An Empirical Study of the Impact of the Euro on Cross-Country Diversification

Abstract

1. Introduction

2. Literature Review

3. Methodology and Data

4. Empirical Results

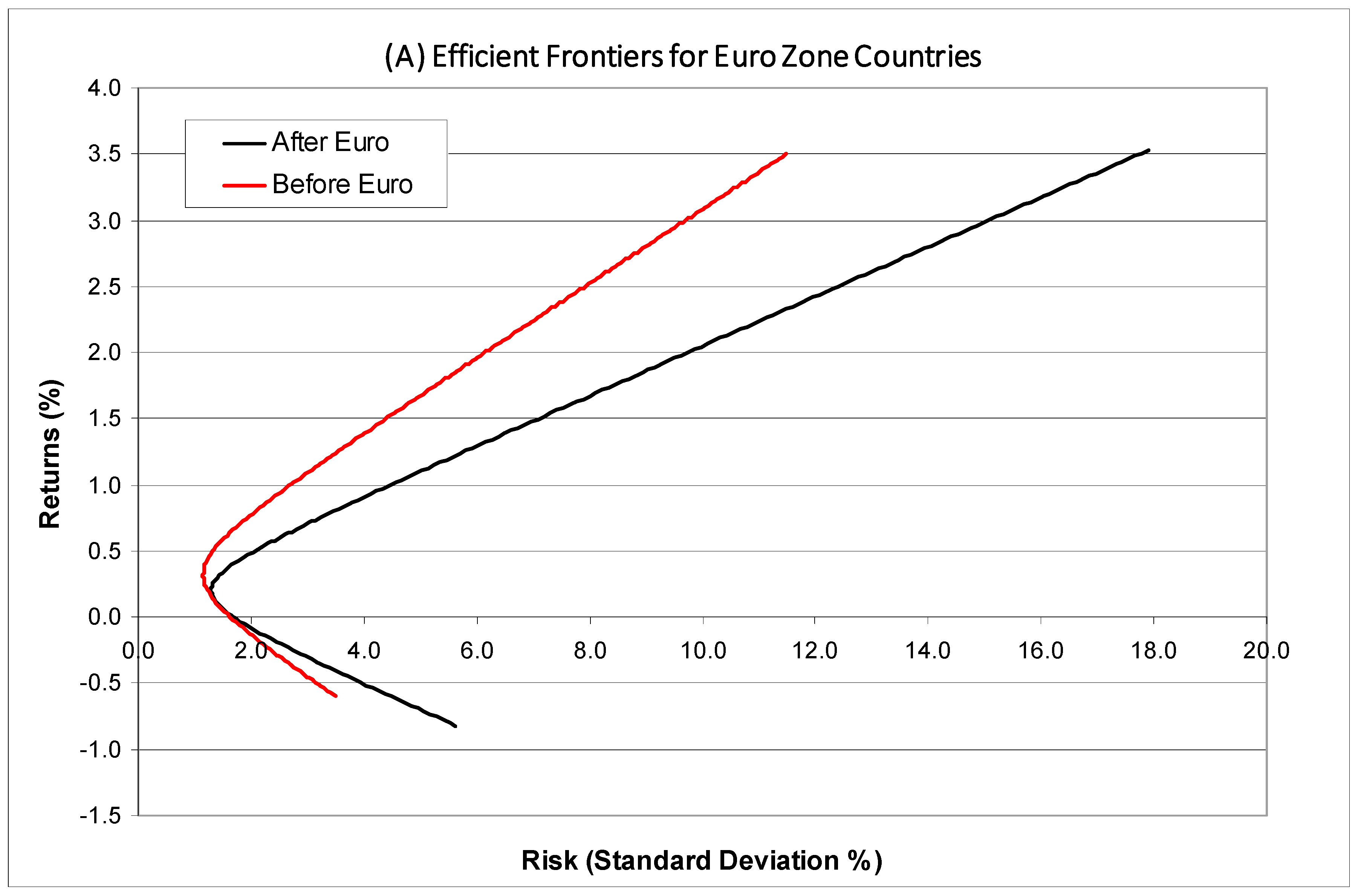

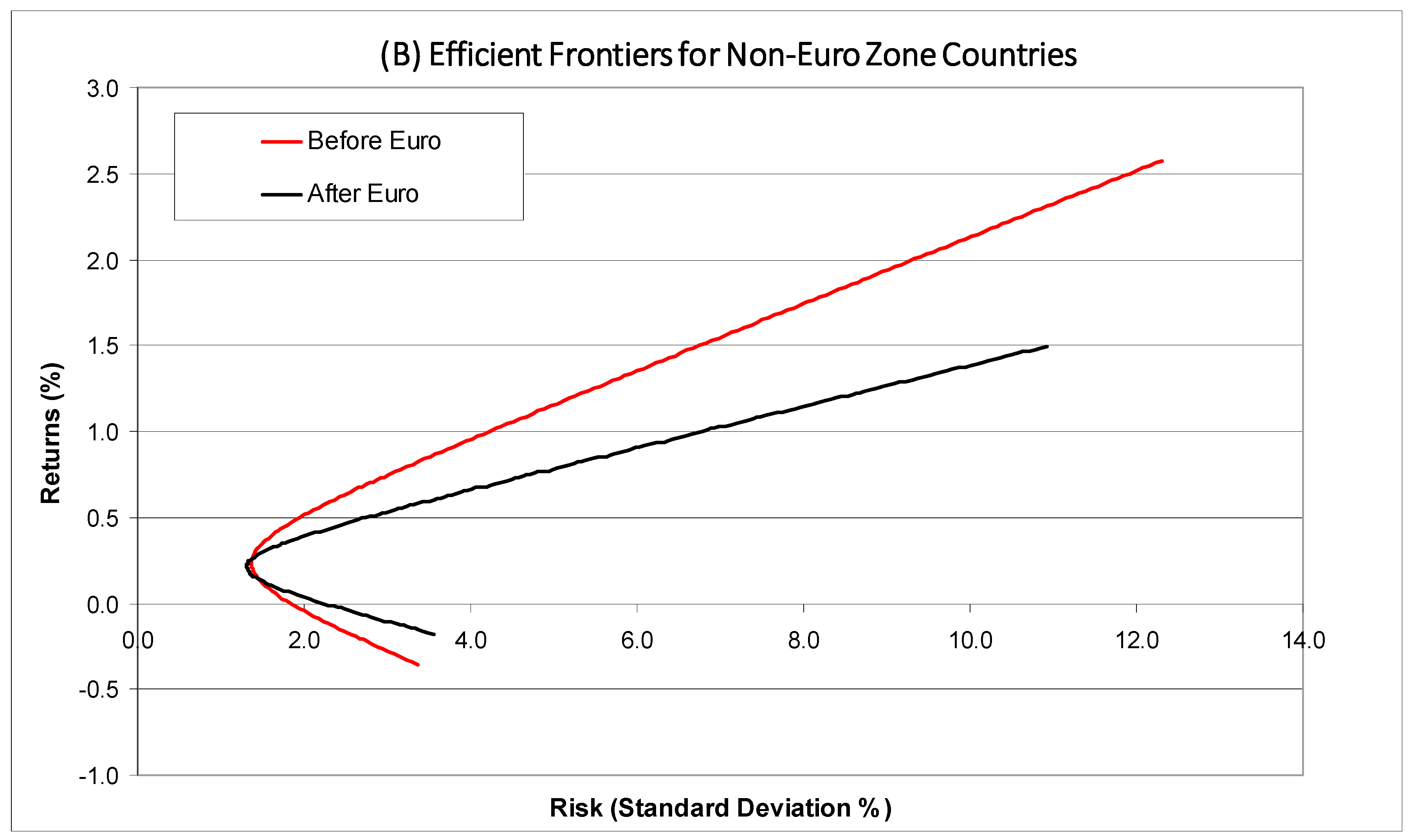

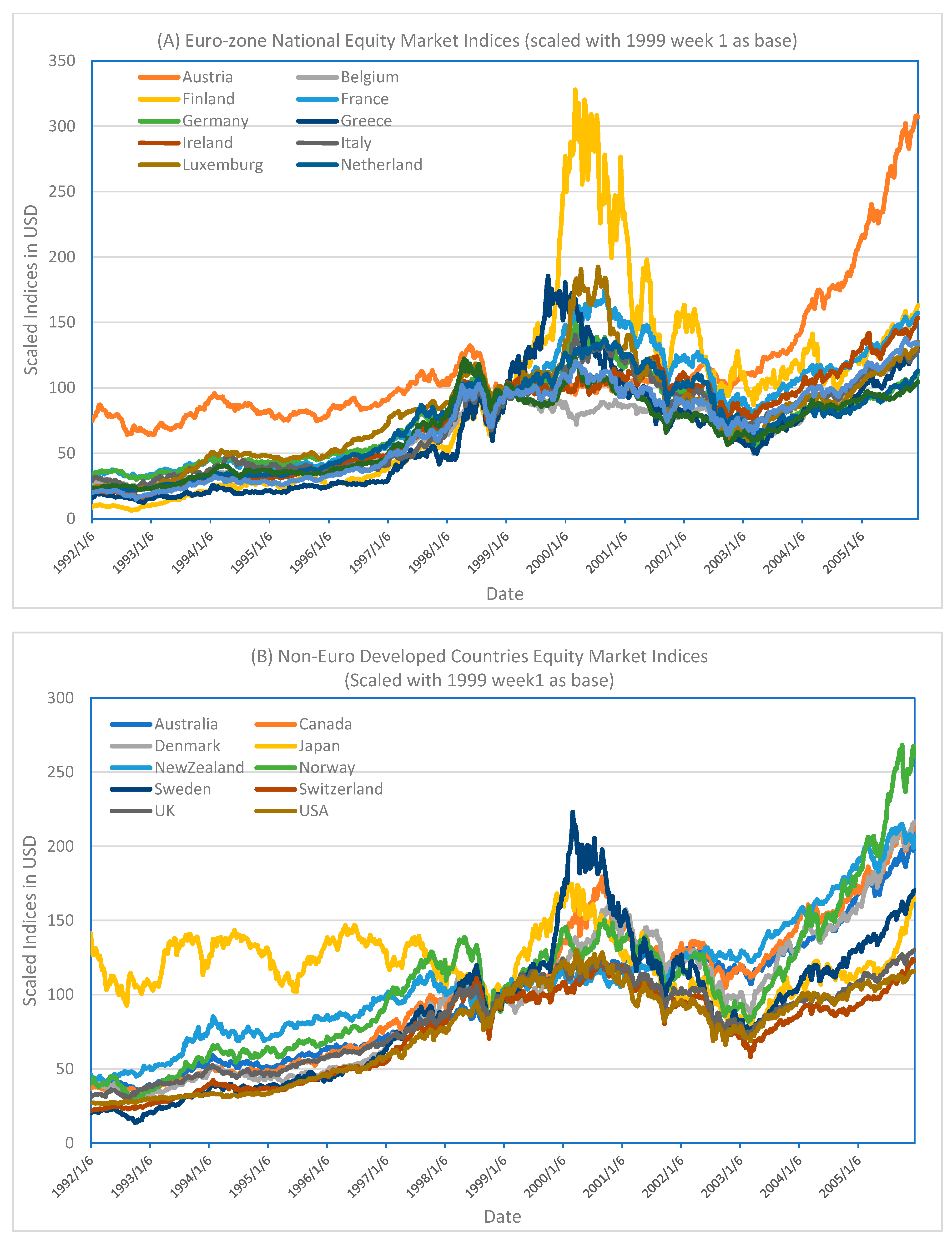

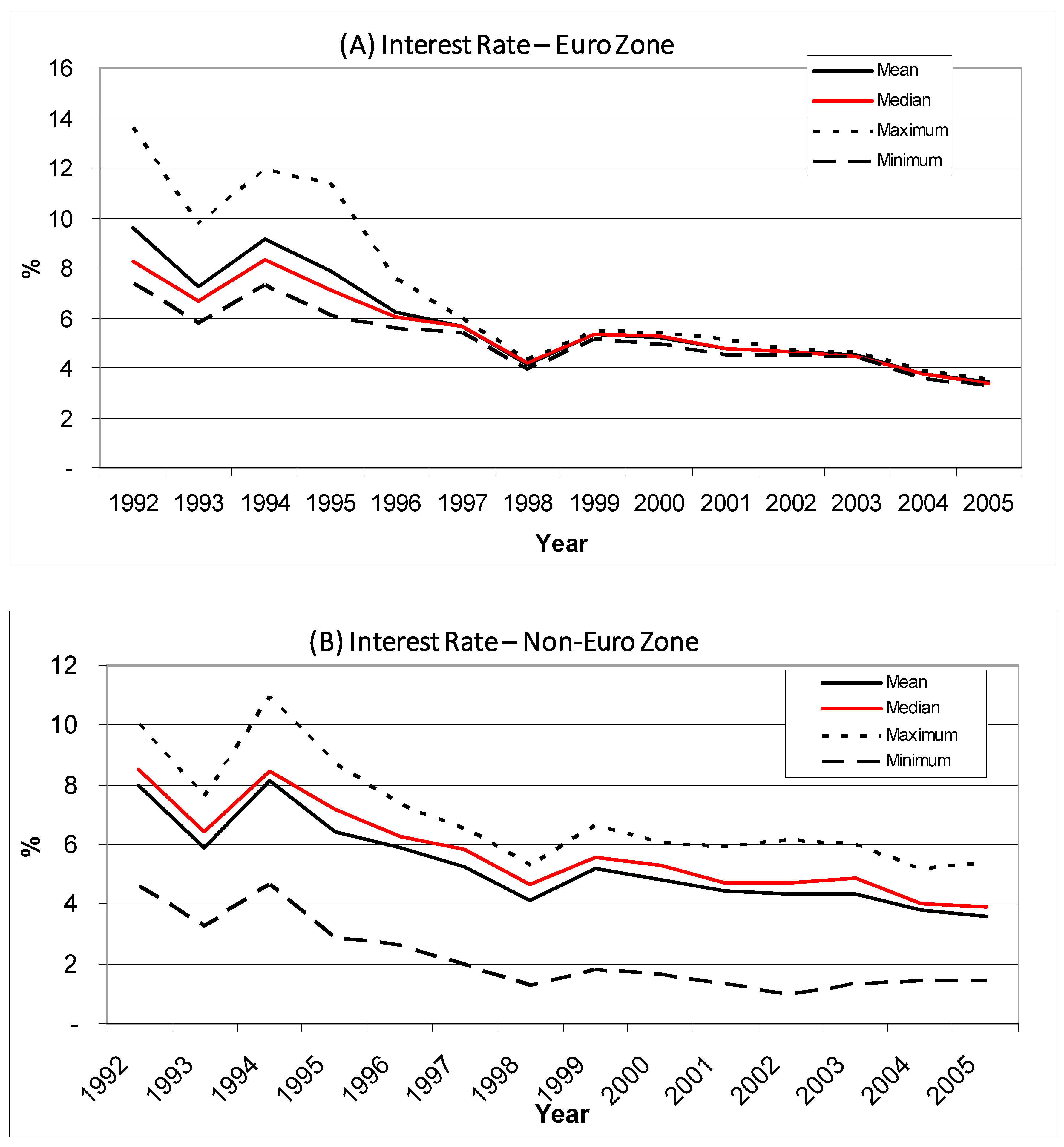

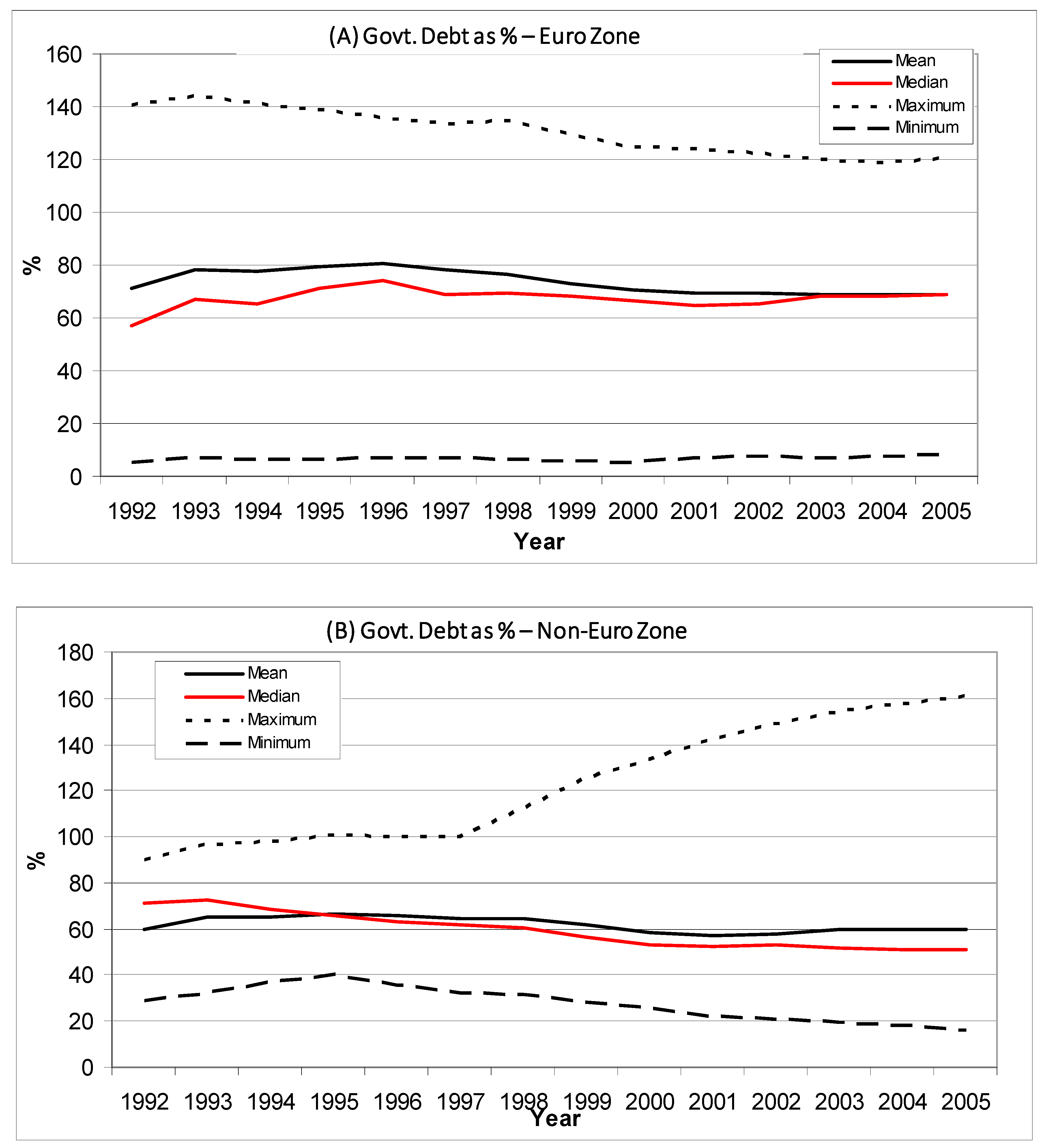

