Effect of the Shadow Economy on Tax Reform in Developing Countries

Abstract

1. Introduction

2. Discussion on the Effect of the Shadow Economy on Tax Reform

2.1. Effect of the Shadow Economy on Revenue-Enhancing Structural Tax Reform

2.2. Effect of the Shadow Economy on Tax Transition Reform

3. Empirical Strategy

3.1. Empirical Strategy concerning the Effect of the Shadow Economy on Structural Tax Reform

3.1.1. Model Specification

3.1.2. Econometric Approach

3.2. Empirical Strategy concerning the Effect of the Shadow Economy on Tax Transition Reform

3.2.1. Model Specification

3.2.2. Econometric Approach

4. Empirical Results

4.1. Interpretation of Results of Table A1, Table A2 and Table A3

4.2. Interpretation of Results of Table A4

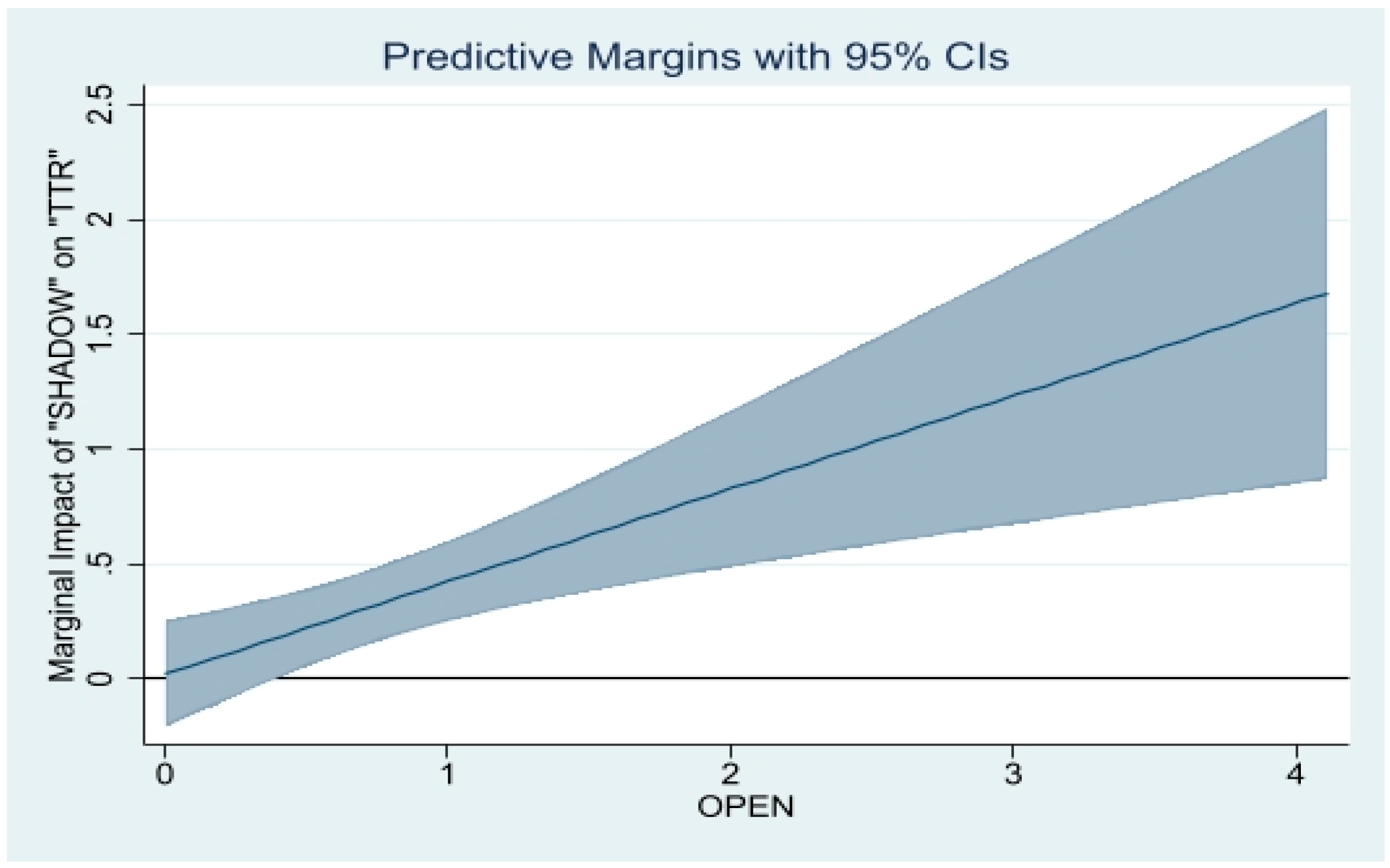

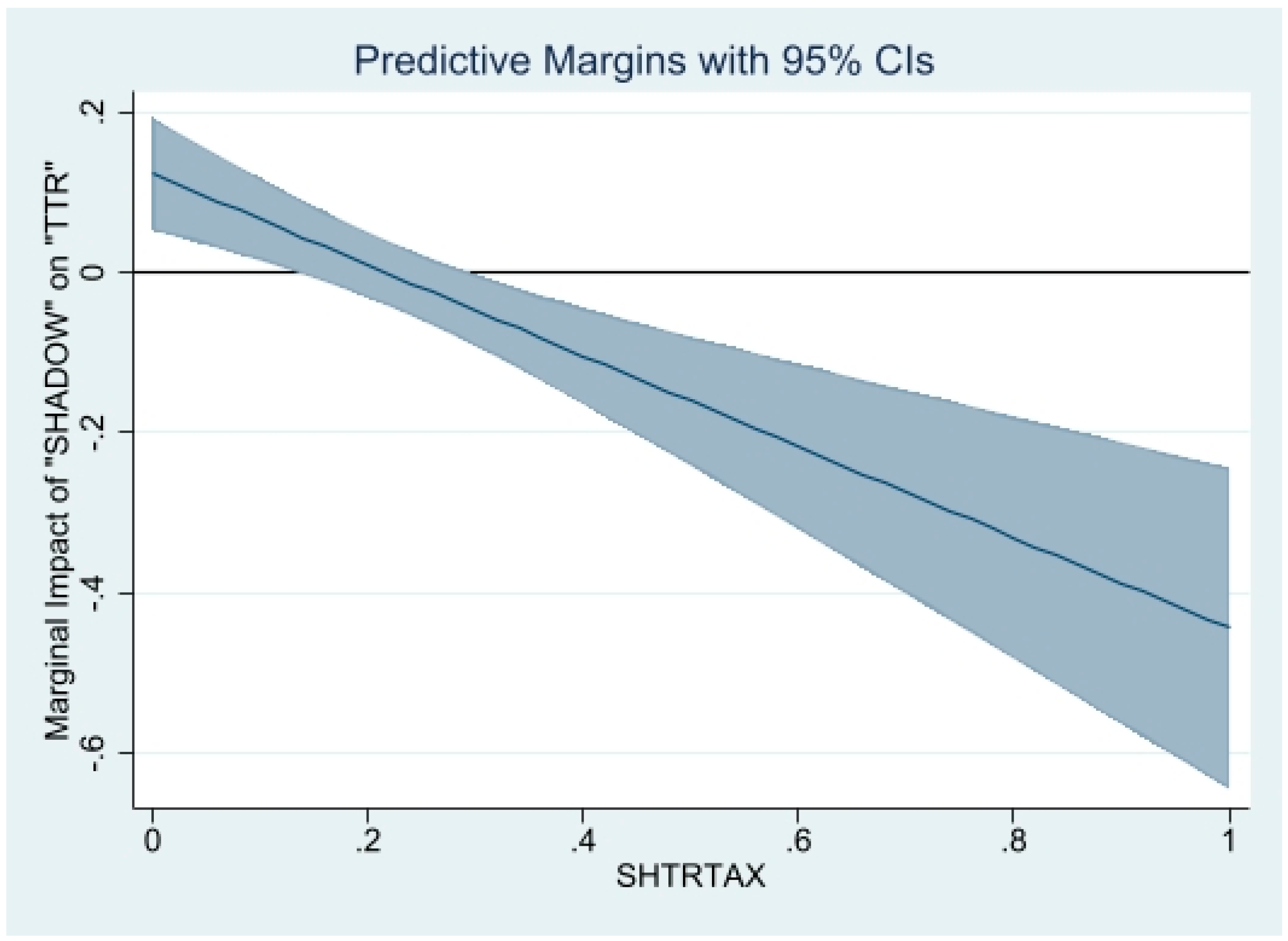

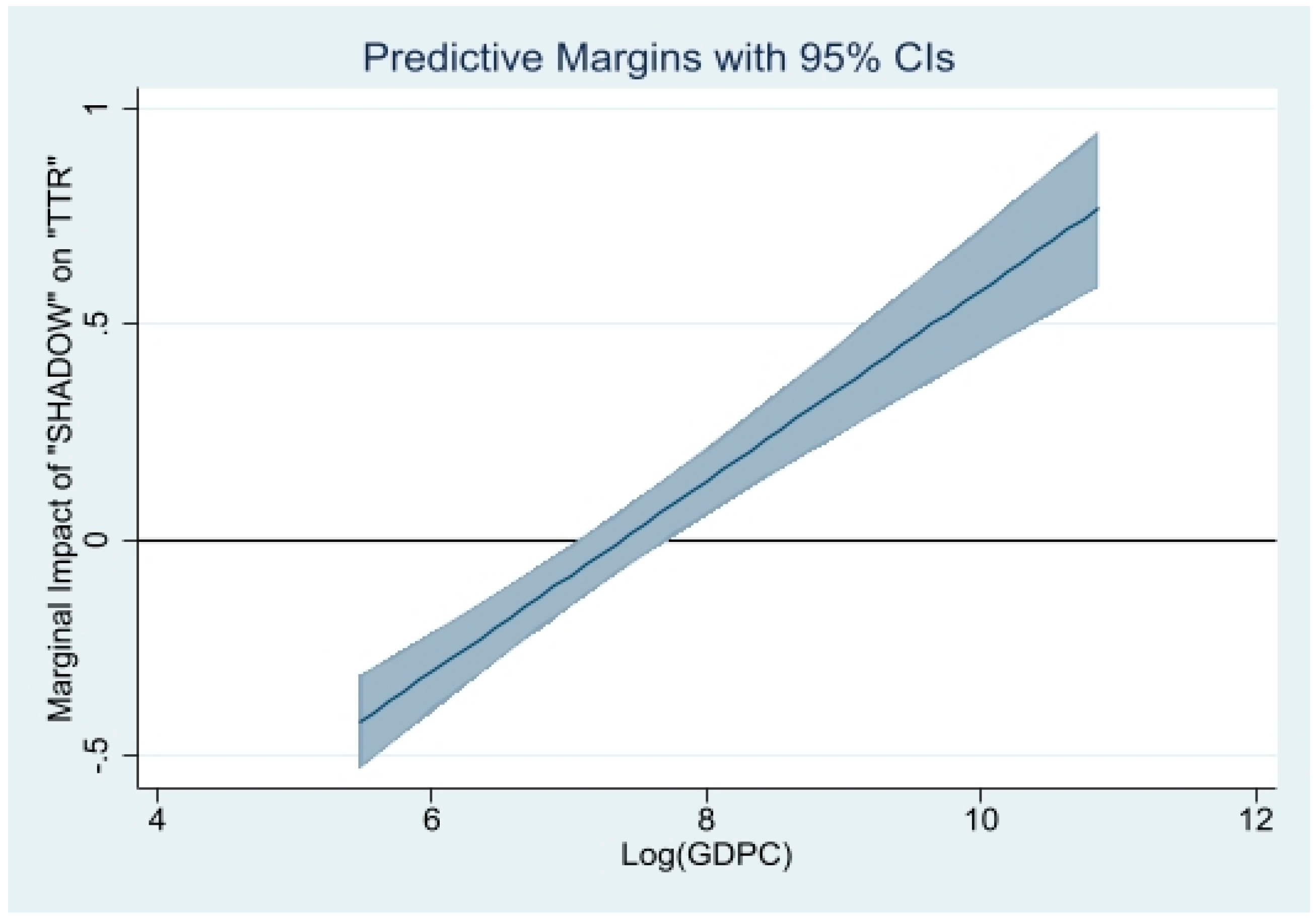

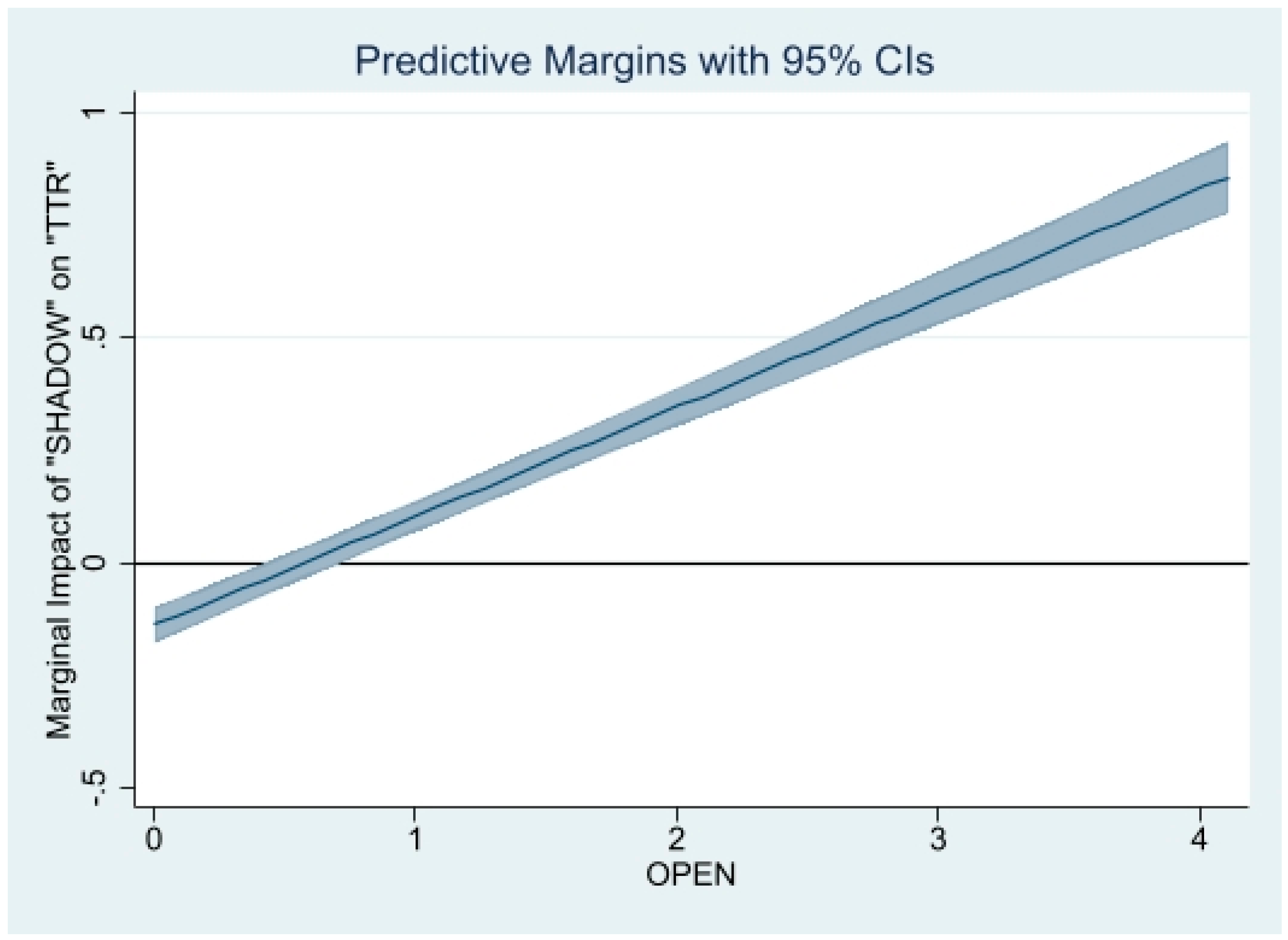

4.3. Interpretation of Results of Table A5 and Table A6

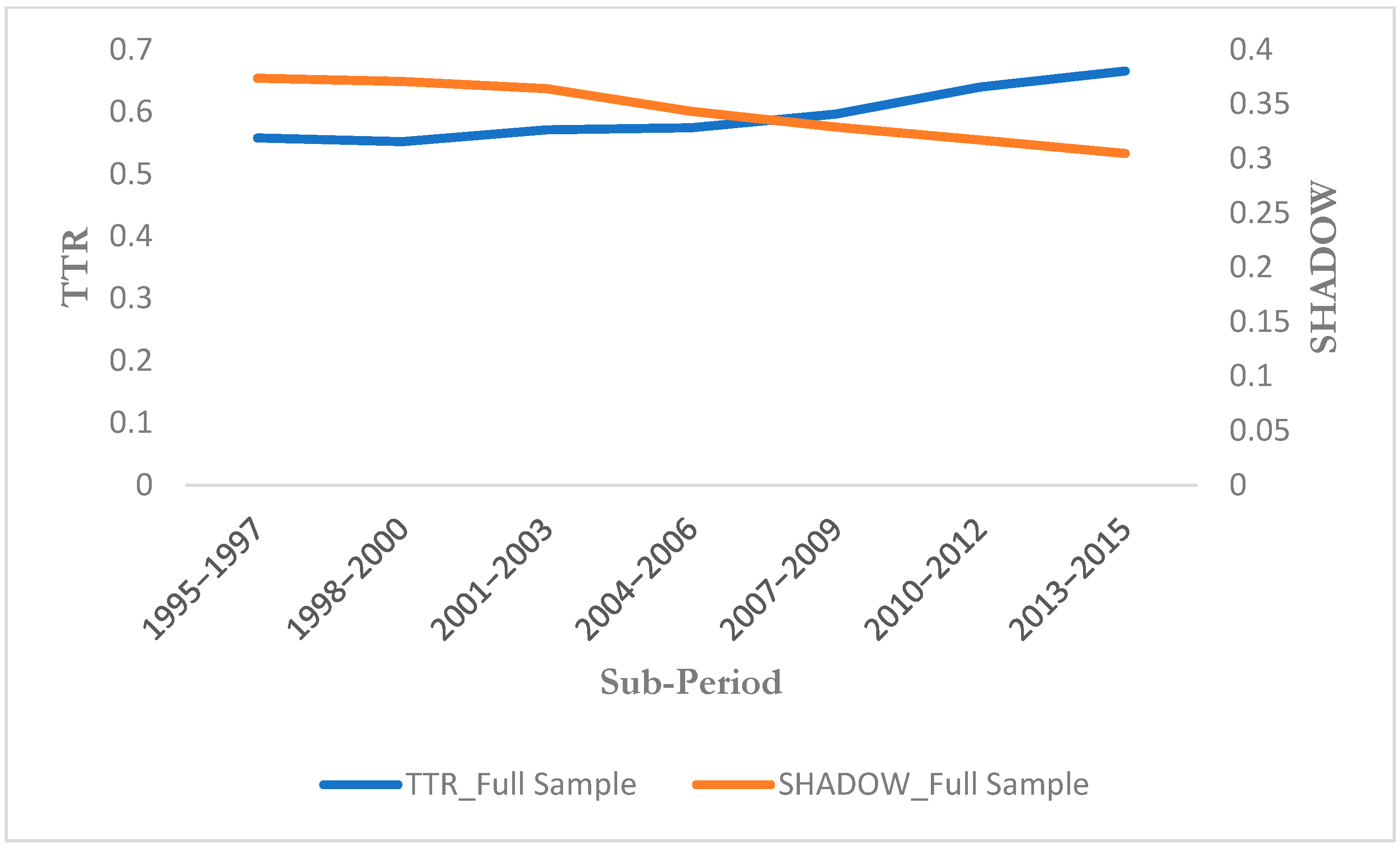

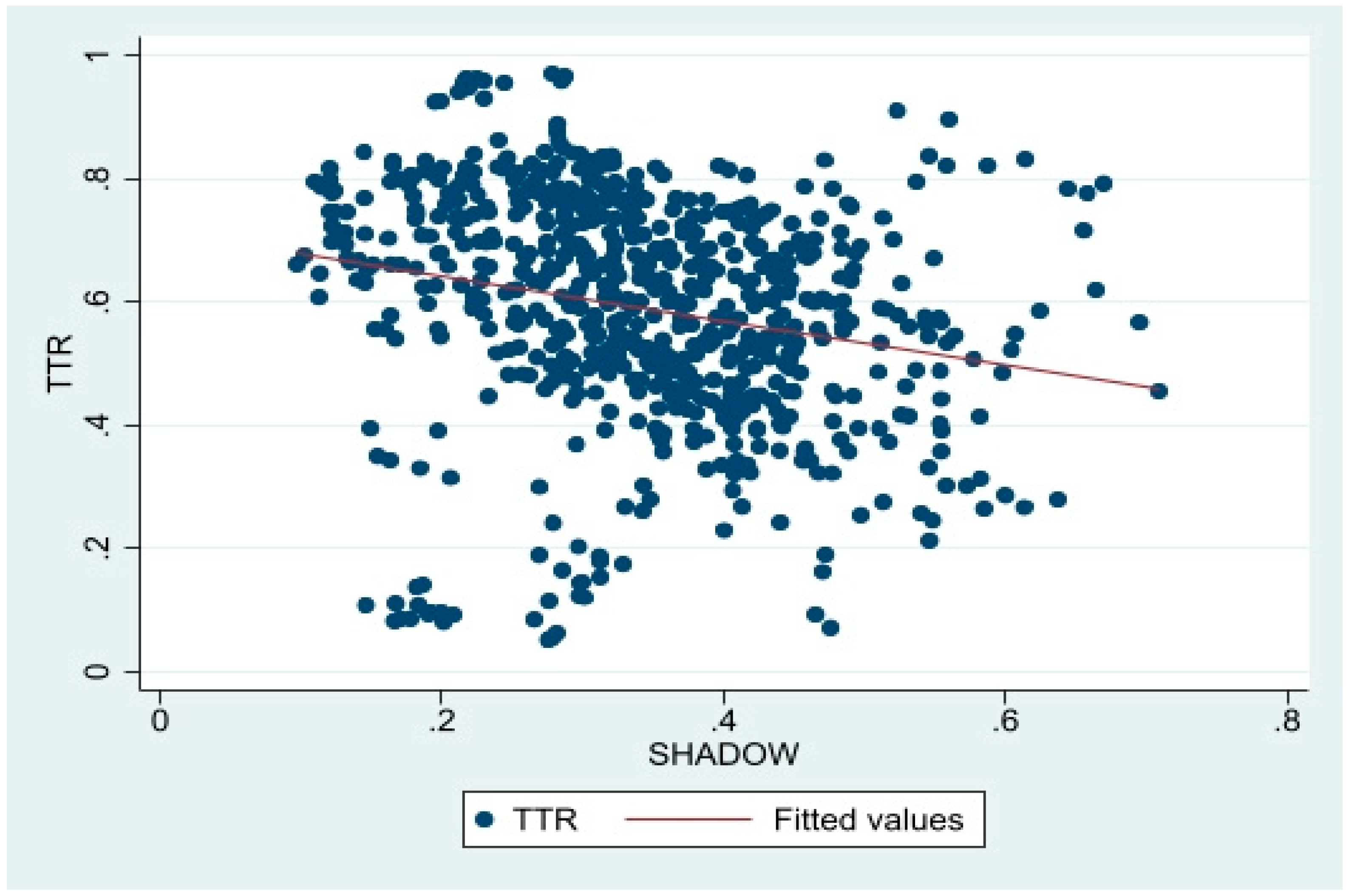

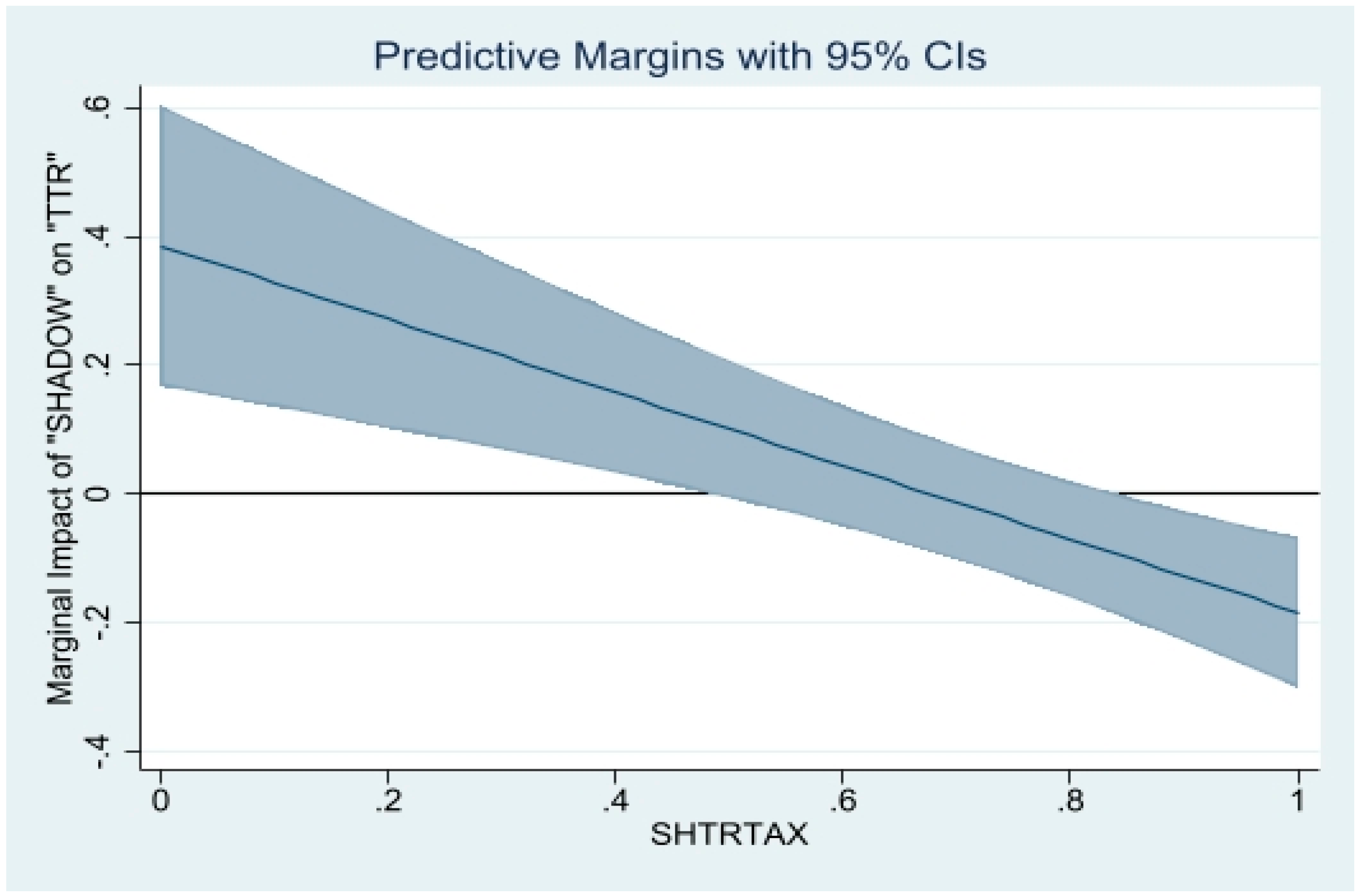

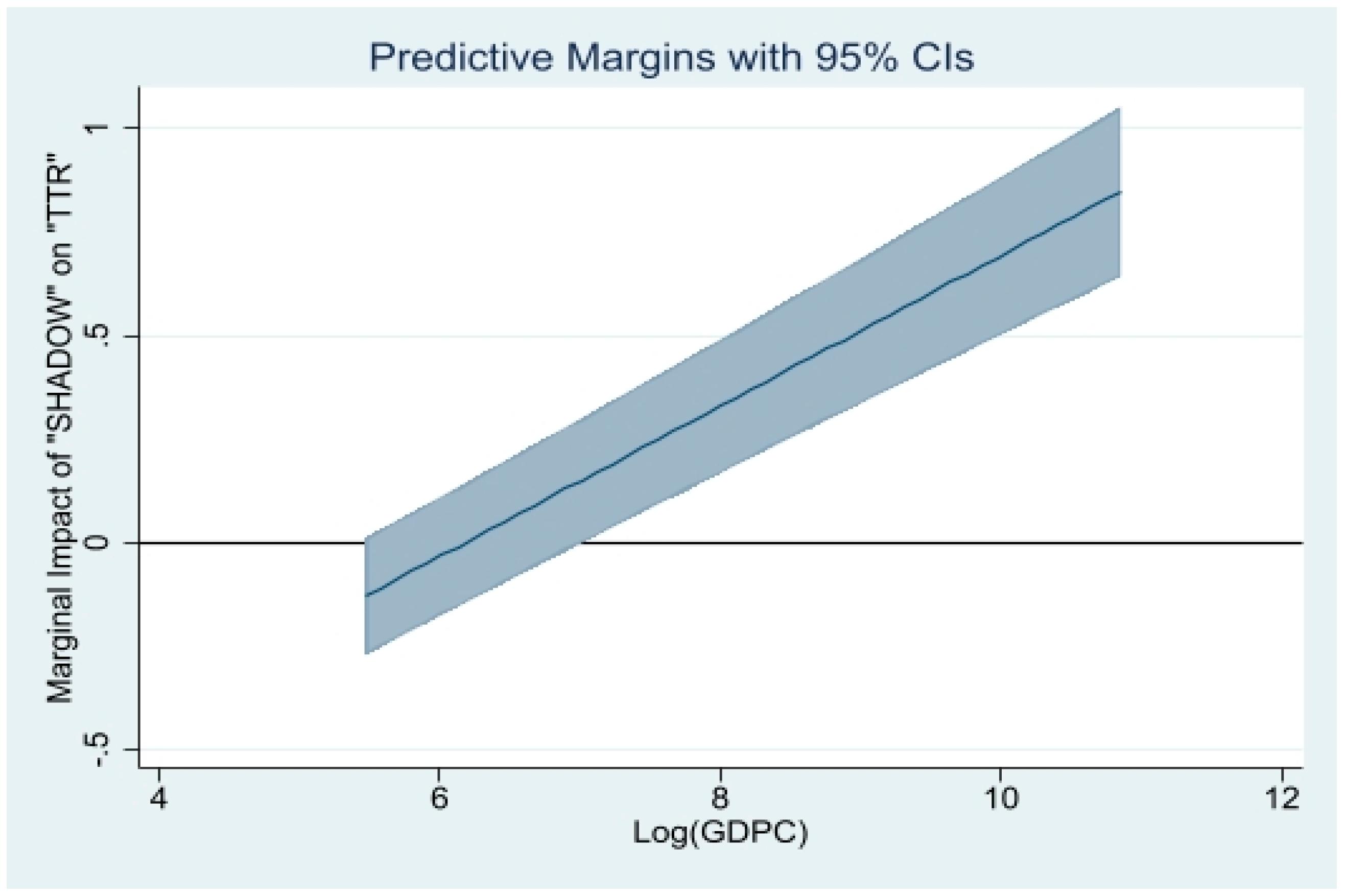

5. Further Analysis

6. Conclusions

Funding

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| All Countries | LICs | LICs | ||||

|---|---|---|---|---|---|---|

| Logit | Probit | Logit | Probit | Logit | Probit | |

| Variables | STR | STR | STR | STR | STR | STR |

| (1) | (2) | (3) | (4) | (5) | (6) | |

| SHADOWt−1 | −0.022 ** | −0.019 ** | −0.0399 *** | −0.036 *** | −0.0008 | 0.0008 |

| (0.009) | (0.009) | (0.0139) | (0.0135) | (0.0158) | (0.0154) | |

| Log(GDPC) | −1.149 *** | −0.744 ** | −0.085 | 0.674 | −4.16 *** | −3.248 *** |

| (0.321) | (0.307) | (0.514) | (0.503) | (0.564) | (0.528) | |

| OPENt−1 | −0.0022 | −0.0014 | 0.0018 | 0.0014 | −0.013 *** | −0.015 *** |

| (0.0013) | (0.0011) | (0.0012) | (0.0012) | (0.0035) | (0.003) | |

| RENTt−1 | −0.028 *** | −0.027 *** | −0.028 *** | −0.026 *** | −0.049 *** | −0.037 ** |

| (0.0066) | (0.0066) | (0.008) | (0.0078) | (0.017) | (0.016) | |

| URt−1 | 0.038 *** | 0.035 *** | −0.0036 | −0.013 | −0.020 | −0.028 * |

| (0.011) | (0.010) | (0.0309) | (0.0308) | (0.017) | (0.0152) | |

| GROWTHt−1 | −0.008 | −0.002 | −0.016 ** | −0.009 | 0.006 | 0.003 |

| (0.005) | (0.005) | (0.007) | (0.007) | (0.009) | (0.0096) | |

| INSTt−1 | −0.145 ** | −0.186 *** | −0.2588 *** | −0.374 *** | 0.169 | −0.0112 |

| (0.067) | (0.0652) | (0.085) | (0.084) | (0.110) | (0.1091) | |

| INFLt−1 | 0.0129 | −0.324 | −0.011 | −0.455 | 1.993 ** | 1.921 ** |

| (0.512) | (0.504) | (0.654) | (0.641) | (0.8198) | (0.783) | |

| Log(POP) | 6.300 *** | 5.213 *** | 7.807 *** | 7.733 *** | 4.027 *** | 4.435 *** |

| (0.576) | (0.524) | (1.177) | (1.161) | (1.165) | (1.058) | |

| Observations—Countries | 536-39 | 536-39 | 312-23 | 312-23 | 208-16 | 208-16 |

| Pseudo-R2 | 0.2359 | 0.2189 | 0.3211 | 0.3128 | 0.316 | 0.3060 |

| LR Chi2 (p-value) | 155.34 (0.0000) | 144.17 (0.0000) | 128.42 (0.0000) | 125.07 (0.0000) | 77.11 (0.0001) | 74.74 (0.0002) |

| Log likelihood | −251.594 | −257.18 | −135.739 | −137.415 | 83.589 | −84.774 |

| Full Sample | LICs | EMs | |

|---|---|---|---|

| Dependent Variable | STR | STR | STR |

