Ensuring Budgetary Resources at the Level of Local Communities in the Current Social-Economic Context: Evidence for Romanian Municipalities

Abstract

1. Introduction

2. Literature Review

3. Fiscal Imbalances in Romania

4. Materials and Method

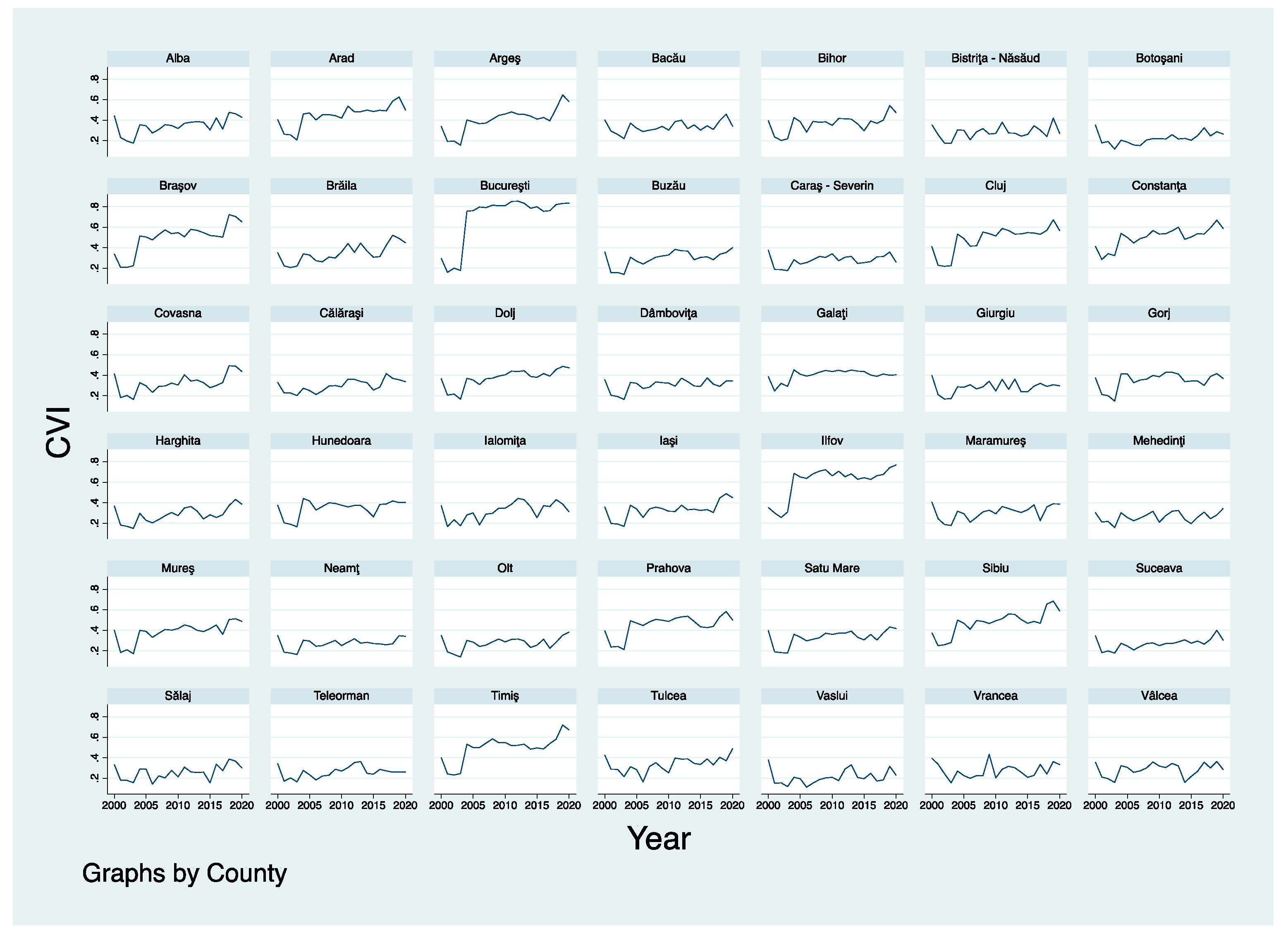

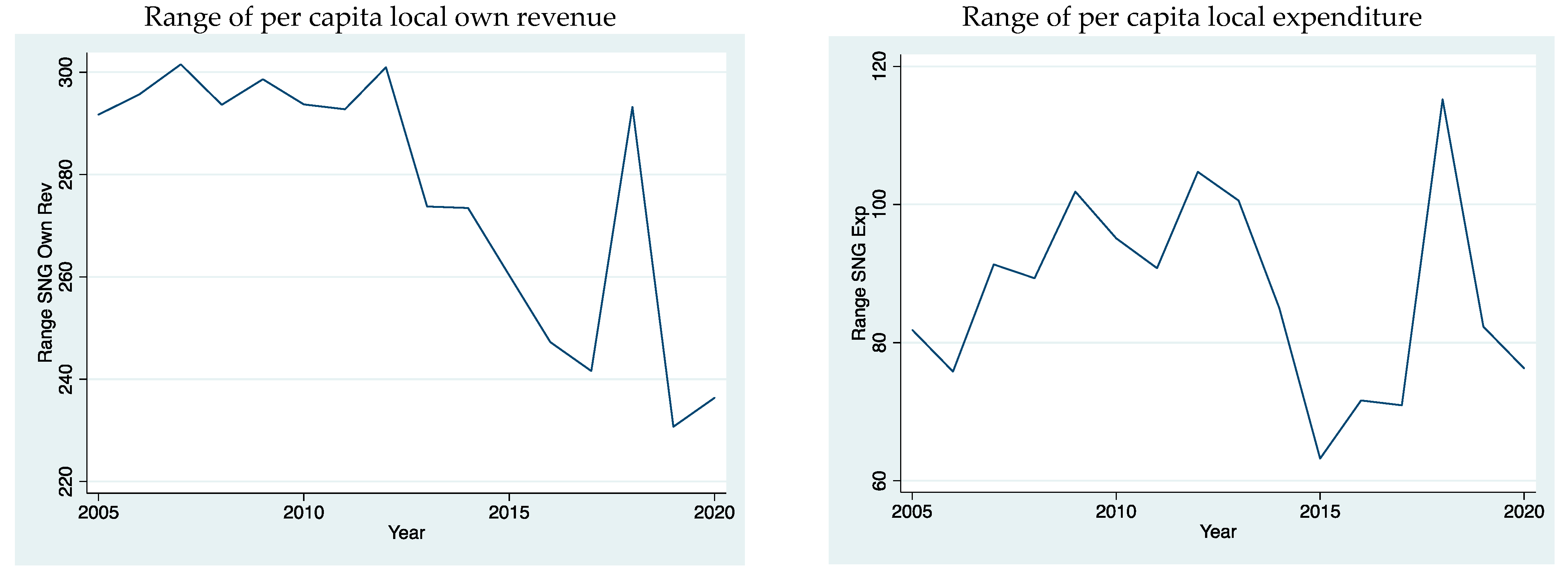

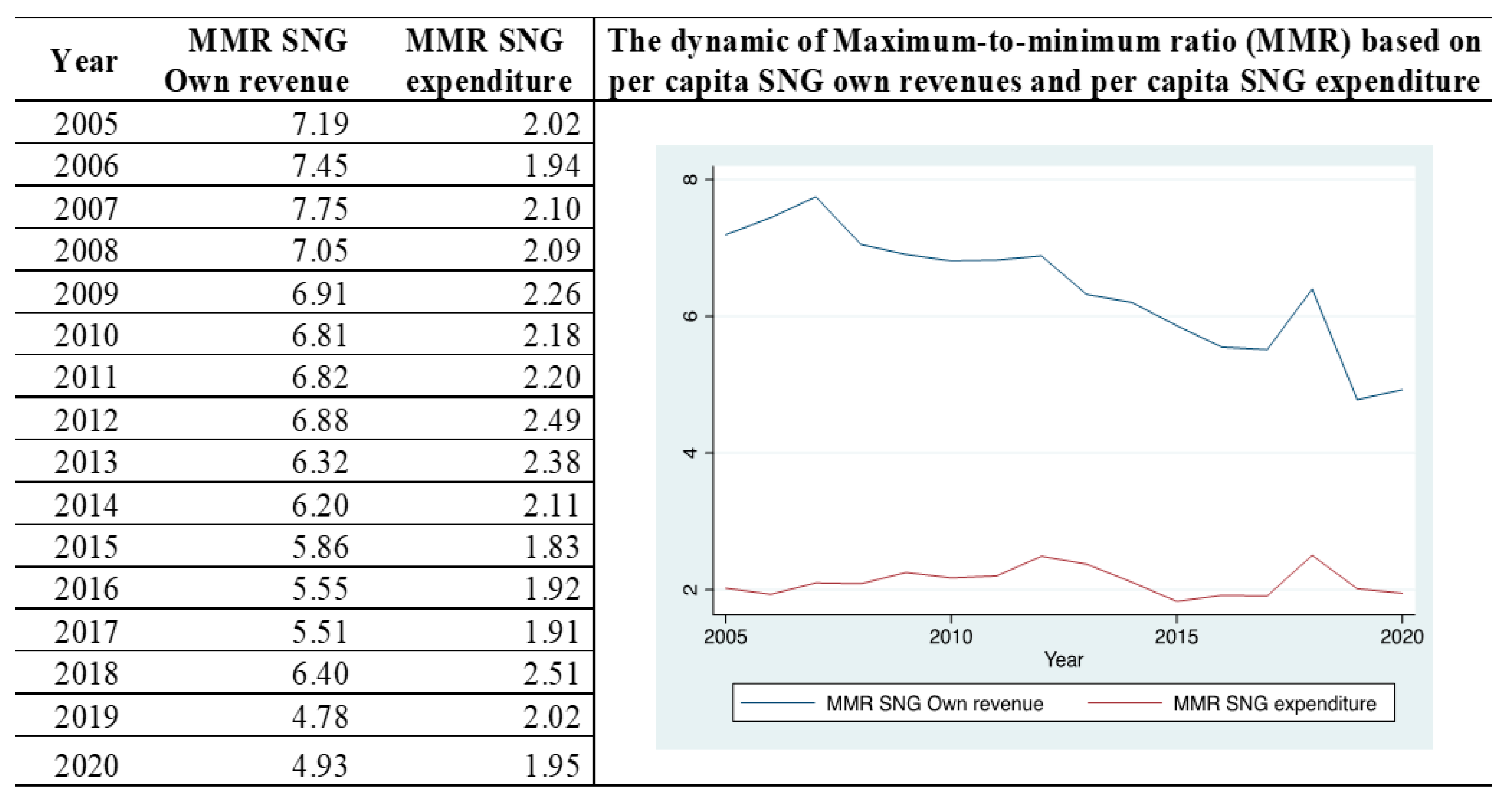