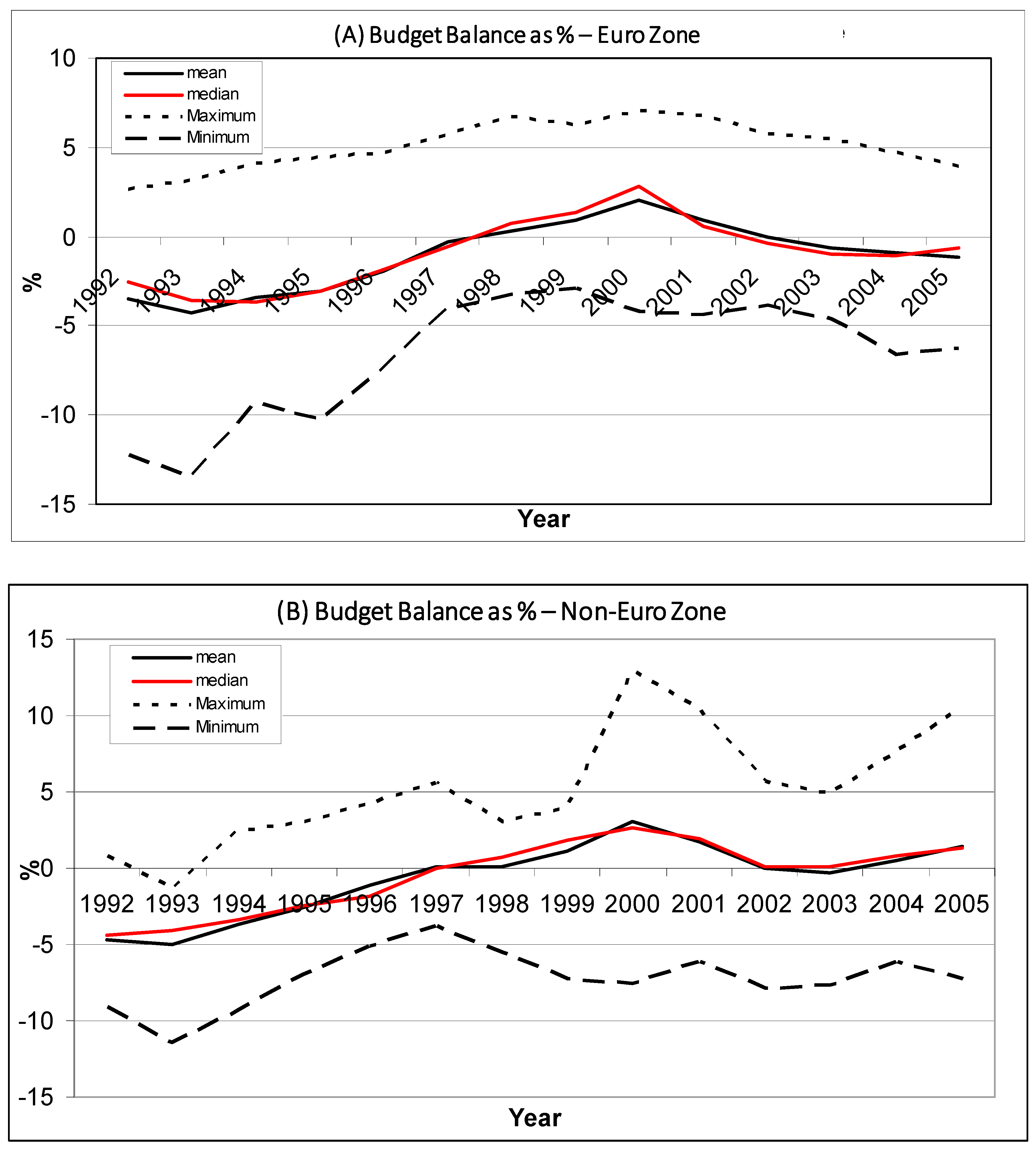

4.1. Preliminary Description

4.2. Correlation Analysis

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Coefficient | R-Squared | ||||

