Abstract

This research examined the gist of financial literacy on the medium entrepreneurs in Indonesia, impacting the retirement planning through some mediator and moderating variables. Implementing the prospect theory and theory of planned behavior to explore these interactions, a series of hypotheses were constructed, considering financial risk tolerance and saving behavior as mediator variables and herding behavior as moderator variables. The study examined partial least square-structural equation modelling (PLS-SEM) obtained by sampling data from 388 entrepreneurs of medium-scale in the Bekasi Regency, Indonesia. The study revealed (a) how financial literacy on retirement planning is serial mediated by financial risk tolerance and saving behavior, (b) herding behavior can strengthen financial literacy’s influence on retirement planning, and (c) saving behavior as a mediator does not influence the relationship between financial literacy and retirement planning. The study confirms how financial risk tolerance and herding behavior bridge a positive relationship between financial literacy and retirement planning.

1. Introduction

In the latest years, communities around the world have abided on more obligations regarding their financial welfare. Brushing fluctuations in the pension background have tarnished the primary catalyst for this improved self-sufficiency of consumers evading financial judgments, involving saving, investing, and decumulating fortune to workers and pensioners. Individuals must be more concerned for their economic welfare in the retirement period. With the leverage in private duty to fortify financial well-being in retirement and the speedy improvement of various products in financial markets, developing relates to whether persons have adequate financial expertise and competencies to design and protect sufficiently for retirement in the latest years.

Indonesia is positioned as the most financial illiterate country in the Asia–Pacific territory (Amirio 2015). A domestic survey carried out by financial literacy and presence in 2020 showed that entrepreneurs’ financial literacy indicator was lesser than employees in the entirety of the regions in Indonesia. The average score for the financial literacy indicator in employees was 37.4%, and 28.3% for entrepreneurs (Indonesia Financial Service Authority 2020). Statistics Center Bureau (2021), entrepreneurs’ income is more excellent than employees. Besides, statistics from the National Survey of Social and Economy (2020) show that 18.58% of the labor force comprises medium entrepreneurs, and employees are 38.11% of the total labor force in Indonesia. Concurrently, medium entrepreneurs have a slight tendency to benefit from the Social Security Program. The government has seemingly legalized the pension program in the Government Law of the Republic of Indonesia comprising the Prerequisite of Involvement in the Social Security Program, which specifies which companies are necessitated to prepare social security for their workers. Conversely, On the other hand, entrepreneurs often do not think about their old age, so they do not have a definite pension guarantee, especially related to sound financial management and independent retirement planning.

The significance of pension planning urges the necessity for researchers associated with retirement planning. Furthermore, low levels of financial knowledge are connected to financial activities, possibly to obtain long-term aftereffects. A significant fraction of homemakers have poor literacy of basic economic views in China and Germany, which allow them to have a more advanced financial acquaintance (Bucher-Koenen and Lusardi 2011; Niu et al. 2020). Moreover, an extensive assortment of financial literacy occurs amid diverse social factions. In detail, women and the elderly show sinking ranks of financial literacy (Hilgert et al. 2003; Niu et al. 2020). Additionally, some studies reveal that financial literacy does not influence retirement planning because of higher levels of education (Noone et al. 2010; Almenberg and Säve-Söderbergh 2011; Crossan et al. 2011; Aluodi et al. 2017; Farrar et al. 2019; Niu et al. 2020). However, financial literacy is an aspect correlated to retirement planning, which has obtained some awareness and is recognized as necessary in various kinds of research. The literature defines which financial literacy is a critical aspect that certainly influences retirement planning in several advanced states (Bucher-Koenen and Lusardi 2011; Lusardi and Mitchell 2011; Van Rooij et al. 2011; Sekita 2011; Boisclair et al. 2017; Ricci and Caratelli 2017; Kalmi and Ruuskanen 2018; Larisa et al. 2020). Previous literature provided ambiguous and contradictory results. A further study of the impact of financial literacy on the retirement planning of medium entrepreneurs (ME) in Indonesia is considered to address this research gap. The self-employed, such as entrepreneurs, have a better tendency to plan for pension, but they are unprotected by social security mainly because of limited financial knowledge.

Subsequently, the prospect theory is a behavioral model which reveals how individuals determine, among choices that comprise risk and vagueness, a course of action (Kahneman and Tversky 1979). It shows the informatively precise concept of personal decision-making by bordering risky alternatives. The public is loss-repellent; since individuals are averse to losses rather than equivalent profits, they are more eager to bear risks to elude a loss. Prospect theory suggests saving behavior that may be ideal as a practicality intensification perspective to reserve cash for the future, specifically for deficient revenue persons (Anderson et al. 2017). On the other end, some people with stable wages may not have ample cash flow in poverty circumstances and then need to use traditional savings vehicles. Corresponding to prospect theory (Kahneman and Tversky 1979), persons are risk-avoidant around profits and risk-taking in terms of the shortfall. When individuals do not have sufficient knowledge or cannot appraise the estimated result of a particular financial judgment, they tend to identify such a verdict from the field of sustaining returns, demonstrating an inclination toward the status quo and becoming more risk-disinclined. Individuals’ dislike of risk considering investments falls with the skill to manage and recognize financial data and threat circumstances (Riley and Chow 1992). Consequently, risk tolerance is significantly related to financial literacy; financial literacy is positively linked with pension savings of households throughout time and managing for risk acceptance, and increases wealth accumulation for retirement planning (Van Rooij et al. 2012). This study addresses the research gap in how financial literacy influences saving behavior, risk tolerance, and the resulting retirement planning.

Moreover, the theory of planned behavior (TPB) approach states that individuals are more likely to intend to follow a certain action if they feel they have the resources and support from the surrounding environment to perform the behavior (Ajzen 1991). In the context of retirement planning, individual financial literacy will also greatly determine retirement planning activities, such as knowing financial products to support investment in appropriate products to prepare for old age. Financial literacy delivers knowledge of financial instruments and facilities on the market. It enhances financial decision-taking (Altman 2012) due to financial knowledge, and precious information is the key aspect of financial literacy (Lusardi and Mitchell 2007). It improves people’s competencies to analyze information and aid them in making rational investment decisions (Lusardi and Mitchell 2014) even though it has not been integrated into an existent wide-ranging and well-recognized psychosocial concept. In a casing, the reasons state that financial literacy has a link with the decision of retirement planning, which can be moderated with herding behavior. Medium entrepreneurs who pursue herding behavior in society have amassed sufficient knowledge and have been more convinced considering information from their colleagues’ for decision-making regarding retirement planning. So, there is an influence of the role of herding behavior in filling the research gap above; it strengthens the influence of the relationship between financial literacy on retirement planning for medium entrepreneurs (ME).

