Towards Common Prosperity: Accelerated Depreciation Policy of Fixed Assets and Labor Income Share

Abstract

1. Introduction

2. Literature Review

2.1. The ADP: Economic Impact

2.1.1. Research on Labor Force Employment

2.1.2. Research on the Enterprise Human Capital Structure

2.1.3. Research on Enterprise Fixed Asset Investment

2.2. Influence Factors in the Labor Income Share

2.2.1. Measuring Labor Income Share

2.2.2. Substitution Effect Between Capital and Labor

2.2.3. Tax Policy

3. Background and Theoretical Hypotheses

3.1. Background

3.2. Theoretical Hypotheses

3.2.1. Relationship of the ADP to Enterprises’ Labor Income Share

3.2.2. Mechanisms of Human Capital Structure Adjustment

3.2.3. Mechanisms of Rent Sharing

4. Research Design

4.1. Data

4.2. Model

4.3. Description of Variables

- Definition of treatment group industries. In this paper, pilot industries were defined with reference to the notice. The remaining industries were considered to be non-pilot industries, among which industry classification standards referred to the Industry Classification Code of National Economy (GB/T4754−2011).

- Explained variables. In the new era, raising the labor income share has significance for narrowing the income gap. Therefore, we selected the enterprise labor income share as the explained variable. Following Bai et al. (2008), value added (of the factor cost method) was used for estimation. That is to say, the enterprise labor income share amounts to revenues allotted for staff/(business revenue − business cost + cash paid to and for staff + fixed asset depreciation).

- Explanatory variables. Treat × Post is the core explanatory variable that this research focuses on. This indicates that an enterprise enjoying the ADP has a value of 1 from the start date of the policy and thereafter, and 0 otherwise.

- Control variables. In this paper, control variables were mainly chosen as follows: Size, Age, Lev, Indept, Roa, Grow, PPE, Capital, Top1, GDP, and IndStr. Table 3 presents detailed definitions for the control variables.

