Disclosure of Key Audit Matters: European Listed Companies’ Evidence on Related Parties Transactions

Abstract

1. Introduction

2. Literature Review

2.1. Related Parties’ Transaction Reporting

2.2. Key Audit Matters Disclosure

3. Methodology

3.1. Data

3.2. Method

4. Results

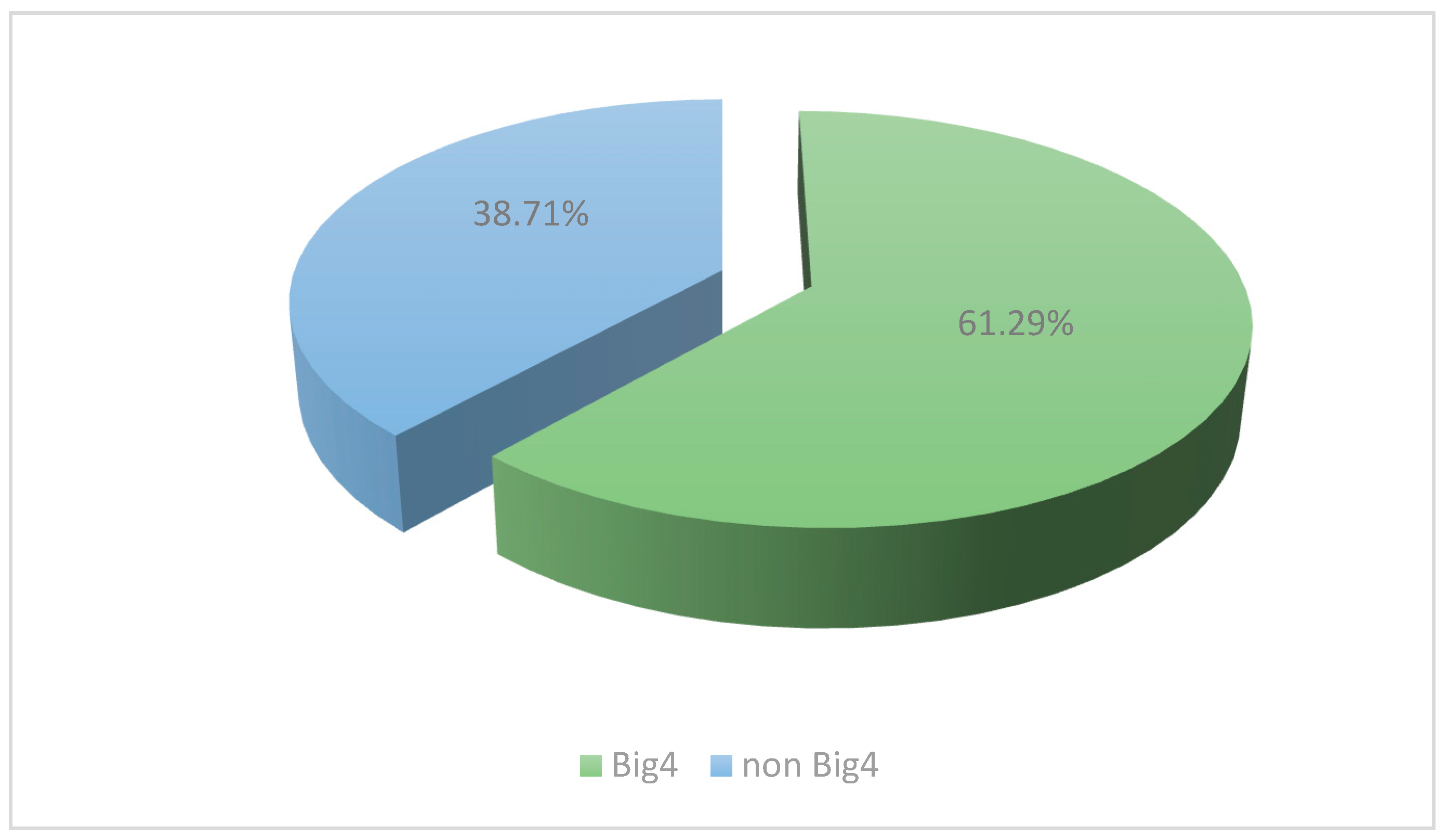

4.1. Type and Opinion of the Auditor

4.2. Audit Period

4.3. Geographical Distribution of the Companies

4.4. Fields of Activity

5. Discussion

6. Conclusions

Author Contributions

Funding

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Aharony, Joseph, Jiwei Wang, and Hongqi Yuan. 2010. Tunneling as an incentive for earnings management during the IPO process in China. Journal of Accounting and Public Policy 29: 1–26. [Google Scholar] [CrossRef]

- Al Lawati, Hidaya, and Khaled Hussainey. 2022. The Determinants and Impact of Key Audit Matters Disclosure in the Auditor’s Report. International Journal of Financial Studies 10: 107. [Google Scholar] [CrossRef]

- Audit Analytics. 2020. Monitoring the Audit Market in Europe. Available online: https://blog.auditanalytics.com/monitoring-the-audit-market-in-europe/ (accessed on 5 June 2023).