| (1) | (2) | (3) | |

| SHADOW | −0.097 *** | −0.117 ** | −0.027 |

| (0.035) | (0.047) | (0.038) | |

| Log(GDPC) | −0.283 ** | −0.562 | −0.168 |

| (0.1405) | (0.348) | (0.375) | |

| GROWTHt−1 | −0.004 | −0.037 | −0.015 |

| (0.017) | (0.024) | (0.024) | |

| INFLt−1 | −0.483 | −0.159 | −2.112 |

| (1.200) | (1.723) | (1.850) | |

| OPENt−1 | 0.004 | 0.008 ** | −0.014 ** |

| (0.002) | (0.003) | (0.007) | |

| Log(POP) | −0.064 | −0.062 | −0.033 |

| (0.064) | (0.091) | (0.158) | |

| RENTt−1 | −0.0146 | −0.005 | −0.025 |

| (0.0106) | (0.011) | (0.023) | |

| INSTt−1 | −0.150 | −0.042 | −0.163 |

| (0.106) | (0.123) | (0.176) | |

| URt−1 | 0.028 | 0.034 | 0.0135 |

| (0.021) | (0.039) | (0.022) | |

| Constant | 5.576 ** | 8.0598 * | 3.315 |

| (2.596) | (4.258) | (6.795) | |

| Observations—Countries | 481-40 | 274-24 | 207-16 |

| First Stage Pseudo-R2 | 0.0240 | 0.045 | 0.056 |

| Log likelihood | −289.781 | −167.688 | −113.137 |

| Dependent Variable | SHADOW | SHADOW | SHADOW |

| (1) | (2) | (3) | |

| STR | −47.415 | −8.377 | 14.237 |

| (86.157) | (11.606) | (16.055) | |

| Observations—Countries | 481-40 | 274-24 | 207-16 |

| Adjusted R2 | 0.2403 | 0.3594 | 0.1801 |

| Dependent Variable | PIT | CIT | GST | VAT | EXCISE | TRTAX | PROPERTY | SUBSIDIES | REVADM |

|---|---|---|---|---|---|---|---|---|---|

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | (9) | |

| SHADOW | −0.097 ** | −0.062 * | −0.257 *** | −0.035 | −0.102 *** | −0.092 * | −0.263 *** | −0.1095 | −0.085 ** |

| (0.043) | (0.0355) | (0.069) | (0.035) | (0.0377) | (0.0486) | (0.098) | (0.1009) | (0.034) | |

| Log(GDPC) | −0.9266 *** | −0.053 | −2.090 *** | −0.575 *** | −0.445 *** | −0.176 | −1.439 *** | −1.652 *** | −0.462 *** |

| (0.2068) | (0.144) | (0.377) | (0.151) | (0.1535) | (0.198) | (0.444) | (0.6166) | (0.1416) | |

| GROWTHt−1 | −0.007 | −0.002 | −0.064 * | −0.008 | −0.023 | 0.0256 | −0.034 | 0.0265 | −0.004 |

| (0.022) | (0.018) | (0.033) | (0.017) | (0.019) | (0.023) | (0.047) | (0.0388) | (0.017) | |

| INFLt−1 | −0.340 | −2.430 | −1.08 | −1.022 | 0.878 | 0.775 | −5.252 | −3.27 | −0.257 |

| (1.716) | (1.525) | (2.691) | (1.364) | (1.248) | (1.74) | (4.355) | (4.767) | (1.206) | |

| OPENt−1 | 0.0097 *** | 0.007 *** | 0.017 *** | 0.0025 | 0.001 | −0.008 ** | −0.0088 | −0.043 ** | 0.0054 ** |

| (0.003) | (0.002) | (0.004) | (0.0024) | (0.002) | (0.00366) | (0.0096) | (0.0209) | (0.0023) | |

| Log(POP) | 0.013 | 0.063 | −0.688 *** | 0.046 | −0.108 | −0.317 *** | −0.018 | −0.876 *** | −0.0995 |

| (0.087) | (0.066) | (0.155) | (0.067) | (0.069) | (0.0906) | (0.169) | (0.310) | (0.0634) | |

| RENTt−1 | −0.041 ** | −0.027 ** | −0.051 ** | −0.021 | −0.024 * | −0.054 ** | −0.1103 | −0.015 | −0.012 |

| (0.0155) | (0.0114) | (0.024) | (0.011) | (0.012) | (0.0216) | (0.0536) | (0.043) | (0.010) | |

| INSTt−1 | 0.052 | −0.324 *** | 0.241 | 0.041 | −0.098 | −0.126 | 0.037 | 0.032 | −0.073 |

| (0.145) | (0.1196) | (0.19) | (0.111) | (0.115) | (0.134) | (0.265) | (0.2909) | (0.105) | |

| URt−1 | 0.091 *** | 0.0495 ** | 0.0674 * | 0.066 *** | 0.025 | −0.011 | 0.1315 ** | 0.283 *** | 0.032 |

| (0.027) | (0.0216) | (0.0406) | (0.021) | (0.023) | (0.029) | (0.0566) | (0.0756) | (0.020) | |

