The Impact of Oil Price and Oil Volatility Index (OVX) on the Exchange Rate in Sub-Saharan Africa: Evidence from Oil Importing/Exporting Countries

Abstract

1. Introduction

2. Literature Review

2.1. Theoretical Background

2.2. Empirical Evidence

2.2.1. Developed Countries

2.2.2. Developing Countries (Africa)

2.2.3. Asymmetric Effects of Oil Prices

2.2.4. Justification for QR Model

3. Data and Methodology

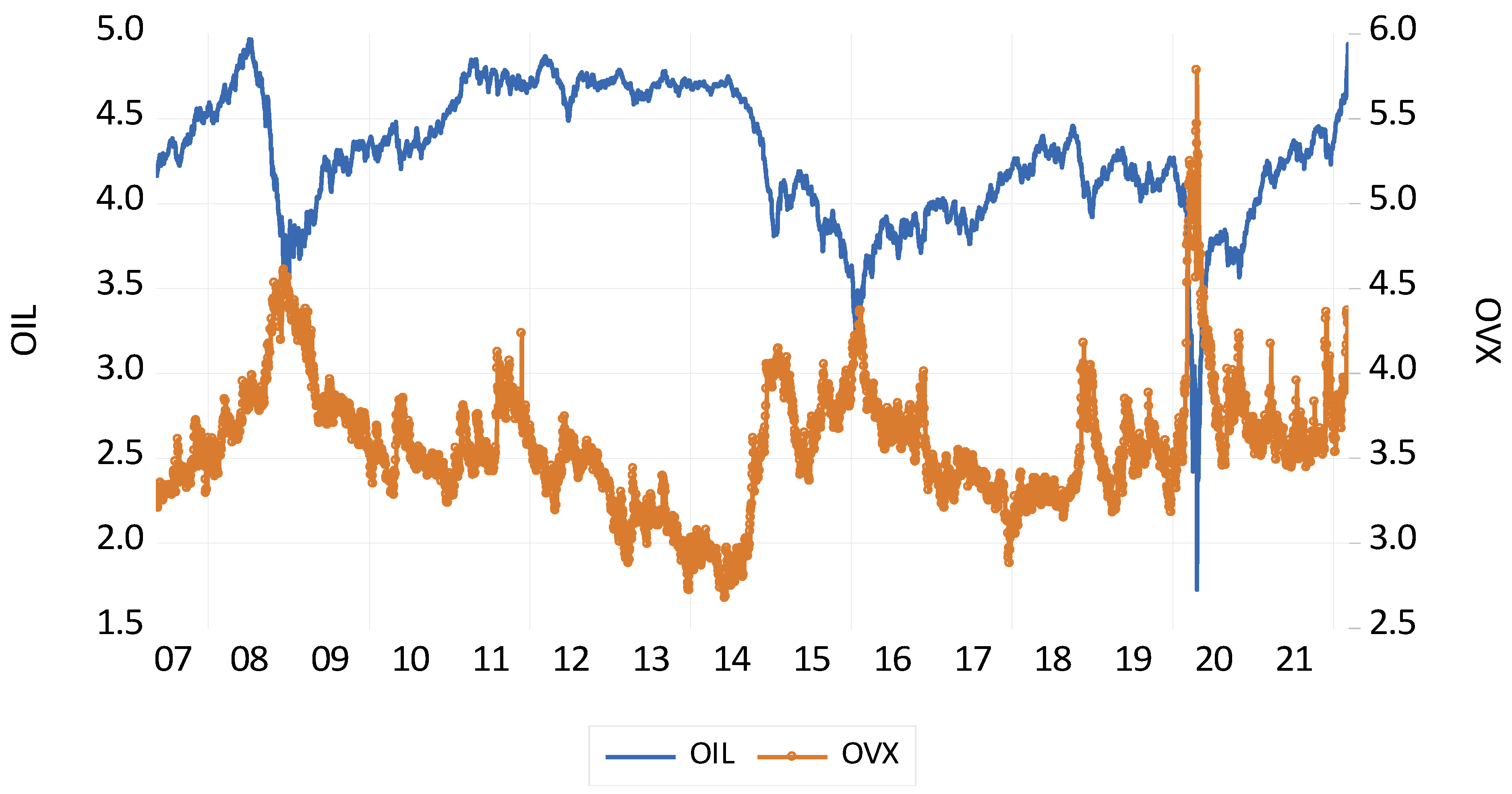

3.1. Data

3.2. Methodology and Research Hypotheses

3.3. Econometric Model

4. Results and Analysis

4.1. Stationarity and Cointegration

4.2. Structural Breaks

4.3. Oil Price and OVX Changes on Exchange Rate

4.3.1. OLS Estimation

Net Oil Importers

Net Oil Exporters

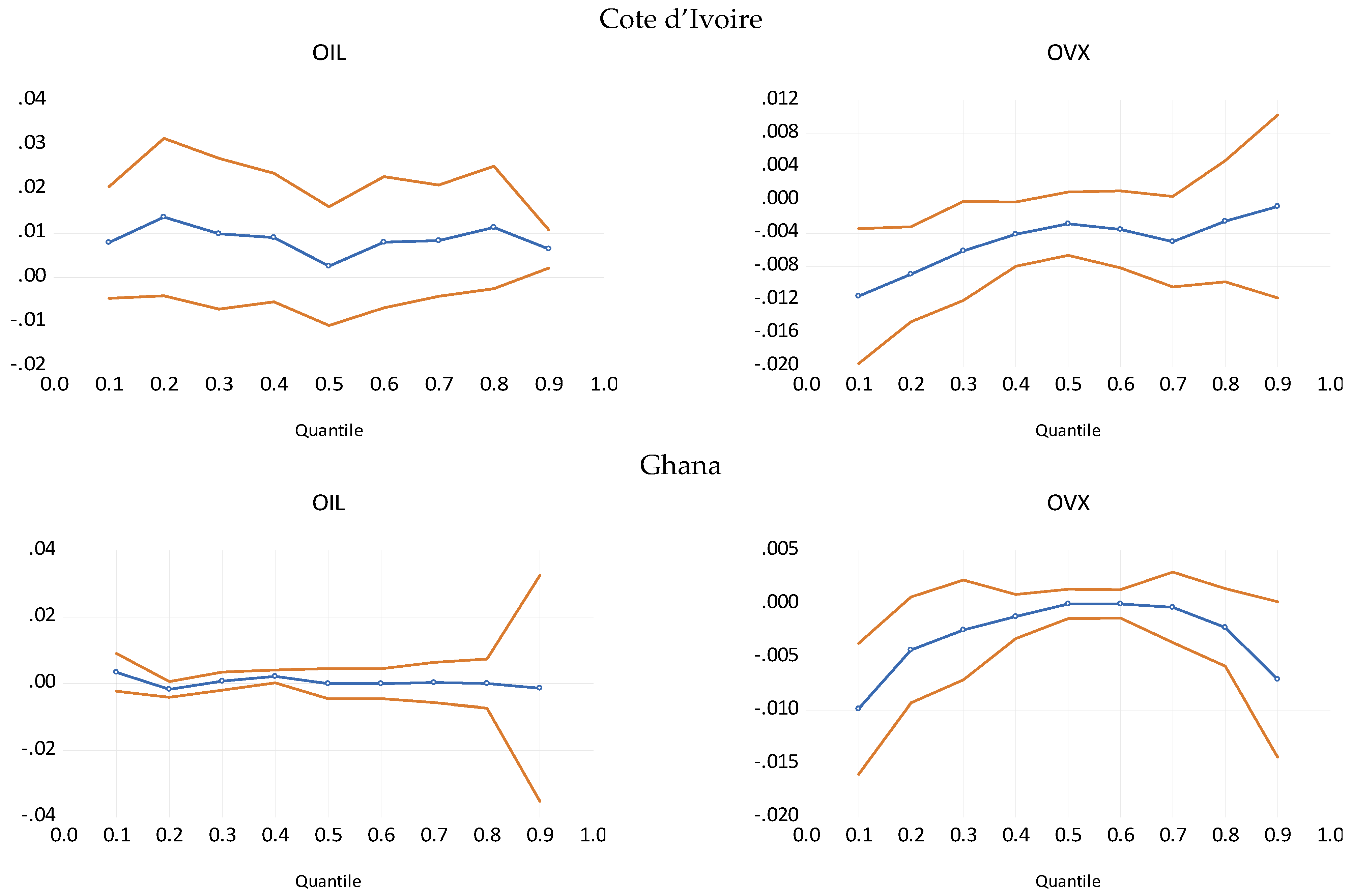

4.3.2. QR model Estimation

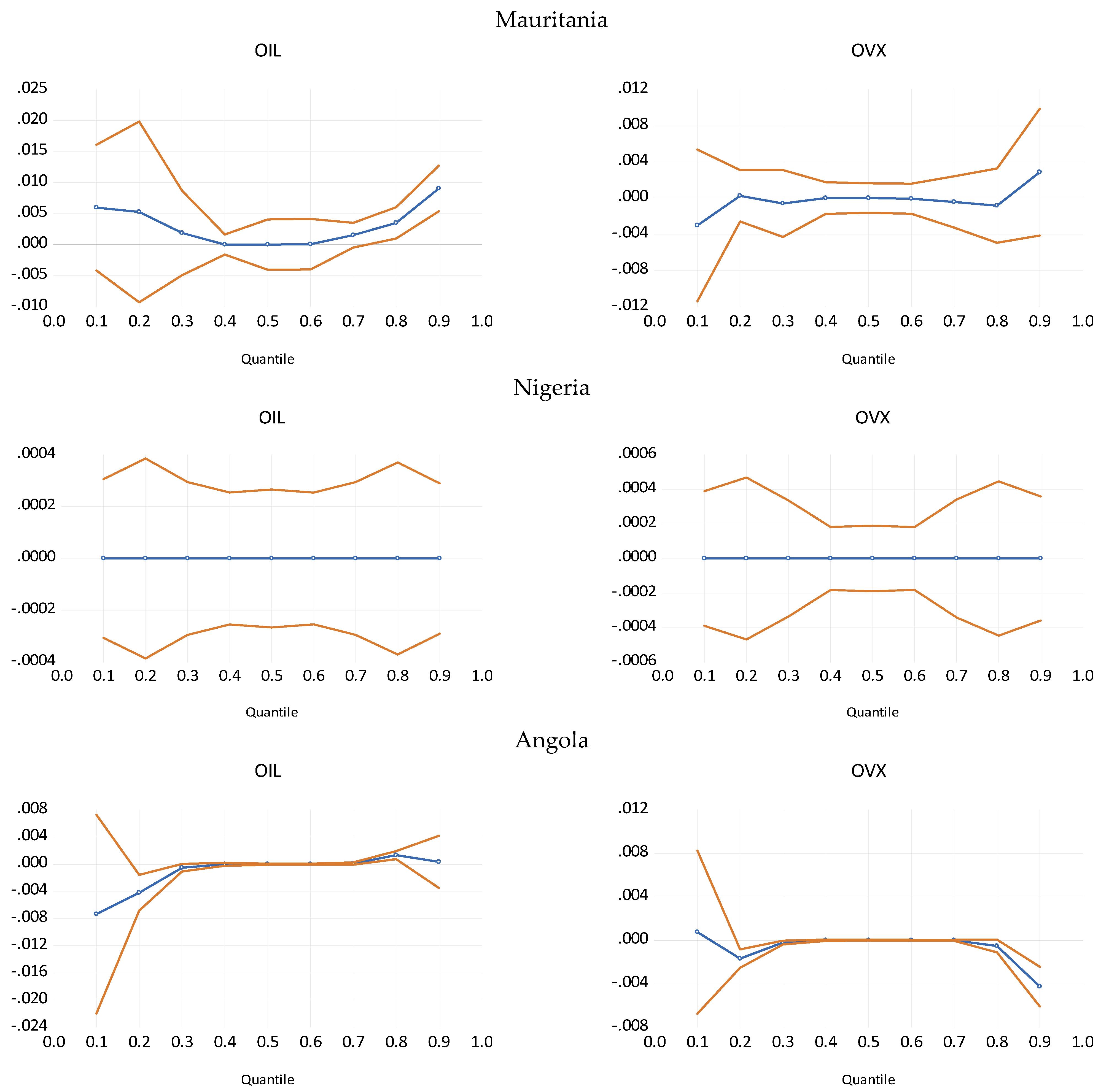

Net Oil Importers

Net Oil Exporters

4.3.3. Asymmetric Impacts of Oil Risk Changes on Exchange Rate under Different Market Conditions

Net Oil Importers

Net Oil Exporters

4.3.4. Summary of Estimation Results

4.4. Robustness Checks: Markov Regime Switching Model

5. Conclusions

5.1. The ‘Big Picture’ in the Exchange Rate–Oil Nexus and Implications for the Countries Concerned

5.2. Limitations and Future Research

Author Contributions

Funding

Conflicts of Interest

| 1 | |

| 2 | Oil price uncertainty and oil price volatility have been used interchangeably in this study. Since volatility is regarded as a measure of uncertainty (Wang et al. 2017; Xiao et al. 2018). |

| 3 | VIX = Chicago Board Options Exchange (CBOE) Volatility Index, which is the stock market option-based implied volatility of the US S&P500 index. OVX is a market-determined forecast which is similar to the implied volatility index (VIX) in the stock market. Both OVX and VIX serves as a gauge of investors fear (Ji and Fan 2016). |

| 4 | Increase in oil prices makes oil expensive for the importing country, such that they demand more USD to buy the same quantity of oil which may lead to depreciation of the local currency (Zhou 1995). |

| 5 | Increase in oil prices will increase the supply of dollars in the oil exporting country relative to the local currency, which may lead to the appreciation of the local currency (Lizardo and Mollick 2010). |

| 6 | Oil price increases lead to income transfer from oil importers to oil exporters which results in reallocation of wealth to a new portfolio equilibrium requiring exchange rate to adjust accordingly (Lv et al. 2018). See Amano and Van Norden (1998), Kilian (2008) for further discussion of the on the theoretical channels. |

| 7 | |

| 8 | We restrict our countries to the following criteria (a) Sub-Sahara African countries, (b) in the top 20 oil producing countries in Africa (African Vault 2015), (c) trade partners in crude oil with the USA (EIA 2020). |

