Strategic Management Accounting in Small and Medium-Sized Enterprises in Emerging Countries and Markets: A Case Study from China

Abstract

:1. Introduction

2. Literature Review

2.1. A Brief Overview of SMA

2.1.1. Current Analysis of SMA

2.1.2. The Importance of SMA

2.2. Application of SMA from the Perspective of SMEs

2.2.1. Current Use of SMA in Developing Countries

2.2.2. Defining the Connection between SMA and SMEs

2.3. Current Research of SMA Use in China

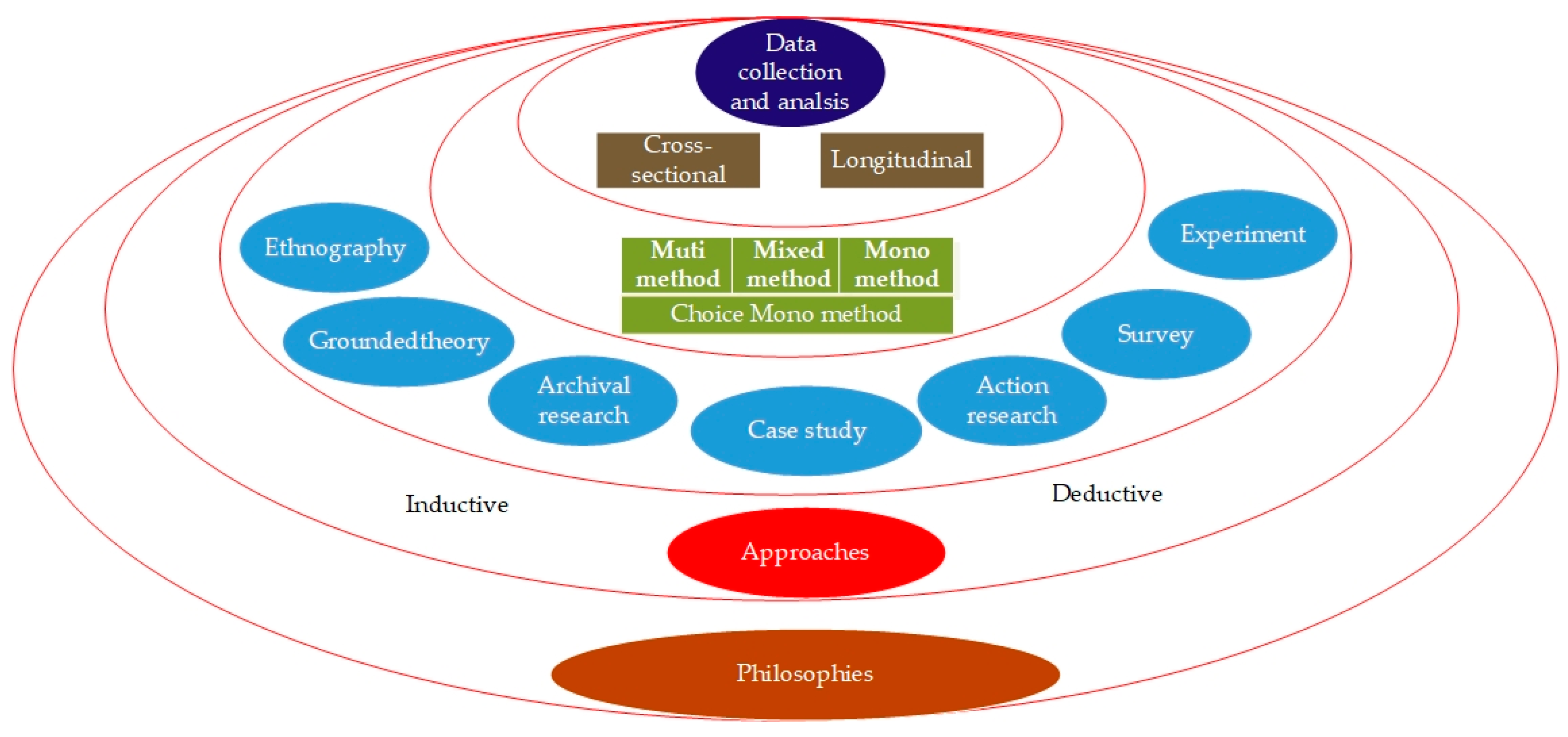

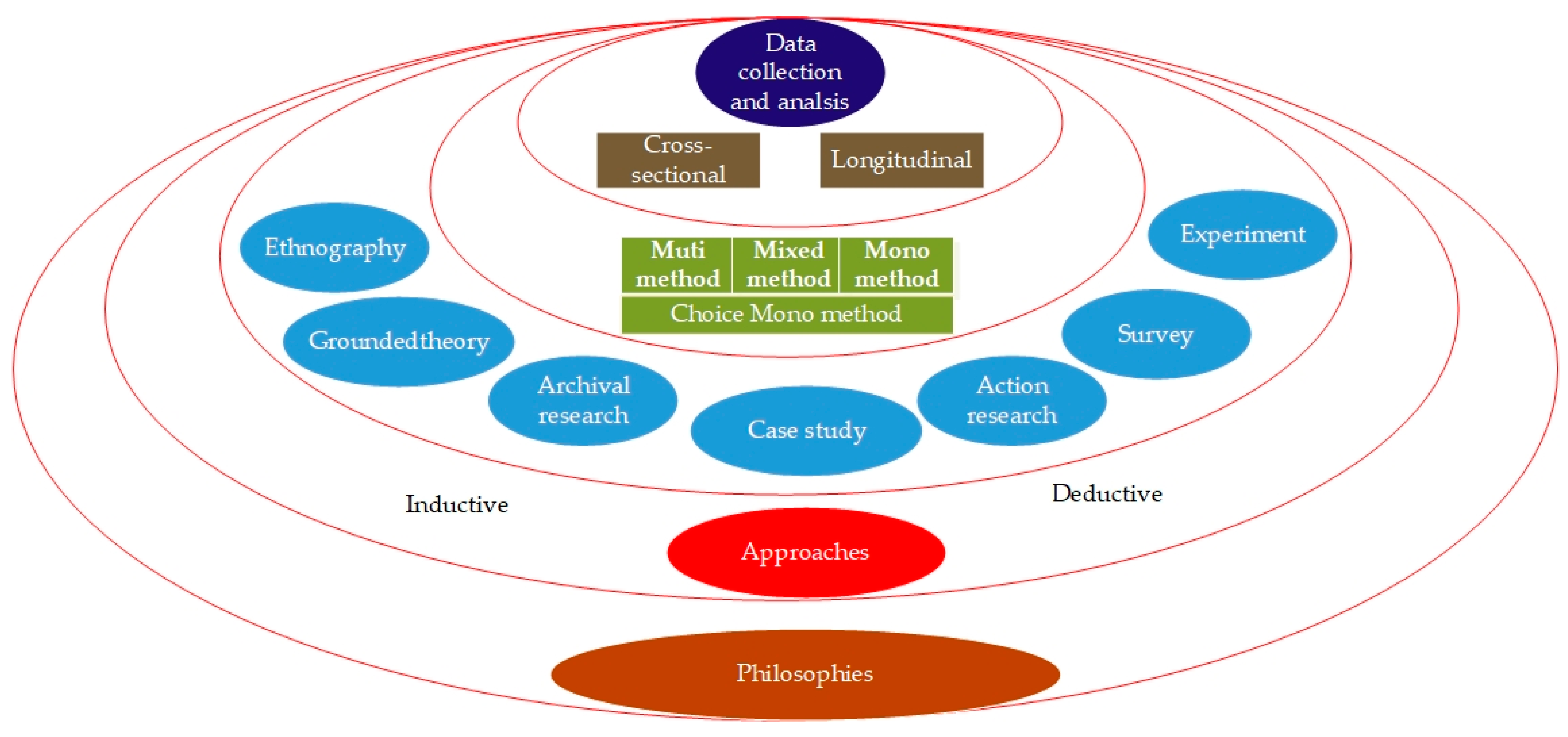

3. Methodology and Data

3.1. Philosophy—Pragmatic

3.2. Approach—Inductive

3.3. Strategy—Case Study

3.4. Choice—Mono Methods

3.5. Time Horizon—Cross-Sectional

3.6. Data Collection and Analysis

3.6.1. Questionnaires

3.6.2. Semi-Structured Interview

3.6.3. Study Design

3.6.4. Ethical Considerations

4. Findings and Discussions

4.1. Awareness of Strategic Management Accounting

4.1.1. Corporate Executives Do Not Fully Understand Accounting and Do Not Pay Attention to It

4.1.2. Corporate Executives Do Not Know SMA, and Its Role Has Not Been Fully Played

4.2. The Use of Strategic Management Accounting on Markets

4.2.1. Product Choice

4.2.2. Product Pricing

4.2.3. Suppliers

4.3. The Use of Strategic Management Accounting on Company Management

4.3.1. Performance Management

4.3.2. Department Cooperation

4.3.3. Employees’ Training

4.3.4. Corporate Cultural

5. Conclusions and Policy Implication

Supplementary Materials

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Ahrens, Thomas, and Christopher S. Chapman. 2006. Doing qualitative field research in management accounting: Positioning data to contribute to theory. Accounting, organizations and society 31: 819–41. [Google Scholar] [CrossRef]