Furthermore, to initiate such empirical research, this study aimed to make the following contributions. First, we aimed to observe financial literacy’s effect on the prospect of pension preparation for MEs in Indonesia. Second, we recognized the relationship between financial literacy and pension planning through financial risk tolerance. The results from this research will be helpful for MEs concerned with enlightening retirement safety. With the escalation in private obligation for fortifying economic well-being in the pension period, rising matters about if people have satisfactory financial experience and competencies to arrange and protect themselves sufficiently for pension in the latest years come to the fore. Third, we enhanced the interaction effects between financial literacy and retirement planning through saving behavior. The results may also support MEs in recognizing their financial proficiency regarding the propensity to organize for retirement within financial instruments dynamically. Fourth, we addressed how the herding behavior of MEs moderates the impact of financial literacy on retirement planning. This paper examined how financial literacy significantly influences retirement planning and further explored how saving behavior and risk tolerance bridge the gap between financial literacy and retirement planning.

In summary of the above discussion, individuals must realize that financial decisions and skills to prepare for a more prosperous life at retirement age are important. Therefore, retirement planning is also important for medium-sized entrepreneurs considering that their financial literacy, which is low compared with their colleagues who work as employees (Indonesia Financial Service Authority 2020), and medium-sized entrepreneurs do not have to participate in the retirement planning program. Furthermore, there are contradictory empirical research results related to the effect of financial literacy on retirement planning. Research conducted by Bucher-Koenen and Lusardi (2011); Lusardi and Mitchell (2011); Boisclair et al. (2017); Ricci and Caratelli (2017); Kalmi and Ruuskanen (2018); and Larisa et al. (2020) found significant effects; on the other hand, research conducted by Aluodi et al. (2017); Farrar et al. (2019); and Niu et al. (2020) found no significant effects. Prospect theory (Kahneman and Tversky 1979) contributes ideas in analyzing the effect of financial literacy on retirement planning, because individuals tend to take high-risk retirement savings decisions in facing uncertain old age finances. In accordance with The Planned Behavior (Ajzen 1991), the environment can provide encouragement to individuals in making choices and making decisions about retirement savings products.

2. Literature Review

2.1. Prospect Theory

Prospect Theory suggests that individuals do not continually perform, instead allowing financial theory norms to handle risk and hesitation. They put psychological aspects and unsystematic behavior into realistic preferences (Kahneman and Tversky 1979). Risk variables connected with psychological aspects cause everyone to have diverse attitudes in replying to each return stage. Risk is regarded as pension preparation; this phrase is recognized as risk tolerance. A person’s risk inclinations for comparative benefits and shortfalls lean to evade losses from investing completed earlier (Agnew et al. 2012). For this purpose, financial risk tolerance can be regarded as an instrument to influence the risk behavior of the person in the practice of investment decision-making. Individuals organize retirement planning to contemplate risk preferences in deciding the kind of investment product that adheres to their risk profile. The variation in one’s financial capability has after-effects on a person’s risk tolerance. The better the individual’s financial literacy, the better the financial risk tolerance that the person has.

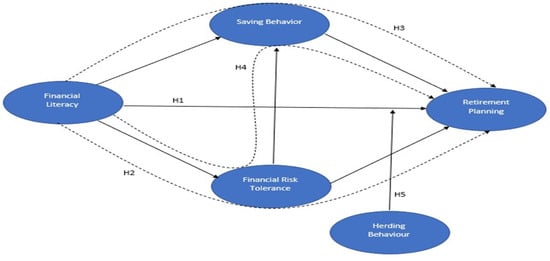

For this reason, individuals in every arrangement of retirement planning should contemplate the effect of uncertainty to confirm whether the retirement planning can be amply accomplished. Regarding gain and loss in selecting an investment product employed as an investment instrument for retirement planning, considering profit and cost is directly linked to the determinant of high-risk, high return in investing so that pensioners achieve an excellent stage of financial literacy. In representing the prospect theory, this research recognized financial literacy and financial risk tolerance as mediators and analyzed their effect on the retirement planning, as illustrated in Figure 1.

Figure 1.

Conceptual Model (----: indirect effect; →: direct effect).

2.2. Theory of Planned Behavior

The Theory of Planned Behavior (TPB) provides a constructive theoretical structure for handling the intricacy of human social behavior (Ajzen 1991). It is often applied to describe behavioral patterns and recognize how people create behavioral judgments (Xiao and Wu 2008). The model of any behavior is the establishment of an aim for behavior. TPB is employed to explore the more profound faiths that affect an individual’s financial behavior (Zocchi 2013). Thus, it is fundamental to determine which approaches be explored and intended to support people in implementing definite financial behaviors. Commonly, people are encouraged to keep emergency funds (Abrahamse and Steg 2009). However, a person’s ability to reserve is affected by the deficiency of chance, acquaintance, deficiency of determination, and manners toward savings and financial organizations. The TPB is persistently concerned with social psychology literature and is utilized in research credit advocating, private finance, and asset management together locally and globally (Ajzen 1991; Rutherford and DeVaney 2009).

The aspects that affect people in arranging retirement planning are variances in lifestyle consciousness in the pre-retirement phase that can shrink endowments to retirement planning (Griffin et al. 2012). After retiring, estimating economic burden is a primary aspect that leads individuals to participate in retirement planning. Expected post-retirement financial circumstances have encouraged people to organize themselves well to achieve post-retirement financial circumstances that meet their expectations. Additionally, estimation and clearness of aims, tradition, and environmental aspects can also encourage people to plan their retirement early. The situation has provided a view into the involved individual, suggesting that well-ready people will obtain a better post-retirement financial situation with retirement planning to create retirement funds. Furthermore, the effect of financial literacy on retirement planning is conducted to determine how an individual’s financial literacy level can influence and encourage individuals to make retirement planning. In connection with the contradictory results of empirical research on the effect of financial literacy on retirement planning, further analysis was carried out by placing the variables of financial risk tolerance and saving behavior as mediatiors and herding behavior as a moderator using prospect theory and the planned behavior as the basis for the analysis. The empirical research conducted to support the conceptual framework of this study comprises: (a) the research of Baskoro and Aulia (2019) on the effect of financial literacy on retirement planning, (b) the research of Heenkenda (2014), Gustafsson and Omark (2015), Chatterjee et al. (2017), Mahdzan et al. (2017), and Zazili et al. (2017) on the effect of financial literacy on financial risk tolerance, saving behavior, and retirement planning, and (c) the research by Choi and Yoon (2020) on herding behavior as a moderating variable between financial literacy and retirement planning. In drawing upon prospect theory, this study identified financial literacy and saving behavior and financial risk tolerance as mediators and examined their impacts on retirement planning, as depicted in Figure 1.