| 9 | To test for multicollinearity, we ran a variance inflation factor test (VIF). The result indicates no multicollinearity. We do not show the VIF results. |

| 10 | The frequency of our current data is daily, and this allowed us to capture the effects of volatility and price changes on the exchange rate. Macro data are always available at a monthly/quarterly basis. For example, industrial production or money supply are available quarterly. Including those variables requires changing the frequency of the whole study, which makes it impossible to use oil prices or OVX. Volatility occurs in short term clusters. On a quarterly basis, observing any volatility is unlikely (OVX is obsolete) which negates the core concept of this article. The central bank base rate for each of the counties under investigation is a good option but difficult to obtain. In addition, the central bank base rate changes infrequently so, econometrically speaking, the base rate would be a ‘constant value’ adding nothing to the regressions (based on daily observations) in this study since it would be repeating itself. From an econometrics point of view a ‘non-varying’ variable would introduce a number of undesirable issues. There is no such thing as LIBOR available for the countries under examination. |

| 11 | The ADF and PP test the null hypothesis of unit root in the data series against the alternative, while the KPSS tests the null hypothesis of stationarity in the data series against the alternative. |

| 12 | A plausible reason could be because Angola has a less diversified economic structure and the economy is mainly driven by oil revenue (see Eagle 2017). |

| 13 | This paper examines the impact of oil price shocks on the Nigerian economy by examining the following variables: real GDP, government expenditure, inflation, real exchange rate and net exports. |

| 14 | (https://www.euronews.com/my-europe/2022/08/23/europes-energy-crisis-haunts-the-euro-as-it-tumbles-to-20-year-low-against-the-dollar) (accessed on 27 September 2022). https://markets.businessinsider.com/news/currencies/dollar-dominance-euro-energy-crisis-parity-currencies-investing-analysis-citi-2022-8 (accessed on 27 September 2022). |

References

- Adeniyi, Oluwatosin Ademola, Olusegun Omisakin, Jameelah Yaqub, and Abimbola Oyinlola. 2012. Oil price-exchange rate nexus in Nigeria: Further evidence from an oil exporting economy. International Journal of Humanities and Social Science (Special Issue) 2: 1–14. [Google Scholar]

- AFDP. 2019. African Development Bank: African Economic Outlook. Available online: https://www.afdb.org/fileadmin/uploads/afdb/Documents/Publications/African_Economic_0utlook_2019_-_EN.Pdf (accessed on 2 May 2020).

- African Vault. 2015. Top 20 Oil Producing Countries in Africa. Africanvault. Available online: https://africanvault.com/oil-producing-countries-in-africa/ (accessed on 6 June 2019).

