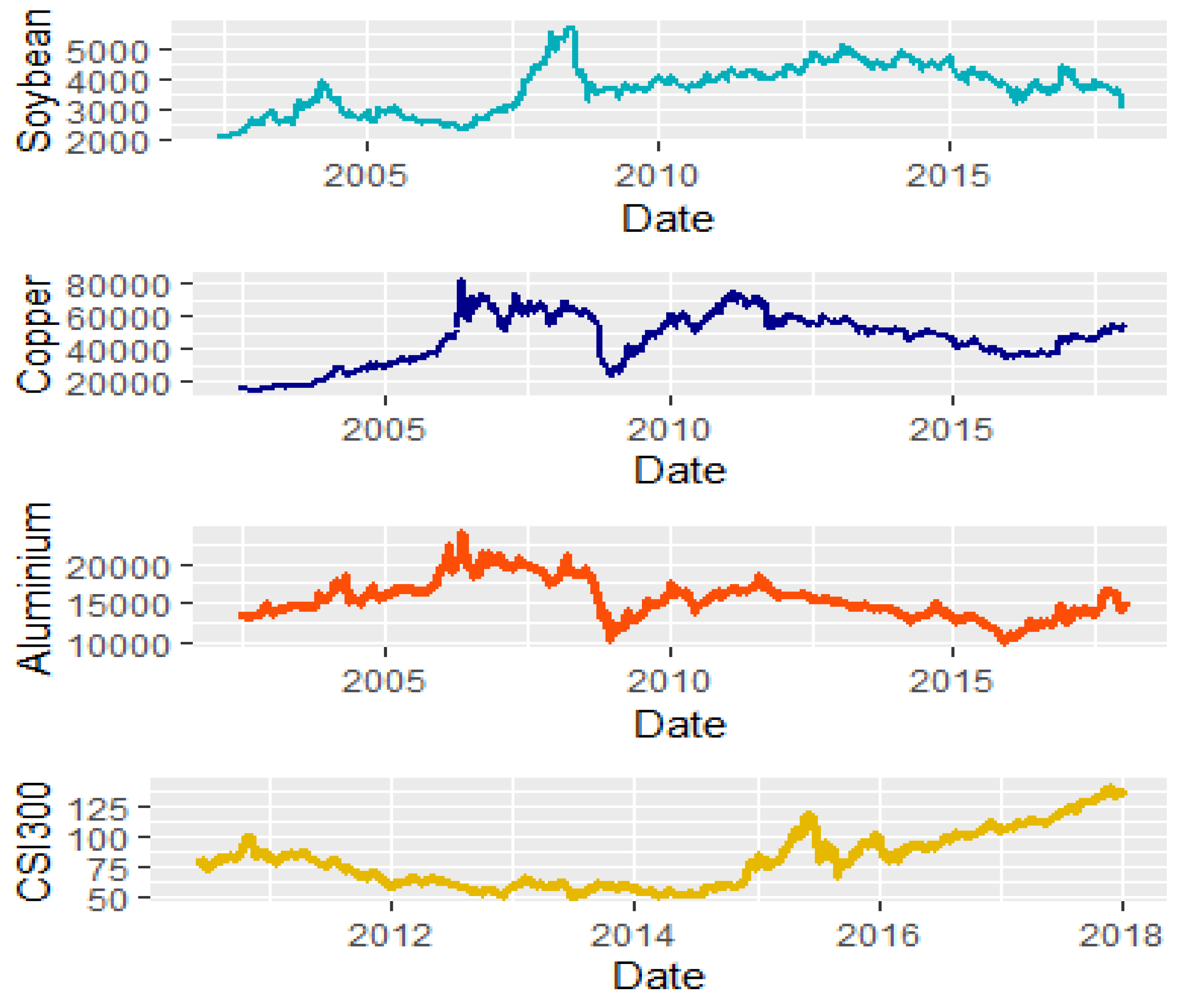

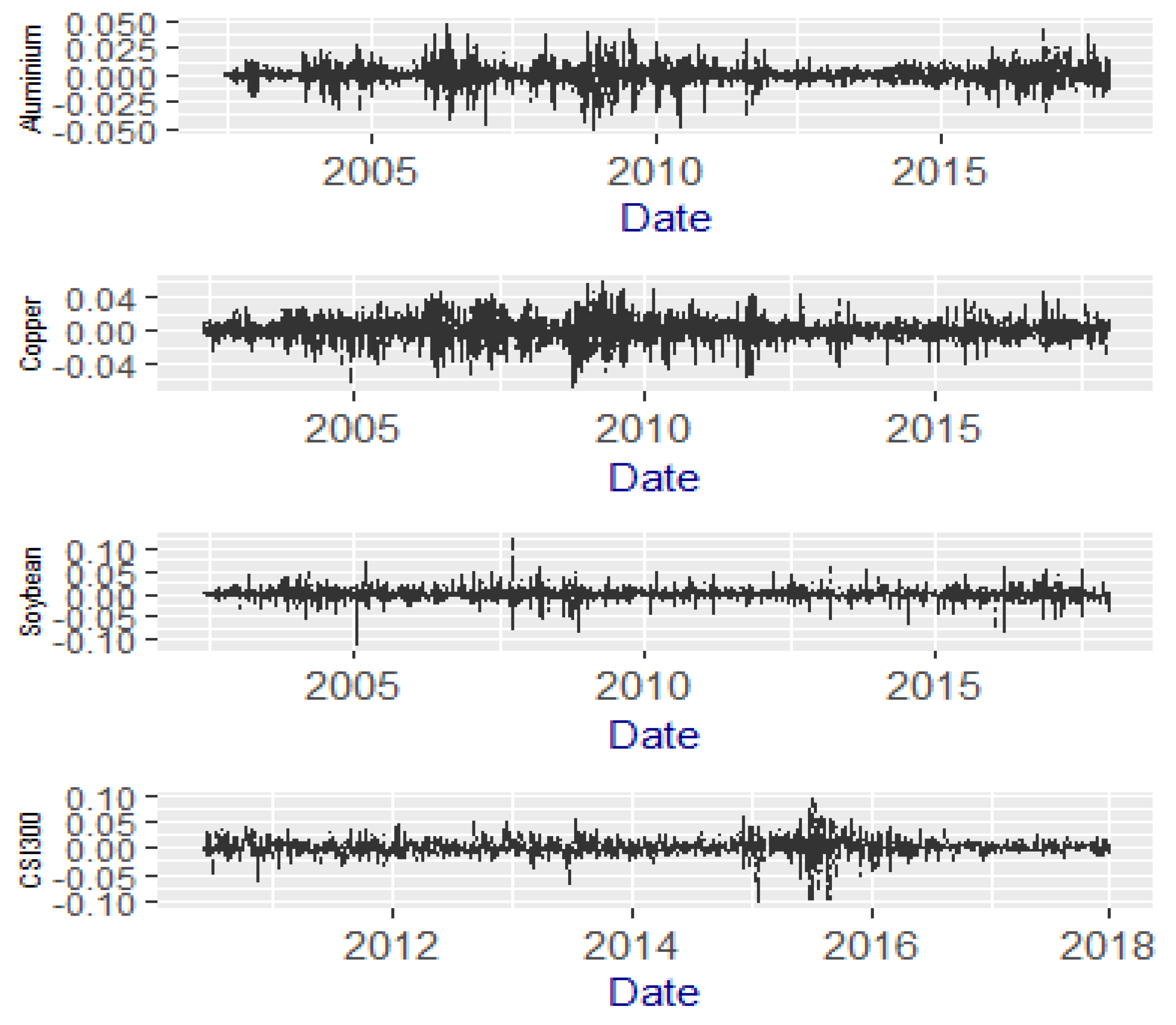

In this part, we provide empirical results. The results can be divided into two parts. First, we report the GARCH-MIDAS model with realized variance. Second, we explore the GARCH-MIDAS model with macroeconomic variables.

3.1. Model with Realized Variance

To build a proper model with macroeconomic fundamentals, we should define the optimal period of

t and MIDAS lag period, which decide the secular component of the volatility

. In the GARCH-MIDAS with fixed-span RV, we employ the log-likelihood function, AIC (Akaike information criterion), and BIC (Bayesian information criterion) as the criteria. The log-likelihood function is as follows:

The optimal number of lags is decided by maximizing the value of LLF and minimizing the AIC and BIC. In the paper, we set the period is 22, which is the monthly aggregation.

