 46,046 |

| Countries | 83 | 83 | 83 | 83 | 83 | 83 |

| Pseudo-R2 | 0.047 | 0.055 | 0.067 | 0.035 | 0.037 | 0.047 |

| Industry and year dummies | Yes | Yes | Yes | Yes | Yes | Yes |

| Dependent Variables | Tax Evasion Ratio | Tax Evasion Dummy | ||||

|---|---|---|---|---|---|---|

| Models | IV Tobit | IV Probit | ||||

| Specifications | (1) | (2) | (3) | (4) | (5) | (6) |

| Log of tax time | 0.442 *** | 0.588 *** | 0.211 *** | 0.676 *** | 0.882 *** | 0.413 *** |

| (0.025) | (0.024) | (0.024) | (0.044) | (0.037) | (0.045) | |

| Log of tax payment | 0.092 *** | 0.142 *** | 0.010 | 0.206 *** | 0.252 *** | 0.094 *** |

| (0.013) | (0.015) | (0.013) | (0.026) | (0.029) | (0.027) | |

| Log of GDP | −0.074 *** | −0.017 | −0.095 *** | −0.038 | −0.060 * | −0.225 ** |

| (0.012) | (0.016) | (0.015) | (0.024) | (0.031) | (0.031) | |

| Inflation | 0.005 *** | 0.006 *** | 0.003 *** | 0.013 *** | 0.015 *** | 0.008 *** |

| (0.0003) | (0.0003) | (0.0003) | (0.001) | (0.001) | (0.001) | |

| Unemployment | −0.010 *** | −0.016 *** | −0.007 *** | −0.020 *** | −0.025 *** | −0.016 *** |

| (0.001) | (0.001) | (0.001) | (0.002) | (0.002) | (0.002) | |

| Agriculture | −0.007 *** | −0.013 *** | −0.003 | 0.004 | −0.007 ** | 0.003 |

| (0.002) | (0.002) | (0.002) | (0.003) | (0.003) | (0.004) | |

| Tax burden | −0.0007 | −0.0008 | −0.004 *** | −0.0002 | −0.001 | −0.005 *** |

| (0.0005) | (0.0005) | (0.001) | (0.001) | (0.001) | (0.001) | |

| Age | 0.027 *** | 0.030 *** | 0.025 *** | 0.034 *** | ||

| (0.002) | (0.003) | (0.005) | (0.006) | |||

| Gender | −0.023 *** | −0.052 *** | −0.058 *** | −0.054 *** | ||

| (0.005) | (0.005) | (0.010) | (0.011) | |||

| Voice and accountability | 0.062 *** | 0.085 *** | ||||

| (0.012) | (0.026) | |||||

| Political stability | −0.036 *** | −0.070 *** | ||||

| (0.007) | (0.015) | |||||

| Government effectiveness | −0.314 *** | −0.478 *** | ||||

| (0.022) | (0.045) | |||||

| Regulatory quality | −0.204 *** | −0.380 *** | ||||

| (0.024) | (0.046) | |||||

| Rule of law | 0.511 *** | 0.905 *** | ||||

| (0.030) | (0.060) | |||||

| Control of corruption | −0.214 *** | −0.366 *** | ||||

| (0.018) | (0.039) | |||||

| Observations | 37,893 | 37,893 | 37,893 | 37,893 | 37,893 | 37,893 |

| Countries | 68 | 68 | 68 | 68 | 68 | 68 |

| Industry and year dummies | Yes | Yes | Yes | Yes | Yes | Yes |

| Wald test: exogeneity | 271.88 *** | 602.85 *** | 161.26 *** | 130.40 *** | 311.47 *** | 67.24 *** |

| Dependent Variables | Log of Tax Time | Log of Tax Payment | ||||

|---|---|---|---|---|---|---|

| Specifications | (1) | (2) | (3) | (1) | (2) | (3) |

| IV Tobit Model in Table 8 | ||||||

| Log of tax time × contiguity matrix | −0.126 *** | −0.157 *** | −0.351 *** | |||

| (0.009) | (0.009) | (0.013) | ||||

| Log of tax time × inverse-distance matrix | 0.620 *** | 1.054 *** | 1.885 *** | |||