- Ahmad, Ahmad Hassan, and Ricardo Moran Hernandez. 2013. Asymmetric adjustment between oil prices and exchange rates: Empirical evidence from major oil producers and consumers. Journal of International Financial Markets, Institutions and Money 27: 306–17. [Google Scholar] [CrossRef]

- Akram, Farooq. 2004. Oil prices and exchange rates: Norwegian evidence. The Econometrics Journal 7: 476–504. [Google Scholar] [CrossRef]

- Allegret, Jean-Pierre, Cécile Couharde, Dramane Coulibaly, and Valérie Mignon. 2014. Current accounts and oil price fluctuations in oil exporting countries: The role of financial development. Journal of International Money and Finance 47: 185–201. [Google Scholar] [CrossRef]

- Aloui, Riadh, Mohamed Safouane Ben Aïssa, and Duc Khuong Nguyen. 2013. Conditional dependence structure between oil prices and exchange rates: A copula-GARCH approach. Journal of International Money and Finance 32: 719–38. [Google Scholar] [CrossRef]

- Amano, Robert A., and Simon Van Norden. 1998. Exchange rates and oil prices. Review of International Economics 6: 683–94. [Google Scholar] [CrossRef]

- Atems, Bebonchu, Devin Kapper, and Eddery Lam. 2015. Do exchange rates respond asymmetrically to shocks in the crude oil market? Energy Economics 49: 227–38. [Google Scholar] [CrossRef]

- Bai, Jushan, and Pierre Perron. 1998. Estimating and testing linear models with multiple structural changes. Econometrica 66: 47–78. [Google Scholar] [CrossRef]

- Bai, Jushan, and Pierre Perron. 2003. Critical values for multiple structural change tests. The Journal 6: 72–78. [Google Scholar] [CrossRef]

- Bala, Umar, and Lee Chin. 2018. Asymmetric impacts of oil price on inflation: An empirical study of African OPEC member countries. Energies 11: 3017. [Google Scholar] [CrossRef]

- Balke, Nathan S., Stephen P. A. Brown, and Mine K. Yucel. 2002. Oil price shocks and the US economy: Where does the asymmetry originate? The Energy Journal 23: 3. [Google Scholar] [CrossRef]

- Basher, Syed Abul, and Perry Sadorsky. 2016. Hedging emerging market stock prices with oil, gold, VIX, and bonds: A comparison between DCC, ADCC and GO-GARCH. Energy Economics 54: 235–47. [Google Scholar] [CrossRef]

- Baur, Dirk G. 2013. The structure and degree of dependence: A quantile regression approach. Journal of Banking & Finance 37: 786–98. [Google Scholar]

- Beckmann, Joscha, Theo Berger, and Robert Czudaj. 2016. Oil price and FX-rates dependency. Quantitative Finance 16: 477–88. [Google Scholar] [CrossRef]

- Bernanke, Ben S. 1983. Irreversibility, uncertainty, and cyclical investment. The Quarterly Journal of Economics 98: 85–106. [Google Scholar] [CrossRef]

- Bodenstein, Martin, Christopher Erceg, and Luca Guerrieri. 2011. Oil shocks and external adjustment. Journal of International Economics 83: 168–84. [Google Scholar] [CrossRef]

- Brahmasrene, Tantatape, Jui-Chi Huang, and Yaya Sissoko. 2014. Crude oil prices and exchange rates: Causality, variance decomposition and impulse response. Energy Economics 44: 407–12. [Google Scholar] [CrossRef]

- Breen, John David, and Liang Hu. 2021. The predictive content of oil price and volatility: New evidence on exchange rate forecasting. Journal of International Financial Markets, Institutions and Money 75: 101–454. [Google Scholar] [CrossRef]

- Chang, Ming-Jen, and Che-Yi Su. 2014. The dynamic relationship between exchange rates and macroeconomic fundamentals: Evidence from Pacific Rim countries. Journal of International Financial Markets, Institutions and Money 30: 220–46. [Google Scholar] [CrossRef]

- Chaudhuri, Kausik, and Betty C. Daniel. 1998. Long-run equilibrium real exchange rates and oil prices. Economics Letters 58: 231–38. [Google Scholar] [CrossRef]

- Chen, Hangato, Li Liu, Yudong Wang, and Yingming Zhu. 2016. Oil price shocks and US dollar exchange rates. Energy 112: 1036–48. [Google Scholar] [CrossRef]

- Chen, Shiu-Sheng, and Hung-Chyn Chen. 2007. Oil prices and real exchange rates. Energy economics 29: 390–404. [Google Scholar] [CrossRef]

- Cifarelli, Giulio, and Giovanna Paladino. 2010. Oil price dynamics and speculation: A multivariate financial approach. Energy Economics 32: 363–72. [Google Scholar] [CrossRef]

- Coleman, Simeon, Juan Carlos Cuestas, and Estefania Mourelle. 2011. Investigating the Oil Price-Exchange Rate Nexus: Evidence from Africa. Available online: http://eprints.whiterose.ac.uk/43089/ (accessed on 1 December 2019).

- Conrad, Daren, and Jaymieon Jagessar. 2018. Real Exchange Rate Misalignment and Economic Growth: The Case of Trinidad and Tobago. Economies 6: 52. [Google Scholar] [CrossRef]

- Czech, Katarzyna, and Ibrahim Niftiyev. 2021. The impact of oil price shocks on oil-dependent countries’ currencies: The case of Azerbaijan and Kazakhstan. Journal of Risk and Financial Management 14: 431. [Google Scholar] [CrossRef]

- Danladi, Jonathan D., and Ugochukwu P. Uba. 2016. Does the volatility of exchange rate affect the economic performance of countries in the West African Monetary zone? A case of Nigeria and Ghana. Journal of Economics, Management and Trade 11: 1–10. [Google Scholar] [CrossRef]

- Devpura, Neluka. 2021. Effect of COVID-19 on the relationship between Euro/USD exchange rate and oil price. MethodsX 8: 101262. [Google Scholar] [CrossRef]

- Diaz, Elena Maria, Juan Carlos Molero, and Fernando Perez de Gracia. 2016. Oil price volatility and stock returns in the G7 economies. Energy Economics 54: 417–30. [Google Scholar] [CrossRef]

- Dickey, David A., and Wayne A. Fuller. 1979. Distribution of the estimators for autoregressive time series with a unit root. Journal of the American Statistical Association 74: 427–31. [Google Scholar]

- Eagle, Beyond. 2017. Oil price volatility and macroeconomy: Tales from top two oil producing economies in Africa. Journal of Economic & Financial Studies 5: 45–55. [Google Scholar]

- Ebenezer, Olamide, Kanayo Ogujiuba, and Andrew Maredza. 2022. Exchange Rate Volatility, Inflation and Economic Growth in Developing Countries: Panel Data Approach for SADC. Economies 10: 67. [Google Scholar]

- Edelstein, Paul, and Lutz Kilian. 2009. How sensitive are consumer expenditures to retail energy prices? Journal of Monetary Economics 56: 766–779. [Google Scholar] [CrossRef]

- EIA. 2020. U.S. Energy Information Administration ‘Petroleum and Other Liquids’. Available online: https://www.eia.gov/international/data/world (accessed on 7 December 2020).

- Elder, John, and Apostolos Serletis. 2010. Oil price uncertainty. Journal of Money, Credit and Banking 42: 1137–59. [Google Scholar] [CrossRef]

- Engemann, Kristie M., Michael T. Owyang, and Howard J. Wall. 2014. Where is an oil shock? Journal of Regional Science 54: 169–85. [Google Scholar] [CrossRef]

- Evgenidis, Anastasios. 2018. Do all oil price shocks have the same impact? Evidence from the euro area. Finance Research Letters 26: 150–155. [Google Scholar] [CrossRef]

- Ferderer, J. Peter. 1996. Oil price volatility and the macroeconomy. Journal of Macroeconomics 18: 1–26. [Google Scholar] [CrossRef]

- Fraj, Salma Hadj, Mekki Hamdaoui, and Samir Maktouf. 2018. Governance and economic growth: The role of the exchange rate regime. International Economics 156: 326–64. [Google Scholar] [CrossRef]

- Ghosh, Sajal. 2011. Examining crude oil price–Exchange rate nexus for India during the period of extreme oil price volatility. Applied Energy 88: 1886–89. [Google Scholar] [CrossRef]

- Giulietti, Monica, Ana Maria Iregui, and Jesús Otero. 2015. A pair-wise analysis of the law of one price: Evidence from the crude oil market. Economics Letters 129: 39–41. [Google Scholar] [CrossRef]

- Golub, Stephen S. 1983. Oil prices and exchange rates. The Economic Journal 93: 576–93. [Google Scholar] [CrossRef]

- Habib, Maurizio Michael, and Margarita M. Kalamova. 2007. Are There Oil Currencies? The Real Exchange Rate of Oil Exporting Countries. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=1032834 (accessed on 10 December 2019).

