Industrial Policy Environment and Private Equity Placement: Evidence from Chinese Real Estate Firms

Abstract

1. Introduction

2. Literature Review and Hypotheses

2.1. Literature Review

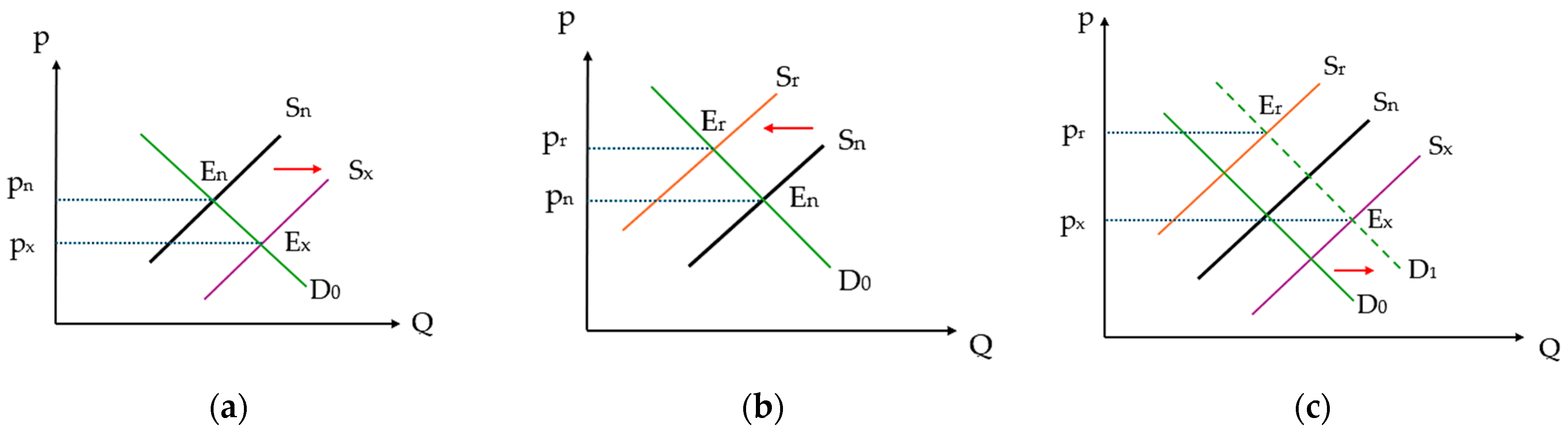

2.2. Hypotheses

3. Methodology

3.1. Data Selection

3.2. Announcement Effect Estimation

3.3. Discount Calculation

3.4. Regressions and Variable Definitions

4. Results and Analysis

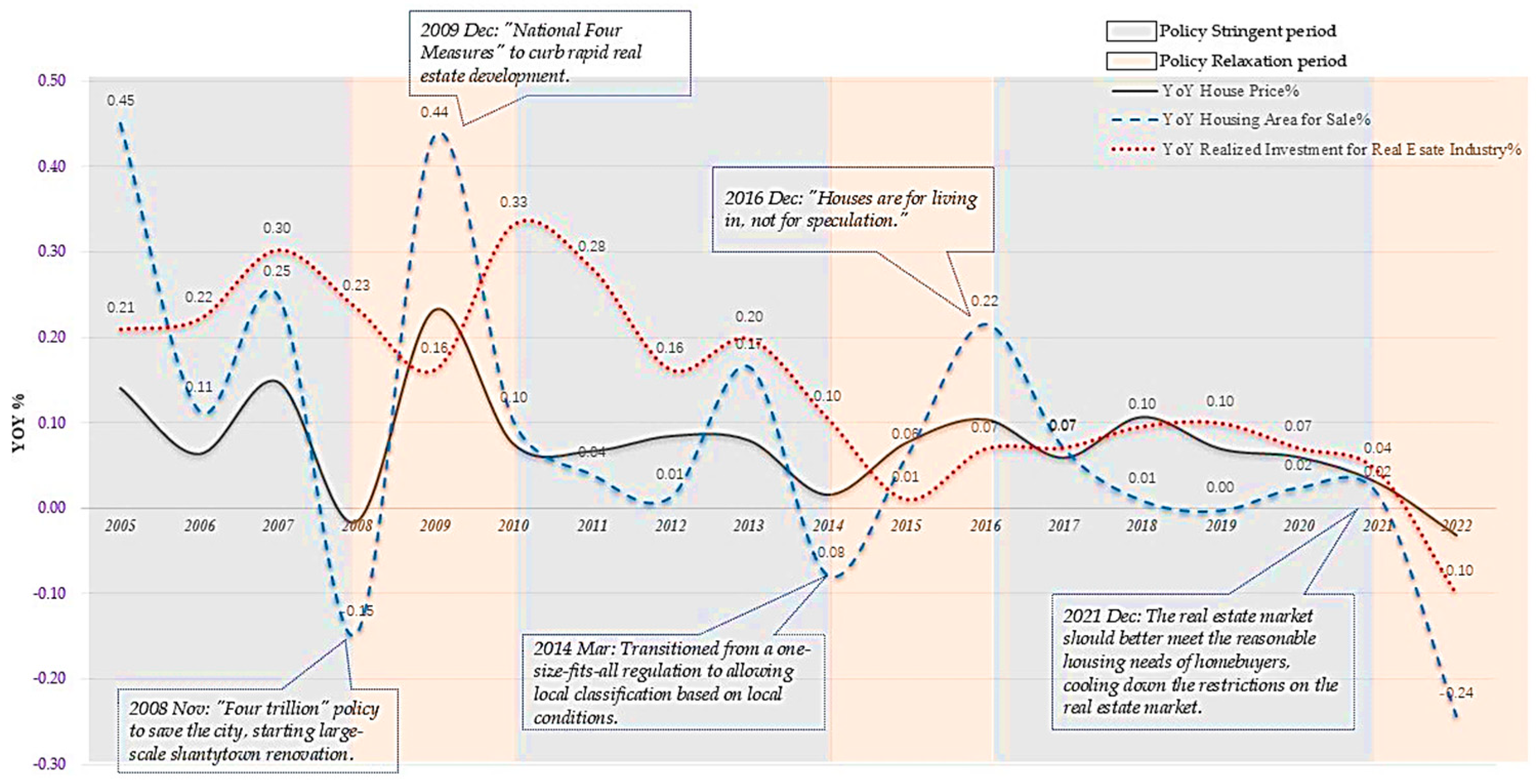

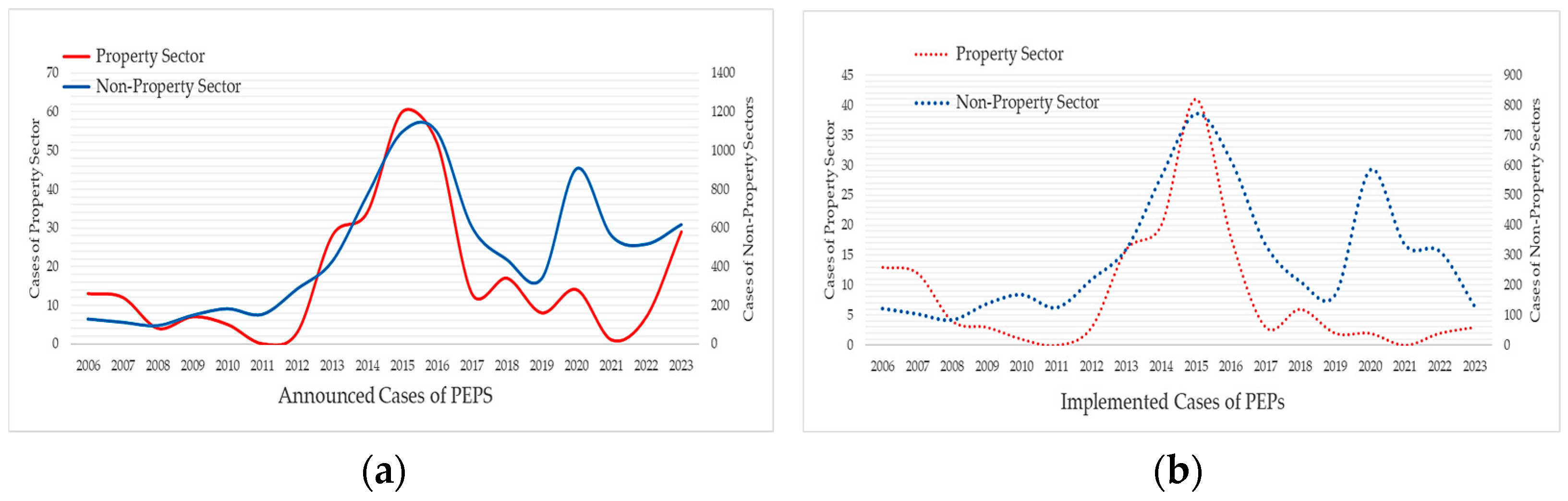

4.1. Policy Environment History and PEP Transactions in China

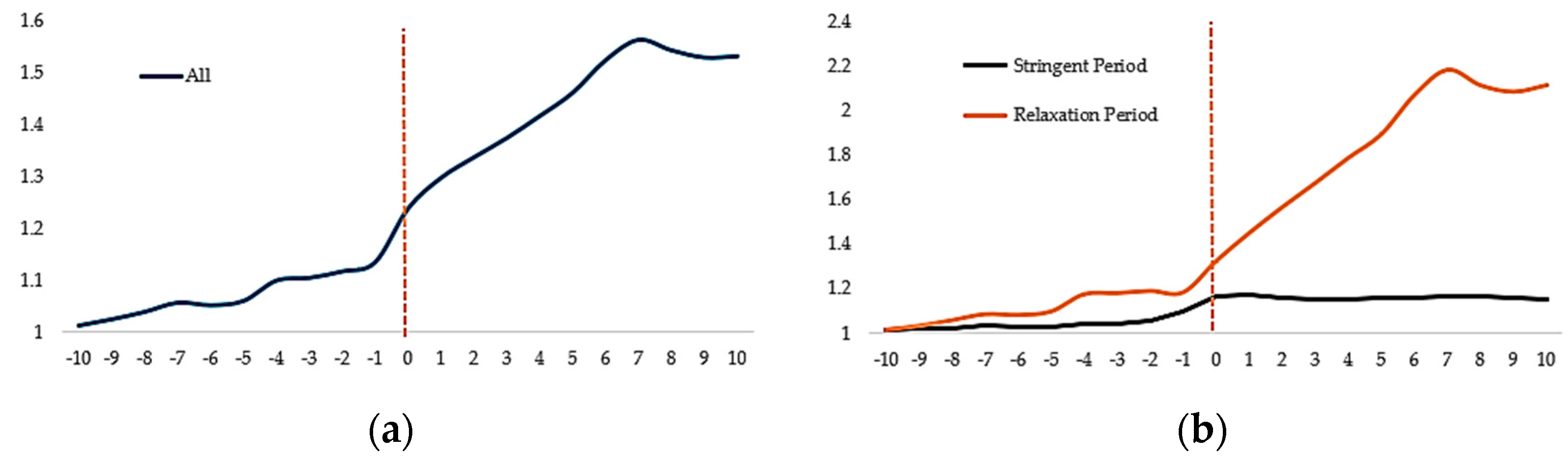

4.2. Announcement Effects in Various Policy Environments

4.3. The Multiple Regression Analysis on CAR in Announcement Periods

4.4. Discount Comparisons across Different Policy Environments

4.5. The Multiple Regression Analysis on Discount

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

Appendix A

Appendix B

| 1 | |

| 2 | For details regarding equity placement regulations in the Hong Kong market, please refer to the Rules Governing the Listing of Securities on The Stock Exchange of Hong Kong Limited, as well as other relevant provisions. |

| 3 | There are instances where companies are included in or excluded from the real estate sector due to changes in their primary business operations. This study primarily focuses on whether companies belonged to the real estate industry during the period of the PEP transaction. |

| 4 | Other financial activities include public offerings, rights issues, convertible debt, etc. |

| 5 | When a listed company encounters financial difficulties or other operational issues, the exchange typically labels its stock as “PT” (Particular Transfer) or “ST” (Special Treatment). Investors should exercise caution with these stocks due to their higher risk and the possibility of delisting. |

| 6 | The method for calculating the discount rate after consolidation is detailed in Appendix A. |

| 7 | For further details on the regulation and issuance mechanisms of PEP transactions, see Ning and Jalil (2023) and Song (2014). |

