The Impact of Political Risks on Financial Markets: Evidence from a Stock Price Crash Perspective

Abstract

1. Introduction

2. Literature Review

2.1. Consequences of Political Risks

2.2. The Influence of Political Events on Financial Markets

2.3. Political Risk and Corporate Finance

3. Data Source, Variables, and Empirical Specification

3.1. Data Source and Sample Selection

3.2. Variable Construction

3.3. Model Specification

4. Empirical Results

4.1. Benchmark Regression Estimation

4.2. Robustness Checks: Altering the Measurement of Stock Price Crash Risk

4.3. Robustness Checks: Instrumental Variable Regression

4.4. Robustness Checks: Altering the Measurement of Political Risk

4.5. Robustness Checks: Winsorization of Stock Price Crash Risk

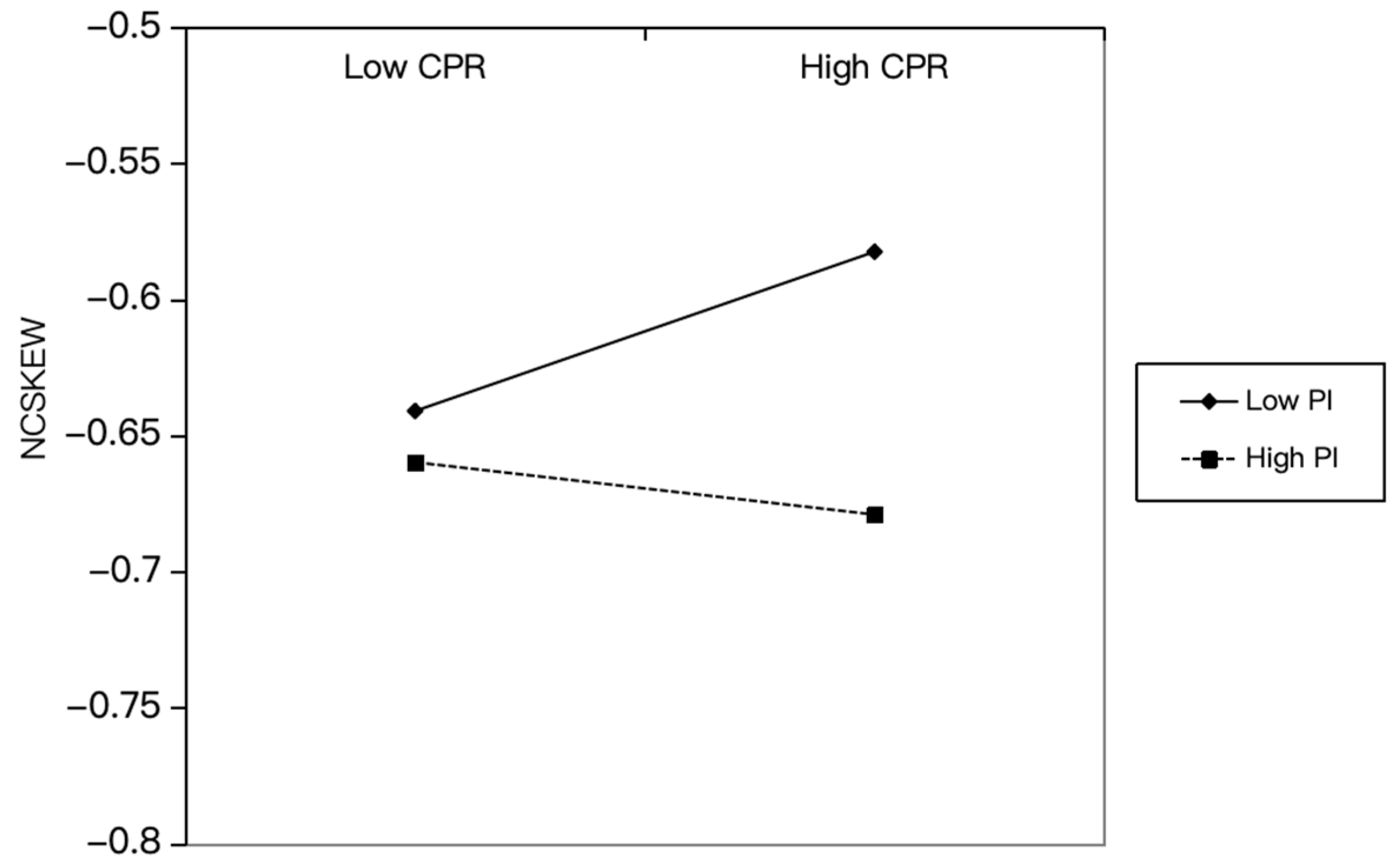

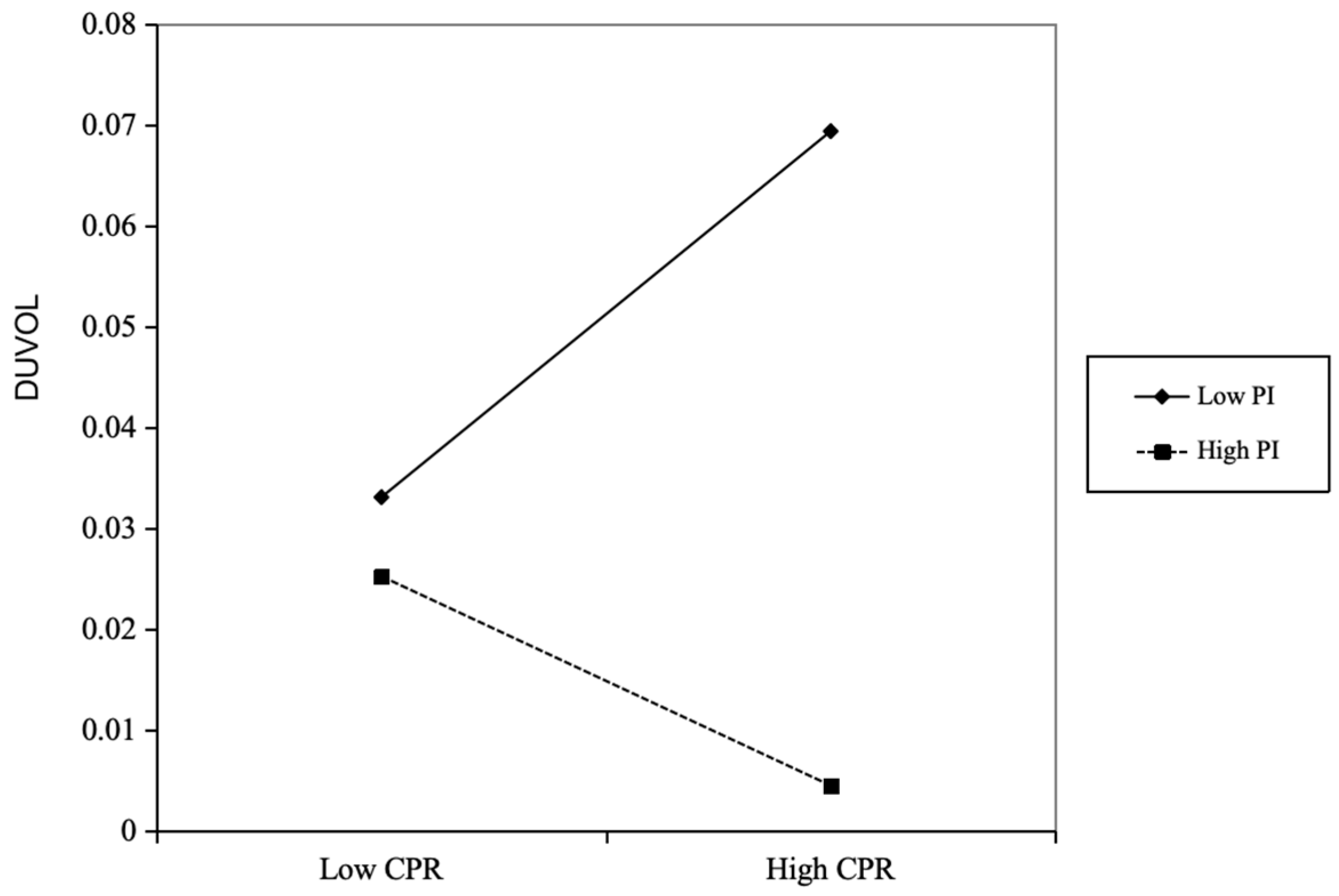

5. Further Discussions on the Effect of Political Involvement

6. Concluding Remarks

Author Contributions

Funding

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A. Calculation Process of Stock Price Crash Risk

Appendix B. Calculation Process of the Corporate Political Risk (CPR) Index

Appendix C. Variable Measure Descriptions

{kind=link}

{kind=link}

| Variable | Definition |

|---|---|

| NCSKEW | Negative return skewness coefficient |

| DUVOL | Up and down volatility of stock returns |

| CPR | Firm-level political risk index |

| Firm_age | Number of years after the firm’s establishment |

| Firm_size | Natural logarithm of total assets |

| Soe | Dummy variable that equals 1 if a firm is state-owned and 0 otherwise |

| Indep | Ratio of the number of independent directors to the number of board directors |

| Board | Natural logarithm of the number of board of directors |

| CEO_duality | Dummy variable that equals 1 if the CEO is also the chairperson of the board and 0 otherwise |

| CEO_age | CEO age |

| CEO_gender | Dummy variable equaling 1 if the CEO is male and 0 otherwise |

| Bga | Equals 1 if a firm’s group affiliation in each year of its ultimate controlling entity had more than one firm in that year and equals 0 otherwise |

| PI | The overlapping ratio of members between the firm’s board of directors and a Party Committee |

| Variable | (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | (9) | (10) | (11) |

|---|---|---|---|---|---|---|---|---|---|---|---|

| (1) NCSKEW | 1.000 | ||||||||||

| (2) DUVOL | 0.881 | 1.000 | |||||||||

| (3) CPR | −0.034 | −0.038 | 1.000 | ||||||||

| (4) Firm_age | −0.049 | −0.056 | 0.053 | 1.000 | |||||||

| (5) Firm_size | −0.070 | −0.098 | 0.264 | 0.161 | 1.000 | ||||||

| (6) Soe | −0.085 | −0.096 | 0.243 | 0.140 | 0.336 | 1.000 | |||||

| (7) Indep | 0.006 | 0.007 | −0.009 | −0.011 | 0.026 | −0.058 | 1.000 | ||||

| (8) Board | −0.033 | −0.041 | 0.124 | 0.004 | 0.257 | 0.264 | −0.486 | 1.000 | |||

| (9) CEO_duality | 0.037 | 0.047 | −0.098 | −0.083 | −0.167 | −0.291 | 0.108 | −0.178 | 1.000 | ||

| (10) CEO_age | −0.027 | −0.022 | 0.061 | 0.121 | 0.122 | 0.082 | 0.015 | 0.043 | 0.172 | 1.000 | |

| (11) CEO_gender | −0.004 | −0.006 | 0.040 | −0.023 | 0.039 | 0.066 | −0.053 | 0.074 | 0.021 | 0.029 | 1.000 |

| (12) Bga | 0.019 | 0.022 | −0.082 | −0.066 | −0.084 | −0.158 | −0.009 | −0.027 | 0.168 | 0.022 | −0.034 |

References

- Ahsan, Tanveer, and Muhammad Azeem Qureshi. 2021. The nexus between policy uncertainty, sustainability disclosure and firm performance. Applied Economics 53: 441–53. [Google Scholar] [CrossRef]

- Alesina, Alberto, Nouriel Roubini, and Gerald D. Cohen. 1997. Political Cycles and the Macroeconomy. Cambridge, MA: MIT Press. [Google Scholar] [CrossRef]

- Antonakakis, Nikolaos, Rangan Gupta, Christos Kollias, and Stephanos Papadamou. 2017. Geopolitical risks and the oil-stock nexus over 1899–2016. Finance Research Letters 23: 165–73. [Google Scholar] [CrossRef]

- Antweiler, Werner, and Murray Z. Frank. 2004. Is all that talk just noise? The information content of internet stock message boards. The Journal of Finance 59: 1259–94. [Google Scholar] [CrossRef]

- Apergis, Nicholas, Matteo Bonato, Rangan Gupta, and Clement Kyei. 2018. Does geopolitical risks predict stock returns and volatility of leading defense companies? Evidence from a nonparametric approach. Defence and Peace Economics 29: 684–96. [Google Scholar] [CrossRef]

- Baker, Malcolm, and Jeffrey Wurgler. 2006. Investor sentiment and the cross-section of stock returns. The Journal of Finance 61: 1645–80. [Google Scholar] [CrossRef]

- Balcilar, Mehmet, Rangan Gupta, Clement Kyei, and Mark E. Wohar. 2016. Does economic policy uncertainty predict exchange rate returns and volatility? Evidence from a nonparametric causality-in-quantiles test. Open Economies Review 27: 229–50. [Google Scholar] [CrossRef]

- Barber, Brad M., and Terrance Odean. 2008. All that glitters: The effect of attention and news on the buying behavior of individual and institutional investors. The Review of Financial Studies 21: 785–818. [Google Scholar] [CrossRef]

- Baur, Dirk G., and Lee A. Smales. 2018. Gold and Geopolitical Risk. SSRN Working Paper No. 3109136. Rochester: SSRN. [Google Scholar]

- Bekaert, Geert, Campbell R. Harvey, Christian T. Lundblad, and Stephan Siegel. 2016. Political risk and international valuation. Journal of Corporate Finance 37: 1–23. [Google Scholar] [CrossRef]

- Benhmad, François. 2012. Modeling nonlinear Granger causality between the oil price and U.S. dollar: A wavelet based approach. Economic Modelling 29: 1505–14. [Google Scholar] [CrossRef]

- Berkman, Henk, Ben Jacobsen, and John B. Lee. 2011. Time-varying rare disaster risk and stock returns. Journal of Financial Economics 101: 313–32. [Google Scholar] [CrossRef]

- Bernanke, Ben S. 1983. Irreversibility, uncertainty, and cyclical investment. The Quarterly Journal of Economics 98: 85–106. [Google Scholar] [CrossRef]

- Bittlingmayer, George. 1998. Output, stock volatility, and political uncertainty in a natural experiment: Germany, 1880–940. The Journal of Finance 53: 2243–57. [Google Scholar] [CrossRef]

- Brounen, Dirk, and Jeroen Derwall. 2010. The impact of terrorist attacks on international stock markets. European Financial Management 16: 585–98. [Google Scholar] [CrossRef]

- Caldara, Dario, and Matteo Iacoviello. 2022. Measuring geopolitical risk. American Economic Review 112: 1194–225. [Google Scholar] [CrossRef]

- Callen, Jeffrey L., and Xiaohua Fang. 2015. Short interest and stock price crash risk. Journal of Banking & Finance 60: 181–94. [Google Scholar] [CrossRef]

- Carney, Mark. 2016. Uncertainty, the Economy and Policy. London: Bank of England. [Google Scholar]

- Carter, David A., and Betty J. Simkins. 2004. The market’s reaction to unexpected, catastrophic events: The case of airline stock returns and the September 11th attacks. The Quarterly Review of Economics and Finance 44: 539–58. [Google Scholar] [CrossRef]

- Chen, Joseph, Harrison Hong, and Jeremy C Stein. 2001. Forecasting crashes: Trading volume, past returns, and conditional skewness in stock prices. Journal of Financial Economics 61: 345–81. [Google Scholar] [CrossRef]

- Chen, Shihua, Yan Ye, and Khalil Jebran. 2022. Tax enforcement efforts and stock price crash risk: Evidence from China. Journal of International Financial Management & Accounting 33: 193–218. [Google Scholar] [CrossRef]

