4.1. A Descriptive Analysis of the Studies

The data described in this section comprise information gathered on AI in auditing between 2017 and 7 June 2024. By number of articles sorted geographically, by number of articles and number of citations from 2017 to 2024, by journals that contributed most to the publications and number of citations, and by the ten most cited papers, one may find the most productive research for the timeframe (

Merigo & Yang, 2017).

Figure 1,

Figure 2,

Figure 3 and

Figure 4 taken together offer a complex picture of the field, highlighting academic, geographical, and chronological aspects that frame AI’s involvement in auditing procedures all around. These domains were selected since they fit the goal of the study—that of evaluating the advancement, influence, and main players in the field of artificial intelligence in auditing. Previous studies underlined the need of knowing temporal patterns in technology adoption (

Merigo & Yang, 2017) and the part that regional research clusters play in inspiring creativity (

Van Eck & Waltman, 2017). Moreover, in bibliometric analyses to track significant contributions and developing trends in a given subject, determining leading journals and authors has been a standard strategy (

Bartolacci et al., 2020;

D. Zhang et al., 2019). This thorough investigation guarantees the study catches important insights on the transforming power of artificial intelligence in auditing and conforms with past research approaches.

Figure 1 below shows the number of publications and citations of papers relating to AI in auditing between 2017 and 2024. As far as publications are concerned, from the data points, it is evident that more citations and publications have occurred in recent years, which indicates that the field is expanding. The data indicate the following number of publications per year: one in 2017, three in 2018, eight in 2019, fifteen in 2020, twenty-two in 2021, thirty-two in 2022, twenty-nine in 2023, and thirteen in 2024. There were intensive references to the cited material from the period before 2021, and the peak in 2023 demonstrates that the research from prior years had a significant impact on the field’s progression.

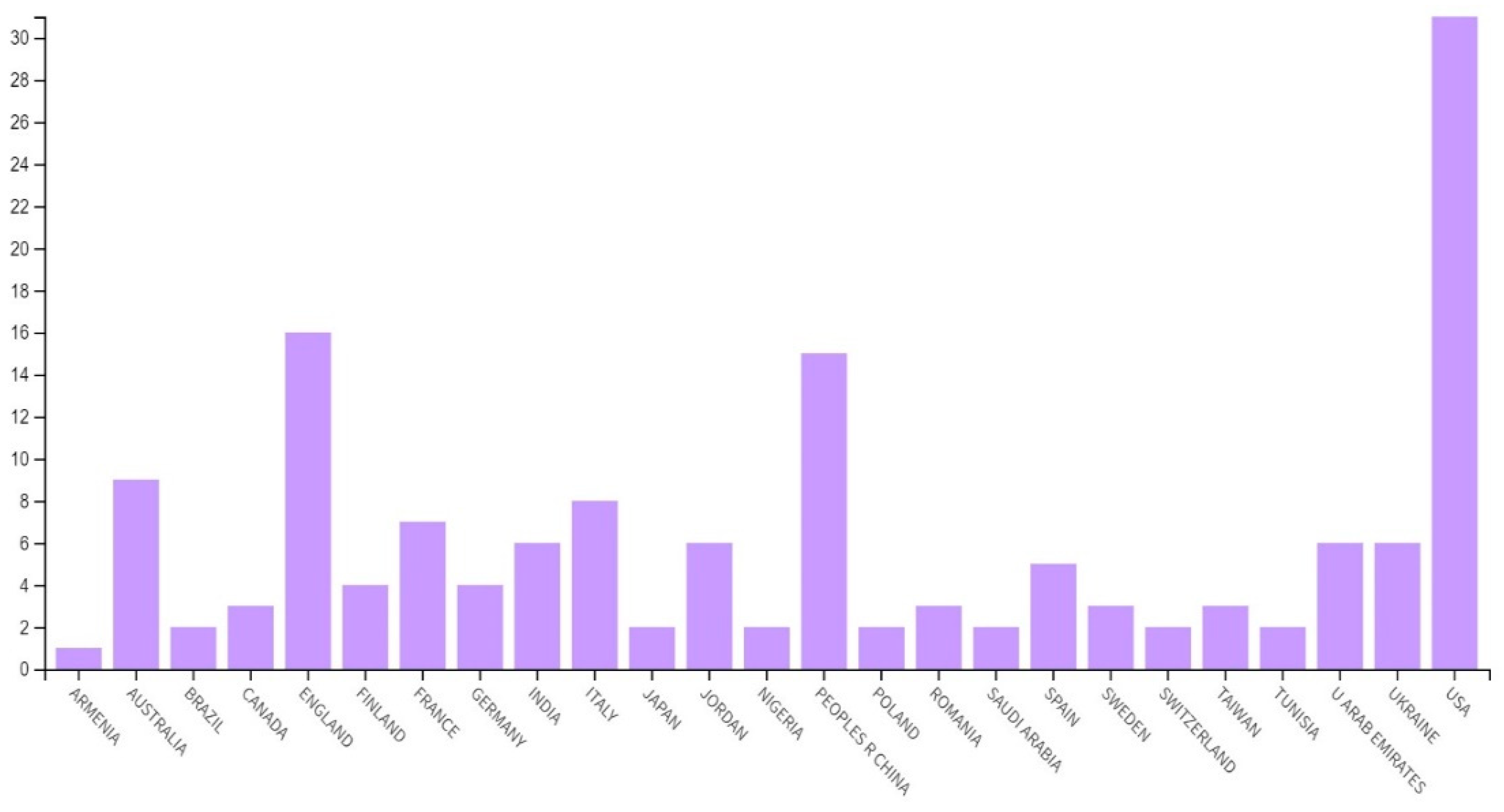

As illustrated in

Figure 2, the articles were classified into three categories. Furthermore, the distribution of articles related to AI in auditing is shown by countries and regions. Out of all of the countries, the US published 31 publications, England published 16, and China published 15, which confirms that AI research activity is high in these countries. Furthermore, additional items of exceptional worth come from Australia (nine), Italy (eight), France (seven), Jordan, Ukraine, the UAE (six), and Spain (five).

