The Determinants of Competitiveness in Global Palm Oil Trade

Abstract

:1. Introduction

2. Literature Review

3. Methodology

3.1. Variables and Conceptual Framework

β5LogEUVit + β6Asiait + β7logTOit + β8RSPOit + eit

3.2. Expected Relationships and Data Source

3.3. Additional Analysis

4. Results

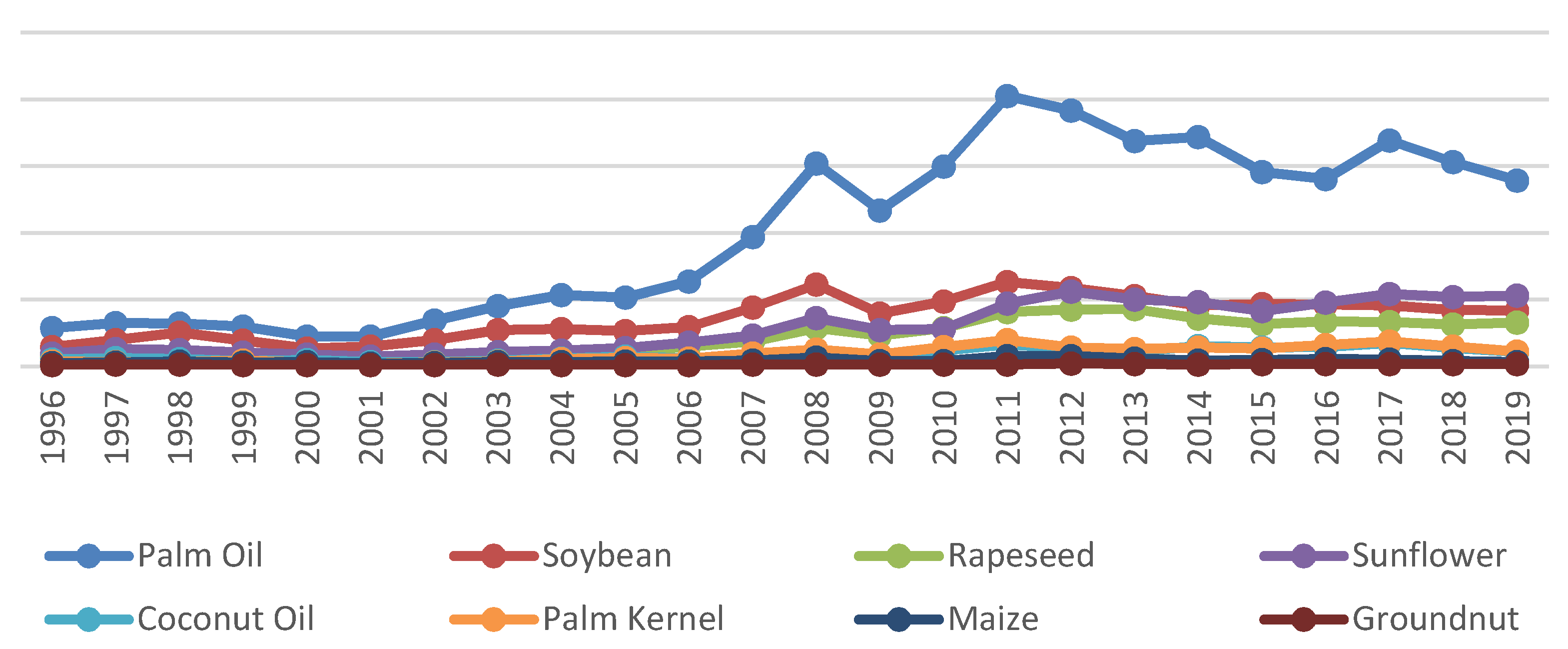

4.1. The Global Production, Consumption, and Trade of Palm Oil

4.2. The Competitiveness of Global Palm Oil Trade and Determinants

4.3. The Stability of Global Palm Oil Competitiveness

5. Conclusions

Author Contributions

Funding

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Anderson, Kym, and Signe Nelgen. 2012. Agricultural Trade Distortions during the Global Financial Crisis. Oxford Review of Economic Policy 28: 235–60. [Google Scholar] [CrossRef]

- Annas, Azwar, Suharno Suharno, and Rita Nurmalina. 2020. The Effect of The European Union Biomass Regulation and Export Taxation on Palm Oil Export. Jurnal Manajemen Dan Agribisnis 17: 1. [Google Scholar] [CrossRef]

- Arip, Affendy M., Lau Sim Yee, and Thien Sie Feng. 2013. Assessing the competitiveness of Malaysia and Indonesia palm oil related industry. World Review of Business Research 3: 138–45. [Google Scholar]

- Arsyad, Muhammad, Achmad Amiruddin, Suharno Suharno, and Siti Jahroh. 2020. Competitiveness of Palm Oil Products in International Trade: An Analysis between Indonesia and Malaysia. Caraka Tani: Journal of Sustainable Agriculture 35: 157–67. [Google Scholar] [CrossRef]

- Ayompe, Lacour M., Marije Schaafsma, and Benis N. Egoh. 2021. Towards Sustainable Palm Oil Production: The Positive and Negative Impacts on Ecosystem Services and Human Wellbeing. Journal of Cleaner Production 278: 123914. [Google Scholar] [CrossRef]

- Bahta, Yonas T. 2021. Competitiveness of South Africa’s Agri-Food Commodities. AIMS Agriculture and Food 6: 945–68. [Google Scholar] [CrossRef]

- Balassa, Bela. 1965. Trade Liberalisation and “Revealed” Comparative Advantage. The Manchester School of Economic and Social Studies 32: 99–123. [Google Scholar] [CrossRef]