| (0.034) | (0.033) | (0.043) | ||||

| Log of tax payment × contiguity matrix | 0.637 *** | 0.556 *** | 0.663 *** | |||

| (0.008) | (0.007) | (0.006) | ||||

| Log of tax payment × inverse-distance matrix | −0.652 *** | −0.075 ** | −0.318 *** | |||

| (0.039) | (0.037) | (0.037) | ||||

| IV Probit Model in Table 8 | ||||||

| Log of tax time × contiguity matrix | −0.126 *** | −0.157 *** | −0.351 *** | |||

| (0.009) | (0.009) | (0.013) | ||||

| Log of tax time × inverse-distance matrix | 0.620 *** | 1.054 *** | 1.885 *** | |||

| (0.034) | (0.033) | (0.043) | ||||

| Log of tax payment × contiguity matrix | 0.637 *** | 0.556 *** | 0.663 *** | |||

| (0.008) | (0.007) | (0.006) | ||||

| Log of tax payment × inverse-distance matrix | −0.652 *** | −0.075 ** | −0.318 *** | |||

| (0.039) | (0.037) | (0.037) | ||||

| Dependent Variables | Tax Evasion Ratio | Tax Evasion Dummy | ||||||

|---|---|---|---|---|---|---|---|---|

| Modifications | Using Tax Complexity Alternative Measurements | Adding a Control Variable | Including Country-Fixed Effects | Using Tax Complexity Alternative Measurements | Adding a Control Variable | Including Country-Fixed Effects | ||

| Specifications | (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) |

| Log of tax time | 0.088 *** | 0.020 * | 0.065 *** | 0.012 *** | ||||

| (0.013) | (0.011) | (0.010) | (0.002) | |||||

| Log of tax payment | 0.086 *** | 0.054 *** | 0.081 *** | 0.138 *** | ||||

| (0.010) | (0.006) | (0.008) | (0.012) | |||||

| TCI | 0.214 *** | 0.078 *** | ||||||

| (0.073) | (0.015) | |||||||

| Tax code complexity | 0.318 *** | 0.478 *** | ||||||

| (0.052) | (0.108) | |||||||

| Tax framework complexity | 0.547 *** | 1.611 *** | ||||||

| (0.111) | (0.248) | |||||||

| Log of GDP | −0.210 *** | −0.211 *** | −0.246 *** | −0.239 *** | −0.404 *** | −0.405 *** | −0.166 *** | −0.475 *** |

| (0.010) | (0.010) | (0.019) | (0.011) | (0.023) | (0.023) | (0.016) | (0.025) | |

| Inflation | 0.015 *** | 0.016 *** | 0.014 *** | 0.018 *** | 0.032 *** | 0.034 *** | 0.013 *** | 0.034 *** |

| (0.001) | (0.001) | (0.001) | (0.001) | (0.002) | (0.002) | (0.001) | (0.002) | |

| Unemployment | −0.007 *** | −0.006 *** | −0.004 *** | 0.005 *** | −0.014 *** | −0.012 *** | −0.003 *** | 0.009 *** |

| (0.001) | (0.001) | (0.001) | (0.001) | (0.002) | (0.002) | (0.001) | (0.002) | |

| Agriculture | 0.032 *** | 0.030 *** | 0.025 *** | 0.031 *** | 0.071 *** | 0.067 *** | 0.018 *** | 0.070 *** |

| (0.001) | (0.001) | (0.003) | (0.001) | (0.003) | (0.003) | (0.002) | (0.003) | |

| Tax burden | −0.001 | −0.001 | −0.010 *** | −0.001 | −0.0002 | −0.0002 | −0.006 | −0.001 |

| (0.001) | (0.001) | (0.001) | (0.001) | (0.001) | (0.001) | (0.001) | (0.001) | |

| Age | 0.029 *** | 0.032 *** | 0.087 *** | 0.032 *** | 0.021 *** | 0.027 *** | 0.050 *** | 0.034 *** |

| (0.002) | (0.002) | (0.004) | (0.002) | (0.004) | (0.004) | (0.003) | (0.004) | |

| Gender | −0.025 *** | −0.028 *** | 0.065 *** | 0.028 *** | −0.025 *** | −0.033 *** | −0.029 *** | 0.030 *** |