|---|---|---|---|---|---|

| rwt | Rwt × Det | Det | Constant | ||

| Austria | 0.4971 *** | −0.1883 *** | 0.3169 *** | −0.0261 | 0.1862 |

| Belgium | 0.6079 *** | 0.1158 | −0.2106 | 0.2346 *** | 0.3628 |

| Finland | 0.9211 *** | 0.6801 *** | −0.4362 | 0.5143 *** | 0.3511 |

| France | 0.7946 *** | 0.3019 *** | −0.0924 | 0.1378 | 0.5307 |

| Germany | 0.7516 *** | 0.3689 *** | −0.1933 | 0.1338 | 0.5708 |

| Greece | 0.7488 *** | 0.0344 | −0.2990 | 0.3798 * | 0.1442 |

| Ireland | 0.6338 *** | −0.0337 | −0.2286 | 0.3091 *** | 0.2649 |

| Italy | 0.7605 *** | 0.1409 | −0.1959 | 0.2034 | 0.2892 |

| Luxemburg | 0.2456 *** | 0.1886 * | −0.2856 * | 0.3564 *** | 0.0967 |

| Netherlands | 0.8186 *** | 0.1735 * | −0.2854 ** | 0.2419 *** | 0.5142 |

| Portugal | 0.6111 *** | −0.1192 | −0.2935 ** | 0.2726 *** | 0.2511 |

| Spain | 0.9657 *** | −0.0866 | −0.2301 | 0.2457 ** | 0.4444 |

| Australia | 0.5838 *** | −0.0918 | 0.0277 | 0.1208 | 0.3459 |

| Canada | 0.8143 *** | −0.0514 | 0.0397 | 0.0974 | 0.5623 |

| Denmark | 0.4376 *** | 0.1742 ** | 0.0065 | 0.1609 | 0.2331 |

| Japan | 0.9785 *** | −0.1313 | 0.3618 ** | −0.2894 *** | 0.3860 |

| New Zealand | 0.4993 *** | −0.2218 *** | 0.0452 | 0.1250 | 0.1568 |

| Norway | 0.7993 *** | −0.1121 | 0.1239 | 0.0934 | 0.2814 |

| Sweden | 0.9866 *** | 0.1838 * | −0.1900 | 0.2501 * | 0.4444 |

| Switzerland | 0.7822 *** | 0.1057 | −0.2732 ** | 0.2567 *** | 0.4663 |

| UK | 0.6722 *** | 0.1778 *** | −0.1801 | 0.1732 ** | 0.5331 |

| US | 0.8170 *** | 0.2919 *** | −0.2460 *** | 0.1799 *** | 0.7616 |

4.3. Cointegration Analysis

5. Discussion

6. Conclusions

Author Contributions

Funding

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

| 1 | The eleven countries include Austria, Belgium, Finland, France, Germany, Ireland, Italy, Luxembourg, Netherlands, Portugal, and Spain. United Kingdom and Denmark opted not to join the euro, although they are EU member countries. Greece could not fulfill the admission criteria initially but joined on 1 January 2001. |

| 2 | A Wall Street Journal article (8/2/2000 p.C12) by Michael R. Sisit states that global diversification becomes harder to achieve because the correlation among industry sectors is growing, in some cases, “frighteningly” so. Correlations among banks jumped from approximately zero in the past to around 0.5 and for telecommunications sectors from around zero to 0.4. The reason for the increase in correlations lies in the boom in cross-border investment, global deregulation, increased competition, industry consolidation, and mergers and acquisitions. |

| 3 | McGee (1999) presents performance figures for national stock market benchmarks over the two months after the euro. The figures range from −7.8% for Belgium to 5.1% for Ireland. Further, it provides similarly diverging economic growth forecasts for the different countries ranging from 1.6% for Germany to 6.8% for Ireland. Investment analysts argue that when the currency and debt markets are unified, “the only markets left that can move in response to Europe’s remaining national economic differences are stock market”. Monetary union has not eliminated other important economic differences that affect the stock market, such as labor regulations and taxes. So macroeconomic differences are being reflected in stock prices to a degree never seen. |

| 4 | Mean variance analysis is the standard portfolio analysis to maximize the mean return and minimize risk (variance of return). The ability to minimize risk through diversification depends on the correlation among assets. |

| 5 | The “EMU Assessment” Special Issue of Economic Policy (De Menil and Portes 2003) covers the impact of the euro on fiscal policy, inflation convergence, trade, monetary transmission, and government bond spreads. It does not cover stock markets. Bartram et al. (2007) use the copula dependence model and found an increased dependence for the larger European equity markets of Germany, France, Italy, and the Netherlands but none for the rest. |

| 6 | For a detailed discussion of the test methodologies for cointegration, see Johansen and Juselius (1990), Dickey et al. (1991), and Dercon (1995), to mention a few. These and other studies provide details on alternative testing procedures as well. See also Whistler and White (2004) Shazam Econometrics Software User’s Reference Manual. Version 10, pp. 167–77. |

| 7 | An earlier version of this study was based on Morgan Stanley Capital International Indices (MSCI) for each country. The results are qualitatively the same as the ones reported here. I switched to Data Stream indices because the MSCI do not have weekly series for earlier years. |

| 8 | Cross-country correlations of the eurozone and non-eurozone countries show the same patterns as reported in Table 2. Austria’s correlations with other countries decreased after the euro. Other cross-correlations show mixed results. The correlations of Austria, Japan, and New Zealand with the world market index decreased after the euro. |

| 9 | One possible reason for such results is the fact that the post-1999 period experienced a hi-tech (dotcom) bubble burst and a general decline in stock prices across the globe. |

| 10 | The results of the unit root test are not reported. They are available from the author. |

| 11 | The only difference between Equations (1)–(3) and (5) is that Equation (5) is for multiple indices and involves multivariate regression. The choice of France and Germany as the regressand in the eurozone and the US in the comparison analysis was purely in consideration of their relative economic sizes. The use of any other index does not change the results qualitatively. |

| 12 | Haynes and Alemna (2023), Cavallaro and Villani (2021), and Monfort et al. (2013) show the existence of club clusters in the European zones and, hence, economic convergences based on the growth and economic development of the countries. |

| 13 | The series is not available for Greece and Luxembourg in the eurozone and New Zealand, so the figures do not include interest rates from these countries. |

References

- Aggarwal, Raj, and NyoNyo A. Kyaw. 2005. Equity Market Integration in the NAFTA Region: Evidence from Unit Root and Cointegration Tests. International Review of Financial Analysis 14: 393–406. [Google Scholar] [CrossRef]

- Bartram, Sohnke M., Stephen J. Taylor, and Yaw-Huei Wang. 2007. The Euro and European Financial Market Dependence. Journal of Banking and Finance 31: 1461–81. [Google Scholar] [CrossRef]

- Barunik, Jozef, and Lukas Vacha. 2013. Contagion among Central and Eastern European stock markets during the financial crisis. arXiv arXiv:1309.0491. [Google Scholar]

- Bekaert, Geert, and Campbell R. Harvey. 1995. Time-Varying World Market Integration. Journal of Finance 50: 403–44. [Google Scholar]

- Beliu, Sonila, and Matthew L. Higgins. 2004. Fractional cointegration analysis of EU convergence. Applied Economics 36: 1607–11. [Google Scholar] [CrossRef]

- Bremus, Franziska, and Tatsiana Kliatskova. 2020. Legal harmonization, institutional quality, and countries’ external positions: A sectoral analysis. Journal of International Money and Finance 107: 102217. [Google Scholar] [CrossRef]

- Buch, Claudia M. 2000. Capital Market Integration in Euroland: The Role of Banks. German Economic Review 1: 443–64. [Google Scholar] [CrossRef][Green Version]