- Balassa, Bela, and Marcus Noland. 1989. ‘Revealed’ Comparative Advantage in Japan and the United States. Journal of Economic Integration 4: 8–15. [Google Scholar] [CrossRef] [Green Version]

- Balogh, Jeremiás Máté, and A. Jámbor. 2017a. Determinants of Revealed Comparative Advantages: The Case of Cheese Trade in the European Union. Acta Alimentaria 46: 305–11. [Google Scholar] [CrossRef] [Green Version]

- Balogh, Jeremiás Máté, and Attila Jámbor. 2017b. The Global Competitiveness of European Wine Producers. British Food Journal 119: 2076–88. [Google Scholar] [CrossRef]

- Baltagi, Badi. H. 2008. Econometric Analysis of Panel Data (Volume 4). Chichester: John Wiley & Sons. [Google Scholar]

- Basiron, Yusof. 2007. Palm Oil Production through Sustainable Plantations. European Journal of Lipid Science and Technology 109: 289–95. [Google Scholar] [CrossRef]

- Bhawsar, Pragya, and Utpal Chattopadhyay. 2015. Competitiveness: Review, Reflections and Directions. Global Business Review 16: 665–79. [Google Scholar] [CrossRef]

- Bojang, Baseedy, and Alieu Gibba. 2021. The Global Competitiveness of West African Cashew Exporters. Bulgarian Journal of Agricultural Science 27: 1084–92. [Google Scholar]

- Bojnec, Stefan, and Imre Fertő. 2015. Institutional Determinants of Agro-Food Trade. In Transformations in Business and Economics 14: 35–52. [Google Scholar]

- Bojnec, Štefan, and Imre Fertő. 2008. European Enlargement and Agro-Food Trade. Canadian Journal of Agricultural Economics 56: 563–79. [Google Scholar] [CrossRef]

- Dalum, Bent, Keld Laursen, and Gert Villumsen. 1998. Structural Change in OECD Export Specialisation Patterns: De-Specialisation and ‘Stickiness. International Review of Applied Economics 12: 423–43. [Google Scholar] [CrossRef]

- Deardorff, Alan V. 2011. Comparative Advantage and International Trade and Investment in Services. Singapore: World Scientific Publishing Co. Pte. Ltd., pp. 105–27. [Google Scholar] [CrossRef] [Green Version]

- Delgado, Mercedes, Christian Ketels, Michael E. Porter, and Scott Stern. 2012. The Determinants of National Competitiveness. NBER Working Paper No. 18249. Cambridge: National Bureau of Economic Research. [Google Scholar]

- Franke, George R. 2010. Multicollinearity. In International Encyclopedia of Marketing. New York: Wiley Online Library. [Google Scholar] [CrossRef]

- Food Agriculture and Organization (FAO). 2022. Food and Agriculture Data. Available online: fao.org/faostat/en/ (accessed on 3 March 2022).

- Guerrieri, Paolo, and Filippo Vergara Caffarelli. 2012. Trade Openness and International Fragmentation of Production in the European Union: The New Divide? Review of International Economics 20: 535–51. [Google Scholar] [CrossRef]

- Hardi, Irsan, Dawood Taufiq Carnegie, and Syathi Putri Bintusy. 2021. Determinants Comparative Advantage of Non-Oil Export 34 Provinces in Indonesia. International Journal of Business, Economics, and Social Development 2: 98–106. [Google Scholar] [CrossRef]

- Huo, Da. 2014. Impact of Country-Level Factors on Export Competitiveness of Agriculture Industry from Emerging Markets. Competitiveness Review 24: 393–413. [Google Scholar] [CrossRef]

- Indexmundi. 2022a. Commodity Price. Available online: https://www.indexmundi.com/commodities/ (accessed on 3 March 2022).

- Indexmundi. 2022b. Palm Oil Domestic Consumption by Country in 1000 MT. Available online: https://www.indexmundi.com/agriculture/?commodity=palm-oil&graph=domestic-consumption (accessed on 3 March 2022).

- International Monetary Fund. 2022. World Economic Outlook, Database—WEO Groups and Aggregates Information. Available online: https://www.imf.org/external/pubs/ft/weo/2021/02/weodata/groups.htm (accessed on 3 March 2022).

- Jansik, Csaba, Xavier Irz, and Nataliya Kuosmanen. 2014. Competitiveness of Northern European Dairy Chains. Jokioinen: MTT Agrifood Research Finland 161. [Google Scholar]

- Kadarusman, Yohanes Berenika, and Eusebius Pantja Pramudya. 2019. The Effects of India and China on the Sustainability of Palm Oil Production in Indonesia: Towards a Better Understanding of the Dynamics of Regional Sustainability Governance. Sustainable Development 27: 898–909. [Google Scholar] [CrossRef]

- Kea, Sokvibol, Hua Li, Saleh Shahriar, Nazir Muhammad Abdullahi, Samnang Phoak, and Tharo Touch. 2019. Factors Influencing Cambodian Rice Exports: An Application of the Dynamic Panel Gravity Model. Emerging Markets Finance and Trade 55: 3631–52. [Google Scholar] [CrossRef]

- Kim, Misu. 2019. Export Competitiveness of India’s Textiles and Clothing Sector in the United States. Economies 7: 47. [Google Scholar] [CrossRef] [Green Version]

- Lafay, Gérard. 1992. The Measurement of Revealed Comparative Advantages. In International Trade Modelling. New York: Springer, pp. 209–34. [Google Scholar] [CrossRef]

- Laursen, Keld. 2015. Revealed Comparative Advantage and the Alternatives as Measures of International Specialization. Eurasian Business Review 5: 99–115. [Google Scholar] [CrossRef]