4.4. Descriptive Statistics

5. Results and Discussion

5.1. Baseline Regression Results

5.2. Robustness Test

5.2.1. Dynamic Effect Analysis

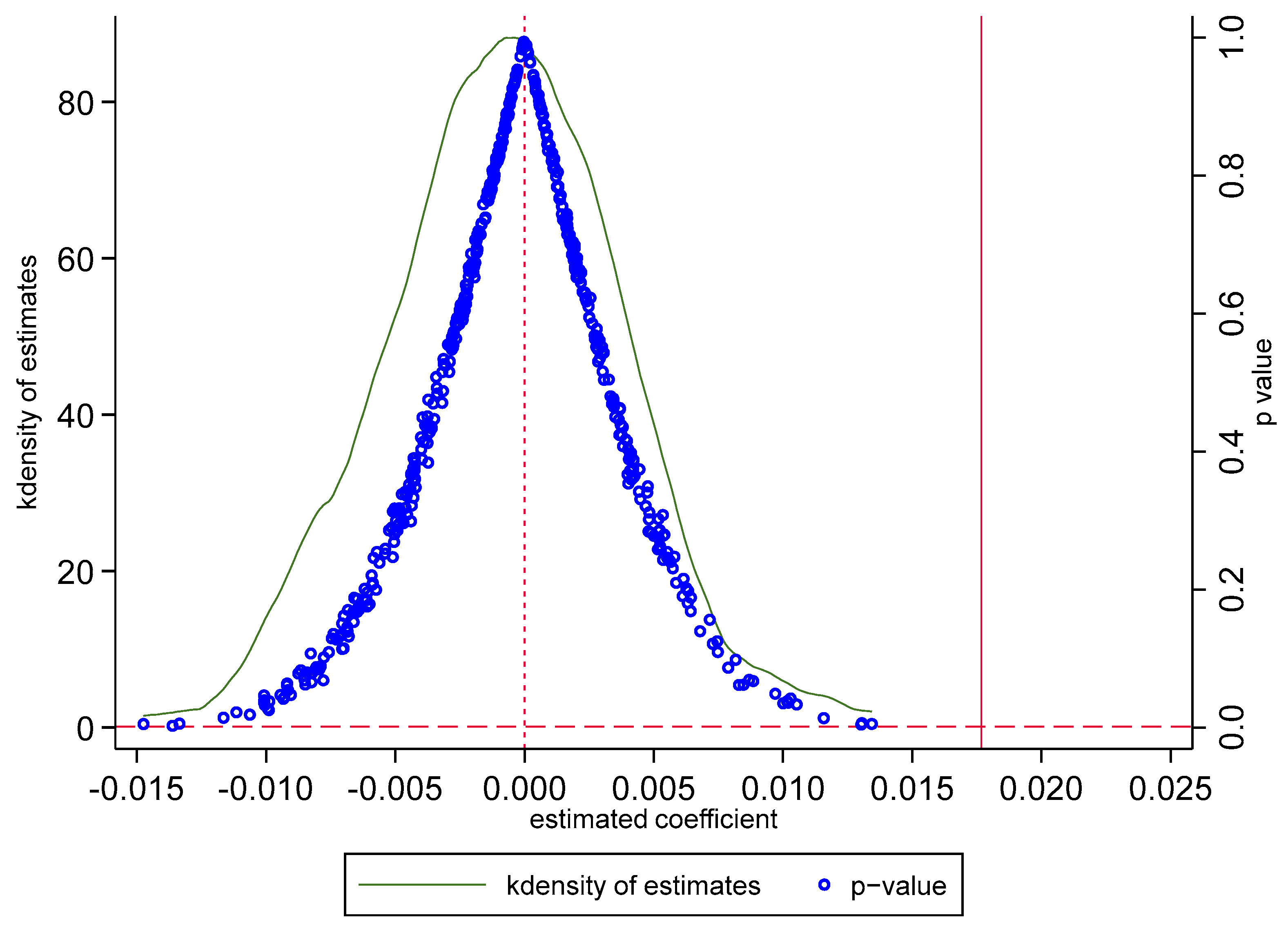

5.2.2. Placebo Test

5.2.3. Double Machine Learning Model

5.2.4. Alternative Metrics for the Labor Income Share

5.2.5. Expected Effect Test

5.2.6. Exclusion of Other Policy Implications for the Sample Period

5.3. Further Analysis

6. Mechanism Test and Heterogeneity Analysis

6.1. Mechanism

6.1.1. Impact on Human Capital Structure

6.1.2. Impact on Enterprise Rent

6.2. Heterogeneity Analysis

6.2.1. Ownership Differences

6.2.2. Scale Difference

6.2.3. Differences in Financing Constraints

6.2.4. Differences in Factor Intensity

6.2.5. Differences Between Manufacturing and Service Industries

6.2.6. Differences in Labor Skill Levels

7. Conclusions

Author Contributions

Funding

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Acemoglu, D. (2003). Labor-and capital-augmenting technical change. Journal of the European Economic Association, 1(1), 1–37. [Google Scholar] [CrossRef]

- Acemoglu, D., & Restrepo, P. (2018). Artificial intelligence, automation and work. In The economics of artificial intelligence: An agenda. IDEAS Working Paper Series from RePEc. University of Chicago Press. [Google Scholar]

- Acemoglu, D., & Restrepo, P. (2022). Demographics and automation. Review of Economic Study, 89(1), 1–44. [Google Scholar] [CrossRef]

- Alvarez-Cuadrado, F., Long, N. V., & Poschke, M. (2018). Capital-labor substitution, structural change and the labor income share. Journal of Economic Dynamics & Control, 87, 206–231. [Google Scholar]

- Angelopoulos, K., Asimakopoulos, S., & Malley, J. (2015). Tax smoothing in a business cycle model with capital skill complementarity. Journal of Economic Dynamics and Control, 51, 420–444. [Google Scholar] [CrossRef]

