Risk-Oriented Efficiency Assessment within the Level of Capitalization for Financial Institutions: Evidence from Turkish Securities Firms

Abstract

1. Introduction

2. Literature Review

2.1. Relevant Literature on Securities Firms’ Efficiency

2.2. Relevant Literature of Banks’ Risk, Efficiency, and Capital

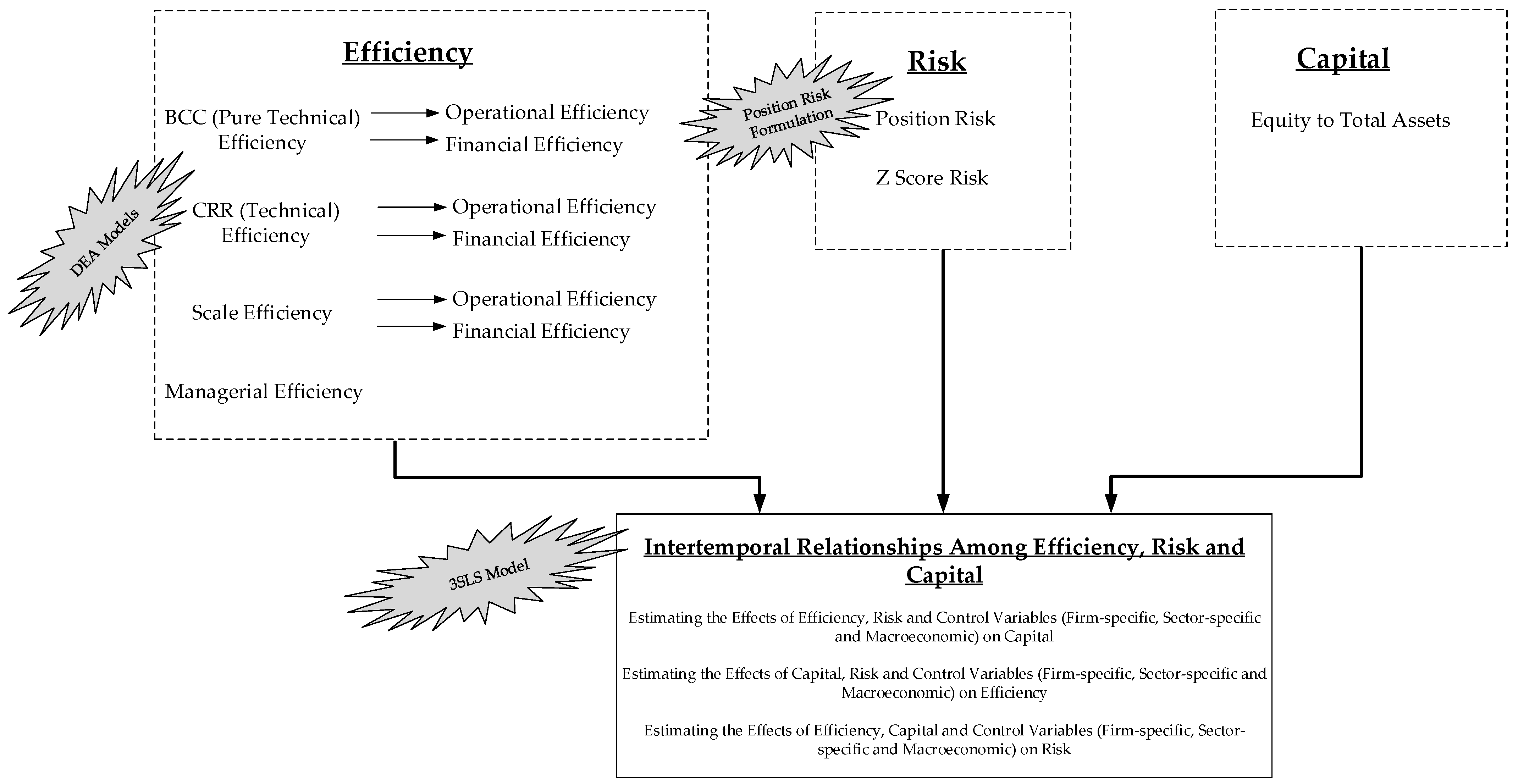

3. Data and Methodological Framework

3.1. Data Description

3.2. Measuring Efficiency of Securities Firms

- Capital: The capital was determined as the first input item. Capital has been used as an input both in measuring banks’ efficiency (see Mamatzakis and Bermpei 2014; Tan and Floros 2013; Lee and Chih 2013; Coelli et al. 2005) and brokerage firms’ efficiency (see Wang et al. 2003; Aktas and Kargin 2007; Zhang et al. 2006; Demirbag et al. 2016).

- Operating Expense: Operating expense is another input item that also was widely used in previous studies (see Zhang et al. 2006; Mamatzakis and Bermpei 2014; Tan and Floros 2013; Delis et al. 2014; Wild 2016; Van Anh 2022).

- Brokerage Revenue: Given the nature of brokerage firms, we defined brokerage revenues as the first output item. As mentioned previously, the most important source of income for brokerage firms is brokerage revenues, which provide for the purchase and sale of capital market instruments on behalf of their customers.

- Other Operating Revenue: Other operating revenue included corporate finance, asset management, and income from credit transactions as another output item These revenues were not classified individually, as done by Zhang et al. (2006), because they differed significantly between institutions, and each was not an important source of income.

- Revenue from Proprietary Trading (market-making activities): The final output item included the net revenues that institutions obtained from their own portfolios; namely, proprietary trading. In addition to capital market instruments such as equities, fixed income, and derivative transactions, the income from deposits, repos, reverse repos, Takasbank Money Market, etc. was combined and classified as the final output item. Firms in non-financial sectors generally generated financial income by evaluating excess cash in deposits or other products, while brokerage firms could generate income from arbitrage transactions by borrowing and investing in accordance with market conditions in addition to using cash surplus.

- Capital: As in the first alternative model.

- Labor: As the personnel expenses were used as input, in the previous alternative, the number of employees represented was determined as the input item in this approach. Indeed, the number of employees has been widely used in both banking (see Fiordelisi et al. 2011; Sealey and Lindley 1977; Hughes and Mester 1998 and brokerage activity Hu and Fang 2010).

- Branch Network: In addition to capital, the branch network was added as physical capital. The reason behind a preference for the branch network was that bank-affiliated brokerage firms can use the parent bank branches, which are effective in a much wider area as agents. In this way, these institutions create significant transaction volume at these branches as well as their own branches opened with their own capital.

- Trading Volume: Similar to Aktas and Kargin (2007), the total transaction volume was selected.

- Activities Other Than Brokerage Activities: The activities of brokerage firms other than brokerage were also taken into consideration; the size of the managed assets, the loan volume given to customers for stock transactions, and the size of the public offering brokerage were used.

3.3. Measuring Risk of Securities Firms

3.4. Measuring the Relationship of Risk, Capital, and Efficiency

3.5. Control Variables

- “Firm size” was proxied by a natural logarithm of the total assets (see Guillén et al. 2014; Chiaramonte et al. 2015; Fiordelisi et al. 2011).

- “Growth” proxied by asset growth.

- “Business model” was approximated by the ratio of non-brokerage income3 to total income in order to capture the income diversification (as in recent studies such as Tan and Floros 2013; Barth et al. 2013; Fiordelisi et al. 2011; Mateev et al. 2022).

- “Profitability” was substituted with return on equity (Lepetit and Strobel 2013; Wild 2016; Hu and Yu 2015; etc.).

- Income per staff (see Chiaramonte et al. 2015; Delis et al. 2014) was replaced by labor profitability.

- We also examined the impact of qualified employees on the efficiency using the qualified employee ratio. We defined qualified employees in the departments requiring license and qualifications; namely, research, corporate finance, international marketing, and treasury departments. The ratio represented the number of staff in those departments to the total number of employees.