| 8 | During this period, the lower number of successfully completed transactions was due to several PEPs still being in the process of implementation. |

| 9 | In the models for the policy loosening period, the market sentiment variable Bull exhibited significant multicollinearity with the models. Consequently, this variable was excluded from Models (3) and (4). |

| 10 | The formula for BHAR is shown in Appendix B. |

| 11 | Aside from the unexpected bankruptcy of China Evergrande, other major industry players, such as Country Garden, have also faced significant debt crises. Notably, China Vanke, the first publicly listed real estate company in China, reported its first loss since its initial public offering in 2024. This reflects the challenging operating conditions faced by the entire industry at this stage. |

References

- An, Hui, and Ruidong Wang. 2013. An Empirical Analysis of Influencing Factors in Real Estate Prices of China and The Current Real Estate Regulating Policy. Finance & Economics 3: 115–24. [Google Scholar] [CrossRef]

- Baek, Jae-Seung, Jun-Koo Kang, and Inmoo Lee. 2006. Business Groups and Tunneling: Evidence from Private Securities Offerings by Korean Chaebols. The Journal of Finance 61: 2415–49. [Google Scholar] [CrossRef]

- Barclay, Michael J., Clifford G. Holderness, and Dennis P. Sheehan. 2007. Private Placements and Managerial Entrenchment. Journal of Corporate Finance 13: 461–84. [Google Scholar] [CrossRef]

- Bohnenkamp, Guido, and Christian Kammann. 2024. Current Developments on the Chinese Real Estate Market. International Journal of Innovation Economic Development 9: 7–14. [Google Scholar] [CrossRef]

- Brophy, David J., Paige Ouimet, and Clemens Sialm. 2004. PIPE Dreams? The Performance of Companies Issuing Equity Privately. Cambridge: National Bureau of Economic Research. [Google Scholar] [CrossRef]

- Chaplinsky, Susan, and David Haushalter. 2005. Financing Under Extreme Uncertainty: Evidence from Private Investments in Public Equities. Available online: https://ssrn.com/abstract=690186 (accessed on 20 April 2024).