- Beasley, Mark, Joseph Carcello, Dana Hermanson, and Paul Lapides. 2000. Fraudulent financial reporting: Consideration of industry traits and corporate governance mechanisms. Accounting Horizons 14: 441–54. [Google Scholar] [CrossRef]

- Bodu, Sebastian. 2019. Piața de Capital. Legea nr. 24-2017 Privind Emitenții de Instrumente Financiare și Operașiuni de Piață–București. București: Rosetti. ISBN 978-606-025-007-4. [Google Scholar]

- Botes, Vida, Mary Low, and Aleena Sutton. 2020. Key audit matters and their implications for the audit environment. International Journal of Economics and Accounting 9: 374–96. [Google Scholar] [CrossRef]

- Camacho-Miñano, María-del-Mar, Nora Muñoz-Izquierdo, Morton Pincus, and Patricia Wellmeyer. 2023. Are key audit matter disclosures useful in assessing the financial distress level of a client firm? The British Accounting Review. [Google Scholar] [CrossRef]

- Cameran, Mara, and Domenico Campa. 2023. Key Audit Matters and Audit Outcomes: Evidence from the European Union. April 21. Available online: https://ssrn.com/abstract=4425465 (accessed on 5 June 2023).

- Căpăţână-Verdeş, Neli. 2019. Testing Compliance with IAS 24 fot Related Parties Listed on Bucharest Stock Exchange, in European Union Financial Regulation and Administrative Area: EUFIRE 2019; Edited by Mihaela Tofan, Irina Bilan and Elena Cigu. Iaşi: Editura Universităţii “Al. I. Cuza”, pp. 23–42. Available online: http://eufire.uaic.ro/wp-content/uploads/2019/08/EUFIRE_Conference_Proceeding2019.pdf (accessed on 10 November 2020).

- Cheung, Yan-Leung, Yuehua Qi, Raghavendra Rau, and Aris Stouraitis. 2009. Buy high, sell low: How listed firms price asset transfers in related party transactions. Journal of Banking & Finance 33: 914–24. [Google Scholar]

- Corlaciu, Alexandra, and Adriana Tiron-Tudor. 2013. Research on the Factors that Influence the Level of Related Party Disclosures as Required by ISA 24. Audit Financiar 11: 10–24. [Google Scholar]

- Crucean, Andreea Claudia, and Camelia-Daniela Hategan. 2023. Impact of Information Technology on Audit Quality: European Listed Companies’ Evidence. In Contemporary Studies of Risks in Emerging Technology, Part B. Bingley: Emerald Publishing Limited, pp. 327–39. [Google Scholar]

- Dang, Van Cuong, and Quang Khai Nguyen. 2021. Internal corporate governance and stock price crash risk: Evidence from Vietnam. Journal of Sustainable Finance & Investment, 1–18. [Google Scholar] [CrossRef]

- Dang, Van Cuong, and Quang Khai Nguyen. 2022. Audit committee characteristics and tax avoidance: Evidence from an emerging economy. Cogent Economics & Finance 10: 2023263. [Google Scholar]

- Ecim, Dusan, Warren Maroun, and Alain Duboisee de Ricquebourg. 2023. An analysis of key audit matter disclosures in South African audit reports from 2017 to 2020. South African Journal of Business Management 54: 3669. [Google Scholar] [CrossRef]

- El-Helaly, Moataz. 2018. Related-party transactions: A review of the regulation, governance and auditing literature. Managerial Auditing Journal 33: 779–806. [Google Scholar] [CrossRef]

- Epstein, Barry J., and Eva K. Jermakowicz. 2008. Chapter 23 Related-party disclosures. In Interpretation and Application of International Financial Reporting Standards. Hoboken: John Wiley & Sons Inc., pp. 852–63. [Google Scholar]

- Financial Accounting Standards Board. n.d. FAS 57 Related Parties’ Transactions. Available online: https://www.fasb.org/page/PageContent?pageId=/reference-library/superseded-standards/summary-of-statement-no-57.html&bcpath=tff (accessed on 31 March 2023).

