The Dynamics of the Profitability and Growth of Restaurants; The Case of Norway

Abstract

:1. Introduction

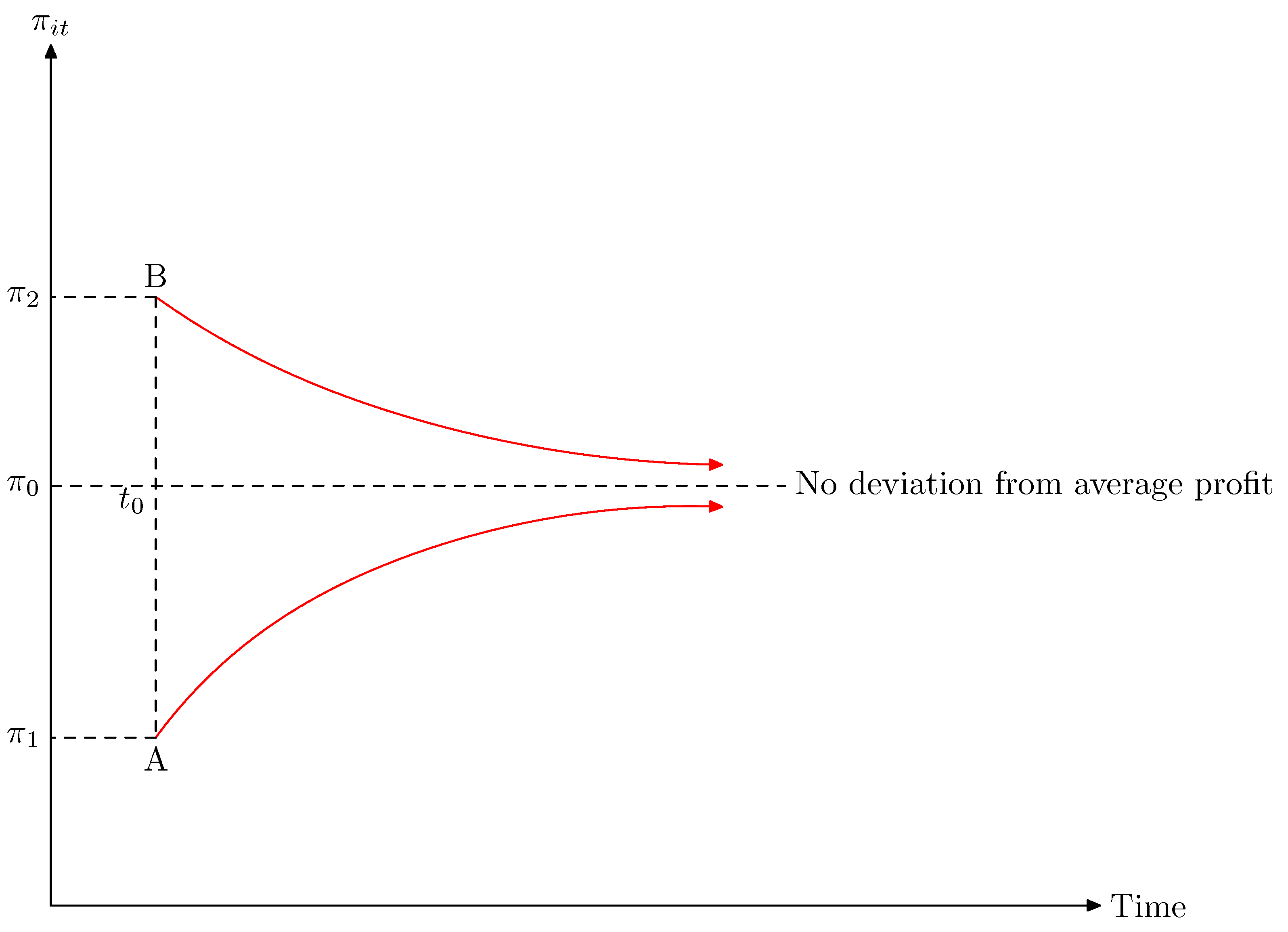

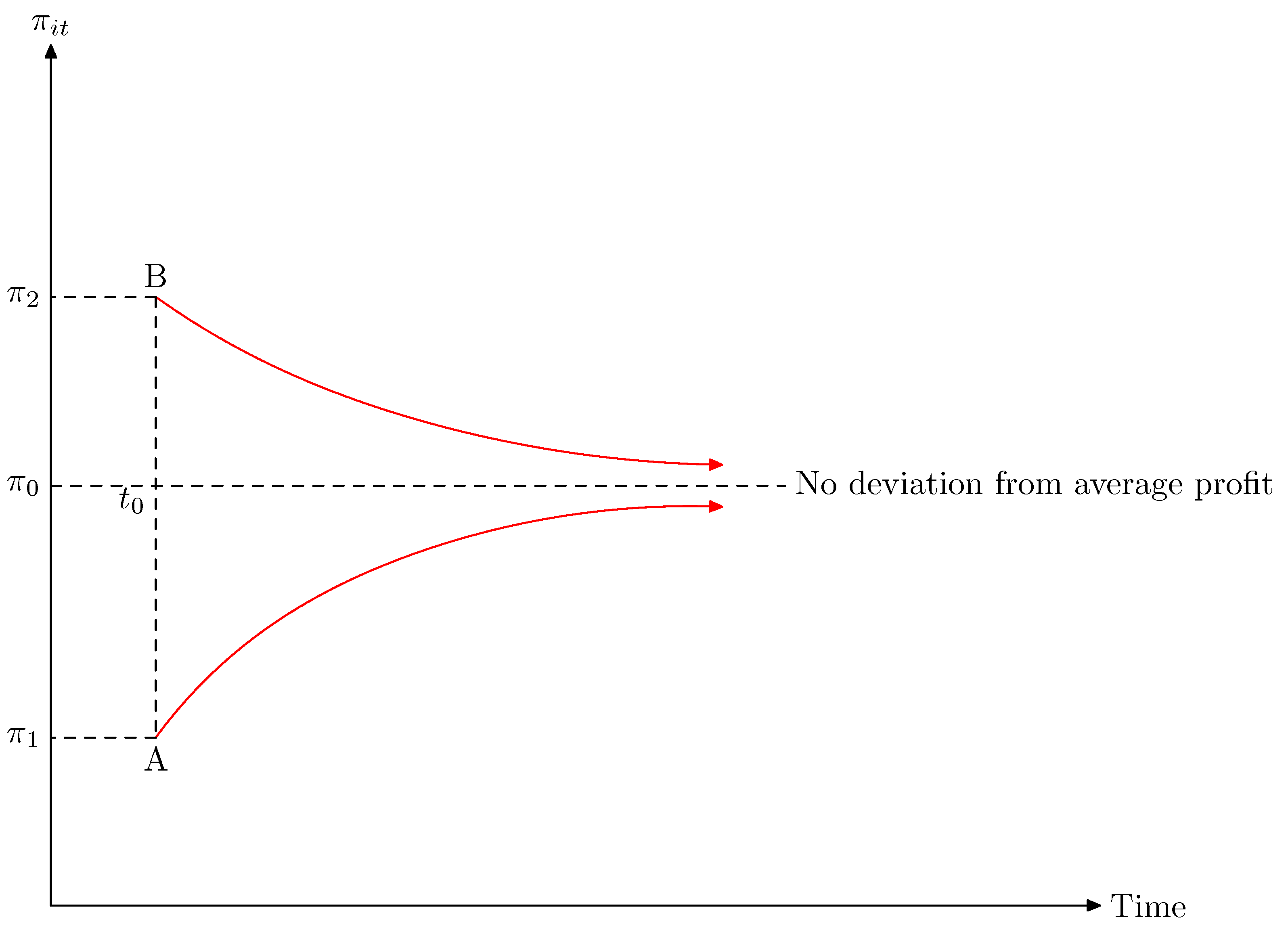

2. Profitability and Degree of Profit Persistence—Theory and Literature Review

3. Law of Proportionate Effect (LPE)

Profit Rate and Growth

4. Methodology and Data

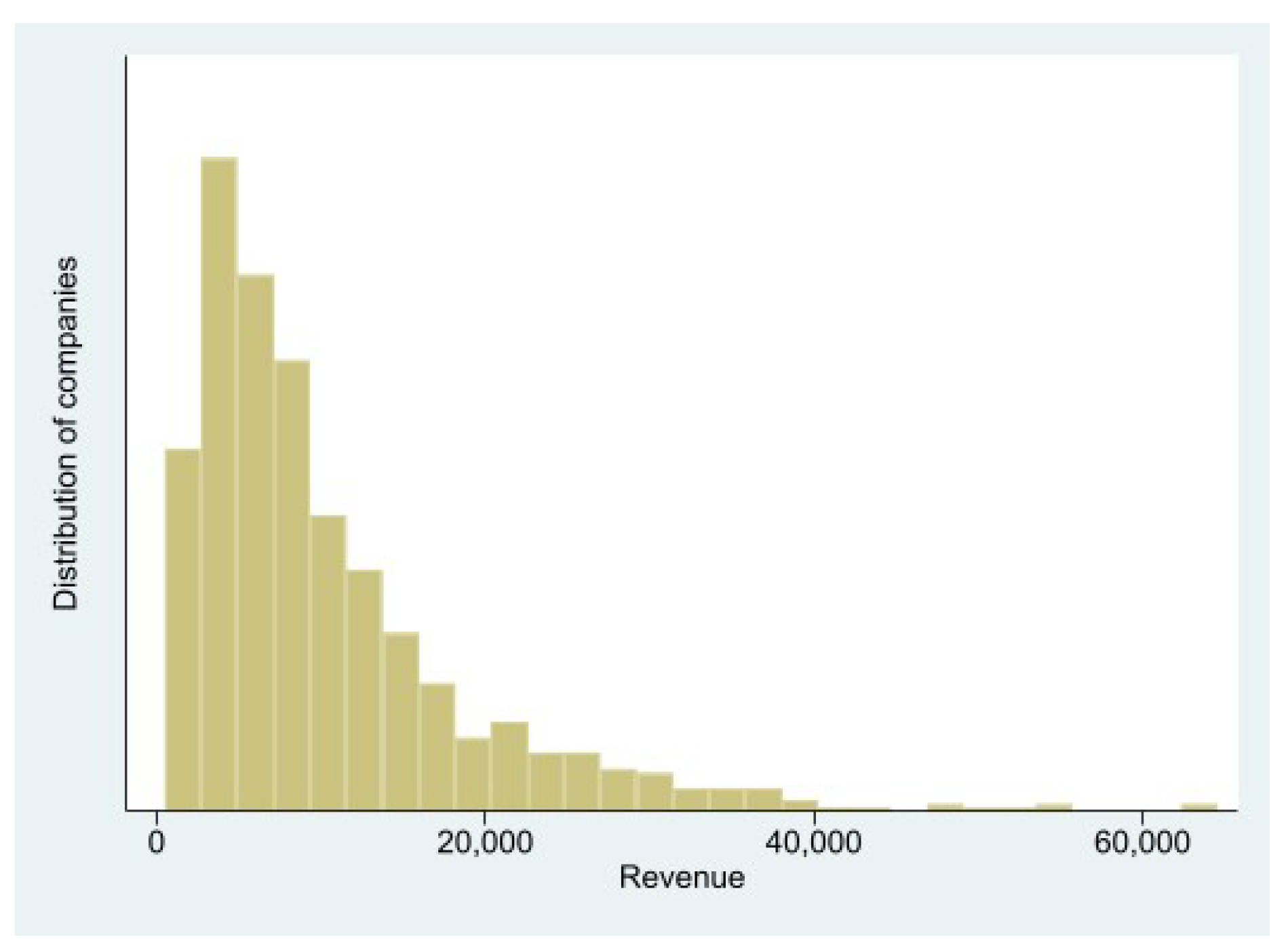

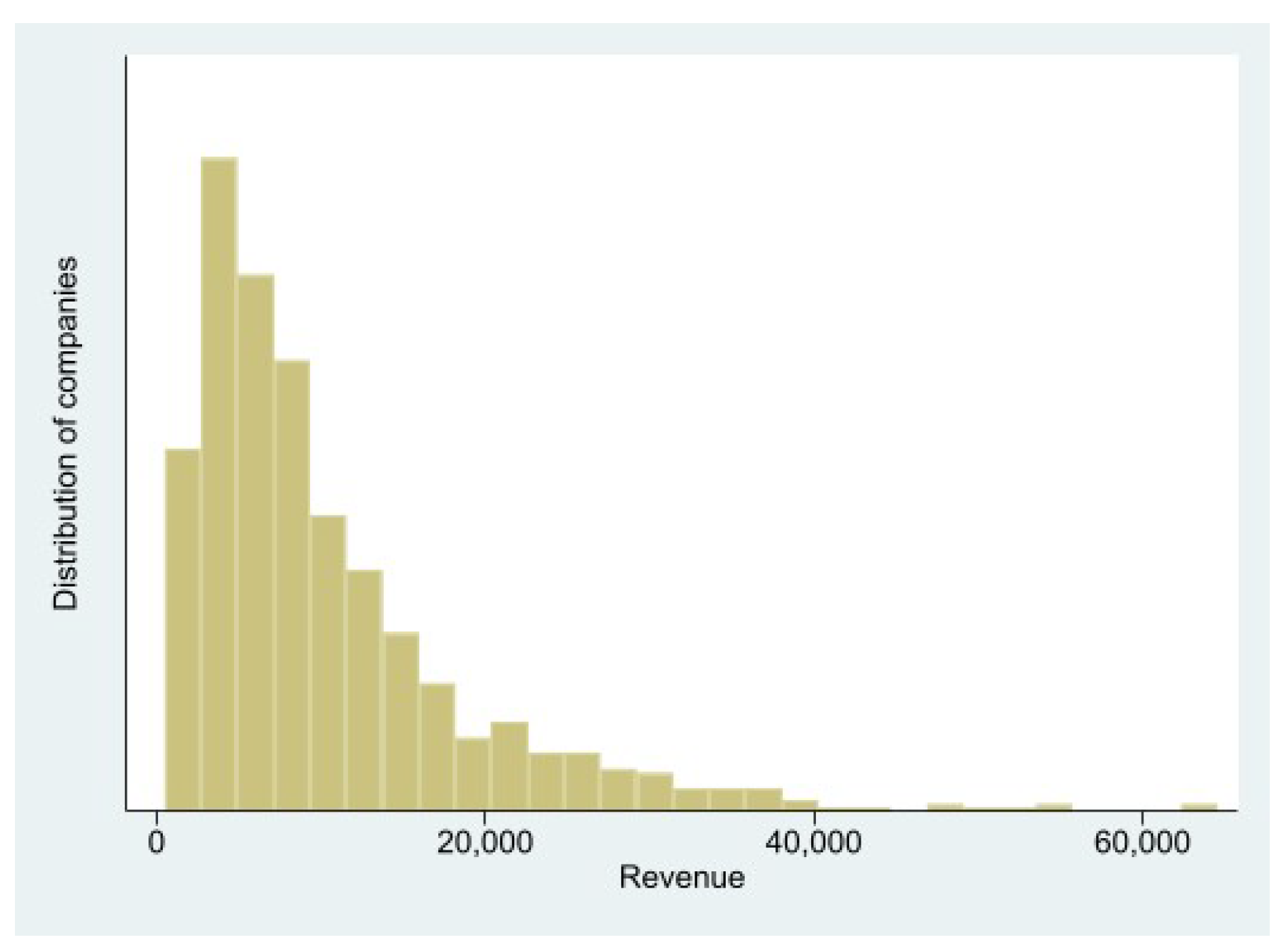

The Sample

5. The Models

6. Findings

7. Discussion

7.1. Profitability and Degree of Profit Persistence (PoP) (Hypotheses 1–5)

7.2. Law of Proportionate Effect (LPE) (Hypotheses 5–6)

7.3. Profit Rate and Growth (Hypotheses 7–8)

8. Limitations

9. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Abrigo, Michael R. M., and Inessa Love. 2016. Estimation of panel vector autoregression in stata. The Sage Journal 16: 778–804. [Google Scholar] [CrossRef] [Green Version]

- Ali, Anis, and Shaha Faisal. 2020. Capital structure and financial performance: A case of Saudi petrochemical industry. Journal of Asian Finance, Economics, and Business 7: 105–12. [Google Scholar] [CrossRef]

- Audretsch, David B., Luuk Klomp, Enrico Santarelli, and A. Roy Thurik. 2004. Gibrat’s Law: Are the services different? Review of Industrial Organization 24: 301–24. [Google Scholar] [CrossRef] [Green Version]

- Baños-Caballero, Sonia, Pedro J. García-Teruel, and Pedro Martínez-Solano. 2014. Working capital management, corporate performance, and financial constraints. Journal of Business Research 67: 332–38. [Google Scholar] [CrossRef]

- Bartoloni, Eleanora, and Maurizio Baussola. 2009. The persistence of profits, sectoral heterogeneity and firms’ characteristics. International Journal of the Economics of Business 16: 87–111. [Google Scholar] [CrossRef]

- Bentzen, Jan, Erik Madsen, and Valdemar Smith. 2012. Do firms’ growth rates depend on firm size? Small Business Economics 39: 937–47. [Google Scholar] [CrossRef]

- Bhangu, Parneet Kaur. 2020. Persistence of profitability in top firms: Does it vary across sectors? Competitiveness Review: An International Business Journal 30: 269–87. [Google Scholar] [CrossRef]