| Constant | 7.903 ** | −0.393 | 32.738 *** | 3.482 | 7.784 *** | 8.82 | 18.947 ** | 27.128 *** | 6.9045 *** |

| (3.273) | (2.578) | (6.385) | (2.576) | (2.834) | (3.818) | (7.549) | (9.138) | (2.569) | |

| Observations—Countries | 481-40 | 481-40 | 481-40 | 481-40 | 481-40 | 481-40 | 481-40 | 481-40 | 481-40 |

| First Stage Pseudo-R2 | 0.1059 | 0.055 | 0.3266 | 0.0606 | 0.0338 | 0.1028 | 0.3064 | 0.471 | 0.0338 |

| Log likelihood | −154.713 | −195.108 | −92.769 | −209.270 | −252.224 | −129.961 | −53.265 | −31.591 | −278.549 |

| Dependent Variable | SHADOW | SHADOW | SHADOW | SHADOW | SHADOW | SHADOW | SHADOW | SHADOW | SHADOW |

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | (9) | |

| Indicator of the type (area) of structural tax reform | 1.753 | −0.179 | 2.798 *** | 3.807 * | 26.826 | 4.142 *** | 0.797 | 1.343 ** | 14.562 |

| (1.484) | (1.447) | (0.946) | (3.416) | (31.182) | (1.4099) | (0.627) | (0.584) | (32.248) | |

| Observations—Countries | 481-40 | 481-40 | 481-40 | 481-40 | 481-40 | 481-40 | 481-40 | 481-40 | 481-40 |

| Adjusted R2 | 0.2011 | 0.1984 | 0.2350 | 0.2021 | 0.2405 | 0.2526 | 0.203 | 0.2267 | 0.2014 |

| Variables | TTR | TTR | TTR | TTR | TTR |

|---|---|---|---|---|---|

| (1) | (2) | (3) | (4) | (5) | |

| SHADOW | 0.241 *** | 0.386 *** | 0.415 *** | −1.124 *** | 0.0221 |

| (0.0870) | (0.111) | (0.0976) | (0.0937) | (0.118) | |

| SHADOW*SHTRTAX | −0.570 *** | ||||

| (0.141) | |||||

| SHADOW*LICs | −0.374 *** | ||||

| (0.0442) | |||||

| SHADOW*Log(GDP) | 0.182 *** | ||||

| (0.0126) | |||||

| SHADOW*OPEN | 0.403 *** | ||||

| (0.119) | |||||

| SHTRTAX | −0.0597 *** | 0.111 *** | −0.0595 *** | −0.0517 *** | −0.0504 *** |

| (0.0139) | (0.0373) | (0.0139) | (0.0139) | (0.0140) | |

| Log(GDPC) | 0.0962 *** | 0.103 *** | 0.104 *** | 0.0422 *** | 0.115 *** |

| (0.0130) | (0.0148) | (0.0142) | (0.0133) | (0.0108) | |

| OPEN | 0.0380 *** | 0.0412 *** | 0.0400 *** | 0.0515 *** | −0.0794 *** |

| (0.00668) | (0.00702) | (0.00666) | (0.00894) | (0.0284) | |

| RENT | −0.293 *** | −0.293 *** | −0.276 *** | −0.287 *** | −0.301 *** |

| (0.0562) | (0.0628) | (0.0590) | (0.0540) | (0.0491) | |

| UR | 0.241 *** | 0.225 *** | 0.155 *** | 0.0616 * | 0.140 *** |

| (0.0473) | (0.0471) | (0.0488) | (0.0333) | (0.0374) | |

| GROWTH | 0.160 *** | 0.147 *** | 0.144 *** | 0.120 *** | 0.124 *** |

| (0.0262) | (0.0167) | (0.0257) | (0.0279) | (0.0288) | |

| INST | 0.0229 *** | 0.0227 *** | 0.0211 *** | 0.0201 *** | 0.0213 *** |

| (0.00443) | (0.00465) | (0.00431) | (0.00376) | (0.00426) | |

| INFL | −0.0372 * | −0.0374 ** | −0.0445 ** | −0.0417 ** | −0.0388 * |

| (0.0207) | (0.0184) | (0.0203) | (0.0192) | (0.0202) | |

| Log(POP) | 0.207 *** | 0.192 *** | 0.186 *** | 0.186 *** | 0.199 *** |

| (0.0211) | (0.0200) | (0.0175) | (0.0174) | (0.0195) | |

| Constant | −3.576 *** | −3.441 *** | −3.305 *** | −2.828 *** | −3.525 *** |

| (0.426) | (0.412) | (0.375) | (0.369) | (0.407) | |

| Observations—Countries | 666-114 | 666-114 | 666-114 | 666-114 | 666-114 |

| Within R-squared | 0.3741 | 0.3841 | 0.3841 | 0.3975 | 0.4008 |

| Variables | Location a | Scale b | Q10th | Q20th | Q30th | Q40th | Q50th | Q60th | Q70th | Q80th | Q90th |

