The Role of Canceled Warrants in the LME Market

Abstract

:1. Introduction

2. Literature Review

3. Research Model and Data

3.1. Research Model

3.2. Data

3.3. Stationarity Check: Unit Root Tests

4. Empirical Results

4.1. Regression Results

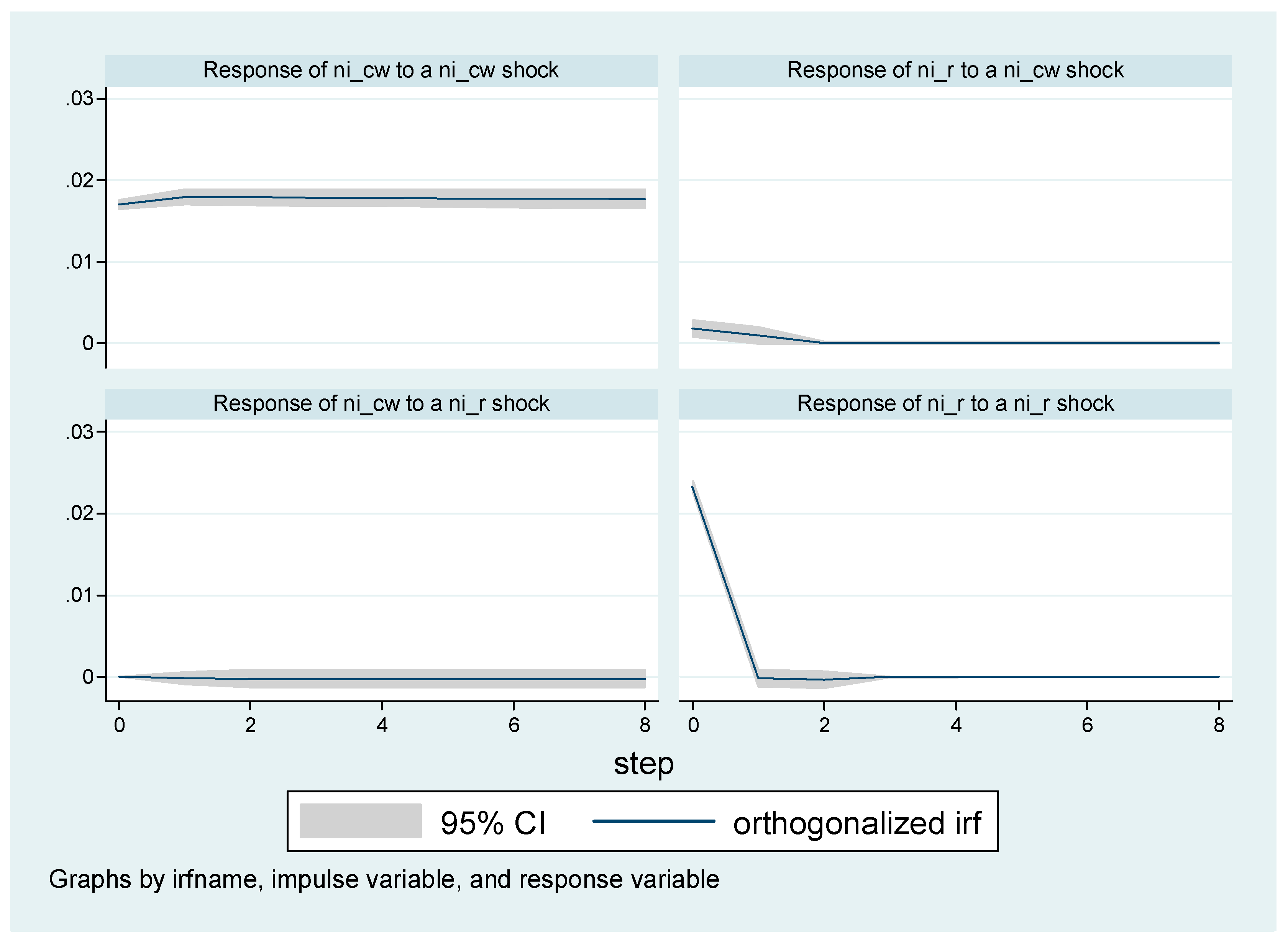

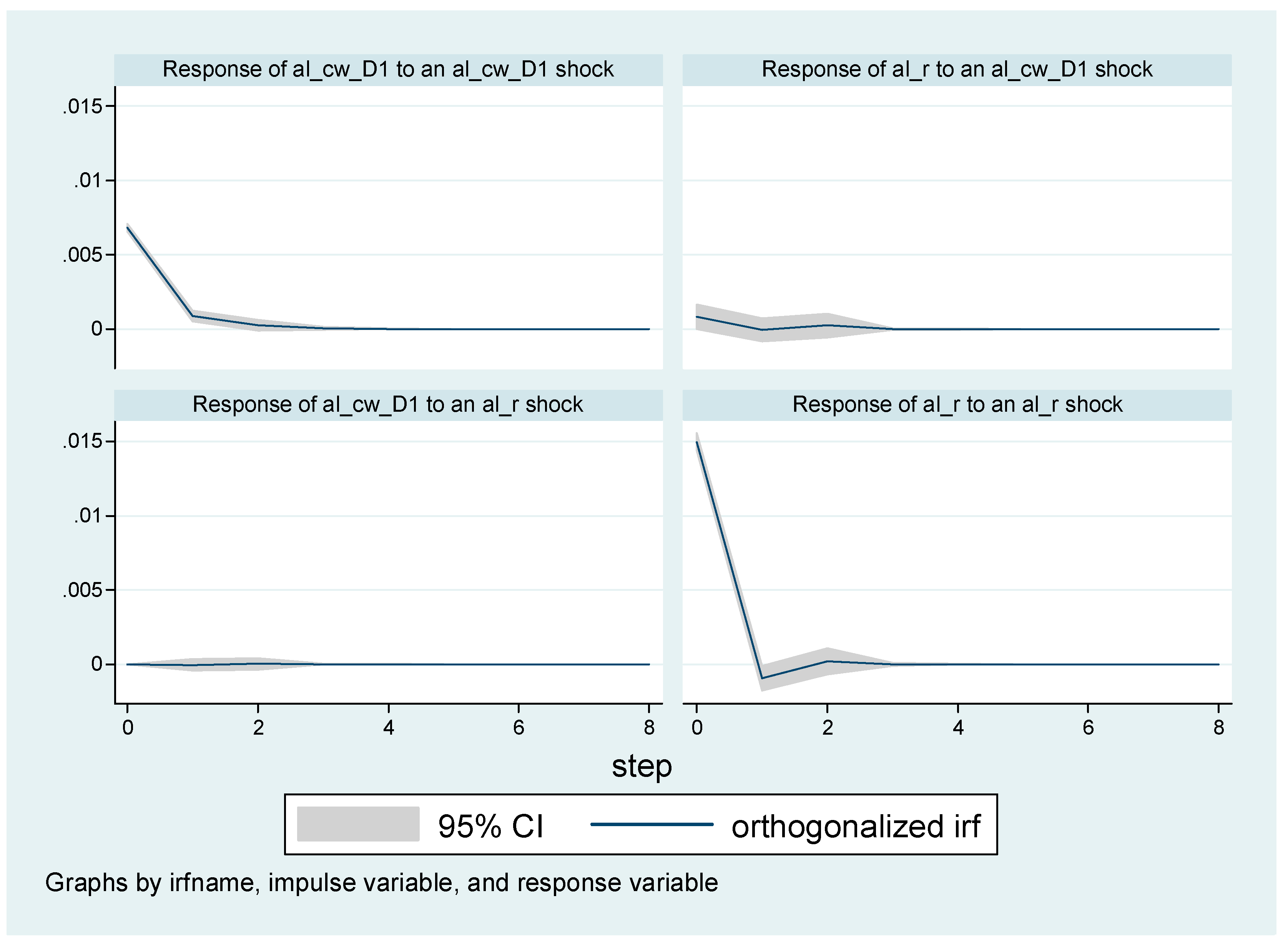

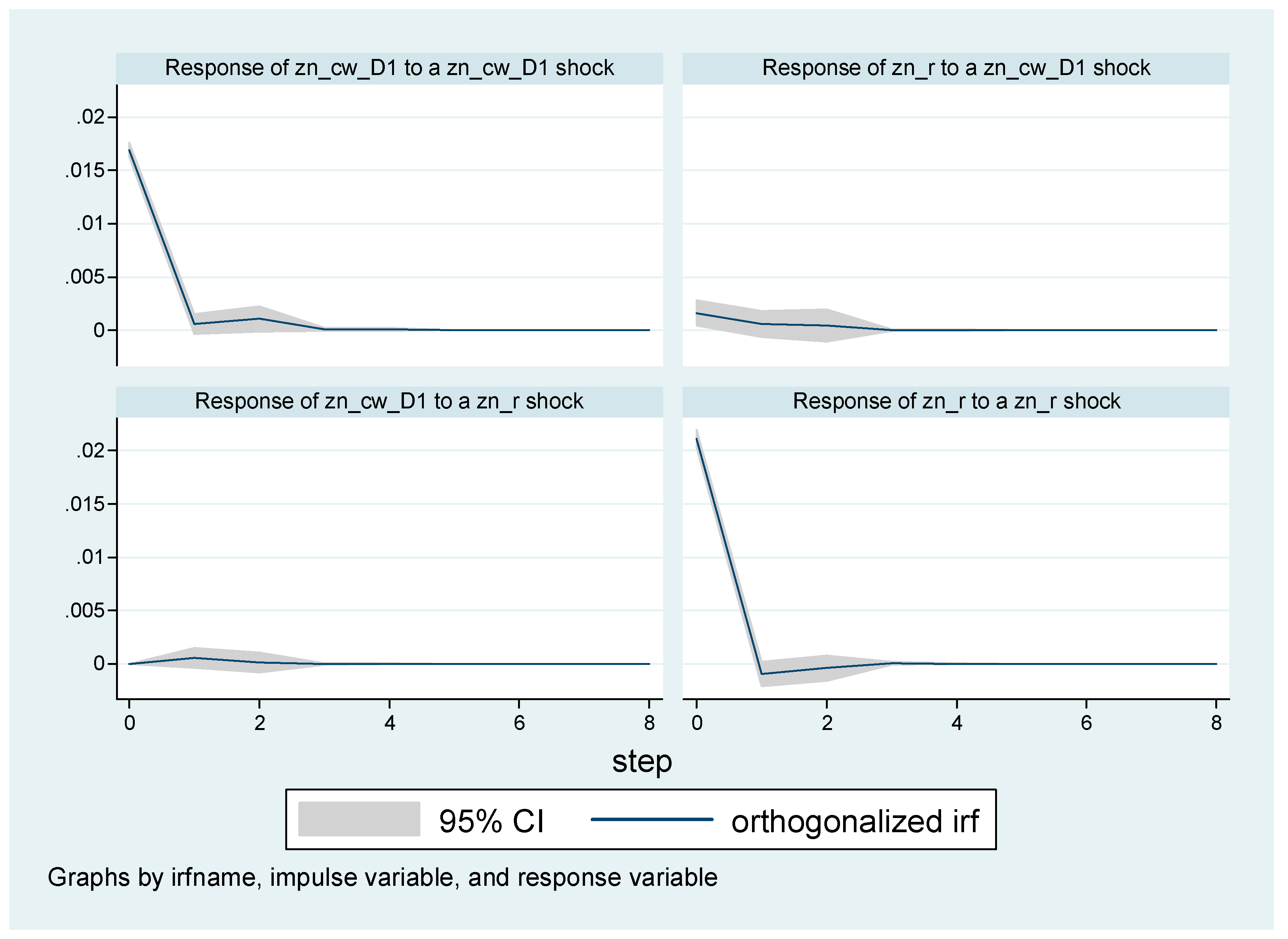