- Hamilton, James D. 1996. This is what happened to the oil price-macroeconomy relationship. Journal of Monetary Economics 38: 215–20. [Google Scholar] [CrossRef]

- Hamilton, James D. 2003. What is an oil shock? Journal of Econometrics 113: 363–98. [Google Scholar] [CrossRef]

- Hammond, John L. 2011. The resource curse and oil revenues in Angola and Venezuela. Science & Society 75: 348–78. [Google Scholar]

- Hu, Ling. 2006. Dependence patterns across financial markets: A mixed copula approach. Applied Financial Economics 16: 717–29. [Google Scholar] [CrossRef]

- International Energy Agency. 2004. World Energy Outlook 2004. Available online: https://iea.blob.core.windows.net/assets/e2be51f1-b04c-433f-9a68-93bfd46c7ad4/WorldEnergyOutlook2004.pdf (accessed on 6 March 2019).

- IEA. 2019. Africa Energy Outlook 2019. World Energy Outlook Special Report. Available online: https://www.iea.org/reports/africa-energy-outlook-2019 (accessed on 6 June 2019).

- Issa, Ramzi, Robert Lafrance, and John Murray. 2008. The turning black tide: Energy prices and the Canadian dollar. Canadian Journal of Economics/Revue canadienne d’économique 41: 737–59. [Google Scholar] [CrossRef]

- Iwayemi, Akin, and Babajide Fowowe. 2011. Impact of oil price shocks on selected macroeconomic variables in Nigeria. Energy Policy 39: 603–12. [Google Scholar] [CrossRef]

- Ji, Qiang, and Ying Fan. 2016. Modelling the joint dynamics of oil prices and investor fear gauge. Research in International Business and Finance 37: 242–51. [Google Scholar] [CrossRef]

- Jiang, Jiaqi, and Rongbao Gu. 2016. Asymmetrical long-run dependence between oil price and US dollar exchange rate—Based on structural oil shocks. Physica A: Statistical Mechanics and Its Applications 456: 75–89. [Google Scholar] [CrossRef]

- Jin, Xuejun, and Fangfei Zhu. 2019. Global Oil Shocks and China’s Commodity Markets: The Role of OVX. Emerging Markets Finance and Trade 57: 914–29. [Google Scholar] [CrossRef]

- Keith, Benes, Andrew Cheon, Johannes Urpelainen, and Joonseok Yang. 2015. Low Oil Prices: An Opportunity for Fuel Subsidy Reform. New York: Columbia University. [Google Scholar]

- Khan, Khalid, Chi-Wei Su, Ran Tao, and Muhammad Umar. 2021. How do geopolitical risks affect oil prices and freight rates? Ocean & Coastal Management 215: 105955. [Google Scholar]

- Kilian, Lutz. 2008. A comparison of the effects of exogenous oil supply shocks on output and inflation in the G7 countries. Journal of the European Economic Association 6: 78–121. [Google Scholar] [CrossRef]

- Kin, Sibanda, and Mlambo Courage. 2014. The impact of oil prices on the exchange rate in South Africa. Journal of Economics 5: 193–99. [Google Scholar] [CrossRef]

- Kocaarslan, Baris, Mehmet Ali Soytas, and Ugur Soytas. 2020. The asymmetric impact of oil prices, interest rates and oil price uncertainty on unemployment in the US. Energy Economics 86: 104625. [Google Scholar] [CrossRef]

- Koenker, Roger, and Gilbert Bassett, Jr. 1978. Regression quantiles. Econometrica: Journal of the Econometric Society 46: 33–50. [Google Scholar] [CrossRef]

- Konstantakopoulou, Ioanna. 2016. New evidence on the Export-led-growth hypothesis in the Southern Euro-zone countries (1960–2014). Economics Bulletin 36: 429–39. [Google Scholar]

- Korhonen, Iikka, and Tuuli Juurikkala. 2009. Equilibrium exchange rates in oil exporting countries. Journal of Economics and Finance 33: 71–79. [Google Scholar] [CrossRef]

- Korley, Maud, and Evangelos Giouvris. 2021. The regime-switching behaviour of exchange rates and frontier stock market prices in Sub-Saharan Africa. Journal of Risk and Financial Management 14: 122. [Google Scholar] [CrossRef]

- Kwiatkowski, Denis, Peter C. Phillips, Peter Schmidt, and Yongcheol Shin. 1992. Testing the null hypothesis of stationarity against the alternative of a unit root: How sure are we that economic time series have a unit root? Journal of Econometrics 54: 159–78. [Google Scholar] [CrossRef]

- Lariau, Ana, Moataz El-Said, and Misa Takebe. 2016. An Assessment of the Exchange Rate Pass-Through in Angola and Nigeria. International Monetary Fund. Available online: https://www.imf.org/en/Publications/WP/Issues/2016/12/31/An-Assessment-of-the-Exchange-Rate-Pass-Through-in-Angola-and-Nigeria-44281 (accessed on 8 June 2020).

- Lee, Chien-Chiang, and Jhih-Hong Zeng. 2011. The impact of oil price shocks on stock market activities: Asymmetric effect with quantile regression. Mathematics and Computers in Simulation 81: 1910–20. [Google Scholar] [CrossRef]

- Lee, Kiseok, Shawn Ni, and Ronald A. Ratti. 1995. Oil shocks and the macroeconomy: The role of price variability. The Energy Journal 16: 39–56. [Google Scholar] [CrossRef]

- Li, Zheng-Zheng, Chi-Wei Su, and Meng Nan Zhu. 2021. How Does Uncertainty Affect Volatility Correlation between Financial Assets? Evidence from Bitcoin, Stock and Gold. Emerging Markets Finance and Trade 58: 2682–94. [Google Scholar] [CrossRef]

- Liu, Ming-Lei, Qiang Ji, and Ying Fan. 2013. How does oil market uncertainty interact with other markets? An empirical analysis of implied volatility index. Energy 55: 860–68. [Google Scholar] [CrossRef]

- Lizardo, Radhamés A., and André V. Mollick. 2010. Oil price fluctuations and US dollar exchange rates. Energy Economics 32: 399–408. [Google Scholar] [CrossRef]

- Lv, Xin, Donald Lien, Qian Chen, and Chang Yu. 2018. Does exchange rate management affect the causality between exchange rates and oil prices? Evidence from oil exporting countries. Energy Economics 76: 325–43. [Google Scholar] [CrossRef]

- Maghyereh, Aktham I., Basel Awartani, and Elie Bouri. 2016. The directional volatility connectedness between crude oil and equity markets: New evidence from implied volatility indexes. Energy Economics 57: 78–93. [Google Scholar] [CrossRef]

- Malik, Farooq, and Zaghum Umar. 2019. Dynamic connectedness of oil price shocks and exchange rates. Energy Economics 84: 104501. [Google Scholar] [CrossRef]

- Mekki, Rabiâa. 2005. The Impact of Foreign Direct Investment on Trade: Evidence from Tunisia’s Trade. In Capital Flows and Foreign Direct Investments in Emerging Markets. London: Palgrave Macmillan, pp. 133–44. [Google Scholar]

- Mensah, Emmanuel Kwasi, Umberto Triacca, Eric Amoo Bondzie, and Gabriel Obed Fosu. 2016. Crude oil price, exchange rate and gross domestic product nexus in an emerging market: A cointegration analysis. Opec Energy Review 40: 212–31. [Google Scholar] [CrossRef]

- Mensi, Walid, Shawkat Hammoudeh, and Seong-Min Yoon. 2015. Structural breaks, dynamic correlations, asymmetric volatility transmission, and hedging strategies for petroleum prices and USD exchange rate. Energy Economics 48: 46–60. [Google Scholar] [CrossRef]

- Mork, Knut Anton. 1989. Oil and the macroeconomy when prices go up and down: An extension of Hamilton’s results. Journal of Political Economy 97: 740–44. [Google Scholar] [CrossRef]

- Muhammad, Zahid, Hassan Suleiman, and Reza Kouhy. 2012. Exploring oil price—Exchange rate nexus for Nigeria. OPEC Energy Review 36: 383–95. [Google Scholar] [CrossRef]