- “Market design” by using the Herfindahl–Hirschman Index (HHI) (see Tan and Floros 2013; Boyd et al. 2006; Mare et al. 2017; Saeed and Izzeldin 2016). As the brokerage was the core services of these firms, trading volume was used for the HHI calculation.

- Market size was defined as the natural logarithm of the total market capitalization of the exchange as in Fiordelisi et al. (2011).

- Annual inflation rate and GDP growth were used as in earlier studies (see Lepetit and Strobel 2013; Dong et al. 2017; Bitar et al. 2018; etc.)

3.6. Summary of Methodological Framework

4. Results and Discussion

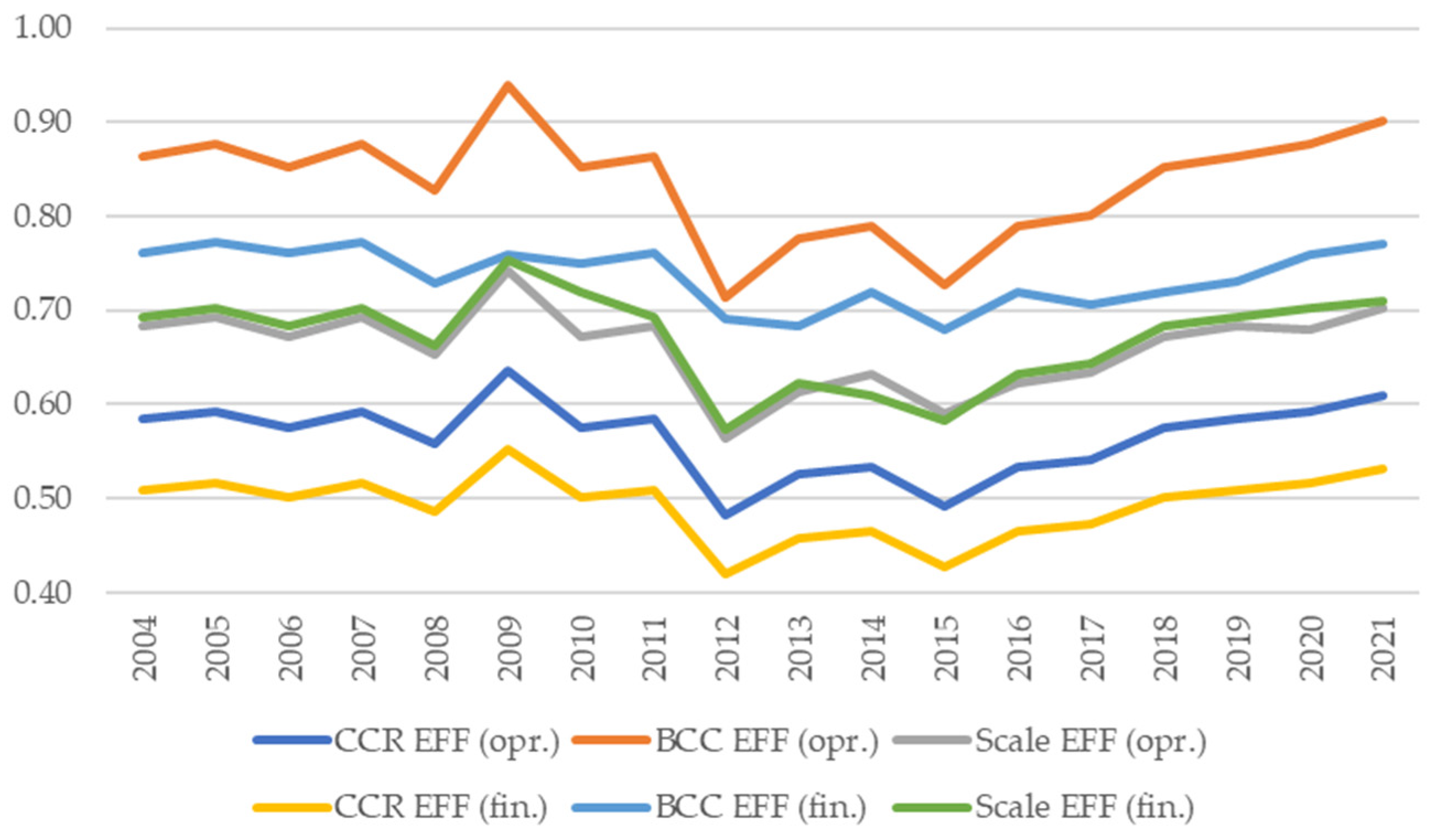

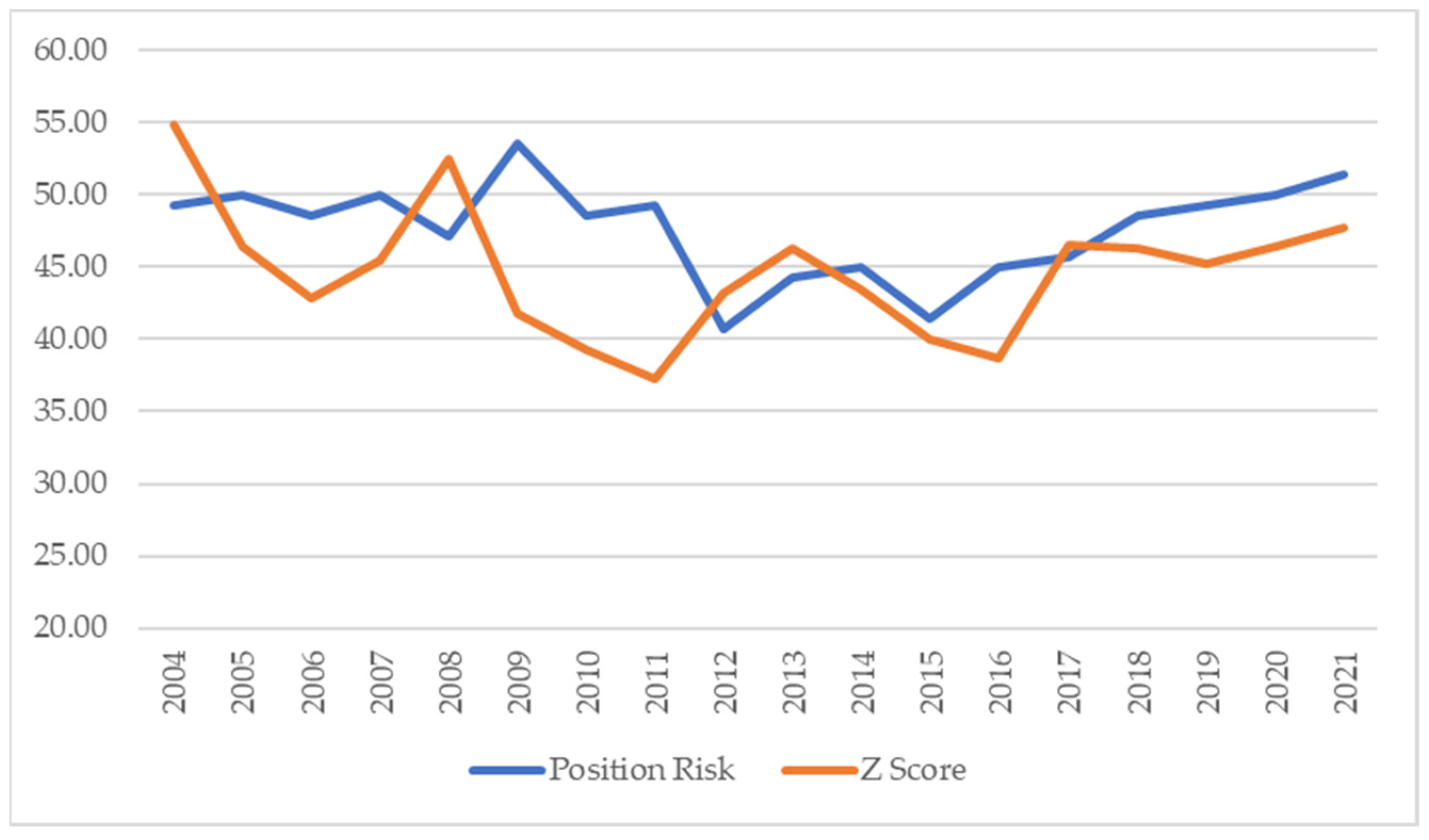

4.1. Results of the Efficiency and Risk Analyses

4.2. Results for the Relationships of Risk, Capital, and Efficiency

- Estimating the effects of position risk on operational efficiency: The position risk had a significant and positive relationship with the operational efficiency. The findings suggested that the securities firms with higher position risks required a higher trading volume, proprietary trading, and margin trading, which were output for the operating efficiency.