- Chen, Xiao, and Kun Wang. 2005. Related Party Transactions, Corporate Governance and State Ownership Reform. Economic Research Journal 4: 77–128. [Google Scholar]

- Chen, Yan, and Guangzhen Lin. 2013. Research on the Policy Control of Commercial Real Estate in Shenzhen. Construction Economy 7: 71–74. [Google Scholar] [CrossRef]

- Cronqvist, Henrik, and Mattias Nilsson. 2004. The choice between rights offerings and private equity placements. Journal of Financial Economics 78: 375–407. [Google Scholar] [CrossRef]

- De Jong, Frank, Angelien Kemna, and Teun Kloek. 1992. A contribution to event study methodology with an application to the Dutch stock market. Journal of Banking Finance & Trade Economics 16: 11–36. [Google Scholar] [CrossRef]

- Dong, Gang Nathan, Ming Gu, and Hua He. 2020. Invisible Hand and Helping Hand: Private Placement of Public Equity in China. Journal of Corporate Finance 61: 101400. [Google Scholar] [CrossRef]

- Edgerton, Jesse. 2012. Agency Problems in Public Firms: Evidence from Corporate Jets in Leveraged Buyouts. The Journal of Finance 67: 2187–213. [Google Scholar] [CrossRef]

- Fang, Hanming, Quanlin Gu, Wei Xiong, and Li-An Zhou. 2016. Demystifying the Chinese housing boom. NBER Macroeconomics Annual 30: 105–66. [Google Scholar] [CrossRef]

- Folta, Timothy B., and Jay J. Janney. 2004. Strategic benefits to firms issuing private equity placements. Strategic Management Journal 25: 223–42. [Google Scholar] [CrossRef]

- Ge, Lulan, Zhiyuan Li, Yongming Liu, and Ling Feng. 2023. Real Estate Credit Policies, Investment, and Macroeconomic Fluctuations in China. Nankai Economic Studies 2: 3–23. [Google Scholar] [CrossRef]

- Geng, Jianxin, Yuejin Lv, and Xiaoping Zou. 2011. An Empirical Study on the Long-Term Return Performance of Private Placements of Listed Companies in China. Journal of Audit & Economics 26: 52–58. [Google Scholar]

- Gu, Haifeng, and Di Wu. 2014. Research on the influencing factors of the announcement effect of Private placement of Chinese listed companies: An empirical analysis based on event study method. Review of Economy and Management 30: 82–88. [Google Scholar] [CrossRef]

- He, Xianjie, and Hongjun Zhu. 2009. Tunneling, Information Asymmetry and Private Placement Discount. China Accounting Review 7: 283–98. [Google Scholar]

- Hertzel, Michael, and Richard L. Smith. 1993. Market Discounts and Shareholder Gains for Placing Equity Privately. The Journal of Finance 48: 459–85. [Google Scholar] [CrossRef]

- Hertzel, Michael, Michael Lemmon, James S. Linck, and Lynn Rees. 2002. Long-run Performance Following Private Placements of Equity. The Journal of Finance 57: 2595–617. [Google Scholar] [CrossRef]

- Hu, Lipeng, and Yun Zhang. 2016. Announcement Effects of the Seasoned Equity Offerings and Private Placements of A-share Listed Companies. Finance Forum 21: 66–80. [Google Scholar] [CrossRef]

- Huaxi-Security. 2023. Historical Review of Real Estate Policies. Available online: https://pdf.dfcfw.com/pdf/H301_AP202305101586440193_1.pdf (accessed on 17 July 2024).

- Jensen, Michael C. 1993. The Modern Industrial Revolution, Exit, And the Failure of Internal Control Systems. The Journal of Finance 48: 831–80. [Google Scholar] [CrossRef]

- Jensen, Michael C., and William H. Meckling. 1976. Theory of the Firm: Managerial Behavior, Agency Costs and Ownership Structure. Journal of Financial Economics 3: 305–60. [Google Scholar] [CrossRef]

- Kang, Jun-Koo, Yong-Cheol Kim, and René M. Stulz. 1999. The Underreaction Hypothesis and The New Issue Puzzle: Evidence from Japan. The Review of Financial Studies 12: 519–34. [Google Scholar] [CrossRef]

- Kato, Kiyoshi, and James S. Schallheim. 1993. Private Equity Financings in Japan and Corporate Grouping (Keiretsu). Pacific-Basin Finance Journal 1: 287–307. [Google Scholar] [CrossRef]

- Krishnamurthy, Srinivasan, Paul Spindt, Venkat Subramaniam, and Tracie Woidtke. 2005. Does Investor Identity Matter in Equity Issues? Evidence From Private Placements. Journal of Financial Intermediation 14: 210–38. [Google Scholar] [CrossRef]

- Li, Minghui. 2009. The influence of ownership structure and corporate governance on equity agency cost: A study based on the data of Chinese listed companies from 2001 to 2006. Journal of Financial Research 2: 149–68. [Google Scholar]

- Li, Xiangfei, Zaisheng Zhang, and Chao Huang. 2014. Study of Influence Estate Control Policies on Real Estate Index Based on the Method of Hilbert-Huang Transform. Systems Engineering-Theory & Practice 34: 1369–78. [Google Scholar]

- Lin, Bin, and Jing Rao. 2009. Why do Listed Companies Disclose the Auditor’s Internal Control Reports voluntarily?—An Empirical Study Based on Signaling Theory in China. Accounting Research 2: 45–94. [Google Scholar] [CrossRef]

- Lin, Frank, and Gerard Gannon. 2007. Private Placement and Share Price Reaction: Evidence from The Australian Biotechnology and Health Care Sector. Available online: http://citeseerx.ist.psu.edu/document?repid=rep1&type=pdf&doi=9b295d40433342e96b4c31df137a6c28e1d4df40 (accessed on 16 April 2024).

- Liu, Lixue. 2008. An empirical study on stock price effect of Private placement announcements of Chinese listed companies. Pioneering with Science & Technology Monthly 10: 40–42. [Google Scholar] [CrossRef]

- Louisiana, Dalia, Eric Higgins, H. Friday, and Joseph Mason. 2007. Positive Performance and Private Equity Placements: Outside Monitoring or Inside Expertise? Journal of Real Estate Portfolio Management 13: 389–400. [Google Scholar] [CrossRef]

- Lu, Deng, Sifei Li, and Weixing Wu. 2011. Market Discounts and Announcement Effects of Private Placements: Evidence from China. Applied Economics Letters 18: 1411–14. [Google Scholar] [CrossRef]

- Lu, Rui, Minghai Wei, and Wenjing Li. 2008. Managerial Power, Perquisite Consumption and Performance of Property Right: Evidence from Chinese Listed Companies. Nankai Business Review 5: 85–112. [Google Scholar] [CrossRef]

- Lu, Zhenghua, and Jia Chen. 2015. Cash Dividend Policy and Effect of Private Placement Announcement. Finance and Accounting Monthly 15: 115–19. [Google Scholar] [CrossRef]