2.3. Relationship between Financial Literacy and Retirement Planning

Financial literacy is the capacity to know how money toils in the world, that is, how the people obtains or creates it, how people handle it, how people capitalize on it (turns it into more), and how people contribute it to support others (Kusairi et al. 2019). It is acquired by the level of education (through which people can expand their basic literacy and numeracy competencies required to obtain financial knowledge and improve financial literacy). Evidence shows that financial results in pension age are suggestively enhanced and as a critical factor in retirement planning (Lusardi and Mitchell 2007; Van Rooij et al. 2011). Regarding Remund (2010), financial literacy can be compressed as an understanding of economic constructs; capability to correspond related to financial concepts; capacity to handle individual finances; competence in formulating proper financial decisions; and assurance in meritoriously arranging for the outlook financial literacy necessitates. It is usually supposed that financial literacy might increase the level of financial decisions. Some empirical studies reveal how financial literacy affects retirement planning behavior, subsequently impacting retirement prosperity. Many people are constrained in identifying fundamental financial concepts (Van Rooij et al. 2012). The obligation for pension endowment has gradually moved from institutions, organizations, and owners toward people, many of whom are ill-prepared to arrange for their pension.

Lusardi and Mitchell (2011) stated the significance of financial literacy as the main factor in retirement planning, assessing individuals’ ability to understand interest rates, inflation, and risk. However, it is an element of retirement planning activities, and retirement planning leads to enhanced prosperity and revenue safety in old age, estimated to be connected with these improved results (Agnew et al. 2012). In retirement planning, existing capital and chances significantly impact retirement planning, such as enough revenue and financial literacy and arranging for retirement with the spare time available. From an entrepreneur’s perspective, the financial literacy echelons of SMEs in Indonesia can affect their financial judgments in the range of management of financial sources, suitable portion of reserves and a better assortment of investment instruments, and responsiveness of progress funding choices. Based on the explanation above, this study’s objective was to determine whether the financial literacy of medium-sized entrepreneurs influences retirement planning as suggested by the results of previous empirical research, such as that by Baskoro and Aulia (2019). People can engage in financial planning for the pension period. Thus, we posit the following hypothesis:

Hyphotesis 1.

Financial literacy has a positive impact on retirement planning.

2.4. Mediation Effect of Financial Risk Tolerance on the Relationship between Financial Literacy and Retirement Planning

Risk tolerance is the inclination to make a risky or less risky choice regarding the trade-off between risk and gain (Dohmen et al. 2011). Primarily, economic and financial experts utilize the view of risk tolerance in investment and monetary judgments. This study employed risk tolerance as an individual inclination for risk. The personal preference of risk was assessed as an individual’s personality and eagerness to grasp a financial risk if they have some precautionary money for saving or investment (Kusairi et al. 2019). People are eager to achieve a convinced target, where deeds result as vague and are commonly attended by the likelihood of some shortfall (Grable 2008). Overall, risk tolerance as a construct is derived from the capacity of financial psychology and is almost contrariwise linked with the economic perception of risk avoidance (Kimball and dan Shapiro 2008).

The alliance between financial literacy on financial risk adoption (i.e., investing in the capital market) has obtained substantial consideration by academics and stakeholders. Educational achievement is an aspect of risk tolerance because well-educated people have better knowledge and thus better recognize the type of risk than persons with decreased stages of academic achievement. Reliability of interest mixed with the persistence of determination expressively explains variances in achievement results (Duckworth et al. 2007). Individuals’ definite concern in financial topics, which, in families is having a concern and effort to obtain market information and the latest methods of saving, is associated with variances in saving behavior (Gunnarsson and Wahlund 1997). These findings state that financial attentiveness emerges as outstanding among investors that invest in capital markets and hold more complicated instruments to warrant stock. Hermansson and Jonsson (2021) revealed that financial literacy is linked with higher risk tolerance; it displays a meaningfully higher correlation. Their result indicated that financial literacy confirms a significant relationship with the lower-risk-tolerance scale. Thus, financial literacy is positively related with risk-tolerance divergency. Hence, the empirical results support the literature on financial risk tolerance.

According to prospect theory, people are risk-reluctant in profits and risk-striving regarding losses (Kahneman and Tversky 1979). These faults are amplified when people have inadequate competencies and fail to recognize the dangers of assured financial judgments. When people have no adequate knowledge or cannot appraise the predictable result of a particular financial decision, they are inclined to observe such choices from the perspective of maintaining profits and, thus, exhibit a fondness for the status quo and become more risk-averse. A mixture of a person’s eagerness and capability to secure financial risks is financial risk tolerance (FRT) (Faff et al. 2008). Then, to assess one’s FRT precisely, the degree of financial literacy should be regarded together with other psychological traits, time perspective, fiscal sources, and capability to mitigate risk. Educational achievement, earnings, and prosperity are linked to financial risk tolerance (Hallahan et al. 2004). The perception of FRT is influenced by individuals’ financial numeracy and financial management skills (Sages and Grable 2010). Therefore, individuals with high financial knowledge can mitigate financial risks.

A person’s most crucial decisions can compose pension investment judgments, emphasizing the significance of comprehending personal investing decision direction aspects. Larson et al. (2016) regarded critical aspects such as financial literacy and risk tolerance as affecting pension investment judgments. Their research concentrated on teenagers identified for their risk behavior and the distinctive circumstances that influence the reviews they create. The study observed the impact of risk tolerance on teenagers’ retirement planning that exhibited four investment choices between conventional and extremely risky. People were required to choose an investment selection and thus accomplish the FRT gauge because the investment’s yield could not repose the investment made or could not reach the predetermined level (Sun et al. 2020). People were required to choose an investment selection and thus accomplish the FRT gauge. Pension preparation for persons with a great FRT is greater than for persons that obviate risks (Yuh and DeVaney 1996). Afterward, people with great tolerance regarding risk desire are likely to make high-risk investments, such as in stocks. Those that avoid risks choose to put their money in markets and savings accounts that create magnificent financial strategies (Hariharan et al. 2000; Jacobs-Lawson and Hershey 2005). Based on the explanation above, the objective of this study was to determine whether the financial risk tolerance of medium-sized entrepreneurs is considered as a mediating variable that connects the effect of financial literacy to retirement planning, in accordance with the results of previous studies, such as those by Heenkenda (2014) and Tavor and Garyn-Tal (2016). Thus, we posit the following hypothesis:

Hypothesis 2.

Financial risk tolerance mediates the relationship between financial literacy and retirement planning.

2.5. Mediation Effect of Saving Behavior on the Relationship between Financial Literacy and Retirement Planning

Saving is a deed of reserving existing capital for future necessities. Some people could oppose the description of saving, although they may diverge in the way of saving. Saving schemes include reserving cash, investment funds, deposits, purchasing shares in the capital market, or participating in a pension schedule. Saving proposes spending less than a specified amount of income to expend it in the forthcoming years, whereby the actual reason to accrue savings for future consumption (Mori 2019). People usually reserve their funds in the pension period. Retirees must have some individual savings to accommodate for lost wages after pension. It is fundamental to seek which aspects affect saving behavior the most. The Latest empirical results suggest that FL is positively linked with prosperity accretion and households’ savings over time (Van Rooij et al. 2012). Conversely, the link between FL and its impact on the savings behavior of people for preparing pursuits accumulated more support (Jacobs-Lawson and Hershey 2005).