Figure 3 shows the international contributions to AI studies, and the figures contributing to the studies hail from various countries, which implies that there is interest in the development of AI in auditing across the world.

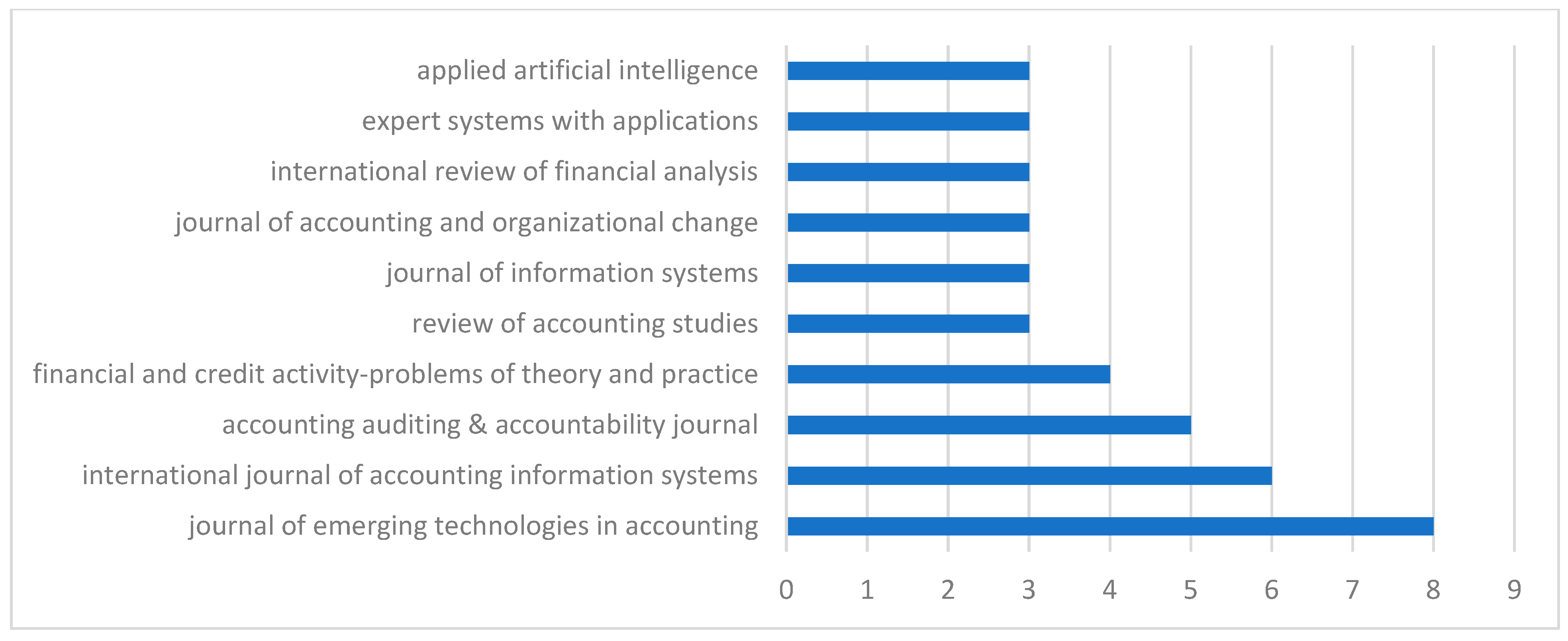

In

Figure 3 below, the journals with the highest impact have greatly contributed to the improvement of knowledge in the field of AI in auditing. Some of the top journals that publish research articles related to the field are the Journal of Emerging Technologies in Accounting, with nine publications, and the International Journal of Accounting Information Systems, with seven publications. Although there are only a few core journals in this field, they remain the most influential and significant in the established research.

Table 3 lists the top ten papers contributing to the field of AI in auditing, providing details such as the journal name, the paper’s author(s), year of publication, and the total number of citations. The most referenced paper was, “The Emergence of Artificial Intelligence: how automation is changing auditing.”. The paper titled “Shift to Automation in Auditing: Its Impact and Implications”, composed by Kokina and Davenport, has been cited 153 times.

Kokina and Davenport (

2017) addressed the topic of how artificial intelligence is affecting the auditing profession, particularly concerning how automation is changing some of the essential processes in auditing by improving the speed and precision of the work being carried out. Their research also explored the skepticism linked to AI and stressed the significance of subsequent analysis in seeking to eliminate such prejudices and, therefore, increase the openness to AI-based auditing systems.