| (0.005) | (0.005) | (0.006) | (0.004) | (0.009) | (0.010) | (0.005) | (0.009) | |

| Voice and accountability | 0.037 *** | 0.057 *** | 0.292 *** | 0.013 | 0.043 * | 0.093 *** | 0.189 *** | 0.014 |

| (0.011) | (0.011) | (0.016) | (0.011) | (0.024) | (0.025) | (0.011) | (0.023) | |

| Political stability | −0.009 | −0.012 | −0.075 *** | −0.001 | −0.017 | −0.011 | −0.007 | −0.011 |

| (0.009) | (0.009) | (0.010) | (0.008) | (0.018) | (0.018) | (0.008) | (0.016) | |

| Government effectiveness | −0.229 *** | −0.220 *** | −0.109 *** | −0.283 *** | −0.243 *** | −0.215 *** | −0.100 *** | −0.354 *** |

| (0.023) | (0.023) | (0.031) | (0.024) | (0.049) | (0.050) | (0.025) | (0.050) | |

| Regulatory quality | −0.081 *** | −0.150 *** | −0.199 *** | −0.070 *** | −0.119 *** | −0.285 *** | −0.095 *** | −0.067 * |

| (0.017) | (0.019) | (0.025) | (0.018) | (0.035) | (0.042) | (0.019) | (0.037) | |

| Rule of law | 0.369 *** | 0.427 *** | 0.196 *** | 0.421 *** | 0.721 *** | 0.848 *** | 0.131 *** | 0.807 *** |

| (0.025) | (0.026) | (0.031) | (0.025) | (0.053) | (0.056) | (0.025) | (0.053) | |

| Control of corruption | −0.216 *** | −0.205 | −0.133 *** | −0.210 *** | −0.602 *** | −0.571 *** | −0.159 *** | −0.572 *** |

| (0.017) | (0.017) | (0.024) | (0.018) | (0.040) | (0.041) | (0.020) | (0.042) | |

| Tax morale | −0.018 *** | −0.019 *** | ||||||

| (0.003) | (0.003) | |||||||

| Observations | 46,046 | 46,046 | 29,712 | 46,046 | 46,046 | 46,046 | 29,712 | 46,046 |

| Countries | 83 | 83 | 39 | 83 | 83 | 83 | 39 | 83 |

| Pseudo-R2 | 0.018 | 0.018 | 0.103 | 0.018 | 0.018 | 0.018 | 0.082 | 0.018 |

| Industry and year dummies | Yes | Yes | Yes | Yes | Yes | Yes | Yes | Yes |

| Dependent Variables | Tax Evasion Ratio | Tax Evasion Dummy | ||

|---|---|---|---|---|

| Country Groups | HUP Countries | LLOW Countries | HUP Countries | LLOW Countries |