According to the theory of planned behavior (TPB), the intention is its crucial concept intended to influence a specified behavior because it signifies how eager people are to execute the achievement (Ajzen 1991). Conduct such as reserving money is not under eager supervision as the readiness of chances and capital influences the ability to implement the behavior (Ajzen 1991). Besides, circumstantial factors (ethnicity, society, family, and occupation situation), unique variances (enthusiasm, participation, acquaintance, manners, character, way of life, and demographics), and psychological process aspects (information handing, acquiring) are linked to people’s readiness and capacity to save for their pension (Joo and Grable 2005). Somebody might pursue a particular behavior or deed if the behavior leads toward a specific result. They might believes it reasonable if the they have faith in people and consider it proper and if the person has the source and chance to implement the behavior.

Financial literacy is one of the psychological constructs which has an extensive impact on awareness of saving sources, as people necessitate more literacy regarding pension saving and investment schemes to protect a sound retirement existence (Jacobs-Lawson and Hershey 2005). Knowledge-based arranging is related to developing the efficacy of preparing and decreasing the unpredictability of the program’s quality (Faught et al. 2018; Wahyuni et al. 2022). It has been stated as a proxy compilation of financial data found and accumulated regularly (Lim et al. 2018). Yoong et al. (2012) indicated that by improving a person’s literacy, the emotional capacity to foresee the impacts of deeds might also increase. Financial literacy can help people create financial options cost-effectively (Sabri and Juen 2014). Financially well-educated people comprehend the substance of retirement planning and are inclined to better plan for their pension, as they commonly gather assets for pension preparation. Therefore, persons who have an excellent education in financial planning will identify how to plan suitably for their retirement, which affects the outcome of acceptable saving strategies.

There are aspects with significant correlations between retirement planning and the ability to have good saving behavior for their retirement years (Hassan et al. 2016; Yap et al. 2017). Reserving adequate money in one’s savings account can preserve living standards during the pension period. People are estimated to remain employed and formulate an added provision in working-age years (Suh 2021). Some can forestall saving strategies and adopt a lower level of pension saving for the duration of their living course based on the prior generation’s experience. For example, the baby boomer generation gathered extensive private pensions and housing prosperity, which significantly impacted their financial comfort in pensions (Hills and Bastagli 2013). Post-pension data indicate that people who participated in planning conduct accumulated more prosperity (Hershey et al. 2013). Satisfactory assurance in present pension savings can encourage some people to save more for retirement, and, consecutively, saving more can raise the degree of certainty on existing savings growth. Based on the explanation above, the objective of this study was to find out whether the saving behavior of medium-sized entrepreneurs to be considered as a mediating variable that connects the effect of financial literacy retirement planning, in accordance with the results of previous studies, including those by Beckmann (2013) and Zazili et al. (2017). Thus, we posit the following hypothesis:

Hypothesis 3.

Saving behavior mediates the relationship between financial literacy and retirement planning.

2.6. Serial Mediation Effect of Financial Risk Tolerance and Saving Behavior on the Relationship between Financial Literacy and Retirement Planning

Financial literacy improves people’s capability to assess their risks and comprehend information considering the financial instruments they use (Van Rooij et al. 2012). As argued in the prior literature, better knowledge has been linked with risk tolerance. It mediates the relationship between knowledge and risk tolerance (Yao et al. 2005; Grable 2008) and links financial literacy and educational accomplishment with wealth buildup and arranging behavior (Lusardi and Mitchell 2007; Chatterjee and Zahirovic-Herbert 2010; Wahyuni et al. 2021) in prior literature. Furthermore, financial risk tolerance can predict an individual’s intention to save in preparing financial buffers, such as the need for emergency funds, pension funds, and investments for future needs. A good understanding of financial risk tolerance will be able to direct an individual on whether to save in stocks or not (Yao and Curl 2011).

Individuals who have saving behavior that is driven by future interests will be very helpful in the process of accumulating pension fund assets. Therefore, a study stated that saving behavior has a positive and significant influence on retirement planning (Zazili et al. 2017; Nguyen et al. 2017). Moreover, individuals can calculate that the burden of living in the future will be greater than the current cost of living due to the inflation factor. When approaching retirement age, an individual’s income will also decrease. Therefore, an increase in the cost of living and a decrease in income before retirement age contributes to the increasing burden of dependents in terms of living costs when entering retirement age (Khan et al. 2017). Based on the explanation above, the objective of this study was to find out whether financial risk tolerance and saving behavior of medium-sized entrepreneurs should be considered as serial mediating factors that connect the effect of financial literacy to retirement planning in accordance with the results of previous research, such as that by Heenkenda (2014), Chatterjee et al. (2017), and Zazili et al. (2017). Thus, we posit the following hypothesis:

Hypothesis 4.

Financial risk tolerance and saving behavior mediate the relationship between financial literacy and retirement planning.

2.7. Moderating Role of Herding Behavior on the Relationship between Financial Literacy and Retirement Planning

Financial literacy is a skill related to investing effectively and providing optimal returns (Giesler and Veresiu 2014). Investors with high financial literacy tend to engage in irrational behavior less than other people (Disney and Gathergood 2013). Consequently, these investors apply the right method when making investment decisions (Al-Tamimi and Kalli 2009). They disregard imprecise information and only consider procedure-appropriate information during investment scrutiny (Jain et al. 2015). Hayat and Anwar (2016) argued that financial literacy impacts investors’ risk-taker capability because financial literacy provides several approaches to mitigate difficult circumstances (Almenberg and Säve-Söderbergh 2011). For people who have poor financial literacy with respect to financial decision-making, it is not optimal, for the role of herding behavior can help the level of individual financial literacy through input and guidance from other individuals (Disney and Gathergood 2013; Kim and Petrick 2021). Then, financial literacy encourages investors to improve their decision-making abilities by properly handling and analyzing information that indirectly influences herding behavior (Hayat and Anwar 2016). Based on the explanation above, the objective of this study was to find out whether the herding behavior of medium-sized entrepreneurs should be considered as a moderator that strengthens the influence of financial literacy on retirement planning in accordance with the results of previous research, such as that by Choi and Yoon (2020). Thus, we posit the following hypothesis:

Hypothesis 5.

Herding behavior moderates the relationship between the financial literacy and retirement planning.