- Arulampalam, W., Devereux, M. P., & Maffini, G. (2012). The direct incidence of corporate income tax on wages. European Economic Review, 56(6), 1038–1054. [Google Scholar] [CrossRef]

- Auerbach, A. J. (2018). Measuring the effects of corporate tax cuts. Journal of Economic Perspectives, 32(4), 97–120. [Google Scholar] [CrossRef]

- Bai, C. E., & Qian, Z. J. (2009). Who has eroded residents’ income? An analysis of China’s national income distribution patterns. Social Sciences in China, 5, 99–115. [Google Scholar]

- Bai, C. E., Qian, Z. J., & Wu, K. P. (2008). Determinants of factor shares in China’s industrial sector. Economic Research Journal, 8, 16–28. [Google Scholar]

- Barkai, S. (2020). Declining labor and capital shares. The Journal of Finance, 75(5), 2421–2463. [Google Scholar] [CrossRef]

- Beck, T., Levine, R., & Levkov, A. (2010). Big bad banks? The winners and losers from bank deregulation in the United States. The Journal of Finance, 65(5), 1637–1667. [Google Scholar] [CrossRef]

- Bentolila, S., & Saint-Paul, G. (2003). Explaining movements in the labor share. Contributions to Macroeconomics, 3(1), 1–31. [Google Scholar] [CrossRef]

- Benzell, S. G., Kotlikoff, L. J., Lagarda, G., & Sachs, J. D. (2015). Robots are US: Some economics of human replacement. NBER Working Paper Series No. 20941. National Bureau of Economic Research. [Google Scholar]

- Button, P. (2019). Do tax incentives affect business location and economic development? Evidence from state film incentives. Regional Science and Urban Economics, 77, 315–359. [Google Scholar] [CrossRef] [PubMed]

- Chen, Y. J., Li, P., & Lu, Y. (2018). Career concerns and multitasking local bureaucrats: Evidence of a target-based performance evaluation system in China. Journal of Development Economics, 133, 84–101. [Google Scholar] [CrossRef]

- Dai, M., Xu, J. W., & Shi, B. Z. (2013). The shocks from the exchange rate of RMB, and the employment in manufacturing industry: The experience evidence from the data on firms. Management World, 11, 14–27. [Google Scholar]

- Deran, E. (1967). Changes in factor income shares under the social security tax. The Review of Economics and Statistics, 49(4), 627–630. [Google Scholar] [CrossRef]

- Duffy, J., Papageorgiou, C., & Perez-Sebastian, F. (2004). Capital-skill complementarity? Evidence from a panel of countries. The Review of Economics and Statistics, 86(1), 327–344. [Google Scholar] [CrossRef]

- Fan, Z., & Liu, Y. (2020). Tax compliance and investment incentives: Firm responses to accelerated depreciation in China. Journal of Economic Behavior & Organization, 176, 1–17. [Google Scholar]

- Garrett, D. G., Ohrn, E., & Su’arez Serrato, J. C. (2020). Tax policy and local labor market behavior. American Economic Review: Insights, 2(1), 83–100. [Google Scholar]

- Griliches, Z. (1969). Capital-skill complementarity. Review of Economics and Statistics, 51(4), 465–468. [Google Scholar] [CrossRef]

- Guo, K. M. (2019). Artificial intelligence, structural transformation and labor share. Management World, 35(7), 60–77. [Google Scholar]

- Hadlock, C. J., & Pierce, J. R. (2010). New evidence on measuring financial constraints: Moving beyond the KZ index. Review of Financial Studies, 23(5), 1909–1940. [Google Scholar] [CrossRef]

- Hall, R. E., & Jorgenson, D. W. (1967). Tax policy and investment behavior. The American Economic Review, 57(3), 391–414. [Google Scholar]

- Harrison, A. (2005). Has globalization eroded labor’s share? Some cross-country evidence. IDEAS Working Paper Series from PePEc. World Scientific Publishing. [Google Scholar]