- Ngoma, Abubakar Lawan, Normaz Wana Ismail, and Zulkornain Yusop. 2016. An analysis of real oil prices and real exchange rates in five African countries: Applying symmetric and asymmetric cointegration models. Foreign Trade Review 51: 162–79. [Google Scholar] [CrossRef]

- Nusair, Salah A., and Dennis Olson. 2019. The effects of oil price shocks on Asian exchange rates: Evidence from quantile regression analysis. Energy Economics 78: 44–63. [Google Scholar] [CrossRef]

- Nusair, Salah A., and Jamal A. Al-Khasawneh. 2018. Oil price shocks and stock market returns of the GCC countries: Empirical evidence from quantile regression analysis. Economic Change and Restructuring 51: 339–72. [Google Scholar] [CrossRef]

- Olomola, Philip A., and Akintoye V. Adejumo. 2006. Oil price shock and macroeconomic activities in Nigeria. International Research Journal of Finance and Economics 3: 28–34. [Google Scholar]

- Omotosho, Babatunde S. 2019. Oil price shocks, fuel subsidies and macroeconomic (in) stability in Nigeria. CBN Journal of Applied Statistics (JAS) 10: 1. [Google Scholar]

- Ozsoz, Emre, and Mustapha Akinkunmi. 2012. Real exchange rate assessment for Nigeria: An evaluation of determinants, strategies for identification and correction of misalignments. OPEC Energy Review 36: 104–23. [Google Scholar] [CrossRef]

- Peersman, Gert, and Ine Van Robays. 2009. Oil and the Euro area economy. Economic Policy 24: 603–51. [Google Scholar] [CrossRef]

- Peng, Wei, Shichao Hu, Wang Chen, Yu-Feng Zeng, and Lu Yang. 2019. Modeling the joint dynamic value at risk of the volatility index, oil price, and exchange rate. International Review of Economics & Finance 59: 137–49. [Google Scholar]

- Pershin, Viyaly, Juan Carlos Molero, and Fernado Perez de Gracia. 2016. Exploring the oil prices and exchange rates nexus in some African economies. Journal of Policy Modeling 38: 166–80. [Google Scholar] [CrossRef]

- Pesaran, M. Hashem, Yongcheol Shin, and Richard J. Smith. 2001. Bounds testing approaches to the analysis of level relationships. Journal of Applied Econometrics 16: 289–326. [Google Scholar] [CrossRef]

- Phillips, Peter C., and Pierre Perron. 1988. Testing for a unit root in time series regression. Biometrika 75: 335–46. [Google Scholar] [CrossRef]

- Pindyck, Robert S. 1993. A note on competitive investment under uncertainty. The American Economic Review 83: 273–77. [Google Scholar]

- Ravazzolo, Francesco, and Philip Rothman. 2013. Oil and US GDP: A real-time out-of-sample examination. Journal of Money, Credit and Banking 45: 449–63. [Google Scholar] [CrossRef]

- Raymond, Jennie E., and Robert W. Rich. 1997. Oil and the macroeconomy: A Markov state-switching approach. Journal of Money, Credit, and Banking 29: 193–213. [Google Scholar] [CrossRef]

- Reboredo, Juan C. 2012. Modelling oil price and exchange rate co-movements. Journal of Policy Modeling 34: 419–40. [Google Scholar] [CrossRef]

- Reboredo, Juan C., and Miguel A. Rivera-Castro. 2013. A wavelet decomposition approach to crude oil price and exchange rate dependence. Economic Modelling 32: 42–57. [Google Scholar] [CrossRef]

- Said, Husani, and Evangelos Giouvris. 2017a. Illiquidity, Monetary conditions, and the financial crisis in the United Kingdom. In Handbook of Investors’ Behavior during Financial Crises. Cambridge: Academic Press, pp. 277–302. [Google Scholar]

- Said, Husaini, and Evangelos Giouvris. 2017b. Illiquidity as an investment style during the financial crisis in the United Kingdom. In Handbook of Investors’ Behavior during Financial Crises. Cambridge: Academic Press, pp. 419–46. Available online: http://ebookcentral.proquest.com/lib/rhul/detail.action?docID=4890799 (accessed on 7 July 2020).

- Said, Husaini, and Evangelos Giouvris. 2019. Oil, the Baltic Dry index, market (il)liquidity and business cycles: Evidence from net oil exporting/oil importing countries. Financial Markets and Portfolio Management 33: 349–16. [Google Scholar] [CrossRef]

- Salisu, Afees A., and Hakeem Mobolaji. 2013. Modeling returns and volatility transmission between oil price and US–Nigeria exchange rate. Energy Economics 39: 169–76. [Google Scholar] [CrossRef]

- Sari, Ramazan, Shawkat Hammoudeh, and Ugur Soytas. 2010. Dynamics of oil price, precious metal prices, and exchange rate. Energy Economics 32: 351–62. [Google Scholar] [CrossRef]

- Soojin, Jo. 2014. The effects of oil price uncertainty on global real economic activity. Journal of Money, Credit and Banking 46: 1113–35. [Google Scholar]

- Su, Xianfang, Huiming Zhu, Wanhai You, and Yinghua Ren. 2016. Heterogeneous effects of oil shocks on exchange rates: Evidence from a quantile regression approach. SpringerPlus 5: 1187. [Google Scholar] [CrossRef]

- Switzer, Lorne N., and Alan Picard. 2016. Stock market liquidity and economic cycles: A non-linear approach. Economic Modelling 57: 106–19. [Google Scholar] [CrossRef]

- Tsagkanos, Athanasios, and Costas Siriopoulos. 2013. A long-run relationship between stock price index and exchange rate: A structural nonparametric cointegrating regression approach. Journal of International Financial Markets, Institutions and Money 25: 106–18. [Google Scholar] [CrossRef]

- Tsai, I-Chun. 2012. The relationship between stock price index and exchange rate in Asian markets: A quantile regression approach. Journal of International Financial Markets, Institutions and Money 22: 609–21. [Google Scholar] [CrossRef]

- Turhan, Ibrahim, Erk Hacihasanoglu, and Ugur Soytas. 2013. Oil prices and emerging market exchange rates. Emerging Markets Finance and Trade 49: 21–36. [Google Scholar] [CrossRef]

- Umar, Muhammad, Chi-Wei Su, Syed Kumail Abbas Rizvi, and Oana-Ramona Lobonţ. 2021. Driven by fundamentals or exploded by emotions: Detecting bubbles in oil prices. Energy 231: 120873. [Google Scholar] [CrossRef]

- Volkov, Nikanor I., and Ky-Hyang Yuhn. 2016. Oil price shocks and exchange rate movements. Global Finance Journal 31: 18–30. [Google Scholar] [CrossRef]

- Wang, Kai-Hua, Chi-Wei Su, Yidong Xiao, and Lu Liu. 2022. Is the oil price a barometer of China’s automobile market? From a wavelet-based quantile-on-quantile regression perspective. Energy 240: 122501. [Google Scholar] [CrossRef]

- Wang, Yong, Erwei Xiang, Wenjuan Ruan, and Wei Hu. 2017. International oil price uncertainty and corporate investment: Evidence from China’s emerging and transition economy. Energy Economics 61: 330–39. [Google Scholar] [CrossRef]

- Wang, Yudong, Chongfeng Wu, and Li Yang. 2013. Oil price shocks and stock market activities: Evidence from oil importing and oil exporting countries. Journal of Comparative Economics 41: 1220–39. [Google Scholar] [CrossRef]

- Wu, Chih-Chiang, Huimin Chung, and Yu-Hsien Chang. 2012. The economic value of co-movement between oil price and exchange rate using copula-based GARCH models. Energy Economics 34: 270–82. [Google Scholar] [CrossRef]

- Xiao, Jihong, Min Zhou, Fengming Wen, and Fenghua Wen. 2018. Asymmetric impacts of oil price uncertainty on Chinese stock returns under different market conditions: Evidence from oil volatility index. Energy Economics 74: 777–86. [Google Scholar] [CrossRef]

- You, Wanhai, Yawei Guo, Huiming Zhu, and Yong Tang. 2017. Oil price shocks, economic policy uncertainty and industry stock returns in China: Asymmetric effects with quantile regression. Energy Economics 68: 1–18. [Google Scholar] [CrossRef]

- Yousefi, Ayoub, and Tony S. Wirjanto. 2004. The empirical role of the exchange rate on the crude-oil price formation. Energy Economics 26: 783–99. [Google Scholar] [CrossRef]

- Zankawah, Mutawakil M., and Chris Stewart. 2020. Measuring the volatility spill-over effects of crude oil prices on the exchange rate and stock market in Ghana. The Journal of International Trade & Economic Development 29: 420–39. [Google Scholar]