- Lugo Arias, Elkyn Rafael, Mario Alberto de la Puente Pacheco, and Jose Lugo Arias. 2020. An Examination of Palm Oil Export Competitiveness through Price-Nominal Exchange Rate. International Trade Journal 34: 495–509. [Google Scholar] [CrossRef]

- Matkovski, Bojan, Branimir Kalaš, Stanislav Zekić, and Marija Jeremić. 2019. Agri-Food Competitiveness in South East Europe. Outlook on Agriculture 48: 326–35. [Google Scholar] [CrossRef]

- Mulatu, Abay. 2016. On the Concept of ‘competitiveness’ and Its Usefulness for Policy. Structural Change and Economic Dynamics 36: 50–62. [Google Scholar] [CrossRef]

- Narayan, Seema, and Poulomi Bhattacharya. 2019. Relative Export Competitiveness of Agricultural Commodities and Its Determinants: Some Evidence from India. World Development 117: 29–47. [Google Scholar] [CrossRef]

- OECD. 2014. Competitiveness (In International Trade). Available online: https://stats.oecd.org/glossary/detail.asp?ID=399 (accessed on 3 March 2022).

- Prasetyo, Agung, and Sri Marwanti. 2017. Comparative Advantage and Export Performance of Indonesian Crude Palm Oil in International Markets. Jurnal Agro Ekonomi 35: 89–103. [Google Scholar] [CrossRef]

- Pratama, Rozy A., and Tri Widodo. 2020. The Impact of Nontariff Trade Policy of European Union Crude Palm Oil Import on Indonesia, Malaysia, and the Rest of the World Economy: An Analysis in GTAP Framework. Jurnal Ekonomi Indonesia 9: 39–52. [Google Scholar] [CrossRef]

- Ramadhani, Tri Nugraha, and Rokhedi Priyo Santoso. 2019. Competitiveness Analyses of Indonesian and Malaysian Palm Oil Exports. Economic Journal of Emerging Markets 11: 46–58. [Google Scholar] [CrossRef]

- Rifin, Amzul. 2010. Export Competitiveness of Indonesia’s Palm Oil Product. Trends in Agricultural Economics 3: 1–18. [Google Scholar] [CrossRef]

- Rifin, Amzul. 2013. Competitiveness of Indonesia’s Cocoa Beans Export in the World Market. International Journal of Trade, Economics and Finance 4: 279. [Google Scholar] [CrossRef] [Green Version]

- Rifin, Amzul, Feryanto, Herawati, and Harianto. 2020. Assessing the Impact of Limiting Indonesian Palm Oil Exports to the European Union. Journal of Economic Structures 9: 1–13. [Google Scholar] [CrossRef] [Green Version]

- Johnson, Adrianne. 2014. Green Governance or Green Grab? The Roundtable on Sustainable Palm Oil (RSPO) and Its Governing Process in Ecuador. Land Deal Politics Initiative (LDPI) Working Paper. The Hague: ISS, vol. 54, pp. 1–16. [Google Scholar]

- Rosyadi, Fachry Husein, Jangkung Handoyo Mulyo, Hani Perwitasari, and Dwidjono Hadi Darwanto. 2021. Export Intensity and Competitiveness of Indonesia’s Crude Palm Oil to Main Destination Countries. Agricultural Economics (Czech Republic) 67: 189–99. [Google Scholar] [CrossRef]

- Rusu, Valentina Diana, and Angela Roman. 2018. An Empirical Analysis of Factors Affecting Competitiveness of C.E.E. Countries. Economic Research-Ekonomska Istrazivanja 31: 2044–59. [Google Scholar] [CrossRef] [Green Version]

- RSPO. 2022. Our Organisation. Available online: https://rspo.org/about/our-organisation (accessed on 3 March 2022).

- Saeyang, R., and A. Nissapa. 2021. Trade Competitiveness in the Global Market: An Analysis of Four Palm Oil Products from Indonesia, Malaysia and Thailand. International Journal of Agricultural Technology 17: 1077–94. [Google Scholar]

- Salleh, Kamalrudin Mohamed, Ramli Abdullah, Ayatollah Khomeini, Ab Rahman, N Balu, Ali Zulhusni, and Ali Nordin. 2016. Revealed Comparative Advantage and Competitiveness of Malaysian Palm Oil Exports against Indonesia in Five Major Markets. Malaysian Palm Oil Board MPOB 16: 1–7. [Google Scholar]

- Senaviratna, Namr, and Tmja Cooray. 2019. Diagnosing Multicollinearity of Logistic Regression Model. Asian Journal of Probability and Statistics 5: 1–9. [Google Scholar] [CrossRef]

- Serin, Vildan, and Abdulkadir Civan. 2008. Revealed Comparative Advantage and Competitiveness: A Case Study for Turkey towards the EU. Journal of Economic and Social Research 10: 25–41. [Google Scholar]

- Sharma, Manmohan, S. K. Gupta, and A. K. Mondal. 2012. Production and trade of major world oil crops. In Technological Innovations in Major World Oil Crops. New York: Springer, vol. 1, pp. 1–15. [Google Scholar]

- Shimizu, Hiroko, and Pierre Desrochers. 2012. The Health, Environmental and Economic Benefits of Palm Oil. IEM’s Economic Note 2012: 1–4. [Google Scholar]

- Simionescu, Mihaela, Elena Pelinescu, Samer Khouri, and Svitlana Bilan. 2021. The Main Drivers of Competitiveness in the EU-28 Countries. Journal of Competitiveness 13: 129–45. [Google Scholar] [CrossRef]