- Binder, Michael, Cheng Hsiao, and M. Hashem Pesaran. 2005. Estimation and inference in short panel vector autoregressions with unit roots and cointegration. Econometric Theory 21: 795–837. [Google Scholar] [CrossRef] [Green Version]

- Blundell, Richard, and Stephen Bond. 1998. Initial conditions and moment restrictions in dynamic panel data models. Journal of Econometrics 87: 115–43. [Google Scholar] [CrossRef] [Green Version]

- Cable, John R., and Dennis C. Mueller. 2008. Testing for persistence of profits’ differences across firms. International Journal of the Economics of Business 15: 201–28. [Google Scholar] [CrossRef]

- Cantele, Silvia, and Fabio Cassia. 2020. Sustainability implementation in restaurants: A comprehensive model of drivers, barriers, and competitiveness-mediated effects on firm performance. International Journal of Hospitality Management 87: 102510. [Google Scholar] [CrossRef]

- Cowling, Marc. 2004. The Growth—Profit Nexus. Small Business Economics 22: 1–9. [Google Scholar] [CrossRef]

- Deszczynski, Bartosz. 2021. Firm Competitive Advantage Through Relationship Management. Cham: Springer Nature Switzerland AG. [Google Scholar] [CrossRef]

- Dinh, Hung The, and Cuong Duc Pham. 2020. The effect of capital structure on financial performance of Vietnamese listing pharmaceutical enterprises. Journal of Asian Finance, Economics, and Business 7: 329–40. [Google Scholar] [CrossRef]