Several papers have analyzed how AI and automation are changing the auditing profession, particularly robotic process animation (RPA) and the preservation of audit quality disrupted by COVID-19. After the first study, “Applying Robotic Process Automation (RPA) in Auditing”,

Huang and Vasarhelyi’s (

2019) study in the paper titled “A Framework” indicates that RPA decreases the audit’s volume of manual tasks and enhances efficiency so that auditors can concentrate on evaluation. In their study, “The Impact of COVID-19 on Auditing Quality”,

Albitar et al. (

2020) emphasized the urgent need for remote audit tools. However, they also highlighted concerns regarding audit quality and information validation.

Tiberius and Hirth (

2019), in “Impacts of Digitization on Auditing”, predicted that digitization would transform audits into fully digital processes and require auditors to develop digital competencies. Their predictions were based on findings from the “Delphi Study for Germany”. In addition,

Qasim and Kharbat (

2020), in their paper “Blockchain Technology, Business Data Analytics, and Artificial Intelligence: Use in the Accounting Profession and Ideas for Inclusion into the Accounting Curriculum”, emphasized that integrating blockchain and AI into accounting curricula is essential for preparing future accountants for technological advancements. In the paper titled “Digital Systems and New Challenges of Financial Management—FinTech, XBRL, Blockchain and Cryptocurrencies”,

Mosteanu and Faccia (

2020) stated that the implementation of digital systems is accompanied by new regulation risks. Therefore, governance frameworks must be updated. In the study titled “Mediating Effect of Use Perceptions on Technology Readiness and Adoption of Artificial Intelligence in Accounting”, conducted by

Damerji and Salimi (

2021), the authors proved that positive perceptions have a direct impact on AI adoption and reiterated the call for education and training to enhance technology readiness among employees. Finally, in the article “Intelligent Process Automation in Audit”,

C. Zhang (

2019) found that the automation of any audit reduces time consumption and results in a boost in audit accuracy.

In their research work “The Digital Transformation of External Audit and Its Impact on Corporate Governance”,

Manita et al. (

2020) identified the reality that digitalization augments audit firms’ governmental functions by providing a pertinent audit service, broadening service provision, and improving audit quality by following advanced data analysis, creating new audit profiles, and encouraging innovativeness, a development that highlights the need for proper governance and ethics owing to the emergence of complexities. It transforms the corporate environment by eradicating managerial discretion, thus enhancing firm governance. This means that improved audit standards are called for, as well as corresponding changes in the curricula offered in educational institutions. The research work of

Munoko et al. (

2020) titled “The Ethical Implications of Using Artificial Intelligence in Auditing” examined the gains and dilemmas arising from the use of AI in auditing. On the one hand, it focused on unveiling the strengths that AI can bring into the auditing field, including accuracy and efficiency; on the other hand, it outlined possible ethical problems with the rise of AI. Therefore, governance needs to face these changes in auditing.

Table 4 shows the authors who are most productive and have published many papers in the field of AI in auditing in the WoS database between 2017 and 2024. There were four publications written by Miklos A. Vasarhelyi, who has contributed significantly. Each of the following authors has published two papers: Khaled Hussainey, Maria Axente, Ting Sun, Aaron Saiewitz, Jakob Mokander, Robyn L. Raschke, Awni Rewashed, Prashant Singh Rana, and Delia Deliu. As is pointed out in

Figure 4, Vasarhelyi has the highest author productivity in the field, and his works aim to unlock the possibilities offered by AI in auditing. For example, Vasarhelyi intervened on how best to sell auditing with RPA and the ethical dilemmas associated with deploying AI in audits. In addition, in

Figure 4, there is a group of authors who have been contributing continuously to the development of AI in auditing practices and technologies; thanks to authors such as Hussainey, Axente, Sun, Saiewitz, Mokander, Raschke, Rawashdeh, Rana, and Deliu, AI is becoming diverse and has a wide range of research in this field.