- Alamri, Ahmad Mohammed. 2018. Association between strategic management accounting facets and organizational performance. Baltic Journal of Management 14: 212–34. [Google Scholar] [CrossRef]

- Albu, Nadia, and Cătălin Nicolae Albu. 2012. Factors Associated with the Adoption and Use of Management Accounting Techniques in Developing Countries: The Case of Romania. Journal of International Financial Management and Accounting 23: 245–76. [Google Scholar] [CrossRef]

- Ali Qalati, Sikandar, Wenyuan Li, Naveed Ahmed, Manzoor Ali Mirani, and Asadullah Khan. 2020. Examining the Factors Affecting SME Performance: The Mediating Role of Social Media Adoption. Sustainability 13: 75. [Google Scholar] [CrossRef]

- Almaryani, Majeed A. Hatif, and Hamza H. Sadik. 2012. Strategic Management Accounting Techniques in Romanian Companies: Some Survey Evidence. Procedia Economics and Finance 3: 387–96. [Google Scholar] [CrossRef] [Green Version]

- Asthana, Vinay. 2012. Strategic Management: Formulation, Implementation, and Control, 12th ed. Abhigyan: Foundation for Organisational Research & Education, vol. 30. [Google Scholar]

- Baines, Annette, and Kim Langfield-Smith. 2003. Antecedents to management accounting change: A structural equation approach. Accounting Organizations and Society 28: 675–98. [Google Scholar] [CrossRef]

- Baker, Richar, and Bruno Cohanier. 2014. What qualitative research can tell us about performance management systems. Qualitative Research in Accounting and Management 11: 380–415. [Google Scholar] [CrossRef]

- Ban, Tae Hyun, and Sin-Geun Song. 2012. The Relationship between Business Strategy, Management Innovation, Strategic Managerial Accounting System and Business Performance. Korean Accounting Journal 21: 203–36. [Google Scholar]

- Barnham, Chris. 2015. Quantitative and qualitative research: Perceptual foundations. International Journal of Market Research 57: 837–54. [Google Scholar] [CrossRef]

- Bhamu, Jaiprakash, and Kuldip Singh Sangwan. 2014. Lean manufacturing: Literature review and research issues. International Journal of Operations and Production Management 34: 876–940. [Google Scholar] [CrossRef]

- Bromwich, Michael. 1990. The case for strategic management accounting: The role of accounting information for strategy in competitive markets. Accounting, Organizations and Society 15: 27–46. [Google Scholar] [CrossRef]

- Cadez, Simon, and Chris Guilding. 2008. An exploratory investigation of an integrated contingency model of strategic management accounting. Accounting, Organizations and Society 33: 836–63. [Google Scholar] [CrossRef] [Green Version]

- Cadez, Simon, and Chris Guilding. 2012. Strategy, strategic management accounting and performance: A configurational analysis. Industrial Management and Data Systems 112: 484–501. [Google Scholar] [CrossRef] [Green Version]

- Cao, Xiaofeng. 2021. Is JIT just in time or on time production? Enterprise Management 5: 28–31. [Google Scholar] [CrossRef]

- Carlsson-Wall, Martin, Kalle Kraus, and Johnny Lind. 2015. Strategic management accounting in close inter-organisational relationships. Accounting and Business Research 45: 27–54. [Google Scholar] [CrossRef]

- Cescon, Franco, Antonio Costantini, and Luca Grassetti. 2018. Strategic choices and strategic management accounting in large manufacturing firms. Journal of Management and Governance 23: 605–36. [Google Scholar] [CrossRef]

- Chi, Renyong, Xiaomiao Mei, and Hongpeng Ruan. 2020. How do intelligent manufacturing and SME organizational change match? Studies in Science of Science 38: 1244–50. [Google Scholar] [CrossRef]

- Darabi, Fariba, Mark NK Saunders, and Murray Clark. 2020. Trust initiation and development in SME-university collaborations: Implications for enabling engaged scholarship. European Journal of Training and Development 45: 320–45. [Google Scholar] [CrossRef]

- Diabate, Ardjouman, Brou Mathias Allate, Dongping Wei, and Liying Yu. 2019. Do Firm and Entrepreneur Characteristics Play a Role in SMEs’ Sustainable Growth in a Middle-Income Economy like Côte d’Ivoire? Sustainability 11: 1557. [Google Scholar] [CrossRef] [Green Version]