|---|---|---|---|---|---|---|---|---|---|---|---|

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | (9) | (10) | (11) | |

| SHADOW | 0.265 *** | −0.0610 | 0.356 *** | 0.333 *** | 0.313 *** | 0.289 *** | 0.262 *** | 0.236 ** | 0.215 ** | 0.195 * | 0.163 |

| (0.0953) | (0.0451) | (0.116) | (0.106) | (0.101) | (0.0967) | (0.0955) | (0.0983) | (0.103) | (0.110) | (0.123) | |

| SHTRTAX | −0.0668 ** | 0.0286 ** | −0.110 *** | −0.0989 *** | −0.0891 *** | −0.0783 *** | −0.0656 ** | −0.0533 * | −0.0436 | −0.0341 | −0.0188 |

| (0.0275) | (0.0143) | (0.0347) | (0.0316) | (0.0295) | (0.0281) | (0.0276) | (0.0284) | (0.0299) | (0.0320) | (0.0365) | |

| Log(GDPC) | 0.152 *** | −0.00427 | 0.158 *** | 0.157 *** | 0.155 *** | 0.154 *** | 0.152 *** | 0.150 *** | 0.148 *** | 0.147 *** | 0.145 *** |

| (0.0329) | (0.0185) | (0.0524) | (0.0466) | (0.0418) | (0.0371) | (0.0325) | (0.0297) | (0.0288) | (0.0292) | (0.0325) | |

| OPEN | 0.0517 *** | 0.00945 | 0.0375 ** | 0.0411 *** | 0.0443 *** | 0.0479 *** | 0.0521 *** | 0.0561 *** | 0.0593 *** | 0.0625 *** | 0.0675 *** |

| (0.0127) | (0.00615) | (0.0155) | (0.0143) | (0.0135) | (0.0129) | (0.0128) | (0.0131) | (0.0138) | (0.0147) | (0.0166) | |

| RENT | −0.308 *** | −0.0196 | −0.279 *** | −0.286 *** | −0.293 *** | −0.301 *** | −0.309 *** | −0.318 *** | −0.324 *** | −0.331 *** | −0.341 ** |

| (0.0958) | (0.0480) | (0.103) | (0.0965) | (0.0931) | (0.0925) | (0.0965) | (0.104) | (0.113) | (0.123) | (0.141) | |

| UR | 0.203 * | 0.0472 | 0.133 | 0.150 | 0.167 | 0.184 | 0.205 * | 0.226 ** | 0.242 ** | 0.257 ** | 0.282 ** |

| (0.109) | (0.0491) | (0.139) | (0.128) | (0.120) | (0.113) | (0.108) | (0.108) | (0.110) | (0.115) | (0.127) | |

| GROWTH | 0.132 | −0.0140 | 0.153 | 0.148 | 0.143 | 0.138 | 0.132 | 0.126 | 0.121 | 0.116 | 0.109 |

| (0.0843) | (0.0461) | (0.123) | (0.110) | (0.100) | (0.0912) | (0.0838) | (0.0812) | (0.0824) | (0.0862) | (0.0974) | |

| INST | 0.0137 ** | −0.00375 | 0.0193 ** | 0.0179 ** | 0.0166 ** | 0.0152 ** | 0.0136 * | 0.0119 * | 0.0107 | 0.00943 | 0.00742 |

| (0.00699) | (0.00323) | (0.00927) | (0.00852) | (0.00791) | (0.00738) | (0.00698) | (0.00686) | (0.00695) | (0.00723) | (0.00799) | |

| INFL | −0.0709 ** | 0.0289 ** | −0.114 *** | −0.103 *** | −0.0935 *** | −0.0826 ** | −0.0697 ** | −0.0573 | −0.0475 | −0.0380 | −0.0225 |

| (0.0340) | (0.0128) | (0.0358) | (0.0342) | (0.0335) | (0.0336) | (0.0343) | (0.0358) | (0.0375) | (0.0397) | (0.0433) | |

| Log(POP) | 0.298 *** | 0.0153 | 0.275 *** | 0.281 *** | 0.286 *** | 0.292 *** | 0.299 *** | 0.305 *** | 0.310 *** | 0.315 *** | 0.324 *** |

| (0.0416) | (0.0207) | (0.0573) | (0.0522) | (0.0480) | (0.0443) | (0.0415) | (0.0405) | (0.0412) | (0.0430) | (0.0478) | |

| Constant | −5.486 *** | −0.177 | −5.221 *** | −5.287 *** | −5.348 *** | −5.414 *** | −5.493 *** | −5.569 *** | −5.629 *** | −5.687 *** | −5.781 *** |

| (0.883) | (0.461) | (1.280) | (1.156) | (1.054) | (0.959) | (0.878) | (0.841) | (0.844) | (0.875) | (0.974) | |

| Observations—Countries | 666-114 | 666-114 | 666-114 | 666-114 | 666-114 | 666-114 | 666-114 | 666-114 | 666-114 | 666-114 | 666-114 |

| Effect of the Shadow Economy on Tax Transition Reform Conditioned on the Share of Trade Tax Revenue in Non-Resource Tax Revenue | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| Variables | Location a | Scale b | Q10th | Q20th | Q30th | Q40th | Q50th | Q60th | Q70th | Q80th | Q90th |

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | (9) | (10) | (11) | |

| SHADOW*SHTRTAX | −0.535 *** | 0.0500 | −0.609 ** | −0.591 ** | −0.574 *** | −0.555 *** | −0.532 *** | −0.510 *** | −0.494 *** | −0.477 *** | −0.450 ** |

| (0.177) | (0.102) | (0.269) | (0.242) | (0.217) | (0.194) | (0.175) | (0.166) | (0.167) | (0.175) | (0.199) | |

| SHADOW | 0.405 *** | −0.0988 * | 0.552 *** | 0.517 *** | 0.482 *** | 0.444 *** | 0.400 *** | 0.356 *** | 0.325 *** | 0.291 ** | 0.238 * |

| (0.115) | (0.0592) | (0.161) | (0.146) | (0.134) | (0.123) | (0.114) | (0.111) | (0.113) | (0.118) | (0.131) | |

| SHTRTAX | 0.0931 ** | −0.00291 | 0.0974 | 0.0964 | 0.0954 * | 0.0943 * | 0.0929 ** | 0.0917 ** | 0.0908 ** | 0.0897 ** | 0.0882 * |

| (0.0457) | (0.0262) | (0.0710) | (0.0639) | (0.0571) | (0.0508) | (0.0451) | (0.0420) | (0.0417) | (0.0432) | (0.0488) | |

| Turning point of “SHTRTAX” | 0.906 (=0.552/0.609) | 0.875 (=0.517/0.591) | 0.85 (=0.482/0.574) | 0.8 (=0.444/0.555) | 0.752 (=0.400/0.532) | 0.698 (=0.356/0.510) | 0.658 (=0.325/0.494) | 0.61 (=0.291/0.477) | 0.529 (=0.238/0.450) | ||

| Effect of the Shadow Economy on Tax Transition Reform Conditioned on the Real per Capita Income | |||||||||||

| Variables | Location a | Scale b | Q10th | Q20th | Q30th | Q40th | Q50th | Q60th | Q70th | Q80th | Q90th |

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | (9) | (10) | (11) | |

| SHADOW*Log(GDP) | 0.146 *** | −0.00657 | 0.156 *** | 0.153 *** | 0.151 *** | 0.149 *** | 0.146 *** | 0.143 *** | 0.140 *** | 0.138 *** | 0.135 ** |

| (0.0472) | (0.0192) | (0.0573) | (0.0535) | (0.0506) | (0.0485) | (0.0472) | (0.0475) | (0.0487) | (0.0507) | (0.0549) | |

| SHADOW | −0.829 ** | −0.0513 | −0.752 * | −0.771 * | −0.790 ** | −0.808 ** | −0.832 ** | −0.854 ** | −0.872 ** | −0.889 ** | −0.914 ** |

| (0.359) | (0.150) | (0.427) | (0.400) | (0.379) | (0.365) | (0.359) | (0.365) | (0.379) | (0.397) | (0.434) | |

| Log(GDPC) | 0.0908 *** | −0.00843 | 0.104 ** | 0.100 ** | 0.0973 ** | 0.0943 ** | 0.0904 *** | 0.0867 *** | 0.0837 ** | 0.0810 ** | 0.0768 ** |

| (0.0349) | (0.0183) | (0.0513) | (0.0462) | (0.0418) | (0.0381) | (0.0346) | (0.0331) | (0.0331) | (0.0342) | (0.0377) | |

| Effect of the Shadow Economy on Tax Transition Reform Conditioned on the Level of Trade Openness | |||||||||||

| Variables | Location a | Scale b | Q10th | Q20th | Q30th | Q40th | Q50th | Q60th | Q70th | Q80th | Q90th |

| (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | (9) | (10) | (11) | |

| SHADOW*OPEN | 0.388 *** | 0.0574 | 0.298 * | 0.325 ** | 0.343 ** | 0.363 *** | 0.386 *** | 0.416 *** | 0.434 *** | 0.452 *** | 0.485 *** |

| (0.110) | (0.0525) | (0.173) | (0.152) | (0.138) | (0.125) | (0.111) | (0.0959) | (0.0897) | (0.0868) | (0.0890) | |

| SHADOW | 0.0589 | −0.109 * | 0.229 | 0.179 | 0.144 | 0.107 | 0.0624 | 0.00607 | −0.0290 | −0.0621 | −0.125 |

| (0.121) | (0.0584) | (0.173) | (0.153) | (0.142) | (0.132) | (0.122) | (0.117) | (0.116) | (0.120) | (0.131) | |

| OPEN | −0.0635 | −0.00962 | −0.0484 | −0.0529 | −0.0559 | −0.0592 | −0.0632 | −0.0681 ** | −0.0712 ** | −0.0741 ** | −0.0797 ** |

| (0.0396) | (0.0187) | (0.0622) | (0.0549) | (0.0500) | (0.0452) | (0.0400) | (0.0347) | (0.0325) | (0.0313) | (0.0319) | |

| Variables | TTR | TTR | TTR | TTR | TTR |

|---|---|---|---|---|---|

| (1) | (2) | (3) | (4) | (5) | |

| TTRt−1 | 0.495 *** | 0.520 *** | 0.522 *** | 0.458 *** | 0.499 *** |

| (0.0143) | (0.0137) | (0.0119) | (0.0188) | (0.0116) | |

| SHADOW | 0.0723 ** | 0.123 *** | 0.192 *** | −1.632 *** | −0.139 *** |

| (0.0301) | (0.0357) | (0.0342) | (0.176) | (0.0203) | |

| SHADOW*SHTRTAX | −0.567 *** | ||||

| (0.129) | |||||

| SHADOW*LICs | −0.202 *** | ||||

| (0.0394) | |||||

| SHADOW*Log(GDP) | 0.221 *** | ||||

| (0.0237) | |||||

| SHADOW*OPEN | 0.242 *** | ||||

| (0.0114) | |||||

| LICs | 0.0762 *** | ||||

| (0.0214) | |||||

| SHTRTAX | −0.159 *** | −0.0165 | −0.133 *** | −0.163 *** | −0.160 *** |

| (0.0180) | (0.0512) | (0.0141) | (0.0222) | (0.0164) | |

| Log(GDPC) | −0.0171 *** | −0.0170 *** | −0.00111 | −0.0883 *** | −0.0165 *** |

| (0.00410) | (0.00232) | (0.00465) | (0.00811) | (0.00238) | |

| OPEN | 0.0187 *** | 0.0189 *** | 0.0151 *** | 0.0368 *** | −0.0467 *** |

| (0.00552) | (0.00452) | (0.00480) | (0.00528) | (0.00306) | |

| RENT | −0.297 *** | −0.279 *** | −0.293 *** | −0.288 *** | −0.288 *** |

| (0.0224) | (0.0174) | (0.0161) | (0.0214) | (0.0129) | |

| UR | 0.0586 | 0.0238 | −0.00910 | 0.0559 | −0.00349 |

| (0.0485) | (0.0392) | (0.0444) | (0.0506) | (0.0437) | |

| GROWTH | 0.515 *** | 0.514 *** | 0.504 *** | 0.425 *** | 0.454 *** |

| (0.0393) | (0.0280) | (0.0375) | (0.0377) | (0.0275) | |

| INST | 0.0191 *** | 0.0179 *** | 0.0188 *** | 0.0256 *** | 0.0239 *** |

| (0.00314) | (0.00233) | (0.00162) | (0.00341) | (0.00186) | |

| INFL | 0.0191 | 0.0312 *** | 0.00267 | 0.0469 *** | 0.00553 |

| (0.0158) | (0.0112) | (0.0107) | (0.0147) | (0.0103) | |

| Log(POP) | 0.00578 ** | 0.00511 *** | 0.00436 * | 0.00690 ** | 0.00517 ** |

| (0.00278) | (0.00166) | (0.00234) | (0.00288) | (0.00212) | |

| Observations—Countries | 555-114 | 555-114 | 555-114 | 555-114 | 555-114 |

| AR1 (p-value) | 0.0270 | 0.0269 | 0.0263 | 0.0327 | 0.0283 |

| AR2 (p-value) | 0.1207 | 0.1094 | 0.10 | 0.10 | 0.1087 |

| OID (p-value) | 0.3849 | 0.5027 | 0.4040 | 0.4127 | 0.3012 |

Appendix A.1. Definition and Source of Variables

| Variables | Definition | Source |

| STR | This is the first indicator of revenue-enhancing structural tax reform. It identifies the episodes of large tax revenue mobilization identified over the period from 2000 to 2015 (see Akitoby et al. 2020). The variable “STR” takes the value of 1 for a year characterized by a large revenue mobilization and the value of 0 for other years. The different areas of tax policy and revenue administration where major reforms took place are as follows: Personal Income Tax (“PIT”); Corporate Income Tax (“CIT”); Goods and Services Tax (“GST”); Value Added Tax (“VAT”); Excise Tax (“EXCISE”); Trade Tax (“TRTAX”); Property Tax (“PROPERTY”); Subsidies (“SUBSIDIES”); and Revenue Administration (“REVADM”). | Data extracted from Akitoby et al. (2020) |