In the GARCH-MIDAS model, we use 9-month MIDAS lag years to achieve the best performance of the secular component volatility. This means a history of 9 months’ realized volatility will be averaged by the MIDAS weights to determine the long-run conditional variance. The nine lag months cost 198 observations for initialization.

Table 5 illustrates the coefficient estimates of the GARCH-MIDAS model with realized variance as estimated by Equations (1)–(7). The parameter estimates for the commodities futures and the CSI 300 stock index futures are reported in the first six columns with the corresponding

t-statistics reported in parentheses. The

s of the GARCH-MIDAS models with RV are strongly significant and positive, which means in the Chinese futures market, the RV has a significantly positive influence on the long-run variance. The high-level RV will lead to higher long-run variance.

In the GARCH-MIDAS models with commodity futures, the sums of α and β are less than 1, which means the short-run variances in the commodities futures market has a lower persistence.

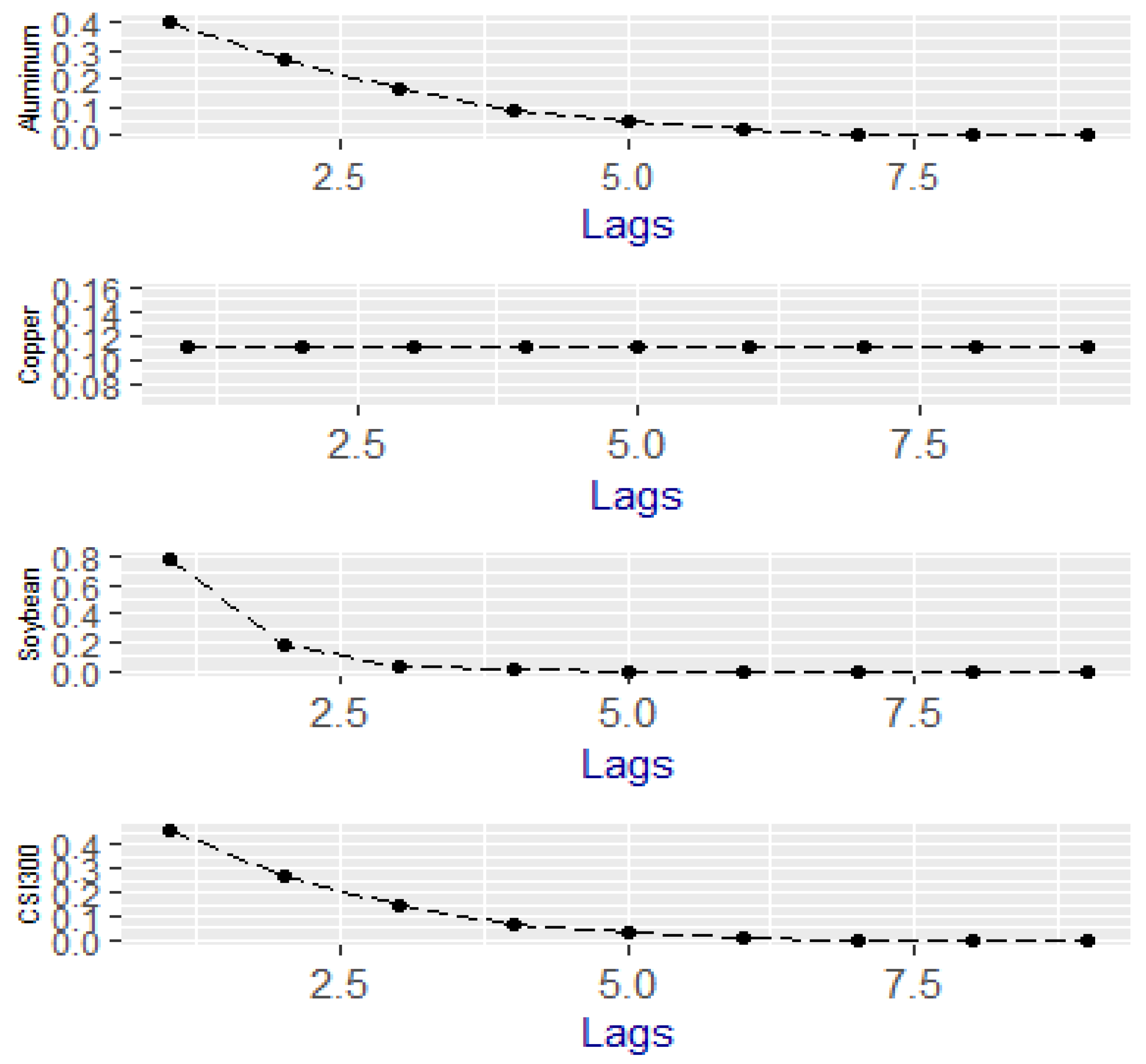

Figure 3 illustrates the estimated exponential weights of the GARCH-MIDAS model with the fixed span RV for the 9-month lag.