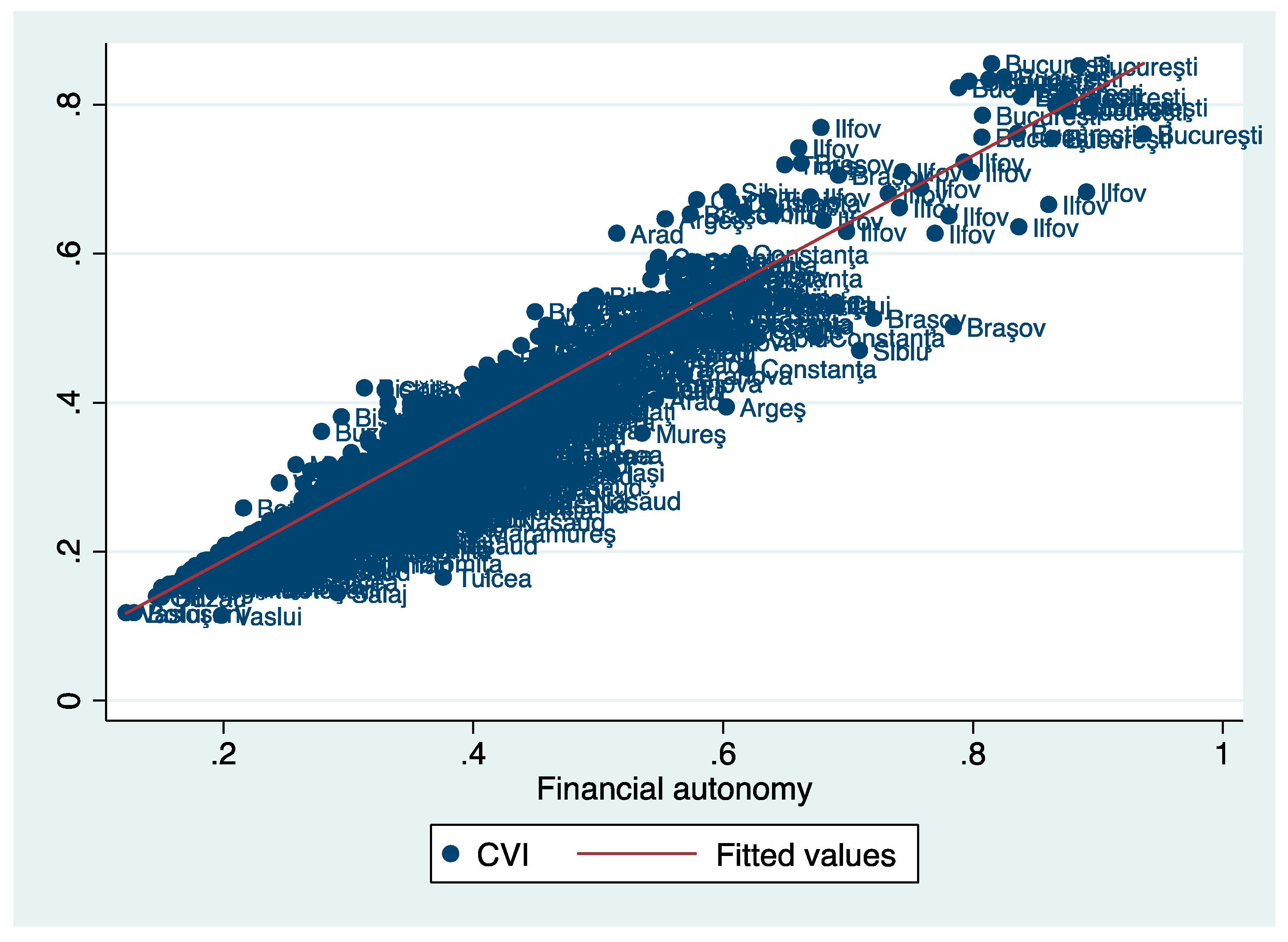

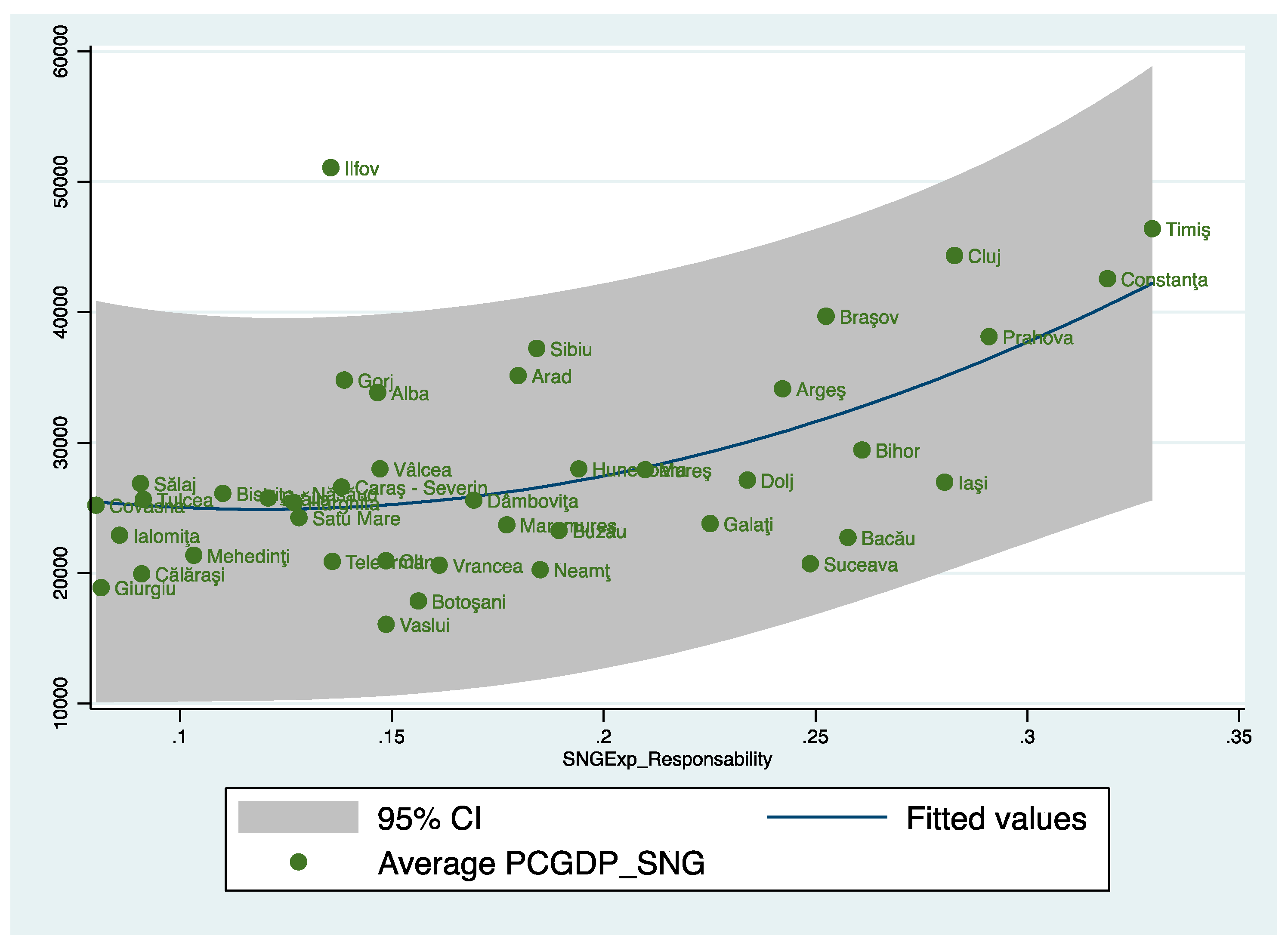

5. Results

6. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Alfada, Anisah. 2019. Does Fiscal Decentralization Encourage Corruption in Local Governments? Evidence from Indonesia. Journal of Risk and Financial Management 12: 118. [Google Scholar] [CrossRef]