- Estimating the effects of capital on operational efficiency: The level of the capital-to asset-ratio and the operational efficiency were positively related, but the coefficient was negligible.

- Estimating the effects of control variables on operational efficiency: The income diversification and qualified employee coefficients indicated that they had significant effect on the operational efficiency of a firm. When considering the output of operational efficiency, the more varied activities (brokerage, corporate finance, and margin trading) were associated with more diversified revenue. In addition, if a firm wants to engage in different activities given the level of capital, it needs further licensed market professionals (namely, a higher qualified-person ratio).

- Estimating the effect of the operational efficiency’s on the position risk: The firms with higher position risk in their portfolio, operate more efficiently. As operational efficiency is relevant with wide range of activities, this result implies that the firms can engage in more business areas with more diversified portfolio.

- Estimating the effect of the level of capitalization on the position risk: We can further report that there was also positive and significant relationship between the position risk and capital. In the context of the Turkish brokerage industry, this finding can be explained by the fact that firms with higher levels of capital were more capable of proprietary trading (with more risk assets), which increased their position risk. Moreover, the firms with more risk-weighted assets required more capital to compensate for potential loses.

- Estimating the effect of control variables on the position risk: It was interesting to note that the results showed that there was a positive relationship between qualified persons and the position risk. This was mainly explained by engaging in risky and arbitrary proprietary transactions (e.g., derivatives and leveraged trading), which required qualified employees. Unsurprisingly, another significant piece of evidence was that the position risk and the asset size had a positive relationship.

- Estimating the effect of the operational efficiency on the level of capitalization: The findings suggested that there was no evidence of an association between capital and the operational efficiency.

- Estimating the effect of the position risk on the level of capitalization: The position risk had a positive effect on the capital, which can be interpreted as a higher position risk requiring additional capital due to market conditions.

- Estimating the effect of the control variables on the level of capitalization: The size and growth of assets showed positive and significant relationships with the capitalization level, as expected. Income diversification also had a positive and significant relation with capital. Firms with a higher capitalization could engage in more varied activities. It is worth noting that there was no significant relation between capital and the ROE.

- Estimating the effects of the Z-score on the operational efficiency: There was a negative and significant relationship between the Z-score and the efficiency. The firms that operated more efficiently had higher Z-scores, which meant lower risk. This result implied that a firm with an optimal and efficient labor and branch network structure had a lower probability of distress. These findings were accordance with those of Tan and Floros (2013); Mamatzakis and Bermpei (2014), and Dong et al. (2017).

- Estimating the effects of the operational efficiency on the Z-score: The Z-score and capital were positively related, but the coefficient in the position risk was much higher.

- Estimating the effects of capital on the Z-score: Capital and the Z-score were positively related, which signified that the probability of insolvency was reduced by the capital, as expected.

- Estimating the effects of the control variables on the position risk: It was interesting note that the asset size also had a significant and negative relationship with the Z-score. The firms with a higher amount of assets were in the lower upper bound of insolvency risk.

5. Conclusions

- In general, our results showed that there was a significant and positive relationship between a firm’s risk incentive (in terms of the risk-weighted assets ratio) and the technical, pure, and scale efficiencies.

- The level of capitalization had a positive relationship with the risk incentive; this relationship was negative when the risk indicator was the Z-score (which is widely used as a proxy of firm distress). The firms that operated more efficiently had a higher Z-score, which implied that a firm with an optimal and efficient labor and branch network structure had a lower probability of distress.

- The level of capital and the efficiency were positively related, but the coefficient was negligible in each alternative model.

- In terms of the control variables, market capitalization also had a significant and positive effect on a brokerage firm’s productivity in Turkish capital markets. The estimates implied that when the concentration ratio rose, the securities industry showed a decrease in technical efficiency (with both financial and operational variables). These results indicated that firms had less incentive to enhance efficiency when the industry became more concentrated.

- Performance and efficiency at the unit level has become a contemporary major issue for regulators that aids in the identification of significant inefficiency. This analysis may guide the regulator when new structural changes are required for regulators.

- A risk-based efficiency analysis with a wide range of control variables will be a useful tool for policymakers, especially for minimum capital requirements.

- As in other sectors, a clear efficiency assessment in the sector will also support shareholders in positioning themselves in the sector and determining their strategies.

- The calculation of the position risk and efficiency score using a publicly available dataset allows securities firms to compare and position themselves with peer groups.

- Firms can benefit from the relationships between efficiency and the control variables in the model (firms and sector- or macroeconomic-specific variables) while conducting a scenario analysis, even for strategies during changing market and economic conditions.

- As the study was data-sensitive, maintaining the data in a precise and up-to-date manner affects the consistency of such studies. This fact emphasized the importance of data management in the securities industry. Such works require a statistical background for practitioners. In this context, it is important to support the practitioners and managers who provide such analyses for securities firms and the statistical information infrastructures with training and practices.

- Last but not least, when considering the recent policy framework of banking regulations globally, e.g., the USA’s Volcker Rule or the UK’s ring-fencing of deposits, securities firms will become more remarkable; our findings offer valuable insight into how to better structure this industry.

Author Contributions

Funding

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

| 1 | Table 2 gives a brief review of prior studies. |

| 2 | |

| 3 | In Turkey, the main activity of securities firms is brokerage services. More than half of their revenue comes from such services. Market making, corporate finance, and asset management are ancillary services. |

| 4 | We checked for multicollinearity issues by computing the variance inflation factor (VIF) given in Table 7, the highest value of which was about 1.49; the mean was approximately 1.2. |

| 5 | The estimates of each model are available upon request from the authors. |

References

- Aktas, Huseyin, and Mamhmut Kargin. 2007. Efficiency and productivity of brokerage houses in Turkish capital market. Iktisat Isletme ve Finans 22: 97. [Google Scholar]

- Allen, Linda, and Anoop Rai. 1996. Operational efficiency in banking: An international comparison. Journal of Banking and Finance 20: 655–72. [Google Scholar] [CrossRef]

- Altman, Edward I. 1968. Financial ratios, discriminant analysis and the prediction of corporate bankruptcy. The Journal of Finance 23: 589–609. [Google Scholar] [CrossRef]

- Altunbas, Yener, Santiago Carbo, Edward P. M. Gardener, and Philip Molyneux. 2007. Examining the relationships between capital, risk and efficiency in European banking. European Financial Management 13: 49–70. [Google Scholar] [CrossRef]

- Aysan, A. F., and Ş. P. Ceyhan. 2008. What determines the banking sector performance in globalized financial markets? The case of Turkey. Physica A 387: 1593–602. [Google Scholar] [CrossRef]

- Azad, Abdul Kalam, Susila Munisamy, Abdul Kadar Muhammed Masum, and Paolo Saona. 2017. Bank efficiency in Malaysia: A use of malmquist meta-frontier analysis. Eurasian Business Review 7: 287–311. [Google Scholar] [CrossRef]

- Banker, Rajiv D., Abraham Charnes, and William Wager Cooper. 1984. Some models for estimating technical and scale inefficiencies in Data Envelopment Analysis. Management Science 30: 1078–92. [Google Scholar] [CrossRef]

- Barth, James, Chen Lin, Yue Ma, Jesús Seade, and Frank Song. 2013. Do Bank Regulation, Supervision and Monitoring Enhance or Impede Bank Efficiency? Journal of Banking & Finance 37: 2879–92. [Google Scholar]