- Cărăuşu, Dumitru Nicuşor, Bogdan Florin Filip, Elena Cigu, and Carmen Toderaşcu. 2018. Contagion of capital markets in CEE countries: Evidence from wavelet analysis. Emerging Markets Finance and Trade 54: 618–41. [Google Scholar] [CrossRef]

- Cavallaro, Eleonora, and Ilaria Villani. 2021. Club Convergence in EU Countries. Journal of Economic Integration 36: 125–61. [Google Scholar] [CrossRef]

- Chan, Kam C., Benton E. Gup, and Ming-Shiun Pan. 1992. An Empirical Analysis of Stock Prices in Major Asian Markets and the United States. Financial Review 27: 289–95. [Google Scholar] [CrossRef]

- DeFusco, Richard A., John M. Geppert, and George P. Tsetsekos. 1996. Long-Run Diversification Potential in Emerging Stock Markets. Financial Review 31: 343–63. [Google Scholar] [CrossRef]

- De Menil, Georges, and R. Portes, eds. 2003. EMU Assessment. In Economic Policy. Hoboken: Blackwell Publishers. [Google Scholar]

- Dercon, Stefan. 1995. On Market Integration and Liberalization: Methods and Application to Ethiopia. Journal of Development Studies 32: 112–43. [Google Scholar] [CrossRef]

- Dickey, David D., Dennis W. Jansen, and Daniel L. Thornton. 1991. A Primer on Cointegration with an Application to Money and Income. St. Louis: Federal Reserve Bank of St. Louis, pp. 58–78. [Google Scholar]

- Halpern, Philip. 1993. Investing Abroad: A Review of Capital Market Integration and Manager Performance. Journal of Portfolio Management 19: 47–57. [Google Scholar] [CrossRef]

- Haynes, Philip, and David Alemna. 2023. Convergence Trends in Euro Economies: Financial Crisis Recovery and the COVID-19 Pandemic. Economies 11: 284. [Google Scholar] [CrossRef]

- Heaney, Richard, Vince Hooper, and Martin Jaugietis. 1999. Regional Integration of National Stock Markets. SSRN Electronic Journal. [Google Scholar] [CrossRef]

- Heaney, Richard, Vince Hooper, and Martin Jaugietis. 2002. Regional Integration of Stock Markets in Latin America. Journal of Economic Integration 17: 745–60. [Google Scholar] [CrossRef]

- Johansen, Søren, and Katarina Juselius. 1990. Maximum Likelihood Estimation and Inference on Cointegration-with Applications to the Demand for Money. Oxford Bulletin of Economics and Statistics 52: 169–210. [Google Scholar] [CrossRef]

- Krarup, Troels. 2021. Money and the ‘level playing field’: The epistemic problem of European financial market integration. New Political Economy 26: 36–51. [Google Scholar] [CrossRef]

- McGee, Suzanne. 1999. Tax Inquiry Turns Banking Grayer in Luxembourg. Wall Street Journal 20. [Google Scholar]

- Monfort, Mercedes, Juan Carlos Cuestas, and Javier Ordóñez. 2013. Real convergence in Europe: A cluster analysis. Economic Modelling 33: 689–94. [Google Scholar] [CrossRef]

- Pardal, Pedro, Rui Dias, Petr Šuleř, Nuno Teixeira, and Tomáš Krulický. 2020. Integration in Central European capital markets in the context of the global COVID-19 pandemic. Equilibrium. Quarterly Journal of Economics and Economic Policy 15: 627–50. [Google Scholar] [CrossRef]

- Steeley, Patricia L., and James M. Steeley. 1999. Changes in the Comovement of European Equity Markets. Economic Inquiry 37: 473–81. [Google Scholar] [CrossRef]

- Steeley, Patricia L., James M. Steeley, and Eric J. Pentecost. 1998. Exchange Controls and European Stock Market Integration. Applied Economics 30: 263–66. [Google Scholar] [CrossRef]

- Umutlu, Mehmet, Seher Goren Yargi, and Adam Zaremba. 2023. Market segmentation and international diversification across country and industry portfolios. Research in International Business and Finance 65: 101954. [Google Scholar] [CrossRef]

- Whistler, Diana, and Kenneth White. 2004. Shazam Econometrics Software: User’s Reference Manual. Version 10, (Northwest Econometrics). Vancouver: Northwest Econometrics Ltd. [Google Scholar]

| Panel A: 13 January 1992–19 December 2005. | |||||||||||||

| The returns are based on Data Stream country total return market indices. The returns are measured weekly and expressed in percent. Autocorrelation functions (ACFs) of the index returns for up to 6 lags are reported. * ACF coefficient indicating significance at the 5% level. All mean returns are significant at the 5% level, except for Japan’s index return. The number of observations is 728 for all countries covering the weeks from 13 January 1992 to 19 December 2005. | |||||||||||||

| Mean | Median | Std. Deviation | Minimum | Maximum | Kurtosis | Skew-ness | ACF Coefficients for Lags | ||||||

| 1 | 2 | 3 | 4 | 5 | 6 | ||||||||

| Austria | 0.211 | 0.279 | 1.855 | −6.711 | 6.851 | 0.968 | −0.097 | 0.085 * | 0.098 * | 0.031 * | 0.083 * | 0.038 * | −0.048 * |

| Belgium | 0.248 | 0.383 | 2.258 | −10.672 | 13.485 | 5.14 | −0.070 | −0.061 | 0.011 | 0.034 | 0.003 | −0.059 | 0.029 |

| Finland | 0.508 | 0.529 | 4.607 | −19.272 | 15.488 | 1.524 | −0.188 | −0.012 | 0.033 | 0.047 | −0.005 | 0.135 * | 0.015 * |

| France | 0.256 | 0.386 | 2.696 | −11.791 | 10.867 | 1.853 | −0.253 | −0.102 * | 0.007 * | 0.067 * | −0.012 * | −0.029 * | 0.056 * |

| Germany | 0.198 | 0.381 | 2.608 | −11.735 | 11.478 | 1.852 | −0.374 | −0.002 | −0.003 | 0.03 | −0.024 | 0.004 | 0.064 |

| Greece | 0.37 | 0.281 | 4.071 | −18.405 | 16.468 | 2.387 | 0.209 | −0.026 | 0.008 | 0.031 | −0.007 | 0.059 | 0.014 |

| Ireland | 0.309 | 0.432 | 2.398 | −10.759 | 9.177 | 2.077 | −0.395 | 0.081 * | 0.049 * | −0.050 * | 0.017 | 0.070 * | −0.019 |

| Italy | 0.254 | 0.326 | 3.149 | −13.308 | 10.493 | 1.44 | −0.160 | −0.025 | 0.043 | 0.054 | −0.022 | −0.055 | −0.014 |

| Luxemburg | 0.271 | 0.312 | 2.411 | −16.884 | 14.462 | 8.717 | −0.317 | 0.134 * | 0.084 * | 0.109 * | 0.069 * | 0.075 * | 0.061 * |

| Netherlands | 0.26 | 0.409 | 2.585 | −14.360 | 12.627 | 4.592 | −0.597 | −0.097 * | 0.069 * | 0.029 * | −0.039 * | −0.054 * | 0.048 * |

| Portugal | 0.23 | 0.128 | 2.198 | −11.768 | 10.374 | 3.784 | −0.191 | 0.081 * | 0.105 * | 0.066 * | 0.046 * | 0.069 * | 0.039 * |

| Spain | 0.302 | 0.42 | 2.752 | −10.222 | 12.963 | 1.692 | −0.174 | −0.031 | 0.017 | 0.096 | −0.029 | 0.012 | −0.002 |

| Australia | 0.236 | 0.244 | 1.803 | −8.611 | 8.937 | 2.354 | 0.01 | −0.093 * | 0.046 * | −0.019 * | −0.006 | −0.015 | −0.012 |

