1. Introduction

Over the last few decades, the banking system has embarked upon drastic change on a global scale. Financial institutions like banks have adopted a diversification approach to move away from a traditional deposit-taking and lending model toward more technologically-driven fees-based and commission-based services, such as e-banking, consumer credits, securities trading, insurance and investment brokerage. This trend appears inevitable since increasing domestic and foreign rivalry in the banking business puts pressure on traditional interest margins. In addition, the quick pace of technological progress also facilitates new services, helps cut transaction costs and saves time for clients. However, the genuine benefits of the new and non-traditional fees-based and commission-based model are still under scrutiny. While recent literature, such as

Chiorazzo et al. (

2008),

Hamdi et al. (

2017),

Meslier et al. (

2014) and

Trivedi (

2015), supports the positive impacts of non-interest income on banks’ profitability, some question whether the new sources of income may entail a higher level of risk and instability (

DeYoung and Roland 2001;

Stiroh 2004;

Williams and Prather 2010).

Upon the expansion of fees-based services in banking industry, a new line of research has been pursued and light has been shed on the causality between fees-based products and the performance of the bank.

Abuzayed et al. (

2018) argued that diversification of income sources into non-correlated activities could decentralize risk and decrease the propensity of financial distress. Moreover, diversification might enhance the intermediation role of banks and motivate managerial efficiency (

Drucker and Puri 2009;

Hamdi et al. 2017).

In contrast, previous literature has challenged the link between diversification and banks, stability, providing evidence that bank size, ownership structure and model are the significant determinants of stability rather than diversification (

Chiorazzo et al. 2008;

Kohler 2015;

Lee et al. 2014). Furthermore,

Lee et al. (

2014) found no evidence supporting the expected benefits of diversification, perhaps because diversified banks tend to take more risks and operate with greater financial leverage than non-diversified counterparts (

Cebenoyan and Strahan 2004).

The new evidence in this recent line of research motivates this research to examine whether the diversification model has positive or negative impacts on the stability of banks. This research extends the literature in the context of ASEAN countries where little evidence is documented, and even if it is, the impacts vary from one country to another (

Lee et al. 2014;

Nguyen and Pham 2020). Additionally, since

King and Levine (

1993) find that financial diversification and bank stability are robustly associated with economic growth, we aim to shed more light on the impacts of economic growth on such a relationship in ASEAN markets.

The impacts of diversification on listed banks’ stability are examined with a modelling approach described in

Kohler (

2015), in which Z score and risk-adjusted profitability measures are the alternative proxies for the stability. The robustness of our findings is controlled with a variety of diversification indicators, non-linear effects, and heterogeneity and endogeneity considerations.

This study aims to determine the extent of the influence of business models on banks’ stability. Our contributions are the empirical evidence along with policy implications regarding business models of banks in ASEAN countries where little is known about the effects of income diversification.

We find that diversification of business models significantly reduces the level of stability at banks in the ASEAN region, except for Malaysia and Thailand where diversification effects are statistically positive. Such findings demonstrate significant different effects of diversification between ASEAN and developed countries.

The paper is organized as follows:

Section 2 reviews the literature on the relationship between bank diversification and stability before the development of hypotheses.

Section 3 outlines the data, variables and methodology, while

Section 4 presents the empirical results.

Section 5 concludes along with several practical implications.

2. Literature Review

Bank stability has been revisited, especially after the failure of banking system during the financial crisis in 2008–2009. Among a variety of factors, diversification emerged and was debated upon in the previous literature. In most research, bank diversification involves two main aspects: income diversification and funding sources diversification. In our paper, we focus on the impacts of income diversification, which are the increase in share of fee, net trading profit and other non-interest income (

Mahdaleta et al. 2016).

Until recently, the literature has suggested a mixed picture of such impacts. A variety of studies reveal positive effects of income diversification on bank stability. For instance,

Froot et al. (

1993) and

Froot and Stein (

1998) emphasize the importance of how income and asset diversification can reduce the probability of bank distress since revenues from different activities are not perfectly correlated. In a study of European banks, the researchers report that the emergence of non-interest income activities contributes to the stability of retail-oriented banks by strengthening the intermediation function and reducing information asymmetries (

Baele et al. 2007;

Kohler 2015).