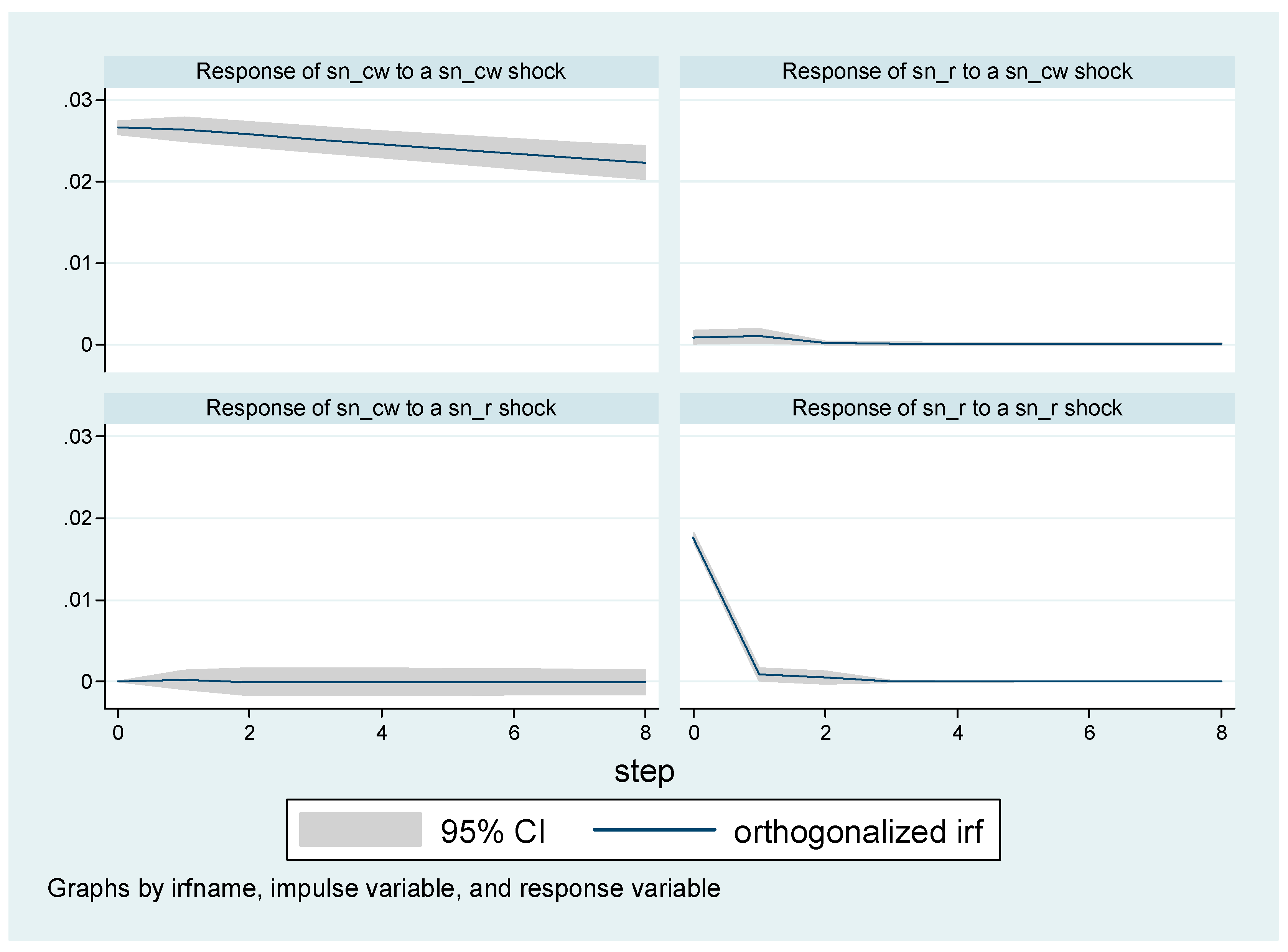

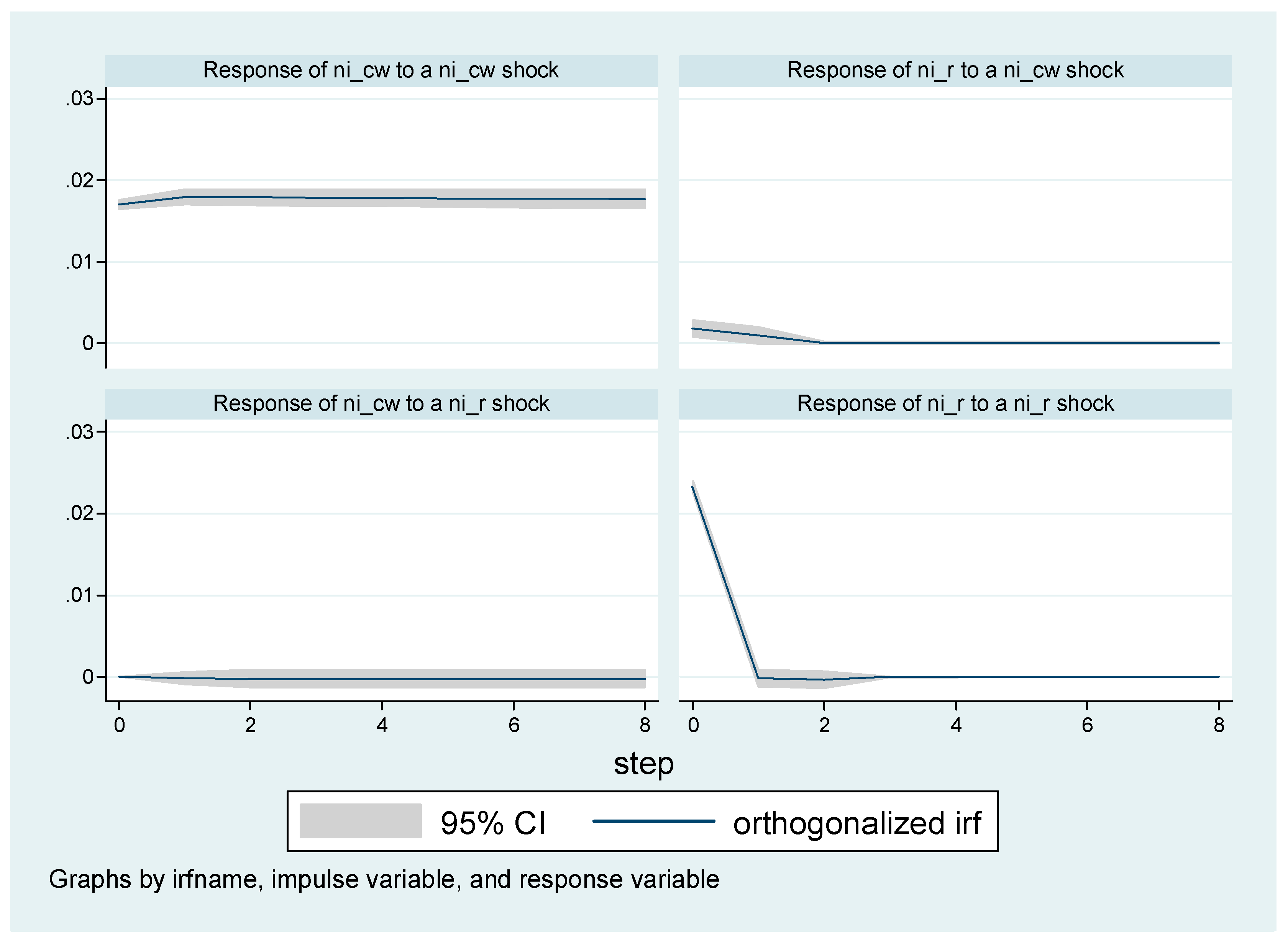

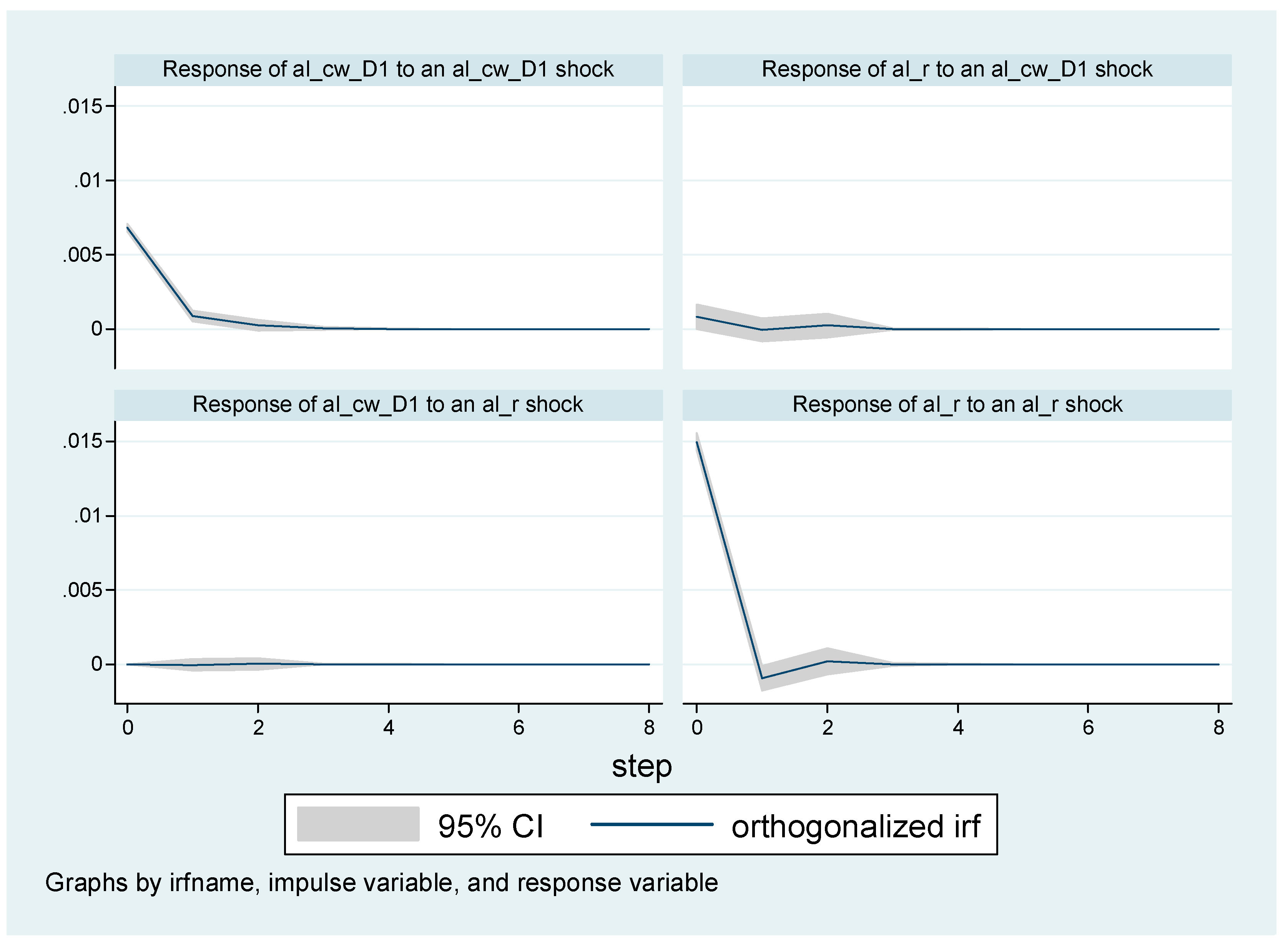

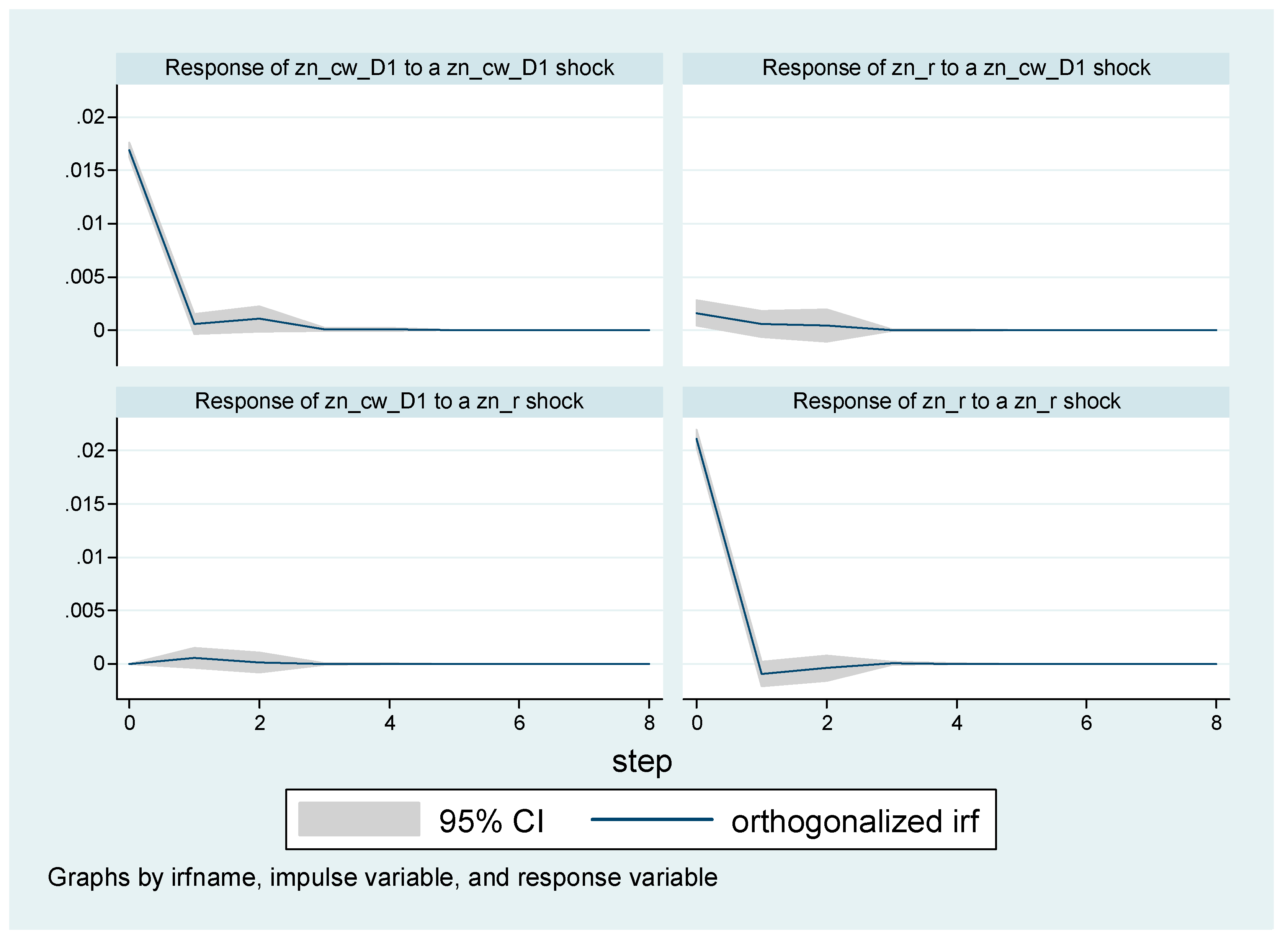

4.2. VAR Model Specifications and Impulse Response Results

5. Summary and Conclusions

Funding

Acknowledgments

Conflicts of Interest

References

- Arouri, Mohamed El Hedi, Fredj Jawadi, and Prosper Mouak. 2011. The Speculative Efficiency of the Aluminum Market: A Nonlinear Investigation. International Economics 126–27: 73–89. [Google Scholar] [CrossRef]

- Canarella, Giorgio, and Stephen K. Pollard. 1986. The “Efficiency” of the London Metal Exchange: A Test with Overlapping and Non-Overlapping Data. Journal of Banking and Finance 10: 575–93. [Google Scholar] [CrossRef]