| Canada | 0.263 | 0.41 | 2.086 | −11.071 | 8.384 | 3.578 | −0.712 | −0.074 * | 0.070 * | 0.022 * | −0.081 * | 0.061 * | 0.007 * |

| Denmark | 0.255 | 0.299 | 2.26 | −11.419 | 8.443 | 1.712 | −0.322 | 0.042 | 0.076 | 0.023 | −0.034 | −0.032 | 0.003 |

| Japan | 0.062 | 0.229 | 2.906 | −10.516 | 14.283 | 1.386 | 0.112 | −0.046 | −0.032 | −0.009 | 0 | 0.039 | 0.014 |

| New Zealand | 0.225 | 0.246 | 1.936 | −8.642 | 7.525 | 2.465 | −0.085 | 0.003 | 0.054 | 0.016 | 0.003 | −0.067 | −0.047 |

| Norway | 0.295 | 0.453 | 2.764 | −14.140 | 11.944 | 2.901 | −0.601 | 0.004 | 0.120 * | −0.009 * | −0.043 * | 0.092 * | 0 |

| Sweden | 0.348 | 0.478 | 3.294 | −12.940 | 18.576 | 2.182 | −0.041 | −0.011 | 0.035 | 0.053 | −0.061 | 0.105 * | 0.048 * |

| Switzerland | 0.27 | 0.416 | 2.485 | −14.732 | 10.131 | 4.14 | −0.653 | −0.128 * | 0.070 * | 0.011 * | 0.002 * | −0.022 * | 0.071 * |

| UK | 0.218 | 0.316 | 2.142 | −12.365 | 8.371 | 3.129 | −0.396 | −0.083 * | 0.031 | 0.047 | −0.075 * | 0 | −0.031 |

| US | 0.225 | 0.346 | 2.291 | −12.175 | 9.462 | 2.892 | −0.297 | −0.123 * | 0.026 * | 0.011 * | −0.087 * | 0.039 * | −0.011 * |

| World | 0.183 | 0.332 | 1.995 | −8.460 | 7.566 | 1.401 | −0.452 | −0.048 | 0.047 | 0.033 | −0.076 | 0.029 | −0.014 |

| Panel B: Comparison of the before and after euro periods. | |||||||||||||

| Returns (%) are based on the Data Stream total market index for each country and are calculated on a weekly basis. Both samples have an equal number of observations: 364 each for all countries. | |||||||||||||

| Before Euro (13 January 1992–28 December 1998) | After Euro (6 January 1999–19 December 2005) | ||||||||||||

| Mean | Median | Std. Deviation | Minimum | Maximum | Mean | Median | Std. Deviation | Minimum | Maximum | ||||

| Austria | 0.093 | 0.217 | 1.93 | −6.711 | 6.851 | 0.33 | 0.337 | 1.772 | −6.002 | 5.825 | |||

| Belgium | 0.38 | 0.432 | 1.884 | −9.010 | 7.052 | 0.116 | 0.312 | 2.574 | −10.672 | 13.485 | |||

| Finland | 0.735 | 0.606 | 3.707 | −14.502 | 13.926 | 0.281 | 0.484 | 5.355 | −19.272 | 15.488 | |||

| France | 0.328 | 0.464 | 2.438 | −10.038 | 8.03 | 0.185 | 0.21 | 2.933 | −11.791 | 10.867 | |||

| Germany | 0.314 | 0.443 | 2.209 | −11.735 | 5.556 | 0.083 | 0.2 | 2.951 | −8.505 | 11.478 | |||

| Greece | 0.559 | 0.263 | 4.101 | −13.217 | 15.851 | 0.18 | 0.302 | 4.038 | −18.405 | 16.468 | |||

| Ireland | 0.461 | 0.357 | 2.354 | −10.759 | 9.177 | 0.157 | 0.5 | 2.435 | −8.278 | 6.879 | |||

| Italy | 0.385 | 0.16 | 3.503 | −13.308 | 10.493 | 0.122 | 0.43 | 2.748 | −11.981 | 9.079 | |||

| Luxemburg | 0.415 | 0.392 | 1.705 | −9.567 | 6.771 | 0.126 | 0.165 | 2.948 | −16.884 | 14.462 | |||

| Netherlands | 0.438 | 0.419 | 2.253 | −12.761 | 7.337 | 0.082 | 0.393 | 2.87 | −14.360 | 12.627 | |||

| Portugal | 0.419 | 0.251 | 2.392 | −11.768 | 10.374 | 0.042 | 0.046 | 1.97 | −9.537 | 6.102 | |||

| Spain | 0.477 | 0.533 | 2.909 | −10.222 | 12.963 | 0.127 | 0.242 | 2.577 | −8.732 | 8.485 | |||

| Australia | 0.261 | 0.219 | 1.948 | −5.984 | 8.937 | 0.211 | 0.309 | 1.648 | −8.611 | 5.868 | |||

| Canada | 0.292 | 0.388 | 1.998 | −11.071 | 6.819 | 0.234 | 0.442 | 2.174 | −9.739 | 8.384 | |||

| Denmark | 0.266 | 0.237 | 2.177 | −11.419 | 7.097 | 0.245 | 0.332 | 2.344 | −7.978 | 8.443 | |||

| Japan | −0.055 | −0.103 | 2.713 | −9.544 | 14.283 | 0.18 | 0.4 | 3.086 | −10.516 | 11.373 | |||

| New Zealand | 0.245 | 0.233 | 2.211 | −8.387 | 7.525 | 0.205 | 0.2624 | 1.616 | −8.642 | 5.683 | |||

| Norway | 0.285 | 0.393 | 2.998 | −14.140 | 11.944 | 0.305 | 0.466 | 2.513 | −9.973 | 7.16 | |||

| Sweden | 0.486 | 0.553 | 3.203 | −12.940 | 18.576 | 0.209 | 0.314 | 3.381 | −10.328 | 10.9 | |||

| Switzerland | 0.444 | 0.552 | 2.386 | −14.732 | 10.131 | 0.096 | 0.255 | 2.571 | −10.626 | 9.179 | |||

| UK | 0.334 | 0.291 | 1.96 | −8.118 | 7.755 | 0.101 | 0.361 | 2.307 | −12.365 | 8.371 | |||

| US | 0.376 | 0.433 | 1.939 | −12.175 | 7.716 | 0.075 | 0.199 | 2.59 | −9.989 | 9.462 | |||

| World | 0.239 | 0.372 | 1.807 | −8.399 | 5.912 | 0.127 | 0.225 | 2.168 | −8.460 | 7.566 | |||

| Panel A: Eurozone Countries | |||||||||||

| N = 364 before as well as after the euro. The figures reported are Pearson correlations. All correlation coefficients (before and after the euro) are positive and statistically significant at the 1% level. | |||||||||||

| Before Euro | Austria | Belgium | Finland | France | Germany | Greece | Ireland | Italy | Luxemburg | Netherlands | Portugal |

| Belgium | 0.538 | ||||||||||

| Finland | 0.442 | 0.515 | |||||||||

| France | 0.541 | 0.641 | 0.526 | ||||||||

| Germany | 0.585 | 0.687 | 0.557 | 0.748 | |||||||

| Greece | 0.279 | 0.338 | 0.346 | 0.339 | 0.348 | ||||||

| Ireland | 0.458 | 0.5 | 0.448 | 0.485 | 0.534 | 0.382 | |||||

| Italy | 0.359 | 0.472 | 0.435 | 0.551 | 0.554 | 0.222 | 0.337 | ||||

| Luxemburg | 0.38 | 0.414 | 0.281 | 0.352 | 0.41 | 0.22 | 0.388 | 0.25 | |||

| Netherlands | 0.6 | 0.735 | 0.588 | 0.754 | 0.808 | 0.36 | 0.583 | 0.554 | 0.423 | ||