Figure 3 shows the optimal weights of the Aluminum, Soybean, and CSI 300. From

Figure 3, we know the optimal weights of the four weights return decay with the increase of the lags.

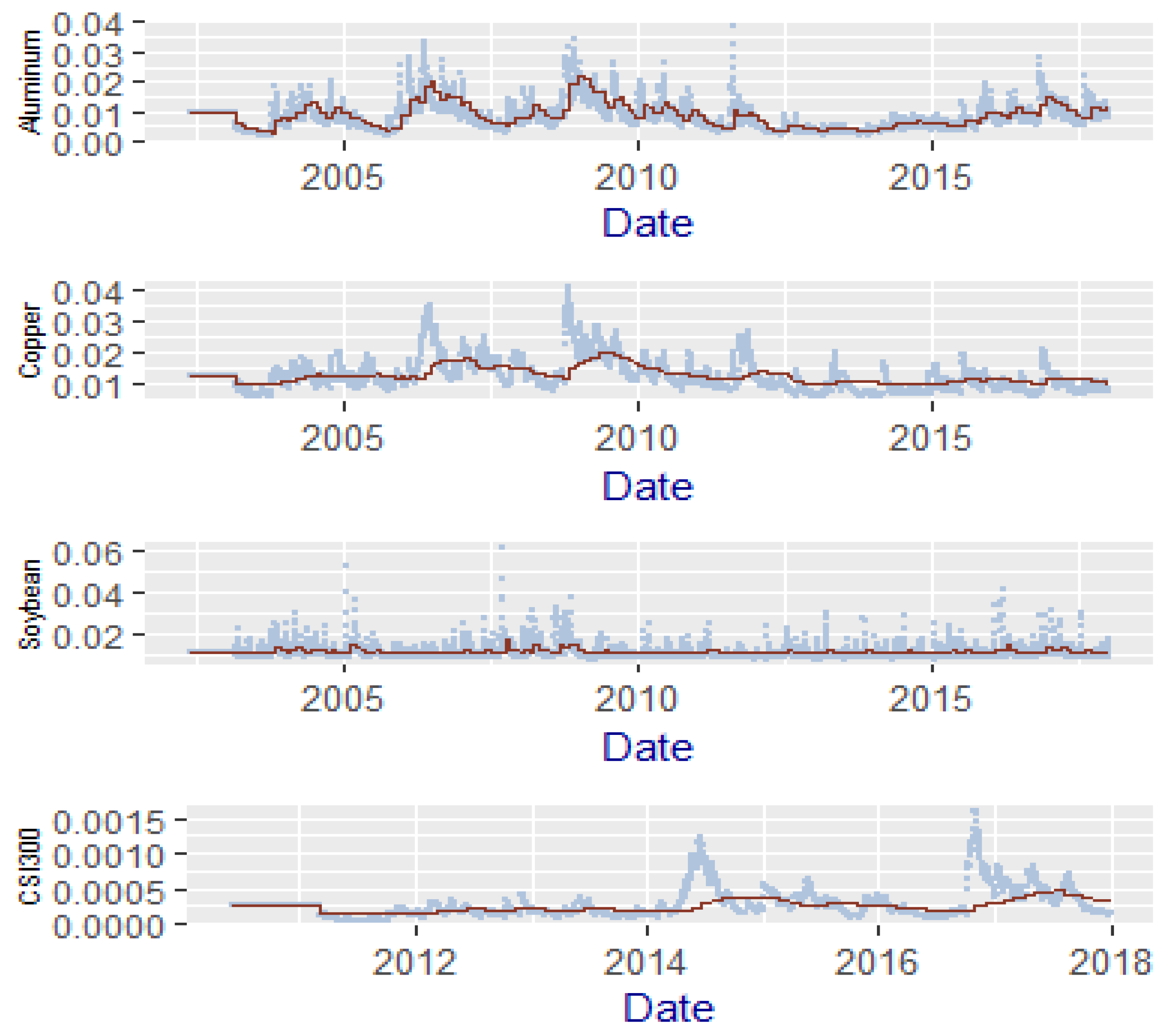

Figure 4 displays the different volatility components in the GARCH-MIDAS model with the fixed-span RV. The dashed lines are the conditional volatility in the futures market, while the solid lines stand for the secular component of the volatility in the GARCH-MIDAS model. In the GARCH-MIDAS model, the secular component is volatility, with the information of the lagging RV, and looks smoother.

Figure 3 illustrates the exponential lag weights for the GARCH-MIDAS model with fixed-span RV over the full sample period. The GARCH-MIDAS with monthly fixed-span RV uses nine lagged monthly RV in the MIDAS regression.

Figure 4 shows the estimated conditional variance and the secular component of GARCH-MIDAS model with monthly fixed RV in the MIDAS filter. In the GARCH-MIDAS model, we set the lag as 9. The solid line is the conditional variance and the dotted line is the long-run variance.

Table 5 illustrates the parameter estimates of the GARCH-MIDAS model is fitted with monthly fixed span RV.

µ,

α,

β,

θ and W are the parameters in the GARCH-MIDAS model. LLF, AIC, and BIC are the likelihood function value, AIC value, and BIC value. We set the lag is 9. The

in the table is

, the optimal

is 1. The numbers in parentheses are robust t-statistics computed with HAC standard errors.

3.2. Model with Macroeconomic Variables

How do macroeconomic fundamentals influence the volatility of futures returns? In this part, we try to answer the question.

Schwert (

1989),

Engle and Rangel (

2008),

Engle et al. (

2013) try to explain how much the macroeconomy affects the stock return volatility.

Schwert (

1989),

Engle et al. (

2013) employ the IP growth rate and PPI as the macroeconomic fundamentals and test the relationship between the macroeconomic variables and the stock market returns at monthly and quarterly horizons. Based on the references, we employ the IP, PPI, CPI, M2, and short-term interest rate as the macroeconomic fundamentals.