- Marciukaityte, Dalia, Samuel H. Szewczyk, and Raj Varma. 2005. Investor Overoptimism and Private Equity Placements. Journal of Financial Research 28: 591–608. [Google Scholar] [CrossRef]

- Myers, Stewart C., and Nicholas S. Majluf. 1984. Corporate Financing and Investment Decisions When Firms Have Information That Investors Do Not Have. Journal of Financial Economics 13: 187–221. [Google Scholar] [CrossRef]

- Ning, Yuping, and Rohaya Binti Abdul Jalil. 2023. Private Placement of China-Listed Real Estate Firms: A Conceptual Idea. Journal of Risk and Financial Management 16: 516. [Google Scholar] [CrossRef]

- Rogoff, Kenneth, and Yuanchen Yang. 2021. Has China’s housing production peaked? China World Economy 29: 1–31. [Google Scholar] [CrossRef]

- Shi, Jinyan, Conghui Yu, Sicen Guo, and Yanxi Li. 2020. Market Effects of Private Equity Placement: Evidence from Chinese Equity and Bond Markets. The North American Journal of Economics and Finance 53: 101214. [Google Scholar] [CrossRef]

- Song, He, Yao Li, and Yu Long. 2019. Does Venture Capital Affect the Underpricing Rate of Listed Companies’ Private Placement? Journal of Finance and Economics 45: 59–72. [Google Scholar] [CrossRef]

- Song, Pengcheng. 2014. Private Placement of Public Equity in China. Berlin/Heidelberg: Springer. [Google Scholar]

- Song, Xin, Xiaodi Liu, and Huiyu Chen. 2024. Driving force of value reversal in Chinese overleveraged firms: The mechanism and path of private placement. PLoS ONE 19: e0303544. [Google Scholar] [CrossRef]

- Sun, Dianbo. 2015. An Empirical Study on the Effect of Private Placement Announcements of Listed Companies in China. Times Finance 33: 143–59. [Google Scholar]

- Tan, Ruth S. K., Pheng L. Chng, and Y. H. Tong. 2002. Private placements and rights issues in Singapore. Pacific-Basin Finance Journal 10: 29–54. [Google Scholar] [CrossRef]

- Tao, Qizhi, Zhao Zhao, Mingming Zhang, and Xueman Xiang. 2018. Managerial Placement and Entrenchment. Emerging Markets Finance and Trade 54: 3366–83. [Google Scholar] [CrossRef]

- Veld, Chris, Patrick Verwijmeren, and Yuriy Zabolotnyuk. 2020. Wealth Effects of Seasoned Equity Offerings: A Meta-Analysis. International Review of Finance 20: 77–131. [Google Scholar] [CrossRef]

- Wang, Huacheng, Jinzhao Liu, Shenghao Gao, and Xiaoquan Qing. 2020. Tunneling or Signaling? An Analysis on Big Shareholder Participation and SEO Discount. Management Review 32: 266–79. [Google Scholar] [CrossRef]

- Wruck, Karen Hopper. 1989. Equity ownership concentration and firm value: Evidence from private equity financings. Journal of Financial Economics 23: 3–28. [Google Scholar] [CrossRef]

- Wruck, Karen Hopper, and Yilin Wu. 2009. Relationships, Corporate Governance, And Performance: Evidence from Private Placements of Common Stock. Journal of Corporate Finance 15: 30–47. [Google Scholar] [CrossRef]

- Wu, Jingfeng. 2016. Empirical Test of Short-term Market Reaction after Private Placement. Statistics & Decision 17: 156–59. [Google Scholar] [CrossRef]

- Xiong, Wei. 2023. Derisking Real Estate in China’s Hybrid Economy. NBER Working Paper w31118. Available online: https://ssrn.com/abstract=4413855 (accessed on 14 July 2024).

- Xu, Liping, Yu Xin, and Gongmeng Chen. 2006. Ownership Concentration Outside Blockholders, and Operating Performance: Evidence from China’s Listed Companies. Economic Research Journal 1: 90–100. [Google Scholar]

- Xu, Shoufu. 2010. Research on the announcement effect of private placement of listed companies and its influencing factors. Securities Market Herald 5: 65–72. [Google Scholar]

- Xu, Shoufu. 2011. An Analysis on the External Factors Affecting the Preference for Private Placements of Public Companies. Journal of Shanghai Economic Management College 9: 37–43. [Google Scholar] [CrossRef]

- Xu, Suichen, Janice How, and Peter Verhoeven. 2017. Corporate governance and private placement issuance in Australia. Accounting Finance & Trade Economics 57: 907–33. [Google Scholar] [CrossRef]

- Yao, Dongmin, Li Jiang, and Feiran Wang. 2022. Administrative Expenses, Transaction Costs and Total Factor Productivity of Enterprises: A Quasi-Experimental Study Based on the Reform of “Reform of Business Administration”. World Economic Papers 2: 36–56. [Google Scholar]

- Yermack, David. 2006. Flights of Fancy: Corporate Jets, CEO Perquisites, and Inferior Shareholder Returns. Journal of Financial Economics 80: 211–42. [Google Scholar] [CrossRef]

- Yi, Tian, Yunjue Wang, and Weicong Yang. 2006. Private placement creates new investment opportunities. Securities Guide 3: 35–37. [Google Scholar]

- Yu, Jun, Shuzhen Wang, and Zhonghong Cao. 2016. Private Placement Shareholder Wealth Effect from Perspective of Investor Sentiment. Journal of Shandong University of Finance and Economics 28: 11–18. [Google Scholar] [CrossRef]

- Yu, Jun, Zhubao Wei, Shuzhen Wang, and Jing Tang. 2013. Private Placement Discount of Chinese Listed Companies Based on the Perspective of the Investors’ Sentiment. Presented at the 19th International Conference on Industrial Engineering and Engineering Management, Changsha, China, October 27–29; pp. 121–30. [Google Scholar]

- Zhang, Ming, and Siyong Guo. 2009. Private Placement under the Control of Major Shareholder and Wealth Tunneling. Accounting Research, 78–86+97. [Google Scholar] [CrossRef]

- Zhang, Weidong. 2007. The Short-run Performance of Private Investment in Public Equity and Complete Listing. Accounting Research 12: 63–97. [Google Scholar] [CrossRef]

- Zhang, Weidong, and Dezhong Li. 2008. The influencial factors of Private Equity’s (PE) discount rate and the empirical study of the relationship between them and the short-term stock price—From the China’s listed companies’ empirical evidence. Accounting Research 9: 73–80. [Google Scholar] [CrossRef]

- Zhang, Weidong, Jenny Jing Wang, Guomin Luo, and Yanqi Sun. 2021. Tunnelling in asset-injecting private placements: Evidence from China. Accounting and Finance 61: 5501–22. [Google Scholar] [CrossRef]

- Zhang, Xinyuan. 2017. The Research on Announcement Effect of A-share Listed Company’s Private Placements in China: A Case study of the Real Estate Industry. Master’s thesis, Shanxi University of Finance and Economics, Taiyuan, China. [Google Scholar]