3. Methodology

3.1. Sample and Data Collection

The reason for choosing medium entrepreneur respondents is that medium entrepreneurs significantly contribute to Indonesia’s gross domestic product (GDP), estimated at around 61.07% in 2021. They comprise a workforce of around 3.8 million people. Hence, their contribution has a significant impact on the Indonesian economy. Due to their vast contribution, it is necessary to consider how their condition in retirement will remain prosperous through retirement planning. Besides that, medium-sized entrepreneurs have a relatively larger capital capacity compared with micro and small entrepreneurs; therefore, they have the flexibility to reserve cash for retirement planning. Furthermore, the medium-sized entrepreneurs are engaged in trading household needs, agricultural products, restaurants, and hotels, and this group is the largest group of medium-sized entrepreneurs in Bekasi Regency.

The population of this study comprised medium-sized business persons who carry out and have domiciles/places of business in the Bekasi City area, West Java Province, Indonesia Country. The population in this study comprised 11,438 medium business actors based on data from the Ministry of Cooperatives and SMEs. The respondents used were medium-sized business persons who have their place of business in Bekasi City. The respondents were selected because the perpetrators already had company registration certificates and a trading business licenses registered at the Bekasi City Investment and One-Stop Integrated Service Office. The assortment of an entire amount of 838 personal medium entrepreneurs was composed, and a survey questionnaire was applied for the data compilation. Of the 838, only 409 questionnaires were returned (48.80% response rate). Of the 409 questionnaires, 21 survey questionnaires were unfinished and were eliminated, leading to 388 questionnaires being applied in the data analysis (46.30% actual response rate).

The financial literacy data measurement results showed that respondents had an average score of 4.04. This indicates that respondents generally have a good score on financial literacy. The indicator of the compound interest concept had the highest value of 4.11, and the lowest value was the understanding of inflation of 4.02. Furthermore, the measurements of financial risk tolerance data showed that respondents scored an average value of 4.06 and generally have a good score on financial risk tolerance. The indicator of daring to take a higher risk was the highest indicator at 4.10, and borrowing cash for investment was the lowest at 4.01.

The measurement of saving behavior data results showed that the respondents had an average value of 4.05. This indicates that the respondents generally have an excellent score regarding saving behavior. The indicator for saving for emergency funds was the highest indicator at 4.14, and the indicator for saving was the lowest at 4.01. Furthermore, the measurement of herding behavior data showed that the respondents had an average value of 4.07. This indicates that the respondents generally have an excellent score regarding herding behavior. The indicator following the investment decisions of other entrepreneurs was the highest indicator, which was 4.15, and the indicator for many successful entrepreneurs in making retirement planning was the lowest, which was 4.01.

The summary of data statistics (mean and standard deviation) is as follows. (a) Financial literacy: mean = 4.04 and standard deviation = 1.05; (b) financial risk tolerance: mean = 4.06 and standard deviation = 1,04; (c) saving behavior: mean = 4.05 and standard deviation = 0.99; (d) herding behavior: mean = 4.07 and standard deviation = 1.02; and (e) retirement planning: mean = 4.07 and standard deviation = 1.02.

Table 1 recapitulates the most important data and attributes of the sample. Of the 388 entrepreneurs who fulfilled the survey, the classification by attributes revealed, by gender, 296 men (76.78%); by education background, 73.19% had at least a bachelor’s degree; and by business sectors, section consumer goods (60.82%). Most entrepreneurs who answered (44.07%) had been in their business tenure more than ten years and had annual income sales lower than IDR 15 billion (69.33%).

Table 1.

The respondent profiles.

3.2. Measurement Items

This research formed and embraced constructs determined and adjusted from the existent literature. The authors identified four constructs based on the literature evaluation (financial literacy, financial risk tolerance, saving behavior, and herding behavior) influencing retirement planning. For example, respondents were requested to declare the substance of financial literacy to increase their retirement planning, utilizing a five-point scale, from “Strongly disagree” (1) to “strongly agree” (5).

Financial literacy was formed by four items, namely: I have the knowledge to calculate compound interest; I have the knowledge to understand insurance unit-link; I have the knowledge to understand diversification risk of investment portfolios; I have the knowledge to understand inflation level (Lusardi and Mitchell 2011; Larisa et al. 2020). Financial risk tolerance was formed by five items, namely: I am ready to bear the risk of every investment allocated; I dare to take a risk on every investment allocated; I put all my investments in fluctuating instruments; I allocate investment funds sourced from third party loans; I still consistently make investment funds even though there is a very significant decline in investment value (Hermansson and Jonsson 2021; Chatterjee et al. 2017).

Saving behavior was formed by six items, namely: I save when income is greater than consumption; I make meaningful financial contributions to my voluntary retirement savings plan; I save my rest of income to mitigate inflation; I keep accumulated substantial savings for retirement; I make a conscious effort to save for retirement; I am saving for an emergency reserve (Alkhawaja and Albaity 2020). Herding behavior was formed by five items, namely: I plan my retirement finances because of the influence of other entrepreneurs who live prosperously; I plan my retirement finances because of input from other entrepreneurs; I plan my retirement finances based on input from social media information; I plan my retirement finances because I follow the investment decisions of other entrepreneurs; I plan my retirement finances because other entrepreneurs have been involved in other retirement plans (Kim and Petrick 2021; Kumari et al. 2019).

Retirement planning was formed by seven items, namely: I visit financial planning sites to increase my knowledge about old age financial planning; I identify plan income and expenses in old age; I often coordinate related to retirement plans with financial planning consultants; I have a special savings fund for old age need; I have an asset or property to rent/sell for old age needs; I invest in the capital market for old age needs; I have life insurance that can be claimed after a certain age (Suh 2021).

4. Data Analysis and Results

To understand the direct and indirect impact of financial literacy on retirement planning with the mediating influence of financial risk tolerance and saving behavior also the moderation effect of herding behavior on SMEs in Indonesia, the PLS-SEM (Partial Least Squares–Structural Equation Modeling) was used for analysis to evaluate the overall measurement model.

4.1. Measurement Model

Convergent validity was confirmed. We evaluated convergent validity by assessing loading factors that must be higher than 0.7, composite reliabilities higher than 0.8, and the average extracted variance (AVE) higher than 0.5 for all variables (Fornell and Larcker 1981). Based on the test results of convergent validity, it was confirmed that some loading factor values met the requirements for the model test in the study and the rest were lower than 0.7. By Cronbach α, we verified the scales of internal reliability. Table 2 shows the loading factor, AVE, CR, and (C-α) of all variables.

Table 2.

Convergent validity.