- Suroso, Arif Imam, Iyung Pahan, and Hansen Tandra. 2021. Triple Bottom Line in Indonesia Commercial Palm Oil Mill Business: Analytical Network Process Approach. International Journal of Sustainable Development and Planning 16: 965–72. [Google Scholar] [CrossRef]

- Suroso, Arif Imam, Hansen Tandra, Yusman Syaukat, and Mukhamad Najib. 2021. The issue in Indonesian palm oil stock decision making: Sustainable and risk criteria. Decision Science Letters 10: 241–46. [Google Scholar] [CrossRef]

- Suroso, Arif Imam, and Arief Ramadhan. 2014. Structural Path Analysis of the Influences from Smallholder Oil Palm Plantation toward Household Income: One Aspect of e-Government Initative. Advanced Science Letters 20: 352–56. [Google Scholar] [CrossRef]

- Suroso, Arif Imam, and Arief Ramadhan. 2012. Decision Support System for Agribusiness Investment as e-Government Service Using Computable General Equilibrium Model. In Proceedings of the 2011 2nd International Congress on Computer Applications and Computational Science. Berlin/Heidelberg: Springer, pp. 157–62. [Google Scholar]

- Suroso, Arif Imam, Sugiharto, and Arief Ramadhan. 2014. Decision Support System for Agricultural Appraisal in Dryland Areas. Advanced Science Letters 20: 1980–86. [Google Scholar] [CrossRef]

- Tandra, Hansen, Arif Imam Suroso, Yusman Syaukat, and Mukhamad Najib. 2021. Indonesian Oil Palm Export Market Share and Competitiveness to European Union Countries: Is The Roundtable on Sustainable Palm Oil (RSPO) Influential? Jurnal Manajemen & Agribisnis 18: 342. [Google Scholar] [CrossRef]

- Torok, Aron, and Attila Jambor. 2016. Determinants of the Revealed Comparative Advantages: The Case of the European Ham Trade. Agricultural Economics 62: 471–82. [Google Scholar] [CrossRef] [Green Version]

- Török, Áron, Ákos Szerletics, and Lili Jantyik. 2020. Factors Influencing Competitiveness in the Global Beer Trade. Sustainability 12: 5957. [Google Scholar] [CrossRef]

- Tsurumi, Tetsuya, and Shunsuke Managi. 2014. The Effect of Trade Openness on Deforestation: Empirical Analysis for 142 Countries. Environmental Economics and Policy Studies 16: 305–24. [Google Scholar] [CrossRef] [Green Version]

- UNcomtrade. 2022. UNcomtrade Database. Available online: https://comtrade.un.org/data/ (accessed on 3 March 2022).

- United States Department of Agriculture (USDA). 2022. Oilseeds: World Markets and Trade. Available online: https://apps.fas.usda.gov/psdonline/circulars/oilseeds.pdf (accessed on 3 March 2022).

- Wattanakul, Thanet, Sakkarin Nonthapot, and Tanawat Watchalaanun. 2021. Factors Influencing the Processed Pineapple Export Competitiveness of Thailand. Australasian Accounting, Business and Finance Journal 15: 119–27. [Google Scholar] [CrossRef]

- Widodo, Tri. 2009. Comparative Advantage: Theory, Empirical Measures and Case Studies. Review of Economic and Business Studies (REBS) 4: 57–82. [Google Scholar]

- World Economic Forum. 2011. World Economic Forum, The Global Competitiveness Report 2011–2012. Available online: https://www3.weforum.org/docs/WEF_GCR_Report_2011-12.pdf (accessed on 3 March 2022).

- Zahan, Khairul Azly, and Manabu Kano. 2018. Biodiesel Production from Palm Oil, Its by-Products, and Mill Effluent: A Review. Energies 11: 2132. [Google Scholar] [CrossRef] [Green Version]

- Zhang, Kevin Honglin. 2015. What Drives Export Competitiveness? The Role of Fdi in Chinese Manufacturing. Contemporary Economic Policy 33: 499–512. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

| Variables | Values | Source | Expected Sign |

|---|---|---|---|

| RSCA | The values range between −1 and +1 | Calculation by Author | |

| TBI | The values range between −1 and +1 | Calculation by Author | |

| LogGDPpc | USD | World Bank | − |

| LogPOP | Total | World Bank | − |

| FDI | % of GDP (net, inflows) | World Bank | − |

| logIMPAVFO | USD | UN Comtrade | + |

| expAsia | Dummy Variable, 1 = the countries that have exported palm oil to Asian countries, 0 = otherwise | UN Comtrade | + |

| Logeuv | Index | FAOSTAT | + |

| LogTO | % of GDP | World Bank | + |

| RSPOpart | Dummy Variable, 1 = the countries already have an organization to participate in RSPO, 0 = otherwise or not reported on the website, converting from RSPO member data in the first participation of the organization in year t while observing the country i origin | RSPO member | + |

| Countries | 1996–2003 | Countries | 2004–2011 | Countries | 2012–2019 |

|---|---|---|---|---|---|

| Malaysia | 48.62% | Indonesia | 45.98% | Indonesia | 55.33% |

| Indonesia | 34.83% | Malaysia | 39.78% | Malaysia | 30.38% |

| Nigeria | 3.19% | Thailand | 3.06% | Thailand | 3.70% |

| Thailand | 2.66% | Nigeria | 2.02% | Colombia | 2.02% |

| Colombia | 2.11% | Colombia | 1.77% | Nigeria | 1.56% |

| Papua New Guinea | 1.33% | Papua New Guinea | 1.08% | Papua New Guinea | 0.92% |