- Hicks, J. R. (1932). Theory of wages. Macmilan. [Google Scholar]

- House, C., & Shapiro, M. D. (2008). Temporary investment tax incentives: Theory with evidence from bonus depreciation. American Economic Review, 98(3), 737–768. [Google Scholar] [CrossRef]

- Karabarbounis, L., & Neiman, B. (2014). The global decline of the labor share. Quarterly Journal of Economics, 129(1), 61–103. [Google Scholar] [CrossRef]

- Kline, P., Petkova, N., Williams, H., & Zidar, O. (2019). Who profits from patents? Rent-sharing at innovative firms. Quarterly Journal of Economics, 134(3), 1343–1404. [Google Scholar] [CrossRef]

- Koowattanatianchai, N., & Charles, M. B. (2015). A mixed methods approach to studying asset replacement decisions. International Journal of Business Innovation and Research, 9(5), 544–567. [Google Scholar] [CrossRef]

- Li, B., Liu, C., & Sun, S. T. (2021). Do corporate income tax cuts decrease labor share? Regression discontinuity evidence from China. Journal of Development Economics, 150, 102624. [Google Scholar] [CrossRef]

- Li, J. Q., & Zhao, X. Y. (2021). Accelerated depreciation policy of fixed assets and capital-labor ratio. Finance and Trade Economics, 42(04), 67–82. [Google Scholar]

- Liu, G. C., Ye, Y. W., Chen, X. X., & Zhang, J. (2023). Fixed assets depreciation, tax planning and abnormal investment. Economic Research Journal, 58(04), 23–40. [Google Scholar]

- Liu, Q. R., & Zhao, C. (2020). Tax incentives and upgrading firms’ human capital. Economic Research Journal, 55(4), 70–85. [Google Scholar]

- Liu, Y., & Mao, J. (2019). How do tax incentives affect investment and productivity? Firm-level evidence from China. American Economic Journal: Economics Policy, 11(3), 261–291. [Google Scholar] [CrossRef]

- Moon, S. T. (2022). Capital gains taxes and real corporate investment: Evidence from Korea. American Economic Review, 112(8), 2669–2700. [Google Scholar] [CrossRef]

- Ohrn, E. (2019). The effect of tax incentives on U.S. manufacturing: Evidence from state accelerated depreciation policies. Journal of Public Economics, 180, 104084. [Google Scholar] [CrossRef]

- Song, J., & Li, X. C. (2019). Industry investment, labour skill preference and industrial transformation and upgrading. The Journal of World Economy, 5, 145–167. [Google Scholar]

- Tirole, J. (2006). Theory of corporate finance. Princeton University Press. [Google Scholar]

- Tuzel, S., & Zhang, M. B. (2021). Economic stimulus at the expense of routine-task jobs. The Journal of Finance, 76(6), 3347–3399. [Google Scholar] [CrossRef]

- Uzawa, H. (1962). Production functions with constant elasticities of substitution. Review of Economic Studies, 29(4), 291–299. [Google Scholar] [CrossRef]

- Wang, X. Y., & Huang, Y. J. (2017). Foreign direct investment and labor share in the listed companies: Looting a burning house or icing on the cake. China Industrial Economics, 4, 135–154. [Google Scholar]

- Wei, X. H., Dong, Z. Q., & Lan, J. J. (2017). Does regional gender imbalance affect labor share of income? Theoretical analysis and evidence from China. The Journal of World Economy, 4, 129–146. [Google Scholar]

- Xiao, S. T., Sun, R., Yuan, C., & Sun, J. (2022). Enterprise digital transformation, human capital structure adjustment, and labor income share. Management World, 38(12), 220–237. [Google Scholar]

- Xu, D. D., Zhao, T. H., & Xu, J. X. (2021). Tax incentives, fixed asset investment and labor income share: Evidence from the fixed assets accelerated depreciation reform in 2014. Management Review, 33(3), 244–254. [Google Scholar]