| TTR | This is the second indicator of tax reform, referred to as ‘tax transition reform’. It reflects the extent of the reform of the tax revenue structure towards a lower dependence of the non-resource tax revenue on international trade tax revenue (and hence in favor of a greater dependence of the non-resource tax revenue on domestic tax revenue). Practically, it captures the convergence of the tax revenue structure of a given developing country towards the developed countries’ tax revenue structure. Its values range between 0 and 100, with higher values reflecting greater tax revenue structure convergence, i.e., greater tax reforms. | Author’s computation (see Section 3.2.1) based on data extracted from the ‘UNU-WIDER Government Revenue Dataset’. Version 2021. https://www.wider.unu.edu/project/grd-%E2%80%93-government-revenue-dataset (Accessed in 20 June 2021). |

| SHADOW | This is the measure of the share of the size of the shadow economy in the official GDP. It has been computed by Medina and Schneider (2018) using the multiple indicators, multiple causes (MIMIC) method. The latter extracts covariance information from observable variables classified as causes or indicators of the latent shadow economy (see Schneider et al. 2010 for more details on this approach). | Data extracted from Medina and Schneider (2018) |

| SHTRTAX | This is the share of international trade tax revenue in total non-resource tax revenue. Non-resource tax revenue is the difference between total tax revenue (as a share of GDP, excluding social contributions) and tax revenue collected on natural resources (the latter includes a significant component of economic rent, primarily from oil and mining activities) as a share of GDP. | Author’s calculation based on data extracted from the UNU-WIDER Government Revenue Dataset’. Version 2021. https://www.wider.unu.edu/project/grd-%E2%80%93-government-revenue-dataset (Accessed in 20 June 2021). |

| GDPC | Real per capita Gross Domestic Product (constant 2015 USD). | World Development Indicators (WDIs) of the World Bank |

| GROWTH | Real Growth Rate of the Gross Domestic Product, annual change (constant 2015 USD). | WDI |

| OPEN | This is the indicator of trade openness, measured by the share (in percentage) of the sum of exports and imports of GDP. | WDI |

| INFL | The variable “INFL” has been calculated using the following formula: INFL (2), where refers to the absolute value of the annual inflation rate (not in percentage), denoted “INFLATION”. The inflation rate is based on Consumer Price Index (CPI), where missing values have been replaced with values of the GDP Deflator. | Authors’ calculation based on data from the WDI. |

| EDU | This is the average of the gross primary school enrollment (in percentage), gross secondary school enrollment (in percentage), and gross tertiary school enrollment (in percentage). | Author’s calculation based on data collected from the WDI. |

| RENT | This is the share of total natural resource rents in GDP. | WDI |

| UR | Rate of total unemployment (i.e., for both male and female) as a share of total labor force. | WDI |

| POP | Total Population | WDI |

| INST | This is the variable capturing the institutional quality. It has been computed by extracting the first principal component (based on factor analysis) of the following six indicators of governance: political stability and absence of violence/terrorism; regulatory quality; rule of law; government effectiveness; voice and accountability; and corruption. Higher values of the index “INST” are associated with better governance and institutional quality, while lower values reflect worse governance and institutional quality. | Data on the components of “INST” variables have been extracted from World Bank Governance Indicators developed by Kaufmann et al. (2010) and updated recently. See online at: https://info.worldbank.org/governance/wgi/ (Accessed in 20 June 2022). |

Appendix A.2. Descriptive Statistics on Variables Used in the Analysis over the Full Sample

| Variable | Observations | Mean | Standard Deviation | Minimum | Maximum |

| STR | 481 | 0.308 | 0.462 | 0 | 1 |

| PIT | 481 | 0.116 | 0.321 | 0 | 1 |

| CIT | 481 | 0.154 | 0.361 | 0 | 1 |

| GST | 481 | 0.083 | 0.276 | 0 | 1 |

| VAT | 481 | 0.175 | 0.380 | 0 | 1 |

| EXCISE | 481 | 0.233 | 0.423 | 0 | 1 |

| TRTAX | 481 | 0.089 | 0.286 | 0 | 1 |

| PROPERTY | 481 | 0.037 | 0.190 | 0 | 1 |

| SUBSIDIES | 481 | 0.027 | 0.162 | 0 | 1 |

| REVADM | 481 | 0.287 | 0.453 | 0 | 1 |

| SHADOW | 481 | 36.104 | 7.869 | 20.380 | 68.460 |

| GROWTH | 481 | 4.320 | 4.360 | −36.392 | 20.716 |

| UR | 481 | 7.782 | 5.388 | 0.390 | 28.640 |

| GDPC | 481 | 3453.151 | 5453.988 | 295.737 | 35,852.240 |

| INFLATION | 481 | 0.064 | 0.067 | −0.043 | 0.738 |

| EDU | 460 | 55.715 | 20.661 | 1.612 | 94.347 |

| OPEN | 480 | 77.687 | 33.455 | 20.964 | 311.354 |

| INST | 444 | −1.100 | 1.336 | −3.750 | 2.989 |

| POP | 481 | 14,100,000 | 20,400,000 | 255,068 | 102,000,000 |

| RENT | 481 | 7.674 | 10.221 | 0.006 | 58.650 |

Appendix A.2.1. Pairwise Correlation Statistics on Variables Used in the Analysis over the Full Sample of 40 LICs and Ems

| STR | PIT | PIT | GST | VAT | EXCISE | TRTAX | PROPERTY | SUBSIDIES | REVADM | |

| STR | 1.0000 | |||||||||

| PIT | 0.5445 * | 1.0000 | ||||||||

| CIT | 0.6396 * | 0.5638 * | 1.0000 | |||||||

| GST | 0.4518 * | 0.3837 * | 0.4142 * | 1.0000 | ||||||

| VAT | 0.6900 * | 0.6184 * | 0.5324 * | 0.4168 * | 1.0000 | |||||

| EXCISE | 0.8264 * | 0.4902 * | 0.5149 * | 0.4576 * | 0.5758 * | 1.0000 | ||||

| TRTAX | 0.4700 * | 0.2043 * | 0.1087 * | 0.3806 * | 0.3549 * | 0.4825 * | 1.0000 | |||

| PROPERTY | 0.2958 * | 0.2017 * | 0.1284 * | 0.1390 * | 0.4286 * | 0.3579 * | 0.1302 * | 1.0000 | ||

| SUBSIDIES | 0.2500 * | 0.1394 * | 0.1777 * | 0.2748 * | 0.2948 * | 0.2115 * | 0.1725 * | −0.0329 | 1.0000 | |

| REVADM | 0.9514 * | 0.5723 * | 0.6085 * | 0.4748 * | 0.7252 * | 0.8142 * | 0.4134 * | 0.3109 * | 0.2628 * | 1.0000 |

| SHADOW | −0.0323 | 0.1021 * | 0.0009 | −0.0080 | 0.0500 | 0.0398 | 0.0204 | −0.0106 | 0.0346 | 0.0066 |

| GROWTH | 0.0869 * | 0.0309 | 0.0170 | −0.0007 | 0.0290 | 0.0398 | 0.0675 | 0.0090 | −0.0555 | 0.0774 * |

| UR | −0.0669 | 0.0565 | 0.0455 | −0.0326 | 0.0520 | −0.0969 * | −0.0476 | −0.0193 | 0.0788 * | −0.0583 |

| GDPC | −0.0840 * | −0.0947 * | −0.0600 | −0.0817 * | −0.0995 * | −0.0787 * | 0.0079 | −0.0216 | −0.0613 | −0.1197 * |

| INFLATION | −0.0411 | −0.0184 | −0.0400 | −0.0676 | −0.0488 | −0.0098 | −0.0071 | −0.0932 * | −0.0345 | −0.0374 |

| EDU | −0.0466 | −0.0478 | −0.0026 | −0.1790 * | 0.0160 | −0.0884 * | −0.0005 | −0.0392 | −0.1330 * | −0.0797 * |

| OPEN | 0.0559 | 0.0641 | 0.1113 * | 0.1057 * | −0.0214 | −0.0363 | −0.0862 * | −0.1194 * | −0.1223 * | 0.0875 * |

| INST | −0.0525 | 0.0317 | −0.0471 | 0.0569 | −0.0012 | −0.0382 | 0.0766 | 0.0373 | −0.0452 | −0.0617 |

| POP | 0.0421 | −0.0763 * | 0.0761 * | −0.1362 * | −0.0483 | 0.0490 | −0.0081 | 0.0120 | −0.0964 * | −0.0259 |

| RENT | 0.0554 | −0.0661 | 0.0049 | 0.0076 | −0.0629 | −0.0085 | −0.0871 * | −0.0570 | −0.0399 | 0.0597 |

| Note: * p-value < 0.1. | ||||||||||

Appendix A.2.2. (Continued): Pairwise Correlation Statistics on Variables Used in the Analysis over the Full Sample of 40 LICs and EMs

| SHADOW | GROWTH | UR | GDPC | INFLATION | EDU | OPEN | INST | POP | RENT | |

| SHADOW | 1.0000 | |||||||||

| GROWTH | −0.0616 | 1.0000 | ||||||||

| UR | 0.0592 | −0.1413 * | 1.0000 | |||||||

| GDPC | −0.1950 * | −0.1570 * | 0.2600 * | 1.0000 | ||||||

| INFLATION | 0.0659 | −0.1049 * | −0.1367 * | −0.0867 * | 1.0000 | |||||

| EDU | −0.0296 | 0.0223 | 0.1369 * | 0.2237 * | 0.0071 | 1.0000 | ||||

| OPEN | 0.0278 | 0.0480 | 0.2635 * | 0.0584 | −0.0350 | 0.2392 * | 1.0000 | |||

| INST | −0.1968 * | −0.0366 | 0.4596 * | 0.6609 * | −0.1875 * | 0.3124 * | 0.1120 * | 1.0000 | ||

| POP | −0.1467 * | 0.0610 | −0.1418 * | −0.0357 | 0.0747 | 0.1044 * | −0.1956 * | −0.0459 | 1.0000 | |

| RENT | −0.0512 | 0.0078 | −0.0397 | −0.2065 * | 0.0372 | −0.2887 * | 0.0837 * | −0.5100 * | −0.0748 | 1.0000 |

| Note: * p-value < 0.1. The variables “SHADOW”, “OPEN”, “UR”, “GROWTH”, and “RENT” are expressed in percentage. | ||||||||||

Appendix A.3. List of the 40 Developing Countries Contained in the Full Sample, including Low-Income Countries (LICs) and Emerging Markets (EMs)

| Full Sample (40 Developing Countries) | LICs | EMs | |

| Algeria | Mauritania | Burkina Faso | Algeria |

| Armenia | Moldova | Burundi | Armenia |

| Bahamas, The | Morocco | Cabo Verde | Bahamas, The |

| Belize | Namibia | Cambodia | Belize |

| Bosnia and Herzegovina | Nepal | Central African Republic | Bosnia and Herzegovina |

| Bulgaria | Nicaragua | Comoros | Bulgaria |

| Burkina Faso | Paraguay | Congo, Rep. | Ecuador |

| Burundi | Philippines | Gambia, The | Georgia |

| Cabo Verde | Rwanda | Guinea | Jamaica |

| Cambodia | Senegal | Guinea-Bissau | Morocco |

| Central African Republic | Sierra Leone | Guyana | Namibia |

| Comoros | Solomon Islands | Kyrgyz Republic | Paraguay |

| Congo, Rep. | Turkey | Lao PDR | Philippines |

| Ecuador | Uganda | Liberia | Turkey |

| Gambia, The | Ukraine | Maldives | Ukraine |

| Georgia | Uruguay | Mauritania | Uruguay |

| Guinea | Moldova | ||

| Guinea-Bissau | Nepal | ||

| Guyana | Nicaragua | ||

| Jamaica | Rwanda | ||

| Kyrgyz Republic | Senegal | ||

| Lao PDR | Sierra Leone | ||

| Liberia | Solomon Islands | ||

| Maldives | Uganda | ||

Appendix A.4. Descriptive Statistics on Variables Used in the Analysis Covering the Full Sample of 114 Developing Countries

| Variable | Observations | Mean | Standard Deviation | Minimum | Maximum |

| TTR | 666 | 0.595 | 0.183 | 0.054 | 0.971 |

| SHADOW | 666 | 0.344 | 0.116 | 0.098 | 0.709 |

| SHTRTAX | 666 | 0.191 | 0.189 | 0 | 1 |

| UR | 666 | 0.079 | 0.059 | 0.005 | 0.321 |

| GDPC | 666 | 6523.865 | 9088.266 | 237.276 | 57,723.070 |

| INFLATION | 666 | 0.106 | 0.290 | −0.069 | 4.140 |

| RENT | 666 | 0.075 | 0.108 | 0.000 | 0.620 |

| OPEN | 666 | 0.877 | 0.561 | 0.003 | 4.193 |

| GROWTH | 666 | 0.043 | 0.034 | −0.084 | 0.220 |

| INST | 666 | −0.572 | 1.766 | −4.892 | 3.955 |

| POP | 666 | 44,900,000 | 170,000,000 | 214,065.700 | 1,360,000,000 |

| Note: The variables “SHADOW”, “SHRTAX”, “OPEN”, “UR”, “GROWTH”, and “RENT” are not expressed in percentage for the sake of the analysis. | |||||