| Côte D’Ivoire | 1.22% | Ecuador | 0.94% | Ecuador | 0.87% |

| Ecuador | 0.99% | Ghana | 0.84% | Honduras | 0.82% |

| The Democratic Republic of The Congo | 0.66% | Côte D’Ivoire | 0.74% | Côte D’Ivoire | 0.71% |

| Cameroon | 0.65% | Honduras | 0.62% | Brazil | 0.70% |

| Countries | 1996–2003 | Countries | 2004–2011 | Countries | 2012–2019 |

|---|---|---|---|---|---|

| Indonesia | 15.80% | China | 13.73% | Indonesia | 16.73% |

| India | 12.84% | Indonesia | 12.91% | India | 15.00% |

| China | 9.78% | EU-27 | 12.09% | EU-27 | 10.93% |

| EU-27 | 8.57% | India | 12.07% | China | 9.49% |

| Malaysia | 7.38% | Malaysia | 5.87% | Malaysia | 4.96% |

| Pakistan | 5.69% | Pakistan | 4.65% | Pakistan | 4.74% |

| Nigeria | 4.37% | Nigeria | 3.18% | Thailand | 3.52% |

| Thailand | 2.55% | Thailand | 2.73% | Bangladesh | 2.28% |

| Egypt | 2.32% | Bangladesh | 2.20% | Nigeria | 2.21% |

| Japan | 1.92% | Egypt | 2.15% | USA | 2.20% |

| Countries | 1996–2003 | Countries | 2004–2011 | Countries | 2012–2019 |

|---|---|---|---|---|---|

| Malaysia | 59.17% | Malaysia | 43.21% | Indonesia | 51.63% |

| Indonesia | 23.70% | Indonesia | 42.62% | Malaysia | 33.64% |

| Netherlands | 4.19% | Netherlands | 4.73% | Netherlands | 3.85% |

| Singapore | 2.03% | Germany | 0.88% | Germany | 1.09% |

| Papua New Guinea | 1.66% | Singapore | 0.80% | Guatemala | 1.09% |

| China, Hong Kong, SAR | 1.05% | Thailand | 0.79% | Colombia | 0.91% |

| Côte d’Ivoire | 0.87% | Ecuador | 0.76% | Honduras | 0.69% |

| Germany | 0.84% | Colombia | 0.72% | Thailand | 0.64% |

| Costa Rica | 0.64% | Côte d’Ivoire | 0.54% | Côte d’Ivoire | 0.62% |

| Colombia | 0.57% | Costa Rica | 0.49% | Ecuador | 0.57% |

| Countries | 1996–2003 | Countries | 2004–2011 | Countries | 2012–2019 |

|---|---|---|---|---|---|

| India | 18.89% | China | 17.42% | India | 19.90% |

| China | 12.91% | India | 13.10% | China | 13.11% |

| Netherlands | 5.96% | Pakistan | 5.85% | Netherlands | 6.39% |

| United Kingdom | 4.76% | Netherlands | 5.59% | Pakistan | 5.91% |

| Germany | 4.70% | Bangladesh | 5.25% | Italy | 3.66% |

| Japan | 3.58% | Germany | 4.00% | Spain | 3.30% |

| Bangladesh | 2.92% | Malaysia | 3.13% | USA | 3.29% |

| Singapore | 2.72% | USA | 2.90% | Germany | 3.06% |

| Italy | 2.50% | Italy | 2.48% | Bangladesh | 2.26% |

| China, Hong Kong, SAR | 2.12% | Russian Federation | 2.30% | Russian Federation | 2.16% |

| Countries | 1996–2003 | Countries | 2004–2011 | Countries | 2012–2019 |

|---|---|---|---|---|---|

| Malaysia | 0.952 | Indonesia | 0.958 | Niger | 0.963 |

| Indonesia | 0.925 | Malaysia | 0.942 | Indonesia | 0.963 |

| Honduras | 0.918 | Solomon Isds | 0.933 | Togo | 0.936 |

| Côte d’Ivoire | 0.849 | Guatemala | 0.805 | Malaysia | 0.926 |

| Costa Rica | 0.781 | Benin | 0.802 | Sao Tome and Principe | 0.901 |

| Uganda | 0.744 | Costa Rica | 0.787 | Guatemala | 0.894 |

| Guatemala | 0.720 | Côte d’Ivoire | 0.785 | Nepal | 0.891 |

| Togo | 0.678 | Ecuador | 0.754 | Côte d’Ivoire | 0.797 |

| Colombia | 0.487 | Uganda | 0.678 | Uganda | 0.792 |

| Panama | 0.278 | Colombia | 0.566 | Benin | 0.764 |

| Countries | 1996–2003 | Countries | 2004–2011 | Countries | 2012–2019 |

|---|---|---|---|---|---|

| Indonesia | 0.970 | Indonesia | 0.998 | Indonesia | 0.998 |

| Malaysia | 0.966 | Ecuador | 0.977 | Malaysia | 0.893 |

| Costa Rica | 0.947 | Costa Rica | 0.909 | Guatemala | 0.887 |

| Ecuador | 0.848 | Malaysia | 0.877 | Cambodia | 0.782 |

| Colombia | 0.847 | Côte d’Ivoire | 0.802 | Ecuador | 0.726 |

| Côte d’Ivoire | 0.709 | Thailand | 0.799 | Thailand | 0.723 |

| Honduras | 0.654 | Guatemala | 0.739 | Honduras | 0.636 |

| Thailand | 0.550 | Honduras | 0.646 | Costa Rica | 0.626 |

| Guatemala | 0.498 | Colombia | 0.606 | Côte d’Ivoire | 0.608 |

| Panama | 0.148 | Solomon Isds | 0.471 | Colombia | 0.337 |

| Group/Period | 1996–2003 | 2004–2011 | 2012–2019 |

|---|---|---|---|

| Group A (RSCA > 0 and TBI > 0) | 8 Countries (Colombia, Costa Rica, Cote d’Ivoire, Guatemala, Honduras, Indonesia, Malaysia, and Panama) | 8 Countries (Colombia, Costa Rica, Cote d’Ivoire, Ecuador, Guatemala, Indonesia, Malaysia, and Solomon Isds) | 7 Countries (Colombia, Costa Rica, Cote d’Ivoire, Ecuador, Guatemala, Indonesia, and Malaysia) |