4.2. Co-Word Analysis

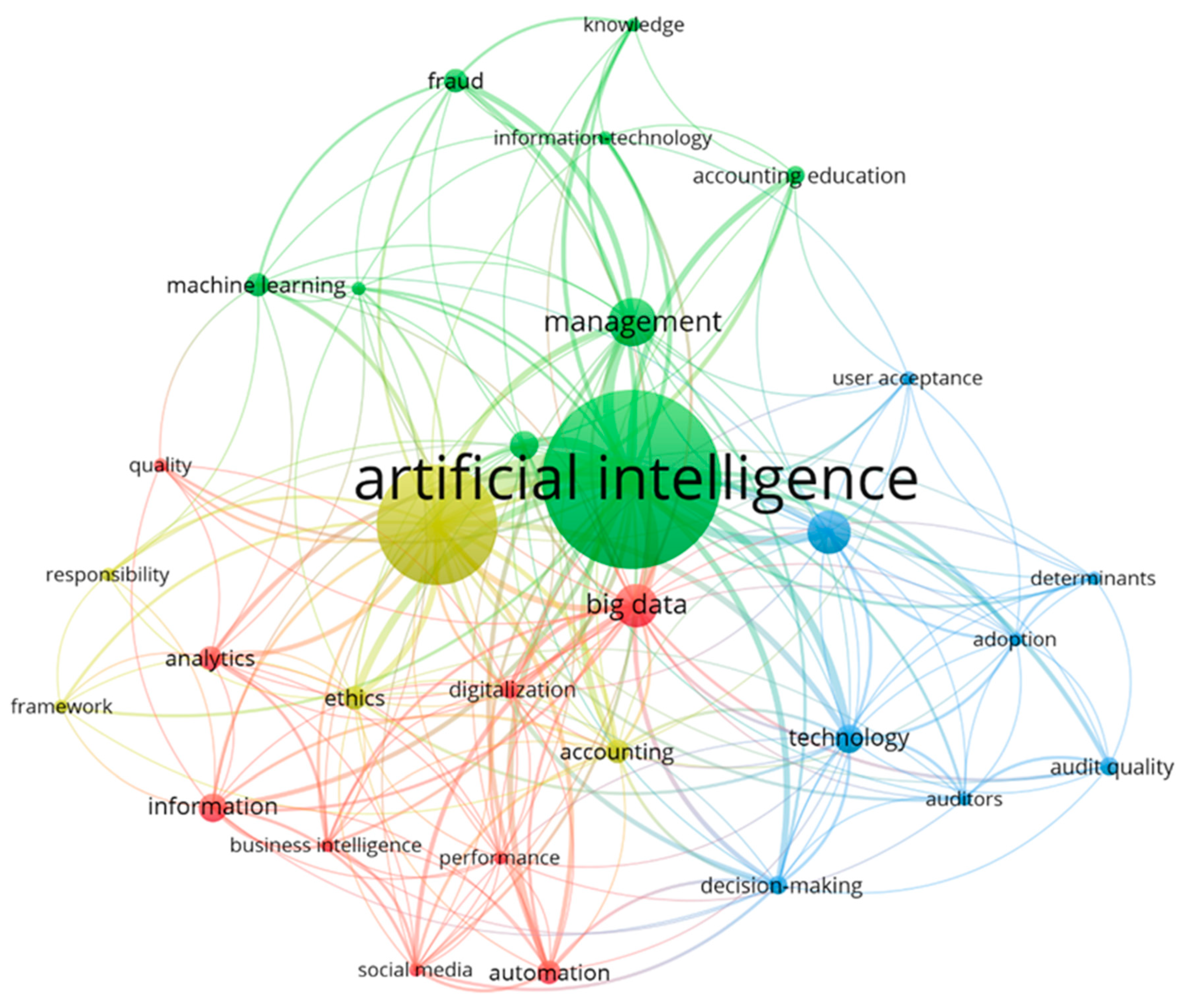

Using clustering, the VOSviewer program examines keyword co-occurrence to provide insightful analysis of the links and trends within certain study fields. The relevant software in VOSviewer contains a function called clustering, which sorts keywords according to their frequency, as described in

Van Eck and Waltman’s (

2017) work. The co-occurrence of keywords was identified from the titles, abstracts, and citation contexts using the text-mining feature of VOSviewer (

Van Eck & Waltman, 2011). For

Figure 5, the VOSviewer tool was employed in the co-occurrence analysis of the keywords to establish a network of keywords or clusters based on total links and the strength of the links connecting them. The structure of the network is such that the layers formed by the different clusters were assigned different colorations. These are collections of key terms that are associated with a particular domain. Management and fraud sit under the umbrella of the Green Cluster and include keywords such as artificial intelligence, information technology, knowledge, and accounting education. Big data, digitization, information, analytics, automation, social media ethics, and performance form the red cluster keywords. Keywords belonging to the blue cluster are technology, decision making, adoption, auditors, user acceptance, determinants, and audit quality. Keywords shown in the yellow cluster include audit quality, responsibility, and framework.

In this analysis, a screening of words was conducted. For example, impact, future, opportunities, etc., were eliminated due to their lesser importance and the infrequency of their application. The minimum keyword count was set to three, meaning that only keywords that appeared at least three times in the database were selected. This choice was made to capture the main keywords while excluding those that occur very rarely in a text. Though their occurrence is important, it was considered that they would not make a meaningful contribution to the analysis. To enhance the next level of analysis, the process of replacement was used in which words close in meaning were replaced with the most precise words. For instance, turning “AI” into “artificial intelligence” and the same for “artificial intelligence (AI)” and “artificial intelligence” while changing “audit” to “auditing” ensured that the clustering occurred within the correct context. Undertaking this approach assisted in the extraction of significant information and recognizing the links between the keywords, various relationships and connections, and hidden patterns in the research domain (

Guleria & Kaur, 2021).

Table 4 highlights nine keywords along with their frequency and total link strength, showing how interconnected these concepts are in the research field. The terms include big data (nine mentions, link strength 51), digitalization (four mentions, link strength 21), information (six mentions, link strength 22), business intelligence (three mentions, link strength 21), social media (three mentions, link strength 23), analytics (five mentions, link strength 19), automation (five mentions, link strength 24), performance (three mentions, link strength 15), and quality (three mentions, link strength 9). These findings support previous research that underscores the transformative role of digital technologies in auditing. For instance, combining big data and business intelligence helps auditors process big datasets, hence making audit information more relevant and of better quality (

Huang & Vasarhelyi, 2019;

Tiberius & Hirth, 2019). The high degree of connection between digitalization and automation points to the significance of both concepts for improving efficiency and accuracy in audit works (

Albitar et al., 2020;

Manita et al., 2020). Furthermore, the existence of social media and analytics symbolizes the necessity for auditors to adopt a more diverse and data-driven approach to maintain audit quality in an ever-evolving digital landscape (

Qasim & Kharbat, 2020;

Damerji & Salimi, 2021). Thus, the categorization of performance and quality suggests that constant endeavors are being made to increase the efficiency and accuracy of auditing processes due to the employment of technology and the updating of methodologies by scholars (e.g.,

C. Zhang, 2019;

Mosteanu & Faccia, 2020).