Acharya et al. (

2006) and

Lepetit et al. (

2008) add that non-interest income could boost competition and financial innovation. The positive evidence of diversification in EU and US banks is also documented in the studies relating to Asia and other emerging countries (e.g.,

Sanya and Wolfe 2011;

Nguyen et al. 2012;

Amidu and Wolfe 2013;

Nguyen and Pham 2020).

Other findings supported the positive impacts by providing further evidence on positive influence of non-credit income on profitability and risk reduction.

Boyd and Prescott (

1986) and

Drucker and Puri (

2009) show that expanding operations across different products and services as well as geographically reduces risk concentration, thereby decreasing the likelihood of financial distress. Such desirable effects are achieved through lower monitoring costs, greater efficiencies, and scale economy of managerial skills. Moreover, evidence from the US, Pakistan, India and the Philippines advocates the positive impacts of income diversification on profitability (

Ismail et al. 2015;

Trivedi 2015;

Li et al. 2021).

Meslier et al. (

2014),

Saunders et al. (

2014) and

Sissy et al. (

2017) highlight that bank performance is boosted via cross-border diversification.

Moreover, the literature shows mixed results on the effects of diversification upon risk and return. While

Craigwell and Maxwell (

2006) and

Stiroh and Rumble (

2006) find that fees-based activities actually darkened the risk profile, they still impose positive effects on profitability.

Sianipar (

2015) claims that although income diversification can lower idiosyncratic and total risk, it does not raise the market value of the bank significantly.

As a result, the link between income diversification and banks’ stability in ASEAN might be distinctive. Little evidence is found in existing papers involving ASEAN banking systems, and almost none is found on the direct causality of income diversification on banks’ stability. A rare paper (

Meslier et al. 2014) provides evidence of positive relationship between income diversification and risk-adjusted performance of banks in Philippines; however, the relationship is insignificant for small banks.

Nguyen and Pham (

2020) examined listed and unlisted banks in Vietnam and demonstrated evidence of diversification impacts on risk mitigation; and such impacts are stronger for unlisted banks and for banks undergoing restructuring. Given the heterogeneity and divergence in size, dynamics, efficiency and technology adopted among ASEAN banking system, income diversification is likely to have dissimilar effects on banks’ stability in each country. Our paper, therefore, seeks to shed more light on that matter.

3. Data and Methodology

3.1. Data

The sample of listed banks in ASEAN is arranged in panel form. The dependent and independent variables data are extracted from Refinitiv Eikon and cross-checked with the official periodical reports of listed banks in ASEAN stock exchanges in 2011–2019 period. Bank data has tremendous advantages over corporate data with respect to accuracy, especially for listed banks, since such data are input by better-trained staff and checked by internal audit, creditworthy auditors and the central bank.

Using equity screening application on Refinitiv Eikon, we collected the initial sample consisting of 236 banks and 2585 observations from 2010 to 2019 of five ASEAN countries (Vietnam, Thailand, Indonesia, Malaysia and Philippines). In all countries, except for Vietnam, under the name of one bank there were numerous types of equity, including ordinary shares, American Depositary Receipts (ADRs), non-voting depositary receipts, and rights and preference shares. However, we just keep the ordinary shares to avoid duplication, resulting in a drop of 124 datapoints and 693 observations. We further filtered out missing dependent variables for two consecutive years to keep the series in each datapoint sufficiently long to be consistent with a more robust econometric technique (i.e., the DGMM). The final sample comprised 99 banks and 987 observations. All of the observations were free from outlier problem since they were winsorized at the 5% and 95% levels.