- Chesney, Marc, Ganna Reshetar, and Mustafa Karaman. 2011. The impact of terrorism on financial markets: An empirical study. Journal of Banking & Finance 35: 253–67. [Google Scholar] [CrossRef]

- Chletsos, Michael, and Andreas Sintos. 2024. Political stability and financial development: An empirical investigation. The Quarterly Review of Economics and Finance 94: 252–66. [Google Scholar] [CrossRef]

- Choi, Wonseok, Chune Young Chung, and Kainan Wang. 2022. Firm-level political risk and corporate investment. Finance Research Letters 46: 102307. [Google Scholar] [CrossRef]

- Christensen, Dane M., Hengda Jin, Suhas A. Sridharan, and Laura A. Wellman. 2022. Hedging on the hill: Does political hedging reduce firm risk? Management Science 68: 4356–79. [Google Scholar] [CrossRef]

- Da, Zhi, Joseph Engelberg, and Pengjie Gao. 2011. In search of attention. The Journal of Finance 66: 1461–99. [Google Scholar] [CrossRef]

- Ding, Haoyuan, Yi Li, Chang Xue, and Liang Wang. 2022. The Belt and Road Initiative, political involvement, and China’s OFDI. International Studies of Economics 17: 459–83. [Google Scholar] [CrossRef]

- El Ghoul, Sadok, Omrane Guedhami, Yongtae Kim, and Hyo Jin Yoon. 2021. Policy uncertainty and accounting quality. The Accounting Review 96: 233–60. [Google Scholar] [CrossRef]

- Gala, Vito D., Giovanni Pagliardi, and Stavros A. Zenios. 2023. Global political risk and international stock returns. Journal of Empirical Finance 72: 78–102. [Google Scholar] [CrossRef]

- Gao, Zhenyu, Haohan Ren, and Bohui Zhang. 2020. Googling investor sentiment around the world. Journal of Financial and Quantitative Analysis 55: 549–80. [Google Scholar] [CrossRef]

- Girma, Sourafel, and Anja Shortland. 2008. The political economy of financial development. Oxford Economic Papers 60: 567–96. [Google Scholar] [CrossRef]

- Hasan, Mostafa Monzur, and Haiyan Jiang. 2023. Political sentiment and corporate social responsibility. The British Accounting Review 55: 101170. [Google Scholar] [CrossRef]

- Hassan, Tarek A., Stephan Hollander, Laurence van Lent, and Ahmed Tahoun. 2019. Firm-level political risk: Measurement and effects. The Quarterly Journal of Economics 134: 2135–202. [Google Scholar] [CrossRef]

- He, Jia, Xinyang Mao, Oliver M. Rui, and Xiaolei Zha. 2013. Business groups in China. Journal of Corporate Finance 22: 166–92. [Google Scholar] [CrossRef]

- Heston, Steven L., and Nitish Ranjan Sinha. 2016. News vs. sentiment: Predicting stock returns from news stories. Financial Analysts Journal 73: 67–83. [Google Scholar] [CrossRef]

- Jia, Ning. 2018. Corporate innovation strategy and stock price crash risk. Journal of Corporate Finance 53: 155–73. [Google Scholar] [CrossRef]

- Karolyi, G. Andrew, and Rodolfo Martell. 2010. Terrorism and the stock market. International Review of Applied Financial Issues and Economics 2: 285. [Google Scholar] [CrossRef]

- Kelly, Bryan, Ľuboš Pástor, and Pietro Veronesi. 2016. The price of political uncertainty: Theory and evidence from the option market. The Journal of Finance 71: 2417–80. [Google Scholar] [CrossRef]

- Kim, Chansog (Francis), Incheol Kim, Christos Pantzalis, and Jung Chul Park. 2019. Policy uncertainty and the dual role of corporate political strategies. Financial Management 48: 473–504. [Google Scholar] [CrossRef]

- Kim, Jeong-Bon, Yinghua Li, and Liandong Zhang. 2011. Corporate tax avoidance and stock price crash risk: Firm-level analysis. Journal of Financial Economics 100: 639–62. [Google Scholar] [CrossRef]

- Lim, Ivan, and Duc Duy Nguyen. 2021. Hometown lending. Journal of Financial and Quantitative Analysis 56: 2894–933. [Google Scholar] [CrossRef]

- Liu, Guanchun, May Hu, and Chen Cheng. 2021. The information transfer effects of political connections on mitigating policy uncertainty: Evidence from China. Journal of Corporate Finance 67: 101916. [Google Scholar] [CrossRef]

- Liu, Haiyue, Yile Wang, Rui Xue, Martina Linnenluecke, and Cynthia Weiyi Cai. 2022. Green commitment and stock price crash risk. Finance Research Letters 47: 102646. [Google Scholar] [CrossRef]

- Luo, Yan, and Chenyang Zhang. 2020. Economic policy uncertainty and stock price crash risk. Research in International Business and Finance 51: 101112. [Google Scholar] [CrossRef]

- Murray, Daniel. 2018. Geopolitical risk and commodities: An investigation. Global Commodities Applied Research Digest 3: 95–106. [Google Scholar]

- Neacsu, Marius-Cristian. 2016. Geoeconomic vs. geostrategic conflicts case study: Russia–western world. Strategic Impact 58: 13–22. [Google Scholar]

- Nguyen, My, and Justin Hung Nguyen. 2020. Economic policy uncertainty and firm tax avoidance. Accounting & Finance 60: 3935–78. [Google Scholar] [CrossRef]

- Pan, Wei-Fong. 2018. Geopolitical Risk Impacts on Asset Markets: Evidence from Data over Century. SSRN Working Paper No. 3222468. Rochester: SSRN. [Google Scholar] [CrossRef]

- Pastor, Lubos, and Pietro Veronesi. 2012. Uncertainty about government policy and stock prices. The Journal of Finance 67: 1219–64. [Google Scholar] [CrossRef]

- Peng, Lin, and Wei Xiong. 2006. Investor attention, overconfidence and category learning. Journal of Financial Economics 80: 563–602. [Google Scholar] [CrossRef]

- Pham, Anh Viet. 2019. Political risk and cost of equity: The mediating role of political connections. Journal of Corporate Finance 56: 64–87. [Google Scholar] [CrossRef]

- Portes, Jonathan. 2023. The impact of Brexit on the UK economy: Reviewing the evidence. VOXEU Column. Available online: https://cepr.org/voxeu/columns/impact-brexit-uk-economy-reviewing-evidence (accessed on 15 May 2024).

- Rigobon, Roberto, and Brian Sack. 2005. The effects of war risk on US financial markets. Journal of Banking & Finance 29: 1769–89. [Google Scholar] [CrossRef]

- Rivlin, Paul. 2018. Leverage of economic sanctions: The case of US sanctions against Iran, 1979–2016. In Geo-Economics and Power Politics in the 21st Century. London: Routledge, pp. 99–113. [Google Scholar]

- Roe, Mark J., and Jordan I. Siegel. 2011. Political instability: Effects on financial development, roots in the severity of economic inequality. Journal of Comparative Economics 39: 279–309. [Google Scholar] [CrossRef]

- Tetlock, Paul C. 2007. Giving content to investor sentiment: The role of media in the stock market. The Journal of Finance 62: 1139–68. [Google Scholar] [CrossRef]

- Wang, Bo, and Chao Xu. 2017. The impacts of Muslim refugee crisis on European society. Arab World Studies 3: 60–74. (In Chinese). [Google Scholar]

- Wang, Liang. 2023. Mitigating firm-level political risk in China: The role of multiple large shareholders. Economics Letters 222: 110960. [Google Scholar] [CrossRef]

- Wang, Liang, Qikai Wang, and Fan Jiang. 2023a. Booster or stabilizer? Economic policy uncertainty: New firm-specific measurement and impacts on stock price crash risk. Finance Research Letters 51: 103462. [Google Scholar] [CrossRef]

- Wang, Liang, Yu Zhang, and Chengshuang Qi. 2023b. Does the CEOs’ hometown identity matter for firms’ environmental, social, and governance (ESG) performance? Environmental Science and Pollution Research 30: 69054–63. [Google Scholar] [CrossRef] [PubMed]

- Wellman, Laura A. 2017. Mitigating political uncertainty. Review of Accounting Studies 22: 217–50. [Google Scholar] [CrossRef]

- Wisniewski, Tomasz Piotr. 2009. Can political factors explain the behaviour of stock prices beyond the standard present value models? Applied Financial Economics 19: 1873–84. [Google Scholar] [CrossRef]

- Wu, Keping, Yumei Fu, and Dongmin Kong. 2022. Does the digital transformation of enterprises affect stock price crash risk? Finance Research Letters 48: 102888. [Google Scholar] [CrossRef]

- Xiong, Chenran, Limao Wang, Qiushi Qu, Ning Xiang, and Bo Wang. 2020. Progress and prospect of geopolitical risk research. Progress in Geography 39: 695–706. (In Chinese). [Google Scholar] [CrossRef]

| Variable | (1) | (2) | (3) | (4) |

|---|---|---|---|---|

| NCSKEW | DUVOL | NCSKEW | DUVOL | |

| CPR | 0.0767 *** | 0.0451 *** | 0.0723 *** | 0.0440 *** |

| (0.0154) | (0.0125) | (0.0141) | (0.0120) | |

| Firm age | −0.0411 | −0.0307 | ||

| (0.0736) | (0.0485) | |||

| Firm size | 0.0235 | −0.0094 | ||

| (0.0165) | (0.0096) | |||

| Soe | −0.0151 | −0.0174 | ||

| (0.0245) | (0.0131) | |||

| Indep | 0.1503 | 0.1453 * | ||

| (0.1251) | (0.0765) | |||

| Board | 0.0121 | 0.0254 | ||

| (0.0375) | (0.0260) | |||

| CEO dual role | −0.0061 | 0.0037 | ||

| (0.0125) | (0.0082) | |||

| CEO age | −0.0014 | −0.0007 | ||

| (0.0012) | (0.0008) | |||

| CEO gender | 0.0217 | 0.0251 | ||

| (0.0373) | (0.0216) | |||

| Bga | −0.0211 | −0.0152 | ||

| (0.0373) | (0.0231) | |||

| Constant | −0.2754 *** | −0.1788 *** | −0.6563 ** | 0.0527 |

| (0.0015) | (0.0012) | (0.2875) | (0.2299) | |

| Firm fixed effect | Yes | Yes | Yes | Yes |

| Year fixed effect | Yes | Yes | Yes | Yes |

| Observation | 23,677 | 23,677 | 23,677 | 23,677 |

| Firm number | 3408 | 3408 | 3408 | 3408 |

| R2 | 0.2307 | 0.2291 | 0.2312 | 0.2296 |

| Variable | (1) | (2) |

|---|---|---|

| Crash | Crash | |

| CPR | 0.0269 * | 0.0273 * |

| (0.0137) | (0.0137) | |

| Constant | 0.1033 *** | 0.1463 |

| (0.0013) | (0.1573) | |

| Controls | No | Yes |

| Firm fixed effect | Yes | Yes |

| Year fixed effect | Yes | Yes |

| Observation | 23,677 | 23,677 |

| Firm number | 3408 | 3408 |

| R2 | 0.1590 | 0.1593 |

| First Stage | Second Stage | ||

|---|---|---|---|

| Variable | (1) | (2) | (3) |

| CPR | NCSKEW | DUVOL | |

| Mean CPR | 0.3362 *** | ||

| (0.0730) | |||

| CPR | 1.4067 *** | 1.0534 *** | |

| (0.3341) | (0.2280) | ||

| Controls | Yes | Yes | Yes |

| Year fixed effect | Yes | Yes | Yes |

| Firm fixed effect | Yes | Yes | Yes |

| Observation | 23,677 | 23,677 | 23,677 |

| Firm number | 3408 | 3408 | 3408 |

| R2 | 0.112 | 0.131 | 0.147 |

| Variable | (1) | (2) |

|---|---|---|

| NCSKEW | DUVOL | |

| PS | 0.0991 *** | 0.0811 *** |

| (0.0201) | (0.0163) | |

| Constant | −0.9111 ** | 0.0116 |

| (0.2937) | (0.2324) | |

| Controls | Yes | Yes |

| Firm fixed effect | Yes | Yes |

| Year fixed effect | Yes | Yes |

| Observation | 23,677 | 23,677 |

| Firm number | 3408 | 3408 |

| R2 | 0.2311 | 0.2296 |

| Variable | (1) | (2) |

|---|---|---|

| NCSKEW | DUVOL | |

| CPR | 0.0698 *** | 0.0429 *** |

| (0.0140) | (0.0116) | |

| Constant | −0.5461 * | 0.0743 |

| (0.2701) | (0.2253) | |

| Controls | Yes | Yes |

| Firm fixed effect | Yes | Yes |

| Year fixed effect | Yes | Yes |

| Observation | 23677 | 23677 |

| Firm number | 3408 | 3408 |

| R2 | 0.2298 | 0.2277 |

| Variable | (1) | (2) |

|---|---|---|

| NCSKEW | DUVOL | |

| CPR | 0.0627 *** | 0.0406 *** |

| (0.0118) | (0.0109) | |

| Constant | −0.4346 * | 0.0780 |

| (0.2478) | (0.2120) | |

| Controls | Yes | Yes |

| Firm fixed effect | Yes | Yes |

| Year fixed effect | Yes | Yes |

| Observation | 23,677 | 23,677 |

| Firm number | 3408 | 3408 |

| R2 | 0.2295 | 0.2257 |

| Variable | (1) | (2) |

|---|---|---|

| NCSKEW | DUVOL | |

| CPR | 0.0506 *** | 0.0376 *** |

| (0.0092) | (0.0092) | |

| Constant | −0.3507 | 0.0383 |

| (0.2130) | (0.1828) | |

| Controls | Yes | Yes |

| Firm fixed effect | Yes | Yes |

| Year fixed effect | Yes | Yes |

| Observation | 23,677 | 23,677 |

| Firm number | 3408 | 3408 |

| R2 | 0.2275 | 0.2220 |

| Variable | (1) | (2) |

|---|---|---|

| NCSKEW | DUVOL | |

| CPR | 0.0753 *** | 0.0438 *** |

| (0.0177) | (0.0130) | |

| CPR × PI | −0.1499 *** | −0.1017 *** |

| (0.0460) | (0.0215) | |

| Controls | Yes | Yes |

| Firm fixed effect | Yes | Yes |

| Year fixed effect | Yes | Yes |

| N | 23,677 | 23,677 |

| F-test | 15.19 | 36.66 |

| Firm number | 3408 | 3408 |

| R2 | 0.2312 | 0.2296 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Ma, Y.; Wei, Q.; Gao, X. The Impact of Political Risks on Financial Markets: Evidence from a Stock Price Crash Perspective. Int. J. Financial Stud. 2024, 12, 51. https://doi.org/10.3390/ijfs12020051

Ma Y, Wei Q, Gao X. The Impact of Political Risks on Financial Markets: Evidence from a Stock Price Crash Perspective. International Journal of Financial Studies. 2024; 12(2):51. https://doi.org/10.3390/ijfs12020051

Chicago/Turabian StyleMa, Yanping, Qian Wei, and Xiang Gao. 2024. "The Impact of Political Risks on Financial Markets: Evidence from a Stock Price Crash Perspective" International Journal of Financial Studies 12, no. 2: 51. https://doi.org/10.3390/ijfs12020051

APA StyleMa, Y., Wei, Q., & Gao, X. (2024). The Impact of Political Risks on Financial Markets: Evidence from a Stock Price Crash Perspective. International Journal of Financial Studies, 12(2), 51. https://doi.org/10.3390/ijfs12020051