- Zhou, Dongxia. 2016. A study on the impact of private placement of A-share listed companies on stock prices—Taking the real estate industry as an example. Modern Business Trade Industry 37: 104–5. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| (a) | ||||||

|---|---|---|---|---|---|---|

| Variable | N | Mean | Median | SD | Max | Min |

| Discount | 126 | 0.105 | 0.155 | 0.408 | 0.763 | −1.847 |

| Fraction | 126 | 0.267 | 0.229 | 0.190 | 1.189 | 0.015 |

| Proceed | 126 | 3.317 | 2.050 | 5.960 | 64.540 | 0.265 |

| Firm Size | 126 | 30.695 | 8.045 | 90.627 | 856.203 | 0.119 |

| Top1 | 126 | 39.792 | 41.260 | 17.070 | 89.410 | 6.500 |

| Leverage | 126 | 0.662 | 0.705 | 0.172 | 0.914 | 0.028 |

| ROE | 126 | 0.093 | 0.090 | 0.095 | 0.433 | −0.315 |

| Tobin’s Q | 126 | 1.653 | 1.228 | 1.962 | 19.094 | 0.776 |

| (b) | ||||||

| Policy Environments | Freq. | Percent% | Cum.% | |||

| Cases in Policy Relaxation Period | 61 | 48.41 | 48.41 | |||

| Cases in Policy Stringent Period | 65 | 51.59 | 100 | |||

| Total | 126 | 100 | ||||

| Variables | Definition | Reference/Source |

|---|---|---|

| Policy | Dummy variable: If the industrial policy environment is tightening at the time of the event, Policy is equal to 1; otherwise, it is equal to 0. | Author |

| CAR | Cumulative abnormal return; the calculation method is referenced in Equation (3). | Zhang (2007) |

| Discount_p | Discount rate; the calculation method is referenced in Equation (6). Discount_p represents the discount rate calculated using the closing price on the tenth trading day after the event as the benchmark. | Wruck and Wu (2009) |

| Discount_b | Discount rate; the calculation method is referenced in Equation (6). Discount_b represents the discount rate calculated using the closing price on the last trading day before the event. | Wruck and Wu (2009) |

| Ctrl_Shareholder | Dummy variable: If the controlling shareholder or their related parties participate in the transaction, Ctrl_Shareholder is equal to 1; otherwise, it is equal to 0. | Sun (2015) |

| Proceed | Natural logarithm of the funds raised from the transaction. | Barclay et al. (2007) |

| Ln_Share | Natural logarithm of the number of shares issued in the transaction. | Wu (2016) |

| Auction | Dummy variable: If the pricing mechanism is through an auction, Auction is equal to 1; otherwise, it is equal to 0. | Wang et al. (2020) |

| Fraction | The percentage of shares issued as a proportion of the total shares outstanding after the transaction. | Hertzel and Smith (1993) |

| Rsize | The amount raised as a percentage of the total assets at the end of the year preceding the event. | Tao et al. (2018) |

| Top1 | Shareholding percentage of the largest controlling shareholder in the year preceding the event. | Zhang et al. (2021) |

| Top3 | Shareholding percentage of the top three controlling shareholders in the year preceding the event. | Chen and Wang (2005) |

| Tobinq | Tobin’s Q ratio in the year preceding the event; calculated as Market Value/Total Assets. | Jensen and Meckling (1976) |

| Tobinq1 | Tobin’s Q ratio in the year preceding the event; calculated as Market Value/(Total Assets − Net Intangible Assets − Net Goodwill). | CSMAR |

| ROE | Return on equity in the year preceding the event. | Tao et al. (2018) |

| ROA | Return on assets in the year preceding the event. | Tao et al. (2018) |

| Size | Natural logarithm of the total assets in the year preceding the event. | Hertzel and Smith (1993) |

| Ln_MV | Natural logarithm of market value in the year preceding the event. | Wruck (1989) |

| Leverage | Debt ratio of the company in the year preceding the event. | Zhang (2007) |

| Chg_Lev | Change in leverage; the difference between the debt ratio in the event year and the debt ratio in the preceding year. | Tao et al. (2018) |

| Bull | Dummy variable: If the market is in a bull phase at the time of the event, Bull is equal to 1; otherwise, it is equal to 0. | Sun (2015) |

| Board | Natural logarithm of the number of board members. | Li (2009) |

| Indboard | The proportion of independent directors; calculated as Number of Independent Directors/Total Number of Board Members. | Li (2009) |

| Mfee | Management expense ratio in the year preceding the event; calculated as Administrative Expenses/Operating Income. | Lu et al. (2008) |

| Balance | Equity balance in the year preceding the event; calculated as Sum of the Shareholding Ratio of the Second to Fifth Largest Shareholders/Shareholding Ratio of the Largest Shareholder. | Xu et al. (2006) |

| Period | Policy Stages | Policy Trend | Milestone | Policy Name and Main Content |

|---|---|---|---|---|

| 1978–1991 | Real Estate Enlightenment | Neutral | 1980 Dec | National Urban Planning Meeting Summary: Introduced policies on the comprehensive development of real estate and the levy of urban land use fees. |

| 1992–1997 | Real Estate Regulation Start | Stringent | 1993 Jun | The “National 16 Measures”: Strengthened the macro-management of the real estate market to promote healthy development. |

| 1998–2002 | Full Marketization | Relaxation | 1998 Jul | Notice on Further Deepening the Reform of the Urban Housing System and Accelerating Housing Construction: Ended the physical allocation of housing and initiated the gradual implementation of the monetary distribution of housing. |

| 2003–2007 | Market Regulation | Stringent | 2003 Jun | Notice on Further Strengthening the Management of Real Estate Credit Business: Enhanced the management of real estate development loans and prohibited cross-regional lending. |

| 2008–2009 | Investment for Market Rescue | Relaxation | 2008 Nov | “Four Trillion” Policy: Focused on renovating approximately 150 million square meters of dilapidated housing across China, including shantytowns. |

| 2010–2013 | Curbing Rapid Housing Price Increase | Stringent | 2010 Apr | Notice on Resolutely Curbing the Rapid Increase of Housing Prices in Some Cities: Allowed commercial banks to suspend loans for third and subsequent housing purchases and for non-local residents unable to provide proof of local tax or social insurance. |

| 2014–2016 | Policy Relaxation for Inventory Reduction | Relaxation | 2014 Mar | Government Work Report: Introduced differentiated regulations for various cities, aimed at increasing the supply of small- and medium-sized commercial and shared-property housing, curbing speculative investment, and promoting stable market development. |

| 2017–2021 | House for Living, Not for Speculation | Stringent | 2016 Dec | Central Economic Work Conference: Emphasized “houses are for living, not for speculation” as a core principle. Used financial, land, fiscal, investment, and legislative tools to establish systems aligning with national conditions and market rules. |

| Since 2022 | Stabilizing Real Estate Industry | Relaxation | 2022 Mar | Government Work Report: Continued the principle of “houses are for living, not speculation”, promoted new housing models, integrated renting and buying, and boosted the rental market; also focused on stabilizing housing prices and supporting the sector. |

| (a) | ||||||||

|---|---|---|---|---|---|---|---|---|

| Window | All | Stringent | Relaxation | DIF | T-Test | Wilcoxon Test | ||

| N | 109 | 59 | 50 | T-Value | p-Value | Z-Value | p-Value | |

| [−10, 10] | 0.1335 *** | 0.0665 ** | 0.2125 *** | −0.1459 | 2.8215 | 0.0057 | 2.9130 | 0.0034 |