- Bayyurt, Nizamettin, and Ahmet Akın. 2014. Effects of foreign acquisitions on the performance of securities firms: Evidence from Turkey. Procedia—Social and Behavioral Sciences 150: 156–61. [Google Scholar] [CrossRef][Green Version]

- Beccalli, Elena. 2004. Cross-country comparisons of efficiency: Evidence from the UK and Italian investment firms. Journal of Banking and Finance 28: 1363–83. [Google Scholar] [CrossRef]

- Berger, Allen N., and Robert De Young. 1997. Problem loans and cost efficiency in commercial banking. Journal of Banking and Finance 21: 849–70. [Google Scholar] [CrossRef]

- Bitar, Mohammad, Kuntara Pukthuanthong, and Thomas Walker. 2018. The effect of capital ratios on the risk, efficiency and profitability of banks: Evidence from OECD countries. Journal of International Financial Markets, Institutions and Money 53: 227–62. [Google Scholar] [CrossRef]

- Boyd, John, and David Runkle. 1993. Size and performance of banking firms: Testing the predictions of theory. Journal of Monetary Economics 31: 47–67. [Google Scholar] [CrossRef]

- Boyd, John, Mr Gianni De Nicoló, and Abu Jalal. 2006. Bank Risk-Taking and Competition Revisited: New Theory and New Evidence. International Monetary Fund Working Paper, N. 297. Washington, DC: International Monetary Fund. [Google Scholar]

- Charnes, Abraham, William Wager Cooper, and Edwardo Rhodes. 1978. Measuring the efficiency of decision making units. European Journal of Operational Research 3: 429–44. [Google Scholar] [CrossRef]

- Chen, Shaw K., Xuanjuan Chen, Bing-Xuan Lin, and Rongsa Zhong. 2005. The impact of government regulation and ownership on the performance of securities companies: Evidences from China. Global Finance Journal 16: 113–24. [Google Scholar] [CrossRef]

- Chen, X., and Z. Chen. 2000. The prediction of Chian listed company’s financial dilemma. China Accounting Financial Review 3: 55–92. [Google Scholar]

- Chiaramonte, Laura, Ettore Croci, and Federica Poli. 2015. Should we trust the Z-score? Evidence from the European Banking Industry. Global Finance Journal 28: 111–31. [Google Scholar] [CrossRef]

- Coelli, Timothy, Dodla Sai Prasada Rao, Christopher J. O’Donnell, and George Edward Battese. 2005. An Introduction to Efficiency and Productivity Analysis, 2nd ed. New York: Springer. ISBN 978-0-7923-8062-7. [Google Scholar]

- Dahiyat, Ahmet. 2012. The Application of CAMELS Rating System to Jordanian Brokerage Firms. International Research Journal of Finance and Economics 88: 16–23. [Google Scholar]

- Delis, Manthos D., Iftekhar Hasan, and Efthymios G. Tsionas. 2014. The risk of financial intermediaries. Journal of Banking & Finance 44: 1–12. [Google Scholar]

- Demir, Nazmi, Syed F. Mahmud, and Senol Babuscu. 2005. The technical inefficiency effects of Turkish banks after financial liberalization. The Developing Economimes 43: 396–411. [Google Scholar] [CrossRef]

- Demirbag, Mehmet, McGuinness Martina, Akın Ahmet, Bayyurt Nizamettin, and Basti Eyup. 2016. The professional service firm (PSF) in a globalised economy: A study of the efficiency ofsecurities firms in an emerging market. International Business Review 25: 1089–102. [Google Scholar] [CrossRef]

- Dong, Yizhe, Claudia Girardone, and Jing-Ming Kuo. 2017. Governance, efficiency and risk taking in Chinese banking. The British Accounting Review 49: 211–29. [Google Scholar] [CrossRef]

- Dyson, Robert G., and Emmanuel Thanassoulis. 1988. Reducing Weight Flexibility in Data Envelopment Analysis. Journal of the Operational Research Society 39: 563–76. [Google Scholar] [CrossRef]

- Fiordelisi, Franco, David Marques-Ibanez, and Phil Molyneux. 2011. Efficiency and risk in European banking. Journal of Banking and Finance 35: 1315–26. [Google Scholar] [CrossRef]

- Fukuyama, Hirofumi, and Roman Matousek. 2011. Efficiency of Turkish banking: Two-stage network system. Variable returns to scale model. Journal of International Financial Markets 21: 75–91. [Google Scholar] [CrossRef]

- Fukuyama, Hirofumi, and William L. Weber. 1999. The efficiency and productivity of Japanese securities firms, 1988–1993. Japan and the World Economy 11: 115–33. [Google Scholar] [CrossRef]

- Greenley, Gordon. 1994. Strategic planning and company performance: An appraisal of theempirical evidence. Scandinavian Journal of Management 10: 383–96. [Google Scholar] [CrossRef]

- Guillén, Jorge, Rengifo Erick, and Ozsoz Emre. 2014. Relative power and efficiency as a main determinant of banks’ profita-bility in Latin America. Borsa Istanbul Review 142: 119–25. [Google Scholar] [CrossRef]

- Hannan, Timothy, and Gerald Hanweck. 1988. Bank Insolvency Risk and the Market for Large Certificates of Deposit. Journal of Money, Credit and Banking 20: 203–11. [Google Scholar] [CrossRef]

- Hausman, Jerry A. 1978. Specification Tests in Econometrics. Econometrica 46: 1251–71. [Google Scholar]

- Hellmann, Thomas F., Kevin C. Murdock, and Joseph E. Stiglitz. 2000. Liberalization, moral hazard, in banking and prudential regulation: Are capital requirements enough? American Economic Review 90: 147–65. [Google Scholar] [CrossRef]

- Hesse, Heiko, and Martin Čihák. 2007. Cooperative Banks and Financial Stability. International Monetary Fund Working Paper, 2. Washington, DC: International Monetary Fund. [Google Scholar]

- Hu, Jin-Li, and Chin-Yi Fang. 2010. Do market share and efficiency matter for each other? An application of the zero-sum gains data envelopment analysis. Journal of the Operational Research Society 61: 647–57. [Google Scholar] [CrossRef]

- Hu, Jin-Li, and Hsueh-E. Yu. 2015. Risk, capital, and operating efficiency: Evidence from Taiwan’s life insurance market. Emerging Markets Finance and Trade 51: S121–S32. [Google Scholar] [CrossRef]

- Hughes, Joseph P., and Choon-Goel Moon. 1995. Measuring Bank Efficiency when Managers Trade Return for Reduced Risk. Working Paper. Newark: Department of Economics, Rutgers University, vol. 20. [Google Scholar]

- Hughes, Joseph P., and Loretta J. Mester. 1998. Bank capitalization and cost: Evidence of scale economies in risk management and signaling. The Review of Economics and Statistics 80: 314–25. [Google Scholar] [CrossRef]

- Ihsan, Ihsan. 2007. Bank ownership and productivity developments: Evidence from Turkey. Studies in Economics and Finance 24: 115–39. [Google Scholar]

- Isik, Ihsan. 2008. Productivity, technology and efficiency of de novo banks: A counter evidence from Turkey. Journal of Multinational Financial Management 18: 427–42. [Google Scholar] [CrossRef]

- Kartal, Fikret. 2013. Development of Capital Markets in Turkey and Analysis of Financial Structure of the Intermediary Institutions. Eurasian Journal of Business and Management, Eurasian Publications 1: 1–14. [Google Scholar]

- Kwan, Simon, and Robert Allen Eisenbeis. 1997. Bank Risk, Capitalization, and Operating Efficiency. Journal of Financial Services Research 12: 117–31. [Google Scholar] [CrossRef]

- Laeven, Luc, and Ross Levine. 2007. Is there a diversification discount in financial conglomerates? Journal of Financial Economics 85: 331–67. [Google Scholar] [CrossRef]

- Lee, Dong-Gull, Jabonn Kim, and Hyounggoo Kang. 2014. Do larger brokerage firms enjoy larger economies of scale and scope? Seoul Journal of Economics 27: 445–67. [Google Scholar]