- Gordon, Elisabeth A., Elain Henry, Timoty J. Louwers, and Brad J. Reed. 2007. Auditing related party transactions: A literature overview and research synthesis. Accounting Horizons 21: 81–102. [Google Scholar] [CrossRef]

- Grosu, Maria, Ioan-Bogdan Robu, and Costel Istrate. 2020. The Quality of Financial Audit Missions by Reporting the Key Audit Matters. Audit Financiar 18: 182–95. [Google Scholar] [CrossRef]

- Habib, Ahsan, Haiyan Jiang, and Donghua Zhou. 2015. Related-party transactions and audit fees: Evidence from China. Journal of International Accounting Research 14: 59–83. [Google Scholar] [CrossRef]

- Hategan, Camelia-Daniela, Ruxandra Ioana Pitorac, and Andreea Claudia Crucean. 2022. Impact of COVID-19 pandemic on auditors’ responsibility: Evidence from European listed companies on key audit matters. Managerial Auditing Journal 37: 886–907. [Google Scholar] [CrossRef]

- Hegazy, Mohamed Abdel Aziz, and Noha Mahmoud Kamareldawla. 2021. Key audit matters: Did IAASB unravel the knots of confusion in audit reports decisions? Managerial Auditing Journal 36: 1025–52. [Google Scholar] [CrossRef]

- Henry, Elain, Elisabeth A. Gordon, Brad Reed, and Thimoty J. Louwers. 2007. The Role of Related Party Transactions in Fraudulent Financial Reporting. Available online: https://ssrn.com/abstract=993532 (accessed on 5 June 2023).

- Huang, Derek-Teshun, and Zhien-Chia Liu. 2010. A study of the relationship between related party transactions and firm value in high technology firms in Taiwan and China. African Journal of Business Management 4: 1924. [Google Scholar]

- Iwanowicz, Tomasz, and Bartolomiej Iwanowicz. 2019. ISA 701 and Materiality Disclosure as Methods to Minimize the Audit Expectation Gap. Journal of Risk and Financial Management 12: 161. [Google Scholar] [CrossRef]

- Jensen, Michael C., and William H. Meckling. 1976. Theory of the firm. Managerial Behaviour, Agency Costs and Ownership Structure. Journal of Financial Economics 3: 305–60. [Google Scholar]

- Jian, Ming, and Tak J. Wong. 2010. Propping through related party transactions. Review of Accounting Studies 15: 70–105. [Google Scholar] [CrossRef]

- Jorgensen, Bjorn N., and Julia Morley. 2017. Discussion of “are related party transactions red flags?”. Contemporary Accounting Research 34: 929–39. [Google Scholar] [CrossRef]

- Kitiwong, Weerapong, and Naruanard Sarapaivanich. 2020. Consequences of the implementation of expanded audit reports with key audit matters (KAMs) on audit quality. Managerial Auditing Journal 35: 1095–119. [Google Scholar] [CrossRef]

- Kitiwong, Weerapong, and Sillapaporn Srijunpetch. 2019. Cultural influences on the disclosures of key audit matters. Journal of Accounting Profession 15: 45–63. [Google Scholar]

- Kohlbeck, Mark, and Brian W. Mayhew. 2017. Are related party transactions red flags? Contemporary Accounting Research 34: 900–28. [Google Scholar] [CrossRef]

- Liu, Hui, Jiaki Ning, Yue Zhang, and Junrui Zhang. 2022. Key audit matters and debt contracting: Evidence from China. Managerial Auditing Journal 37: 657–78. [Google Scholar] [CrossRef]

- OECD. 2022. Transfer Pricing Guidelines for Multinational Enterprises and Tax Administrations. Available online: https://www.oecd-ilibrary.org/taxation/oecd-transfer-pricing-guidelines-for-multinational-enterprises-and-tax-administrations-2022_0e655865-en (accessed on 31 March 2023).

- Özcan, Ahmet. 2021. What factors affect the disclosure of key audit matters? Evidence from manufacturing firms. International Journal of Management Economics and Business 17: 149–16. [Google Scholar] [CrossRef]

- Pinto, Ines, and Ana Isabel Morais. 2018. What matters in disclosures of key audit matters: Evidence from Europe. Journal of International Financial Management & Accounting 30: 145–62. [Google Scholar]

- Rautiainen, Antti, Jani Saastamoinen, and Kati Pajunen. 2021. Do key audit matters (KAMs) matter? Auditors’ perceptions of KAMs and audit quality in Finland. Managerial Auditing Journal 36: 386–404. [Google Scholar] [CrossRef]

- Rossing, Christian Plesner, Martine Cools, and Carsten Rohde. 2017. International transfer pricing in multinational enterprises. Journal of Accounting Education 39: 55–67. [Google Scholar] [CrossRef]

- Sikka, Prem, and Hugh Willmott. 2010. The dark side of transfer pricing: Its role in tax avoidance and wealth retentiveness. Critical Perspectives on Accounting 21: 342–56. [Google Scholar] [CrossRef]

- Sirois, Louis-Philippe, Jean Bédard, and Palash Bera. 2018. The informational value of key audit matters in the auditor’s report: Evidence from an eye-tracking study. Accounting Horizons 32: 141–62. [Google Scholar] [CrossRef]

- Sneller, Lineke, Ries Bode, and Arnoud Klerkx. 2017. Do IT matters matter? IT-related key audit matters in Dutch annual reports. International Journal of Disclosure and Governance 14: 139–51. [Google Scholar] [CrossRef]

- Suttipun, Muttanachai. 2021. Impact of key audit matters (KAMs) reporting on audit quality: Evidence from Thailand. Journal of Applied Accounting Research 22: 869–82. [Google Scholar] [CrossRef]

- Tong, Yan, Mingzhu Wang, and Feng Xu. 2014. Internal control, related party transactions and corporate value of enterprises directly controlled by Chinese central government. Journal of Chinese Management 1: 1–14. [Google Scholar] [CrossRef]

- Wallis, Mark, Matt Pinnuck, Amir Ghandar, and Zowie Pateman. 2022. Key Audit Matters. Insight 2022, Chartered Accountants Australia and New Zealand. Available online: https://www.charteredaccountantsanz.com/news-and-analysis/insights/research-and-insights/key-audit-matters-in-australia (accessed on 5 June 2023).

- Wang, Hong-Da, Chia-Ching Cho, and Chan-Jane Lin. 2019. Related party transactions, business relatedness, and firm performance. Journal of Business Research 101: 411–25. [Google Scholar] [CrossRef]