This new proposed method was implemented to examine the discriminant validity through the Heterotrait–Monotrait ratio of correlations (HTMT) where the HTMT must be lower than 0.90 (Gold et al. 2001). All constructs in this model were concluded to be adequate for discriminant validity and are portrayed in Table 3. The measurement of goodness-of-fit model was revealed to be satisfactory (Standardized Root Mean Square Residual (SRMR) = 0.071, and Normal Fit Index (NFI) = 0.928) and verified the planned model because of SRMR value <0.08 and NFI value >0.9 (Henseler et al. 2015). Conclusively, we postulate that the framework provided satisfactory data and thus was adequate to examine the hypothesis for the research.

Table 3.

Discriminant validity.

4.2. Hypothesis Testing

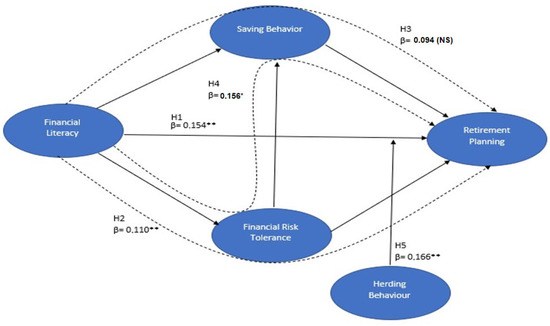

The study evaluated the structural links among the variables by examining the mediator effects that were utilized to examine hypotheses in the conceptual model. The research shown in Table 4 reveals the coefficients of the study model. Table 4 and Figure 2 describe that the path coefficients from financial literacy to retirement planning were positive and significant (ß = 0.154; p value < 0.05), while the indirect relationship of financial literacy on retirement planning through financial risk tolerance as a mediator was positively significant (ß = 0.110, p < 0.05). Therefore, H1 and H2 are supported. Conversely, the indirect relationship of financial literacy on retirement planning through saving behavior as a mediator was positive and non-significant (ß = 0.117, p < 0.05). Therefore, is not supported. Moreover, the indirect relationship of financial literacy on retirement planning through financial risk tolerance and saving behavior as a mediator was positively significant (ß = 0.156, p < 0.01). Therefore, is supported. Based on the abovementioned results, we can determine that financial risk tolerance fully mediates the relationship between financial literacy and retirement planning. Thus, there are joint mediators, which are financial risk tolerance and saving behavior, which bridge the gap between financial literacy and retirement planning. Finally, herding behavior as a moderator strengthens the relationship between financial literacy and retirement planning (ß = 0.166, p < 0.05).

Table 4.

Hypothesis testing.

Figure 2.

Analysis results (* p value < 0.01; ** p value < 0.05; NS: Not Significant; ----: indirect effect).

The research data were obtained by distributing questionnaires to 388 selected respondents. The quantitative data were obtained and selected through reliability and validity tests. The selected data were then processed using the SEM-PLS application to measure the influence between variables.

5. Discussion

The outcomes of this research support the findings of (Robb and Woodyard 2011; Hassan et al. 2016; Lusardi et al. 2017; and Larisa et al. 2020), which revealed that financial literacy has a significant impact on financial planning in the retirement period. With higher financial literacy, retirement planning will be more optimal because individuals will have more alternative financial instruments, simpler financial management, and better risk management to obtain good returns. Concerning financial planning activities for old age, the findings showed that respondents tended to prepare pension funds in the form of unit link insurance products because insurance money can cover the needs of their families in old age. In addition, the type of unit link insurance has many variations of placement of investment funds, such as in the form of equity (stocks), money market, and fixed and mixed income and (combination of shares, money market, or fixed income). It is easier for entrepreneurs to adjust to their future financial needs. Investing in unit-linked insurance products is an investment that can be an alternative in planning a retirement fund. This is in line with the fact that investing in unit links is a retirement planning endeavor that many entrepreneurs have carried out. Regarded the measurement of financial literacy, it can be seen that financial knowledge related to unit link investment is a financial product that was already familiar to them. The optimal old-age financial planning may be caused by the high financial literacy, especially related to investment. By good financial literacy, they must select the most suitable investment facilities to prepare for their old age finances, which are included in long-term financial planning. Therefore, high financial literacy of entrepreneurs can help financial planning in the retirement period become more optimal because entrepreneurs understand financial products such as unit links and the calculation of the value of investment returns such as income interest rates. Financial literacy is the level of an individual’s ability to make decisions related to finance; therefore, the higher the level of financial literacy of an individual, the greater their ability to participate in financial planning for the future, in this case, retirement planning. For example, a person who has a bachelor’s degree in finance will know how to invest in retirement savings and how to calculate future financial needs, and then they are encouraged to participate in retirement planning by open retirement savings consisting of a portfolio of assets such as equity, bonds, or cash. Financial needs in their retirements can become more prosperous because of the available assets (Lusardi et al. 2017; Larisa et al. 2020).

The results of empirical research data from the hypothesis state that financial literacy indirectly impacts financial retirement planning through the mediation of financial risk tolerance. The high financial literacy of entrepreneurs seeks to obtain optimal investment returns by placing investment funds with risk characteristics of asset values experiencing volatility, such as unit links, mutual funds, or forex (Chatterjee et al. 2017; Kulathunga et al. 2020; Ariadi et al. 2020). Thus, a higher prevalence of financial knowledge will help entrepreneurs develop investment fund placements with high risk because they are ready to bear investment losses in the future. As a result, entrepreneurs with higher financial literacy can accept the risk of a decline in investment value because they believe that investments in products such as unit links and mutual funds will rebound at a certain momentum. When entrepreneurs have sufficient knowledge to estimate market risk and credit risk from the expected returns from placing investment funds, they tend to view the decision from the perspective of retaining profits and, therefore, show an inclination toward risk-taking. Prior studies have determined which persons are willing to take risks considering investment volatility with a good capability to manage and recognize financial knowledge and the risk circumstances (Nguyen et al. 2019). Risk tolerance can aid an individual in recognizing the degree of risk from an investment and aid a person in allowing and aligning the existent risks to match the investment with the aim of the risk. Someone is eager to agree with the level of return recorded and obtained in the future. Thus, entrepreneurs have a greater-risk tolerance, so they are eager to tolerate the risk of loss from investment because the investment delivers a chance to provide a good level of gain. If entrepreneurs are risk-averse, they may attempt as much as conceivable to reduce the risk, and they prefer to assign their assets to low-risk investments. They will adjust the type of investment chosen based on the their tolerance for risk. The results of this study support the findings of Chatterjee et al., 2017, Kulathunga et al., 2020, and Nguyen et al., 2019, which reveal that financial literacy has a significant impact on financial risk tolerance.