- Dixon, Rob, and Smith D. D. Smith. 1993. Strategic management accounting. Omega 21: 605–18. [Google Scholar] [CrossRef]

- Emerson, Robert M., Rachel I. Fretz, and Linda L. Shaw. 1995. Writing Ethnographic Fieldnotes. Chicago: University of Chicago Press. [Google Scholar]

- Fan, Qiuyan. 2019. Cross Border e-Commerce in China: What Does This Mean to Australian Small to Medium Size Enterprises (SMEs)? Journal of Economics, Business and Management 7: 50–54. [Google Scholar] [CrossRef]

- Fong, Songjie, and Congying Chen. 2011. Strategic management accounting of social networking site service company in China. Journal of Technology Management in China 6: 125–39. [Google Scholar] [CrossRef]

- Gagne, Margaret L., and Richard Discenza. 2013. Target costing. The Journal of Business and Industrial Marketing 10: 16–22. [Google Scholar] [CrossRef]

- Girin, Jacques. 2011. Empirical Analysis of Management Situations: Elements of Theory and Method. European Management Review 8: 197–212. [Google Scholar] [CrossRef]

- Hadid, Wael, and Mahmoud Al-Sayed. 2021. Management accountants and strategic management accounting: The role of organizational culture and information systems. Management Accounting Research 50: 100725. [Google Scholar] [CrossRef]

- Helgeson, Jennifer F., Payam Aminpour, Juan F. Fung, Alfredo Roa Henriquez, Ariela Zycherman, David Butry, Claudia Nierenberg, and Yating Zhang. 2022. Natural hazards compound COVID-19 impacts on small businesses disproportionately for historically underrepresented group operators. International Journal of Disaster Risk Reduction 72: 102845. [Google Scholar] [CrossRef] [PubMed]

- Hergert, Michael, and Deigan Morris. 1989. Accounting data for value chain analysis. Strategic Management Journal 10: 175–88. [Google Scholar] [CrossRef]

- Ibragimova, A. K. 2019. Information Database of Strategic Management Accounting and Controlling. Vestnik of Voronezh State Agrarian University 12: 176–83. [Google Scholar] [CrossRef]

- Jusoh, Ruzita, and Ah Lay Tan. 2012. A business strategy, strategic role of accountant, strategic management accounting and their links to firm performance: An exploratory study of manufacturing companies in Malaysia. Asia-Pacific Management Accounting Journal 7: 59–92. [Google Scholar]

- Kaplan, Robert S., and David P. Norton. 1996. Strategic learning and the balanced scorecard. Strategy and Leadership 24: 18–24. [Google Scholar] [CrossRef]

- Kaplan, Bonnie, and Joseph A. Maxwell. 2005. Qualitative Research Methods for Evaluating Computer Information Systems. New York: Springer New York. [Google Scholar]

- Lachmann, Maik, Thorsten Knauer, and Rouven Trapp. 2013. Strategic management accounting practices in hospitals. Journal of Accounting and Organizational Change 9: 336–69. [Google Scholar] [CrossRef]

- Langfield-Smith, Kim, and L. Parker. 2008. Strategic management accounting: How far have we come in 25 years? Accounting, Auditing and Accountability Journal 21: 204–28. [Google Scholar] [CrossRef]

- Laurinkevičiūtė, Asta, and Žaneta Stasiškienė. 2011. SMS for decision making of SMEs. Clean Technologies and Environmental Policy 13: 797–807. [Google Scholar] [CrossRef]

- Lavia López, Oro, and Martin R. W. Hiebl. 2014. Management Accounting in Small and Medium-Sized Enterprises: Current Knowledge and Avenues for Further Research. Journal of Management Accounting Research 27: 81–119. [Google Scholar] [CrossRef]

- Le, Thanh Tiep, and Muhammad Ikram. 2022. Do sustainability innovation and firm competitiveness help improve firm performance? Evidence from the SME sector in Vietnam. Sustainable Production and Consumption 29: 588–99. [Google Scholar] [CrossRef]

- Leonidou, Leonidas C., Dayananda Palihawadana, Bilge Aykol, and Paul Christodoulides. 2022. Effective Small and Medium-Sized Enterprise Import Strategy: Its Drivers, Moderators, and Outcomes. Journal of International Marketing 30: 18–39. [Google Scholar] [CrossRef]

- Li, Renling. 2015. Analysis on the application and characteristics of strategic management in small and medium-sized enterprises. Modern Economic Information 3: 107–08. [Google Scholar]