- Bahl, Roy W., and Shyam Nath. 1986. Public Expenditure Decentralization in Developing Countries. Environment and Planning C: Government and Policy 4: 405–18. [Google Scholar] [CrossRef]

- Beramendi, Pablo. 2003. Political Institutions and Income Inequality: The Case of Decentralization. Markets and Political Economy Working Paper No. SP II 2003-09. Berlin: Wissenschaftszentrum Berlin. [Google Scholar]

- Bird, Richard M., and Andrey V. Tarasov. 2002. Closing the Gap: Fiscal Imbalances and Intergovernmental Transfers in Developed Federations. WP 02/02, International Studies Program. Atlanta: Andrew Young School of Policy Studies, Georgia State University. [Google Scholar]

- Bird, Richard M., and Andrey V. Tarasov. 2004. Closing the gap: Fiscal imbalances and intergovernmental transfers in developed federations. Environment and Planning C: Government and Policy 22: 77–102. [Google Scholar] [CrossRef]

- Bonomi Savignon, Andrea, Lorenzo Costumato, and Benedetta Marchese. 2019. Performance Budgeting in Context: An Analysis of Italian Central Administrations. Administrative Sciences 9: 79. [Google Scholar] [CrossRef]

- Bostan, Ionel, Andrei-Alexandru Morosan, Cristian-Valentin Hapenciuc, Pavel Stanciu, and Iulian Condratov. 2022. Are Structural Funds a Real Solution for Regional Development in the European Union? A Study on the Northeast Region of Romania. Journal of Risk and Financial Management 15: 232. [Google Scholar] [CrossRef]

- Bostan, Ionel, Carmen Toderașcu, and Anca Florentina Gavriluţă. 2018. Challenges and Vulnerabilities on Public Finance Sustainability. A Romanian Case Study. Journal of Risk and Financial Management 11: 55. [Google Scholar] [CrossRef]

- Brezovnik, Boštjan. 2008. Decentralization in theory and practice. Lex Localis 6: 87–103. [Google Scholar] [CrossRef]

- Carniti, Elena, Floriana Cerniglia, Riccarda Longaretti, and Alessandra Michelangeli. 2019. Decentralization and economic growth in Europe: For whom the bell tolls. Regional Studies 53: 775–89. [Google Scholar] [CrossRef]

- Choi, NakHyeok. 2021. Analyzing Local Government Capacity and Performance: Implications for Sustainable Development. Sustainability 13: 3862. [Google Scholar] [CrossRef]

- Constitution of Romanian. 2003. Available online: https://www.presidency.ro/en/the-constitution-of-romania (accessed on 27 September 2022).

- Costea, Ioana Maria. 2013. Financial Crisis and Insolvency of Administrative-Territorial units. Journal Analele Științifice ale Universității “Alexandru Ioan Cuza” Iași. Seria Științe Juridice 59: 121–30. [Google Scholar]

- Costea, Ioana Maria. 2020. Budgetary Premises of Local Autonomy and Descentralisation. Journal Analele Științifice ale Universității “Alexandru Ioan Cuza” Iași. Seria Științe Juridice 66: 325–42. [Google Scholar]

- Cowell, Frank A. 2011. Measuring Inequality, 3rd ed. LSE Perspectives in Economic Analysis. New York: Oxford University Press. [Google Scholar]

- DFPLB/Directorate for Fiscal Policies and Local Budgeting under Ministry of Regional Development and Public Administration and European Grants. 2021. Statement of Revenue and Expenditure of Administrative-Territorial Units. Available online: http://www.dpfbl.mdrap.ro/sit_ven_si_chelt_uat.html (accessed on 12 August 2022).

- Donahue, Amy Kneedler, Sally Coleman Selden, and Patricia W. Ingraham. 2000. Measuring Government Management Capacity: A Comparative Analysis of City Human Resources Management Systems. Journal of Public Administration Research and Theory 10: 381–412. [Google Scholar] [CrossRef]

- Ebel, Robert, and Serdar Yilmaz. 2004. On the Measurement and Impact of Fiscal Decentralization. Washington, DC: Urban Institute. [Google Scholar]

- European Commision. 2021. Eurostat. Available online: https://ec.europa.eu/eurostat/data/database (accessed on 14 August 2022).