- Zhou, Su. 1995. The response of real exchange rates to various economic shocks. Southern Economic Journal 61: 936–54. [Google Scholar] [CrossRef]

- Zhu, Huiming, Yawei Guo, Wanhai You, and Yaqin Xu. 2016. The heterogeneity dependence between crude oil price changes and industry stock market returns in China: Evidence from a quantile regression approach. Energy Economics 55: 30–41. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

| Countries | Crude Oil | Thousand Barrels per | Day |

|---|---|---|---|

| Exports | Imports | Net Exports | |

| Cote d’Iviore | 26.7 | 62.35 | −35.65 |

| Ghana | 1.93 | 2.05 | −0.12 |

| Nigeria | 2114.00 | 441.00 | 1673.00 |

| Angola | 1710.90 | 134.50 | 1576.40 |

| Mauritania | - | - | −201.00 |

| Exchange Rate Returns and Oil Indices | Mean | SD | Skewness | Kurtosis | J–BTest |

|---|---|---|---|---|---|

| Cote d’Ivoire | −0.0051 | 0.6619 | −0.0294 | 5.9117 | 1367.68 ** |

| Ghana | −0.0526 | 0.8710 | −0.1979 | 22.8740 | 63,715.54 ** |

| Mauritania | −0.0083 | 0.8194 | −1.7153 | 60.4144 | 533,444.4 ** |

| Nigeria | −0.0305 | 1.0671 | −10.7678 | 337.5160 | 18,118,819 ** |

| Angola | −0.0472 | 0.5842 | −7.8260 | 168.0834 | 4,433,972 ** |

| Oil Price | 0.0166 | 3.1931 | −5.4473 | 245.2984 | 9,485,884 ** |

| Oil Volatility | 0.0235 | 5.7300 | 1.6546 | 31.1969 | 129,970.5 ** |

| Exchange Rate Series and Oil Indices | ADF t-Test | PP-Test | KPSS-Test | |||

|---|---|---|---|---|---|---|

| Level | First Diff. | Level | First Diff. | Level | First Diff. | |

| Countries and oil indices | ||||||

| Cote d’Ivoire | −1.6722 | −69.244 *** | −1.678 | −69.291 *** | 5.434 *** | 0.037 |

| Ghana | −0.829 | −22.007 *** | −0.834 | −80.646 *** | 7.580 *** | 0.080 |

| Mauritania | −1.165 | −40.656 *** | −1.125 | −100.418 *** | 7.131 *** | 0.064 |

| Nigeria | −0.015 | −51.577 *** | −0.002 | −82.037 *** | 7.196 *** | 0.106 |

| Angola | 0.801 | −21.907 *** | 0.847 | −66826 *** | 6.689 *** | 0.625 |

| OIL | −2.6310 * | −13.164 *** | −2.483 | −66.280 *** | 2.079 *** | 0.073 |

| OVX | −4.467 *** | −66.613 *** | −4.0948 *** | −68.496 *** | 0.421 | 0.030 |

| Country | F-Statistics | Lag Order |

|---|---|---|

| Cote d’Ivoire | 1.154 | (4,3,1) |

| Ghana | 2.256 | (4,2,0) |

| Mauritania | 2.381 | (4,0,0) |

| Nigeria | 4.731 | (3,0,0) |

| Angola | 6.750 | (4,4,0) |

| Countries | 0 vs. 1 | 1 vs. 2 | 2 vs. 3 | 3 vs. 4 | 4 vs. 5 | Number of Breaks | BD1 | BD2 |

|---|---|---|---|---|---|---|---|---|

| Cote d’Ivoire | 78.42 | 17.25 | 2.70 | 0.00 | 0.00 | 2 | 20 January 2010 | 25 March 2013 |

| Ghana | 1.37 | 0.00 | 0.00 | 0.00 | 0.00 | 0 | ||

| Mauritania | 1.23 | 0.00 | 0.00 | 0.00 | 0.00 | 0 | ||

| Nigeria | 3.83 | 0.00 | 0.00 | 0.00 | 0.00 | 0 | ||

| Angola | 2.67 | 0.00 | 0.00 | 0.00 | 0.00 | 0 |

| Currency | Variable | OLS | Bearish | Market | Normal | Market | Bullish | Market | |||

|---|---|---|---|---|---|---|---|---|---|---|---|

| Q0.1 | Q0.2 | Q0.3 | Q0.4 | Q0.5 | Q0.6 | Q0.7 | Q0.8 | Q0.9 | |||

| CFA | Constant | −0.01 | −0.73 | −0.43 | −0.24 | −0.10 | 0.00 | 0.10 | 0.23 | 0.41 | 0.72 |

| OIL | 0.01 | 0.01 | 0.01 | 0.01 | 0.01 | 0.00 | 0.01 | 0.01 | 0.01 | 0.01 | |

| OVX | −0.01 | −0.01 | −0.01 | −0.01 | −0.00 | −0.00 | −0.00 | −0.00 | −0.00 | −0.00 | |

| ß4 | −0.00 | −0.41 | −0.27 | −0.16 | −0.10 | −0.04 | 0.05 | 0.17 | 0.23 | 0.29 | |

| ß5 | 0.04 | 0.17 | 0.13 | 0.07 | 0.07 | 0.01 | −0.01 | 0.03 | −0.00 | −0.05 | |

| GHS | Constant | −0.05 | −0.75 | −0.34 | −0.16 | −0.06 | 0.00 | 0.00 | 0.09 | 0.24 | 0.59 |

| OIL | 0.00 | 0.00 | −0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | −0.00 | |

| OVX | −0.01 | −0.01 | −0.00 | −0.00 | −0.00 | −0.00 | −0.00 | −0.00 | −0.00 | −0.01 | |

| ß4 | −0.06 | −0.01 | −0.01 | 0.01 | −0.01 | −0.02 | 0.00 | −0.08 | −0.19 | −0.31 | |

| ß5 | 0.04 | 0.22 | 0.07 | 0.05 | 0.05 | 0.00 | 0.00 | 0.01 | 0.00 | −0.02 | |

| OUG | Constant | −0.00 | −0.62 | −0.30 | −0.15 | −0.02 | 0.00 | 0.03 | 0.16 | 0.32 | 0.59 |

| OIL | 0.01 | 0.01 | 0.01 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.01 | |

| OVX | 0.00 | −0.00 | 0.00 | −0.00 | −0.00 | −0.00 | −0.00 | −0.00 | −0.00 | 0.00 | |

| ß4 | −0.03 | −0.39 | −0.12 | −0.02 | 0.02 | 0.00 | −0.03 | 0.02 | 0.06 | 0.26 | |

| ß5 | −0.03 | −0.05 | −0.05 | −0.02 | −0.10 | 0.00 | −0.03 | −0.11 | −0.07 | 0.05 | |

| NGN | Constant | −0.02 | −0.33 | −0.13 | −0.04 | −0.01 | 0.00 | −0.00 | 0.03 | 0.10 | 0.28 |

| OIL | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.01 | |

| OVX | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | −0.00 | −0.00 | −0.00 | −0.00 | −0.00 | |

| ß4 | −0.03 | −0.04 | 0.03 | 0.01 | 0.00 | 0.00 | 0.00 | −0.00 | −0.04 | 0.02 | |

| ß5 | −0.06 | 0.33 | 0.13 | 0.04 | 0.01 | 0.00 | −0.00 | −0.03 | −0.10 | −0.28 | |

| WAN | Constant | −0.05 | −0.30 | −0.06 | −0.00 | 0.00 | −0.00 | 0.00 | 0.00 | 0.01 | 0.18 |

| OIL | 0.00 | −0.01 | −0.00 | −0.00 | −0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | |

| OVX | 0.00 | 0.00 | −0.00 | −0.00 | −0.00 | −0.00 | −0.00 | −0.00 | −0.00 | −0.00 | |

| ß4 | 0.04 | 0.20 | 0.03 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | −0.00 | −0.09 | |

| ß5 | −0.07 | −0.61 | −0.60 | −0.23 | −0.03 | 0.00 | 0.00 | 0.02 | 0.13 | 0.34 |

| Currency | Variable | Q0.1 = Q0.2 | Q0.2 = Q0.3 | Q0.3 = Q0.4 | Q0.4 = Q0.5 | Q0.5 = Q0.6 | Q0.6 = Q0.7 | Q0.7 = Q0.8 | Q0.8 = Q0.9 | Q0.1 = Q0.5 | Q0.5 = Q0.9 |

