The Role of Green Innovation in the Effect of Corporate Social Responsibility on Firm Performance

Abstract

:1. Introduction

2. Literature Review

2.1. Corporate Social Responsibility

2.2. Green Innovation

2.3. Firm Performance

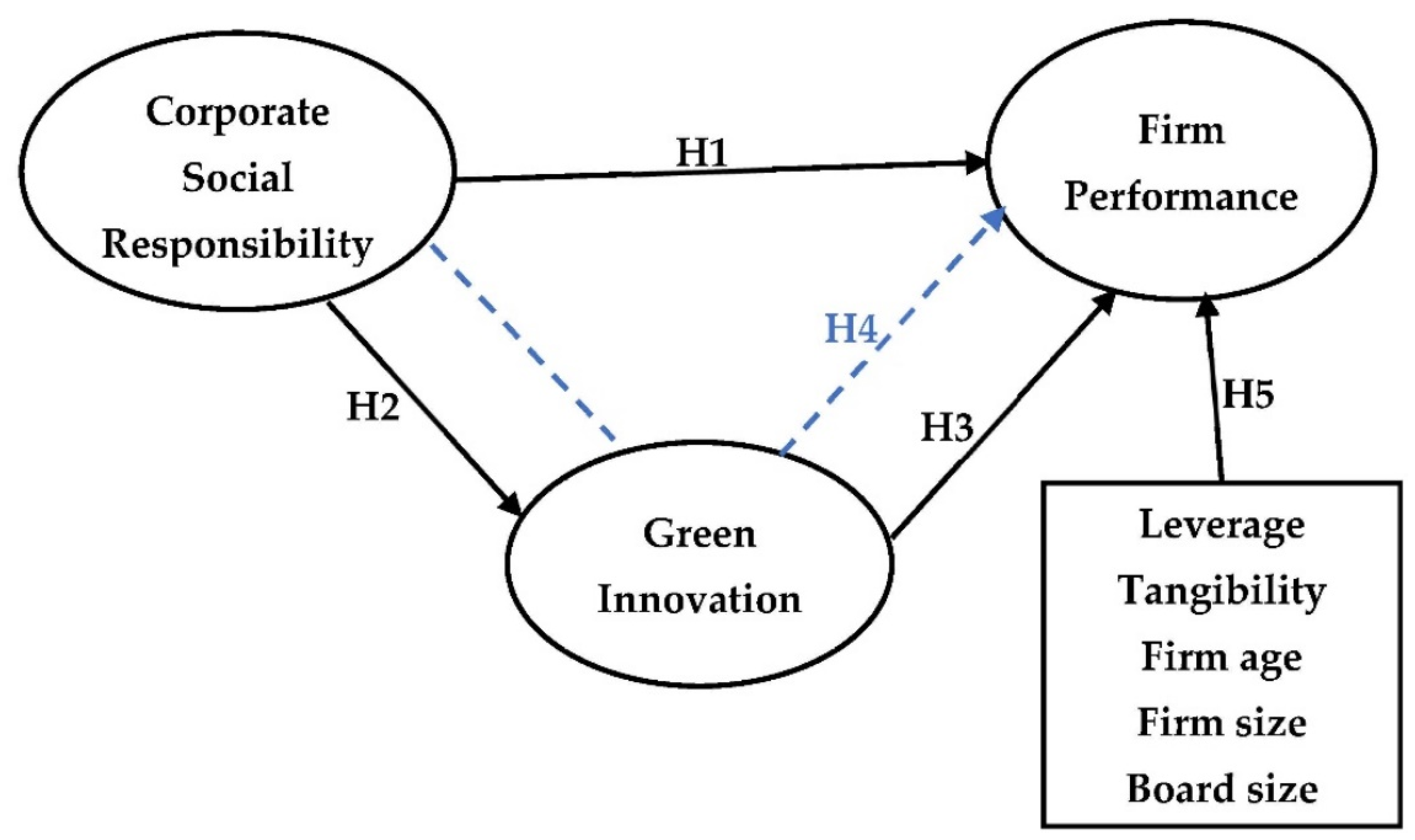

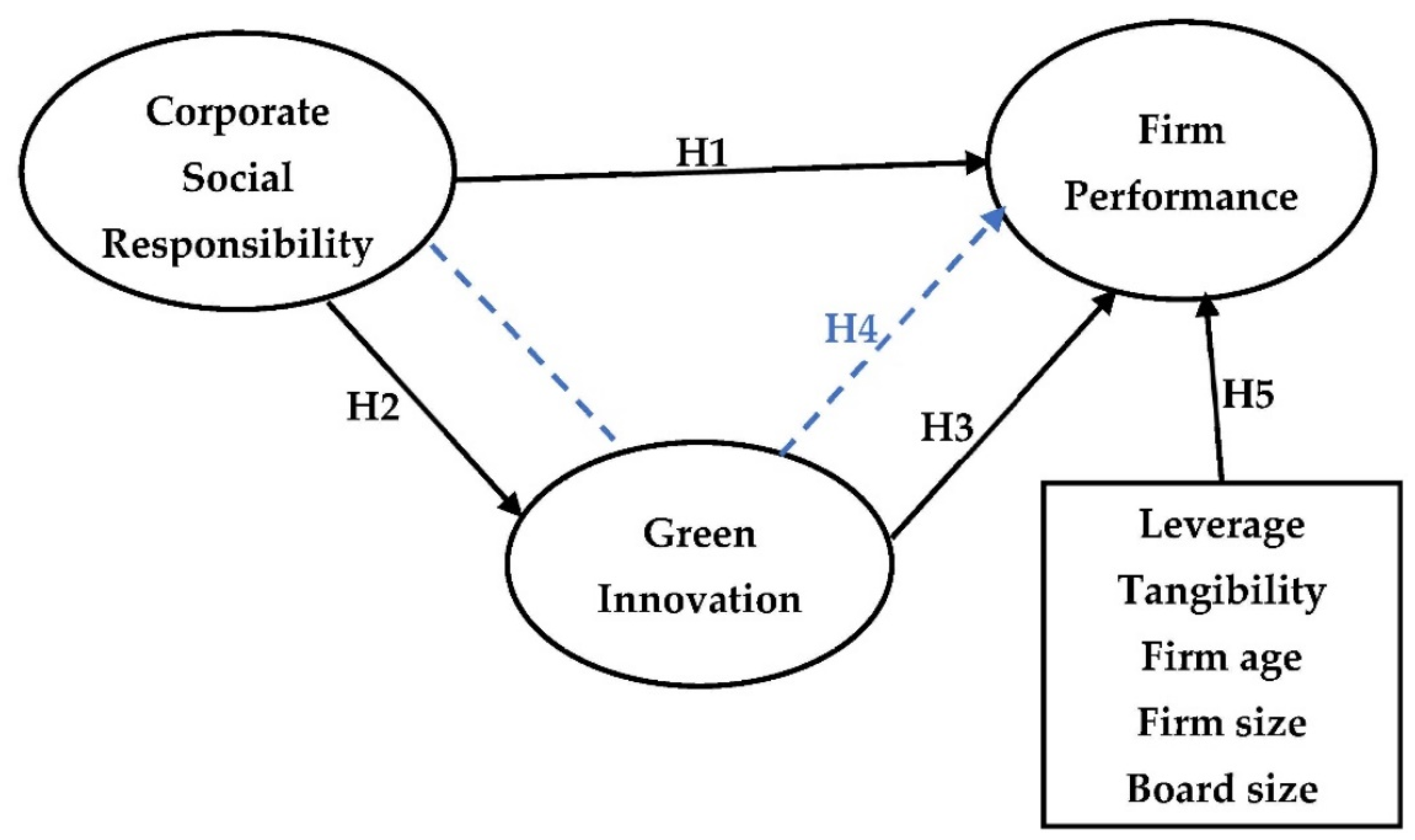

2.4. Corporate Social Responsibility and Green Innovation

2.5. Green Innovation and Firm Performance

2.6. Corporate Social Responsibility and Firm Performance

2.7. Mediation Effects of Green Innovation

2.8. Diagnostic Use of Sustainability Control Variables Leverages, Tangibility, Firm Age, Firm Size and Board Size

3. Methodology

- ROA: Return on Assets

- EBIT: Earnings Before Interest and Tax

- TA: Total Assets

4. Results

4.1. Descriptive Statistics and Correlation

4.2. Mediation Effect

5. Discussion

6. Managerial Implication and Theoretical Contribution

7. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Abbas, Jawad. 2020. Impact of total quality management on corporate green performance through the mediating role of corporate social responsibility. Journal of Cleaner Production 242: 118458. [Google Scholar] [CrossRef]

- Abeysekara, Nadeesha, Haijun Wang, and Duminda Kuruppuarachchi. 2019. Effect of supply-chain resilience on firm performance and competitive advantage A study of the Sri Lankan apparel industry. Business Process Management Journal 25: 1673–95. [Google Scholar] [CrossRef]

- Agustia, Dian, Tjiptohadi Sawarjuwono, and Wiwiek Dianawati. 2019. The mediating effect of environmental management accounting on green innovation—Firm value relationship. International Journal of Energy Economics and Policy 9: 299–306. [Google Scholar] [CrossRef]

- Agyabeng-mensah, Yaw, Esther Ahenkorah, Ebenezer Afum, Adu Nana Agyemang, Carin Agnikpe, and Foday Rogers. 2020. Examining the influence of internal green supply chain practices, green human resource management and supply chain environmental cooperation on firm performance. Supply Chain Management: An International Journal 25: 585–99. [Google Scholar] [CrossRef]

- Albort-morant, Gema, Antonio Leal-millán, and Gabriel Cepeda-carrión. 2016. The antecedents of green innovation performance: A model of learning and capabilities. Journal of Business Research 69: 4912–17. [Google Scholar] [CrossRef]

- Al-Matari, Ebrahim Mohammed, Abdullah Kaid Al-Swidi, and Faudziah Hanim Bt Fadzil. 2014. The measurements of firm performance’s dimensions. Asian Journal of Finance and Accounting 6: 24. [Google Scholar] [CrossRef]

- Al-Shammari, Marwan, Soumendra Nath Banerjee, and Abdul A. Rasheed. 2021. Corporate social responsibility and firm performance: A theory of dual responsibility. Management Decision. [Google Scholar] [CrossRef]

- Amores-Salvadó, Javier, Gregorio Martín-deCastro, and Jose E. Navas-López. 2014. Green corporate image: Moderating the connection between environmental product innovation and firm performance. Journal of Cleaner Production 83: 356–65. [Google Scholar] [CrossRef]

- Anser, Muhammad Khalid, Zhihe Zhang, and Lubna Kanwal. 2018. Moderating effect of innovation on corporate social responsibility and firm performance in the realm of sustainable development. Corporate Social Responsibility and Environmental Management 25: 799–806. [Google Scholar] [CrossRef]

- Antonioli, Davide, Susanna Mancinelli, and Massimiliano Mazzanti. 2013. Is environmental innovation embedded within high-performance organisational changes? The role of human resource management and complementarity in green business strategies. Research Policy 42: 975–88. [Google Scholar] [CrossRef]

- Arfi, Wissal Ben, Lubica Hikkerova, and Jean-Michel Sahut. 2018. External knowledge sources, green innovation, and performance. Technological Forecasting and Social Change 129: 210–20. [Google Scholar] [CrossRef]

- Awan, Usama, Andrzej Kraslawski, and Janne Huiskonen. 2018. Impact of relational governance on performance improvement in export manufacturing firms. Journal of Industrial Engineering and Management 11: 349–70. [Google Scholar] [CrossRef] [Green Version]

- Baah, Charles, and Zhihong Jin. 2019. Sustainable supply chain management and organizational performance: The intermediary role of competitive advantage. Journal of Management and Sustainability 9: 119–31. [Google Scholar] [CrossRef] [Green Version]

- Barba-Sánchez, Virginia, and Carlos Atienza-Sahuquillo. 2016. Environmental Proactivity and Environmental and Economic Performance: Evidence from the Winery Sector. Sustainability 8: 1014. [Google Scholar] [CrossRef] [Green Version]

- Basana, Sautma Ronni, Widjojo Suprapto, Fransisca Andreani, and Zeplin Jiwa Husada Tarigan. 2022. The impact of supply chain practice on green hotel performance through internal, upstream, and downstream integration. Uncertain Supply Chain Management 10: 169–80. [Google Scholar] [CrossRef]

- Bhattu-Babajee, Reena, and Boopen Seetanah. 2021. Value-added intellectual capital and financial performance: Evidence from Mauritian companies. Journal of Accounting in Emerging Economies 12: 486–506. [Google Scholar] [CrossRef]

- Broadstock, David C, Roman Matousek, Martin Meyer, and Nickolaos G. Tzeremes. 2019. Does corporate social responsibility impact firms’ innovation capacity? The indirect link between environmental and social governance implementation and innovation performance. Journal of Business Research 119: 99–110. [Google Scholar] [CrossRef]

- Brown, Halina Szejnwald, Martin de Jong, and David L. Levy. 2009. Building institutions based on information disclosure: Lessons from GRI’s sustainability reporting. Journal of Cleaner Production 17: 571–80. [Google Scholar] [CrossRef]

- Calza, Francesco, Adele Parmentola, and Ilaria Tutore. 2017. Types of Green Innovations: Ways of Implementation in a Non-Green Industry. Sustainability 9: 1301. [Google Scholar] [CrossRef] [Green Version]

- Canh, Nguyen Thi, Nguyen Thanh Liem, Phung Anh Thu, and Nguyen Vinh Khuong. 2019. The impact of innovation on the firm performance and corporate social responsibility of vietnamese manufacturing firms. Sustainability 11: 3666. [Google Scholar] [CrossRef] [Green Version]

- Chakroun, Salma, Bassem Salhi, Anis Ben Amar, and Anis Jarboui. 2020. The impact of ISO 26000 social responsibility standard adoption on firm financial performance Evidence from France. Management Research Review 43: 545–71. [Google Scholar] [CrossRef]

- Chan, Ling-Foon, A. N. Bany-Ariffin, and Annual Bin Md Nasir. 2019. Does the method of corporate diversification matter to firm’s performance? Asia-Pacific Contemporary Finance and Development 26: 207–33. [Google Scholar] [CrossRef]

- Chen, Yongjian (Ken), Nicole Coviello, and Chatura Ranaweera. 2020. How does dynamic network capability operate? A moderated mediation analysis with NPD speed and firm age. Journal of Business and Industrial Marketing 36: 292–306. [Google Scholar] [CrossRef]

- Chiou, Tzu-Yun, Hing Kai Chang, Fiona Lettice, and Sai Ho Chung. 2011. The influence of greening the suppliers and green innovation on environmental performance and competitive advantage in Taiwan. Transportation Research Part E 47: 836. [Google Scholar] [CrossRef]

- Dahlsrud, Alexander. 2008. How corporate social responsibility is defined: An analysis of 37 definitions. Corporate Social Responsibility and Environmental Management 15: 1–13. [Google Scholar] [CrossRef]

- El-Khatib, Rwan. 2017. Determinants of corporate leverage in publicly listed GCC companies—Conventional versus Sukuk. Global Corporate Governance 19: 77–102. [Google Scholar] [CrossRef]

- Farooq, Omer, Deborah E. Rupp, and Mariam Farooq. 2017. The multiple pathways through which internal and external corporate social responsibility influence organizational identification and multifoci outcomes: The moderating role of cultural and social orientations. Academy of Management Journal 60: 954–85. [Google Scholar] [CrossRef]

- Feng, Mingming, Xiaodan Wang, and Jerry Glenn Kreuze. 2017. Corporate social responsibility and firm financial performance: Comparison analyses across industries and CSR categories. American Journal of Business 32: 106–33. [Google Scholar] [CrossRef]

- Flammer, Caroline. 2015. Does corporate social responsibility lead to superiorfinancial performance? A regression discontinuityapproach. Management Science 61: 2549–68. [Google Scholar] [CrossRef] [Green Version]

- Galbreath, Jeremy. 2017. Drivers of Green Innovations: The impact of export intensity, women leaders, and absorptive capacity. Journal of Business Ethics 158: 47–61. [Google Scholar] [CrossRef]

- García-Villaverde, Pedro M., Gloria Parra-Requena, and María J. Ruiz-Ortega. 2017. From pioneering orientation to new product performance through competitive tactics in SMEs. BRQ Business Research Quarterly 20: 275–90. [Google Scholar] [CrossRef]

- Gharsalli, Mazen. 2019. High leverage and variance of SMEs performance. Journal of Risk Finance 20: 155–75. [Google Scholar] [CrossRef]

- Gillani, Fatima, Kamran Ali Chatha, Muhammad Shakeel Sadiq Jajja, and Sami Farooq. 2020. Implementation of digital manufacturing technologies: Antecedents and consequences. International Journal of Production Economics 229: 107748. [Google Scholar] [CrossRef]

- Gordon, Melissa, Michael Lockwood, Frank Vanclay, Dallas Hanson, and Jacki Schirmer. 2012. Divergent stakeholder views of corporate social responsibility in the Australian forest plantation sector. Journal of Environmental Management 113: 390–98. [Google Scholar] [CrossRef]

- Gras-gil, Ester, Mercedes Palacios Manzano, and Joaquín Hernández Fernández. 2016. Investigating the relationship between corporate social responsibility and earnings management: Evidence from Spain. BRQ Business Research Quarterly 19: 289–99. [Google Scholar] [CrossRef] [Green Version]

- Gürlek, Mert, and Muharrem Tuna. 2017. Reinforcing competitive advantage through green organizational culture and green innovation. The Service Industries Journal 38: 467–91. [Google Scholar] [CrossRef]

- Habib, Ashfaq, Muhammad Asif Khan, József Popp, and Mónika Rákos. 2022. The influence of operating capital and cash holding on firm profitability. Economies 10: 69. [Google Scholar] [CrossRef]

- Handayani, Rini, Sugeng Wahyudi, and Suharnomo Suharnomo. 2017. The effects of corporate social responsibility on manufacturing industry performance: The mediating role of social collaboration and green innovation. Business: Theory and Practice 18: 152–59. [Google Scholar] [CrossRef] [Green Version]

- Hansen, Erik G., and Stefan Schaltegger. 2016. The sustainability balanced scorecard: A systematic review of architectures. Journal of Business Ethics 133: 193–221. [Google Scholar] [CrossRef]

- Hermanto, Yustinus B., Lusy Lusy, and Maria Widyastuti. 2021. How financial performance and state-owned enterprise (SOE) values are affected by good corporate governance and intellectual capital perspectives. Economies 9: 134. [Google Scholar] [CrossRef]

- Hernández, Juan Pablo Sánchez-Infante, Benito Yañez-Araque, and Juan Moreno-García. 2020. Moderating effect offirm size on the influence of corporate socialresponsibility in the economic performance of micro-, small- and medium-sized enterprises. Technological Forecasting and Social Change 151: 119774. [Google Scholar] [CrossRef]

- Ho, Ying-Chin, Wen Bo Wang, and Wen Ling Shieh. 2016. An empirical study of green management and performance in Taiwanese electronics firms. Cogent Business and Management 3: 1266787. [Google Scholar] [CrossRef]

- Hou, Tony Chieh-Tse. 2019. The relationship between corporate social responsibility and sustainable financial performance: Firm-level evidence from Taiwan. Corporate Social Responsibility and Environmental Management 26: 19–28. [Google Scholar] [CrossRef] [Green Version]

- Jin, Mingzhou, Renzhong Tang, Yangjian Ji, Fei Liu, Liang Gao, and Donald Huisingh. 2017. Impact of advanced manufacturing on sustainability: An overview of the special volume on advanced manufacturing for sustainability and low fossil carbon emissions. Journal of Cleaner Production 161: 69–74. [Google Scholar] [CrossRef]

- Junaid, Muhammad, Qingyu Zhang, and Muzzammil Wasim Syed. 2022. Effects of sustainable supply chain integration on green innovation and firm performance. Sustainable Production and Consumption 30: 145–157. [Google Scholar] [CrossRef]

- Khan, Md. Habib-Uz-Zaman, Muhammad Azizul Islam, Johra Kayeser Fatima, and Khadem Ahmed. 2011. Corporate sustainability reporting of major commercial banks in line with GRI: Bangladesh evidence. Social Responsibility Journal 7: 347–62. [Google Scholar] [CrossRef] [Green Version]

- Khan, Parvez Alam, and Satirenjit Kaur Johl. 2019. Nexus of comprehensive green innovation, environmental management system-14001-2015 and firm performance: A conceptual framework. Cogent Business and Management 6: 1691833. [Google Scholar] [CrossRef]

- Kraus, Sascha, Shafique Ur Rehman, and F. Javier Sendra García. 2020. Corporate social responsibility and environmental performance: The mediating role of environmental strategy and green innovation. Technological Forecasting and Social Change 160: 120262. [Google Scholar] [CrossRef]

- Łaszkiewicz, Edyta. 2019. Eco-innovations in SMEs. Science for Environment Policy 20: 119–31. [Google Scholar] [CrossRef]

- Lee, Jung Wan, Young Min Kim, and Young Ei Kim. 2018. Antecedents of adopting corporate environmental responsibility and green practices. Journal of Business Ethics 148: 397–409. [Google Scholar] [CrossRef]

- Leitão, João, Sónia de Brito, and Serena Cubico. 2019. Eco-Innovation Influencers: Unveiling the Role of Lean Management Principles Adoption. Sustainability 11: 2225. [Google Scholar] [CrossRef] [Green Version]

- Lepak, David P., Ken G. Smith, and M. Susan Taylor. 2007. Introduction to special topic forum value creation and value capture: A multilevel perspective. Academy of Management Review 32: 180–94. [Google Scholar] [CrossRef] [Green Version]

- Li, Yiwei, Mengfeng Gong, Xiu-Ye Zhang, and Lenny Koh. 2017. The impact of environmental, social, and governance disclosure on firm value: The role of CEO power. The British Accounting Review 50: 60–75. [Google Scholar] [CrossRef] [Green Version]

- Liang, Chin Chia, Yuwen Liu, Carol Troy, and Wen Wen Chen. 2020. Firm characteristics and capital structure: Evidence from ASEAN-4 economies. Advances in Pacific Basin Business, Economics, and Finance 8: 149–62. [Google Scholar] [CrossRef]

- Mallon, Mark R., Stephen E. Lanivich, and Ryan L. Klinger. 2017. Resource configurations for new family venture growth. International Journal of Entrepreneurial Behavior and Research 24: 521–37. [Google Scholar] [CrossRef]

- Mardnly, Zukka, Sulaiman Mouselli, and Riad Abdulraouf. 2018. Corporate governance and firm performance: An empirical evidence from Syria. International Journal of Islamic and Middle Eastern Finance and Management 11: 591–607. [Google Scholar] [CrossRef]

- Mazodier, Marc, Francois Anthony Carrillat, Claire Sherman, and Carolin Plewa. 2021. Can donations be too little or too much? European Journal of Marketing 55: 271–96. [Google Scholar] [CrossRef]

- Mbanyele, William, Hongyun Huang, Yafei Li, Linda T. Muchenje, and Fengrong Wang. 2022. Corporate social responsibility and green innovation: Evidence from mandatory csr disclosure laws. Economics Letters 212: 1–7. [Google Scholar] [CrossRef]

- Moon, Jeremy, Andrew Crane, and Dirk Matten. 2005. Can corporations be citizens? Corporate citizenship as a metaphor for business participation in society. Business Ethics Quarterly 15: 429–53. [Google Scholar] [CrossRef] [Green Version]

- Munasinghe, Mohan, Priyangi Jayasinghe, Yvani Deraniyagala, Valente José Matlaba, Jorge Filipe dos Santos, Maria Cristina Maneschy, and José Aroudo Mota. 2019. Value–Supply Chain Analysis (VSCA) of crude palm oil production in Brazil, focusing on economic, environmental and social sustainability. Sustainable Production and Consumption 17: 161–75. [Google Scholar] [CrossRef]

- Nguyen, Nguyen Thi Thao, Nguyen Phong Nguyen, and Tu Thanh Hoai. 2021. Ethical leadership, corporate social responsibility, firm reputation, and firm performance: A serial mediation model. Heliyon 7: e06809. [Google Scholar] [CrossRef] [PubMed]

- Novitasari, Maya, and Dian Agustia. 2021. Green supply chain management and firm performance: The mediating effect of green innovation. Journal of Industrial Engineering and Management 14: 391–403. [Google Scholar] [CrossRef]

- Oliveira, Juliana Albuquerquer Saliba de, Leonardo Fernando Cruz Basso, Herbert Kimura, and Vinicius Amorim Sobreiro. 2019. Innovation and financial performance of companies doing business in Brazil. International Journal of Innovation Studies 2: 153–64. [Google Scholar] [CrossRef]

- Orlitzky, Marc, Frank L. Schmidt, and Sara L. Rynes. 2003. Corporate social and financial performance: A meta-analysis. Sage Journals 24: 403–41. [Google Scholar] [CrossRef]

- Ozbek, O. Volkan, and Brian Boyd. 2020. The Influence of CEO duality and board size on the market value of spun-off subsidiaries: The contingency effect of firm size. Journal of Strategy and Management 13: 333–50. [Google Scholar] [CrossRef]

- Perda Kaltim Pasal 23 Ayat 1. 2013. Peraturan Daerah Provinsi Kalimantan Timur No.09 Tahun 2013 Tentang Anggaran Pendapatan dan Belanja Daerah tahun Anggaran [East Kalimantan Provincial Regulation No. 09 of 2013 Concerning the Regional Revenue and Expenditure Budget for the Fiscal Year] 2014. Available online: https://peraturan.bpk.go.id/Home/Details/21308/perda-prov-kalimantan-timur-no-3-tahun-2013 (accessed on 20 December 2021).

- PP RI No. 47 Tahun. 2012. Tentang Tanggung Jawab Sosial dan Lingkungan Perseroan Terbatas [About Social and Environmental Responsibility of Limited Liability Companies]. Available online: https://peraturan.bpk.go.id/Home/Details/5260/pp-no-47-tahun-2012 (accessed on 20 December 2021).

- Rehfeld, Katharina-Maria, Klaus Rennings, and Andreas Ziegler. 2007. Integrated product policy and environmental product innovations: An empirical analysis. SSRN Electronic Journal 61: 91–100. [Google Scholar] [CrossRef] [Green Version]

- Saeidi, Parvaneh, Lorenzo Adalid Armijos Robles, Sayedeh Parastoo Saeidi, and Maria Isabel Vera Zamora. 2021. How does organizational leadership contribute to the firm performance through social responsibility strategies? Heliyon 7: e07672. [Google Scholar] [CrossRef]

- Sáez-Martínez, Francisco J., Cristina Díaz-García, and Ángela González-Moreno. 2016. Factors Promoting Environmental Responsibility in European SMEs: The Effect on Performance. Sustainability 8: 898. [Google Scholar] [CrossRef] [Green Version]

- Saha, Raiswa, Shashi Kashav, Roberto Cerchione, Rajwinder Sigh, and Richa Dahiya. 2019. Effect of ethical leadership and corporate social responsibility on firm performance: A systematic review. Corporate Social Responsibility and Environmental Management 27: 409–29. [Google Scholar] [CrossRef]

- Santoso, Ruben Wahyu, Hotlan Siagian, Zeplin Jiwa Husada Tarigan, and Ferry Jie. 2022. Assessing the benefit of adopting ERP technology and practicing green supply chain management toward operational performance: An evidence from Indonesia. Sustainability 14: 4944. [Google Scholar] [CrossRef]

- Sapta, I. Ketut Setia, I. Nengah Sudja, I. Nengah Landra, and Ni Wayan Rustiarini. 2021. Sustainability performance of organization: Mediating role of knowledge management. Economies 9: 97. [Google Scholar] [CrossRef]

- Shahzad, Mohsin, Ying Qu, Abaid Ullah Zafar, Saif Ur Rehman, and Tahir Islam. 2020a. Exploring the influence of knowledge management process on corporate sustainable performance through green innovation. Journal of Knowledge Management 24: 2079–106. [Google Scholar] [CrossRef]

- Shahzad, Mohsin, Ying Qu, Saad Ahmed Javed, Abaid Ullah Zafar, and Saif Ur Rehman. 2020b. Relation of environment sustainability to csr and green innovation: A case of pakistani manufacturing industry. Journal of Cleaner Production 253: 119938. [Google Scholar] [CrossRef]

- Siagian, Hotlan, Zeplin Jiwa Husada Tarigan, and Ferry Jie. 2021. Supply chain integration enables resilience, flexibility, and innovation to improve business performance in COVID-19 Era. Sustainability 13: 4669. [Google Scholar] [CrossRef]

- Soewarno, Noorlailie, Bambang Tjahjadi, and Febrina Fithrianti. 2019. Green innovation strategy and green innovation: The roles of green organizational identity and environmental organizational legitimacy. Management Decision 57: 3061–78. [Google Scholar] [CrossRef]

- Somjai, Sudawan, Ratchada Fongtanakit, and Khomsan Laosillapacharoen. 2020. Impact of environmental commitment, environmental management accounting and green innovation on firm performance: An empirical investigation. International Journal of Energy Economics and Policy 10: 204–10. [Google Scholar] [CrossRef]

- Su, Xiaofeng, Anxin Xu, Wenhe Lin, Youcheng Chen, Sangtao Liu, and Wenxing Xu. 2020. Environmental leadership green innovation practices, environmental knowledge learning, and firm performance. SAGE Open 10: 2158244020922909. [Google Scholar] [CrossRef]

- Tang, Mingfeng, Grace Walsh, Daniel Lerner, Markus A. Fitza, and Qiaohua Li. 2017. green innovation, managerial concern and firm performance: An empirical study. Business Strategy and the Environment 27: 39–51. [Google Scholar] [CrossRef]

- Tarigan, Zeplin Jiwa Husada, Hotlan Siagian, and Ferry Jie. 2021. Impact of enhanced enterprise resource planning (ERP) on firm performance through green supply chain management. Sustainability 13: 4358. [Google Scholar] [CrossRef]

- Tarigan, Zeplin Jiwa Husada, Novia Chandra Tanuwijaya, and Hotlan Siagian. 2020. Does top management attentiveness affect green performance through green purchasing and supplier collaboration? Academy of Strategic Management Journal 19: 1–9. [Google Scholar]

- Tariq, Adeel, Yuosre F. Badir, Waqas Tariq, and Umair Saeed Bhutta. 2017. Drivers and consequences of green product and process innovation: A systematic review, conceptual framework, and future outlook. Technology in Society 51: 8–23. [Google Scholar] [CrossRef]

- Tjahjadi, Bambang, Noorlailie Soewarno, and Febriani Mustikaningtiyas. 2021. Good corporate governance and corporate sustainability performance in Indonesia: A triple bottom line approach. Heliyon 7: e06453. [Google Scholar] [CrossRef]

- Wang, Qian, Junsheng Dou, and Shenghua Jia. 2016. A meta-analytic review of corporate social responsibility and corporate financial performance: The moderating effect of contextual factors. Business and Society 55: 1083–121. [Google Scholar] [CrossRef]

- Weber, Olaf. 2017. Corporate sustainability and financial performance of Chinese banks. Sustainability Accounting, Management and Policy Journal 8: 358–85. [Google Scholar] [CrossRef] [Green Version]

- Wei, An-Pin, Chi-Lu Peng, Hao-Chen Huang, and Sang-Pao Yeh. 2020. Effects of Corporate social responsibility on firm performance: Does customer satisfaction matter? Sustainability 12: 7545. [Google Scholar] [CrossRef]

- Welford, Richard. 2007. Corporate governance and corporate social responsibility: Issues for Asia. Corporate Social Responsibility and Environmental Management 14: 42–51. [Google Scholar] [CrossRef]

- Wong, Christina W. Y., Kee-hung Lai, Kuo-Chung Shang, Chin-Shan Lu, and T. K. P. Leung. 2012. Green operations and the moderating role of environmental management capability of suppliers on manufacturing firm performance. International Journal of Production Economics 140: 283–94. [Google Scholar] [CrossRef]

- Wongthongchai, Jirawat, and Krittapha Saenchaiyathon. 2019. The key role of institution pressure on green supply chain practice and the firm’s performance. Journal of Industrial Engineering and Management 12: 432–46. [Google Scholar] [CrossRef]

- Wood, Donna J. 1991. Corporate social performance revisited. Academy Ol ManagemenI Review 16: 691–718. [Google Scholar] [CrossRef]

- Xie, Xuemei, Jiage Huo, and Hailiang Zou. 2019. Green process innovation, green product innovation, and corporate financial performance: A content analysis method. Journal of Business Research 101: 697–706. [Google Scholar] [CrossRef]

- Xue, Min, Francis Boadu, and Yu Xie. 2019. The penetration of green innovation on firm performance: Effects of absorptive capacity and managerial environmental concern. Sustainability 11: 2455. [Google Scholar] [CrossRef] [Green Version]

- Yadav, Inder Sekhar, Debasis Pahi, and Phanindra Goyari. 2020. The size and growth of firms: New evidence on law of proportionate effect from Asia. Journal of Asia Business Studies 14: 91–108. [Google Scholar] [CrossRef]

- Yakob, Noor Azuddin, and Norraidah Abu Hasan. 2021. Exploring the interaction effects of board meetings on information disclosure and financial performance in public listed companies. Economies 9: 139. [Google Scholar] [CrossRef]

- Yang, Minghui, Paulo Bento, and Ahsan Akbar. 2019. Does CSR influence firm performance indicators? evidence from Chinese pharmaceutical enterprises. Sustainability 11: 5656. [Google Scholar] [CrossRef] [Green Version]

- Yin, Jianhua, Lidong Gong, and Sen Wang. 2018. Large-scale assessment of global green innovation research trends from 1981 to 2016: A bibliometric study. Journal of Cleaner Production 197: 827–41. [Google Scholar] [CrossRef]

- Zhang, Dayong, Zhao Rong, and Qiang Ji. 2019a. Green innovation and firm performance: Evidence from list companies in China. Resources, Conservation and Recycling 144: 48–55. [Google Scholar] [CrossRef]

- Zhang, Jhunru, Hadrian Geri Djajadikerta, and Terri Trireksani. 2019b. Corporate sustainability disclosure’s importance in China: Financial analysts’ perception. Social Responsibility Journal 16: 1169–89. [Google Scholar] [CrossRef]

- Zhou, Guichuan, Lan Zhang, and Liming Zhang. 2019. Corporate social responsibility, the atmospheric environment, and technological innovation investment. Sustainability 11: 481. [Google Scholar] [CrossRef] [Green Version]

- Zhu, Qinghua, Joseph Sarkis, and Yong Geng. 2005. Green supply chain management in China: Pressures, practices, and performance. International Journal of Operations &Production Management 25: 449–68. [Google Scholar] [CrossRef]

{kind=link}

| Descriptive | N | Mean | Median | Standard Deviation |

|---|---|---|---|---|

| Firm Performance | 253 | 0.068 | 0.062 | 0.057 |

| Green Innovation | 253 | 0.555 | 0.500 | 0.273 |

| Corporate Social Responsibility | 253 | 43.909 | 42.000 | 22.552 |

| Firm Size | 253 | 13.288 | 14.919 | 4.297 |

| Firm Age | 253 | 3.603 | 3.689 | 0.450 |

| Board Size | 253 | 5.289 | 5.000 | 2.634 |

| Tangibility | 253 | 0.437 | 0.450 | 0.194 |

| Leverage | 253 | 1.026 | 0.533 | 1.491 |

| FP | GI | CSR | FS | FA | BS | Tang | Lev | |

|---|---|---|---|---|---|---|---|---|

| FP | 1.000 | |||||||

| GI | 0.238 *** | 1.000 | ||||||

| (0.000) | ||||||||

| CSR | 0.364 *** | 0.217 *** | 1.000 | |||||

| (0.000) | (0.001) | |||||||

| Firm Size | 0.372 *** | 0.121 * | 0.298 *** | 1.000 | ||||

| (0.000) | (0.054) | (0.000) | ||||||

| Firm Age | 0.025 | 0.050 | 0.047 | 0.101 | 1.000 | |||

| (0.697) | (0.432) | (0.456) | (0.109) | |||||

| Board Size | −0.037 | 0.085 | 0.067 | 0.057 | 0.041 | 1.000 | ||

| (0.557) | (0.175) | (0.290) | (0.366) | (0.515) | ||||

| Tangibility | −0.289 *** | −0.012 | −0.024 | −0.089 | 0.044 | −0.055 | 1.000 | |

| (0.000) | (0.855) | (0.705) | (0.156) | (0.490) | (0.380) | |||

| Leverage | −0.076 | −0.060 | −0.056 | −0.065 | 0.082 | 0.260 *** | −0.058 | 1.000 |

| (0.231) | (0.343) | (0.376) | (0.303) | (0.194) | (0.000) | (0.360) |

| (1) Green Innovation | (2) Firm Performance | |

|---|---|---|

| CSR | 0.0026198 | 0.0006382 |

| (3.52) | (4.43) | |

| Green Innovation | 0.0325373 | |

| (2.83) | ||

| Firm Size | 0.003424 | |

| (4.57) | ||

| Firm Age | −0.0004618 | |

| (−0.07) | ||

| Board Size | −0.0019376 | |

| (−1.61) | ||

| Tangibility | −0.0776591 | |

| (−4.93) | ||

| Leverage | −0.0010379 | |

| (−0.49) | ||

| _cons | 0.4403044 | 0.0236121 |

| (3.52) | (0.87) | |

| r2 | 0.0470 | 0.3064 |

| r2_a | 0.0432 | 0.2866 |

| N | 253 | 253 |

| Input | Statistic Test | Std. Error | p-Value | |

|---|---|---|---|---|

| a | 0.0026198 | 2.20510708 | 0.00003866 | 0.02744658 |

| b | 0.0325373 | |||

| Sa | 0.0007448 | |||

| Sb | 0.0114959 |

| Hypothesis | Regression Coefficient | T Value | p-Value | Notes | |

|---|---|---|---|---|---|

| H1 | CSR → GI | 0.0026 | 3.52 | 0.001 *** | Significantly Positive |

| H2 | GI → FP | 0.0325 | 2.83 | 0.005 *** | Significantly Positive |

| H3 | CSR → FP | 0.0006 | 4.43 | 0.000 *** | Significantly Positive |

| H4 | CSR → GI → FP | 0.0001 | 2.23 | 0.026 ** | Significantly Positive |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Novitasari, M.; Tarigan, Z.J.H. The Role of Green Innovation in the Effect of Corporate Social Responsibility on Firm Performance. Economies 2022, 10, 117. https://doi.org/10.3390/economies10050117

Novitasari M, Tarigan ZJH. The Role of Green Innovation in the Effect of Corporate Social Responsibility on Firm Performance. Economies. 2022; 10(5):117. https://doi.org/10.3390/economies10050117

Chicago/Turabian StyleNovitasari, Maya, and Zeplin Jiwa Husada Tarigan. 2022. "The Role of Green Innovation in the Effect of Corporate Social Responsibility on Firm Performance" Economies 10, no. 5: 117. https://doi.org/10.3390/economies10050117

APA StyleNovitasari, M., & Tarigan, Z. J. H. (2022). The Role of Green Innovation in the Effect of Corporate Social Responsibility on Firm Performance. Economies, 10(5), 117. https://doi.org/10.3390/economies10050117