The characteristics of entrepreneurs are more likely to be aggressive in tolerating high risk because they have confidence in the ability of their investment portfolio. Thus, there is a willingness to take big risks in optimizing the return on the principal investment. In the context of obtaining maximum returns, the investment portfolio of entrepreneurs will change regularly as there are efforts to continuously develop investment options with the highest returns in the portfolio. Entrepreneurs with a high risk tolerance tend to have a higher risk profile where the investment options placed have unstable investment value volatility. They provide a great opportunity for entrepreneurs to make optimal profits in the context of financial preparation in their old age. On the other hand, when investment tends to decline, entrepreneurs cut losses with a certain threshold level and then divert them to re-investment in other financial products that have better returns in covering losses from their previous investments. They try to increase their income optimally and sustainably even though the investment risk they face is very high. Some entrepreneurs try to keep their funds from being idle, where the source of funding entrepreneurs comes from bank loans or profits from their investment placements. Thus, the higher the financial risk tolerance, the more diversified business activities are ready to support daily operational activities, even though some productive assets experience a decline or loss. The results of this study support the findings by (Larisa et al. 2020; Chatterjee et al. 2017; Nguyen et al. 2019; Aeknarajindawat 2020; Rahman et al. 2019), which show that financial risk tolerance has a significant effect on retirement planning. The higher the financial risk tolerance of the entrepreneur, the more mature financial planning will be in their old age. Financial risk tolerance will lead them to be concerned with their own risk profile, an understanding owhich will open their mind regarding their future situations; referring to the prospect theory, if the future is estimated as risky, then people will tend to prepare savings today in the high-risk investment products and vice versa. For example, Mr. A has a high-risk profile, so the choice of investment products is more on stock and derivative products, while if Mr. A has a low-risk profile, the choice of retirement savings products is more on bond investment products and bank deposits.

The results of empirical data research from the hypothesis state that financial literacy does not indirectly influence financial retirement planning through the mediation of saving behavior. Most entrepreneurs tend to focus more on their business needs. The remaining profits are more focused on purchasing raw materials or business capital rather than being used for saving. For this reason, entrepreneurs with good financial knowledge are more likely to optimize cash flow from their business activities to anticipate uncertain business conditions than for personal needs in the future (Alkhawaja and Albaity 2020; Hauff et al. 2020; Suh 2021; Ariadi et al. 2021). For example, entrepreneurs with high knowledge are more likely to turn their business profits into working capital, such as purchasing products for their business activities. It is based on the value of the inflation rate in Indonesia, which is almost close to the interest rate on bank deposits, so entrepreneurs are more likely to pursue profits from their business higher than the inflation rate. Thus, individuals who have high financial literacy are more likely to turn their funds around for their business activities when compared with investing in savings assets for their old age. They believe that their business will provide regular income results (Van Rooij et al. 2011).

Conversely, entrepreneurs’ high level of saving behavior provides a great opportunity to increase the certainty of relatively stable welfare, or future income receipts that are relatively the same as their current income. Entrepreneurs always project future business income related to the context of saving behavior. They try to prepare funding reserves in productive assets such as new business units, receivable accounts, mutual funds, or unit links. To overcome the uncertainty of business sales that can impact the income of entrepreneurs, a precautionary fund can help entrepreneurs synchronize their income from their business in preparing for their financial needs in their old age while maintaining the liquidity of the cash flow of business operations. For this reason, greater the funds collected by entrepreneurs can improve their welfare in their old age, even though there is a decline in their business activities. In addition, entrepreneurs seek to increase their income optimally and sustainably, so they try to set aside a small portion of their income for emergency funds and special needs funds. Then, entrepreneurs have many opportunities to increase their savings, which has been indirectly implemented in their daily operational activities. This study’s results support the findings of (Anderson et al. 2017; Koe and Yeoh 2021; Graf 2017; Ventura and Horioka 2020), which show that saving behavior has a significant effect on financial retirement planning.

The results of empirical data research state that higher financial risk tolerance can increase saving behavior in medium-scale entrepreneurs. Therefore, the financial risk tolerance of entrepreneurs is oriented to the readiness to bear losses in the event of a decrease in the value of their investment or business activities and dare to take many risks in improving financial performance, especially returns on business profits. The saving behavior of entrepreneurs is oriented towards preparing emergency funds that are used to maintain business liquidity so that it runs smoothly and cash flow can be used for purchasing raw materials or business capital and saving funds for special purposes in the form of capital reserves to develop sustainable business activities, as well as a buffer if there is a loss to the business. For this reason, entrepreneurs who have a high financial risk tolerance tend to have a high intensity of saving (Alkhawaja and Albaity 2020; Larson et al. 2016; Parker et al. 2012). Characteristics of entrepreneurs are very open to tolerating a decline in investment due to market risk and credit risk, so they try to mitigate the risk of loss by allocating reserve funds for emergency activities (force majeure) and special reserve funds. Thus, entrepreneurs generally prepare capital in the form of retained earnings accumulated from previous financial years, and at the same time, they also obtain a salary every month. In the context of monthly salary income, SMEs tend to put their salary results into current receivable accounts because they are trying to increase sales turnover, and payments are mostly in the form of receivable accounts. This provides a great opportunity for entrepreneurs to obtain optimal profits, and then they are placed into several liquid financial instrument products. Entrepreneurs’ fund storage activities are aimed at precautionary funds where the pool of funds will be allocated to prepare for their financial retirement planning. Then, the greater the saving of funds collected by entrepreneurs can improve their welfare in their old age even though there is a decline in their business activities. The results of this study constitute a novelty in that joint mediators such as financial risk tolerance and saving behavior have an indirectly significant effect on financial literacy on retirement planning.

The results of empirical data research are based on the hypothesis that financial literacy affects retirement planning which is moderated by herding behavior in medium-scale entrepreneurs. It is due to the ability of financial literacy to focus on knowledge of compound interest calculations in the form of profit margin percentages and risk premiums and knowledge of unit link insurance products. It is related to the financial planning of entrepreneurs through productive assets that generate passive income or ownership of special properties. Furthermore, herding behavior is more oriented toward preparing financial retirement planning for entrepreneurs, which is influenced by factors such as following investment decisions from other entrepreneurs, encouraging input from other entrepreneurs, and seeing other entrepreneurs who have lived prosperously. Thus, herding behavior strengthens the relationship between the high financial literacy of entrepreneurs in improving their financial planning in old age to be more optimal (Kim and Petrick 2021; Chan et al. 2020; Clauss et al. 2018). The readiness for future financial plans from entrepreneurs can be motivated and encouraged by other fellow entrepreneurs in preparing retirement planning. The role of herding behavior can facilitate and strengthen entrepreneurs’ confidence and reinforce determining the types of investments that are influenced by the level of financial knowledge of everyone. It shows that entrepreneurs have prepared financial planning in their old age with financial products whose yields are already above the central bank’s interest rate. The role of herding behavior can strengthen the choice of investment products with higher profits, such as unit link insurance, cryptocurrency in the form of bitcoin, or investment in future products such as gold, whose transactions use information technology. Encouragement and input from colleagues, other entrepreneurs, and information from social media influence people to decide to improve long-term investment performance, despite the high market risk volatility due to the decline in the value of unit link insurance, bitcoin, or gold.