|---|---|---|---|---|---|---|---|---|---|---|---|

| CFA | OIL | 0.41 | 0.54 | 0.87 | 0.14 | 0.22 | 0.93 | 0.52 | 0.45 | 0.49 | 0.57 |

| OVX | 0.40 | 0.17 | 0.28 | 0.29 | 0.61 | 0.38 | 0.30 | 0.67 | 0.02 | 0.69 | |

| ß4 | 0.02 | 0.00 | 0.06 | 0.06 | 0.00 | 0.00 | 0.18 | 0.29 | 0.00 | 0.00 | |

| ß5 | 0.67 | 0.06 | 0.62 | 0.00 | 0.35 | 0.25 | 0.43 | 0.35 | 0.10 | 0.36 | |

| GHS | OIL | 0.00 | 0.00 | 0.00 | 0.23 | 0.01 | 0.04 | 0.07 | 0.00 | 0.26 | 0.93 |

| OVX | 0.00 | 0.00 | 0.00 | 0.01 | 0.38 | 0.01 | 0.01 | 0.00 | 0.00 | 0.04 | |

| ß4 | 0.03 | 0.00 | 0.00 | 0.29 | 0.01 | 0.00 | 0.00 | 0.22 | 0.99 | 0.00 | |

| ß5 | 0.78 | 0.00 | 0.00 | 0.00 | 0.10 | 0.07 | 0.00 | 0.00 | 0.02 | 0.86 | |

| OUG | OIL | 0.00 | 0.09 | 0.74 | 0.08 | 0.00 | 0.49 | 0.23 | 0.04 | 0.22 | 0.00 |

| OVX | 0.00 | 0.00 | 0.00 | 0.23 | 0.05 | 0.00 | 0.00 | 0.00 | 0.45 | 0.38 | |

| ß4 | 0.00 | 0.00 | 0.00 | 0.40 | 0.73 | 0.19 | 0.73 | 0.47 | 0.00 | 0.01 | |

| ß5 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.03 | 0.26 | 0.56 | 0.60 | |

| NGN | OIL | 0.02 | 0.00 | 0.54 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 1.00 | 1.00 |

| OVX | 0.00 | 0.00 | 0.29 | 0.00 | 0.00 | 0.58 | 0.00 | 0.00 | 1.00 | 1.00 | |

| ß4 | 0.00 | 0.00 | 0.31 | 0.00 | 0.00 | 0.20 | 0.00 | 0.75 | 0.66 | 0.83 | |

| ß5 | 0.00 | 0.27 | 0.00 | 0.00 | 0.00 | 0.26 | 0.00 | 0.00 | 0.00 | 0.00 | |

| WAN | OIL | 0.73 | 0.01 | 0.90 | 0.00 | 0.00 | 0.02 | 0.00 | 0.76 | 0.32 | 0.85 |

| OVX | 0.00 | 0.00 | 0.06 | 0.03 | 0.00 | 0.00 | 0.46 | 0.02 | 0.84 | 0.00 | |

| ß4 | 0.00 | 0.00 | 0.00 | 0.00 | 0.03 | 0.01 | 0.00 | 0.00 | 0.00 | 0.00 | |

| ß5 | 0.00 | 0.00 | 0.24 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

| Currency | Variable | OLS | Bearish | Market | Normal | Market | Bullish | Market | |||

|---|---|---|---|---|---|---|---|---|---|---|---|

| Q0.1 | Q0.2 | Q0.3 | Q0.4 | Q0.5 | Q0.6 | Q0.7 | Q0.8 | Q0.9 | |||

| CFA | Constant | 0.03 | −0.72 | −0.43 | −0.23 | −0.08 | 0.01 | 0.142 | 0.25 | 0.47 | 0.77 |

| OIL+ | −0.06 | 0.00 | −0.12 | −0.14 | −0.11 | −0.03 | 0.00 | 0.02 | −0.03 | −0.14 | |

| OIL− | −0.08 | 0.03 | −0.13 | −0.15 | −0.12 | −0.05 | −0.03 | −0.03 | −0.11 | −0.25 | |

| OVX+ | −0.10 | −0.50 | −0.39 | −0.29 | −0.16 | −0.03 | 0.04 | 0.11 | 0.13 | 0.22 | |

| OVX− | −0.09 | −0.51 | −0.39 | −0.28 | −0.15 | −0.02 | 0.06 | 0.14 | 0.18 | 0.28 | |

| H0: ß11 = ß12 | 1.39 | −0.99 | 0.34 | 0.32 | 0.47 | 0.84 | 2.32 | 2.71 | 4.19 | 3.50 | |

| H0: ß21 = ß22 | −1.48 | 1.25 | −0.07 | −0.10 | −0.40 | −0.87 | −2.57 | −2.92 | −4.51 | −3.80 | |

| GHS | Constant | −0.01 | −0.98 | −0.43 | −0.23 | −0.09 | −0.00 | 0.03 | 0.20 | 0.37 | 0.93 |

| OIL+ | −0.09 | 0.06 | 0.03 | 0.03 | 0.02 | −0.00 | −0.03 | −0.12 | −0.18 | −0.34 | |

| OIL− | −0.12 | −0.42 | −0.21 | −0.09 | −0.02 | −0.00 | −0.03 | −0.07 | −0.04 | 0.04 | |

| OVX+ | −0.10 | −0.31 | −0.28 | −0.16 | −0.08 | −0.00 | 0.01 | 0.02 | 0.05 | −0.00 | |

| OVX- | −0.09 | −0.08 | −0.16 | −0.11 | −0.06 | −0.00 | 0.01 | −0.01 | −0.02 | −0.18 | |

| H0: ß11 = ß12 | 1.63 | 16.08 | 11.28 | 7.90 | 4.44 | 0.00 | −1.18 | −4.98 | −7.46 | −11.23 | |

| H0: ß21 = ß22 | −1.72 | −16.73 | −11.84 | −8.26 | −4.44 | 0.00 | 1.09 | 4.84 | 7.58 | 11.42 | |

| OUG | Constant | 0.04 | −0.39 | −0.14 | −0.07 | −0.00 | 0.00 | 0.08 | 0.14 | 0.25 | 0.37 |

| OIL+ | −0.04 | −0.29 | −0.17 | −0.08 | −0.01 | −0.00 | 0.01 | 0.02 | 0.03 | 0.22 | |

| OIL− | −0.06 | −0.20 | −0.13 | −0.07 | −0.03 | −0.00 | −0.04 | −0.03 | −0.08 | 0.08 | |

| OVX+ | −0.09 | −0.35 | −0.21 | −0.10 | −0.06 | −0.00 | −0.02 | −0.02 | 0.02 | 0.20 | |

| OVX− | −0.08 | −0.40 | −0.23 | −0.11 | −0.05 | −0.00 | 0.01 | 0.01 | 0.07 | 0.26 | |

| H0: ß11 = ß12 | 1.32 | −3.48 | −2.45 | −0.93 | 2.23 | 0.00 | 4.91 | 3.43 | 5.16 | 6.25 | |

| H0: ß21 = ß22 | −1.46 | 3.36 | 2.29 | 0.79 | −2.46 | 0.00 | −5.08 | −3.48 | −5.28 | −6.11 | |

| NGN | Constant | −0.02 | −0.63 | −0.23 | −0.10 | −0.03 | 0.00 | 0.02 | 0.08 | 0.20 | 0.50 |

| OIL+ | 0.04 | 0.155 | −0.05 | −0.04 | −0.02 | −0.00 | 0.01 | 0.03 | 0.03 | −0.05 | |

| OIL− | 0.02 | 0.14 | −0.04 | −0.03 | −0.01 | −0.00 | 0.01 | 0.02 | 0.02 | −0.05 | |

| OVX+ | −0.13 | −0.10 | −0.04 | −0.03 | −0.01 | −0.00 | 0.00 | 0.01 | 0.01 | 0.01 | |

| OVX- | −0.12 | −0.11 | −0.05 | −0.34 | −0.02 | −0.00 | 0.01 | 0.02 | 0.02 | 0.02 | |

| H0: ß11 = ß12 | 0.85 | 0.76 | −1.98 | −3.16 | −2.04 | 0.00 | 1.73 | 4.28 | 3.42 | 0.56 | |

| H0: ß21 = ß22 | −0.84 | 0.42 | 3.52 | 4.34 | 2.41 | 0.00 | −2.00 | −5.48 | −5.11 | −1.75 | |

| WAN | Constant | −0.11 | −0.05 | −0.01 | −0.00 | −0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.02 |