- Li, Gongjun. 2019. Innovative application of strategic management accounting in private enterprises. Commercial Accounting 5: 58–66. [Google Scholar]

- Li, Lin, and Zan Guo. 2020. Analysis of the Quality Evaluation Standard of Labor Relations of Private SMEs: A Perspective Based on Decent Work. Journal of Macro-Quality Research 8: 48–56. [Google Scholar] [CrossRef]

- Marriott, Neil, and Pru Marriott. 2000. Professional accountants and the development of a management accounting service for the small firm: Barriers and possibilities. Management Accounting Research 11: 475–92. [Google Scholar] [CrossRef]

- McLachlin, Ron. 1997. Management initiatives and just on-time manufacturing. Journal of Operations Management 15: 271–92. [Google Scholar] [CrossRef]

- Mitchell, Falconer, and Gavin C. Reid. 2000. Problems, challenges and opportunities: The small business as a setting for management accounting research. Management Accounting Research 11: 385–90. [Google Scholar] [CrossRef] [Green Version]

- Müller, Julian M., Oana Buliga, and Kai-Ingo Voigt. 2021. The role of absorptive capacity and innovation strategy in the design of industry 4.0 business Models—A comparison between SMEs and large enterprises. European Management Journal 39: 333–43. [Google Scholar] [CrossRef]

- Nguyen, Hung Quoc, and Oanh Thi Tu Le. 2020. Factors Affecting the Intention to Apply Management Accounting in Enterprises in Vietnam. Journal of Asian Finance Economics and Business 7: 95–107. [Google Scholar] [CrossRef]

- Nguyen, Thieu Manh, and Thanh Thi Nguyen. 2021. The Application of Strategic Management Accounting: Evidence from the Consumer Goods Industry in Vietnam. The Journal of Asian Finance, Economics and Business 8: 139–46. [Google Scholar]

- Nguyen, Phuong Anh, Thuy Anh Tram Uong, and Quang Dung Nguyen. 2020. How Small- and Medium-Sized Enterprise Innovation Affects Credit Accessibility: The Case of Vietnam. Sustainability 12: 9559. [Google Scholar] [CrossRef]

- Nixon, Bill, and John Burns. 2012. The paradox of strategic management accounting. Management Accounting Research 23: 229–44. [Google Scholar] [CrossRef]

- Noordin, Raman, Yuserrie Zainuddin, and Michael Tayles. 2009. Strategic management accounting information elements: Malaysian evidence. Asia-Pacific Management Accounting Journal 4: 17–34. [Google Scholar]

- Oboh, Collins S., and Solabomi O. Ajibolade. 2017. Strategic management accounting and decision making: A survey of the Nigerian Banks. Future Business Journal 3: 119–37. [Google Scholar] [CrossRef]

- OECD. 2019. OECD SME and Entrepreneurship Outlook 2019. Paris: OECD. [Google Scholar] [CrossRef]

- Parker, Lee D. 2012. Qualitative management accounting research: Assessing deliverables and relevance. Critical Perspectives on Accounting 23: 54–70. [Google Scholar] [CrossRef]

- Pavlatos, Odysseas, and Xara Kostakis. 2018. The impact of top management team characteristics and historical financial performance on strategic management accounting. Journal of Accounting and Organizational Change 14: 455–72. [Google Scholar] [CrossRef]

- Petera, Petr, and Libuše Šoljaková. 2019. Use of strategic management accounting techniques by companies in the Czech Republic. Economic Research-Ekonomska Istraživanja 33: 46–67. [Google Scholar] [CrossRef]

- Powell, Tim. 2001. The Knowledge Value Chain (KVC): How to Fix It When It Breaks. National Online. Medford: Information Today, Inc. [Google Scholar]

- Quinn, Martin. 2011. Routines in management accounting research: Further exploration. Journal of Accounting and Organizational Change 7: 337–57. [Google Scholar] [CrossRef] [Green Version]

- Richards, Lyn. 1999. Using NVivo in Qualitative Research. Thousand Oaks: Sage Publications. [Google Scholar]

- Rigby, Darrell, and Barbara Bilodeau. 2015. Management Tools and Trends 2015. London: Bain & Company, Available online: https://www.bain.com/insights/management-tools-and-trends (accessed on 2 August 2015).