- Cheng, Ing-Haw, and Wei Xiong. 2014. Financialization of Commodity Markets. Annual Review of Financial Economics 6: 419–41. [Google Scholar] [CrossRef]

- Figuerola-Ferretti, Isabel, and Christopher L. Gilbert. 2008. Commonality in the LME Aluminum and Copper Volatility Processes through a FIGARCH Lens. The Journal of Futures Markets 28: 935–62. [Google Scholar] [CrossRef]

- Guzmán, Juan Ignacio, and Enrique Silva. 2018. Copper Price Determination: Fundamentals versus Non-fundamentals. Mineral Economics 31: 283–300. [Google Scholar] [CrossRef]

- Irwin, Scott H., and Dwight R. Sanders. 2012. Testing the Masters Hypothesis in commodity futures markets. Energy Economics 34: 256–69. [Google Scholar] [CrossRef]

- Kang, Sang Hoon, and Seong-Min Yoon. 2016. Dynamic Spillovers between Shanghai and London Nonferrous Metal Futures Markets. Finance Research Letters 19: 181–88. [Google Scholar] [CrossRef]

- Koitsiwe, Kegomoditswe, and Tsuyoshi Adachi. 2018. The Role of Financial Speculation in Copper Prices. Applied Economics and Finance 5: 87–94. [Google Scholar] [CrossRef]

- MacDonald, Ronald, and Mark Taylor. 1988. Metal Prices, Efficiency and Cointegration: Some Evidence from the LME. Bulletin of Economic Research 40: 235–39. [Google Scholar] [CrossRef]

- Otani, Kiyoshi. 1983. The Price Determination in the Inventory Stock Market: A Disequilibrium Analysis. International Economic Review 24: 709–19. [Google Scholar] [CrossRef]

- Otto, Sascha Werner. 2011. A Speculative Efficiency Analysis of the London Metal Exchange in a Multi-Contract Framework. International Journal of Economics and Finance 3: 3–16. [Google Scholar] [CrossRef]

- Park, Jaehwan. 2018. Volatility Transmission between Oil and LME Futures. Applied Economics and Finance 5: 65–72. [Google Scholar] [CrossRef]

- Park, Jaehwan. 2019. Effect of Speculators’ Position Changes in the LME Futures Market. Working Paper. under review. [Google Scholar]

- Park, Jaehwan, and Byungkwon Lim. 2018. Testing Efficiency of the London Metal Exchange: New Evidence. International Journal of Financial Studies 6: 32. [Google Scholar] [CrossRef]

- Singleton, Kenneth J. 2014. Investor Flows and the 2008 Boom/Bust in Oil Prices. Management Science 60: 300–18. [Google Scholar] [CrossRef]

- Tang, Ke, and Wei Xiong. 2012. Index Investment and the Financialization of Commodities. Financial Analysts Journal 68: 54–74. [Google Scholar] [CrossRef]

| 1 | The LME opened in 1877; it has continued strengthening since then, and became recognized as the global benchmark for the metal market. Major producers and consumers use LME contracts for hedging price risks, and for the reference price for spot and future prices. Park and Lim (2018) provided a good discussion of the LME. They found that the LME was an inefficient market due to financialization by institutional investors. |

| 2 | See details in Metal Bulletin (http://www.metalbulletin.com/Glossary.html). The CWs are the ratio of CWs to total warrants, where total warrants are the on warrants and canceled warrants. |

| 3 | This information is a valuable investment factor of consumption trends, which can provide a meaningful implication of possible future price directions. |

| 4 | The LME does not report intra-day data and tick data. It is not possible to compute daily realized volatility measures for LME markets (Figuerola-Ferretti and Gilbert 2008). They used monthly rather realized volatility data. |

| 5 | Figuerola-Ferretti and Gilbert (2008) concluded that the LME aluminum and copper scedastic processes are both highly persistent. They argued that the strong symmetry of the two processes implied that the processes may be the outcome of common market microstructure factors. |

| 6 | Koitsiwe and Adachi (2018) reported that commodity assets under management by financial investors dramatically increased in value, from about $13 billion in 2003 to $450 billion in 2011. Irwin and Sanders (2012) reported that a total of $161.2 billion was invested in commodity index investments as of 31 March 2010. A total of 78% of index investments were in the U.S. futures market, which invited major index funds with rising trading volumes. |