In the paper, we are interested in linking the daily futures return volatility with the monthly macroeconomic data. We start with the specifications involving the macroeconomic series, the level of IP, PPI, CPI, M2, and short-term interest rate. In the paper, we focus on the one-side filters. We employ the different weighting schemes to test the relationship between the level of macroeconomic series and the long-run variance. The parameter estimates of the GARCH-MIDAS model with the level of macroeconomic series are illustrated in

Table 6,

Table 7,

Table 8,

Table 9 and

Table 10.

Table 6 illustrates the parameter estimates of GARCH-MIDAS models with the level of CPI. For the specifications with macroeconomic level in the MIDAS filter, nine lags are taken into the GARCH-MIDAS model. The numbers in the parentheses are the

t-statistics of the estimated parameters.

Table 7 illustrates the parameter estimates of GARCH-MIDAS models with the level of IP. For the specifications with macroeconomic level in the MIDAS filter, nine lags are taken into the GARCH-MIDAS model. The numbers in the parentheses are the

t-statistics of the estimated parameters.

Table 8 illustrates the parameter estimates of GARCH-MIDAS models with the level of PPI. For the specifications with macroeconomic level in the MIDAS filter, nine lags are taken into the GARCH-MIDAS model. The numbers in the parentheses are the

t-statistics of the estimated parameters.

Table 9 illustrates the parameter estimates of GARCH-MIDAS models with the level of M2. For the specifications with macroeconomic level in the MIDAS filter, nine lags are taken into the GARCH-MIDAS model. The numbers in the parentheses are the t-statistics of the estimated parameters.

Table 10 illustrates the parameter estimates of GARCH-MIDAS models with the interest rate level. The results of the GARCH-MIDAS model including the CSI 300 futures are parsimonious, and we only test the relationship between the commodity futures and interest rate. For specifications with macroeconomic level in the MIDAS filter, nine lags are taken into the GARCH-MIDAS model. The numbers in the parentheses are the

t-statistics of the estimated parameters.