| Specifications | (1) | (2) | (3) | (4) |

| Log of tax time | 0.046 *** | 0.080 *** | 0.113 *** | 0.058 ** |

| (0.006) | (0.014) | (0.011) | (0.022) | |

| Log of tax payment | 0.104 *** | 0.564 *** | 0.168 *** | 0.561 *** |

| (0.011) | (0.033) | (0.022) | (0.053) | |

| Log of GDP | −0.314 *** | −0.190 *** | −0 712 *** | −0.180 *** |

| (0.024) | (0.029) | (0.046) | (0.046) | |

| Inflation | 0.018 *** | 0.007 *** | 0.026 *** | 0.011 *** |

| (0.001) | (0.0004) | (0.003) | (0.001) | |

| Unemployment | 0.0004 | −0.001 | 0.006 *** | 0.001 |

| (0.001) | (0.002) | (0.002) | (0.003) | |

| Agriculture | 0.042 *** | 0.012 *** | 0.072 *** | 0.012 *** |

| (0.002) | (0.002) | (0.004) | (0.004) | |

| Tax burden | −0.002 *** | −0.019 *** | −0.006 *** | 0.024 *** |

| (0.001) | (0.001) | (0.001) | (0.002) | |

| Age | 0.035 *** | 0.126 *** | 0.039 *** | 0.135 *** |

| (0.002) | (0.006) | (0.004) | (0.009) | |

| Gender | 0.041 *** | −0.138 | 0.076 *** | 0.104 *** |

| (0.007) | (0.008) | (0.013) | (0.013) | |

| Voice and accountability | −0.053 *** | −0.136 *** | −0.024 | −0.116 *** |

| (0.017) | (0.021) | (0.032) | (0.034) | |

| Political stability | −0.064 *** | 0.061 *** | −0.144 *** | 0.157 *** |

| (0.011) | (0.014) | (0.020) | (0.022) | |

| Government effectiveness | −0.190 *** | −0.354 *** | −0.478 *** | −0.460 *** |

| (0.034) | (0.042) | (0.067) | (0.070) | |

| Regulatory quality | −0.082 *** | −0.068 * | −0.029 | −0.017 |

| (0.022) | (0.037) | (0.041) | (0.058) | |

| Rule of law | 0.524 *** | 0.864 *** | 0.798 *** | 1.055 *** |

| (0.033) | (0.035) | (0.063) | (0.057) | |

| Control of corruption | −0.247 *** | 0.052 | −0.393 *** | −0.131 ** |

| (0.020) | (0.034) | (0.039) | (0.055) | |

| Observations | 25,839 | 20,207 | 25,839 | 20,207 |

| Countries | 46 | 37 | 46 | 37 |

| Pseudo-R2 | 0.063 | 0.142 | 0.034 | 0.070 |

| Industry and year dummies | Yes | Yes | Yes | Yes |

| Dependent Variables | Tax Evasion Ratio | Tax Evasion Dummy | ||||

|---|---|---|---|---|---|---|

| Industry | Tertiary | Secondary | Primary | Tertiary | Secondary | Primary |

| Specifications | (1) | (2) | (3) | (4) | (5) | (6) |

| Log of tax time | 0.021 *** | 0.053 *** | 0.109 *** | 0.079 *** | 0.049 *** | 0.081 *** |

| (0.003) | (0.009) | (0.027) | (0.022) | (0.007) | (0.018) | |

| Log of tax payment | 0.013 *** | 0.094 *** | 0.089 *** | 0.050 *** | 0.065 *** | 0.068 *** |

| (0.001) | (0.007) | (0.018) | (0.018) | (0.006) | (0.013) | |

| Log of GDP | −0.003 | −0.241 *** | −0.382 *** | −0.039 | −0.146 *** | −0.231 *** |

| (0.017) | (0.011) | (0.028) | (0.028) | (0.009) | (0.020) | |

| Inflation | 0.004 *** | 0.004 *** | 0.005 *** | 0.006 *** | 0.004 *** | 0.004 *** |

| (0.0005) | (0.0004) | (0.001) | (0.001) | (0.0003) | (0.001) | |

| Unemployment | 0.009 *** | −0.004 *** | −0.007 *** | 0.008 *** | −0.003 *** | −0.004 ** |

| (0.001) | (0.001) | (0.003) | (0.002) | (0.001) | (0.002) | |

| Agriculture | 0.008 *** | 0.012 *** | 0.021 *** | 0.020 *** | 0.009 *** | 0.014 *** |

| (0.002) | (0.001) | (0.003) | (0.003) | (0.001) | (0.002) | |

| Tax burden | −0.001 * | −0.004 *** | 0.003 | −0.004 *** | −0.003 *** | 0.002 |

| (0.001) | (0.001) | (0.002) | (0.001) | (0.001) | (0.001) | |

| Age | 0.007 ** | −0.057 *** | −0.071 *** | 0.023 *** | −0.026 *** | −0.032 *** |

| (0.003) | (0.002) | (0.007) | (0.006) | (0.002) | (0.005) | |

| Gender | −0.003 | 0.073 *** | 0.103 *** | −0.015 | 0.034 *** | 0.054 *** |

| (0.006) | (0.006) | (0.014) | (0.010) | (0.004) | (0.010) | |

| Voice and accountability | −0.073 *** | 0.119 *** | 0.135 *** | −0.110 *** | 0.099 *** | 0.107 *** |

| (0.016) | (0.012) | (0.029) | (0.026) | (0.008) | (0.020) | |

| Political stability | −0.037 *** | −0.035 *** | −0.087 *** | −0.065 *** | −0.022 *** | −0.062 *** |