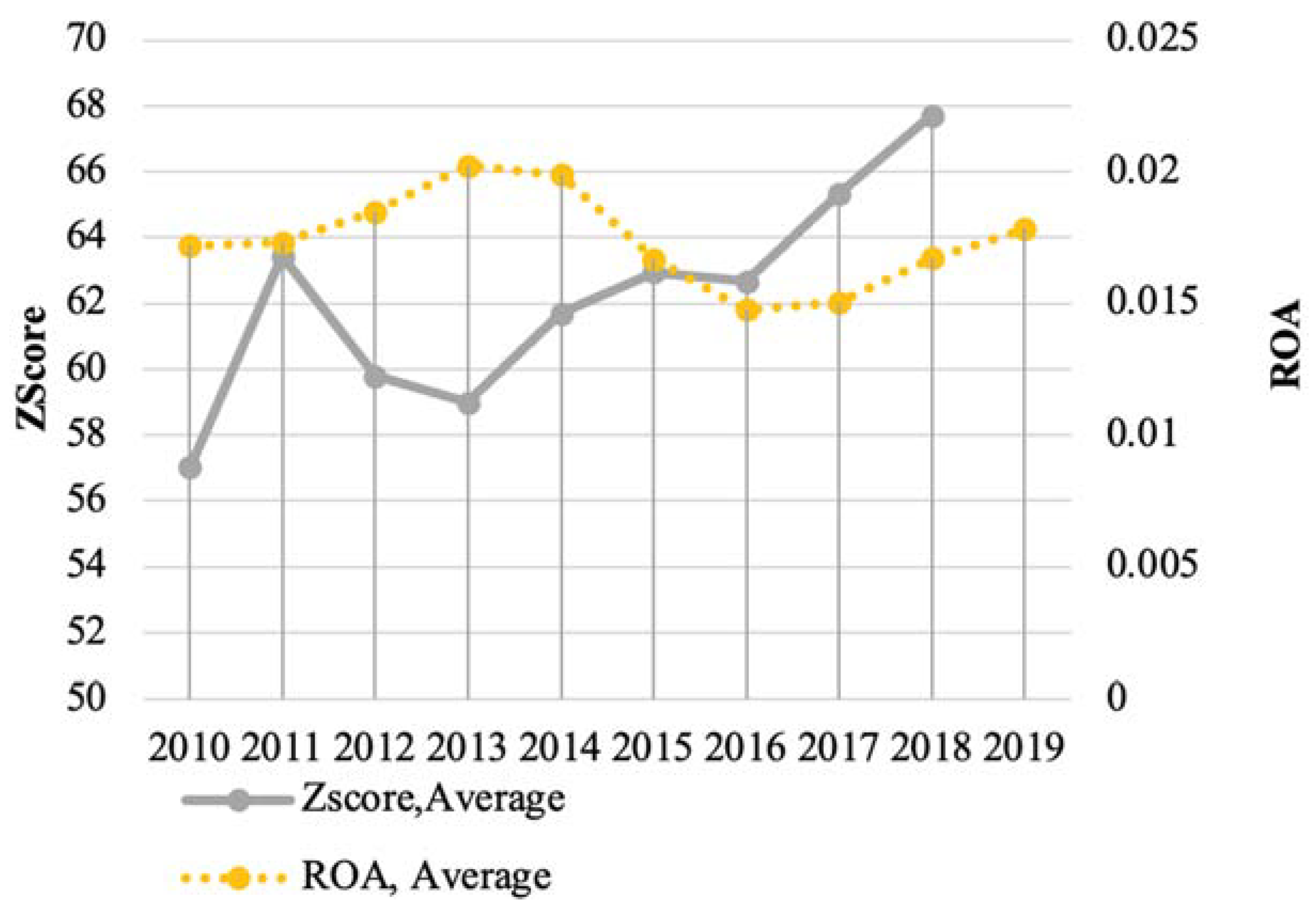

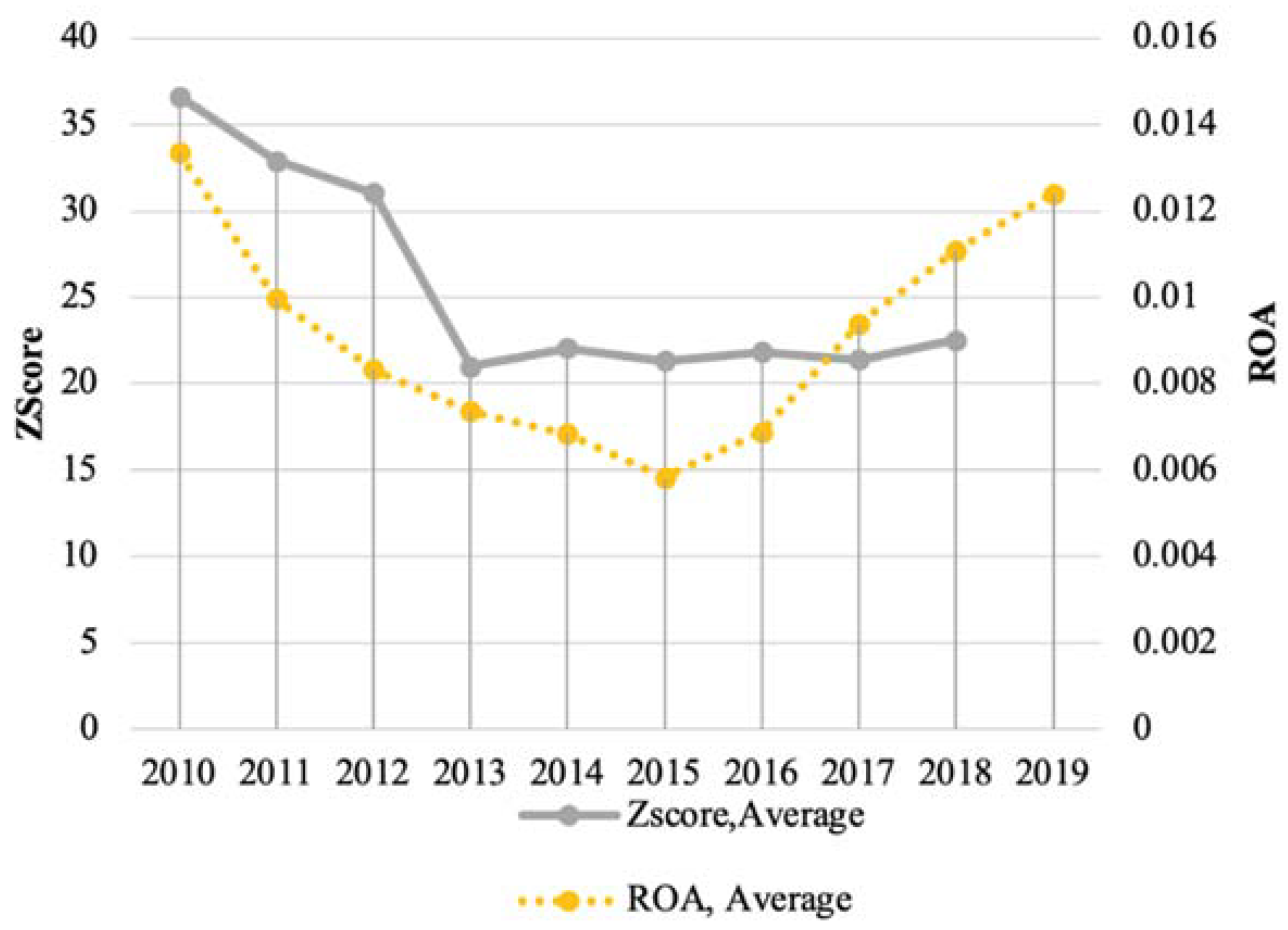

In the sample, we employed several alternative proxies for bank’s stability, including Z-score, risk-adjusted return on assets (RAROA) and risk-adjusted capital adequacy ratio. Z-score was calculated by the sum of ROA and CAR, divided by SDROA, where ROA was return on assets, CAR was the fraction of total equity divided by total assets and SDROA was the standard deviation of ROA. To enhance the robustness, RAROA and RACAR were also considered as varieties of risk-adjusted measures for banks’ stability. According to

Kohler (

2015), the higher Z-score or RAROA or RACAR entails lower risk and higher stability.