- Yagan, D. (2015). Capital tax reform and real economy: The effects of the 2003 dividend tax cut. American Economic Review, 105(12), 3531–3563. [Google Scholar] [CrossRef]

- Yang, Y., & Zhang, H. (2021). The value-added tax reform and labor market outcomes: Firm-level evidence from China. China Economic Review, 69, 101678. [Google Scholar] [CrossRef]

- Young, A. T. (2010). One of the things we know that ain’t so: Is US labor’s share relatively stable. Journal of Macroeconomics, 32(1), 90–102. [Google Scholar] [CrossRef]

- Zhang, K. Z., He, F., Huang, Y. Y., & Cui, X. Y. (2021). Tax incentives, rent sharing and within-firm wage inequality. Economic Research Journal, 56(06), 110–126. [Google Scholar]

- Zhang, T., & Li, J. C. (2023). Network infrastructure, inclusive green growth, and regional inequality: From causal inference based on double machine learning. The Journal of Quantitative & Technical Economics, 40, 113–135. [Google Scholar]

- Zwick, E., & Mahon, J. (2017). Tax policy and heterogeneous investment behavior. American Economic Review, 107(1), 217–248. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

| Research Area | Policy Impact | Reference | Research Findings |

|---|---|---|---|

| Labor force employment | Investment growth | House and Shapiro (2008) | The policy resulted in 100,000 to 200,000 new job positions. |

| Ohrn (2019) | The policy absorbed employment and slightly improved wage levels. | ||

| Garrett et al. (2020) | The policy absorbed employment and slightly improved wage levels. | ||

| No significant impact | Yagan (2015); Button (2019) | The policy did not play a significant role in absorbing employment. | |

| Enterprise human capital structure | Skill upgrading | Liu and Mao (2019) | The policy prompted equipment updates, replacing low-skilled workers with high-skilled ones. |

| Workforce restructuring | Liu and Mao (2019) | The affected enterprises increased skilled workers and decreased routine workers. | |

| Labor ratio improvement | Liu and Zhao (2020) | The policy encouraged fixed asset additions and improved the ratio of skilled to unskilled labor. | |

| Enterprise fixed asset investment | Investment growth | Hall and Jorgenson (1967) | The ADP improved investment behavior through a reduction in capital user cost. |

| Zwick and Mahon (2017) | The policy stimulated significant growth in enterprise investment. | ||

| Ohrn (2019) | Short-term tax incentives from ADP lowered investment costs, particularly for financially constrained firms. | ||

| Fan and Liu (2020) | The policy enhanced investment efficiency based on data from Chinese listed firms. |

| Research Area | Influence on LS | Reference | Research Findings |

|---|---|---|---|

| Capital–labor substitution | Decrease | Karabarbounis and Neiman (2014); Bentolila and Saint-Paul (2003) | Capital deepening affects the labor income share due to falling capital goods prices. |

| Benzell et al. (2015) | AI squeezes out the labor income share by increasing the ratio of intangible assets. | ||

| Alvarez-Cuadrado et al. (2018) | Capital bias stimulates capital input, weakening the labor income share. | ||

| Barkai (2020) | Higher returns on non-labor factors lead to a drop in the labor income share. | ||

| Acemoglu and Restrepo (2022) | Technological progress favors capital, reducing the labor income share. | ||

| Tax policy | Increase | Deran (1967) | Social security tax reduces the capital share, increasing the labor income share. |

| Decrease | Yang and Zhang (2021) | Investment incentive effect of the reform declines the labor income share. | |

| Li et al. (2021) | Lowering income tax rates reduces the labor income share. |

| Variable Name | Variable Symbol | Definition |

|---|---|---|

| Enterprise size | Size | The natural logarithm of total corporate assets |

| Enterprise age | Age | The natural logarithm of the establishment years of the enterprise |

| Asset–liability ratio | Lev | Total liabilities/Total assets |

| Ratio of independent directors | Indept | Independent directors/Total directors |

| Profitability | Roa | Net profit/Total assets |

| Enterprise growth | Grow | Market value of corporate equity + Book value of liabilities/Total assets |

| Capital–output ratio | PPE | Net fixed assets/Total operating income |

| Capital intensity | Capital | Total assets/Total revenue |

| Large shareholder ownership ratio | Top1 | Number of shares held by the largest shareholder /Total shares outstanding |

| Regional economic development level | GDP | The natural logarithm of GDP in the city where the enterprise is registered |

| Industrial structure | IndStr | The proportion of the secondary industry in GDP of the province where the company is registered |

| N | Mean | Std | Min | Median | Max | |

|---|---|---|---|---|---|---|

| LS | 14,213 | 0.2923 | 0.1201 | 0.0569 | 0.2805 | 0.7176 |

| Size | 14,213 | 22.4592 | 1.3489 | 19.4769 | 22.2799 | 26.3760 |

| Age | 14,213 | 2.8255 | 0.3820 | 2.0794 | 2.8332 | 3.4012 |

| Lev | 14,213 | 0.4391 | 0.1997 | 0.0511 | 0.4352 | 0.9519 |

| Indept | 14,213 | 0.3746 | 0.0538 | 0.3333 | 0.3333 | 0.5714 |

| Roa | 14,213 | 0.0407 | 0.0606 | −0.2390 | 0.0378 | 0.2264 |

| Grow | 14,213 | 2.0314 | 1.3124 | 0.8343 | 1.6031 | 8.4958 |

| PPE | 14,213 | 0.4246 | 0.3750 | 0.0370 | 0.3099 | 2.0339 |

| Capital | 14,213 | 2.3411 | 1.8400 | 0.4600 | 1.8216 | 12.2596 |

| Top1 | 14,213 | 0.3408 | 0.1487 | 0.0838 | 0.3185 | 0.7457 |

| GDP | 14,213 | 8.9924 | 1.1024 | 6.2238 | 9.1170 | 10.6739 |

| IndStr | 14,213 | 0.4025 | 0.1176 | 0.1580 | 0.4160 | 0.6390 |

| (1) | (2) | |

|---|---|---|

| LS | LS | |

| Treat × Post | 0.0180 *** (0.0044) | 0.0177 *** (0.0035) |

| Controls | No | Yes |

| Year FE | Yes | Yes |

| Enterprise FE | Yes | Yes |

| N | 14,213 | 14,213 |

| R2 | 0.7341 | 0.8266 |

| (1) | (2) | |

|---|---|---|

| LS | LS | |

| Treat × Post | 0.0589 *** | 0.0594 *** |

| (0.0035) | (0.0035) | |

| Linear term | Yes | Yes |

| Quadratic term | No | Yes |

| Year FE | Yes | Yes |

| Enterprise FE | Yes | Yes |

| N | 14,213 | 14,213 |

| (1) | (2) | (3) | (4) | |

|---|---|---|---|---|

| Alternative Metrics for Labor Income Share | Rejection Sample | |||

| LS_1 | LS_2 | LS | LS | |

| Treat × Post | 0.0604 *** | 0.0205 *** | 0.0221 *** | 0.0178 *** |

| (0.0166) | (0.0055) | (0.0039) | (0.0036) | |

| Controls | Yes | Yes | Yes | Yes |

| Year FE | Yes | Yes | Yes | Yes |

| Enterprise FE | Yes | Yes | Yes | Yes |

| N | 14,213 | 14,213 | 12,935 | 13,551 |

| R2 | 0.7477 | 0.6153 | 0.8279 | 0.8272 |

| (1) | (2) | |

|---|---|---|

| lnemp | lnkl | |

| Treat × Post | 0.0788 *** | 0.0730 ** |

| (0.0238) | (0.0233) | |

| Controls | Yes | Yes |

| Year FE | Yes | Yes |

| Enterprise FE | Yes | Yes |

| N | 14137 | 13625 |

| R2 | 0.9464 | 0.8870 |

| (1) | (2) | (3) | (4) | (5) | (6) | |

|---|---|---|---|---|---|---|

| Skill | Unskill | Skill_Rate | LS | lnrent | LS | |

| Treat × Post | 0.0525 *** | −0.0233 | 0.0486 *** | 0.0611 *** | 0.2040 *** | 0.0159 *** |