- Lee, Tung-Hao, and Shu-Hwa Chih. 2013. Does financial regulation affect the profit efficiency and risk of banks? Evidence from China’s commercial banks. The North American Journal of Economics and Finance 26: 705–24. [Google Scholar] [CrossRef]

- Lepetit, Laetitia, and Frank Strobel. 2013. Bank insolvency risk and time-varying Z-score measures. Journal of International Financial Markets Institutions and Money 25: 73–87. [Google Scholar] [CrossRef]

- Locurcio, Marco, Morano Pierluigi, Tajani Francesco, and Anelli Debora. 2021. A multi-criteria decision analysis for the assessment of the real estate credit risks. In Appraisal and Valuation. Contemporary Issues and New Frontiers. Cham: Springer, pp. 327–37. [Google Scholar]

- Mamatzakis, Emmanuel, and Theodora Bermpei. 2014. What drives investment bank performance? The role of risk, liquidity and fees prior to and during the crisis. International Review of Financial Analysis 35: 102–17. [Google Scholar] [CrossRef]

- Mare, Davide Salvatore, Fernando Moreira, and Roberto Rossi. 2017. Nonstationary Z-Score measures. European Journal of Operational Research 260: 348–58. [Google Scholar] [CrossRef]

- Mateev, Miroslav, Tarek Nasr, and Ahmad Sahyouni. 2022. Capital regulation, market power and bank risk-taking in the MENA region: New evidence for Islamic and conventional banks. The Quarterly Review of Economics and Finance 86: 134–55. [Google Scholar] [CrossRef]

- Radic, Nemanja, Franco Fiordelisi, and Claudia Girardone. 2012. Efficiency and risk-taking in pre-crisis in- vestment banks. Journal of Financial Services Research 41: 81–101. [Google Scholar] [CrossRef]

- Rime, Bertrand. 2001. Capital requirements and bank behavior: Empirical evidence for Switzerland. Journal of Banking and Finance 25: 789–805. [Google Scholar] [CrossRef]

- Saeed, Momna, and Marwan Izzeldin. 2016. Examining the relationship between default risk and efficiency in Islamic and conventional banks. Journal of Economic Behavior & Organization 132: 127–54. [Google Scholar]

- Saeed, Momna, Marwan Izzeldin, M. Kabir Hassan, and Vasileios Pappas. 2020. The inter-temporal relationship between risk, capital and efficiency: The case of Islamic and conventional banks. Pacific-Basin Finance Journal 62: 101328. [Google Scholar] [CrossRef]

- Sahut, Jean-Michel, and Mehdi Mili. 2011. Banking distress in MENA countries and the role of mergers as a strategic policy to resolve distress. Economic Modelling 28: 138–46. [Google Scholar] [CrossRef][Green Version]

- Sealey, Calvin W., and James T. Lindley. 1977. Inputs, Outputs, and a Theory of Production and Cost at Depository Financial Institutions. Journal of Finance 32: 1251–66. [Google Scholar] [CrossRef]

- Seiford, Lawrence, and Robert Thrall. 1990. Recent developments in DEA: The mathematical programming approach to frontier analysis. Journal of Econometrics 46: 7–38. [Google Scholar] [CrossRef]

- Shrader, Charles, Lew Taylor, and Dan R. Dalton. 1984. Strategic planning and organisational performance: A critical review. Journal of Management 10: 149–71. [Google Scholar] [CrossRef]

- Shrieves, Ronald E., and Drew Dahl. 1990. The impact of regulation on bank equity infusions. Journal of Banking and Finance 14: 1920–28. [Google Scholar]

- Tan, Yong, and Christos Floros. 2013. Risk, capital and efficiency in Chinese banking. Journal of International Financial Markets, Institutions & Money 26: 378–93. [Google Scholar]

- TCMA. 2009. Turkish Economy & Capital Markets, 1st ed. Istanbul: Turkish Capital Markets Association Publication. ISBN 978-975-6483-23-7. [Google Scholar]

- Van Anh, Do. 2022. Does better capitalization enhance bank efficiency and limit risk taking? Evidence from ASEAN commercial banks. Global Finance Journal 53: 100617. [Google Scholar] [CrossRef]

- Vander, Vennet. 2002. Cost and profit efficiency of financial conglomerates and universal banks in Europe. Journal of Money, Credit, and Banking 34: 254–82. [Google Scholar]

- Wall, Larry D., and David R. Peterson. 1988. Capital changes at large affiliated banks. Journal of Financial Services Research 1: 253–75. [Google Scholar] [CrossRef]

- Wang, Kuo-Liang, Yu-Ting Tseng, and Chia-Hsiang Weng. 2003. A study of production efficiencies of integrated securities firms in Taiwan. Applied Financial Economics 13: 159–67. [Google Scholar] [CrossRef]

- Wild, Joerg. 2016. Efficiency and risk convergence of Eurozone financial markets. Research in International Business and Finance 36: 196–211. [Google Scholar] [CrossRef]

- Williams, Jonathan. 2004. Determining management behaviour in European banking. Journal of Banking and Finance 28: 2427–60. [Google Scholar] [CrossRef]

- Yeyati, Eduardo Levy, and Alejandro Micco. 2007. Concentration and foreign penetration in Latin American banking sectors: Impact on competition and risk. Journal of Banking & Finance 31: 1633–47. [Google Scholar]

- Zhang, Wei David, Shuo Zhang, and Xueming Luo. 2006. Technological progress, inefficiency, and productivity growth in the US securities industry, 1980–2000. Journal of Business Research 59: 589–94. [Google Scholar] [CrossRef]

- Zopounidis, Constantin, Emilios Galariotis, Michael Doumpos, Stavroula Sarri, and Kostas Andriosopoulos. 2015. Multiple criteria decision aiding for finance: An updated bibliographic survey. European Journal of Operational Research 247: 339–48. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

| References | Time Horizon | Country | Methodology | Conclusion | ||

|---|---|---|---|---|---|---|

| Fukuyama and Weber (1999) | 1988–1993 | Japan | DEA + Malmquest Index (compared efficiency change during the research period) | Input -Labor (number) -Physical capital | Output -Brokerage revenue Underwriting revenue | Big four securities companies were more cost-efficient than smaller ones. Overall cost efficiency remained constant during the research period (1988–1993). |

| Wang et al. (2003) | 1991–1993 | Taiwan | DEA + Tobit (for examining the relationship between each efficiency measure and firm specific attributes—i.e., firm size, service composition, having branch) | Input -Labor (number) -Capital (floor area of office) | Output -Brokerage revenue-Equity-dealing revenue -Underwriting revenue | The authors reported that smaller regional firms experienced large decreases in both efficiency and productivity. They also mentioned that the firm size had a positive impact on efficiency scores due to the existence of scale economies and the advantage from joint use of inputs. |

| Chen et al. (2005) | 1999–2000 | China | Ratio Analysis + Regression analysis (profitability (ROE) as dependent variable and leverage, asset size, and government ownership as independent variables) | Results showed that direct investment from the government will reduce a firm’s profitability. The authors suggested to reduce state ownership in this industry, which may lead to better corporate governance and improved financial performance in the long run. | ||

| Zhang et al. (2006) | 1980–2000 | USA | DEA + Malmquest Index (compared efficiency change during the research period) | Input -Labor (compensation) -Fixed assets (non-labor, non-interest expense) -Equity | Output (Revenue) -Brokerage -Market making -Corporate finance -Asset management -Total | Results indicated that the US securities industry in general is quite cross-sectionally inefficient. The relative productivity of the US securities industry in general declined. They also stated that smaller regional firms, due to their inability to respond to technological innovation, were less efficient. |

| Hu and Fang (2010) | 2001–2005 | Taiwan | DEA (maximizing the market share to analyze the competition among securities firms in Taiwan) | Input -Labor (number) -Financial capital | Output -Market share | The empirical results indicated that firms with larger market shares achieved higher efficiency scores. The authors suggested that mergers among large-sized financial institutions should be encouraged in order to increase market shares and efficiency scores. |

