1. Introduction

In recent years, ESG investing has undeniably gained remarkable traction, successfully capturing the attention of both institutional and individual investors on a global scale. ESG funds, which incorporate environmental, social, and governance factors into their investment strategies, have emerged as a prominent avenue for aligning financial goals with sustainability objectives. The phenomenon under discussion is important in the country of China, as there has been a considerable surge in sustainable and responsible investment, attracting considerable attention.

The Chinese market has witnessed a remarkable presence of ESG funds, indicating their popularity among investors. As of October 2021, the number of ESG mutual funds in China reached an impressive 344, with assets owned or under management amounting to RMB 549.24 billion (

Liu et al. 2023). This significant market presence underscores the relevance and potential impact of ESG funds in China’s investment landscape. Furthermore, the concept of ESG gained even more prominence in China’s securities market after the country set forth its ambitious goal of achieving “double carbon” (

W. Zhu 2023). This entails a strong focus on environmental and social responsibility, thereby driving the popularity of ESG investing in China.

Against this backdrop, this paper aims to delve into the realm of ESG funds in China, with specific emphasis on three critical aspects: management fees, ESG scores, and investment performance. While management fees have always been a crucial consideration for investors, the unique characteristics of ESG funds warrant closer examination. These funds often require specialized research, data analysis, and ongoing monitoring to ensure adherence to ESG criteria, potentially leading to higher management fees compared to traditional funds. By exploring the relationship between management fees and ESG funds in China, we can shed light on the cost–benefit analysis for investors and evaluate the potential impact on long-term returns.

Furthermore, assessing the investment performance of ESG funds is paramount in understanding their efficacy as investment vehicles. Questions emerge as to whether investing in ESG funds in China can generate competitive returns while simultaneously promoting sustainable practices. Through the analysis of historical performance data, risk-adjusted returns, and benchmark comparisons, this study aims to provide insights into the investment performance of ESG funds in China. Such analysis can aid investors in making informed decisions about incorporating ESG funds into their portfolios, potentially driving positive change in the financial markets and encouraging sustainable practices among Chinese companies. In brief, this paper considers the following two hypotheses: (a) ESG funds charge higher management fees; and (b) ESG funds outperform other funds.

The significance of this research lies in its ability to inform investors, asset managers, and policymakers about the nuances of ESG funds in China, particularly in relation to their management fees and investment performance. By bridging the gap in our understanding, we can contribute to the ongoing discourse surrounding responsible investing and provide valuable insights for individuals and organizations seeking to align their financial goals with their environmental and social values.

The structure of this paper is as follows:

Section 2 provides a literature review on management fees and investment performance of investment funds in general, with a specific focus on ESG funds.

Section 3 discusses the data and sample used in this study.

Section 4 presents the performance metrics and regression results of the sampled funds.

Section 5 summarizes the key findings and concludes the paper.

2. Literature Review

The following sections summarize previous research conducted on fund management fees and performance. These studies have explored the association between these fees and performance in various contexts. Additionally, some of these studies have examined the relationship within ESG funds.

Previous research has explored the association between fund fees and performance but yielded mixed conclusions. Some studies suggest a negative relationship between management fees and performance. For example,

Ben-David et al. (

2023) found a strong negative correlation between long-run performance and incentive fees in hedge funds. Both

Wermers (

2000) and

Gruber (

1996) concluded that there is a significant negative correlation between fees and risk-adjusted returns in mutual funds.

Cooper et al. (

2021) studied equity funds and observed a statistically significant negative association between net-of-fee performance and fees.

Phalippou (

2020) argued that private equity managers should not be paid their profit sharing due to the underperformance of private equity funds compared to typical equity funds.

On the other hand, some studies suggest a positive association between management fees and performance.

Brown (

2012) demonstrated that hedge fund managers delivered high excess returns justifying their high-performance fees.

Ippolito (

1992) found that the risk-adjusted return of high-fee open-end funds exceeds the investment cost caused by the fees.

In addition, some studies suggest there is no significant relationship between fees and performance.

Cao et al. (

2008) found an insignificant relationship between fees and performance in funds.

Berk and Green (

2004) argued that fund fees should be irrelevant if investors allocate capital among funds in a way that overall investment has zero expected performance over a passive benchmark.

Berk and van Binsbergen (

2015) found that while the average gross value contributed by fund managers is positive, the funds’ alphas after fees are zero, supporting the view that fund costs should not matter to investors.

Pastor et al. (

2020) argued that increased transaction costs associated with reduced liquidity and more turnover offset the predicted gross profits, resulting in no excess return due to higher fund costs.

Stambaugh (

2020) and

M. Zhu (

2018) suggested fund-manager skill plays a role in the relationship between fees and performance. They argued that greater skill allows managers to identify profit opportunities more accurately, but active management corrects prices more, diminishing the profits offered by those opportunities.

Factors such as the types of funds, the size of funds, and other characteristics further exert an influence on the fees for management.

Latzko (

1999) found that larger funds tend to have lower cost ratios and management fees.

Dellva and Olson (

2005) explored a range of factors affecting fees, including operational expenses, fund types, performance, duration time, subscription fees, 12b-1 fees, and redemption fees.