| (0.0148) | (0.0397) | (0.0147) | (0.0156) | (0.0294) | (0.0039) | |

| skill_rate | 0.1072 *** | |||||

| (0.0319) | ||||||

| lnrent | 0.0575 *** | |||||

| (0.0034) | ||||||

| Controls | Yes | Yes | Yes | Yes | Yes | Yes |

| Year FE | Yes | Yes | Yes | Yes | Yes | Yes |

| Enterprise FE | Yes | Yes | Yes | Yes | Yes | Yes |

| N | 6711 | 7527 | 7107 | 7107 | 13,410 | 13,410 |

| R2 | 0.9355 | 0.9503 | 0.9157 | 0.8080 | 0.8146 | 0.7794 |

| (1) | (2) | (3) | (4) | (5) | (6) | |

|---|---|---|---|---|---|---|

| Ownership | Scale | Financing Constraints | ||||

| State-Owned | Private | Large | Middle and Small | High | Low | |

| Treat × Post | 0.0078 | 0.0207 *** | 0.0030 | 0.0175 *** | 0.0139 *** | 0.0082 |

| (0.0059) | (0.0043) | (0.0046) | (0.0048) | (0.0040) | (0.0055) | |

| Controls | Yes | Yes | Yes | Yes | Yes | Yes |

| Year FE | Yes | Yes | Yes | Yes | Yes | Yes |

| Enterprise FE | Yes | Yes | Yes | Yes | Yes | Yes |

| N | 5826 | 8387 | 8480 | 5733 | 7066 | 7147 |

| R2 | 0.8373 | 0.8329 | 0.8638 | 0.8379 | 0.8654 | 0.8634 |

| (1) | (2) | (3) | (4) | (5) | (6) | |

|---|---|---|---|---|---|---|

| Factor Intensity | Industry | Labor Skill Level | ||||

| Capital Intensive | Labor Intensive | Manufacturing | Services | High | Low | |

| Treat × Post | 0.0297 *** | 0.0062 | 0.0193 *** | 0.0101 | 0.0155 *** | 0.0505 |

| (0.0075) | (0.0054) | (0.0047) | (0.0096) | (0.0037) | (0.0277) | |

| Controls | Yes | Yes | Yes | Yes | Yes | Yes |

| Year FE | Yes | Yes | Yes | Yes | Yes | Yes |

| Enterprise FE | Yes | Yes | Yes | Yes | Yes | Yes |

| N | 7770 | 6443 | 7720 | 3825 | 7066 | 7147 |

| R2 | 0.8094 | 0.8500 | 0.8181 | 0.8284 | 0.8455 | 0.8902 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2025 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Yang, Y.; Zeng, B. Towards Common Prosperity: Accelerated Depreciation Policy of Fixed Assets and Labor Income Share. Int. J. Financial Stud. 2025, 13, 46. https://doi.org/10.3390/ijfs13010046

Yang Y, Zeng B. Towards Common Prosperity: Accelerated Depreciation Policy of Fixed Assets and Labor Income Share. International Journal of Financial Studies. 2025; 13(1):46. https://doi.org/10.3390/ijfs13010046

Chicago/Turabian StyleYang, Ying, and Bing Zeng. 2025. "Towards Common Prosperity: Accelerated Depreciation Policy of Fixed Assets and Labor Income Share" International Journal of Financial Studies 13, no. 1: 46. https://doi.org/10.3390/ijfs13010046

APA StyleYang, Y., & Zeng, B. (2025). Towards Common Prosperity: Accelerated Depreciation Policy of Fixed Assets and Labor Income Share. International Journal of Financial Studies, 13(1), 46. https://doi.org/10.3390/ijfs13010046