- Enqvist, Julius, Michael Graham, and Jussi Nikkinen. 2014. The impact of working capital management on firm profitability in different business cycles: Evidence from Finland. Research in International Business and Finance 32: 36–49. [Google Scholar] [CrossRef]

- Federico, Juan S., and Joan-Lluis Capelleras. 2015. The heterogeneous dynamics between growth and profits: The case of young firms. Small Business Economics 44: 231–53. [Google Scholar] [CrossRef]

- Fitzsimmons, Jason R., Paul Steffens, and Evan J. Douglas. 2005. Growth and profitability in small and medium sized Australian firms. Paper presented at AGSE Entrepreneurship Exchange, Conference, Melbourne, Australia, February 1–4. [Google Scholar]

- García-Teruel, Pedro Juan, and Pedro Martínez-Solano. 2007. Effects of working capital management on SME profitability. International Journal of Managerial Finance 3: 164–77. [Google Scholar] [CrossRef]

- Gibrat, Robert. 1931. Les inégalits économiques. Paris: Sirey. [Google Scholar]

- Giotopoulos, Joannis. 2014. Dynamics of firm profitability and growth: Do knowledge-intensive (business) services persistently outperform? International Journal of the Economics of Business 21: 291–319. [Google Scholar] [CrossRef]

- Goddard, John, Phil Molyneux, and John O. S. Wilson. 2004. Dynamics of growth and profitability in banking. Journal of Money, Credit and Banking 36: 1069–90. [Google Scholar] [CrossRef]

- Gschwandtner, Adelina, and Stefan Hirsch. 2018. What drives firm profitability? A comparison of the US and EU food processing industry. The Manchester School 86: 390–416. [Google Scholar] [CrossRef] [Green Version]

- Hirsch, Stefan, and Adelina Gschwandtner. 2013. Profit persistence in the food industry: Evidence from five European countries. European Review of Agricultural Economics 40: 741–59. [Google Scholar] [CrossRef] [Green Version]

- Hirsch, Stefan, David Lanter, and Robert Finger. 2021. Profitability and profit persistence in EU food retailing: Differences between top competitors and fringe firms. Agribusiness 37: 235–63. [Google Scholar] [CrossRef]

- Hirsch, Stefan. 2018. Successful in the long run: A meta-regression analysis of persistent firm profits. Journal of Economic Surveys 32: 23–49. [Google Scholar] [CrossRef]

- Holtz-Eakin, Douglas, Whitney Newey, and Harvey S. Rosen. 1988. Estimating Vector Autoregressions with Panel Data. Econometrica 56: 1371–95. [Google Scholar] [CrossRef]

- Jang, SooCheong (Shawn), and Kwangmin Park. 2011. Inter-relationship between firm growth and profitability. International Journal of Hospitality Management 30: 1027–35. [Google Scholar] [CrossRef]

- Kim, Eojina, Juan Luis Nicolau, and Liang (Rebecca) Tang. 2021. The Impact of Restaurant Innovativeness on Consumer Loyalty: The Mediating Role of Perceived Quality. Journal of Hospitality & Tourism Research 45: 1464–88. [Google Scholar] [CrossRef]

- Lepak, David P., Ken G. Smith, and M. Susan Taylor. 2007. Value Creation and Value Capture. A Multilevel Perspective. Academy of Management Review 2: 180–94. [Google Scholar] [CrossRef] [Green Version]

- Madhok, Anoop, Sali Li, and Richard L. Priem. 2010. The resource-based view revisited: Comparative firm advantage, willingness-based isolating mechanisms and competitive heterogeneity. European Management Review 7: 91–100. [Google Scholar] [CrossRef]