- Rosavina, Monica, Raden Aswin Rahadi, Mandra Lazuardi Kitri, Shimaditya Nuraeni, and Lidia Mayangsari. 2019. P2P lending adoption by SMEs in Indonesia. Qualitative Research in Financial Markets 11: 260–79. [Google Scholar] [CrossRef]

- Roslender, Robin, and Susan J. Hart. 2003. In search of strategic management accounting: Theoretical and field study perspectives. Management Accounting Research 14: 255–79. [Google Scholar] [CrossRef]

- Roslender, Robin, and Susan J. Hart. 2010. Strategic Management Accounting: Lots in a Name? Accountancy Discussion Papers 1005: 1–27. [Google Scholar]

- Saunders, Mark N. K., Philip Lewis, and Adrian Thornhill. 2012. Research Methods for Business Students, 6th ed. New York: Prentice Hall Financial Times. [Google Scholar]

- Shi, Wenquan. 2021. Analyzing enterprise asset structure and profitability using cloud computing and strategic management accounting. PLoS ONE 16: e0257826. [Google Scholar] [CrossRef] [PubMed]

- Simmonds, Kenneth. 1982. Strategic Management Accounting for Pricing: A Case Example. Accounting and Business Research 12: 206–14. [Google Scholar] [CrossRef]

- Singh, Rajesh K., Suresh K. Garg, and S. G. Deshmukh. 2008. Strategy development by SMEs for competitiveness: A review. Benchmarking 15: 525–47. [Google Scholar] [CrossRef]

- Sogunro, Olusegun A. 2002. Selecting a quantitative or qualitative research methodology: An experience. Educational Research Quarterly 26: 3. [Google Scholar]

- Teerasoponpong, Siravat, and Apichat Sopadang. 2022. Decision support system for adaptive sourcing and inventory management in small- and medium-sized enterprises. Robotics and Computer-Integrated Manufacturing 73: 102226. [Google Scholar] [CrossRef]

- Tian, Jinfang, Wei Cao, Qian Cheng, Yikun Huang, and Shiyang Hu. 2022. Corporate Competing Culture and Environmental Investment. Frontiers in Psychology 12: 774173. [Google Scholar] [CrossRef] [PubMed]

- Tong, Li Zhong, Jindan Wang, and Zhongmin Pu. 2022. Sustainable supplier selection for SMEs based on an extended PROMETHEE II approach. Journal of Cleaner Production 330: 129830. [Google Scholar] [CrossRef]

- Tuan, Tran Trung. 2020. The Impact of Balanced Scorecard on Performance: The Case of Vietnamese Commercial Banks. The Journal of Asian Finance, Economics and Business 7: 71–79. [Google Scholar] [CrossRef]

- Turner, Michael J., Sean A. Way, Demian Hodari, and Wiarda Witteman. 2017. Hotel property performance: The role of strategic management accounting. International Journal of Hospitality Management 63: 33–43. [Google Scholar] [CrossRef]

- Vu, Thi Kim Anh, Bich Ha Dam, and Thi Thuy Van Ha. 2022. Factors Affecting the Application of Strategy Management Accounting in Vietnamese Logistics Enterprises. Journal of Distribution Science 20: 27–39. [Google Scholar]

- Wang, Baso. 2021. Characteristics and Development Strategy Choice of Small and Medium-sized Enterprises in China. Journal of Hanjiang Normal University 41: 37–42. [Google Scholar]

- Wang, Meng, and Wenggi Zhang. 2016. Some financing characteristics and countermeasures under the new normal. Economic Review Journal 2: 56–59. [Google Scholar]

- Ward, Megan, and David Mowat. 2012. Creating an organizational culture for evidence-informed decision making. Healthy Manage Forum 25: 146–50. [Google Scholar] [CrossRef]

- Wisner, Priscilla S. 2001. The Impact of Work Teams on Performance: A quasi-experimental field study. Advances in Management Accounting 10: 1–28. [Google Scholar]

- Zhang, Conghui, Le Zhang, and Weihua Su. 2020. Cross-border e-commerce talent demand analysis based on the perspective of small and medium enterprises. The World of Survey and Research 7: 12–17. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