| (0.011) | (0.009) | (0.019) | (0.019) | (0.007) | (0.014) | |

| Government effectiveness | −0.106 *** | −0.474 *** | −0.398 *** | −0.119 ** | −0.251 *** | −0.208 *** |

| (0.032) | (0.025) | (0.058) | (0.057) | (0.020) | (0.045) | |

| Regulatory quality | −0.084 *** | −0.037 ** | −0.169 *** | −0.096 ** | −0.046 *** | −0.117 *** |

| (0.025) | (0.019) | (0.042) | (0.042) | (0.015) | (0.031) | |

| Rule of law | 0.409 *** | 0.447 *** | 0.460 *** | 0.604 *** | 0.290 *** | 0.259 *** |

| (0.035) | (0.026) | (0.054) | (0.057) | (0.020) | (0.041) | |

| Control of corruption | −0.396 *** | −0.116 *** | −0.099 ** | −0.607 *** | −0.114 *** | −0.080 *** |

| (0.023) | (0.021) | (0.050) | (0.041) | (0.016) | (0.036) | |

| Observations | 15,636 | 24,955 | 5455 | 15,636 | 24,955 | 5455 |

| Countries | 70 | 83 | 75 | 70 | 83 | 75 |

| Pseudo-R2 | 0.108 | 0.065 | 0.052 | 0.049 | 0.046 | 0.045 |

| Industry and year dummies | Yes | Yes | Yes | Yes | Yes | Yes |

| Moran’s I | I | E(I) | sd(I) | Z | p-Value |

| 0.112 | −0.012 | 0.026 | 5.112 | 0.000 | |

| Geary’s C | C | E(C) | sd(C) | Z | p-Value |

| 0.853 | 1.000 | 0.094 | −1.570 | 0.058 |

| Dependent Variable | Tax Evasion Ratio | |

|---|---|---|

| Weighting Matrix | Contiguity Matrix | Inverse-Distance Matrix |

| Specifications | (1) | (2) |

| Log of tax time | 0.112 * | 0.087 * |

| (0.059) | (0.052) | |

| Log of tax payment | 0.122 ** | 0.113 ** |

| (0.061) | (0.048) | |

| Marginal Effect | ||

| Direct Effect | ||

| Log of tax time | 0.116 * | 0.091 * |

| (0.061) | (0.055) | |

| Log of tax payment | 0.126 ** | 0.119 ** |

| (0.063) | (0.050) | |

| Indirect Effect | ||

| Log of tax time | 0.045 | 0.041 |

| (0.036) | (0.035) | |

| Log of tax payment | 0.049 | 0.053 |

| (0.033) | (0.033) | |

| Total Effect | ||

| Log of tax time | 0.162 * | 0.131 |

| (0.090) | (0.086) | |

| Log of tax payment | 0.175 ** | 0.172 ** |

| (0.087) | (0.073) | |

| Observations | 83 | 83 |

| Pseudo-R2 | 0.065 | 0.068 |

| Wald test: spatial terms | 14.02 *** | 12.78 *** |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Saptono, P.B.; Mahmud, G.; Salleh, F.; Pratiwi, I.; Purwanto, D.; Khozen, I. Tax Complexity and Firm Tax Evasion: A Cross-Country Investigation. Economies 2024, 12, 97. https://doi.org/10.3390/economies12050097

Saptono PB, Mahmud G, Salleh F, Pratiwi I, Purwanto D, Khozen I. Tax Complexity and Firm Tax Evasion: A Cross-Country Investigation. Economies. 2024; 12(5):97. https://doi.org/10.3390/economies12050097

Chicago/Turabian StyleSaptono, Prianto Budi, Gustofan Mahmud, Fauzilah Salleh, Intan Pratiwi, Dwi Purwanto, and Ismail Khozen. 2024. "Tax Complexity and Firm Tax Evasion: A Cross-Country Investigation" Economies 12, no. 5: 97. https://doi.org/10.3390/economies12050097

APA StyleSaptono, P. B., Mahmud, G., Salleh, F., Pratiwi, I., Purwanto, D., & Khozen, I. (2024). Tax Complexity and Firm Tax Evasion: A Cross-Country Investigation. Economies, 12(5), 97. https://doi.org/10.3390/economies12050097