- Ezcurra, Roberto, and Pedro Pascual. 2008. Fiscal decentralization and regional disparities: Evidence from several European Union countries. Environment and Planning A: Economy and Space 40: 1185–201. [Google Scholar] [CrossRef]

- Galizzi, Giovanna, Gaia Viviana Bassani, and Cristiana Cattaneo. 2018. Adoption of Gender-Responsive Budgeting (GRB) by an Italian Municipality. Administrative Sciences 8: 68. [Google Scholar] [CrossRef]

- Gavriluțǎ (Vatamanu), Anca Florentina, Mihaela Onofrei, and Elena Cigu. 2020. Fiscal Decentralization and Inequality: An Analysis on Romanian Regions. Ekonomický Časopis 68: 3–32. [Google Scholar]

- Gemmell, Norman, Eichard Kneller, and Ismael Sanz. 2013. Fiscal Decentralization and Economic Growth: Spending versus Revenue Decentralization. Economic Inquiry 51: 1915–31. [Google Scholar] [CrossRef]

- Hajilou, Mehran, Mohammad Mirehei, Sohrab Amirian, and Mehdi Pilehvar. 2018. Financial Sustainability of Municipalities and Local Governments in Small-Sized Cities; a Case of Shabestar Municipality. Lex Localis 16: 77–106. [Google Scholar] [CrossRef]

- Hofman, Bert, and Susana Cordeiro Guerra. 2007. Ensuring Inter-Regional Equity and Poverty Reduction. In Fiscal Equalization. Edited by Jorge Martinez-Vazquez and Bob Searle. Boston: Springer. [Google Scholar] [CrossRef]

- Hunter, James Stuart Hardy. 1974. Vertical intergovernmental financial imbalance: A framework for evaluation. Finanzarchiv 2: 481–92. [Google Scholar]

- Hunter, James Stuart Hardy. 1977. Federalism and Fiscal Balance. Canberra: Australian National University Centre for Research on Federal Financial Relations. [Google Scholar]

- Iimi, Atsushi. 2005. Decentralization and Economic Growth Revisited: An Empirical Note. The Journal of Urban Economics 57: 449–61. [Google Scholar] [CrossRef]

- Kowalik, Paweł. 2015. Horizontal fiscal imbalance in Germany. Business and Economic Horizons 11: 1–13. [Google Scholar] [CrossRef]

- Kowalik, Paweł. 2016. Measurement of vertical fiscal imbalance in Germany. Argumenta Oeconomica 2: 131–46. [Google Scholar] [CrossRef]

- Law No. 215 on Local Government. 2001. Available online: https://edirect.e-guvernare.ro/Uploads/Legi/11683/Legea%20215%20din%202001%20actualizata.pdf (accessed on 25 September 2022).

- Li, Shantong, and Zhaoyuan Xu. 2008. The Trend of Regional Income Disparity in the People’s Republic of China. ADB Institute Discussion Paper No. 85. Tokyo: Asian Development Bank Institute. Available online: http://www.adbi.org/discussionpaper/2008/01/25/2468.regional.income.disparity.prc/ (accessed on 16 August 2022).

- Lisbon Treaty. 2007. Treaty of Lisbon Amending the Treaty on European Union and the Treaty Establishing the European Community, Signed at Lisbon. OJ C 306: 271. Available online: https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX%3A12007L%2FTXT (accessed on 28 September 2022).

- Lockwood, Ben. 2005. Fiscal Decentralization: A Political Economy Perspective. Warwick Economic Research Papers No. 721. Coventry: University of Warwick, Department of Economics, pp. 1–35. Available online: http://wrap.warwick.ac.uk/274/ (accessed on 18 August 2022).

- Lukáč, Jozef, Katarína Teplická, Katarína Čulková, and Daniela Hrehová. 2021. Evaluation of the Financial Performance of the Municipalities in Slovakia in the Context of Multidimensional Statistics. Journal of Risk and Financial Management 14: 570. [Google Scholar] [CrossRef]

- Mainali, Raju. 2021. Spatial Fiscal Interactions in Colombian Municipalities: Evidence from Oil Price Shocks. Journal of Risk and Financial Management 14: 248. [Google Scholar] [CrossRef]

- Martinez-Vazquez, Jorge, and Jameson Boex. 1999. The Design of Equalization Grants: Theory and Applications. Part One: “Theory and Concepts”. Washington, DC: World Bank Institute, Andrew Young School of Policy Studies, Georgia State University. [Google Scholar]

- Martinez-Vazquez, Jorge, and Jameson Boex. 2001. Russia’s Transition to a New Federalism. Washington, DC: The World Bank. [Google Scholar]

- Martinez-Vazquez, Jorge, and Robert M. McNab. 2003. Fiscal decentralization and economic growth. World Development 31: 1597–1616. [Google Scholar] [CrossRef]

- Morariu, Alunica, Marian Ionel, and Emil Raul Mihailescu. 2010. Legal Regime Applicable to Local Budget’s Execution. Ovidius University Annals, Economic Sciences Series, Ovidius University of Constantza 10: 734–39. [Google Scholar]

- Morgan, Kevin. 2002. English question: Regional perspectives on a fractured nation. Regional Studies 36: 797–810. [Google Scholar] [CrossRef]