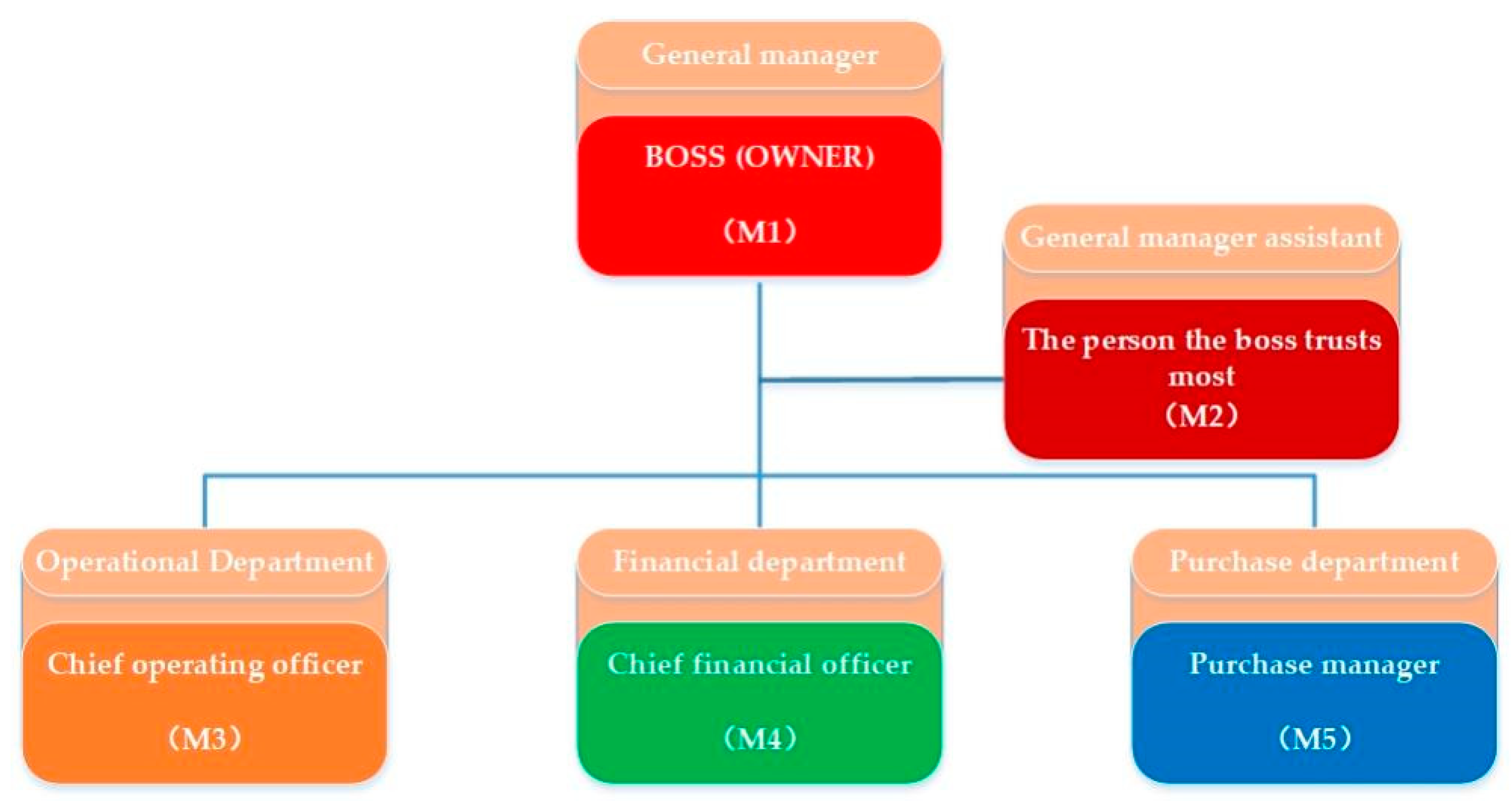

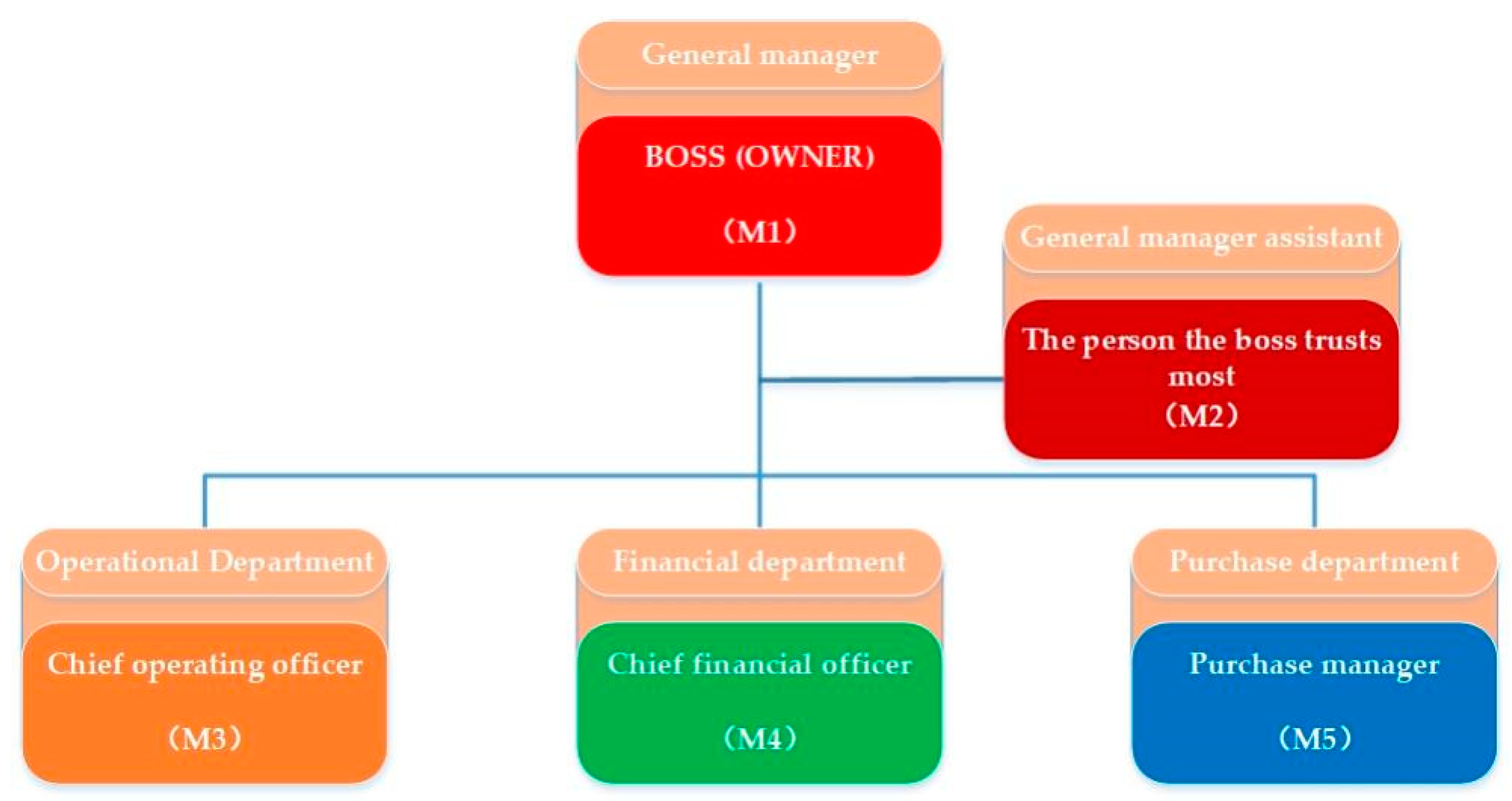

| Interviewee ID | Role and Department | Date | Duration | Formation |

|---|---|---|---|---|

| M1 | General manager (boss) | 13 August 2020 | 55 min | Face-to-face |

| M2 | General manager assistant | 14 August 2020 | 81 min | Face-to-face |

| M3 | Chief operating officer (Operational Department) | 15 August 2020 | 45 min | Face-to-face |

| M4 | CFO (Financial department) | 15 August 2020 | 58 min | Face-to-face |

| M5 | Purchase manager (purchase department) | 16 August 2020 | 40 min | Face-to-face |

| M6 | CFO assistant | 8 March 2020 | 30 min | Video communication through wechat |

| E1 | Group leader Worked for one year (operating department) | 17 August 2020 | 35 min | Face-to-face |

| E2 | Employee Worked for half a year | 17 August 2020 | 25 min | Face-to-face |

| E3 | Employee (Purchase department) Worked for 2 years | 8 March 2020 | 25 min | Video communication through wechat |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Ma, L.; Chen, X.; Zhou, J.; Aldieri, L. Strategic Management Accounting in Small and Medium-Sized Enterprises in Emerging Countries and Markets: A Case Study from China. Economies 2022, 10, 74. https://doi.org/10.3390/economies10040074

Ma L, Chen X, Zhou J, Aldieri L. Strategic Management Accounting in Small and Medium-Sized Enterprises in Emerging Countries and Markets: A Case Study from China. Economies. 2022; 10(4):74. https://doi.org/10.3390/economies10040074

Chicago/Turabian StyleMa, Lindong, Xihui Chen, Jiawen Zhou, and Luigi Aldieri. 2022. "Strategic Management Accounting in Small and Medium-Sized Enterprises in Emerging Countries and Markets: A Case Study from China" Economies 10, no. 4: 74. https://doi.org/10.3390/economies10040074

APA StyleMa, L., Chen, X., Zhou, J., & Aldieri, L. (2022). Strategic Management Accounting in Small and Medium-Sized Enterprises in Emerging Countries and Markets: A Case Study from China. Economies, 10(4), 74. https://doi.org/10.3390/economies10040074