- Markman, Gideon D., and William B. Gartner. 2002. Is extraordinary growth profitable? A study of Inc. 500 high–growth companies. Entrepreneurship Theory and Practice 27: 65–75. [Google Scholar] [CrossRef]

- Mazur, Karolina. 2013. Isolating mechanisms as sustainability factors of resource-based competitive advantage. Management 17: 31. [Google Scholar] [CrossRef] [Green Version]

- Morettini, Lucio, Bianca Potì, and Roberto Gabriele. 2020. Persistent fast growth and profitability (CNR-IRCrES Working Paper 10/2020). Istituto di Ricerca sulla Crescita Economica Sostenibile. Available online: http://dx.doi.org/10.23760/2421-7158.2020.010 (accessed on 16 January 2022).

- Mueller, Dennis C. 1986. Profits in the Long Run. Cambridge: Cambridge University Press. [Google Scholar]

- Muller, Emmanuel, and Andrea Zenker. 2001. Business services as actors of knowledge transformation: The role of KIBS in regional and national innovation systems. Research Policy 30: 1501–16. [Google Scholar] [CrossRef]

- Mun, Sung Gyun, and SooCheong (Shawn) Jang. 2015. Working capital, cash holding, and profitability of restaurant firms. International Journal of Hospitality Management 48: 1–11. [Google Scholar] [CrossRef]

- Nguyen, Hieu Thanh, and Anh Huu Nguyen. 2020. The impact of capital structure on firm performance: Evidence from Vietnam. Journal of Asian Finance, Economics, and Business 7: 97–105. [Google Scholar] [CrossRef]

- Nunes, Paulo J. Maçãs, Zélia M. Serrasqueiro, and Tiego N. Sequeira. 2009. Profitability in Portuguese service industries: A panel data approach. The Service Industries Journal 29: 693–707. [Google Scholar] [CrossRef]

- Opstad, Leiv, Johannes Idsø, and Robin Valenta. 2021. The degree of profit persistence in tourism industry. The case of Norwegian campsites. International Journal of Economics and Business Administration 9: 140–55. [Google Scholar] [CrossRef]

- Rumelt, Richard P. 1984. Towards a strategic theory of the firm. Competitive Strategic Management 26: 556–70. [Google Scholar]

- Severt, Kimberly, Yeon Ho Shin, Hsiangting Shatina Chen, and Robin P. DiPietro. 2020. Measuring the Relationships between Corporate Social Responsibility, Perceived Quality, Price Fairness, Satisfaction, and Conative Loyalty in the Context of Local Food Restaurants. International Journal of Hospitality & Tourism Administration, 1–23. [Google Scholar] [CrossRef]

- Skalpe, Ole. 2003. Hotels and restaurants—Are the risks rewarded? Evidence from Norway. Tourism Management 24: 623–34. [Google Scholar] [CrossRef]

- Tschoegl, Adrian E. 1983. Size, growth, and transnationality among the world’s largest banks. Journal of Business 56: 187–201. [Google Scholar] [CrossRef]

- Valenta, Robin, Johannes Idsø, and Leiv Opstad. 2021. Evidence of a Threshold Size for Norwegian Campsites and Its Dynamic Growth Process Implications—Does Gibrat’s Law Hold? Economies 9: 175. [Google Scholar] [CrossRef]

- Van Veldhoven, Ziboud, Paulien Aerts, Sanne Lies Ausloos, Jente Bernaerts, and Jan Vanthienen. 2021. The Impact of Online Delivery Services on the Financial Performance of Restaurants. Paper presented at 7th International Conference on Information Management, London, UK, March 27–29; pp. 13–17. [Google Scholar] [CrossRef]

- Yadav, Inder Sekhar, Debasis Pahi, and Rajesh Gangakhedkar. 2021. The nexus between firm size, growth and profitability: New panel data evidence from Asia–Pacific markets. European Journal of Management and Business Economics. Volume and page ahead-of-print. [Google Scholar] [CrossRef]