| [−5, 5] | 0.1026 *** | 0.0655 *** | 0.1464 *** | −0.0809 | 2.0322 | 0.0446 | 1.7880 | 0.0742 |

| [−3, 3] | 0.0800 *** | 0.0610 *** | 0.1024 *** | −0.0414 | 1.2589 | 0.2108 | 1.0890 | 0.2789 |

| [−1,1] | 0.0650 *** | 0.0616 *** | 0.0690 *** | −0.0074 | 0.3561 | 0.7225 | 0.6080 | 0.5466 |

| (b) | ||||||||

| Window | All | Stringent | Relaxation | DIF | T-Test | Wilcoxon Test | ||

| N | 109 | 59 | 50 | T-Value | p-Value | Z-Value | p-Value | |

| [−10, 10] | 0.5962 ** | 0.3163 *** | 0.9263 | −0.6100 | 1.1464 | 0.2542 | 0.6870 | 0.4954 |

| [−5, 5] | 0.5385 ** | 0.3006 *** | 0.8193 | −0.5187 | 1.0038 | 0.3177 | −0.2310 | 0.8203 |

| [−3, 3] | 0.4511 ** | 0.2882 *** | 0.6434 | −0.3551 | 0.8725 | 0.3849 | −1.0090 | 0.3156 |

| [−1, 1] | 0.3916 ** | 0.2855 *** | 0.5168 | −0.2313 | 0.6869 | 0.4936 | −1.4900 | 0.1375 |

| Event Date | −10 | −9 | −8 | −7 | −6 | ||

|---|---|---|---|---|---|---|---|

| All | 0.0133 | 0.0119 | 0.0138 | 0.0169 | −0.0045 | ||

| Stringent Period | 0.0138 | 0.0064 | 0.0049 | 0.0094 | −0.0057 | ||

| Relaxation Period | 0.0126 | 0.0183 | 0.0242 | 0.0258 | −0.0031 | ||

| Event Date | −5 | −4 | −3 | −2 | −1 | 0 | |

| All | 0.0077 | 0.0368 | 0.0047 | 0.0111 | 0.0157 | 0.0908 *** | |

| Stringent Period | 0.002 | 0.0078 | 0.0053 | 0.0133 | 0.0336 | 0.0666 | |

| Relaxation Period | 0.0145 | 0.0709 * | 0.004 | 0.0085 | −0.0053 | 0.1195 *** | |

| Event Date | 1 | 2 | 3 | 4 | 5 | ||

| All | 0.0474 | 0.0304 | 0.0277 | 0.0307 | 0.0315 | ||

| Stringent Period | 0.0069 | −0.0116 | −0.0076 | −0.0004 | 0.0076 | ||

| Relaxation Period | 0.0951 ** | 0.0801 ** | 0.0695 *** | 0.0674 ** | 0.0596 ** | ||

| Event Date | 6 | 7 | 8 | 9 | 10 | ||

| All | 0.0428 | 0.0257 | −0.0127 | −0.0089 | 0.0015 | ||

| Stringent Period | 0.0000 | 0.0013 | 0.0035 | −0.0050 | −0.0091 | ||

| Relaxation Period | 0.0932 ** | 0.0544 ** | −0.032 | −0.0135 | 0.0141 | ||

| (a) | (b) | ||||

|---|---|---|---|---|---|

| (1) | (2) | (3) | (4) | ||

| Variables | CAR [−3, 3] | CAR [−5, 5] | Variables | CAR [−3, 3] | CAR [−5, 5] |