| Aktas and Kargin (2007) | 2000–2005 | Turkey | DEA + Malmquest Index (compared efficiency change during the research period) | Input -Equity -Operating industry | Output -Equity transactions -Brokerage commissions | Results showed that larger firms were more efficient. The efficiency decreased overall during the research period. |

| Lee et al. (2014) | 2000–2007 | Korea | Estimation with Cobb–Douglas (hybrid, translog, and quadratic cost functions used separately) production function (commission revenue determined by multiplying the commission rates with the total service amount for different service types; i.e., brokerage, prop trading, and wealth management) | Results showed that the firms broadly achieved economies of scale and substantially benefitted from the economies of scope. The authors posited that larger securities firms may benefit from M&A due to the economy of scale. | ||

| References | Banking Sectors Investigated | Time Horizon | Methodology | Variables | Emprical Results |

|---|---|---|---|---|---|

| Mamatzakis and Bermpei (2014) | 97 banks from G7 and Switzerland | 1997–2010 | Stochastic frontier analysis and dynamic panel threshold analysis | SFA; input: personal exp/assets, operating expense/fixed assets;

output: investment bank fee; fixed netput: equity; assets Control variables: Z-score, liquidity/assets, and other control variables (equity/assets, securities/assets, income diver., GDP per capita, stock index, exchange rate, VIX index) | Results suggested a positive impact of Z-score on bank performance. Liquidity had a negative effect on bank efficiency. |

| Fiordelisi et al. (2011) | 1987 banks from EU-26 | 1995–2007 | Granger-causality techniques to investigate the relationship between bank risk, capital, and efficiency and GMM | Risk: EDF (Moody’s KMV) + NPL/loan Efficiency: SFA-input: labor, capital, fixed assets; output: deposits, loans, other earnings Cap: Equity/assets and other control variables (income diver., asset size, HHI, GDP precipitate, GDP growth rate) | They showed that lower bank efficiency Granger-causes higher bank risk. They also found an increase in bank capital preceded cost efficiency improvements. |

| Tan and Floros (2013) | 101 banks in China | 2003–2009 | Three-stage least-squares estimation of banks’ efficiency; capital, and risk taking | Risk: ROE volatility; Z-score, NPL/loan Efficiency: DEA-input: equity, personal expense; output: loans, securities, non-interest income) Cap: Equity/assets Control variables: ROA, loan/asset, assets, revenue/labor Mcap/GDP, Inflation, GDP Growth) | There was a significant and negative relationship between risk (Z-score) and capitalization. The findings suggested that higher liquidity was associated with lower efficiency. |

| Delis et al. (2014) | 8000 banks in the USA | 1985 Q1–2012 Q4 | They modeled risk as the variance in profit where the variance was a multiplicative component of the error term | Risk: risk-weighted assets/assets, NPL/loan, Z-score, coefficient of variation Efficiency: DEA input: Pers. exps./expenses, int. exp./deposits, fixed-asset exp./expenses; output: profits, loans; Control variables: equity/assets, liquid assets/assets, cost/income, int. rates) | Proposed model was able to capture the increase risk in the US banking sector after 2000. Furthermore, larger banks were riskier after 2004. The findings showed that their measure was a good proxy of banks’ default risk. |

| Wild (2016) | 38,000 banks in 38 Eurozone countries | 1999–2012 | Beta and sigma convergence with GMM, fixed-effect estimation and OLS | Efficiency: DEA-input: pers. exps., fixed assets, deposits output: loans, int. income; other inc. SFA input: loans, securities; output: wages, int. cost, fixed assets Risk: Z-score, capital/assets | For commercial banks, an efficiency convergence of both metrics was found. Savings banks showed no signs of convergence and cooperative banks only showed signs of SFA convergence. |

| Saeed et al. (2020) | 65 Islamic and 180 conventional banks in 14 countries | 2004–2016 | Seemingly unrelated regression (SUR) on banks’ efficiency, capital, and risk taking | Risk: Z-score,

CAP = equity/assets SFA: input: capital, labor; output: loans, deposits Control variables: M2/GDP, Mcap/GDP, inflation, asset size, ROE, concentration (3 large banks), etc. | The capitalization response to increases in insolvency risk was more pronounced for Islamic banks. While efficiency and risk were inversely proportional for conv. banks, it was the opposite for Islamic banks. |

| Van Anh (2022) | 146 banks in 5 ASEAN countries | 2005–2015 | Panel vector autoregression analysis | Risk: Z-score,

CAP = equity/assets SFA: input: capital, labor. fund; output: loans, other earnings, credit/GDP Control variables: GDP frowth, GDP per capita, inflation, concentration (5 large banks) | Better-capitalized banks in ASEAN countries were more efficient and took on less credit risk. Capital consistently influenced cost efficiency across banks with different ownership and sizes, and before and after the 2008 crisis. |

| Mateev et al. (2022) | 225 banks in 18 MENA countries | 2005–2018 | Unbalanced dynamic panel model | Risk: Z-score, loan loss/total loan, ROE volat.;

CAP = cap. adeq. ratio, Tier 1, equity/assets Efficiency ROA, net int. margin, cost/income Control variables: deposits/credit, size, income diversity, noninterest inc., GDP growth, inf. | Capital ratio had a strong positive impact on the credit risk of conventional banks, whereas this effect was insignificant in the sample of Islamic banks. Relationship between capital ratio and credit risk was not moderated by market competitive condition. |

| Z-Score for the Assessment of Banks’ Risk | |||||

| Boyd et al. (2006) | 2500 banks in the USA and 2700 banks in 134 other countries | 1993–2004 | OLS and fixed-effect estimator GMM | Z-Score, HHI index, and other control variables (asset size, non-interest cost/operating income, Mcap, labor force, unemployment rate) | More competition was associated with lower probability of failure (higher Z-score). There was a positive relationship between competition and asset allocation (lending more). |

| Yeyati and Micco (2007) | 3000 banks from 8 countries in Latin America | 1993–2005 | OLS and weighted least-squares estimation | Z-score, HHI index, and other control variables (asset size, ROA, equity/assets, deposits/assets, other income/assets, interest rates, inflation) | Foreign penetration weakened banking competition. There was a negative relationship between foreign penetration and risk. |

| Hesse and Čihák (2007) | 16,000+ banks from 29 countries | 1998–2008 | OLS and fixed-effect estimator GMM | Z-score and control variables (asset size, loans/assets, cost/income, income div., HHI, GDP growth, inflation, exchange rates, int. rates) | Higher Z-scores were linked with a higher stability. |

| Lepetit and Strobel (2013) | 15,000 banks from G-20 countries | 1992–2009 | Compared different approaches to the construction of the Z-score with simple root-mean-squares error criteria | Z-score and its components | Time-varying Z-score measures best fit the data. |

| BCC | CCR | Equation No. | |

|---|---|---|---|

| Objective function | minθ, λ θ | minθ, λ θ | (1) |

| Subjected to: | −yi + Y λ ≥0 | −yi + Y λ ≥ 0 | (2) |

| θxi − X λ ≥ 0 | θxi − X λ ≥ 0 | (3) | |

| λ ≥ 0 | λ ≥ 0 | (4) | |

| N1′λ = 1 | (5) |

| Account | Risk Weights (%) |

|---|---|

| Financial assets | |

| Shares (listed) | 20 |

| Shares (non-listed) | 50 |

| Corporate bonds | |

| >1 year | 10 |

| <1 year | 50 |

| Public bonds | |

| >1 year | 5 |

| <1 year | 10 |

| Subsidiaries | 30 |

| Short-term trade receivables | 50 |

| Short-term other receivables | 30 |

| Long-term trade and other receivables | 50 |

| Short-term liabilities | 5 |

| Long-term liabilities | 10 |

| Variables | Acronym | Definition |

|---|---|---|

| Position risk | Position risk | Ratio of risk-weighted assets to capital |

| Default risk | Z-score | Ratio between the return on assets plus capital/total assets and the standard deviation of the return on assets |