{kind=link}

| Big4 | Total nr. of KAM | Percent |

|---|---|---|

| Deloitte & Touche LLP | 24 | 15.79% |

| Ernst & Young LLP | 69 | 45.39% |

| KPMG LLP | 24 | 15.79% |

| PricewaterhouseCoopers LLP | 35 | 23.03% |

| Total | 152 | 100% |

| Non Big4 | Total nr. of KAM | Percent |

|---|---|---|

| Baker Tilly | 8 | 9% |

| BDO | 8 | 9% |

| Crowe UK LLP | 4 | 4% |

| ECOVIS | 2 | 2% |

| Elderton Audit UK | 1 | 1% |

| Grant Thornton LLP | 7 | 7% |

| Hazlewoods LLP | 5 | 5% |

| HW Fisher & Company | 2 | 2% |

| Lohr + Company GmbH | 2 | 2% |

| Mazars | 3 | 3% |

| MHA MacIntyre Hudson | 5 | 5% |

| MJ Abedin & Co. | 3 | 3% |

| Moore Stephens LLP (UK) | 1 | 1% |

| Nexia Smith & Williamson Audit Limited | 2 | 2% |

| RMT Accountants & Business Advisors Ltd. | 3 | 3% |

| Rodl & Partner GmbH | 3 | 3% |

| RSM UK Audit LLP | 2 | 2% |

| Saffery Champness LLP | 1 | 1% |

| Shipleys LLP | 19 | 20% |

| SIA Potapovica un Andersone | 3 | 3% |

| UAB Audito sprendimai | 4 | 4% |

| Welbeck Associates | 8 | 9% |

| Total | 96 | 100% |

| Elderton Audit UK | 1 |

| Moore Stephens LLP (UK) | |

| Saffery Champness LLP | |

| ECOVIS | 2 |

| HW Fisher & Company | |

| Lohr + Company GmbH | |

| Nexia Smith & Williamson Audit Limited | |

| RSM UK Audit LLP | |

| Mazars | 3 |

| MJ Abedin & Co. | |

| RMT Accountants & Business Advisors Ltd. | |

| Rodl & Partner GmbH | |

| SIA Potapovica un Andersone | |

| Crowe UK LLP | 4 |

| UAB Audito sprendimai | |

| Grant Thornton LLP | 5 |

| Hazlewoods LLP | |

| MHA MacIntyre Hudson | |

| Baker Tilly | 8 |

| BDO | |

| Welbeck Associates | |

| Shipleys LLP | 19 |

| Year | Number of KAM | Percent |

|---|---|---|

| 2013 | 9 | 1.94% |

| 2014 | 15 | 5.16% |

| 2015 | 10 | 5.81% |

| 2016 | 22 | 13.76% |

| 2017 | 41 | 18.92% |

| 2018 | 48 | 19.14% |

| 2019 | 36 | 17.63% |

| 2020 | 36 | 16.34% |

| 2021 | 29 | 1.29% |

| Total | 248 | 100% |

| Nr. | Country | No. of KAMs | Percent | Big4 | Non Big4 |

|---|---|---|---|---|---|

| 1 | Australia | 2 | 0.81% | 0 | 2 |

| 2 | Bangladesh | 3 | 1.21% | 0 | 3 |

| 3 | Belgium | 5 | 2.02% | 4 | 1 |

| 4 | Bermuda | 9 | 3.63% | 5 | 4 |

| 5 | Bulgaria | 3 | 1.21% | 3 | 0 |

| 6 | Cayman Islands | 4 | 1.61% | 0 | 4 |

| 7 | China | 3 | 1.21% | 0 | 3 |

| 8 | Cyprus | 3 | 1.21% | 3 | 0 |

| 9 | Finland | 4 | 1.61% | 4 | 0 |

| 10 | France | 10 | 4.03% | 8 | 2 |

| 11 | Germany | 11 | 4.44% | 6 | 5 |

| 12 | Greece | 3 | 1.21% | 2 | 1 |

| 13 | Guernsey | 7 | 2.82% | 3 | 4 |

| 14 | Ireland | 9 | 3.63% | 9 | 0 |

| 15 | Isle of Man | 11 | 4.44% | 6 | 5 |

| 16 | Italy | 6 | 2.44% | 6 | 0 |

| 17 | Jersey | 1 | 0.41% | 1 | 0 |

| 18 | Latvia | 3 | 1.22% | 0 | 3 |

| 19 | Lithuania | 4 | 1.63% | 0 | 4 |

| 20 | Luxembourg | 4 | 1.63% | 4 | 0 |

| 21 | Malta | 2 | 0.81% | 1 | 1 |

| 22 | Mauritius | 1 | 0.41% | 1 | 0 |

| 23 | Netherlands | 7 | 2.85% | 7 | 0 |

| 24 | Norway | 5 | 2.03% | 5 | 0 |

| 25 | Poland | 5 | 2.03% | 5 | 0 |

| 26 | Russian Federation | 1 | 0.41% | 1 | 0 |

| 27 | Spain | 2 | 0.81% | 2 | 0 |

| 28 | Sweden | 8 | 3.25% | 6 | 2 |

| 29 | Switzerland | 6 | 2.44% | 4 | 2 |

| 30 | United Kingdom | 105 | 42.34% | 55 | 50 |

| 31 | United States | 1 | 0.40% | 1 | 0 |

| Total | 248 | 100.00% | 152 | 96 |

| SIC Code | Industry | Number of KAM | Percentage of KAM |

|---|---|---|---|

| 0 | Agriculture, Forestry, Fishing | 2 | 0.81% |

| 1 | Mining, construction | 51 | 20.56% |

| 2 | Production–Groups 20–29 | 27 | 10.89% |

| 3 | Production–Groups 30–39 | 27 | 10.89% |

| 4 | Transport, communications, electrical, gas and plumbing services | 14 | 8.82% |

| 5 | Wholesale and retail trade | 14 | 8.82% |

| 6 | Finance, insurance and real estate | 81 | 32.66% |

| 7 | Services–Groups 70–79 | 19 | 7.66% |

| 8 | Services–Groups 80–89 | 13 | 5.24% |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Pasc, L.-V.; Hategan, C.-D. Disclosure of Key Audit Matters: European Listed Companies’ Evidence on Related Parties Transactions. Int. J. Financial Stud. 2023, 11, 82. https://doi.org/10.3390/ijfs11030082

Pasc L-V, Hategan C-D. Disclosure of Key Audit Matters: European Listed Companies’ Evidence on Related Parties Transactions. International Journal of Financial Studies. 2023; 11(3):82. https://doi.org/10.3390/ijfs11030082

Chicago/Turabian StylePasc, Lioara-Veronica, and Camelia-Daniela Hategan. 2023. "Disclosure of Key Audit Matters: European Listed Companies’ Evidence on Related Parties Transactions" International Journal of Financial Studies 11, no. 3: 82. https://doi.org/10.3390/ijfs11030082

APA StylePasc, L.-V., & Hategan, C.-D. (2023). Disclosure of Key Audit Matters: European Listed Companies’ Evidence on Related Parties Transactions. International Journal of Financial Studies, 11(3), 82. https://doi.org/10.3390/ijfs11030082