- Oates, Wallace E. 1972. Fiscal Federalism. New York: Harcourt Brace Jovanovich. [Google Scholar]

- Oates, Wallace E. 1993. Fiscal Decentralization and Economic Development. National Tax Journal 46: 237–43. [Google Scholar] [CrossRef]

- OECD. 2009. Taxes and Grants: On the Revenue Mix of Sub-Central Governments. Working Paper No. 7. Paris: Organization for Economic Cooperation and Development. [Google Scholar]

- Onofrei, Mihaela, Anca Gavriluţă, Ionel Bostan, Florin Oprea, Gigel Paraschiv, and Cristina Mihaela Lazăr. 2020. The Implication of Fiscal Principles and Rules on Promoting Sustainable Public Finances in the EU Countries. Sustainability 12: 2772. [Google Scholar] [CrossRef]

- Onofrei, Mihaela, Ionel Bostan, Bogdan Narcis Firtescu, Angela Roman, and Valentina Diana Rusu. 2022. Public Debt and Economic Growth in EU Countries. Economies 10: 254. [Google Scholar] [CrossRef]

- Oplotnik, Žan, and Boštjan Brezovnik. 2004. Financing Local Government in Theory and Practice: Short Lesson from Slovenia. Zagreb International Review of Economics & Business 7: 75–93. Available online: https://hrcak.srce.hr/35615 (accessed on 23 August 2022).

- Oplotnik, Žan, Boštjan Brezovnik, and Borut Vojinović. 2012. Local Self-Government Financing and Costs of Municipality in Slovenia. Transylvanian Review of Administrative Sciences 37: 128–42. [Google Scholar]

- Oprea, Florin, Irina Bilan, and Ovidiu Stoica. 2012. Fiscal Vulnerability and Economic Crisis—Romanian Lessons. In Innovation and Sustainable Economic Competitive Advantage. From Regional Development to World Economies. Proceedings of the 18th International Business Information and Management Association, Istanbul, Turkey, 9–10 May 2012. Edited by Khalid S. Soliman. Norristown: IBIMA Publishing, pp. 1795–806. ISBN 978-0-9821489-7-6. [Google Scholar]

- Oprea, Florin, Seyed Mehdian, and Ovidiu Stoica. 2013. Fiscal and Financial Stability in Romania—An Overview. Transylvanian Review of Administrative Sciences 40: 159–82. Available online: https://rtsa.ro/tras/index.php/tras/article/view/148/144 (accessed on 25 September 2022).

- Papcunová, Viera, Jarmila Hudáková, Michaela Štubnová, and Marta Urbaníková. 2020. Revenues of Municipalities as a Tool of Local Self-Government Development (Comparative Study). Administrative Sciences 10: 101. [Google Scholar] [CrossRef]

- Peterson, Paul E. 1995. The Price of Federalism. Washington, DC: Brookings Institution. [Google Scholar]

- Prud’homme, Rémy. 1995. The Dangers of Decentralization. The World Bank Research Observer 10: 201–20. Available online: http://documents.worldbank.org/curated/en/602551468154155279/The-dangers-of-decentralization (accessed on 4 August 2022).

- Rodríguez-Pose, Andrés, and Anne Krøijer. 2009. Fiscal Decentralization and Economic Growth in Central and Eastern Europe. Growth and Change: A Journal of Urban and Regional Policy 40: 387–417. [Google Scholar] [CrossRef]

- Rodríguez-Pose, Andrés, and Roberto Ezcurra. 2010. Does decentralization matter for regional disparities? A cross-country analysis. Journal of Economic Geography 10: 619–44. [Google Scholar] [CrossRef]

- Romanian Court of Accounts. 2021. Local Public Finance Reports 2019. Bucharest: Romanian Court of Accounts. Available online: https://www.curteadeconturi.ro/publicatii/65-rapoarte-privind-finantele-publice-locale/67-rapoartele-privind-finantele-publice-locale-2019 (accessed on 17 August 2022).

- Romanian National Institute of Statistics. 2021. Database. Available online: http://statistici.insse.ro:8077/tempo-online (accessed on 16 August 2022).