| Operational efficiency | CCR EFF (opr.) | Technical efficiency scores derived from operational data |

| BCC EFF (opr.) | Pure technical efficiency scores derived from operational data | |

| Scale EFF (opr.) | Scale efficiency scores derived from operational data | |

| Financial efficiency | CCR Eff (fin.) | Technical efficiency scores derived from financial tables |

| BCC EFF (fin.) | Pure technical efficiency scores derived from financial tables | |

| Scale EFF (fin.) | Scale efficiency scores derived from financial tables | |

| Man. EFF | Ratio of operational expenses to operational income | |

| Capital | CAP | Book value of capital to total assets |

| Firm-specific variables | ||

| Size | Size | Logarithm of total assets |

| Growth | Growth | Growth rate of total assets |

| Profitability | ROE | Return on equity |

| Business model | Inc. dıv. | Ratio of non-brokerage income to total income |

| Labour productivity | LP | Ratio of gross total revenue to total number of employees |

| Qualified employees | Labor | The number of staff that hold the related capital markets licenses for market professionals |

| Sector specific variables | ||

| Market design | HHI | Herfindahl–Hirschman Index of total trading volume |

| Market size | Mcap | Logarithm of total market capitalization of the exchange |

| Macroeconomic | ||

| Inflation | IR | Annual inflation rate |

| GDP growth | GDPG | Annual GDP growth rate |

| Mean | S.D. | Min | Max. | |

|---|---|---|---|---|

| Risk | ||||

| Position risk (%) | 47.6 | 93.4 | 9.8 | 118.9 |

| Z-score | 44.2 | 21.6 | 6.5 | 114.8 |

| Operational Efficiency (%) | ||||

| CCR Eff (opr.) | 56.5 | 29.8 | 21.1 | 100 |

| BCC EFF (opr.) | 84.5 | 26.9 | 14.9 | 100 |

| Scale EFF (opr.) | 66.1 | 30.2 | 18.6 | 100 |

| Financial Efficiency (%) | ||||

| CCR Eff (fin.) | 49.2 | 25.9 | 19.4 | 100 |

| BCC EFF (fin.) | 73.5 | 23.4 | 13.9 | 100 |

| Scale EFF (fin.) | 67.0 | 26.2 | 20.3 | 100 |

| Managerial Efficiency (%) | ||||

| Op. Income/Op. Expense | 98.2 | 50.6 | 28.8 | 146.2 |

| Capital | ||||

| Equity to Total Assets | 45.0 | 64.4 | 30.8 | 84.9 |

| Firm-Specific Variables | ||||

| Assets (ln) | 16.9 | 1.6 | 13.8 | 18.9 |

| Growth of assets (%) | 44.2 | 98.2 | −53.5 | 218 |

| Return on equity (%) | 8.4 | 14.4 | −3.6 | 49.7 |

| Income diversification (%) | 40.4 | 22.4 | 7.2 | 87.6 |

| Income per person (normalized) | 37.5 | 19.8 | 7.4 | 82.5 |

| Qualified staff ratio (%) | 12.5 | 12.4 | 0.0 | 17.9 |

| Sector-Specific Variables | ||||

| HHI (trading volume) | 48.9 | 27.1 | 9.6 | 106.0 |

| Mcap (ln) | 12.6 | 15.3 | 1.5 | 13.4 |

| Macroeconomics | ||||

| GDPG | 5.3 | 4.0 | −4.7 | 11.1 |

| IR | 9.4 | 3.4 | 4.0 | 25.2 |

| 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | 11 | 12 | 13 | 14 | 15 | 16 | 17 | 18 | ||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Position risk | 1 | 100.0 | |||||||||||||||||

| Z-score | 2 | 18.1 * | 100.0 | ||||||||||||||||

| CCR EFF (fin.) | 3 | 15.2 * | −39.9 * | 100.0 | |||||||||||||||

| BCC EFF (fin.) | 4 | 14.9 * | −40.7 ** | 49.6 | 100.0 | ||||||||||||||

| Scale EFF (fin.) | 5 | 17.2 | −34.6 * | 45.2 | 50.0 | 100.0 | |||||||||||||

| CCR EFF (opr.) | 6 | 24.4 * | −16.4 * | 20.7 | 43.3 ** | 50.2 ** | 100.0 | ||||||||||||

| BCC EFF (opr.) | 7 | 12.2 * | −36.2 | 10.0 | 39.6 * | 42.1 * | 28.9 | 100.0 | |||||||||||

| Scale EFF (opr.) | 8 | 14.1 | −42.0 * | 11.6 | 46.0 | 48.9 ** | 33.6 | 32.7 | 100.0 | ||||||||||

| Man. EFF | 9 | 23.6 | −15.2 * | 10.7 | 11.6 ** | 22.0 | 14.6 ** | 78.2 | 62.6 * | 100.0 | |||||||||

| CAP | 10 | −44.0 ** | −15.1 * | 1.2 | 1.5 | 3.8 | 6.8 * | 31.7 * | 25.4 * | 6.8 ** | 100.0 | ||||||||

| Size | Size | 27.6 ** | 21.2 | −64.4 | 49.0 * | 42.1 | −12.8 * | −20.3 | −16.2 * | −12.8 | −19.2 | 100.0 | |||||||

| Inc. dıv. | 12 | 28.9 | 8.4 | 22.9 | 28.8 | 27.7 | 32.2 | 46.4 | 37.1 | 32.2 | 47.4 | −17.3 | 100.0 | ||||||

| Growth | 13 | −1.8 | −4.9 | 31.7 | 28.2 * | 10.2 * | −15.2 * | −9.2 * | −7.4 | −15.2 | 34.2 ** | −37.9 * | 49.2 ** | 100.0 | |||||

| Labor | 14 | 11.3 ** | −9.2 | 3.1 | −4.2 | −12.3 * | 2.7 | 5.0 | 4.0 * | 2.7 ** | −4.0 | 1.5 | 0.4 ** | −6.1 * | 100.0 | ||||

| LP | 15 | 2.7 * | −16.9 ** | 6.3 | −7.9 | 7.6 ** | 15.5 ** | 7.3 | 5.8 ** | −15.5 * | 17.4 | 3.3 | 31.9 * | 11.2 * | −2.1 | 100.0 | |||

| ROE | 16 | −14.1 ** | 30.4 ** | 4.7 | 26.7 | 33.6 | 30.1 | 26.4 * | 21.1 | 27.2 | 40.0 * | 12.2 ** | 1.8 | 19.2 | 28.4 | 34.6 | 100.0 | ||

| HHI | 17 | 2.4 | 3.1 | 2.9 * | 8.2 | 15.6 * | 47.5 | 7.1 ** | 3.7 | 6.8 ** | 4.4 | 20.0 | 7.7 | 2.5 | 6.2 * | 29.8 | 28.4 | 100.0 | |

| Mcap | 18 | 19.3 * | 25.4 | 0.6 | 1.2 * | 2.7 * | 6.3 | 16.2 * | 13.0 | 12.3 ** | 3.5 | −1.2 * | 4.4 | 29.4 ** | 1.2 * | 0.0 | 1.6 * | −4.6 ** | 100.0 |

| Multicollinearity Diagnostic Statistics | |||||||||||||||||||

| Vari. inflation factor | 1.08 | 1.09 | 1.34 | 1.230 | 1.42 | 1.36 | 1.19 | 1.80 | 1.10 | 1.21 | 1.28 | 3.14 | 1.32 | 1.49 | 1.29 | 1.09 | 1.70 | 1.13 | 1.70 |

| Tolerance values | 0.99 | 0.92 | 0.75 | 0.85 | 0.98 | 0.94 | 0.88 | 0.92 | 0.88 | 0.83 | 0.82 | 0.31 | 0.75 | 0.70 | 0.77 | 0.92 | 0.65 | 0.82 | 0.68 |