| Constant | 0.562 | 1.017 | Constant | 0.505 | 1.236 |

| (0.958) | (1.544) | (0.708) | (1.504) | ||

| Policy | 0.015 | 0.035 | Policy | −0.098 | −0.098 |

| (0.109) | (0.245) | (−0.760) | (−0.786) | ||

| Discount_p | 0.105 * | 0.146 * | Discount_b | 0.006 | 0.035 |

| (1.753) | (1.950) | (0.117) | (0.600) | ||

| Proceed | 0.003 ** | 0.006 *** | Proceed | 0.003 ** | 0.006 *** |

| (2.283) | (3.182) | (2.326) | (3.503) | ||

| Top1 | −0.001 | −0.001 | Top3 | 0.000 | −0.001 |

| (−0.989) | (−0.673) | (0.251) | (−0.608) | ||

| Tobinq | 0.051 | 0.007 | Tobinq1 | 0.078 ** | 0.060 |

| (1.145) | (0.137) | (2.022) | (1.378) | ||

| ROE | −0.018 | −0.026 | ROA | −0.767 | −0.914 |

| (−0.107) | (−0.128) | (−1.519) | (−1.494) | ||

| Size | 0.002 | −0.017 | Ln_MV | −0.004 | −0.030 |

| (0.117) | (−0.761) | (−0.169) | (−1.124) | ||

| Leverage | 0.374 * | 0.477 * | Leverage | 0.341 | 0.533 ** |

| (1.813) | (1.996) | (1.529) | (2.028) | ||

| Chg_Lev | 0.384 *** | 0.593 *** | Chg_Lev | 0.384 ** | 0.657 *** |

| (2.659) | (3.200) | (2.501) | (3.500) | ||

| Bull | −0.612 *** | −0.461 *** | Bull | −0.551 *** | −0.376 *** |

| (−6.304) | (−4.675) | (−5.832) | (−3.716) | ||

| Board | −0.178 | −0.240 | Board | −0.132 | −0.241 |

| (−1.415) | (−1.569) | (−0.982) | (−1.455) | ||

| Indboard | 0.540 | 0.671 | Indboard | 0.737 | 0.795 |

| (0.708) | (0.782) | (0.892) | (0.835) | ||

| Mfee | 0.369 *** | 0.535 *** | Mfee | 0.324 *** | 0.464 *** |

| (3.903) | (4.351) | (2.958) | (3.447) | ||

| Year-Fixed | Yes | Yes | Year−Fixed | Yes | Yes |

| Area-Fixed | Yes | Yes | Area−Fixed | Yes | Yes |

| N | 102 | 102 | N | 102 | 102 |

| R2 | 0.536 | 0.572 | R2 | 0.506 | 0.540 |

| Adj R2 | 0.268 | 0.324 | Adj R2 | 0.221 | 0.274 |

| F | 20.21 | 17.61 | F | 21.89 | 22.20 |

| Samples | N | Mean | Median | Sign | Coefficient | |

|---|---|---|---|---|---|---|

| Year < 2014 | Leverage | 59 | 0.6727 | 0.7034 | + | Insignificant |

| Chg_Lev | 59 | −0.0098 | −0.0070 | + | Significant | |

| Year > 2014 | Leverage | 50 | 0.6722 | 0.7090 | Mixed | Insignificant |

| Chg_Lev | 50 | −0.0016 | −0.0066 | Mixed | Insignificant |

| (1) | (2) | (3) | (4) | |

|---|---|---|---|---|

| Policy Tightening | Policy Relaxation | |||

| Variables | CAR [−3, 3] | CAR [−5, 5] | CAR [−3, 3] | CAR [−5, 5] |

| Constant | 1.016 | 1.138 | 0.085 | 0.891 |

| (1.435) | (1.295) | (0.119) | (1.210) | |

| Discount_p | 0.054 | 0.080 | 0.649 *** | 0.761 *** |

| (0.996) | (1.266) | (5.227) | (4.505) | |

| Proceed | 0.041 ** | 0.030 | 0.001 | 0.004 ** |

| (2.137) | (1.132) | (0.922) | (2.146) | |

| Top1 | −0.001 | −0.002 | 0.001 | 0.003 * |

| (−1.125) | (−1.289) | (0.834) | (1.743) | |

| Tobinq | 0.088 | 0.036 | −0.122 ** | −0.182 ** |

| (1.313) | (0.428) | (−2.643) | (−2.622) | |

| ROE | 0.292 | 0.258 | −0.534 ** | −1.100 *** |

| (1.304) | (1.009) | (−2.382) | (−3.463) | |

| Size | −0.033 | −0.046 | −0.021 | −0.052 * |

| (−1.399) | (−1.477) | (−0.838) | (−1.875) | |

| Leverage | 0.282 | 0.373 | −0.026 | −0.126 |

| (1.343) | (1.423) | (−0.117) | (−0.431) | |

| Chg_Lev | 0.489 * | 0.693 ** | 0.446 ** | 0.925 *** |

| (2.023) | (2.261) | (2.102) | (3.106) | |

| Indboard | −0.417 | 0.225 | 2.602 *** | 2.999 *** |

| (−0.420) | (0.210) | (3.083) | (3.639) | |

| Bull | −0.884 *** | −0.665 *** | ||

| (−7.361) | (−3.555) | |||

| Year-Fixed | Yes | Yes | Yes | Yes |

| Area-Fixed | Yes | Yes | Yes | Yes |

| N | 50 | 50 | 43 | 43 |

| R2 | 0.705 | 0.655 | 0.774 | 0.801 |

| Adj R2 | 0.421 | 0.323 | 0.548 | 0.601 |

| F | 16.36 | 5.867 | 9.016 | 15.95 |

| ROE | Discount | |||

|---|---|---|---|---|

| (1) | (2) | (3) | (4) | |

| Variables | High | Low | High | Low |

| Constant | −1.402 | 1.223 * | 0.383 | −0.728 |

| (−1.682) | (2.014) | (0.391) | (−1.189) | |

| Policy | −0.022 | −0.116 | −0.121 | −0.004 |

| (−0.321) | (−1.635) | (−1.335) | (−0.103) | |

| Discount_p | 0.142 ** | 0.157 *** | ||

| (2.098) | (3.178) | |||

| Proceed | −0.009 | 0.000 | 0.000 | 0.026 ** |

| (−0.781) | (0.081) | (0.062) | (2.632) | |

| ROE | −0.488 | 0.232 | ||

| (−0.873) | (1.444) | |||

| Size | 0.052 | −0.016 | −0.013 | 0.007 |

| (1.383) | (−0.529) | (−0.345) | (0.350) | |

| Tobinq | 0.108 ** | 0.010 | 0.087 | 0.122 ** |

| (2.135) | (0.117) | (0.939) | (2.492) | |

| Top1 | −0.000 | −0.003 * | −0.002 | −0.001 |

| (−0.260) | (−1.731) | (−0.766) | (−1.482) | |

| Leverage | 0.750 ** | 0.054 | 0.571 | 0.405 ** |

| (2.754) | (0.193) | (1.336) | (2.725) | |

| Chg_Lev | 0.641 * | 0.239 | 0.704 * | 0.292 * |

| (1.810) | (1.044) | (1.939) | (2.034) | |

| Bull | −0.181 | −0.188 * | −0.268 * | −0.049 |

| (−1.592) | (−1.885) | (−1.936) | (−0.917) | |

| Board | −0.214 | −0.084 | −0.077 | −0.018 |

| (−1.163) | (−0.360) | (−0.279) | (−0.177) | |

| Indboard | 2.049 * | −1.545 * | 0.577 | 0.885 |

| (1.935) | (−1.900) | (0.505) | (1.132) | |

| Mfee | −0.911 | 0.428 *** | 0.321 ** | 0.340 |

| (−1.431) | (3.257) | (2.200) | (1.688) | |

| Area-Fixed | Yes | Yes | Yes | Yes |

| N | 45 | 50 | 48 | 47 |

| R2 | 0.543 | 0.686 | 0.492 | 0.521 |

| Adj R2 | 0.163 | 0.450 | 0.0826 | 0.119 |

| F | 2.373 | 10.27 | 4.933 | 2.799 |

| Empirical p-Value | 0.128 | 0.094 | ||

| (a) | |||||||

|---|---|---|---|---|---|---|---|

| Discount | Relaxation | Stringent | DIF | T-Test | Wilcoxon Test | ||

| N | 61 | 65 | T | p-Value | Z | p-Value | |

| Discount_b | 0.1676 *** | −0.0583 | 0.2260 | 3.4464 | 0.0008 | 3.5319 | 0.0004 |

| Discount_p | 0.2532 *** | −0.0330 | 0.2862 | 4.1848 | 0.0001 | 4.2885 | 0.0000 |

| (b) | |||||||

| Discount_b | 0.1544 *** | −0.0063 | 0.1607 | 3.2985 | 0.0013 | 3.5325 | 0.0004 |

| Discount_p | 0.2487 *** | 0.0299 | 0.2188 | 4.3421 | 0.0000 | 4.2648 | 0.0000 |