| OIL+ | 0.14 | 0.04 | 0.03 | −0.00 | −0.00 | −0.00 | −0.00 | −0.00 | −0.00 | 0.01 | |

| OIL− | 0.11 | 0.10 | 0.02 | −0.01 | −0.00 | −0.00 | −0.00 | −0.00 | −0.00 | 0.07 | |

| OVX+ | 0.05 | −0.04 | −0.02 | −0.01 | 0.00 | 0.00 | 0.00 | 0.00 | 0.02 | 0.06 | |

| OVX- | 0.06 | −0.06 | −0.01 | −0.01 | 0.00 | 0.00 | 0.00 | 0.00 | 0.02 | 0.10 | |

| H0: ß11 = ß12 | 1.59 | −2.96 | 8.17 | 4.45 | 1.51 | 0.00 | 0.00 | −1.33 | 0.24 | 7.55 | |

| H0: ß21 = ß22 | −1.48 | 2.15 | −9.05 | −4.19 | −1.49 | 0.00 | 0.00 | 1.73 | 0.10 | −7.05 |

| Currency | Variable | Q0.1 = Q0.2 | Q0.2 = Q0.3 | Q0.3 = Q0.4 | Q0.4 = Q0.5 | Q0.5 = Q0.6 | Q0.6 = Q0.7 | Q0.7 = Q0.8 | Q0.8 = Q0.9 | Q0.1 = Q0.5 | Q0.5 = Q0.9 |

|---|---|---|---|---|---|---|---|---|---|---|---|

| CFA | OIL+ | 0.02 | 0.55 | 0.34 | 0.00 | 0.13 | 0.46 | 0.23 | 0.11 | 0.62 | 0.22 |

| OIL− | 0.01 | 0.61 | 0.41 | 0.00 | 0.61 | 0.97 | 0.09 | 0.08 | 0.31 | 0.04 | |

| OVX+ | 0.04 | 0.01 | 0.00 | 0.00 | 0.00 | 0.05 | 0.46 | 0.23 | 0.00 | 0.00 | |

| OVX− | 0.01 | 0.01 | 0.00 | 0.00 | 0.00 | 0.01 | 0.25 | 0.16 | 0.00 | 0.00 | |

| GHS | OIL+ | 0.53 | 0.90 | 0.51 | 0.23 | 0.00 | 0.00 | 0.09 | 0.00 | 0.38 | 0.00 |

| OIL− | 0.00 | 0.00 | 0.00 | 0.14 | 0.00 | 0.00 | 0.36 | 0.20 | 0.00 | 0.60 | |

| OVX+ | 0.66 | 0.00 | 0.00 | 0.00 | 0.38 | 0.69 | 0.43 | 0.54 | 0.00 | 0.97 | |

| OVX− | 0.21 | 0.14 | 0.06 | 0.00 | 0.53 | 0.41 | 0.80 | 0.04 | 0.35 | 0.07 | |

| OUG | OIL+ | 0.07 | 0.00 | 0.00 | 0.24 | 0.63 | 0.43 | 0.90 | 0.00 | 0.00 | 0.01 |

| OIL− | 0.40 | 0.09 | 0.08 | 0.02 | 0.00 | 0.73 | 0.30 | 0.03 | 0.03 | 0.38 | |

| OVX+ | 0.01 | 0.00 | 0.02 | 0.00 | 0.22 | 0.89 | 0.24 | 0.01 | 0.00 | 0.03 | |

| OVX− | 0.00 | 0.00 | 0.00 | 0.00 | 0.66 | 0.99 | 0.05 | 0.00 | 0.00 | 0.00 | |

| NGN | OIL+ | 0.00 | 0.21 | 0.00 | 0.00 | 0.00 | 0.00 | 0.72 | 0.08 | 0.01 | 0.33 |

| OIL− | 0.00 | 0.18 | 0.00 | 0.00 | 0.00 | 0.01 | 0.96 | 0.05 | 0.00 | 0.16 | |

| OVX+ | 0.10 | 0.12 | 0.00 | 0.00 | 0.05 | 0.00 | 0.67 | 0.91 | 0.01 | 0.76 | |

| OVX− | 0.11 | 0.08 | 0.00 | 0.00 | 0.01 | 0.00 | 0.89 | 0.96 | 0.00 | 0.45 | |

| WAN | OIL+ | 0.83 | 0.00 | 0.04 | 0.63 | 1.00 | 0.11 | 0.96 | 0.00 | 0.39 | 0.00 |

| OIL− | 0.12 | 0.00 | 0.00 | 0.52 | 1.00 | 0.63 | 0.85 | 0.00 | 0.05 | 0.02 | |

| OVX+ | 0.55 | 0.04 | 0.00 | 0.70 | 1.00 | 0.38 | 0.00 | 0.17 | 0.19 | 0.04 | |

| OIL− | 0.17 | 0.30 | 0.01 | 0.38 | 1.00 | 0.63 | 0.00 | 0.00 | 0.07 | 0.00 |

| Bear | Market | ||||||||

| Intercept | OIL+ | OIL− | OVX+ | OVX− | Σ | P11 | P22 | ||

| Cote d’Ivoire | FX rate | 0.04 (0.642) | −0.096 (0.071) | −0.106 (0.077) | −0.120 (0.075) | −0.115 (0.074) | 0.713 | 0.958 | 0.961 |

| Ghana | FX rate | −0.020 (0.111) | −0.222 (0.132) | −0.254 (0.144) | −0.203 (0.128) | −0.188 (0.119) | 2.218 | 0.793 | 0.880 |

| Mauritania | FX rate | 0.015 (0.072) | −0.051 (0.094) | −0.080 (0.098) | −0.151 (0.090) | −0.137 (0.087) | 0.996 | 0.815 | 0.715 |

| Nigeria | FX rate | 0.502 (0.302) | −0.098 (0.285) | −0.079 (0.296) | −0.703 (0.287) | −0.695 (0.278) | 5.732 | 0.898 | 0.685 |

| Angola | FX rate | −0.211 (0.047) | 0.291 (0.060) | 0.267 (0.062) | 0.155 (0.059) | 0.165 (0.057) | 0.528 | 0.735 | 0.628 |

| Bull | Market | ||||||||

| Intercept | OIL+ | OIL− | OVX+ | OVX− | Σ | P11 | P22 | ||

| Cote divoire | FX rate | 0.048 (0.026) | 0.002 (0.040) | −0.050 (0.041) | −0.013 (0.044) | 0.012 (0.041) | 0.106 | 0.958 | 0.961 |

| Ghana | FX rate | −0.023 (0.012) | −0.012 (0.017) | −0.028 (0.018) | −0.047 (0.017) | −0.040 (0.034) | 0.021 | 0.793 | 0.880 |

| Mauritania | FX rate | 0.045 (0.016) | −0.020 (0.020) | −0.039 (0.022) | −0.044 (0.021) | −0.033 (0.020) | 0.028 | 0.815 | 0.715 |

| Nigeria | FX rate | 0.001 (0.004) | −0.007 (0.006) | −0.006 (0.007) | −0.006 (0.007) | −0.006 (0.006) | 0.004 | 0.898 | 0.685 |

| Angola | FX rate | −0.000 (0.000) | −0.000 (0.000) | 0.000 (0.000) | 0.000 (0.000) | 0.000 (0.000) | 0.000 | 0.735 | 0.628 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Korley, M.; Giouvris, E. The Impact of Oil Price and Oil Volatility Index (OVX) on the Exchange Rate in Sub-Saharan Africa: Evidence from Oil Importing/Exporting Countries. Economies 2022, 10, 272. https://doi.org/10.3390/economies10110272

Korley M, Giouvris E. The Impact of Oil Price and Oil Volatility Index (OVX) on the Exchange Rate in Sub-Saharan Africa: Evidence from Oil Importing/Exporting Countries. Economies. 2022; 10(11):272. https://doi.org/10.3390/economies10110272

Chicago/Turabian StyleKorley, Maud, and Evangelos Giouvris. 2022. "The Impact of Oil Price and Oil Volatility Index (OVX) on the Exchange Rate in Sub-Saharan Africa: Evidence from Oil Importing/Exporting Countries" Economies 10, no. 11: 272. https://doi.org/10.3390/economies10110272

APA StyleKorley, M., & Giouvris, E. (2022). The Impact of Oil Price and Oil Volatility Index (OVX) on the Exchange Rate in Sub-Saharan Africa: Evidence from Oil Importing/Exporting Countries. Economies, 10(11), 272. https://doi.org/10.3390/economies10110272