| 8a. Model in which Risk = Position Risk | 8b. Model in which Risk = Z-score | |||||

|---|---|---|---|---|---|---|

| DV: Efficiency | DV: Risk | DV: Capital | DV: Efficiency | DV: Risk | DV: Capital | |

| Equation (1) Y = BCC EFF (opr.) | Equation (2) Y = Risk | Equation (3) Y = CAP | Equation (1) Y = BCC EFF (opr.) | Equation (2) Y = Risk | Equation (3) Y = CAP | |

| Risk | 12.24 ** (0.35) | 11.17 *** (8.07) | 0.123 (0.18) | 8.66 * (1.10) | ||

| EFF | 19.17 ** (−0.4) | 4.82 (1.05) | 5.22 ** (2.11) | 23.66 ** (1.43) | ||

| CAP | 0.03 ** (1.79) | 34.08 *** (8.07) | 0.002 (1.43) | 6.817 ** (1.10) | ||

| ROE | 7.32 ** (0.41) | −15.66 * (−0.84) | −6.18 (−0.14) | 7.12 ** (0.13) | −7.06 (0.81) | −27.12 (−0.64) |

| Size | 7.032 (7.23) | 3.27 ** (2.13) | 8.38 ** (1.35) | 0.03 *** (7.69) | 12.001 ** (2.23) | −1.02 ***(−3.80) |

| Growth | −0.28 * (−2.85) | −0.29 (0.82) | 9.19 **(2.48) | −2.02 *** (−3.58) | 0.9601 * (−1.66) | −0.04 (−1.18) |

| Inc. Div. (%) | 3.05 ** (3.22) | −7.68 * (0.21) | 5.09 ** (1.51) | −1.04 *** (−2.68) | 5636 (−0.39) | −0.903 (−1.04) |

| LP | −1.25 ** (−1.08) | 3.02 (0.28) | 3.75 (1.47) | 9.013 ** (0.27) | 0.96 ** (2.33) | 3.62 (1.54) |

| Labour | 2.03 ** (1.79) | 15.13 ***(4.01) | −0.902 (−1.07) | 1.81 * (1.93) | 0.112 (0.12) | −34.42 (−0.58) |

| HHI | −1.019 *** (−2.60) | −3.13 (−0.42) | 0.57 (1.43) | −1.018 *** (−2.80) | 7.82 * (−0.91) | 0.902 ** (2.21) |

| Mcap | 1.13 **(1.17) | 2.87 ** (2.03) | 7.64 (0.75) | 1.82 *(1.78) | −0.0055 (−0.30) | 26.12 ** (2.54) |

| GDPG | 0.02 * (1.77) | −0.003 ** (−2.13) | −0.08 (−0.12) | 0.014 (1.30) | 297.63 (1.10) | −0.1 (−0.16) |

| IR | 0.001 (0.13) | −0.0005 (−0.62) | 0.396 (0.91) | 0.001 (0.14) | 347.5 * (1.96) | −0.094 (−0.23) |

| Constant | 1.23 ** (2.49) | −18.319 (−1.54) | −18.18 (−0.65) | 1.4 *** (3.15) | 0.026 (0.52) | 61.55 ** (−2.18) |

| No of Obs. | 5575 | 5575 | 5575 | 5575 | 5575 | 5575 |

| Chi2 | 906.86 *** | 1040.14 *** | 1238.32 *** | 112.55 *** | 77.55 ** | 60.22 *** |

| R2 (Overall) | 37.69 | 53.18 | 44.45 | 16.82 | 37.69 | 34.11 |

| 9a. Model in which Risk = Position Risk | 9b. Model in which Risk = Z-score | |||||

|---|---|---|---|---|---|---|

| DV: Efficiency | DV: Risk | DV: Capital | DV: Efficiency | DV: Risk | DV: Capital | |

| Equation (1) Y = BCC EFF (fin.) | Equation (2) Y = Risk | Equation (3) Y = CAP | Equation (1) Y = BCC EFF (fin.) | Equation (2) Y = Risk | Equation (3) Y = Capital | |

| Risk | 9.57 ** (0.27) | 7.32 (1,04) | 0.875 ** (1.37) | 18.45 ** (1.11) | ||

| EFF | 15.147 ** (5.13) | 6.79 *** (1.45) | 4.096 (1.65) ** | 10.566 (1.42) | ||

| CAP | 2.39 *** (2.18) | 41.01 ** (9.04) | 0.251 (0.37) | 2.216 (5.10) * | ||

| ROE | 4.93 ***(5.41) | −28.35 * (−0.80) | 2.14 (5.12) | - | - | - |

| Size | −1.27 (0.26) | 9.03 *** (9.45) | 5.48 * (7.23) | 0.32 ** (0.41) | 9.39 **(3.27) | 4.45 ** (7.89) |

| Growth | −0.1 * (−1.15) | −0.001 (−0.15) | −1.28 (1.58) | −7.032 (7.23) | 1.134 (0.55) | 0.16 (−3.45) |

| Inc. Div. (%) | 2.17 **(2.22) | 0.2 (0.09) | 1.82 ** (1.76) | 3.05 *** (3.22) | 4.396 * (2.15) | −29.03 (−0.49) |

| LP | 1.97 ***(0.98) | 2.154 ** (0.27) | 2.95 ** (2.13) | 1.14 ***(4.10) | 5.64 (1.18) | 0.89 ** (2.18) |

| Labour | 3.79 * (1.03) | 4.21 ** (1.04) | 6.37 ** (4.52) | 1.81 * (−1.93) | 0.0005 (0.987) | 26.26 ** (2.55) |

| HHI | −0.196 (−1.18) | −0.054 (0.53) | 0.89 ** (2.18) | −8.885 (−60) | 9.53 * (−1.87) | −0.93 (−1.06) |

| Mcap | 1.21 ** (0.47) | −0.163 (−0.88) | 26.26 (2.55) | 2.73 ** (0.47) | −0.5(0.97) | 20.375 (5.98) |

| GDPG | −0.0002 (−0.30) | −5.88 (−0.74) | −0.007 (−0.35) | 2.17 (0.18) | 0.02 (0.26) | 0.42 (0.97) |

| IR | 0.005 (0.34) | 349.78 ** (1.98) | −0.09 (−0.22) | 7.57 (0.28) | 237 (8.57) | 0.103 (0.16) |

| Constant | 1.39 *** (3.17) | −3.16 (−0.45) | −61.36 **(−2.18) | 3.14 *** (1.5) | 8.6 (7.5) | −61.36 ** (−2.18) |

| No of Obs. | 5575 | 5575 | 5575 | 5575 | 5575 | 5575 |

| Chi2 | 116.32 * | 60.05 * | 112.52 ** | 87.78 *** | 60.489 ** | 37.05 *** |

| R2 (Overall) | 30.12 | 42.54 | 35.56 | 19.53 | 39.39 | 23.18 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Cevikcan, G.; Tas, O. Risk-Oriented Efficiency Assessment within the Level of Capitalization for Financial Institutions: Evidence from Turkish Securities Firms. Int. J. Financial Stud. 2022, 10, 110. https://doi.org/10.3390/ijfs10040110

Cevikcan G, Tas O. Risk-Oriented Efficiency Assessment within the Level of Capitalization for Financial Institutions: Evidence from Turkish Securities Firms. International Journal of Financial Studies. 2022; 10(4):110. https://doi.org/10.3390/ijfs10040110

Chicago/Turabian StyleCevikcan, Gokben, and Oktay Tas. 2022. "Risk-Oriented Efficiency Assessment within the Level of Capitalization for Financial Institutions: Evidence from Turkish Securities Firms" International Journal of Financial Studies 10, no. 4: 110. https://doi.org/10.3390/ijfs10040110

APA StyleCevikcan, G., & Tas, O. (2022). Risk-Oriented Efficiency Assessment within the Level of Capitalization for Financial Institutions: Evidence from Turkish Securities Firms. International Journal of Financial Studies, 10(4), 110. https://doi.org/10.3390/ijfs10040110