6. Theoretical and Managerial Implications

The results of this study support the consistency and strengthening of the prospect theory in this research model. Financial risk tolerance is positioned as a mediator; this becomes a new model construct responding to the inconsistency of research gaps from the link between financial literacy and retirement planning. The novelty of this research is that financial risk tolerance partially mediates the indirect impact of financial literacy on financial retirement planning from the perspective of prospect theory. In addition, many previous research studies have found that financial literacy improves financial investment decisions in old age. However, none have investigated the indirect effect of financial risk tolerance on the relationship of financial literacy to financial retirement planning from a risk-taker perspective. Another novelty is the development of financial risk tolerance from a risk-taker perspective. The indicators use borrowed funds from third parties to increase investment value and dare to bear the burden of losses that arise if there is a decrease in investment value.

Furthermore, herding behavior is positioned as a moderator. It becomes a new model construct responding to the inconsistency of research gaps in the relationship between financial literacy and retirement planning. The novelty of this study is that herding behavior can strengthen the indirect effect of financial literacy on financial planning in old age from the perspective of the theory of planned behavior (TPB). It is based on the TPB theory, which states that entrepreneurs have the intention to follow certain actions if they feel they have support from the surrounding environment to follow the behavior (Ajzen 1991). In this context, entrepreneurs’ financial literacy greatly determines the preparation of financial planning in their old age, where the determination of the allocation of investment funds is encouraged by other fellow entrepreneurs. For this reason, financial planning decisions are usually more rational in placing investment products. However, the role of herding behavior can strengthen and convince entrepreneurs to allocate their funds to products with very high yields. Metawa et al. (2018) constructed a similar implication in the Egypt Stock Exchange regarding herd behavior as a mediator which bridges the relationship between educational level and investor decision.

The interesting finding is that the mediation analysis method is flexible with multiple mediators. It confirms and is consistent with the findings of Steen et al. (2017), which stated that the joint mediator approach can flexibly estimate the effect of each component and derive sufficient conditions for the identification of model tests. This research model showed financial risk tolerance and saving behavior as joint mediators where the two mediating variables were sequential in influencing financial retirement planning. For example, financial literacy is positioned as an antecedent, which affects financial risk tolerance as the first mediation, then continues to affect saving behavior as a second mediation which increases the preparation of financial planning for old age as a consequent variable. The combination of the first and second mediation is called a joint mediator, which forms a continuous mediator (sequential mediation). Alkhawaja and Albaity (2020) proposed a matching contribution of financial risk tolerance and knowledge of financial planning for retirement which directly influences retirement saving behavior. In contrast, there is a sequential mediation between financial literacy and retirement planning in this research. Based on the theoretical implications above, it was known that the variables in this research model strengthen and support the synergy between the prospect theory and the theory of planned behavior.

From a practical point of view, a greater level of financial risk tolerance has a big influence in preparing entrepreneurs’ retirement financial planning compared with saving behavior. It shows the character of entrepreneurs who tend to take high risks associated with receiving high investment returns. Entrepreneurs already understand the burden of losses that arise from any financial investments made, but they can tolerate the threshold for losses from these investments. Entrepreneurs try to limit existing losses and then reinvest in other products to cover previous losses and provide a surplus of investment profits. Entrepreneurs always calculate the profits and losses from these investments within a certain period, for example, one year or more, to have an optimistic attitude and high expectations in the financial investment process, especially in the financial retirement planning in their old age. Moreover, herding behavior can strengthen the decision to prepare for financial retirement planning from entrepreneurs where high financial literacy provides objective analysis results related to investment returns from financial products. Good financial knowledge from entrepreneurs provides rational decisions related to allocating investment funds to be placed. On the other hand, the herding behavior factor strengthens entrepreneurs to place investment funds in their old age where input and referrals from other business partners provide investment alternatives in other financial products.

7. Conclusions and limitations

This research’s results have provided some suggestively valuable pieces of confirmation of financial literacy to improve financial retirement planning for the medium entrepreneurs in Bekasi Regency, Indonesia. However, saving behavior does not mediate the relationship between financial literacy and retirement planning. Then, the research proposes that financial risk tolerance mediates the link between financial literacy and retirement planning. However, constructing a joint mediator as financial risk tolerance and saving behavior in this conceptual model indirectly significantly affects the linkage of financial literacy to retirement planning. The interesting result was the moderating of herding behavior, which strengthens the relationship between financial literacy and retirement planning. Overall, the impact of herding behavior as a moderating variable had a greater influence than financial risk tolerance and saving behavior as a joint mediator, which is related to the link between financial literacy toward retirement planning.

There are limits to this study which inspire some upcoming research suggestions. The analysis employed a cross-sectional scheme that comprised a longitudinal experiment for the following study to scrutinize the effects of financial literacy on financial risk tolerance and saving behavior that improves financial retirement planning. Finally, this research was performed on a single business sector and entrepreneur scale. It would be attractive and valuable to collect data from various business sectors and small entrepreneurs to comprise a greater substantiation of outcomes.

Author Contributions

Conceptualization, S.H., A.T., S.S. and A.D..; methodology, S.H., A.T., S.S. and A.D.; software, S.H., A.T., S.S. and A.D.; validation, S.H., A.T., S.S. and A.D.; formal analysis, S.H., A.T., S.S. and A.D.; investigation, S.H., A.T., S.S. and A.D.; resources, S.H., A.T., S.S. and A.D.; data curation, S.H., A.T., S.S. and A.D.; writing—original draft preparation, S.H.,; writing—review and editing, S.H., A.T., S.S. and A.D.; visualization, S.H., A.T., S.S. and A.D.; supervision, S.H., A.T., S.S. and A.D.; project administration, S.H.; funding acquisition, S.H. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

The datasets generated during and/or analysed during the current study are available from the corresponding author on reasonable request.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Abrahamse, Wokje, and Linda Steg. 2009. How So Socio-Demographic and Psychological Factors Relate to Households’ Direct and Indirect Use of Energy and Savings? Journal of Economic Psychology 30: 711–20. [Google Scholar] [CrossRef]

- Aeknarajindawat, Natnaporn. 2020. The combined effect of risk perception and risk tolerance on the investment decision making. Journal of Security & Sustainability Issues 9: 807–18. [Google Scholar]

- Agnew, Julie Richardson, Hazel Bateman, and Susan Thorp. 2012. Financial Literacy and Retirement Planning in Australian. UNSW Australian School of Business Research Paper 2012ACTL16. Amsterdam: Elsevier. [Google Scholar]

- Ajzen, Icek. 1991. The theory of planned behavior. Organizational Behavior and Human Decision Processes 50: 179–211. [Google Scholar] [CrossRef]

- Alkhawaja, