1. Introduction

The basic pillar of Industry 4.0 is resource optimization, including materials, energy, technical, technological, personnel, and financial, which, in production enterprises, represent economic value as the core costs to the business.

Ozbalta et al. (

2021) commented that the energy efficiency concept, including notions of environmental safety, is today the major theme for all buildings in production enterprises. This problem also affects administrative, as well as production, buildings. All production enterprises use administrative buildings for administrative activities. This research fills in the gap in the research regarding energy and economic efficiency in administrative buildings. This gap exists because this area is considered less important for production enterprises. Administrative buildings make a significant contribution to a business’s total energy consumption, so it is crucial to improve their energy performance at both the environmental and economic levels. The economic view means that energy costs are an important part of operational costs, and their reduction is based on lower energy consumption and using renewable resources.

Ekung et al. (

2020) said that the costs of clean-energy technologies are very high and their implementation in administrative buildings is voluntary. The best strategies for photovoltaic cost reduction are mandating green buildings, ensuring building design standardization, the use of photovoltaic components, facilitating import licensing, and massive public education. Developing these strategies to improve the photovoltaic value chain will increase the supply capacity of clean energy, which is one of the solutions for improving administrative buildings.

Shukla et al. (

2022) said that there is significant interest in using transparent organic photovoltaics to generate on-site electricity and reduce building energy demand. The net energy benefit is positive for all buildings in various locations. This means that more energy is produced or saved than used. The payback times are less than other buildings using integrated photovoltaic technologies. This study aims to investigate the effects of technical and technological modifications of administrative buildings on the financial side of the enterprise. The main focus is on reducing energy costs and energy consumption. The study is orientated toward solving the various technical innovations in the administrative buildings that will help bring about improvements in energy consumption. Through appropriately chosen innovations, energy costs and energy consumption should be reduced.

This approach brings scientific and practical benefits (suggestion of possibilities for energy saving for administrative buildings), social benefits (motivation of employees to engage with low-cost measures), and economic benefits (reducing energy costs). Optimization of resources is a central component of Industry 4.0. This aspect is aimed at energy, environmental, and economic (EEE) sustainability, and using various models of resource improvement is a priority. The priority document in the EU for energy sustainability is the transformative power of the 2030 Agenda. The 2030 Agenda was determined by the 17 Sustainable Development Goals. The integration element is manifested in the agenda as a connection of all three dimensions of sustainable development: economic, social, and environmental. This research is oriented towards energy cost reduction in the administrative building of a manufacturing enterprise in Slovakia through the implementation of energy management with technical innovations. This paper investigates the following hypothesis: implementing innovations brings positive results in reducing the energy costs of administrative buildings and their total energy consumption. The effort to solve the problem of energy consumption was started in the European Union Energy Performance of Buildings Directive and in the state statement for energy performance.

Gatt et al. (

2020) commented that the complex renovation of buildings to ensure nearly zero energy consumption and addressing “smart-readiness” is a possibility for solving the energy consumption problem. The benefits are reduced energy costs of administrative buildings and reduced energy consumption. The best managerial instrument is energy management implementation. Energy management implementation enables the management of energy consumption and contributes to energy, environmental, and economic sustainability.

2. Literature Review

Vranayová et al. (

2020) commented that buildings in the EU account for 40% of total energy consumption and 36% of total CO

2 emissions. The cornerstone of EU policy in the field of energy efficiency is the reduction in energy consumption, strengthening the energy efficiency of buildings, the rapid pace of building renovation, the minimization of energy costs, the construction of buildings at the A1 level (ultra-low-energy buildings), and the design of buildings with zero energy needs at the A0 level. In industrial enterprises, the main goal of the system energy-saving instrument is to improve energy use and reduce energy costs by implementing various technical innovations.

Lukáč et al. (

2021) commented that energy efficiency and costs are important economic, environmental, and energy sustainability parameters. Strategic modifications (technical, technological, social, personal, and other) of all business processes create the base for performance evaluation in enterprises (for example, EVA indicator) and build the frame of sustainable development.

Hu et al. (

2023) created a multi-objective mathematical optimization model for energy systems. This model considered energy cost reduction, and efficiency maximization rather than objective functions. This mathematical model solved the economic side of energy efficiency.

Al Muala et al. (

2023) presented how to reduce energy costs by using renewable energy sources and storage systems in buildings. The results of their research were the energy management system implementation as a managerial instrument. The results showed that the proposed system reduced the real cost, and energy losses in buildings.

Sayed et al. (

2023) commented that the renewable and ecologically friendly alternatives for energy consumption are renewable energy sources. Significant progress has been made to produce renewable energy sources with acceptable prices at a commercial range such as solar, wind, and biomass energy. This success has been due to technological growth that can use renewable energy sources effectively at lower prices. Renewable energy sources generated new barriers such as visualization effects, noise, stink, and others.

Beer et al. (

2023) investigated the inverse visual influence associated with infrastructure of the renewable energy. The energy infrastructure may prevent their wider deployment in the energy mix.

Knight et al. (

2022) showed relationships between costs and energy savings in the mathematical model. The base of energy efficiency is cost-effectiveness. Based on an analysis of costs energy savings are followed such as energy efficiency indicators. This approach is the possibility for electric utilities and state regulators in the energy efficiency area.

Paramati et al. (

2022) dealt with the role of environmental technologies. In this area of energy demand, energy capability and performance are important factors. The results of their research, across various estimates, confirm that those technologies have a significant effect on energy consumption. Environmental technologies play a major position in improving energy efficiency through energy intensity reduction and energy cost.

Arumägi and Kalamees (

2020) demonstrated the options for energy reduction and construction costs. They provided evidence that wooden nearly zero-energy buildings are technically possible. The novel design processes and procurement models reduce construction costs and energy costs. Financial calculations were based on the investment needed to achieve nearly zero energy levels.

Wu and Skye (

2021) commented on advances in net-zero-energy residential buildings (NZEB—net-zero-energy buildings) that could reduce energy consumption, energy costs, and greenhouse gas emissions. NZEB proposals are connected by energy infrastructure interconnections, renewable energy sources, and energy efficiency measures.

Terés-Zubiaga et al. (

2020) showed that building renovation plays a main position in reducing greenhouse gas emissions. This approach achieves climate protection goals and energy cost reduction. Cost-effective building renovation combines energy efficiency and renewable sources. The solution is using cost-effective interventions that can lead to significant reductions in greenhouse gas emissions and non-renewable primary energy use.

Zhao and Mo (

2023) presented in the article that buildings are responsible for significant energy consumption and carbon emissions. Green buildings offer a solution to reduce energy consumption. The energy costs should be calculated during the complex building projects and energy policy for sustainable development. Retrofitting offers great potential to promote the green building movement. This resource suggests effective subsidy programs as a public policy implication.

Asim et al. (

2022) dealt with the increasing demand for heating, ventilation, and air-conditioning (HVAC) systems. Their importance, as the respiratory system of buildings, in developing and spreading various microbial contaminations and diseases with their huge global energy consumption was the main goal of research. The results of the research present that the industries have to focus on improving the sustainability of HVAC systems. The greatest opportunities for improving the sustainability of HVAC systems exist at the design stage of new facilities and the retrofitting of existing equipment.

Mirnaghi and Haghighat (

2020) comment that the abnormal operation of HVAC systems can result in an increase in energy usage as well as poor indoor air quality, thermal discomfort, and low productivity. Building automated systems (BAS) collects a massive amount of data related to the operation of each component of HVAC systems. These data support for improvement of HVAC systems.

Chen et al. (

2023) presented the importance of data-driven fault detection. The diagnostics for building heating, ventilation, and air-conditioning systems (HVAC) is the base for detection. This process is divided into the following steps: data collection, data cleansing, data preprocessing, baseline establishment, fault detection, fault diagnostics, and potential fault prognostics. This instrument is important for building an effective HVAC system.

Afroz et al. (

2018) said that the appropriate application of advanced control strategies in heating, ventilation, and air-conditioning (HVAC) systems is the key to improving the energy efficiency of buildings.

Umoh et al. (

2024) commented on green architecture and energy efficiency. Green architecture has become an imperative consideration in contemporary construction practices. Their research provides a review of innovative design and construction techniques employed in green architecture to enhance energy efficiency.

Guyomard et al. (

2023) presented that green architecture relies on three instruments: eco-schemes, agro-environment measures, and climate measures.

Elshafei et al. (

2021) commented that green structures turned into a huge path to an economic future. Green building outlines include finding the harmony between living and a maintainable environment. In their research, the usage of modern technologies is seen as part of greener construction changes and utilizing the genetic algorithms innovations.

Economidou et al. (

2020) presented a key pillar of the European Union’s climate and energy strategy. This document informs the reduction in energy demand in buildings by using energy efficiency. Energy efficiency in the EU energy policy agenda was progressively transformed according to the real situation.

da Cunha and de Aguiar (

2020) presented that the energy efficiency of buildings is one of the biggest preoccupations due to the high negative impacts on the environment, economy, and society.

Hummel et al. (

2023) said the main key to reaching climate protection targets is reducing CO

2 emissions for space heating and hot water preparation in buildings. In this case, it is important to understand the balance between CO

2 reduction through thermal renovation activities and the change of heating systems. The results show a high share of thermal renovation until 2050 is cost-efficient to reach a 95% CO

2 reduction. In total, 90% of the buildings are applicable for thermal renovation. Energy needs are reduced more in older buildings than in newer buildings.

Brockway et al. (

2021) presented a macroeconomic view of energy efficiency. Most global energy predictions anticipate a structural break in the relationship between energy consumption and gross domestic product (GDP). The results of their research showed a relationship between energy consumption and GDP. They conclude that global energy prediction may underestimate the future growth rate of global energy demand.

Chen et al. (

2024) said that energy efficiency accounts for approximately 40% of the possibility of reducing greenhouse gases. The critical challenge is mitigating climate change while maintaining economic growth. Their research investigated the impact of energy efficiency on economic growth and environmental sustainability (

Figure 1).

The results show that energy intensity was positively associated with CO

2 emissions, ecological footprint, and economic growth. Energy depletion was negatively associated with economic growth and positively related to CO

2 emissions and ecological footprint. These findings demonstrate that energy intensity positively impacts economic growth and degrades the environment.

Sun et al. (

2021) commented that technical and technological modifications and options reduce energy intensity and carbon emissions without compromising global economic growth.

Zhao et al. (

2022) presented an energy efficiency study investigating the effect of green-bond financing on energy efficiency investment for green economic recovery. The study’s findings showed that green bonds are the primary financing source for energy efficiency projects.

3. Methodology

This research dealt with energy cost reduction and energy consumption after technical innovations and modifications. The purpose of the research was realized in a production enterprise in Slovakia that uses an administrative building for administrative activities for 100% rooms. This administrative building creates high energy and operational costs. This reason is the instrument for changes in the administrative building. The administrative building is very old—its lifetime is 30 years. During its lifetime, small modifications and operational costs were acceptable. The administrative building is used for administrative activities such as an office space. The building has 4 floors—the ground floor and 3 floors. The area of the building is 1266 m2. Since the year 2019, the operational costs of administrative buildings have increased. This fact is a big problem in the enterprise in the financial area, energy consumption and energy costs and the safety of buildings.

As part of the research, we established the basic hypothesis for energy cost reduction: implementing innovations brings positive results in reducing energy costs of administrative buildings and energy consumption. We tested this hypothesis.

The basis for testing was economic, financial, and comparative analysis after implementing technical modifications and other without and low measures in the administrative building in selected enterprises in Slovakia. The year 2022 was a critical moment for innovations in the administrative building. The state of the administrative building was critical and energy, operational costs were too high. The administrative building did not do modifications in the year 2019–2022. The maintenance process was provided according to the real situation and crisis. All the rooms of the administrative building were used. In the administrative building, new climatic conditions (higher temperature) were accepted because the enterprise did not have the financial resources for innovations and modifications. In the year 2022, financial sources were prepared in the amount of EUR 65,000 for investment in the administrative building from reason of the critical situation. The reason was known—high energy costs and the critical state of the administrative building. This situation needed to be solved in the administrative building of the enterprise.

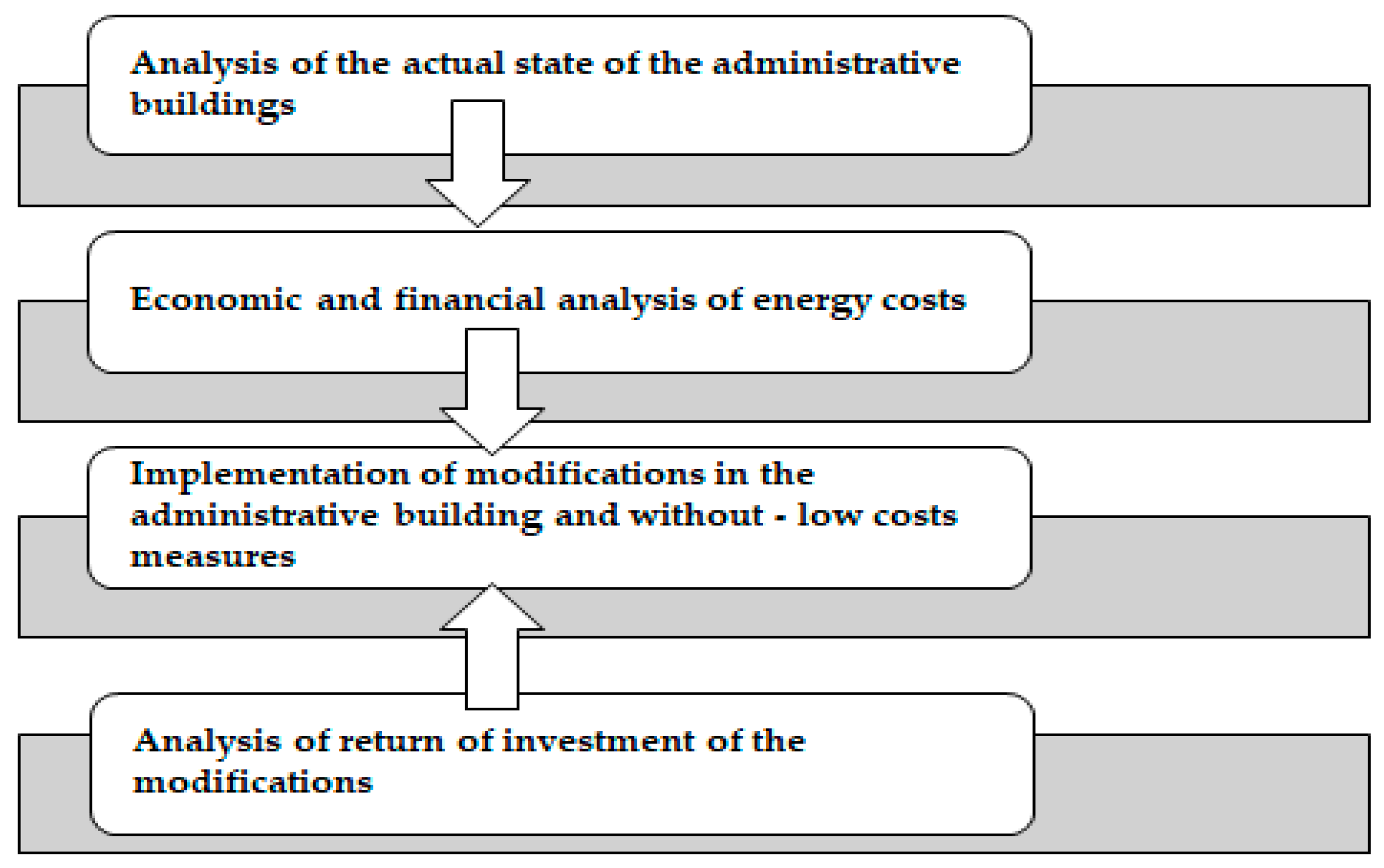

The research was conducted based on the algorithm (

Figure 2).

In the first step of the research, we collected data (

Table 1) for economic and financial analysis in the selected enterprise. We obtained data from the SAP system, and POHODA accounting software (version STORMWARE 1.8 POHODA), at the individual departments of the production enterprise in Slovakia. The rate for energy according to the law was EUR 0.16/kWh and during the time period 2019–2023 was uniform. We selected data from 2019 to 2023 because, since the year 2019, the energy consumption increased from 890 GJ to 1050 GJ. We obtained data—complex costs for administrative buildings and their operability.

Economic and financial analysis:

Economic analysis has used the count of energy costs (multiply energy rate and energy consumption), the development trend of the values (costs) (share of cost in the current period and in the based period), and the structure of costs (index of one kind of costs and SUM of costs) (Formulas (1)–(3)). The financial analysis contains the indicator—the payback period of investment (number of years for the back of investment) in the manufacturing enterprise (Formula (4)).

Formula (1): Energy costs (EUR)

Formula (2): Development trend of costs

Formula (3): Structure (%)

Formula (4): Payback period (years)

where R—energy rate, Co—consumption (Kwh), Ce—energy cost, T—trend, C—costs, (0, 1)—time period, S—structure, Cj—unit cost, Cc—total cost, Pp—payback period, I—investment, and CF—cash flow in years.

The economic analysis was chosen because of the established goal of the research, which was the reduction in energy costs. Energy costs were determined as the product of consumption and the energy rate established by law during the period from 2019 to 2023 (

Table 2). Then, it was necessary to monitor the development of these costs in the period 2019–2023. Based on the structure of costs, it is possible to evaluate the type of costs and their reduction. The financial analysis was used for the implementation of technical modifications to the administrative building, it was necessary to allocate financial resources and determine their return due to the creation of a financial reserve.

4. Results

The research was provided in the selected production enterprises in Slovakia. This enterprise uses administrative buildings for business activities. All rooms are used for 100% of the time in the administrative building. The research followed the algorithm of the research realization in steps in

Figure 2.

4.1. Analysis of the Actual State of Administrative Building

The administrative building (

Figure 3) is located in the manufacturing enterprise. The building is constructed as a prefabricated skeleton. It is built from building material with good insulating properties. The perimeter consists of concrete materials. The roof is flat, not insulated. The building does not have floor thermal insulation. Solar radiation comes from three sides—south, west, and east. The north part is covered by a neighboring building. There are curtains on the windows and blinds on some of the windows. The building is supplied from a central heat supply. The water in the heating elements is heated in exchangers. Regulation is automatic depending on the external environment. The distribution route is long. The building is heated throughout the heating season. The heating system is without thermostatic valves. Pipes do not have thermal insulation. The system is not hydraulically regulated. This building has a life cycle of 30 years.

4.2. Economic Analysis of Energy Costs

In this part of the research, we investigate energy consumption and energy costs and their trend (

Table 2), because the main problem is high energy costs. For economic analysis, energy consumption information from

Table 1 has been used, for the count of energy costs, Formula (1) has been used, and for the trend of costs, Formula (2) has been used. Energy consumption in (GJ) was translated to (kWh).

The results of the indicators are presented in

Table 2.

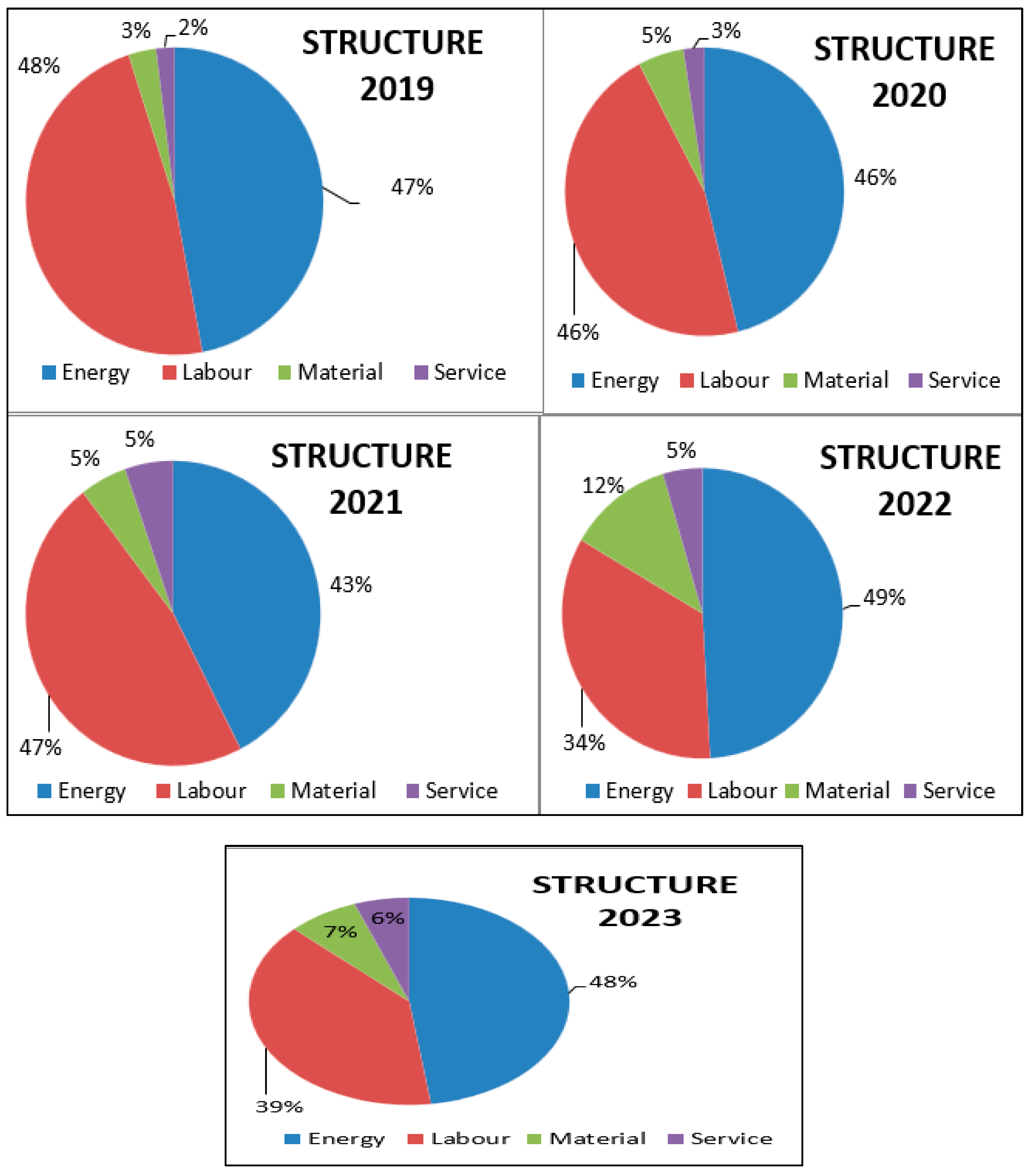

Energy costs have been increasing since 2019 and reached their highest value in 2022, representing an increase of 26% compared to 2021. Energy costs were decreased by 12% in the year 2023. During the period 2019–2023, the conditions in the administrative building did not change. The building was 100% used for business activities. A climatic condition was changed (higher temperature). Despite the climatic changes, the heating condition was the same. We also examined indicators of structure in Formula (3). The results of the indicators are presented in

Figure 4. The structure of the costs for the administrative building is important from the reason for the financial reserve creation. The high structure during 2019–2023 created two types of costs—energy costs and labor costs. Labor costs cannot decrease, because the maintenance department needs specialized staff. A reduction in salaries means staff fluctuation and staff deficit. The energy costs can change because they are connected by energy consumption and kind of energy. It is an available solution for the selected enterprise.

The reason for the decrease in energy costs in the year 2023 was that technical modifications—innovations—were introduced in the administrative building. The implementation of without-cost measures and low-cost measures in the administrative building caused decreasing energy costs and energy consumption. Due to the increase in energy costs, it was necessary to evaluate their share in the total operating costs of the administrative building (

Table 3). Total operating costs contain labor, materials, service, and energy costs for the administrative building. The significance of those operating costs is important for modifications in the administrative building and for budgeting of the modifications. Labor costs create the salary of employees who provide maintenance in the administrative building. Material costs create all costs for the repairing process in the administrative building. Service costs are costs connected with the services of external suppliers. Energy costs create costs for energy consumption and other energy fees (electrometer). The worst trend in operating costs was presented in the year 2022. In this period was the world energy crisis. The opportunities for Slovakia were investment in renewable technologies and green investments.

Based on the available information on operating costs for the administrative building, their share (

Figure 4) was determined for individual cost categories such as labor, material, services, and energy costs. Through this analysis, it was found that the highest share of costs is represented by energy costs and labor costs. Those categories of costs create the share in the level from 34% to 49%. These two types of costs are the reason for the high costs of operating an administrative building. We investigated the main causes of high costs in this administrative building.

The results of the observation were as follows:

Total changes in climate in the environment;

Cold in the corridors due to climate factors;

The corridors are not properly ventilated;

Bad monitoring equipment in the building;

The maintenance system of the administrative building is not managed;

Regular inspections of heating elements are not ensured;

Not acceptable fittings in the heating system;

Bad heating elements;

The services of external suppliers;

Poor technical condition of the building;

High durability of the building;

Insufficient insulation;

Insufficient epithermal regulation;

The unsuitable windows;

The unsuitable doors with bad insulation;

Other factors that are not decisive for modification of the administrative building.

4.3. Implementation of Modifications in the Administrative Building

In this part of the research, we suggest without-cost, low-cost, and high-cost measures for reducing energy costs. In the first step, we dealt with without-cost measures.

Guo et al. (

2023) presented in their research the modifications for reduction energy cost, energy savings, reduced operational costs, and improved sustainability for energy facilities.

Those modifications were used in our research for the administrative building oriented on without-cost measures. We selected the best easy modifications for employees and realization in the administrative building with actual state and lifetime. All the suggestions were included in the standard manual (internal document) for all employees and departments in the administrative building. The control of modifications filling was provided by the maintenance department. Without-cost measures were determined as follows:

Effective room ventilation;

Implementation of temperature attenuation programs in the building;

Setting the minimum heating temperatures;

Not covering heating elements with textiles;

Temperature monitoring on the premises;

Daily monitoring of heat supply;

Checking the tightness of fittings;

Evaluation of energy consumption and comparison from the previous period.

Those without-cost measures introduced for the production enterprise did not increase energy and operational costs, which was the goal of the solution.

Hu et al. (

2023) solved energy techniques for improving energy utilization and reducing energy costs. They commented that energy utilization efficiency and energy cost are equally important indicators. The effective results they achieved by the low-cost measures introduced the energy cost reduction by 24.96% and the energy efficiency increased by 1.67%. We selected some low-cost measures for our production enterprise from the research of

Hu et al. (

2023). The realized low-cost measures for administrative building were as follows:

Window sealing;

Door sealing; door replacement;

Installation of fittings;

Restoration of insulation;

Placement of aluminum foil behind the radiators;

Energy consumption monitoring;

Integration of energy programs;

Training of specialists in the field of energy efficiency.

Those modifications were realized by outsourcing. The costs for realization were determined in the signed contract.

Based on an expert assessment of the state of the administrative building, an external company proposed several modifications, which we classified as high-cost measures for the selected production enterprise. High-cost measures were as follows:

Hydraulic regulation of distributions;

Montage of regulation of distributions;

Installation of automatic valves and fittings;

Replacement of windows and doors;

Insulation of building structures;

Insulation of the façade and building envelope;

Introduction of electronic monitoring devices;

Insulation of distributions;

Improving the condition of technical installations.

We chose from high-cost measures that were approved in the manufacturing enterprise based on the base the financial situation and possibilities to realize the modifications. Those measures were realized such as technical (insulation of the facade, building envelope, insulation of distributions), and technological modifications (installation of automatic valves, montage of regulation of distributions). The innovations were prepared and budgeted on the level of EUR 65,000 of internal resources with a planned payback period of 20 years. In the year 2022, all the suggested modifications were realized (

Table 4). Cost savings were determined based on measurements and statistical evaluations in the internal documentation in the year 2023 after the implementation of technical and technological modifications of the administrative building.

The planned financial sources for modifications were EUR 65,000. The implementation of technical modifications was EUR 62,500. The annual energy cost savings recorded a value of EUR 6356 according to the difference in costs in the year 2022 and in the year 2023 (EUR 53,023 − EUR 46,667 = EUR 6356). The total savings from technical modifications amounted to EUR 6047 (EUR 6356 − EUR 309). The technical modifications and other without-cost measures were statistical values determined on the level of importance by the maintenance department.

This statistical count was introduced in the document of investment for administrative building P/15/2022/U according to its importance of modifications. The insulation of the façade and building envelope create 68%, insulation of distributions create 5%, installation of automatic valves create 17%, montage of regulation of distributions create 5% and without-cost and low-cost measures and others create 5%. These percentages were determined based on statistical methods used in the production enterprise (internal document—law). Cost saving was counted by percentage share of modifications and measures from the total value of savings. Based on modifications and various measures, the maintenance process for administrative buildings improves in the production enterprise. Those changes create the base for a new model of care for administrative buildings in production enterprises.

All possibilities of modifications such as using renewable sources, energy storage, the mathematical optimization of nearly zero-energy buildings, effective room ventilation, temperature attenuation, and others can bring cost reduction and consumption. In this research, we have used some possibilities for modifications.

The design of the administrative building after modifications was satisfying (

Figure 5). It was the benefit for the selected company such as the marketing instrument for customers and suppliers.

4.4. Financial Analysis of Return of Investment of Modifications

In this part of the research, we want to determine the payback period Formula (4) for technical and technological modifications that were implemented in 2022 and that recorded savings in energy costs in 2023. At the same time, the administrative building and its management system recorded technical (new design of the building, new windows, doors, distributions), economic (reducing of energy costs and operational cost of building), and social (new approach of employees, new ergonomic workplace, effective temperature environment), benefits for increasing administrative building lifecycle.

The return on invested financial sources in innovations will be in the range of 6–12 years (

Table 5) for each individual modification which is an acceptable situation for the production enterprise from a financial view. The planned payback period for the innovations in the administrative building was established as 20 years for the selected company. The payback period was 6–12 years. It was an acceptable solution.

5. Discussion

The priority document in the EU for energy sustainability is the transformative power of the 2030 Agenda. The 2030 Agenda was determined by the 17 Sustainable Development Goals. The integration element is manifested in the agenda as a connection of all three dimensions of sustainable development: economic, social, and environmental.

Mariano-Hernández et al. (

2021) commented that building energy use is expected to grow by more than 40% in the next 20 years. Electricity remains the largest energy source consumed by buildings, and that demand is growing. The improvement of building energy efficiency is based on the system of building energy management. Building energy management systems support building managers and proprietors to increase energy efficiency in modern and existing buildings, and decrease energy use. This approach was implemented in our research for the improvement of the administrative building.

Wawak et al. (

2023) presented factors affecting Quality 4.0 in the era of Industry 4.0 and one factor of Quality 4.0 is reducing costs and increasing the efficiency of business processes, activities, and sources. The results confirmed statistically significant factors of Quality 4.0—the competitiveness, interconnection of processes, and increasing process performance. The results of our research showed factors such as performance indicators—reducing energy consumption and reducing energy costs.

Markulik et al. (

2021) in their research uncovered that the minimization of costs is a base frame of process optimization and increasing performance. The principal goal was to focus on performance and energy sustainability. The results of our research were to create an innovation model for administrative buildings by no-cost, low-cost, and high-cost measures for reducing energy costs. By creating the model, we used the knowledge of various authors presenting the energy cost reduction and the use of technical and technological modifications in the administrative building. This model was conceived based on the results of hypothesis H1 and the results of modifications in the selected production enterprise. In this research, we determined the following hypothesis:

H1: Implementing modifications brings positive results in reducing energy costs of administrative buildings and energy consumption.

The hypothesis was confirmed.

Results of the research confirm the hypothesis:

Reducing energy consumption of 143 GJ (

Table 1).

Reducing energy costs of EUR 6356 (

Table 2).

Reducing the structure by 1.3% (

Figure 4).

Cost saving after modification EUR 6047 (

Table 4).

New design of the administrative building (

Figure 5).

The payback period is lower than it was set by the enterprise (

Table 5).

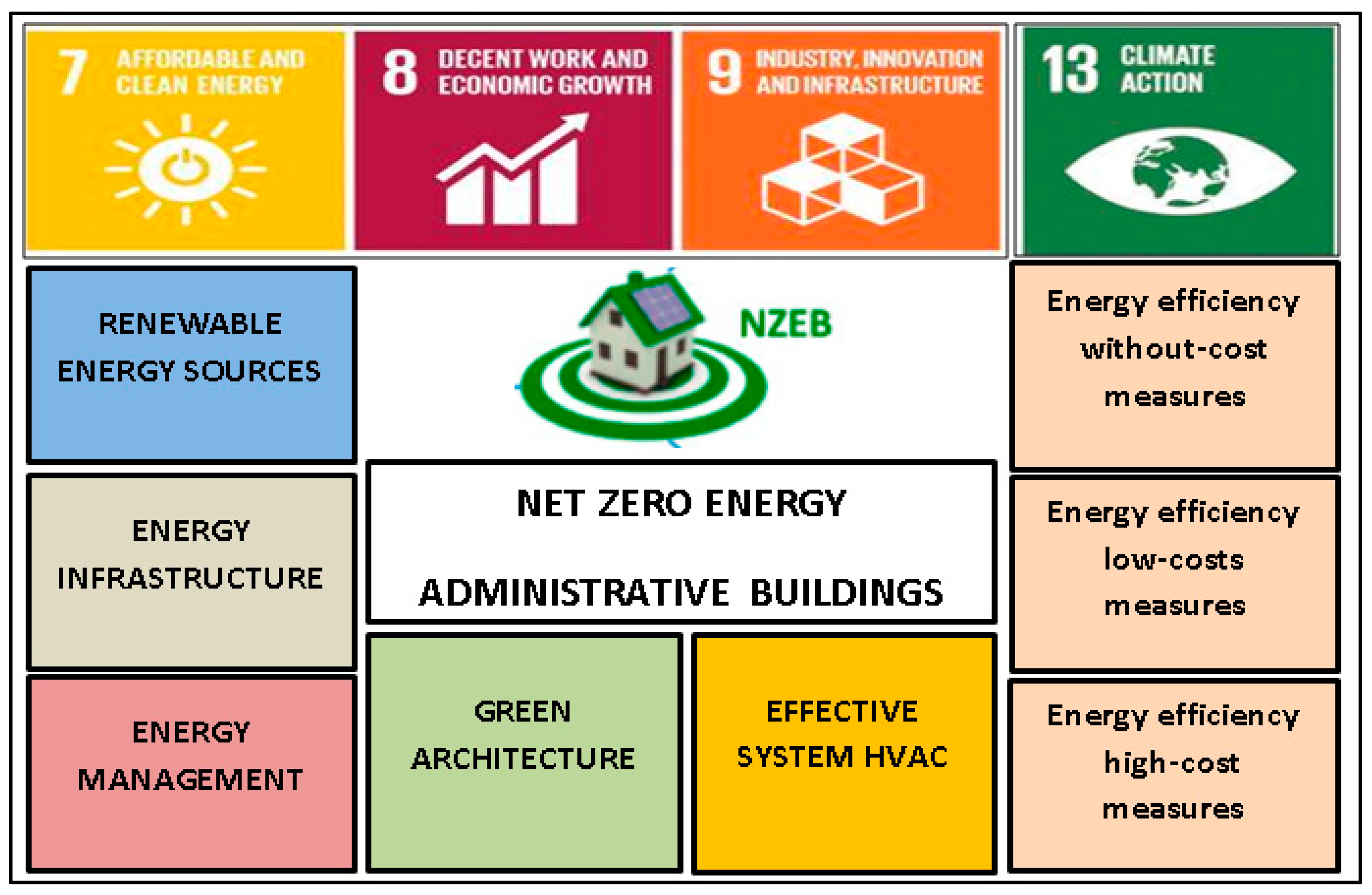

This EEE (energy, economic, environmental) model (

Figure 6) was developed based on a confirmed hypothesis, taking into account all the positive results of the implemented technical and technological modifications and various changes. We tried to design the EEE model in such a way that it accepts all available options for adjustments and measures in administrative buildings in production companies not only the adjustments that were used in the research of the selected production company in Slovakia (for example, NZEB, green architecture, renewable energy sources, energy management and energy infrastructure). All approaches create conditions for the improvement of administrative buildings. The new trends are important in the energy area.

Elia et al. (

2021) commented that the energy technology cost reductions are the result of many innovation trends in the energy system. Those trends are orientated on using multi-factor learning, curve models, and cost models which are needed to improve.

The strategic question is only the financial support of production companies for the realization of technical and technological modifications.

Teplická et al. (

2021) commented that strategic modifications—various technical and technological changes of the administrative buildings increase the performance of processes in the production enterprise. Strategic modifications and innovations are instruments for sustainable development in Industry 4.0 and Quality 4.0. The benefits of strategic technical and technological modifications were presented in the research.

Bouakkaz et al. (

2021) commented on the significance of the power supply and the power balance in the electricity networks for the electricity sector from the reason of the increase in energy demand. Distribution system operators impose an additional cost on electricity consumption during peak hours; on the other hand, they reduce the electricity price during off-peak periods. This approach is one of the possibilities to reduce energy costs for companies and to do some processes during off-peak periods.

Baldini et al. (

2020) presented that the buildings hold a large energy efficiency improvement potential related to energy upgrading of the building envelope. The outcomes show that cost-effective energy efficiency improvements vary considerably, in size and type, among the heterogeneous buildings considered. Regarding district heating tariffs, when all the cost components are variable, the total cost-effective potential increases considerably, with specific energy efficiency improvements distributed differently among building categories, and with the cost components providing different incentives to invest. Evaluating economically attractive investments in energy efficiency improvements for buildings are tariff policies.

Heravi et al. (

2020) commented that nearly zero-energy buildings are viable solutions for reducing the dependency of the building sector on non-renewable energy sources and reducing the destructive environmental impacts of the building sector during their operational period. Nearly zero-energy buildings are climate-specific. That means their development needs to be addressed in various economic, technical, and climatic conditions of different countries. The economic limitations such as high interest rates and low energy prices, improving the performance of the building envelope has played a crucial role in determining the cost-optimal options for a nearly zero-energy building design.

This research was oriented on the administrative building of the production enterprise to achieve energy efficiency.

Potkány et al. (

2012) presented a calculation method with advantages for customers—target costing can calculate operational costs for administrative buildings and be used to save energy. The results of this research bring energy and operational costs reduction, a decrease in energy consumption, and a new design of the administrative building with various modifications. This model was built on the four pillars of TUR—(7) clean energy, (8) economic growth, (9) innovation, and (13) climate action. This model presents an approach to economic dimensions such as reducing energy, reducing energy and operational costs, and fulfilling environmental goals. The model shows the implementation of energy management and energy efficiency. The social dimension is orientated to green architecture and the motivation of the persons for fulfilling the energy measures. The environmental dimension deals with renewable energy sources, energy infrastructure, and effective system HVAC for buildings. The 2030 Agenda for Sustainable Development is a global priority for achieving sustainable development. It expresses the intention of countries to lead their development toward sustainability and to set their national policies, strategies, and planning to contribute to the achievement of global goals.

Economidou et al. (

2020) presented that the reduction in energy demand in buildings through the adoption of energy efficiency policy is a key pillar of the European Union (EU) climate and energy strategy.

Weiner and Szép (

2021) presented Hungary’s energy policy for energy cost reduction for households brought positive and negative effects. The results showed that decreasing energy prices had a positive impact on their energy consumption. This energy policy discourages energy conservation and energy efficiency, erodes the competitiveness of renewables, reduces capital formation in the energy sector, deteriorates the security of supply, and increases energy prices for production companies. This is the reason why energy policy is the key factor in reducing energy costs and consumption. The part of the energy policy is also renewable resources for energy and their use. This area is a priority for energy sustainable development.

Li and Ho (

2022) demonstrated that falling costs of renewable energy create a low-carbon transition in energy areas. The variability of renewable sources decreases the flexibility of energy deliveries. This fact indicates that we should consider the indirect impacts of renewables by their implementation.

Bdour et al. (

2023) commented that renewable energy was recognized as a potential source for energy savings to achieve sustainable and long-term feasible operation and reduction in energy cost in the photovoltaic water plant. The feasibility of the plant showed a fast payback period of up to 1.1 years. Utilizing clean solar photovoltaic energy to power the water plant led to a considerable reduction in greenhouse gases. Those positive benefits show the use of renewable sources for decreasing energy costs.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}