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Inventories | CW Ratio | Effect on Metal Price |

|---|---|---|

| Up | Down | Negative |

| Down | Up | Positive |

| Variable | Mean | Standard Deviation | Skewness | Maximum | Minimum | Kurtosis | Jarque-Bera | |

|---|---|---|---|---|---|---|---|---|

| copper | cu_cw | 0.1836 | 0.1564 | 1.0898 | 0.6742 | 0.0013 | 3.3818 | 458.75 (0.00) |

| cu_r | 0.0002 | 0.0182 | 0.1461 | 0.1244 | −0.0980 | 6.8328 | 307.12 (0.00) | |

| aluminum | al_cw | 0.2194 | 0.1821 | 0.3844 | 0.5996 | 0.0037 | 1.7159 | 7548.3 (0.00) |

| al_r | 0.0005 | 0.0148 | −0.0069 | 0.0660 | −0.0752 | 4.7523 | 133.47 (0.00) | |

| lead | pb_cw | 0.1827 | 0.1792 | 0.9114 | 0.7752 | 0.0004 | 2.6438 | 364.71 (0.00) |

| pb_r | 0.0004 | 0.0221 | −0.0028 | 0.1389 | −0.1236 | 5.8982 | 228.62 (0.00) | |

| zinc | zn_cw | 0.1845 | 0.1797 | 1.1336 | 0.7610 | 0.0019 | 3.1896 | 474.37 (0.00) |

| zn_r | 0.0003 | 0.0209 | −0.0039 | 0.1046 | −0.1083 | 4.9927 | 154.59 (0.00) | |

| tin | sn_cw | 0.1435 | 0.1283 | 1.3391 | 0.6780 | 0.0000 | 4.4941 | 702.47 (0.00) |

| sn_r | 0.0005 | 0.0182 | 0.0856 | 0.1663 | −0.1082 | 9.3753 | 443.00 (0.00) | |

| nickel | ni_cw | 0.1840 | 0.1504 | 0.5176 | 0.8586 | 0.0029 | 2.4871 | 197.66 (0.00) |

| ni_r | 0.0002 | 0.0237 | 0.1358 | 0.1423 | −0.1284 | 5.6834 | 221.95 (0.00) |

| Variables | ADF | PP | Order of Integration | |||

|---|---|---|---|---|---|---|

| Level | 1st Diff | Level | 1st Diff | |||

| copper | cu_cw | −2.560 | −3.155 ** | not determine | ||

| cu_r | −55.75 *** | −55.70 *** | I(0) | |||

| aluminum | al_cw | −0.993 | −39.74 *** | −0.675 | −39.91 *** | I(1) |

| al_r | −53.19 *** | −53.20 *** | I(0) | |||

| lead | pb_cw | −2.582 * | −2.729 ** | I(0) | ||

| pb_r | −49.23 *** | −49.22 *** | I(0) | |||

| zinc | zn_cw | −2.013 | −36.20 *** | −1.602 | −36.01 *** | I(1) |

| zn_r | −52.48 *** | −52.56 *** | I(0) | |||

| tin | sn_cw | −5.383 *** | −5.380 *** | I(0) | ||

| sn_r | −50.18 *** | −50.19 *** | I(0) | |||

| nickel | ni_cw | −3.158 ** | −3.271 ** | I(0) | ||

| ni_r | −51.66 *** | −51.75 *** | I(0) | |||

| Commodity | F-Statistics | MSE | |||

|---|---|---|---|---|---|

| Copper | 0.0001 | 0.0009 | 0.0001 | 0.21 | 0.0182 |

| (0.15) | (0.46) | ||||

| Aluminum | 0.0002 | 0.1212 | 0.0032 | 8.37 *** | 0.0147 |

| (0.91) | (2.89) *** | ||||

| Lead | 0.0004 | −0.0002 | 0.0001 | 0.01 | 0.0222 |

| (0.84) | (–0.11) | ||||

| Zinc | 0.0004 | 0.0829 | 0.0036 | 9.33 *** | 0.0211 |

| (–0.45) | (3.05) *** | ||||

| Tin | −0.0002 | 0.0052 | 0.0013 | 4.39 ** | 0.0182 |

| (–0.52) | (2.10) ** | ||||

| Nickel | −0.0007 | 0.0055 | 0.0012 | 3.97 ** | 0.0236 |

| (–1.22) | (2.01) ** |

© 2019 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Park, J. The Role of Canceled Warrants in the LME Market. Int. J. Financial Stud. 2019, 7, 10. https://doi.org/10.3390/ijfs7010010

Park J. The Role of Canceled Warrants in the LME Market. International Journal of Financial Studies. 2019; 7(1):10. https://doi.org/10.3390/ijfs7010010

Chicago/Turabian StylePark, Jaehwan. 2019. "The Role of Canceled Warrants in the LME Market" International Journal of Financial Studies 7, no. 1: 10. https://doi.org/10.3390/ijfs7010010

APA StylePark, J. (2019). The Role of Canceled Warrants in the LME Market. International Journal of Financial Studies, 7(1), 10. https://doi.org/10.3390/ijfs7010010