| Group B (RSCA > 0 and TBI < 0) | 3 Countries (Netherlands, Togo, and Uganda) | 5 Countries (Cameroon, Netherlands, Niger, Uganda, and United Rep. of Tanzania) | 8 Countries (Benin, Ghana, Netherlands, Nicaragua, Niger, Rwanda, Togo, and Uganda) |

| Group C (RSCA < 0 and TBI > 0) | 2 Countries (Brazil and Thailand) | 2 Countries (Singapore and Thailand) | 3 Countries (Cambodia, Peru, and Thailand) |

| Group D (RSCA < 0 and TBI < 0) | 74 Countries (Albania, Algeria, Andorra, Argentina, Australia, Austria, Azerbaijan, Bulgaria, Burkina Faso, Burundi, Canada, Central African Rep., Chile, China, China, Hong Kong, SAR, Croatia, Cyprus, Egypt, Estonia, Faeroe Isds, Finland, Fmr Sudan, France, French Polynesia, Gabon, Gambia, Germany, Greece, Hungary, Iceland, India, Ireland, Israel, Italy, Jamaica, Japan, Latvia, Lithuania, Madagascar, Mali, Malta, Mauritius, Mexico, Morocco, New Zealand, Nicaragua, Niger, Nigeria, North Macedonia, Norway, Oman, Peru, Philippines, Poland, Portugal, Rep. of Korea, Romania, Russian Federation, Saint Lucia, Senegal, Singapore, Slovakia, Slovenia, Spain, Sweden, Switzerland, Tunisia, Turkey, Ukraine, United Kingdom, Uruguay, USA, Venezuela, and Zambia) | 112 Countries (Albania, Algeria, Argentina, Armenia, Australia, Austria, Azerbaijan, Bahamas, Bahrain, Bangladesh, Barbados, Belarus, Belgium, Benin, Bolivia (Plurinational State of), Bosnia Herzegovina, Botswana, Brazil, Bulgaria, Burundi, Cambodia, Canada, Chile, China, China, Hong Kong SAR, Comoros, Croatia, Cyprus, Czechia, Denmark, Dominican Rep., Egypt, El Salvador, Estonia, Eswatini, Ethiopia, Fiji, Finland, Fmr Sudan, France, French Polynesia, FS Micronesia, Gambia, Germany, Ghana, Greece, Greenland, Guyana, Hungary, Iceland, India, Ireland, Israel, Italy, Jamaica, Japan, Jordan, Kazakhstan, Kyrgyzstan, Latvia, Lebanon, Lithuania, Luxembourg, Madagascar, Malawi, Malta, Mauritius, Mexico, Morocco, Mozambique, Namibia, New Caledonia, New Zealand, Nicaragua, North Macedonia, Norway, Oman, Pakistan, Panama, Peru, Philippines, Poland, Portugal, Rep. of Korea, Rep. of Moldova, Romania, Russian Federation, Rwanda, Saint Kitts and Nevis, Saint Lucia, Samoa, Saudi Arabia, Senegal, Slovakia, Slovenia, South Africa, Spain, Sri Lanka, Suriname, Sweden, Switzerland, Trinidad and Tobago, Tunisia, Turkey, Ukraine, United Arab Emirates, United Kingdom, Uruguay, USA, Vietnam, Yemen, Zimbabwe) | 116 Countries (Albania, Angola, Argentina, Armenia, Australia, Austria, Azerbaijan Bahrain, Barbados, Belarus, Belgium, Bermuda, Bolivia (Plurinational State of), Bosnia Herzegovina, Botswana, Brazil, Brunei Darussalam, Bulgaria, Burkina Faso, Burundi, Cabo Verde, Canada, Chile, China, China, Hong Kong SAR, Comoros, Congo, Croatia, Cyprus, Czechia, Denmark, Dominican Rep., Egypt, El Salvador, Estonia, Eswatini, Ethiopia, Fiji, Finland, France, French Polynesia, Gambia, Georgia, Germany, Greece, Grenada, Guyana, Hungary, Iceland, India, Ireland, Israel, Italy, Jamaica, Japan, Jordan, Kazakhstan, Kyrgyzstan, Lao People’s Dem. Rep., Latvia, Lebanon, Lesotho, Lithuania, Luxembourg, Madagascar, Malawi, Maldives, Malta, Mauritania, Mauritius, Mexico, Montenegro, Morocco, Mozambique, Myanmar, Namibia, Nepal, New Zealand, Nigeria, North Macedonia, Norway, Pakistan, Paraguay, Philippines, Poland, Portugal, Qatar, Rep. of Korea, Rep. of Moldova, Romania, Russian Federation, Saint Lucia, Samoa, Saudi Arabia, Senegal, Serbia, Seychelles, Singapore, Slovakia, Slovenia, South Africa, Spain, State of Palestine, Sweden, Switzerland, Tunisia, Turkey, Ukraine, United Arab Emirates, United Kingdom, United Rep. of Tanzania, Uruguay, USA, Vietnam, Zambia, Zimbabwe) |