- Sacchi, Agnese, and Simone Salotti. 2011. Income Inequality, Regional Disparities, and Fiscal Decentralization in Industrialized Countries. Roma: Collana del Dipartemento di Economia, Universita degli Studi Roma. [Google Scholar]

- Satoła, Lukasz, Aldona Standar, and Agnieszka Kozera. 2019. Financial Autonomy of Local Government Units: Evidence from Polish Rural Municipalitie. Lex Localis-Journal of Local Self-Government 17: 321–42. [Google Scholar] [CrossRef]

- Schneider, Aaron. 2003. Decentralization: Conceptualization and measurement. Studies in Comparative International Development 38: 32–56. [Google Scholar] [CrossRef]

- Schroeder, Larry, and Paul Smoke. 2003. Intergovernmental Fiscal Transfers: Concepts, International Practice and Policy Issues. In Intergovernmental Fiscal Transfers in Asia: Current Practice and Challenges for the Future. Edited by Paul Smoke and Yun-Hwan Kim. Mandaluyong City: Asian Development Bank, pp. 20–59. [Google Scholar]

- Sepulveda, Cristian, and Jorge Martinez-Vazquez. 2011. The Consequences of Fiscal Decentralization on Poverty and Income Inequality. Environment and Planning C: Politics and Space 29: 321–43. [Google Scholar] [CrossRef]

- Shankar, Raja, and Anwar Shah. 2001. Bridging the Economic Divide within Nations: A Scorecard on the Performance of Regional Policies in Reducing Regional Income Disparities. Policy Research Paper 2717. Washington, DC: World Bank. [Google Scholar]

- Slavinskaitė, Neringa. 2017. Fiscal decentralization and economic growth in selected European countries. Journal of Business Economics and Management 18: 745–57. [Google Scholar] [CrossRef]

- Thiessen, Ulrich. 2003. Fiscal decentralization and economic growth in high income OECD countries. Fiscal Studies 24: 237–74. [Google Scholar] [CrossRef]

- Tiebout, Charles M. 1956. A Pure Theory of Local Expenditures. The Journal of Political Economy 64: 416–24. [Google Scholar] [CrossRef]

- Tselios, Vassilis, Andrés Rodríguez-Pose, Andy Pike, John Tomaney, and Gianpiero Torrisi. 2012. Income Inequality, Decentralization, and Regional Development in Western Europe. Environment and Planning A: Economy and Space 44: 1278–301. [Google Scholar] [CrossRef]

- United Nations/Development Programme. 2012. Sustainable Development Goals. New York: United Nations. Available online: https://www.undp.org/sustainable-development-goals (accessed on 29 September 2022).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Variables | (1) | (2) | (3) |

|---|---|---|---|

| (1) PCGDP_SNG | 1.000 | ||

| (2) SNG_EXP | 0.789 * | 1.000 | |

| (3) CVI | 0.806 * | 0.634 * | 1.000 |

| Variables | Obs | Mean | Std. Dev. | Min | Max | p1 | p99 | Skew. | Kurt. |

|---|---|---|---|---|---|---|---|---|---|

| PCGDP_SNG | 588 | 29,368.9 | 13,587.41 | 8822.101 | 126,000 | 12,041.1 | 86,167.21 | 2.545 | 13.508 |

| SNG_EXP | 588 | 1.06 × 109 | 1.03 × 109 | 1.74 × 108 | 9.76 × 109 | 1.99 × 108 | 7.33 × 109 | 5.147 | 33.889 |

| CVI | 588 | 0.371 | 0.129 | 0.115 | 0.855 | 0.159 | 0.811 | 1.209 | 4.796 |

| (1) OLS | (2) Random Effects | |

|---|---|---|

| PCGDP_SNG | PCGDP_SNG | |

| SNG_EXP | 0.00000616 *** | 0.00000983 *** |

| (9.95) | (21.24) | |

| CVI | 53,946.3 *** | 35,138.5 *** |

| (15.14) | (9.51) | |

| _cons | 2847.8 ** | 5940.0 *** |

| (2.81) | (4.40) | |

| N | 588 | 588 |

| R-sq | 0.779 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Onofrei, M.; Bostan, I.; Cigu, E.; Vatamanu, A.F. Ensuring Budgetary Resources at the Level of Local Communities in the Current Social-Economic Context: Evidence for Romanian Municipalities. Economies 2023, 11, 22. https://doi.org/10.3390/economies11010022

Onofrei M, Bostan I, Cigu E, Vatamanu AF. Ensuring Budgetary Resources at the Level of Local Communities in the Current Social-Economic Context: Evidence for Romanian Municipalities. Economies. 2023; 11(1):22. https://doi.org/10.3390/economies11010022

Chicago/Turabian StyleOnofrei, Mihaela, Ionel Bostan, Elena Cigu, and Anca Florentina Vatamanu. 2023. "Ensuring Budgetary Resources at the Level of Local Communities in the Current Social-Economic Context: Evidence for Romanian Municipalities" Economies 11, no. 1: 22. https://doi.org/10.3390/economies11010022

APA StyleOnofrei, M., Bostan, I., Cigu, E., & Vatamanu, A. F. (2023). Ensuring Budgetary Resources at the Level of Local Communities in the Current Social-Economic Context: Evidence for Romanian Municipalities. Economies, 11(1), 22. https://doi.org/10.3390/economies11010022