Tufano and Sevick (

1997) found that funds with smaller boards of directors tend to have lower fees.

Integrating environmental, social, and governance (ESG) factors into investment decisions has gained importance among global institutional investors. There are many studies on how ESG affects the performance of listed companies (

Carnini Pulino et al. 2022;

Aldieri et al. 2023;

Friede et al. 2015). However, research on the relationship between ESG incorporation and portfolio performance is limited and has produced mixed results. Some studies suggest that ESG incorporation improves fund performance by capturing material information about firm fundamentals. Others argue that responsible investing constraints may lead to excluding stocks with higher return potential.

Steen et al. (

2020) examined the connection between Morningstar’s ESG ratings and the performance of mutual funds in Norway. They found no discernible impact of ESG ratings on fund performance and no abnormal risk-adjusted returns. However, they observed a geographical bias, with European funds in the top ESG quintiles exhibiting significantly higher returns and positive alphas.

Lee et al. (

2022) found that the return on sustainable funds is more significant than on non-sustainable ones. Similarly,

Dreyer et al. (

2023) provided evidence that investors could have increased their portfolio ESG performance while also increasing their risk-adjusted returns in the US stock market from 2002 to 2015. Furthermore,

Lee et al. (

2020) found compelling evidence that integrating ESG analyses into ongoing investment practices in Australia does not harm risk-adjusted returns.

On the other hand,

Rahman and Lau (

2023) suggested that an ESG-inclined method does not produce greater risk-adjusted returns, as ESG has returns comparable to any equity factor after adjusting for market cap and volatility bias.

Rompotis (

2022) also found that after factor-adjusting returns and risks, ESG and non-ESG stocks with positive alphas present comparable return-to-risk statistics.

Ferriani and Natoli (

2020) highlighted that during the COVID-19 crisis, low-ESG risk funds performed significantly better than high-risk ones, contrary to past evidence gathered with the old ESG scores. This suggests that the performance of ESG funds can be influenced by external factors such as global crises. Additionally,

Vannoni et al. (

2020) conducted a comparison between the collective performance of several SRI funds and the MSCI World Index. Their findings revealed that, on average, the SRI funds outdid the index. Nevertheless, they underscored the significance of incorporating financial and ESG analysis into the investment process, cautioning that relying solely on sustainability scores does not guarantee a positive financial return.

Overall, the correlation between ESG funds and their financial performance is intricate and diverse. Certain studies suggest that ESG funds can generate superior and risk-adjusted returns, while others indicate similar performance to non-ESG funds. The performance of ESG funds can also be impacted by external elements like market conditions and global crises.

There is limited research on the relationship between management fees and performance, specifically in ESG funds.

Dutta and Paul (

2023) found that ESG funds do not charge higher fees or sacrifice returns compared to traditional funds.

Kreander et al. (

2005) indicated that management fees are a significant explanatory variable for ESG fund performance. However,

Abate et al. (

2021) did not find a positive correlation between management fees and the number of screening criteria applied in ESG funds.

Overall, the relationship between fees and performance, as well as the impact of ESG factors on fund performance, remains complex and requires further investigation to fully understand its implications. The expertise of fund managers and factors such as fund size and type also influence this relationship.

3. Data and Sample

This paper aims to analyze the performance of open-end funds in China by collecting raw data from Wind Information, a reliable source of financial information. The dataset includes information on 16,530 open-end funds that were launched between 21 September 2001 and 30 June 2022.

To ensure accurate performance estimation, this paper focuses on funds with a minimum track record of 5 years, specifically between 30 June 2017 and 30 June 2022. From this 5-year period, this paper extracts data for a more recent 3-year period, specifically from 30 June 2019 to 30 June 2022. The purpose of comparing the 3-year and 5-year performance is to gain insights into the fund’s performance over different time horizons.

To maintain consistency and comparability, this paper excludes a small number of USD-denominated funds and money market funds from the analysis. Furthermore, this study focuses solely on actively managed equity funds, excluding other types of funds such as bond funds, balanced funds, fund of funds, and passive equity funds. This approach ensures that the analysis compares similar types of funds.

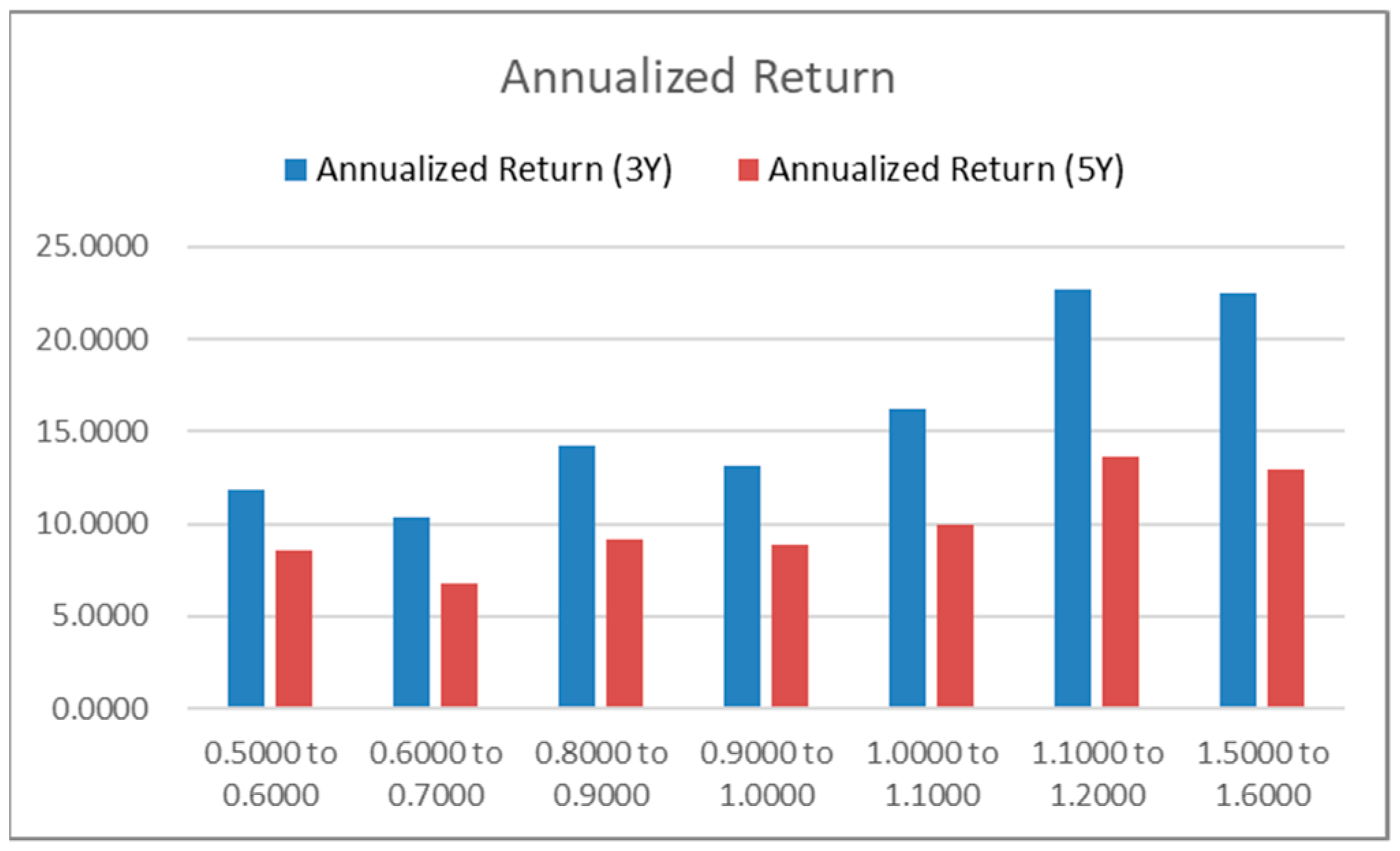

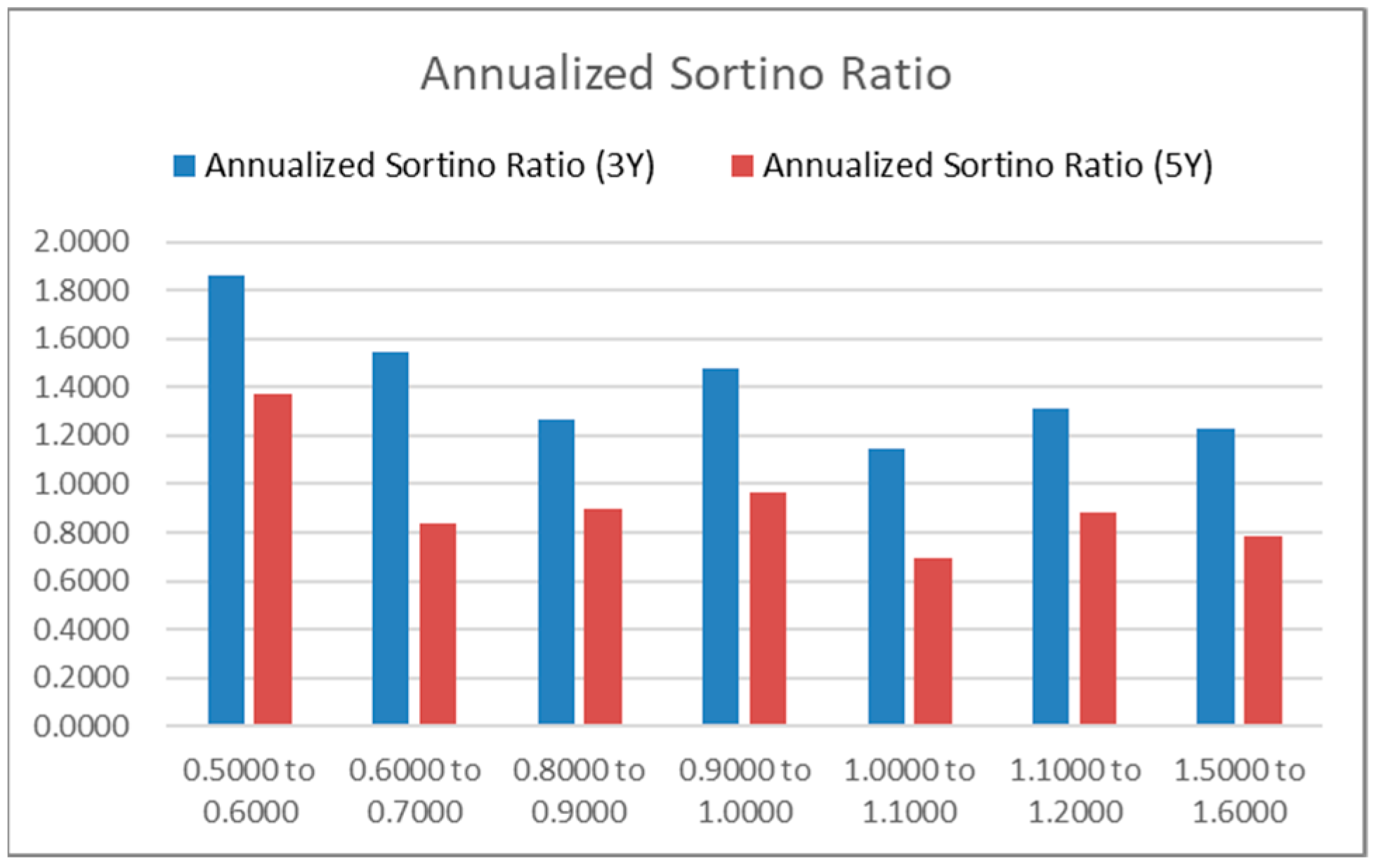

After applying these selection criteria, 1742 funds denominated in RMB are shortlisted for performance analysis. These funds are then divided into 30 groups based on their management fee levels. Each group represents a range of 0.1% management fee.

Table 1 presents the number of funds in each of the 30 management fee groups. Notably, the group charging a fee between 1.1% and 1.2% consists of 623 funds, accounting for 35.76% of the total funds. Similarly, there are 362 funds charging a fee between 1.5% and 1.6%, representing 20.78% of the total funds. It is worth mentioning that the management fees of open-end funds in China tend to be higher compared to those in the European and North American markets.

To ensure statistically robust comparisons, this paper further selects 7 management fee groups that each contain at least 30 funds. These groups are labeled as the “7 Groups” and are considered less susceptible to biases arising from small sample sizes. The sample size of the “7 Groups” is not significantly different from that of the “30 Groups”. The fund count for each management fee group is presented in

Table 1.

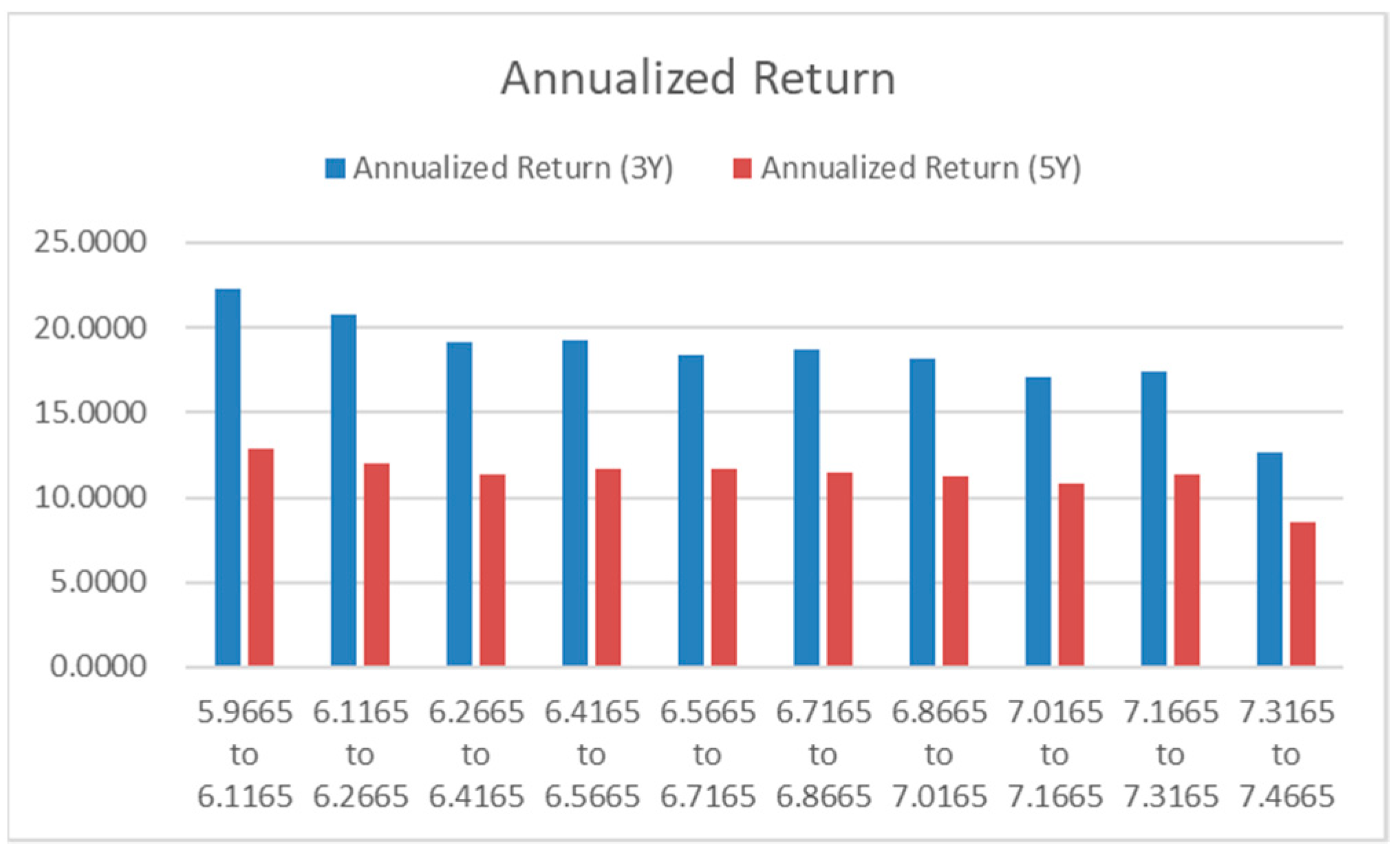

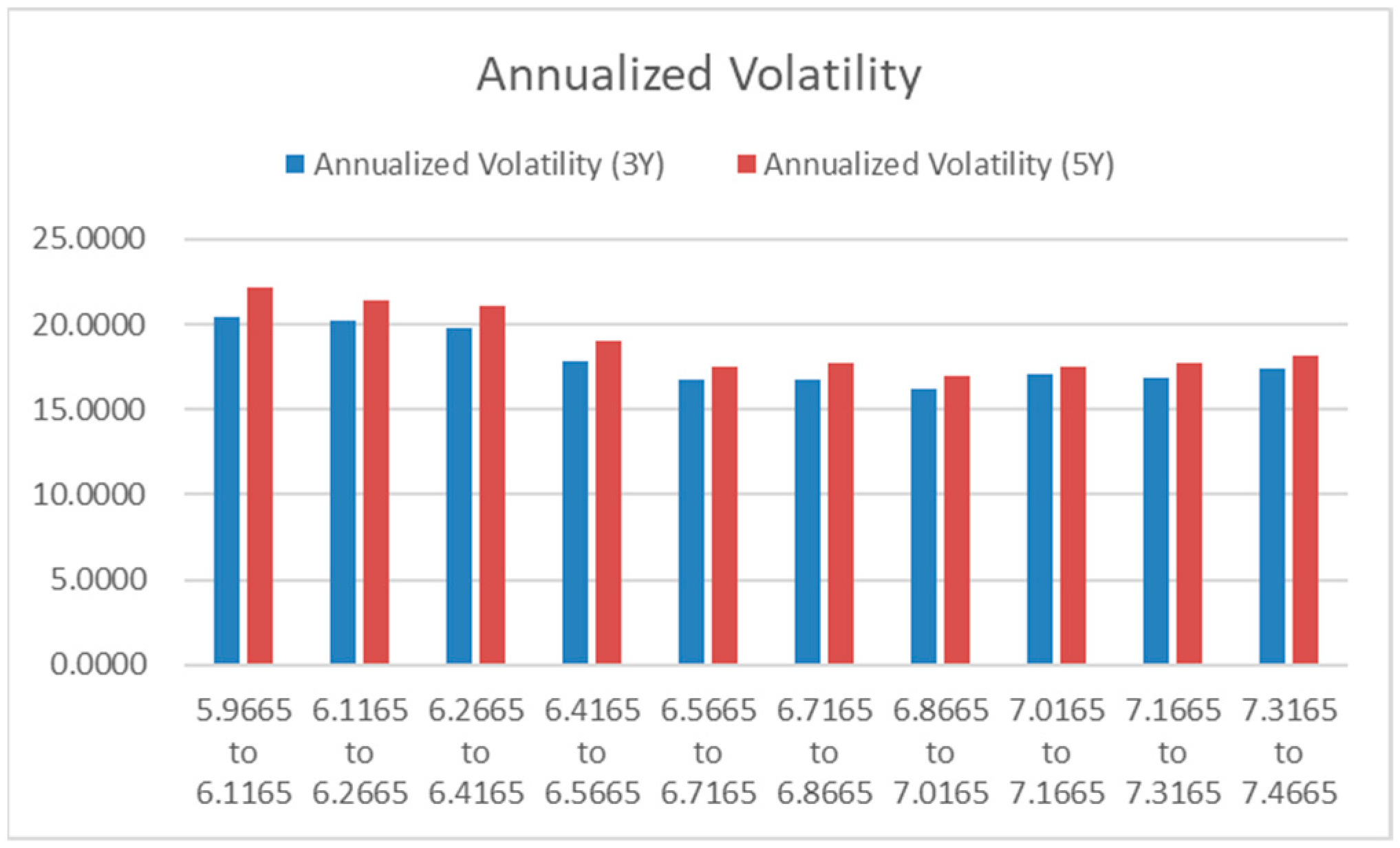

Similarly, this paper categorizes the 1742 funds into 22 groups based on their Wind ESG Comprehensive Score, as shown in