Table 5 lists nine keywords and illustrates their relevance to the research field of AI in auditing. The keywords include artificial intelligence (thirty-seven occurrences, link strength 117), management (ten occurrences, link strength 35), data analytics (six occurrences, link strength 25), machine learning (five occurrences, link strength 16), systems (three occurrences, link strength 12), information technology (three occurrences, link strength 13), fraud (five occurrences, link strength 17), accounting education (four occurrences, link strength 13), and knowledge (three occurrences, link strength 11). The nine keywords represent the growing significance of digital technologies in auditing and accounting. The importance of AI is demonstrated by its key role in improving decision making and operational efficiency in auditing (

Huang & Vasarhelyi, 2019;

Tiberius & Hirth, 2019). The importance of data analytics and machine learning demonstrates the need for auditors to adopt new analytical techniques to enhance audit quality and relevance (

Albitar et al., 2020;

Qasim & Kharbat, 2020). In contrast, words like management and systems reveal the structural transformation required for the adoption of these technologies to occur (

Manita et al., 2020;

Vitali & Giuliani, 2024). The other keywords recognized are information technology and accounting education and are associated with the need to revamp educational curricula in order to develop necessary skills for future accountants (

Damerji & Salimi, 2021;

Thottoli, 2024). The other two keywords were fraud and knowledge, indicating that despite any shortcomings noted in this paper, people continue to work on ways to enhance audit efficiency and credibility by applying technology and enhanced methodologies (

C. Zhang, 2019;

Mosteanu & Faccia, 2020).

From the analysis of the journal articles, eight important keywords and their frequencies, along with the total link strength, are shown in

Table 6. This identifies the importance attached to each concept and their relationships within the research area. These terms are technology (six occurrences, link strength 32), blockchain (nine occurrences, link strength 26), decision making (four occurrences, link strength 29), adoption (three occurrences, link strength 17), auditors (four occurrences, link strength 16), determinants (three occurrences, link strength 13), user acceptance (three occurrences, link strength 12), and audit quality (four occurrences, link strength 13). Likewise,

Table 7 lists five items capturing the words identified to have high relevance, as follows: auditing, with twenty-five mentions and a link strength of 85; accounting, with five mentions and a link strength of 28; ethics, with five mentions and a link strength of 25; framework, with three mentions and a link strength of 9; responsibility, with three mentions and a link strength of 8. These keyword occurrences are in line with other studies that have drawn attention to the uses of digital technologies and frameworks for change in auditing and accounting processes. The emphasis on blockchain and technology attests to the constant advancement of these fields and their significance in making auditors’ work more secure and efficient, as numerous investigations into blockchains in auditing have demonstrated (

Rawashdeh, 2024b;

Sheikha et al., 2021). Decision making and adoption relate to changes in the practice of auditors, who use emerging technologies as tools to transform decision making and audit results and quality (

Sachan & Liu, 2024;

Manita et al., 2020). Auditing, accounting, and ethics remain the focus of further yearly attempts to uphold the profession’s ethical standards, especially when new technologies are being embraced (

Albitar et al., 2020;

Thottoli, 2024;

Wang et al., 2024;

Samiolo et al., 2024). Furthermore, the terms framework and responsibility imply that more profound and adequate regulation and governance must be established to ensure the appropriate application of these technologies (

Munoko et al., 2020;

Jackson & Allen, 2024;

Kunz & Wirtz, 2024). Due to their relationship, these keywords show how technological development and the consideration of ethics impact the modern auditing profession.