In

Table 6,

Table 7,

Table 8,

Table 9 and

Table 10, the most notable parameters are the slope parameters of

for the specification of the MIDAS filter. For the GARCH-MIDAS with the CPI time series, the

ranges from 0.0015 to −0.0046. For the commodity futures, the slope parameters are positive; for the CSI 300 stock index futures, the

is negative. From the

t-statistics, we know the slope parameters are all statistically significant, which indicates the increase of the inflation level leads to a higher commodity futures return volatility. For the CSI 300 stock index futures, the increase of inflation level leads to a lower volatility of stock index futures return.

For

Table 7, we can know the parameter estimates of the GARCH-MIDAS model with the industrial production index. The slope parameter

ranges from −0.031 to 0.00085. For the aluminum futures, soybean futures, and CSI 300 stock index futures, the slope parameters are statistically negative, which means high-level industrial production decreases the return volatility in aluminum futures, soybean futures and the CSI 300 futures market. The increase in the output in manufacturing, mining, electric, and gas industry will decrease the aluminum futures, soybean futures, and CSI 300 futures return volatility. For copper futures, the slope parameter

is positive, which indicates the increase in industrial production increases the copper futures return volatility.

Table 8 reports the GARCH-MIDAS with producer price index, the most interesting parameter

ranges from −0.0019 to 0.00022. In all the GARCH-MIDAS model, the slope parameters are all statistically significant. For the commodity futures return, the increase of the PPI index leads to a higher commodity futures return volatility. For the GARCH-MIDAS model with CSI 300 futures return, the

is significantly negative, which indicates the increase of the PPI index leads to a lower CSI 300 futures return volatility. The empirical results show that the increase in the selling price leads to a higher commodity futures return volatility. The increase in the selling price of the domestic producers decreases the CSI 300 futures return volatility.

Table 9 illustrates the GARCH-MIDAS model with M2. The slope parameter

ranges from −0.004 to 0.0005. For the aluminum futures and the copper futures, the

is statistically positive, which means the increase of money supply leads to a higher aluminum futures and copper futures return volatility. For the soybean futures and the CSI 300 stock futures, the slope parameters are negative, which illustrates the increase of the money supply decreases the futures return volatility in the soybean futures and CSI 300 futures market.

Table 10 shows the parameter estimates of the GARCH-MIDAS model with a short-term interest rate. As the parameter estimates of the stock index futures are parsimonious,

Table 10 only reports the parameter estimates of the commodity futures. The parameter estimates of the

in the GARCH-MIDAS model with short-term interest rate range from −0.0047 to 0.28. In all GARCH-MIDAS models with a short-term interest rate, the parameter estimates of

are all statistically significant. For the aluminum futures and soybean futures, the slope parameters are negative, which means higher short-term interest rate leads to a lower aluminum and soybean futures return volatility. For the copper futures, the parameter estimates are 0.28 with a

t-statistic of 5.86. The parameter estimates of

indicates the higher short-term interest rates will increase the volatility in the Copper futures market.

In this part, we show the relationship between the level of macroeconomic variables and the futures return volatility. To examining the domestic macroeconomic determinants of the volatility of futures returns, we introduce the CPI, IP, PPI, M2, and short-term interest rate into the GARCH-MIDAS model. The research can be divided into two parts: the commodity futures and stock index futures. For the commodity futures market, the macroeconomic fundamentals have a different impact on the commodity futures volatility. CPI and PPI are the economic indicators, which measure the price fluctuations for goods and services. CPI measures expenditures of consumer-related services for residents. PPI evaluates the average changes in the sales prices for the entire domestic market of raw goods and services. M2 measures the money supply, including the elements of M1 and ‘near money.’

According to the empirical results, we can conclude two interesting results. First, based on the parameter estimates of

, we know that parameter estimates of

in the GARCH-MIDAS model with CPI and PPI are all positive, which means the increase of the inflation in the market will lead to higher-level commodities futures return. Second, from

Table 6,

Table 7,

Table 8 and

Table 9 we know the parameter estimates of

in the GARCH-MIDAS model with CSI 300 stock index futures are all negative. The empirical results illustrate that a high level of inflation, industrial production, and money supply will decrease the long-run variance in CSI stock index futures returns.

{kind=link}

{kind=link}

{kind=link}

{kind=link}