| Portugal | 0.395 | 0.532 | 0.36 | 0.529 | 0.544 | 0.408 | 0.41 | 0.403 | 0.302 | 0.571 | |

| Spain | 0.49 | 0.588 | 0.468 | 0.648 | 0.673 | 0.354 | 0.459 | 0.561 | 0.324 | 0.688 | 0.515 |

| After Euro | Austria | Belgium | Finland | France | Germany | Greece | Ireland | Italy | Luxemburg | Netherlands | Portugal |

| Belgium | 0.381 | ||||||||||

| Finland | 0.11 | 0.326 | |||||||||

| France | 0.319 | 0.721 | 0.677 | ||||||||

| Germany | 0.395 | 0.689 | 0.644 | 0.905 | |||||||

| Greece | 0.234 | 0.306 | 0.317 | 0.421 | 0.438 | ||||||

| Ireland | 0.296 | 0.456 | 0.302 | 0.503 | 0.558 | 0.258 | |||||

| Italy | 0.343 | 0.644 | 0.558 | 0.868 | 0.829 | 0.371 | 0.493 | ||||

| Luxemburg | 0.151 | 0.247 | 0.2 | 0.359 | 0.369 | 0.254 | 0.229 | 0.409 | |||

| Netherlands | 0.35 | 0.788 | 0.576 | 0.893 | 0.859 | 0.377 | 0.52 | 0.818 | 0.363 | ||

| Portugal | 0.188 | 0.404 | 0.473 | 0.589 | 0.577 | 0.346 | 0.361 | 0.563 | 0.281 | 0.479 | |

| Spain | 0.344 | 0.672 | 0.601 | 0.821 | 0.818 | 0.387 | 0.458 | 0.79 | 0.299 | 0.79 | 0.589 |

| Changes in the correlations (after euro–before euro). * Indicates statistical significance for the change at the 5% level, using a two-tailed test. | |||||||||||

| Austria | Belgium | Finland | France | Germany | Greece | Ireland | Italy | Luxemburg | Netherlands | Portugal | |

| Belgium | −0.157 * | ||||||||||

| Finland | −0.333 * | −0.189 * | |||||||||

| France | −0.223 * | 0.080 * | 0.151 * | ||||||||

| Germany | −0.190 * | 0.002 | 0.087 | 0.157 * | |||||||

| Greece | −0.045 | −0.032 | −0.028 | 0.081 | 0.09 | ||||||

| Ireland | −0.162 * | −0.044 | −0.146 * | 0.018 | 0.023 | −0.124 | |||||

| Italy | −0.016 | 0.173 * | 0.123 * | 0.317 * | 0.275 * | 0.150 * | 0.155 * | ||||

| Luxemburg | −0.229 * | −0.167 * | −0.081 | 0.007 | −0.041 | 0.034 | −0.158 * | 0.159 * | |||

| Netherlands | −0.250 * | 0.053 | −0.012 | 0.139 * | 0.051 * | 0.017 | −0.063 | 0.264 * | −0.060 | ||

| Portugal | −0.206 * | −0.128 * | 0.112 | 0.059 | 0.032 | −0.062 | −0.049 | 0.160 * | −0.021 | −0.092 | |

| Spain | −0.146 * | 0.084 | 0.133 * | 0.173 * | 0.145 * | 0.033 | 0 | 0.229 * | −0.025 | 0.102 * | 0.074 |

| Panel B: Correlations for Comparison Countries | |||||||||||

| All correlation coefficients (before and after the euro) are positive and statistically significant at the 1% level. | |||||||||||

| Before Euro | Australia | Canada | Denmark | Japan | New Zealand | Norway | Sweden | Switzerland | UK | US | |

| Canada | 0.513 | ||||||||||

| Denmark | 0.304 | 0.349 | |||||||||

| Japan | 0.343 | 0.303 | 0.159 | ||||||||

| New Zealand | 0.539 | 0.383 | 0.269 | 0.28 | |||||||

| Norway | 0.482 | 0.496 | 0.483 | 0.24 | 0.34 | ||||||

| Sweden | 0.54 | 0.544 | 0.431 | 0.283 | 0.343 | 0.642 | |||||

| Switzerland | 0.418 | 0.593 | 0.444 | 0.284 | 0.331 | 0.513 | 0.6 | ||||

| UK | 0.442 | 0.578 | 0.44 | 0.276 | 0.368 | 0.532 | 0.605 | 0.67 | |||

| US | 0.454 | 0.79 | 0.309 | 0.251 | 0.346 | 0.438 | 0.508 | 0.535 | 0.531 | ||

| World | 0.542 | 0.736 | 0.363 | 0.652 | 0.408 | 0.482 | 0.557 | 0.592 | 0.62 | 0.762 | |

| After Euro | Australia | Canada | Denmark | Japan | New Zealand | Norway | Sweden | Switzerland | UK | US | |

| Canada | 0.519 | ||||||||||

| Denmark | 0.508 | 0.483 | |||||||||

| Japan | 0.494 | 0.387 | 0.39 | ||||||||

| New Zealand | 0.46 | 0.307 | 0.322 | 0.276 | |||||||

| Norway | 0.516 | 0.543 | 0.545 | 0.361 | 0.299 | ||||||

| Sweden | 0.529 | 0.61 | 0.552 | 0.459 | 0.3 | 0.523 | |||||

| Switzerland | 0.476 | 0.541 | 0.548 | 0.374 | 0.253 | 0.53 | 0.641 | ||||

| UK | 0.569 | 0.598 | 0.571 | 0.404 | 0.331 | 0.562 | 0.722 | 0.796 | |||

| US | 0.553 | 0.73 | 0.471 | 0.417 | 0.323 | 0.506 | 0.656 | 0.715 | 0.732 | ||

| World | 0.647 | 0.761 | 0.566 | 0.595 | 0.372 | 0.593 | 0.751 | 0.749 | 0.799 | 0.928 | |

| Changes in the correlations (after euro–before euro). * Indicates statistical significance for the change at the 5% level, using a two-tailed test. | |||||||||||

| Australia | Canada | Denmark | Japan | New Zealand | Norway | Sweden | Switzerland | UK | US | ||

| Canada | 0.006 | ||||||||||

| Denmark | 0.205 * | 0.135 * | |||||||||

| Japan | 0.152 * | 0.084 | 0.231 * | ||||||||

| New Zealand | −0.078 | −0.076 | 0.053 | −0.004 | |||||||

| Norway | 0.035 | 0.047 | 0.062 | 0.121 | −0.041 | ||||||

| Sweden | −0.012 | 0.066 | 0.121 * | 0.176 * | −0.044 | −0.119 * | |||||

| Switzerland | 0.058 | −0.052 | 0.104 | 0.09 | −0.078 | 0.017 | 0.04 | ||||

| UK | 0.127 * | 0.02 | 0.131 * | 0.128 * | −0.037 | 0.03 | 0.117 * | 0.126 * | |||

| US | 0.099 | −0.060 | 0.162 * | 0.166 * | −0.024 | 0.067 | 0.148 * | 0.180 * | 0.201 * | ||

| World | 0.106 * | 0.025 | 0.203 * | −0.056 | −0.036 | 0.111 * | 0.194 * | 0.156 * | 0.179 * | 0.167 * | |

| N | Test Statistic | R-Squared | Durbin–Watson | No. of Lags | Cointegration? | |

|---|---|---|---|---|---|---|

| For Euro Area: Regressand: German Index | ||||||

| Before Euro | 365 | −5.3741 * | 0.9964 | 0.4079 | 12 | Yes |

| After Euro | 364 | −4.1974 | 0.9874 | 0.2851 | 2 | No |

| Entire Period | 729 | −5.002 * | 0.9948 | 0.1695 | 7 | Yes |

| For Euro Area: Refressand: French Index | ||||||

| Before Euro | 365 | −5.54 * | 0.9936 | 0.4037 | 2 | Yes |

| After Euro a | 364 | −4.376 | 0.9934 | 0.5314 | 18 | No |

| Entire Period | 729 | −4.1676 | 0.9926 | 0.1669 | 11 | No |

| Non-Euro Area Comparison: Regressand: US Index | ||||||

| Before Euro | 365 | −3.2535 | 0.9942 | 0.2954 | 16 | No |

| After Euro | 364 | −3.6721 | 0.9707 | 0.6154 | 16 | No |

| Entire Period | 729 | −3.7764 | 0.9902 | 0.1638 | 7 | No |

| Cointegration of All Markets: Regressand: World Index | ||||||

| Before Euro | 365 | −4.5588 | 0.9978 | 0.6462 | 15 | No |

| After Euro | 364 | −5.4641 * | 0.9963 | 0.4897 | 3 | Yes |

| Entire period | 729 | −5.6771 * | 0.9981 | 0.4034 | 25 | Yes |

| Country | 1992 | 1993 | 1994 | 1995 | 1996 | 1997 | 1998 | 1999 | 2000 | 2001 | 2002 | 2003 | 2004 |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Austria | 2.28 | 0.60 | 2.58 | 2.18 | 2.45 | 2.00 | 3.50 | 3.40 | 3.53 | 0.88 | 0.98 | 1.38 | 2.38 |

| Belgium | 1.35 | −0.70 | 3.30 | 4.28 | 0.80 | 3.70 | 1.93 | 3.10 | 3.73 | 1.18 | 1.50 | 0.93 | 2.40 |

| Finland | −4.15 | −1.15 | 4.05 | 4.48 | 3.58 | 6.20 | 5.00 | 3.30 | 5.28 | 0.90 | 2.20 | 2.45 | 3.48 |

| France | 1.90 | −0.78 | 1.60 | 1.98 | 1.08 | 2.30 | 3.38 | 3.13 | 4.05 | 2.08 | 1.30 | 0.93 | 2.08 |

| Germany | 1.83 | −0.80 | 2.70 | 1.95 | 1.03 | 1.93 | 1.80 | 1.85 | 3.48 | 1.38 | 0.08 | −0.18 | 1.10 |

| Greece | 0.68 | −1.60 | 2.00 | 2.08 | 2.35 | 3.63 | 3.35 | 3.43 | 4.53 | 4.65 | 3.83 | 4.63 | 4.68 |

| Ireland | NA | NA | NA | NA | NA | NA | 8.63 | 10.68 | 9.20 | 6.30 | 6.08 | 4.40 | 4.55 |

| Italy | 0.70 | −0.85 | 2.30 | 2.95 | 1.03 | 2.05 | 1.75 | 1.65 | 3.15 | 1.68 | 0.38 | 0.35 | 0.98 |

| Luxembourg | NA | 8.70 | 4.20 | 3.80 | 3.60 | 9.00 | 7.55 | 7.81 | 9.02 | 1.55 | 2.46 | 2.93 | 4.53 |

| Netherlands | 1.50 | 0.68 | 2.85 | 3.03 | 3.03 | 3.83 | 4.38 | 4.00 | 3.45 | 1.30 | 0.08 | −0.10 | 1.73 |

| Portugal | NA | NA | NA | NA | 3.55 | 4.15 | 4.68 | 3.88 | 3.85 | 2.03 | 0.53 | −1.20 | 1.20 |

| Spain | 0.93 | −1.03 | 2.35 | 4.98 | 2.45 | 3.88 | 4.48 | 4.73 | 5.08 | 3.55 | 2.68 | 3.00 | 3.08 |

| Australia | 2.08 | 3.85 | 4.83 | 3.55 | 4.30 | 3.75 | 5.33 | 4.50 | 2.85 | 2.68 | 3.83 | NA | NA |

| Canada | 0.93 | 2.35 | 4.83 | 2.75 | 1.58 | 4.45 | 4.10 | 5.45 | 5.30 | 1.70 | 3.25 | NA | NA |

| Denmark | 1.95 | −0.10 | 5.53 | 3.10 | 2.83 | 3.20 | 2.15 | 2.60 | 3.53 | 0.70 | 0.48 | 0.65 | 2.05 |

| Japan | 0.95 | 0.20 | 1.05 | 1.95 | 3.63 | 1.75 | −1.10 | −0.03 | 2.38 | 0.20 | −0.28 | 1.40 | 2.63 |

| New Zealand | NA | 4.70 | 6.10 | 3.90 | 3.30 | 3.10 | −0.54 | 4.88 | 3.71 | 2.50 | 4.40 | 3.74 | 4.39 |

| Norway | 4.00 | 3.30 | 5.58 | 4.15 | 5.90 | 5.18 | 2.40 | 2.13 | 2.90 | 2.45 | 1.28 | 0.30 | 2.83 |

| Sweden | NA | NA | 4.10 | 4.23 | 1.30 | 2.63 | 3.58 | 4.33 | 4.43 | 1.20 | 1.98 | 1.58 | 3.13 |

| Switzerland | 0.03 | −0.28 | 1.05 | 0.40 | 0.53 | 1.88 | 2.80 | 1.33 | 3.60 | 1.05 | 0.30 | −0.28 | 2.08 |

| UK | 0.28 | 2.45 | 4.40 | 2.88 | 2.73 | 3.18 | 3.25 | 3.05 | 4.03 | 2.23 | 2.00 | 2.53 | 3.18 |

| US | 3.33 | 2.68 | 4.00 | 2.53 | 3.70 | 4.50 | 4.18 | 4.43 | 3.65 | 0.78 | 1.60 | 2.70 | 4.23 |

| Euro: Mean | 0.78 | 0.31 | 2.79 | 3.17 | 2.27 | 3.88 | 4.20 | 4.24 | 4.86 | 2.29 | 1.84 | 1.63 | 2.68 |

| Median | 1.35 | −0.79 | 2.64 | 2.99 | 2.45 | 3.70 | 3.94 | 3.41 | 3.95 | 1.61 | 1.40 | 1.15 | 2.39 |

| St. Dev. | 1.93 | 3.04 | 0.84 | 1.14 | 1.12 | 2.12 | 2.14 | 2.55 | 2.09 | 1.69 | 1.77 | 1.85 | 1.37 |

| Others: Mean | 1.69 | 2.13 | 4.15 | 2.94 | 2.98 | 3.36 | 2.61 | 3.27 | 3.64 | 1.55 | 1.88 | 1.58 | 3.06 |

| Median | 1.45 | 2.45 | 4.61 | 2.99 | 3.06 | 3.19 | 3.03 | 3.69 | 3.63 | 1.45 | 1.79 | 1.49 | 2.98 |

| St. Dev. | 1.42 | 1.80 | 1.76 | 1.16 | 1.57 | 1.13 | 2.04 | 1.76 | 0.84 | 0.88 | 1.55 | 1.35 | 0.88 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Ejara, D.D.; Upadhyaya, K. An Empirical Study of the Impact of the Euro on Cross-Country Diversification. Economies 2024, 12, 8. https://doi.org/10.3390/economies12010008

Ejara DD, Upadhyaya K. An Empirical Study of the Impact of the Euro on Cross-Country Diversification. Economies. 2024; 12(1):8. https://doi.org/10.3390/economies12010008

Chicago/Turabian StyleEjara, Demissew Diro, and Kamal Upadhyaya. 2024. "An Empirical Study of the Impact of the Euro on Cross-Country Diversification" Economies 12, no. 1: 8. https://doi.org/10.3390/economies12010008

APA StyleEjara, D. D., & Upadhyaya, K. (2024). An Empirical Study of the Impact of the Euro on Cross-Country Diversification. Economies, 12(1), 8. https://doi.org/10.3390/economies12010008