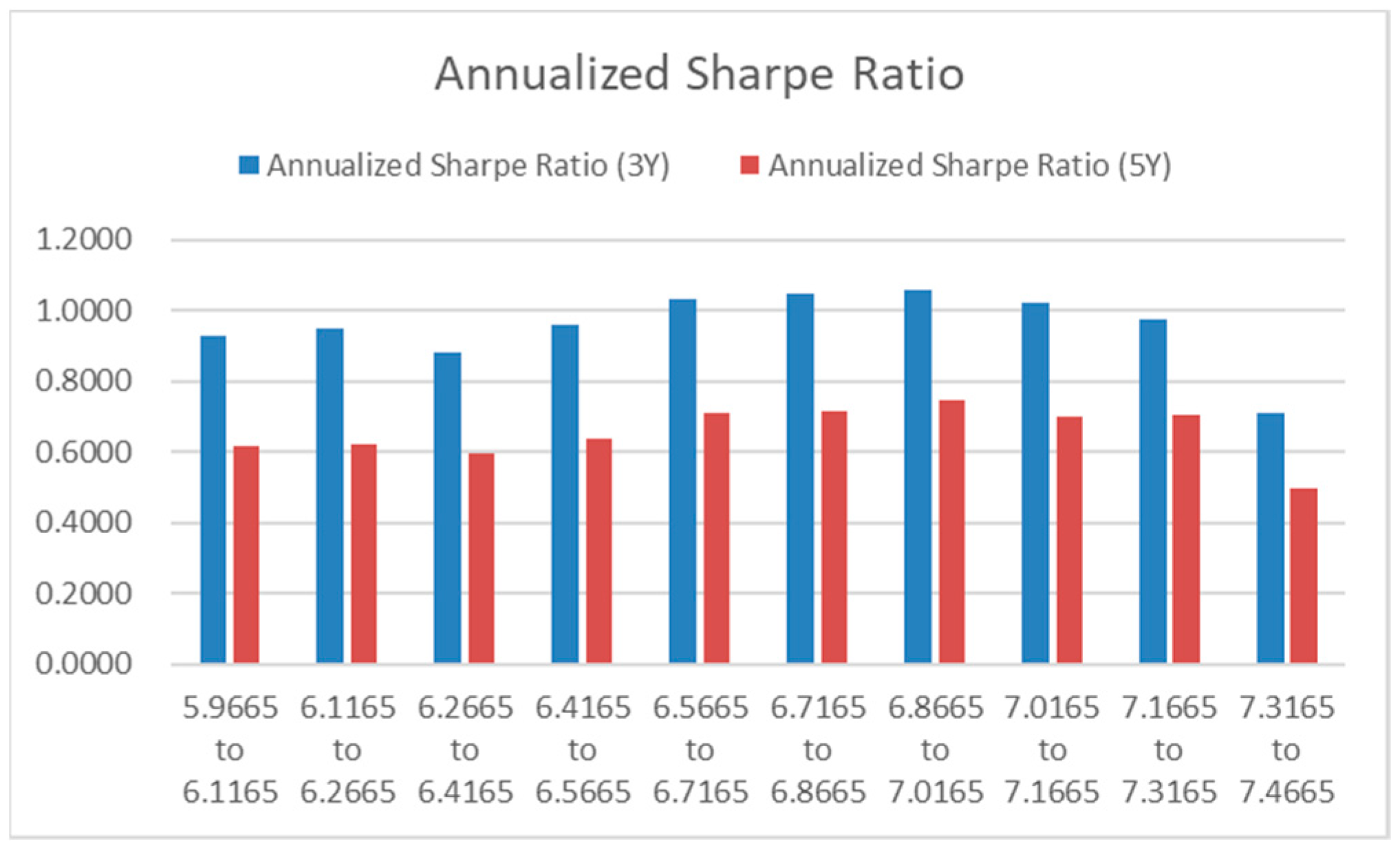

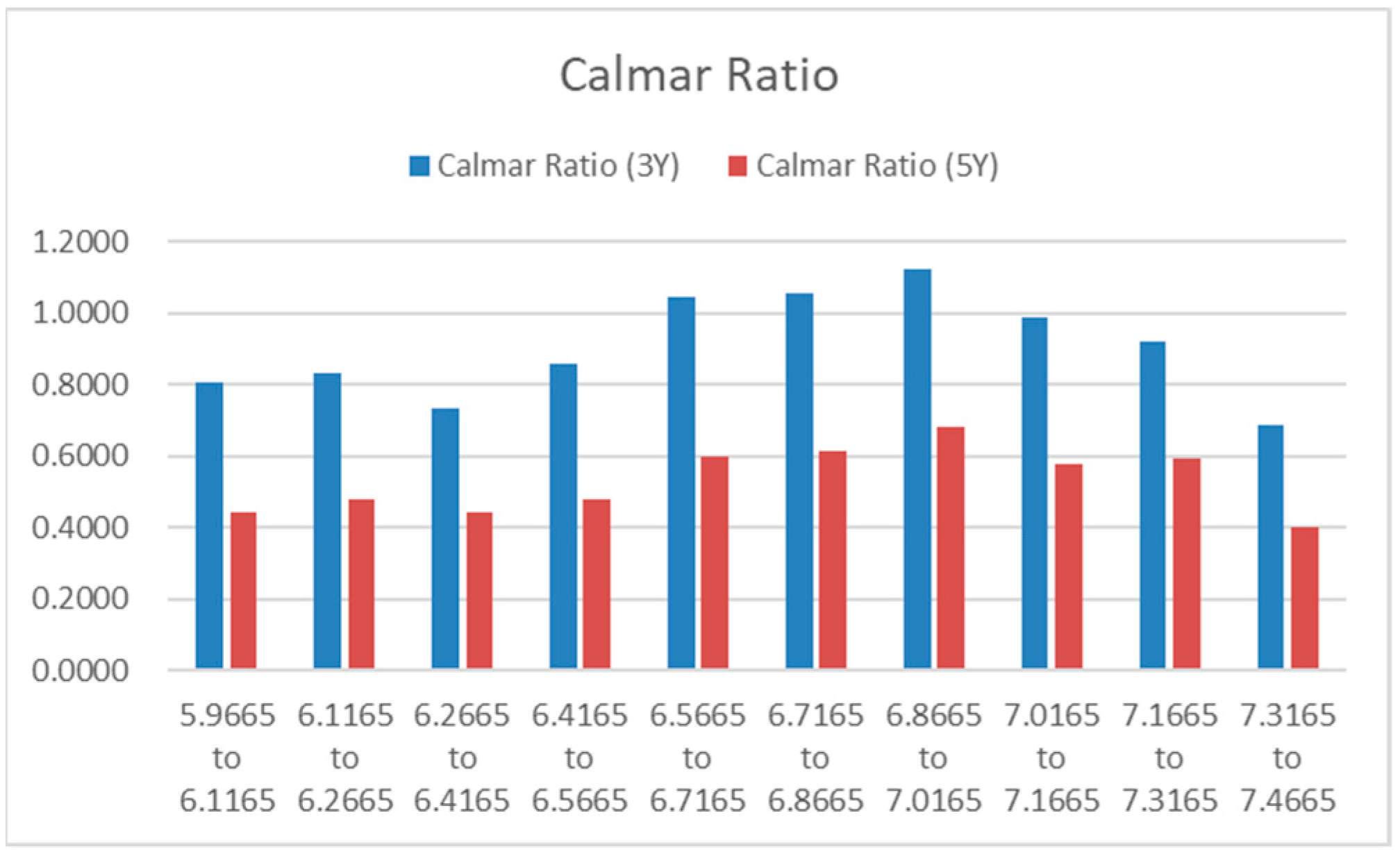

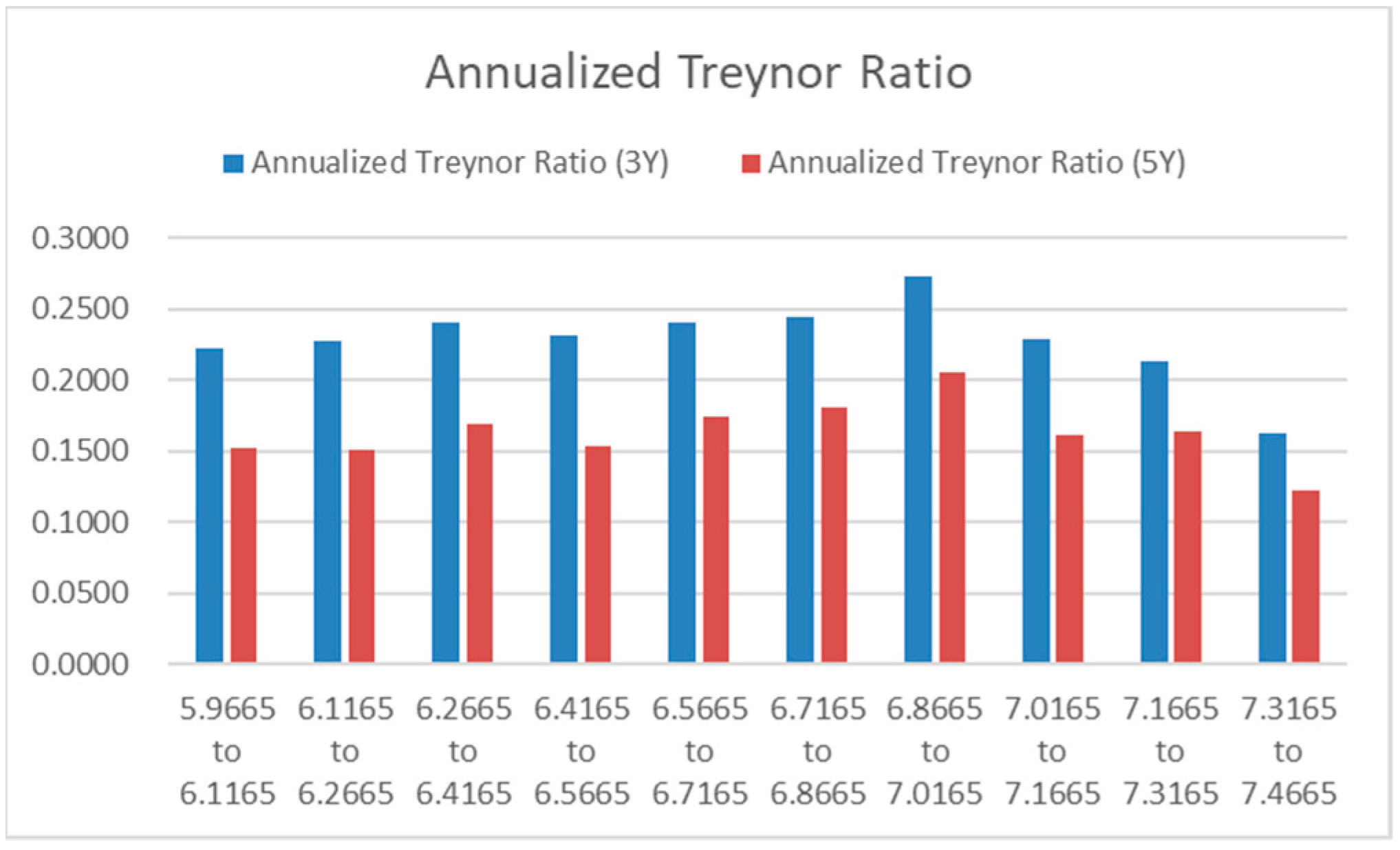

Table 2. This score evaluates companies across three pillars: Environmental, Social, and Governance. It encompasses 25 topics and over 300 underlying indicators, drawing from a vast range of reliable sources. The score, which ranges from 0 to 10, reflects the fund’s sustainable investment ability, the level of ESG management practice in its underlying investments, and the risk of short-term ESG controversies. The ESG score groups have an interval of 0.15. Notably, nearly half of the funds fall within the interval of 6.5665 to 7.0165. The minimum ESG score observed is 5.36, while the maximum is 8.02.

5. Summary and Conclusions

The investigation into the open-end equity funds of China, as presented within this document, highlights numerous pivotal discoveries. Primarily, it is observed that funds which impose higher management fees exhibit elevated returns, thereby implying that these fees may be substantiated by the superior returns bestowed by said funds. Nevertheless, these funds do not manifest superior performance in metrics adjusted to consider risk, indicating that the augmented fees do not result in enhanced performance once the risk level is considered. The analysis reveals that incorporating ESG factors adversely affects fund performance. The findings demonstrate that ESG funds do not impose higher management fees, do not assure superior returns, and yet frequently produce superior risk-adjusted investment performance if their ESG scores are moderately higher. Exceptionally high ESG scores can end up with the worst risk-adjusted investment performance.

These findings contribute to the comprehension of the correlation between management fees, fund performance, and the integration of environmental, social, and governance (ESG) considerations within the framework of China’s open-end equity funds. The outcomes imply that investors should meticulously assess the compromise between management fees and performance while selecting funds. This study emphasizes the significance of conducting additional research to explore the factors that influence fund performance and the role of ESG factors in the Chinese market.

In general, this research offers valuable perceptions for investors, fund managers, and policymakers in China’s fund management industry. The discoveries contribute to the ongoing discourse on the ideal fee structure and the integration of ESG factors in investment decisions, facilitating well-informed decision-making and potentially leading to enhanced performance and sustainable investment practices in the future.

5.1. Limitations of This Research

This study on management fees, ESG scores, and the investment performance of China funds has certain limitations that should be considered. Firstly, the reliance on data from a specific source, Wind Information, introduces the possibility of data inaccuracies and incompleteness, which may affect the generalizability of the findings. Secondly, this study’s period is limited, focusing on a specific period, and may not fully capture long-term trends and performance patterns.

5.2. Implications and Recommendation

The discoveries of this investigation have significant ramifications for various interested parties. To begin with, shareholders have the potential to reap the rewards of the knowledge provided, enabling them to make well-informed choices when putting their money into ESG funds in China. It is irrelevant to remark that ESG funds do not come with higher management fees or higher returns. Many investors who prioritize ESG factors place importance on achieving both social and financial gains. Therefore, they will be pleased to discover that ESG funds demonstrate superior risk-adjusted performance. This can be attributed to the possibility that the companies being invested in by the ESG funds have strong financial resources and a long-term vision for their business.

Furthermore, companies specializing in fund management can utilize the findings to establish appropriate management fees for their ESG funds. Additionally, they can utilize these observations to communicate with investors who are focused on ESG factors that investing in ESG funds could potentially lead to enhanced risk-adjusted performance while also contributing to societal well-being. Lastly, regulators can leverage this research to evaluate existing regulations pertaining to ESG funds in China, with the goal of promoting sustainable finance and responsible investing practices. Collaborative efforts between fund management companies and regulators are crucial in educating investors about ESG investing, fostering standardization and transparency in ESG metrics and reporting, and further advancing sustainable finance practices.

In conclusion, ongoing research in ESG investing is vital to its evolving nature and the dynamic relationship between management fees and investment performance. By promoting collaboration, education, and standardization, stakeholders can collectively contribute to the advancement of sustainable finance practices in China and beyond.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}