| (1) | (2) | (5) | (6) | ||

|---|---|---|---|---|---|

| Variables | Discount_p | Discount_b | Variables | Discount_p | Discount_b |

| Constant | −0.384 | −0.475 | Constant | −0.498 | −0.534 |

| (−0.628) | (−0.973) | (−0.820) | (−1.153) | ||

| Policy | −0.339 *** | −0.182 *** | Policy | −0.363 *** | −0.182 *** |

| (−3.685) | (−2.841) | (−4.321) | (−2.921) | ||

| Ctrl_Share | −0.132 *** | −0.109 ** | Ctrl_Share | −0.135 *** | −0.116 ** |

| (−3.289) | (−2.327) | (−3.687) | (−2.571) | ||

| Auction | −0.148 ** | −0.128 ** | Auction | −0.112 ** | −0.102 * |

| (−2.496) | (−2.347) | (−2.051) | (−1.781) | ||

| Proceed | −0.000 | −0.004 ** | Ln_Share | 0.099 *** | 0.054 * |

| (−0.002) | (−2.057) | (3.001) | (1.840) | ||

| Fraction | 0.361 ** | 0.203 | Rsize | −0.023 | −0.026 * |

| (2.456) | (1.631) | (−1.444) | (−1.930) | ||

| Size | 0.016 | 0.022 | Ln_Mv | −0.026 | −0.003 |

| (0.642) | (1.001) | (−0.881) | (−0.091) | ||

| Top1 | 0.002 | 0.002 | Top3 | 0.002 | 0.002 |

| (1.008) | (1.196) | (1.272) | (1.393) | ||

| Tobinq | 0.106 ** | 0.026 | Tobinq1 | 0.169 *** | 0.066 |

| (2.138) | (0.506) | (4.055) | (1.341) | ||

| Leverage | 0.102 | −0.153 | Leverage | 0.171 | −0.119 |

| (0.485) | (−0.901) | (1.011) | (−0.709) | ||

| ROE | 0.228 | 0.261 | ROA | −0.511 | −0.012 |

| (0.822) | (1.167) | (−0.936) | (−0.024) | ||

| Bull | 0.068 | 0.234 *** | Bull | 0.064 | 0.233 *** |

| (0.716) | (3.835) | (0.698) | (3.727) | ||

| Balance | 0.014 | 0.013 | Balance | 0.016 | 0.014 |

| (1.002) | (0.997) | (1.309) | (1.196) | ||

| Year-Fixed | Yes | Yes | Year-Fixed | Yes | Yes |

| Area-Fixed | Yes | Yes | Area-Fixed | Yes | Yes |

| N | 119 | 119 | N | 119 | 119 |

| R2 | 0.674 | 0.652 | R2 | 0.699 | 0.658 |

| Adj R2 | 0.500 | 0.467 | Adj R2 | 0.538 | 0.476 |

| F | 15.26 | 13.73 | F | 14.42 | 13.15 |

| (1) | (2) | (3) | (4) | |

|---|---|---|---|---|

| Policy Stringent | Policy Relaxation | |||

| Variables | Discount_p | Discount_b | Discount_p | Discount_b |

| Constant | −2.737 ** | −1.638 * | −1.457 ** | −1.381 ** |

| (−2.706) | (−1.997) | (−2.420) | (−2.359) | |

| Ctrl_Shareholder | −0.247 *** | −0.216 *** | −0.137 ** | −0.049 |

| (−2.984) | (−3.318) | (−2.551) | (−0.784) | |

| Auction | −0.200 | −0.116 | −0.157 ** | −0.074 |

| (−1.329) | (−1.343) | (−2.448) | (−1.064) | |

| Proceed | −0.077 *** | −0.052 *** | 0.006 *** | 0.000 |

| (−3.371) | (−2.892) | (3.085) | (0.158) | |

| Fraction | 1.202 *** | 1.030 *** | 0.057 | −0.087 |

| (4.209) | (4.573) | (0.570) | (−0.503) | |

| Size | 0.141 *** | 0.077 * | 0.035 | 0.041 |

| (3.022) | (1.995) | (1.358) | (1.472) | |

| Top1 | −0.003 | −0.001 | 0.004 | 0.005 ** |

| (−0.929) | (−0.473) | (1.666) | (2.627) | |

| Tobinq | 0.066 | 0.107 | 0.188 *** | 0.093 |

| (0.699) | (1.573) | (3.988) | (1.672) | |

| Leverage | −0.328 | −0.355 * | 0.521 * | 0.091 |

| (−1.502) | (−1.926) | (1.803) | (0.297) | |

| ROE | 0.735 * | 0.744 ** | −0.074 | −0.152 |

| (1.909) | (2.365) | (−0.259) | (−0.621) | |

| Bull | 0.081 | 0.199 * | ||

| (0.562) | (2.043) | |||

| Balance | −0.036 | −0.021 | 0.048 ** | 0.059 ** |

| (−1.628) | (−1.138) | (2.446) | (2.566) | |

| Year-Fixed | Yes | Yes | Yes | Yes |

| Area-Fixed | Yes | Yes | Yes | Yes |

| N | 54 | 54 | 50 | 50 |

| R2 | 0.771 | 0.802 | 0.777 | 0.749 |

| Adj R2 | 0.551 | 0.611 | 0.580 | 0.526 |

| F | 4.132 | 8.822 | 6.681 | 2.859 |

| Controlling Shareholders | Pricing Mode | |||

|---|---|---|---|---|

| (1) | (2) | (3) | (4) | |

| Variables | Participation | Non-Participation | Auction | Fixed |

| Constant | −0.322 | −0.797 | −1.921 * | 1.749 * |

| (−0.342) | (−0.809) | (−1.909) | (2.024) | |

| Policy | −0.268 *** | −0.181 *** | −0.265 *** | −0.311 *** |

| (−3.392) | (−2.805) | (−4.058) | (−3.276) | |

| Ctrl_Shareholder | −0.162 ** | −0.077 | ||

| (−2.601) | (−0.847) | |||

| Auction | −0.200 *** | −0.175 | ||

| (−2.813) | (−1.491) | |||

| Proceed | −0.002 | −0.009 | −0.019 | −0.000 |

| (−0.681) | (−0.309) | (−0.891) | (−0.128) | |

| Fraction | 0.281 | 0.277 | 0.858 *** | −0.060 |

| (1.278) | (0.914) | (2.804) | (−0.516) | |

| Size | 0.029 | 0.003 | 0.057 | −0.026 |

| (0.798) | (0.072) | (1.381) | (−0.929) | |

| Top1 | −0.002 | 0.003 | −0.000 | −0.006 |

| (−0.600) | (1.496) | (−0.067) | (−1.203) | |

| Tobinq | 0.118 | 0.213 *** | 0.267 *** | 0.052 |

| (1.131) | (3.270) | (2.938) | (0.616) | |

| Leverage | 0.120 | 0.725 ** | 0.546 * | −0.204 |

| (0.375) | (2.534) | (1.921) | (−0.645) | |

| ROE | −0.215 | −0.097 | 0.671 | −0.255 |

| (−0.698) | (−0.242) | (1.607) | (−1.037) | |

| Bull | −0.135 | −0.054 | −0.087 | −0.243 |

| (−1.011) | (−0.543) | (−0.817) | (−1.404) | |

| Balance | −0.034 | 0.060 *** | 0.017 | −0.057 |

| (−1.175) | (3.010) | (0.802) | (−1.361) | |

| Area-Fixed | Yes | Yes | Yes | Yes |

| N | 64 | 48 | 71 | 38 |

| R2 | 0.460 | 0.769 | 0.590 | 0.614 |

| Adj R2 | 0.208 | 0.566 | 0.389 | 0.287 |

| F | 4.361 | 13.93 | 5.632 | 4.679 |

| Empirical p-Value | 0.208 | 0.366 | ||

| Event Windows | N | Mean | T-Value | p-Value |

|---|---|---|---|---|

| [50, 250] | 96 | 0.0691 | 1.3588 | 0.1774 |

| [50, 500] | 95 | 0.1542 ** | 2.0490 | 0.0432 |

| [50, 700] | 94 | 0.0314 | 0.3595 | 0.7200 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Ning, Y.; Jalil, R.B.A. Industrial Policy Environment and Private Equity Placement: Evidence from Chinese Real Estate Firms. Economies 2024, 12, 279. https://doi.org/10.3390/economies12100279

Ning Y, Jalil RBA. Industrial Policy Environment and Private Equity Placement: Evidence from Chinese Real Estate Firms. Economies. 2024; 12(10):279. https://doi.org/10.3390/economies12100279

Chicago/Turabian StyleNing, Yuping, and Rohaya Binti Abdul Jalil. 2024. "Industrial Policy Environment and Private Equity Placement: Evidence from Chinese Real Estate Firms" Economies 12, no. 10: 279. https://doi.org/10.3390/economies12100279

APA StyleNing, Y., & Jalil, R. B. A. (2024). Industrial Policy Environment and Private Equity Placement: Evidence from Chinese Real Estate Firms. Economies, 12(10), 279. https://doi.org/10.3390/economies12100279