Appendix A.4.1. Correlation Statistics on Variables Used in the Analysis over the Full Sample

| TTR | SHADOW | SHTRTAX | UR | GDPC | INFLATION | RENT | OPEN | GROWTH | INST | POP | |

| TTR | 1.0000 | ||||||||||

| SHADOW | −0.2227 * | 1.0000 | |||||||||

| SHTRTAX | −0.6623 * | 0.1204 * | 1.0000 | ||||||||

| UR | 0.2538 * | −0.0932 * | −0.0636 | 1.0000 | |||||||

| GDPC | 0.0201 | −0.4960 * | 0.0847 * | −0.0112 | 1.0000 | ||||||

| INFLATION | −0.1212 * | 0.1288 * | 0.0006 | −0.0465 | −0.1154 * | 1.0000 | |||||

| RENT | −0.5589 * | 0.0622 | 0.3595 * | −0.0192 | 0.0239 | 0.1067 * | 1.0000 | ||||

| OPEN | 0.2059 * | −0.3237 * | −0.1299 * | 0.0503 | 0.5067 * | −0.0793 * | −0.0586 | 1.0000 | |||

| GROWTH | −0.0674 * | −0.0272 | −0.0157 | −0.0912 * | −0.0846 * | −0.1384 * | 0.0960 * | 0.0139 | 1.0000 | ||

| INST | 0.4808 * | −0.5667 * | −0.2017 * | 0.1975 * | 0.6540 * | −0.2006 * | −0.3995 * | 0.4817 * | −0.0736 * | 1.0000 | |

| POP | 0.0596 | −0.1825 * | −0.0478 | −0.1027 * | −0.0849 * | −0.0129 | −0.0574 | −0.1723 * | 0.1536 * | −0.0614 | 1.0000 |

| Note: * p-value < 0.1. The variables “SHADOW”, “SHRTAX”, “OPEN”, “UR”, “GROWTH”, and “RENT” are not expressed in percentage for the sake of the analysis. | |||||||||||

Appendix A.5. List of the 114 Developing Countries, including 44 LICs in the Full Sample

| Full Sample (114 Developing Countries) | ||

| Albania | Ethiopia ** | Mexico |

| Algeria | Fiji | Moldova ** |

| Angola | Gabon | Mongolia |

| Argentina | Gambia, The ** | Morocco |

| Armenia | Georgia | Mozambique ** |

| Azerbaijan | Ghana ** | Myanmar ** |

| Bahamas, The | Guatemala | Namibia |

| Bahrain | Guinea ** | Nepal ** |

| Bangladesh ** | Guinea-Bissau ** | Nicaragua ** |

| Belarus | Guyana | Niger ** |

| Belize | Haiti ** | Nigeria |

| Benin ** | Honduras ** | Pakistan |

| Bhutan ** | Hong Kong SAR, China | Papua New Guinea ** |

| Bosnia and Herzegovina | Hungary | Paraguay |

| Botswana | India | Philippines |

| Brazil | Indonesia | Poland |

| Brunei Darussalam | Iran, Islamic Rep. | Romania |

| Bulgaria | Israel | Rwanda ** |

| Burkina Faso ** | Jamaica | Saudi Arabia |

| Burundi ** | Jordan | Sierra Leone ** |

| Cabo Verde ** | Kazakhstan | Singapore |

| Cambodia ** | Kenya ** | Slovak Republic |

| Central African Republic ** | Korea Republic ** | Slovenia |

| Chad ** | Kuwait | Solomon Islands ** |

| Chile | Kyrgyz Republic | South Africa |

| China | Lao PDR ** | Sri Lanka |

| Comoros ** | Latvia | Suriname |

| Democratic Republic Congo ** | Lebanon | Tajikistan ** |

| Congo Republic ** | Lesotho ** | Tanzania ** |

| Cote d’Ivoire ** | Liberia ** | Thailand |

| Cyprus | Libya | Tunisia |

| Czech Republic | Lithuania | Turkey |

| Dominican Republic | Madagascar ** | Uganda ** |

| Ecuador | Malaysia ** | Ukraine |

| El Salvador | Maldives | United Arab Emirates |

| Equatorial Guinea | Malta | Uruguay |

| Eritrea ** | Mauritania ** | Zambia ** |

| Estonia | Mauritius | Zimbabwe ** |

| Note: Low-Income Countries (LICs) as defined by the IMF are marked with “**”. | ||

| 1 | These include for example, resources for monitoring and enforcement (e.g., well-trained and educated staff, insufficient data and technology (e.g., electronic payments systems)). |

| 2 | For example, the share of the shadow economy in GDP for countries such as Zimbabwe and Bolivia amounted to 60.6 percent and 62.3 percent, respectively, over the period from 1991 to 2015 (see Medina and Schneider 2018). |

| 3 | For example, the share of the shadow economy in GDP for countries such as Austria and Switzerland amounted to 8.9 percent and 7.2 percent, respectively, over the period from 1991 to 2015 (see Medina and Schneider 2018). |

| 4 | Such a trade liberalization takes place not only under the auspices of the WTO (i.e., through multilateral trade liberalization) but also through countries’ participation in regional trade agreements and plurilateral trade agreements. |

| 5 | It is relatively easy for governments to collect trade tax revenue compared to domestic tax revenue in developing countries. |

| 6 | The advice has usually been made that in reforming the domestic tax revenue structure, policymakers in developing countries should broaden the consumption tax base (e.g., Ban and Gallagher 2015; Reinsberg et al. 2020; Kentikelenis and Seabrooke 2017; Kreickemeier and Raimondos-Møller 2008). |

| 7 | |

| 8 | The literature on the effect of the shadow economy on international trade is limited. Some studies have found that the small size of the entities that operate in the shadow economy undermines the penetration in the regional or international trade markets and hence hampers countries’ participation in international trade (e.g., Elbadawi and Loayza 2008; La Porta and Shleifer 2008). This is because operators (producers) in the informal sector face huge regulatory obstacles that substantially increase their businesses’ transaction costs (e.g., Hall and Sobel 2008) and constrain their participation in international trade. A few other studies have noted that the increase in the shadow economy may help expand opportunities in trade under specific conditions, such as the existence of vertical linkages with the formal sector (e.g., Carr and Chen 2002) or the existence of the possibility to switch jobs from the informal to the formal sector with skill upgrading and new skills, which requires certain levels of education, opportunities for retraining, etc. (e.g., Davis and Haltiwanger 1990; Davis et al. 1996). |

| 9 | This raises equity concerns given that in developing countries, the incomes of operators in the shadow economy are low. |

| 10 | As we will see later, the indicator of tax transition reform used in the empirical analysis has been computed on the basis of this definition. |

| 11 | As we will see later in the analysis, the tax revenue’s dependence on trade tax revenue is measured by the share of international trade tax revenue in non-resource tax revenue. |

| 12 | A rich theoretical literature has been developed on the effect of trade openness on the shadow economy, using various approaches and assumptions concerning the functioning of the labor market and the informal economy (e.g., Sinha 2009). The variety of the theoretical findings reflects the multiple approaches and assumptions made in the theoretical analyses. In these theoretical analyses, the effect of trade openness on the shadow economy depends on the degree of capital mobility between the formal and informal sectors, the existence of vertical linkages between the formal and the informal economy, and whether the informal economy is disconnected from the formal economy and hence constitutes a residual economy (e.g., see a literature review in Bacchetta et al. 2009). |

| 13 | Few studies in the literature have dealt with the effect of the shadow economy on tax revenue (e.g., Ishak and Farzanegan 2020; Mazhar and Méon 2017; Vlachaki 2015). |

| 14 | |

| 15 | As we will see below, our panel data cover only relatively few developing countries and the period from 2000 to 2015, because we rely on the episodes of tax reform identified by Akitoby et al. (2020). |

| 16 | This approach involves using the individual and time effects for the model and treating individuals’ unobserved effects. |

| 17 | Cruz-Gonzalez et al. (2017) have developed routines in the Stata software to address the incidental parameter problem in panel models with individual and time effects and a binary response dependent variable. |

| 18 | However, this approach has the drawback of eliminating all individuals for which there is no variation in the binary response variable. |

| 19 | |

| 20 | |

| 21 | In this equation, the shadow economy indicator is the dependent variable, and the structural tax reform indicator is an explanatory variable. |

| 22 | |

| 23 | High inflation rates could lead to an appreciation of the real exchange rate, thereby favoring imports and hence generating higher trade tax revenue. |

| 24 | Limiting here our period of analysis to the year 2015 also helps ensure that we have the same end year (i.e., 2015) as in the panel dataset developed by Akitoby et al. (2020) and used to estimate model (A.1). We, nevertheless, use data from the year 1995 here, with a view to making full use of available data. |

| 25 | We use the 3-year sub-periods (and not, for example, 5-year sub-periods) because the time dimension of the panel data is relatively short. By allowing us to dampen the effect of business cycles on variables at hand, the use of the 3-year average data also helps reduce the time dimension of the panel data and concurrently ensure the availability of relatively sufficient information to perform the empirical analysis. |

| 26 | It is worth noting that the indicator of tax transition reform has been computed for each developing country per year, before computing the 3-year non-overlapping dataset. |

| 27 | While it is difficult to identify precisely which countries could be considered as ‘developed countries’ versus ‘developing countries’, we follow studies cited above that computed this indicator and opt for considering ‘developed countries’ as the so-called “old-industrialized countries”. This set of countries has a structure of tax revenue that is weakly dependent on international trade tax revenue. The “old-industrialized countries” include Australia, Austria, Belgium, Canada, Denmark, Finland, France, Germany, Greece, Japan, Luxembourg, Netherlands, New Zealand, Norway, Portugal, Spain, Sweden Switzerland, the United Kingdom, and the United States of America (see the studies cited above). |

| 28 | The MIMIC method is a theory-based approach that can be used to estimate the influence of a set of exogenous causal variables on the latent variable (which is, here, the shadow economy) (see Frey and Weck-Hanneman 1984, who were among the first scholars that applied this approach). |

| 29 | Other recent empirical analyses that have used this indicator include, for example, Berdiev and Saunoris (2018), Berdiev et al. (2018, 2020), and Canh et al. (2021). |

| 30 | In fact, the conventional panel quantile regression methods allow the individual effects to only cause parallel (location) shifts of the distribution of the dependent variable with a view to mitigating the effect of the incidental parameters problem. |

| 31 | Rios-Avila (2020) has developed a routine (mmqreg) in the Stata software to estimate quantile regressions via the Methods of Moments. In running the regressions, we have used the “absorb” function to take into account time-invariant unobserved specific effects and time effects. |

| 32 | This estimator uses Driscoll and Kraay’s (1998) technique to correct standard errors for the heteroscedasticity, autocorrelation, and the correlation among countries in the error term. In fact, the Driscoll and Kraay’s (1998) technique uses a nonparametric covariance matrix estimator to generate standard errors that are heteroscedasticity-consistent and robust to very general forms of spatial and temporal dependence (e.g., Hoechle 2007; Vogelsang 2012). |

| 33 | These regressors are the shadow economy, the share of trade tax revenue in total non-resource tax revenue, the level of trade openness, the share of total natural resource rents in GDP, the unemployment rate, the economic growth rate, and the institutional and governance quality. |

| 34 | The dummy “LIC” takes the value of 1 for LICs, as defined by the International Monetary Fund, and 0 otherwise (Appendix A.5 contains the list of the 44 LICs used here). Note that as the model specification is estimated using the within fixed effects approach, the dummy LIC is dropped from the regression. This explains why we have not reported the estimate of this dummy variable. This estimate is indeed not relevant here. |

| 35 | The estimate attached to the indicator of economic growth is negative and significant at the 5% level in column [3] but not significant at the 10% level in column [4] of Table A1. This underlines the difficulty of concluding on a precise direction concerning the effect of the economic growth on the likelihood of structural tax reform in LICs. |

| 36 | This is in contrast with Gupta and Jalles (2022a), who have obtained no significant effect of the unemployment rate on the likelihood of reform in these three tax policy areas. |

| 37 | Values of the real per capita income in the full sample range between USD 237.3 and USD 57,723.1 (see Appendix A.4). |

References

- Adandohoin, Kodjo. 2021. Tax transition in developing countries: Do value added tax and excises really work? International Economics and Economic Policy 18: 379–424. [Google Scholar] [CrossRef]

- Aizenman, Joshua, and Yothin Jimjarak. 2009. Globalisation and developing countries-a shrinking tax base? Journal of Development Studies 45: 653–71. [Google Scholar] [CrossRef]

- Akcigit, Ufuk, and Marc Melitz. 2022. Chapter 6-International trade and innovation. In Handbook of International Economics. Edited by Gita Gopinath, Elhanan Helpman and Kenneth Rogoff. Amsterdam: Elsevier Science, vol. 5, pp. 377–404. [Google Scholar]

- Akitoby, Bernardin, Anja Baum, Clay Hackney, Olamide Harrison, Keyra Primus, and Veronique Salins. 2020. Tax revenue mobilization episodes in developing countries. Policy Design and Practice 3: 1–29. [Google Scholar] [CrossRef]

- Allred, Brent B., and Walter G. Park. 2007. The influence of patent protection on firm innovation investment in manufacturing industries. Journal of International Management 13: 91–109. [Google Scholar] [CrossRef]

- Alm, James, and Abel Embaye. 2013. Using dynamic panel methods to estimate shadow economies around the world. 1984–2006. Public Finance Review 41: 510–43. [Google Scholar] [CrossRef]

- Amemiya, Takeshi. 1978. The Estimation of a Simultaneous Equation Generalized Probit Model. Econometrica 46: 1193–205. [Google Scholar] [CrossRef]

- Amiti, Mary, and Jozef Konings. 2007. Trade Liberalization, Intermediate Inputs, and Productivity: Evidence from Indonesia. American Economic Review 97: 1611–38. [Google Scholar] [CrossRef]

- Arellano, Manuel, and Stephen Bond. 1991. Some tests of specification for panel data: Monte Carlo evidence and an application to employment equations. Review of Economic Studies 58: 277–97. [Google Scholar] [CrossRef]

- Arezki, Rabah, Alou Adessé Dama, and Grégoire Rota-Graziosi. 2021. Revisiting the Relationship between Trade Liberalization and Taxation. Working Paper Series N° 349. Abidjan: African Development Bank. [Google Scholar]

- Asea, Patrick K. 1996. The informal sector: Baby or bath water? Carnegie-Rochester Conference Series on Public Policy 45: 163–71. [Google Scholar] [CrossRef]

- Atkin, David, and Dave Donaldson. 2022. Chapter 1—The role of trade in economic development. In Handbook of International Economics. Edited by Gita Gopinath, Elhanan Helpman and Kenneth Rogoff. Amsterdam: Elsevier Science, vol. 5, pp. 1–59. [Google Scholar]

- Bacchetta, Marc, Ekkehard Ernst, and Juana P. Bustamante. 2009. Globalization and Informal Jobs in Developing Countries. Geneva: International Labour Organization and World Trade Organization. [Google Scholar]

- Bahl, Roy W. 2003. Reaching the Hardest to Tax: Consequences and Possibilities. Paper presented at the ‘Hard to Tax: An International Perspective’ Conference, Atlanta, GA, USA, May 15–16. [Google Scholar]

- Bajada, Christopher, and Friedrich Schneider. 2009. Unemployment and the shadow economy in the OECD. Revue Économique 60: 1033–67. [Google Scholar] [CrossRef]

- Ban, Cornel, and Kevin P. Gallagher. 2015. Recalibrating policy orthodoxy: The IMF since the great recession. Governance 28: 131–46. [Google Scholar] [CrossRef]

- Bas, Maria, and Caroline Paunov. 2021. Input quality and skills are complementary and increase output quality: Causal evidence from Ecuador’s trade liberalization. Journal of Development Economics 151: 102668. [Google Scholar] [CrossRef]

- Bas, Maria, and Vanessa Strauss-Kahn. 2015. Input-trade liberalization, export prices and quality upgrading. Journal of International Economics 95: 250–62. [Google Scholar] [CrossRef]

- Bastiaens, Ida, and Nita Rudra. 2016. Trade liberalization and the challenges of revenue mobilization: Can international financial institutions make a difference? Review of International Political Economy 23: 261–89. [Google Scholar] [CrossRef]

- Baunsgaard, Thomas, and Michael Keen. 2010. Tax Revenue and (or?) Trade Liberalization. Journal of Public Economics 94: 563–77. [Google Scholar] [CrossRef]

- Belloc, Filippo, and Antonio Nicita. 2011. The Political Determinants of Liberalization: Do Ideological Cleavages Still Matter? International Review of Economics 58: 121–45. [Google Scholar] [CrossRef]

- Berdiev, Aziz N., and James W. Saunoris. 2018. Does globalisation affect the shadow economy? The World Economy 41: 222–41. [Google Scholar] [CrossRef]

- Berdiev, Aziz N., Cullen Pasquesi-Hill, and James W. Saunoris. 2015. Exploring the dynamics of the shadow economy across US states. Applied Economics 47: 6136–47. [Google Scholar] [CrossRef]

- Berdiev, Aziz N., James W. Saunoris, and Friedrich Schneider. 2018. Give me liberty, or I will produce underground: Effects of economic freedom on the shadow economy. Southern Economic Journal 85: 537–62. [Google Scholar] [CrossRef]

- Berdiev, Aziz N., James W. Saunoris, and Friedrich Schneider. 2020. Poverty and the shadow economy: The role of governmental institutions. The World Economy 43: 921–47. [Google Scholar] [CrossRef]

- Bergh, Andreas, and Magnus Henrekson. 2011. Government Size and Growth: A Survey and Interpretation of the Evidence. Journal of Economic Surveys 25: 872–97. [Google Scholar] [CrossRef]

- Besley, Timothy, and Torsten Persson. 2011. Pillars of Prosperity: The Political Economics of Development Clusters. Princeton: Princeton University Press. [Google Scholar]

- Besley, Timothy, and Torsten Persson. 2014. Why Do Developing Countries Tax So Little? Journal of Economic Perspectives 28: 99–120. [Google Scholar] [CrossRef]

- Bilal, San, Melissa Dalleau, and Dan Lui. 2012. Trade Liberalisation and Fiscal Adjustments: The Case of EPAs in Africa (ECDPM Discussion Paper 137). Maastricht: European Centre for Development Policy Management. [Google Scholar]

- Bird, Richard M., Jorge Martinez-Vazquez, and Benno Torgler. 2008. Tax Effort in Developing Countries and High Income Countries: The Impact of Corruption, Voice and Accountability. Economic Analysis and Policy 38: 55–71. [Google Scholar] [CrossRef]

- Blundell, Richard, and Stephen R. Bond. 1998. Initial conditions and moment restrictions in dynamic panel data models. Journal of Econometrics 87: 115–43. [Google Scholar] [CrossRef]

- Bond, Stephen. 2002. Dynamic panel data models: A guide to micro data methods and practice. Portuguese Economic Journal 1: 141–62. [Google Scholar] [CrossRef]

- Bornhorst, Fabian, Sanjeev Gupta, and John Thornton. 2009. Natural resource endowments and the domestic revenue effort. European Journal of Political Economy 25: 439–46. [Google Scholar] [CrossRef]

- Bosch, Mariano, Edwin Goñi-Pacchioni, and William Maloney. 2012. Trade liberalization, labor reforms and formal-informal employment dynamics. Labour Economics 19: 653–67. [Google Scholar] [CrossRef]

- Bray, J. Roger, and John T. Curtis. 1957. An ordination of the upland forest communities of Southern Wisconsin. Ecological Monographies 27: 325–49. [Google Scholar] [CrossRef]

- Brun, Jean-François, Gérard Chambas, and Mario Mansour. 2015. Chapter 11. Tax Effort of Developing Countries: An Alternative Measure. In Financing Sustainable Development Addressing Vulnerabilities. Edited by Mathieu Boussichas and Patrick Guillaumont. Paris: Ferdi-Economica, pp. 205–16, 467. [Google Scholar]

- Buehn, Andreas, and Mohammad Reza Farzanegan. 2012. Smuggling around the world: Evidence from a structural equation model. Applied Economics 44: 3047–64. [Google Scholar] [CrossRef]

- Buehn, Andreas, and Mohammad Reza Farzanegan. 2013. Impact of education on the shadow economy: Institutions matter. Economics Bulletin 33: 2052–63. [Google Scholar]

- Buettner, Thiess, and Boryana Madzharova. 2018. WTO membership and the shift to consumption taxes. World Development 108: 197–218. [Google Scholar] [CrossRef]

- Cagé, Julia, and Lucie Gadenne. 2018. Tax revenues and the fiscal cost of trade liberalization. 1792–2006. 1792–2006. Explorations in Economic History 70: 1–24. [Google Scholar] [CrossRef]

- Canay, Ivan A. 2011. A Simple Approach to Quantile Regression for Panel Data. The Econometrics Journal 14: 368–86. [Google Scholar] [CrossRef]

- Canh, Phuc Nguyen, Christophe Schinckus, and Su Dinh Thanh. 2021. What are the drivers of shadow economy? A further evidence of economic integration and institutional quality. The Journal of International Trade & Economic Development 30: 47–67. [Google Scholar]

- Carnahan, Michael. 2015. Taxation Challenges in Developing Countries. Asia & The Pacific Policy Studies 2: 169–82. [Google Scholar]

- Carr, Marilyn, and Martha Alter Chen. 2002. Globalization and the Informal Economy: How Global Trade and Investment Impact on the Working Poor. Working Paper on the Informal Economy 2002/1. Geneva: ILO Employment Sector. [Google Scholar]

- Carstens, Agustín. 2005. Making regional economic integration work. Paper presented at the 20th Annual General Meeting and Conference of the Pakistan Society of Development Economists, Islamabad, Pakistan, January 12; Available online: https://www.imf.org/en/News/Articles/2015/09/28/04/53/sp011205 (accessed on 12 January 2005).

- Chachu, Daniel Ofoe. 2020. Domestic revenue displacement in resource-rich countries: What’s oil money got to do with it? Resources Policy 66: 101656. [Google Scholar] [CrossRef]

- Chambas, Gérard. 2005. Afrique au sud du Sahara: Quelle stratégie de transition fiscale? Afrique Contemporaine 1: 133–63. [Google Scholar] [CrossRef]

- Chen, Yongmin, and Thitima Puttitanun. 2005. Intellectual property rights and innovation in developing countries. Journal of Development Economics 78: 474–93. [Google Scholar] [CrossRef]

- Crivelli, Ernesto, and Sanjeev Gupta. 2014. Resource blessing, revenue curse? Domestic revenue effort in resource-rich countries. European Journal of Political Economy 35: 88–101. [Google Scholar] [CrossRef]

- Crivelli, Ernesto. 2016. Trade liberalization and tax revenue in transition: An empirical analysis of the replacement strategy. Eurasian Economic Review 6: 1–25. [Google Scholar] [CrossRef]

- Cruz-Gonzalez, Mario, Iván Fernández-Val, and Martin Weidner. 2017. Bias Corrections for Probit and Logit Models with Two-way Fixed Effects. The Stata Journal 17: 517–45. [Google Scholar] [CrossRef]

- Davis, Steven J., and John Haltiwanger. 1990. Gross Job Creation and Destruction: Microeconomic Evidence and Macroeconomic Implications. NBER Macroeconomics Annual 5: 123–68. [Google Scholar] [CrossRef]

- Davis, Steven J., John Haltiwanger, and Scott Schuh. 1996. Job Creation and Destruction. Cambridge: MIT Press. [Google Scholar]

- Dell’Anno, Roberto, and Offiong Helen Solomon. 2008. Shadow economy and unemployment rate in USA: Is there a structural relationship: An empirical analysis. Applied Economics 40: 2537–55. [Google Scholar] [CrossRef]

- Dix-Carneiro, Rafael, Pinelopi Goldberg, Costas Meghir, and Gabriel Ulyssea. 2021. Trade and Informality in the Presence of Labor Market Frictions and Regulations. NBER Working Paper 28391. Cambridge: NBER. [Google Scholar]

- Dreher, Axel, Christos Kotsogiannis, and Steve McCorriston. 2009. How do institutions affect corruption and the shadow economy? International Tax and Public Finance 16: 773–96. [Google Scholar] [CrossRef]

- Driscoll, John C., and Aart C. Kraay. 1998. Consistent Covariance Matrix Estimation with Spatially Dependent Panel Data. Review of Economics and Statistics 80: 549–60. [Google Scholar] [CrossRef]

- Duval, Romain, Davide Furceri, and Jakob Miethe. 2020. Robust Political Economy Correlates of Major Product and Labor Market Reforms in Advanced Economies: Evidence from BAMLE for Logit Models. Journal of Applied Econometrics 36: 98–124. [Google Scholar] [CrossRef]

- Elbadawi, Ibrahim, and Norman Loayza. 2008. Informality, employment and economic development in the Arab world. Journal of Development and Economic Policies 10: 25–75. [Google Scholar]

- Fan, Haichao, Yao A. Li, and Stephen R. Yeaple. 2015. Trade Liberalization, Quality, and Export Prices. The Review of Economics and Statistics 97: 1033–51. [Google Scholar] [CrossRef]

- Fernández-Val, Iván, and Martin Weidner. 2016. Individual and time effects in nonlinear panel models with large N, T. Journal of Econometrics 192: 291–312. [Google Scholar] [CrossRef]

- Finger, Joseph M., and Mordechai E. Kreinin. 1979. A measure of export similarity and its possible uses. Economic Journal 89: 905–12. [Google Scholar] [CrossRef]

- Fjeldstad, Odd-Helge. 2014. Tax and Development: Donor support to strengthen tax systems in developing countries. Public Administration and Development 34: 182–93. [Google Scholar] [CrossRef]

- Frey, Bruno S., and Hannelore Weck-Hanneman. 1984. The hidden economy as an ‘unobserved’ variable. European Economic Review 26: 33–53. [Google Scholar] [CrossRef]

- Fujiwara, Kenji. 2013. A Win–Win–Win Tariff–Tax Reform under Imperfect Competition. Review of International Economics 21: 857–67. [Google Scholar] [CrossRef]

- Gërxhani, Klarita, and Herman G. van de Werfhorst. 2013. The effect of education on informal sector participation in a postcommunist country. European Sociological Review 29: 464–76. [Google Scholar] [CrossRef]

- Gërxhani, Klarita. 2004. The informal sector in developed and less developed countries: A literature survey. Public Choice 120: 267–300. [Google Scholar] [CrossRef]

- Gmeiner, Robert, and Michael Gmeiner. 2021. Encouraging domestic innovation by protecting foreign intellectual property. International Review of Law and Economics 67: 106000. [Google Scholar] [CrossRef]

- Gnangnon, Sèna Kimm, and Jean-François Brun. 2019a. Trade openness, tax reform and tax revenue in developing countries. The World Economy 42: 3515–36. [Google Scholar] [CrossRef]

- Gnangnon, Sèna Kimm, and Jean-François Brun. 2019b. Tax Reform and Public Revenue Instability in Developing Countries: Does the Volatility of Development Aid Matter? Journal of International Development 31: 764–85. [Google Scholar] [CrossRef]

- Gnangnon, Sèna Kimm. 2019. Tax Reform and Trade Openness in Developing Countries. Journal of Economic Integration 34: 498–519. [Google Scholar] [CrossRef]

- Gnangnon, Sèna Kimm. 2020. Internet and tax reform in developing countries. Information Economics and Policy 51: 100850. [Google Scholar] [CrossRef]

- Gnangnon, Sèna Kimm. 2021. Tax Reform, Trade Openness and Export Product Diversification in Developing Countries. CESifo Economic Studies 67: 210–34. [Google Scholar] [CrossRef]

- Goldberg, Pinelopi Koujianou, and Nina Pavcnik. 2003. The response of the informal sector to trade liberalization. Journal of Development Economics 72: 463–96. [Google Scholar] [CrossRef]

- Greenaway, David, and Chris Milner. 1991. Fiscal dependence on trade taxes and trade policy reform. The Journal of Development Studies 27: 95–132. [Google Scholar] [CrossRef]

- Grossman, Gene M., and Elhanan Helpman. 1991. Trade, knowledge spillovers, and growth. European Economic Review 35: 517–26. [Google Scholar] [CrossRef]

- Gupta, Sanjeev, and João T. Jalles. 2022a. Can COVID-19 induce governments to implement tax reforms in developing countries? Applied Economics 54: 2288–301. [Google Scholar] [CrossRef]

- Gupta, Sanjeev, and João T. Jalles. 2022b. Do tax reforms affect income distribution? Evidence from developing countries. Economic Modelling 110: 105804. [Google Scholar] [CrossRef]

- Hall, Joshua C., and Russell S. Sobel. 2008. Freedom, entrepreneurship, and economic growth. In Lessons from the Poor. Edited by Alvaro Vargas Llosa. Oakland: The Independent Institute, pp. 247–68. [Google Scholar]

- Hassan, Mirza, and Wilson Prichard. 2016. The Political Economy of Domestic Tax Reform in Bangladesh: Political Settlements, Informal Institutions and the Negotiation of Reform. The Journal of Development Studies 52: 1704–21. [Google Scholar] [CrossRef]

- Hatzipanayotou, Panos, Sajal Lahiri, and Michael S. Michael. 2011. Trade and domestic tax reforms in the presence of a public good and different neutrality conditions. International Tax and Public Finance 18: 273–90. [Google Scholar] [CrossRef]

- Heckman, James J., Jeffrey Smith, and Nancy Clements. 1997. Making The Most Out Of Programme Evaluations and Social Experiments: Accounting For Heterogeneity in Programme Impacts. Review of Economic Studies 64: 487–535. [Google Scholar] [CrossRef]

- Hoechle, Daniel. 2007. Robust Standard Errors for Panel Regressions with Cross-Sectional Dependence. The Stata Journal 7: 281–312. [Google Scholar] [CrossRef]

- International Monetary Fund. 2011. Tax Policy and Administration. Available online: https://www.imf.org/external/np/otm/2010/100110.pdf (accessed on 1 April 2011).