| Mean | Median | Maximum | Minimum | Std Dev | |

|---|---|---|---|---|---|

| RSCA | −0.496 | −0.866 | 0.967 | −1.000 | 0.691 |

| TBI | −0.482 | −0.831 | 1.000 | −1.000 | 0.688 |

| FDI | 4.776 | 2.543 | 86.479 | −37.712 | 8.553 |

| LOG(GDPC) | 9.342 | 9.843 | 11.390 | 5.991 | 1.406 |

| LOG(POP) | 17.257 | 17.231 | 21.065 | 14.843 | 1.541 |

| LOG(IMPAVFO) | 19.878 | 19.827 | 23.291 | 14.597 | 1.491 |

| LOG(EUV) | 4.402 | 4.454 | 5.932 | 3.045 | 0.450 |

| ASIA | 0.636 | 1.000 | 1.000 | 0.000 | 0.482 |

| LOG(TO) | 4.239 | 4.129 | 6.093 | 2.750 | 0.638 |

| RSPO | 0.445 | 0.000 | 1.000 | 0.000 | 0.497 |

| Variables | Level (Prob) | First Differences (Prob) | Conclusions |

|---|---|---|---|

| RSCA | −7.355 *** | −15.974 *** | Stationary |

| TBI | −7.331 *** | −15.481 *** | Stationary |

| FDI | −4.454 *** | −16.465 *** | Stationary |

| GDPC | −2.245 ** | −13.649 *** | Stationary |

| POP | 1.164 | −10.157 *** | Non-Stationary |

| IMPAVFO | −2.261 ** | −14.702 *** | Stationary |

| EUV | −1.400 | −14.742 *** | Non-Stationary |

| TO | −2.260 ** | −15.579 *** | Stationary |

| Variables | RSCA | TBI | ||||

|---|---|---|---|---|---|---|

| OLS | FEM | GLS | OLS | FEM | GLS | |

| C | 3.637 *** | −1.118 *** | −0.980 *** | 4.285 *** | −0.117 | 0.049 |

| FDI | −0.001 | −0.001 | 0.000 | −0.006 ** | −0.001 | −0.001 |

| LOG(GDPC) | −0.167 *** | −0.081 *** | −0.090 *** | −0.115 *** | −0.001 | −0.016 |

| D(LOG(POP)) | 23.724 *** | 2.893 ** | 3.506 *** | 11.354 *** | 5.241 *** | 5.664 *** |

| LOG(IMPAVFO) | −0.174 *** | 0.078 *** | 0.073 *** | −0.250 *** | −0.035 ** | −0.037 ** |

| D(LOG(EUV)) | 0.012 | −4 × 10−4 | 1.09 × 10−5 | −0.006 | −0.009 | −0.009 |

| ASIA | 0.104 *** | −0.005 | −0.006 | 0.301 *** | −0.028 | −0.026 |

| LOG(TO) | 0.100 *** | −0.042 | −0.033 | 0.187 *** | 0.074 * | 0.076 * |

| RSPO | 0.389 *** | −0.045 *** | −0.035 ** | 0.472 *** | −0.012 | −0.002 |

| R-squared | 0.488 | 0.961 | 0.054 | 0.377 | 0.946 | 0.061 |

| F-statistic | 94.727 *** | 451.958 *** | 5.684 *** | 60.325 *** | 315.101 *** | 6.478 *** |

| N | 805 | 805 | 805 | 805 | 805 | 805 |

| Chow Test | 276.079 *** | - | 233.867 *** | |||

| Hausman Test | - | 42.538 *** | 26.595 *** | |||

| Advanced Economies | Emerging and Developing Economies | |||||||

|---|---|---|---|---|---|---|---|---|

| Variables | RSCA | TBI | RSCA | TBI | ||||

| FEM | GLS | FEM | GLS | FEM | GLS | FEM | GLS | |

| C | −0.001 | −0.152 | 0.839 | 0.436 | −1.438 *** | −1.383 *** | −0.205 | −0.200 |

| FDI | −8.670 × 10−5 | −3.320 × 10−5 | −2.450 × 10−4 | −8.040 × 10−5 | −3.790 × 10−3 | −3.833 × 10−3 | −1.775 × 10−3 | −2.695 × 10−3 |

| LOG(GDPC) | −0.243 *** | −0.238 *** | −0.196 *** | −0.186 *** | −0.073 * | −0.038 | 0.103 *** | 0.155 *** |

| D(LOG(POP)) | 2.286 ** | 2.455 *** | 4.576 *** | 4.950 *** | 13.144 *** | 14.896 *** | 12.529 *** | 13.082 *** |

| LOG(IMPAVFO) | 0.075 *** | 0.075 *** | 0.003 | 0.012 | 0.100 *** | 0.072 *** | −0.071 *** | −0.108 *** |

| D(LOG(EUV)) | −0.004 | −0.004 | −0.001 | −0.003 | 0.009 | 0.010 | −0.027 | −0.026 |

| ASIA | 0.007 | 0.009 | −0.011 | −0.004 | 0.020 | 0.011 | −0.044 | −0.040 |

| LOG(TO) | 0.043 | 0.065 * | 0.082 | 0.108 ** | −0.032 | 0.011 | 0.134 ** | 0.206 *** |

| RSPO | −0.053 *** | −0.057 *** | −0.015 | −0.030 | −0.003 | 0.003 | −0.030 | −0.026 |

| R-squared | 0.899 | 0.196 | 0.740 | 0.094 | 0.953 | 0.069 | 0.958 | 0.133 |

| F-statistic | 142.230 *** | 13.731 *** | 45.485 *** | 5.860 *** | 299.543 *** | 3.095 *** | 334.773 *** | 6.423 *** |

| N | 460 | 460 | 460 | 460 | 345 | 345 | 345 | 345 |

| Chow Test | 137.128 *** | 41.360 *** | 157.246 *** | 202.607 *** | ||||

| Hausman Test | 12.389 | 13.975 * | 29.382 *** | 55.698 *** | ||||

| Lags | α | β | p-Value | R-Square | R | β/R | N |

|---|---|---|---|---|---|---|---|

| 1 | −0.0260 | 0.9625 | 0.0000 | 0.9178 | 0.9580 | 1.0047 | 1886 |

| 2 | −0.0290 | 0.9550 | 0.0000 | 0.8912 | 0.9440 | 1.0116 | 1804 |

| 3 | −0.0298 | 0.9509 | 0.0000 | 0.8763 | 0.9361 | 1.0158 | 1722 |

| 4 | −0.0346 | 0.9422 | 0.0000 | 0.8534 | 0.9238 | 1.0199 | 1640 |

| 5 | −0.0346 | 0.9383 | 0.0000 | 0.8355 | 0.9141 | 1.0266 | 1558 |

| 6 | −0.0299 | 0.9402 | 0.0000 | 0.8275 | 0.9097 | 1.0336 | 1476 |

| 7 | −0.0301 | 0.9350 | 0.0000 | 0.8052 | 0.8974 | 1.0419 | 1394 |

| 8 | −0.0255 | 0.9385 | 0.0000 | 0.8050 | 0.8972 | 1.0460 | 1312 |

| 9 | −0.0291 | 0.9304 | 0.0000 | 0.7858 | 0.8864 | 1.0496 | 1230 |

| 10 | −0.0348 | 0.9180 | 0.0000 | 0.7585 | 0.8709 | 1.0541 | 1148 |

| 11 | −0.0355 | 0.9171 | 0.0000 | 0.7605 | 0.8720 | 1.0517 | 1066 |

| 12 | −0.0396 | 0.9098 | 0.0000 | 0.7448 | 0.8630 | 1.0542 | 984 |

| 13 | −0.0355 | 0.9111 | 0.0000 | 0.7364 | 0.8581 | 1.0617 | 902 |

| 14 | −0.0261 | 0.9159 | 0.0000 | 0.7241 | 0.8509 | 1.0764 | 820 |

| 15 | −0.0369 | 0.8999 | 0.0000 | 0.6915 | 0.8316 | 1.0822 | 738 |

| 16 | −0.0236 | 0.9143 | 0.0000 | 0.7005 | 0.8370 | 1.0923 | 656 |

| 17 | −0.0269 | 0.9052 | 0.0000 | 0.6739 | 0.8209 | 1.1026 | 574 |

| 18 | −0.0409 | 0.8878 | 0.0000 | 0.6507 | 0.8066 | 1.1006 | 492 |

| 19 | −0.0403 | 0.8896 | 0.0000 | 0.6559 | 0.8099 | 1.0985 | 410 |

| 20 | −0.0582 | 0.8664 | 0.0000 | 0.6246 | 0.7903 | 1.0963 | 328 |

| 21 | −0.0656 | 0.8500 | 0.0000 | 0.5901 | 0.7682 | 1.1066 | 246 |

| 22 | −0.0794 | 0.8296 | 0.0000 | 0.5478 | 0.7401 | 1.1210 | 164 |

| 23 | −0.1243 | 0.7798 | 0.0000 | 0.5005 | 0.7075 | 1.1022 | 82 |

| Year | Survival Function | Indonesia | Malaysia | Guatemala | Cote d’Ivoire | Netherlands | Colombia | Costa Rica |

|---|---|---|---|---|---|---|---|---|

| 1996 | 0.964 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 |

| 1997 | 0.927 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 |

| 1998 | 0.890 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 |

| 1999 | 0.852 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 |

| 2000 | 0.814 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 |

| 2001 | 0.775 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 |

| 2002 | 0.736 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 |

| 2003 | 0.698 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 |

| 2004 | 0.660 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 |

| 2005 | 0.620 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 |

| 2006 | 0.582 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 |

| 2007 | 0.543 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 |

| 2008 | 0.504 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 |

| 2009 | 0.463 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 |

| 2010 | 0.423 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 |

| 2011 | 0.381 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 |

| 2012 | 0.340 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 |

| 2013 | 0.298 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 |

| 2014 | 0.254 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 |

| 2015 | 0.210 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 |

| 2016 | 0.164 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 |

| 2017 | 0.116 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 |

| 2018 | 0.067 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 |

| 2019 | 0.009 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 | 1.000 |

| Log Rank | 0.000 | |||||||

| Wilcoxon | 0.000 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Tandra, H.; Suroso, A.I.; Syaukat, Y.; Najib, M. The Determinants of Competitiveness in Global Palm Oil Trade. Economies 2022, 10, 132. https://doi.org/10.3390/economies10060132

Tandra H, Suroso AI, Syaukat Y, Najib M. The Determinants of Competitiveness in Global Palm Oil Trade. Economies. 2022; 10(6):132. https://doi.org/10.3390/economies10060132

Chicago/Turabian StyleTandra, Hansen, Arif Imam Suroso, Yusman Syaukat, and Mukhamad Najib. 2022. "The Determinants of Competitiveness in Global Palm Oil Trade" Economies 10, no. 6: 132. https://doi.org/10.3390/economies10060132

APA StyleTandra, H., Suroso, A. I., Syaukat, Y., & Najib, M. (2022). The Determinants of Competitiveness in Global Palm Oil Trade. Economies, 10(6), 132. https://doi.org/10.3390/economies10060132