Regarding independent groups of variables, net interest income (NII) is the one that best captures the traditional interest-based business model. The spread between lending and deposit rates has been a major income source of banks and hence is supposed to exert positive effects on banks’ stability (

Kohler 2015). Alternatively, net non-interest income (NNII) and trading are proxies for non-traditional and fees-based sources of income. NNII and trading activities help banks diversify their revenue streams to spread the risks inherently concentrated on conventional interest-based products and services. NNII and trading could enhance banks’ sustainability for commercially-oriented banks, while they may undermine stability since excessive engagement in fee-generating activities such as currency trading or off-balance sheet securitization tends to damage one’s risk profile (

Kohler 2015;

Altunbas et al. 2011;

DeYoung and Roland 2001).

In principle, most of the variables in the final sample are kept in the fraction form, except for total assets, which is converted to log form to reduce the skewness and enhance variance stability (

Lütkepohl and Xu 2010). Detailed formulae and description for each variable are presented in

Table 1.

3.2. Methodology

The potential causality between income diversification and banks’ stability is examined with a standard linear function. To ensure the robustness of findings, the usual suspects of endogeneity, spatial dependence and country heterogeneity are controlled by Driscoll–Kraay’s robust error and Difference Generalized Method of Moments (DGMM).

We adopt the functional model from

Kohler (

2015) as follows:

With a cross-country panel data, one of the potential selection biases lies in the time-invariant country confounder in that the hypothetical change in the independent or control variables within the same country could inflate the impacts on the dependent variables in an OLS regression model (

Mummolo and Peterson 2018). This paper limits selection bias caused by country heterogeneity with country fixed-effects model. We further control for spatial dependence, heteroscedasticity and serial correlation problems with Driscoll–Kraay’s robust standard errors. Finally, one of the key econometric issues in panel data analysis is potential endogeneity bias since it can yield misleading conclusions or even incorrect signs of the coefficients (

Ullah et al. 2018). Indeed,

Wooldridge (

2010) proved that the omitted and observed/unobserved variables unincorporated in the model are the causes of such endogeneity. Accordingly, we control for the omitted variables as well as potential pairwise correlation between independent variables and the error term with the endogenous treatment in the Difference Generalized Method of Moments (DGMM) model. Specifically, the initial equation in DGMM model is as follows:

Equation (2) is transformed into first-difference form to suppress potential fixed effects assumed in panel data.

5. Conclusions and Implications

With the rise of diversification in the banking business, little is known about the impacts of a diversification model switch, especially in emerging markets. Hence, we set forth to examine whether a gradual change of business model into diversification has positive or negative effects on banks’ stability. We employed net non-interest income (NNII) and foreign exchange trading activities (TRADE) as corresponding proxies for diversification and fees-based activities, and conducted a variety of robustness checks on model levels upon sampling listed banks in ASEAN countries. Our findings indicate that NNII and other fees-based activities (TRADE) tend to have negative impacts on the stability of banks in ASEAN. Evidently, traditional interest-based activities are still key drivers of income for ASEAN banks, and the recent gradual switch to fees-based services has not yet produced a significant effect.

5.1. Theoretical Implications

With evidence of a significant and negative link between the diversification of business models and the stability of ASEAN banks, this paper extends existing empirical evidence of the diversification impacts on banks’ stability with regard to emerging financial markets. Even though the ongoing trend of the fees-based activities model persists, diversification seems to be a barrier to banks’ development and stability in Vietnam, Indonesia, Thailand and Philippines. On the contrary, the more developed financial environments, as in Malaysia, are likely to be motivated by the significant and positive impacts of fees-based diversification. Hence, future research may focus on the mediating effects of factors related to the financial environment on the relationship between diversification models and banks’ stability.

5.2. Practical Implications

The findings can serve as a reference for banks in ASEAN to help them build a more efficient business model in that banks in more developed countries may reach for the fruit of income and fees-based diversification more effectively than their less-developed counterparts in ASEAN region. More specifically, the findings on the negative impacts of diversification suggests that a decision to switch from a traditional to a more fees-based model should be examined more thoroughly on a case-by-case basis, especially for banks in Vietnam and Indonesia. However, in a country with a more developed financial market such as Malaysia, the ostensibly positive sign of diversification motivates the gradual switch to a more contemporary fees-based business model.

{kind=link}

{kind=link}