- Ishak, Phoebe W., and Mohammad Reza Farzanegan. 2020. The impact of declining oil rents on tax revenues: Does the shadow economy matter? Energy Economics 92: 104925. [Google Scholar] [CrossRef]

- James, Alexander. 2015. US state fiscal policy and natural resources. American Economic Journal: Economic Policy 7: 238–57. [Google Scholar] [CrossRef]

- Johnson, Simon, Daniel Kaufmann, and Pablo Zoido-Lobatón. 1998a. Regulatory discretion and the unofficial economy. The American Economic Review 88: 387–92. [Google Scholar]

- Johnson, Sinom, Daniel Kaufmann, and Pablo Zoido-Lobatón. 1998b. Corruption, Public Finances and the Unofficial Economy. Discussion Paper. Washington, DC: The World Bank. [Google Scholar]

- Joshi, Anuradha, Wilson Prichard, and Christopher Heady. 2014. Taxing the Informal Economy: The Current State of Knowledge and Agendas for Future Research. Journal of Development Studies 50: 1325–47. [Google Scholar] [CrossRef]

- Kanniainen, Vesa, Jenni Pääkkönen, and Friedrich Schneider. 2004. Fiscal and Ethical Determinants of Shadow Economy: Theory and Evidence. Discussion Paper No 30. Helsinki: Helsinki Center of Economic Research. [Google Scholar]

- Kaufmann, Daniel, Aart Kraay, and Massimo Mastruzzi. 2010. The Worldwide Governance Indicators Methodology and Analytical Issues. World Bank Policy Research N° 5430 (WPS5430). Washington, DC: The World Bank. [Google Scholar]

- Keen, Michael, and Jenny Ligthart. 2002. Coordinating tariff reduction and domestic tax reform. Journal of International Economics 56: 489–507. [Google Scholar] [CrossRef]

- Keen, Michael. 2012. Tax and development-Again. In Critical Issues in Taxation in Developing Countries. Edited by George Zodrow and Clemens Fuest. Cambridge: MIT Press, pp. 13–44. [Google Scholar]

- Kentikelenis, Alexander E., and Leonard Seabrooke. 2017. The politics of the world polity: Script-writing in intergovernmental organizations. American Sociological Review 82: 1065–92. [Google Scholar] [CrossRef]

- Keshk, Omar M. G. 2003. CDSIMEQ: A program to implement two-stage probit least squares. Stata Journal, Stata Corp LP 3: 157–67. [Google Scholar] [CrossRef]

- Khattry, Barsha, and J. Mohan Rao. 2002. Fiscal Faux Pas?: An analysis of the revenue implications of trade liberalization. World Development 30: 1431–44. [Google Scholar] [CrossRef]

- Kirchler, Erich, Erik Hoelzl, and Ingrid Wahl. 2008. Enforced versus voluntary tax compliance: The slippery slope framework. Journal of Economic Psychology 29: 210–25. [Google Scholar] [CrossRef]

- Koenker, Roger. 2004. Quantile regression for longitudinal data. Journal of Multivariate Analysis 91: 74–89. [Google Scholar] [CrossRef]

- Kreickemeier, Udo, and Pascalis Raimondos-Møller. 2008. Tariff-tax reforms and market access. Journal of Development Economics 87: 85–91. [Google Scholar] [CrossRef]

- Kubota, Keiko. 2005. Fiscal constraints, collection costs, and trade policies. Economics and Politics 17: 129–50. [Google Scholar] [CrossRef]

- La Porta, Rafael, and Andrei Shleifer. 2008. The Unofficial Economy and Economic Development. Brookings Papers on Economic Activity. Washington, DC: The Johns Hopkins University Press, Brookings Institution, pp. 275–352. [Google Scholar]

- Lamarche, Carlos. 2010. Robust penalized quantile regression estimation for panel data. Journal of Econometrics 157: 396–408. [Google Scholar] [CrossRef]

- Lancaster, Tony. 2002. Orthogonal Parameters and Panel Data. The Review of Economic Studies 69: 647–66. [Google Scholar] [CrossRef]

- Lerner, Josh. 2009. The empirical impact of intellectual property rights on innovation: Puzzles and clues. American Economic Review 99: 343–48. [Google Scholar] [CrossRef]

- Lledo, Victor, Mick Moore, and Aaron Schneider. 2004. Governance, Taxes and Tax Reform in Latin America (IDS Working Paper 221). Brighton: Institute of Development Studies. [Google Scholar]

- Loayza, Norman A. 1996. The economics of the informal sector: A simple model and some empirical evidence from Latin America. Carnegie-Rochester Conference Series on Public Policy 44: 129–62. [Google Scholar] [CrossRef]

- Londregan, John, and Keith Poole. 1990. Poverty, the Coup Trap, and the Seizure of Executive Power. World Politics 42: 151–83. [Google Scholar] [CrossRef]

- Lora, Eduardo. 2012. Structural Reforms in Latin America: What Has Been Reformed and How to Measure It. (Updated version.) IDB WP−346. Washington, DC: Inter-American Development Bank. [Google Scholar]

- Machado, José A. F., and João M. C. Santos Silva. 2019. Quantiles via moments. Journal of Econometrics 213: 145–73. [Google Scholar] [CrossRef]

- Maddala, Gangadharrao Soundalyarao. 1983. Limited-Dependent and Qualitative Variables in Econometrics. Cambridge: Cambridge University Press. [Google Scholar]

- Mahon, James E., Jr. 2004. Causes of Tax Reform in Latin America. 1977–1995. Latin American Research Review 39: 3–30. [Google Scholar]

- Mansour, Mario, and Michael Keen. 2009. Revenue Mobilization in Sub-Saharan Africa: Challenges from Globalization. IMF Working Paper 09/157. Washington, DC: International Monetary Fund. [Google Scholar]

- Mazhar, Ummad, and Pierre-Guillaume Méon. 2017. Taxing the unobservable: The impact of the shadow economy on inflation and taxation. World Development 90: 89–103. [Google Scholar] [CrossRef]

- Medina, Leandro, and Friedrich Schneider. 2018. Shadow Economies Around the World: What Did We Learn Over the Last 20 Years? IMF Working Paper, WP/18/17. Washington, DC: International Monetary Fund (IMF). [Google Scholar]

- Mishkin, Frederic S. 2009. Globalization and financial development. Journal of Development Economics 89: 164–69. [Google Scholar] [CrossRef]

- Moller, Lovisa. 2016. Tax Revenue Implications of Trade Liberalization in Low-Income Countries. WIDER Working Paper 2016/173. Helsinki: United Nations University World Institute for Development Economics Research (UNU-WIDER). [Google Scholar]

- Naito, Takumi, and Kenzo Abe. 2008. Welfare- and revenue-enhancing tariff and tax reform under imperfect competition. Journal of Public Economic Theory 10: 1085–94. [Google Scholar] [CrossRef]

- Naito, Takumi. 2006. Growth, revenue, and welfare effects of tariff and tax reform: Win–win–win strategies. Journal of Public Economics 90: 1263–80. [Google Scholar] [CrossRef]

- Neck, Reinhard, Jens Uwe Wächter, and Friedrich Schneider. 2012. Tax avoidance versus tax evasion: On some determinants of the shadow economy. International Tax and Public Finance 19: 104–17. [Google Scholar] [CrossRef]

- Newey, Whitney. 1987. Efficient Estimation of Limited Dependent Variable models with Endogenous Explanatory Variables. Journal of Econometrics 36: 231–50. [Google Scholar] [CrossRef]

- Neyman, Jerzy, and Elizabeth L. Scott. 1948. Consistent estimates based on partially consistent observations. Econometrica 1: 1–32. [Google Scholar] [CrossRef]

- Nickell, Stephen. 1981. Biases in Dynamic Models with Fixed Effects. Econometrica 49: 1417–26. [Google Scholar] [CrossRef]

- Pham, Thi Hong Hanh. 2017. Impacts of globalization on the informal sector: Empirical evidence from developing countries. Economic Modeling 62: 207–18. [Google Scholar] [CrossRef]

- Prichard, Wilson. 2016. Reassessing tax and development research: A new dataset, new findings, and lessons for research. World Development 80: 48–60. [Google Scholar] [CrossRef]

- Prichard, Wilson. 2018. Electoral Competitiveness, Tax Bargaining and Political Incentives in Developing Countries: Evidence from Political Budget Cycles Affecting Taxation. British Journal of Political Science 48: 427–57. [Google Scholar] [CrossRef]

- Reinsberg, Bernhard, Thomas Stubbs, and Alexander Kentikelenis. 2020. Taxing the People, Not Trade: The International Monetary Fund and the Structure of Taxation in Developing Countries. Studies in Comparative International Development 55: 278–304. [Google Scholar] [CrossRef]

- Rios-Avila, Fernando. 2020. MMQREG: Stata Module to Estimate Quantile Regressions via Method of Moments. Statistical Software Components S458750. Boston: Boston College Department of Economics. [Google Scholar]

- Rivers, Douglas, and Quang H. Vuong. 1988. Limited Information Estimators and Exogeneity Tests for Simultaneous Probit Models. Journal of Econometrics 39: 347–66. [Google Scholar] [CrossRef]

- Roodman, David M. 2009. A note on the theme of too many instruments. Oxford Bulletin of Economic and Statistics 71: 135–58. [Google Scholar] [CrossRef]

- Saunoris, James W., and Aishath Sajny. 2017. Entrepreneurship and economic freedom: Cross-country evidence from formal and informal sectors. Entrepreneurship and Regional Development 29: 292–316. [Google Scholar] [CrossRef]

- Scheve, Kenneth, and David Stasavage. 2010. The conscription of wealth: Mass warfare and the demand for progressive taxation. International Organization 64: 529–61. [Google Scholar] [CrossRef]

- Schneider, Friedrich, and Andreas Buehn. 2018. Shadow Economy: Estimation Methods, Problems, Results and Open questions. Open Economics 1: 1–29. [Google Scholar] [CrossRef]

- Schneider, Friedrich, and Dominik H. Enste. 2000. Shadow economies: Size, causes, and consequences. Journal of Economic Literature 38: 77–114. [Google Scholar] [CrossRef]

- Schneider, Friedrich, Andreas Buehn, and Claudio E. Montenegro. 2010. Shadow Economies All over the World: New Estimates for 162 Countries from 1999 to 2007. Policy Research Working Paper 5356. Washington, DC: The World Bank. [Google Scholar]

- Schneider, Friedrich. 1994. Can the shadow economy be reduced through major tax reforms? An empirical investigation for Austria. Supplement to Public Finance/Finances Publiques 49: 137–52. [Google Scholar]

- Schneider, Friedrich. 2005. Shadow economies around the world: What do we really know? European Journal of Political Economy 21: 598–642. [Google Scholar] [CrossRef]

- Schneider, Friedrich. 2010. The influence of public institutions on the shadow economy: An empirical investigation for OECD countries. Review of Law and Economics 6: 441–68. [Google Scholar] [CrossRef]

- Singh, Tarlok. 2010. Does International Trade Cause Economic Growth? A Survey. The World Economy 33: 1517–64. [Google Scholar] [CrossRef]

- Sinha, Anushree. 2009. Chapter 4. Trade and the Informal Economy. In Trade and Employment-From Myths to Facts. Edited by Marion Jansen, Ralf Peters and José Manuel Salazar-Xirinachs. Geneva: International Labour Office. [Google Scholar]

- Studenmund, Arnold H. 2011. Using Econometrics: A Practical Guide. Boston: Addison-Wesley. [Google Scholar]

- Tanzi, Vito, and Howell Zee. 2001. Tax Policy for Developing Countries. Available online: http://www.imf.org/external/pubs/ft/issues/issues27/ (accessed on 1 March 2001).

- Tanzi, Vito. 1977. Inflation, Lags in Collection, and the Real Value of Tax Revenue. IMF Staff Papers 26. Washington, DC: International Monetary Fund, pp. 154–67. [Google Scholar]

- Teobaldelli, Désirée, and Schneider Friedrich. 2013. The influence of direct democracy on the shadow economy. Public Choice 157: 543–67. [Google Scholar] [CrossRef]

- Terkper, Seth E. 2003. Managing small and medium-size taxpayers in developing economies. Tax Notes International 13: 211–34. [Google Scholar]

- Thiessen, Ulrich. 2003. The impact of fiscal policy and deregulation on shadow economies in transition countries: The case of Ukraine. Public Choice 114: 295–318. [Google Scholar] [CrossRef]

- Torgler, Benno, and Friedrich Schneider. 2009. The impact of tax morale and institutional quality on the shadow economy. Journal of Economic Psychology 30: 228–45. [Google Scholar] [CrossRef]

- Torgler, Benno. 2003. Tax Morale in Latin America. Working Paper 2003/03. Basel: Faculty of Business and Economics, University of Basel. [Google Scholar]

- Vlachaki, Mina. 2015. The Impact of the Shadow Economy on Indirect Tax Revenues. Economics and Politics 27: 234–65. [Google Scholar] [CrossRef]

- Vogelsang, Timothy J. 2012. Heteroskedasticity, autocorrelation, and spatial correlation robust inference in linear panel models with fixed-effects. Journal of Econometrics 166: 303–19. [Google Scholar] [CrossRef]

- von Haldenwang, Christian, and Maksym Ivanyna. 2012. A Comparative View on the Tax Performance of Developing Countries: Regional Patterns, Non-tax Revenue and Governance. Economics: The Open-Access, Open-Assessment E-Journal 6: 1–44. [Google Scholar] [CrossRef]

- Waglé, Swarnim. 2011. Coordinating Tax Reforms in the Poorest Countries: Can Lost Tariffs be Recouped? Policy Research Working Paper 5919. Washington, DC: The World Bank. [Google Scholar]

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Gnangnon, S.K. Effect of the Shadow Economy on Tax Reform in Developing Countries. Economies 2023, 11, 96. https://doi.org/10.3390/economies11030096

Gnangnon SK. Effect of the Shadow Economy on Tax Reform in Developing Countries. Economies. 2023; 11(3):96. https://doi.org/10.3390/economies11030096

Chicago/Turabian StyleGnangnon, Sena Kimm. 2023. "Effect of the Shadow Economy on Tax Reform in Developing Countries" Economies 11, no. 3: 96. https://doi.org/10.3390/economies11030096

APA StyleGnangnon, S. K. (2023). Effect of the Shadow Economy on Tax Reform in Developing Countries. Economies, 11(3), 96. https://doi.org/10.3390/economies11030096