4.3. Bibliographic Coupling

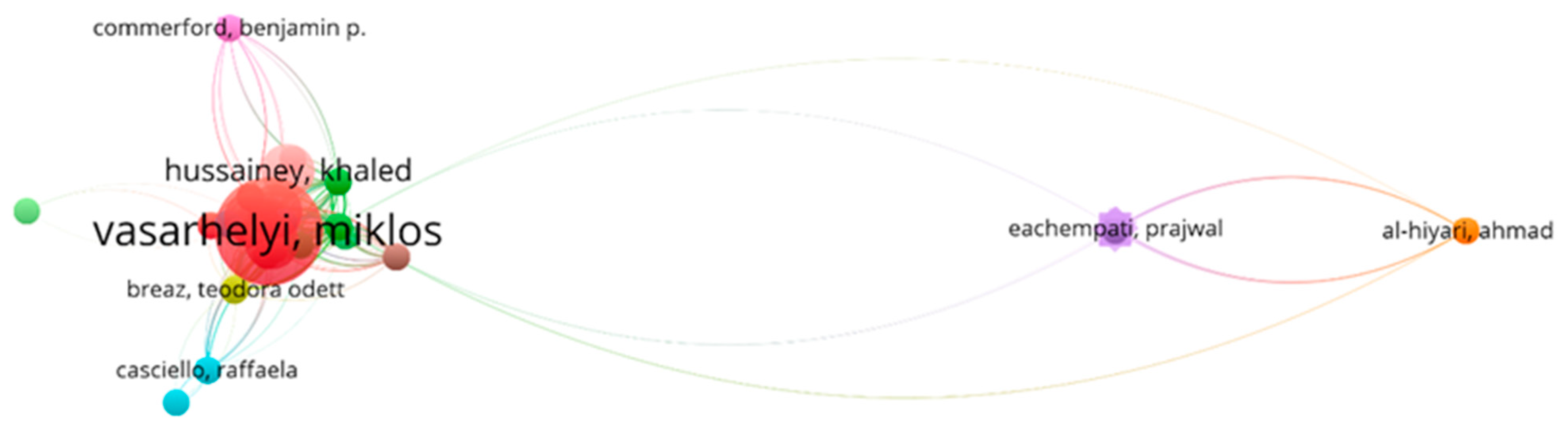

To define the minimum threshold for author citations, a value of 17 was used in

Figure 6, yielding 73 authors for this criterion. As stated, the bibliographic coupling network represents the relationship between these authors through the cultivation of co-citations. The person of most importance in this network is Miklos Vasarhelyi, which is evident from the node assigned to him, which represents the largest data value and expresses the overall productivity and contribution of this researcher in the given field. Other important authors are Khaled Hussainey, Pushkin Kachroo, and Benjamin P. Comerford, among others. They all have a clear connection and can represent co-authorships or co-citations with Vasarhelyi. The positions that form the network consist of clusters: the red area depicts Vasarhelyi’s cluster as it is densely connected. This defines a vast area of research composed of accounting, auditing, and financial reporting, which has a highly convoluted web. Although authors like Ahmad Al-Hiyari, Rajwal Eachempati, and Seema Bawa are not very central, they also have good connections within the network, implying that such authors may be active in areas that are still developing or specialized. In general, this network concentrates on the main authors, especially Vasarhelyi, and reveals a connection of research in the given field within both the experienced scholars and scopes for future research.

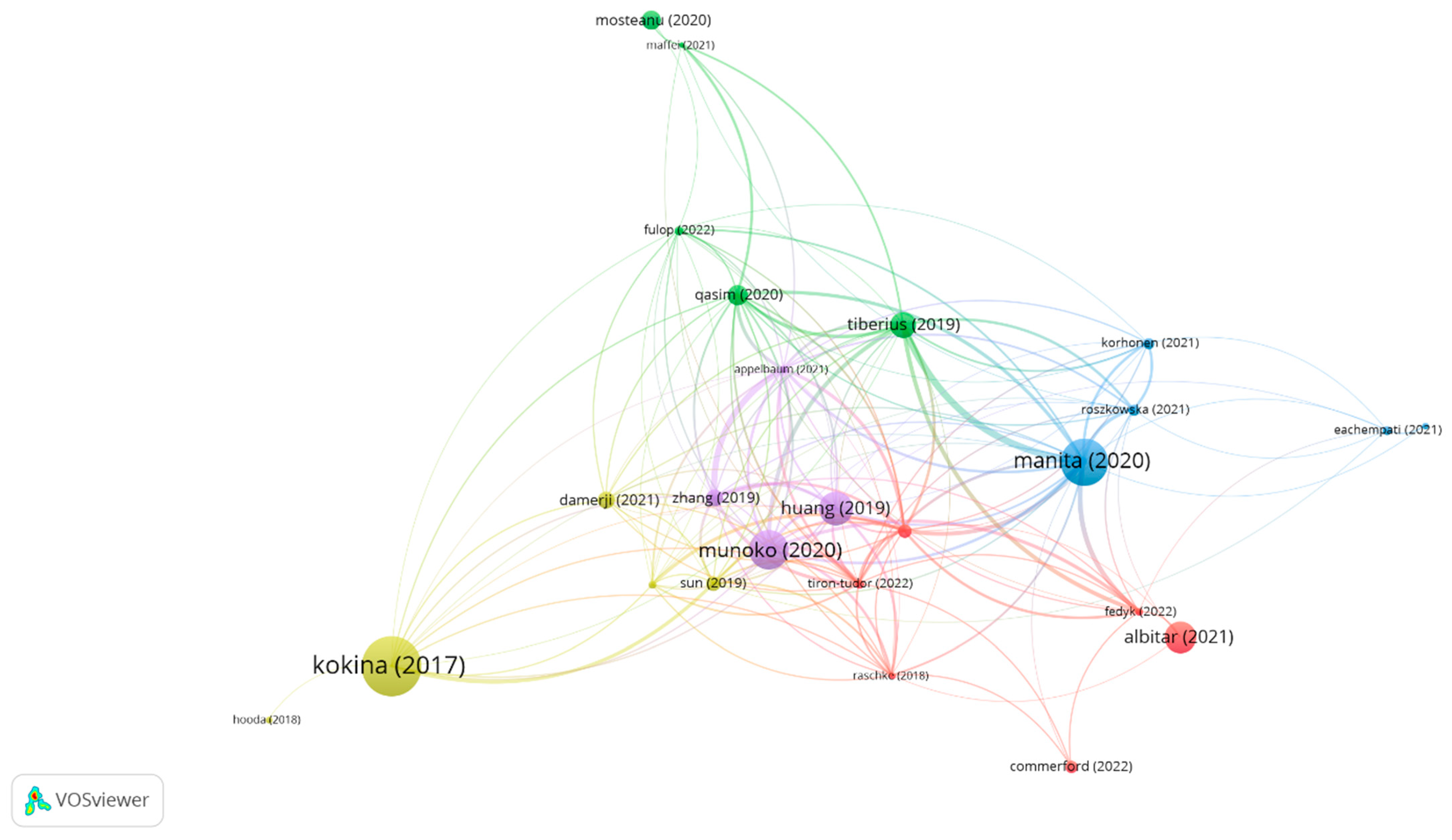

The bibliographic coupling is revealed in the form of network diagrams in

Figure 7, selecting only those documents that have been cited more than 17 times; 25 documents were identified based on this criterion. Each circle corresponds to the document, and documents with higher citation values include

Kokina and Davenport (

2017),

Manita et al. (

2020),

Munoko et al. (

2020),

Qasim and Kharbat (

2020), and

Albitar et al. (

2020). Edges between nodes depict bibliographic coupling, and where the thickness and density of the line are high, the coupling is even more vital. Some references are circled into several clusters of yellow around

Kokina and Davenport (

2017), with other different clusters as documents that often use the same references as the cluster around Manita, Munoko, Qasim, and Albitar. This map shows the organization of research within the field by categorizing the essential documents and the relationships between them: thematic categories emphasize similarity in the stated research objectives due to cited references.

Table 8 below identifies clusters gleaned from the document bibliographic coupling, which indicate five clusters of documents using the same references. The articles of

Albitar et al. (

2020),

Commerford et al. (

2022),

Fedyk et al. (

2022),

Krieger et al. (

2021),

Raschke et al. (

2018), and

Tiron-Tudor and Deliu (

2022) belonging to cluster I are mainly dedicated to increasing the applicability of technology in auditing tasks. First,

Albitar et al. (

2020) looked at the impact of the COVID-19 social distance policy on audit quality. They determined that support was necessary to enhance flexibility and collaboration between auditors and clients.

Commerford et al. (

2022) explored and demonstrated that although such auditors are willing to heed AI algorithm advice, they reduce proposed changes to management’s estimates when receiving the opposite information from AI compared to a human specialist.

Fedyk et al. (

2022) explored the effect of AI on audit quality and fees. The authors found that AI increases audit quality, coupled with a decrease in fees, however, it has an audit replacement effect when human auditors are ultimately replaced by AI systems.

Krieger et al. (

2021) explained how high-quality data analysis is implemented in auditing, and the authors recognized technological talent within audit teams.

Raschke et al. (

2018) noted the creation of opportunities for automated auditing processes by applying AI to reactivate audit inquiries. The last paper, by

Tiron-Tudor and Deliu (

2022), considered how algorithmic systems are embedded in audit work while also discussing the so-called human-in-the-loop approach to improve, on the one hand, the algorithms’ performance and, on the other, enhance the accountability of AI in auditing. In summary, the preceding literature demonstrates the possibility and potential of using advanced technology to improve audit quality and speed, as well as showing, in equal measure, the combination of people and technology for efficient auditing.

Cluster 2 includes five papers by

Tiberius and Hirth (

2019),

Qasim and Kharbat (

2020),

Mosteanu and Faccia (

2020),

Fülöp et al. (

2022), and

Maffei et al. (

2021), and examines the various impacts on digital transformation in financial reporting. Regarding the challenges and prospects of digitization in auditing,

Tiberius & Hirth (

2019) showed that there will be an orientation toward continuous audits in the future and that new technologies will support rather than replace auditors. This is similar to

Qasim and Kharbat’s (

2020) discussion, who argued for a complete overhaul of accounting curricula that involves concepts in blockchain, business data analytics, and advanced technologies so that future accounting professionals are equipped for the dynamic profession. We can also refer to

Mosteanu and Faccia (

2020) on how developments, such as blockchain and XBRL, are transforming the management of finances due to decreased error rates, as well as fraud instances, increased outlook reliability, and reduction in costs. The paper by

Fülöp et al. (

2022) pointed out that digitization is not homogenous in companies, yet professionals depend heavily on digital tools, and their use depends on perceived risks connected to technological development. Finally,

Maffei et al. (

2021) discussed blockchain technology and accountants’ and auditors’ inability to rely on it completely, emphasizing the need for professional judgment and experience. In their study, they also noted that there are new risks emerging due to blockchain technology and that the profession should prepare for and transform to accommodate these changes. These five papers show that digitalization has a significant impact on the accounting and auditing professions, highlighting both opportunities and risks, and demonstrating that integrated and lifelong learning is, therefore, essential.

Cluster 3 looks at four papers from 2020 to 2021 that discuss the pros and cons of using technology in auditing. Drawing upon cutting-edge artificial intelligence,

Eachempati et al. (

2021) explored how accounting information influences the stock market. They discovered that by observing whether the language used is positive or negative, one could forecast market behavior. The study by

Roszkowska (

2021) outlined new fintech, such as blockchain. In their view, this could help stop financial fraud and increase the trustworthiness of financial reports.

Korhonen et al. (

2021) looked at automating management accounting. They found that some tasks they assumed would be best completed by computers are better undertaken by humans, highlighting the need to be careful about what is automated.

Manita et al. (

2020) studied how digital technology is changing external audits. They underscored how it ameliorates audits, enables audit firms to offer more services, and assists them in innovation. This results in improving how companies are run by keeping managers in check. These papers demonstrate how technology impacts auditing in those ways while emphasizing the fact that integration considerations can accompany the gains from technology.

The fourth cluster consists of

Kokina and Davenport (

2017),

Damerji and Salimi (

2021),

Sun (

2019),

Zerbino et al. (

2018), and

Hooda et al. (

2020), which are most relevant to the theoretical frameworks and methods used to implement new technologies in auditing.

Kokina and Davenport (

2017) sought to provide an attractive snapshot of the advanced technologies that have recently appeared in accounting, indicating the current possibilities and potential predispositions of the cognitive technologies used by large accounting companies.

Damerji and Salimi (

2021) examined the moderating effect of beliefs concerning the ease of use and usefulness between technology readiness and the adoption of AI among accounting students; the authors stressed the relevance of individual readiness as a key determinant of the readiness for new technologies.

Sun (

2019) provided an idea for implementing deep learning in auditing procedures, demonstrating how this facilitates the decision making of auditors using natural language search, speech, image, and data. To sum up, the use of process mining enables the audit methodology proposed by

Zerbino et al. (

2018). The outcomes of this methodology highlight the benefits of applying process-mining tools for audit analysis and conducting automated information system audits, as demonstrated in a case study involving a port community system. In their work titled “Ensemble machine learning for predicting fraudulent firms”,

Hooda et al. (

2020) provided auditors with a highly accurate decision-making model to help detect high-risk or potentially fraudulent firms before conducting fieldwork. Altogether, these papers offer sound theoretical and empirical coverage of the critical factors for implementing advanced technologies in auditing.

Cluster 5 includes

Munoko et al. (

2020),

Huang and Vasarhelyi (

2019),

C. Zhang (

2019), and

Appelbaum et al. (

2021), and focused on the ethical, regulatory, and real-life issues related to technology application in auditing.

Munoko et al. (

2020) offered a prospectus of ethical issues that may arise with the use of AI in auditing while discussing the advantages and disadvantages of its implementation. Summarizing the above works,

Huang and Vasarhelyi (

2019) conducted a study on robotic process automation (RPA) in auditing and recommended a framework for employing the technology within this context. They proposed an RPA audit program where some routine tasks are automated, freeing auditors to execute work that requires judgments to a higher degree.

C. Zhang (

2019) also discussed the use of RPA in audit engagements and how it can act as a change agent for enhancing how audits are conducted by integrating innovative technologies.

Appelbaum et al. (

2021) put forward a framework for auditor data literacy to highlight the necessity for technology and ADA in audit procedures. The imperative highlighted is the need to respond to market requirements and guarantee effective audits within a digitalized business environment. To summarize, these works reinforce the importance of paying attention to ethical concerns of integrating technologies in the auditing process, in addition to improving auditor knowledge and abilities to address emerging challenges.

Table 9 below presents a list of the documents used in the content analysis of AI and innovative technologies in auditing. These are documents dating from 2017 to 2024, written by KPMG and other authors from the auditing profession. KPMG’s publications, such as “Monitoring with drones in the energy industry”, released in 2021, stress the importance of drone applications to increase inspection rates in the energy industry, while “Harnessing the power of cognitive technology to transform the audit”, released in 2017, explored incorporating cognitive technologies in audits. In 2024, KPMG’s “All eyes on AI in Audit 2024” and “AI in Financial Reporting and Audit” emphasized the role of AI in enhancing the auditing industry, primarily regarding the accuracy of financial reports. Moreover,

EY’s (

2024) insight titled “Audit Innovation In Audit” captured the general industry trend of auditors adopting technology to bolster effectiveness when selecting audit techniques. Taken together, these documents substantiate the increasing popularity of AI and other similar technologies in auditing. For example,

Munoko et al. (

2020) investigated ethical issues that surround AI being used in audits, and

C. Zhang (

2019) explored the application of the Institute of Internal Auditors (IIA) standards in audit engagements, where automation plays a central role in determining the changes that will be implemented. In the same vein,

Huang and Vasarhelyi (

2019), together with

Appelbaum et al. (

2021), called for increasing automation to increase audit efficiency and efficacy. The documents presented in

Table 4 reflect these trends.

Some reports in

Table 9 show advancements in AI and technology in auditing and are therefore relevant for understanding how AI improves financial reporting. For instance, a

KPMG (

2021) study titled “Monitoring with drones in the energy industry” explored how AI-enabled drones could help in auditing inspections, highlighting a possible implication of the technology in the formulation of decisions by non-Big 4 external auditors. As described in detail in the

KPMG (

2017) report titled “Harnessing the power of cognitive technology to transform the audit”, AI should be used to maintain a good working environment that will enhance both the consistency of audits and their quality. Similarly, Sebastian Stöckle’s article titled “All eyes on AI in Audit 2024”, which he published in 2024, focused on how artificial intelligence is expanding in auditing education and equipping analysts to leverage technology to spearhead insightful financial reporting in the future. The

KPMG (

2024) report “AI in Financial Reporting and Audit” explained that we need rules and regulations to enable auditors to get the maximum from AI to enhance the quality assurance and reliability of financial reports. Lastly, the EY report on audit innovation discussed the transformative integration of IFRS with artificial intelligence to modernize financial reporting, aligning with current technological advancements and the demand for more accurate and transparent financial statements.

.png)

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}