- Yoon, Eunju, and SooCheong Jang. 2005. The effect of financial leverage on profitability and risk of restaurant firms. The Journal of Hospitality Financial Management 13: 35–47. [Google Scholar] [CrossRef] [Green Version]

{kind=link}

{kind=link}

| Variable | Mean | St. Dev. | Min | Max |

|---|---|---|---|---|

| Revenue (1) | 11,096 | 14,150 | 496 | 287,973 |

| Profit rate | 0.0378 | 0.0644 | −0.347 | 0.367 |

| Market share | 0.0013 | 0.0021 | 0.000 | 0.052 |

| Growth rate (2) | 0.0657 | 0.1185 | −0.128 | 0.910 |

| Debt rate (3) | 0.2947 | 0.2021 | 0.071 | 1.642 |

| Working capital (4) | 0.0173 | 0.1585 | −1.302 | 1.810 |

| Salary rate (3) | 0.3738 | 0.0762 | 0.0427 | 0.6072 |

| Employees | 17.55 | 14.09 | 1 | 95 |

| Variable | Model 1 | Model 2 | Model 3 |

|---|---|---|---|

| Profit Deviation | Profit Deviation | Profit Deviation | |

| Equation (2) | Equation (6) without Salary | Equation (6) | |

| Profit rate | 0.247 *** | 0.258 *** | 0.150 ** |

| dev. | (0.0125) | (0.0122) | (0.0090) |

| Growth rate | 0.620 *** | 0.368 *** | |

| (0.0461) | (0.0341) | ||

| Market share | −12.202 * | −17.693 *** | |

| (6.2129) | (4.5794) | ||

| Debt ratio | −1.499 *** | −1.371 ** | |

| (0.1250) | (0.0922) | ||

| Working | 1.349 *** | 0.879 *** | |

| capital | (0.1509) | (0.1114) | |

| Salary rate | −17.441 *** | ||

| (0.2769) | |||

| Constant | −0.259 *** | 0.127 *** | 6.650 *** |

| (0.0136) | (0.1299) | (0.1078) | |

| No. of firms (N) | 866 | 866 | 866 |

| Variable | Model 4 | Model 5 |

|---|---|---|

| LPE, Equation (3) | LPE, Equations (3) and (4) | |

| Revenue | 0.688 *** | 0.789 *** |

| (0.0146) | (0.0156) | |

| Deviation from trend | 0.042 *** | |

| (0.0119) | ||

| Constant | 2.811 *** | 1.903 *** |

| (0.1299) | (0.1392) | |

| No. of firms (N) | 866 | 866 |

| Hypotheses 7–8 | Model 6 | Model 6 |

|---|---|---|

| Variables | L.revenue | Profrate |

| L.revenue (t − 1) | 0.584 *** | −0.069 *** |

| (0.0276) | (0.0109) | |

| Profrate (t − 1) | −0.087 | 0.337 *** |

| (0.0736) | (0.0303) | |

| No. of firms (N) | 866 | 866 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Opstad, L.; Idsø, J.; Valenta, R. The Dynamics of the Profitability and Growth of Restaurants; The Case of Norway. Economies 2022, 10, 53. https://doi.org/10.3390/economies10020053

Opstad L, Idsø J, Valenta R. The Dynamics of the Profitability and Growth of Restaurants; The Case of Norway. Economies. 2022; 10(2):53. https://doi.org/10.3390/economies10020053

Chicago/Turabian StyleOpstad, Leiv, Johannes Idsø, and Robin Valenta. 2022. "The Dynamics of the Profitability and Growth of Restaurants; The Case of Norway" Economies 10, no. 2: 53. https://doi.org/10.3390/economies10020053

APA StyleOpstad, L., Idsø, J., & Valenta, R. (2022). The Dynamics of the Profitability and Growth of Restaurants; The Case of Norway. Economies, 10(2), 53. https://doi.org/10.3390/economies10020053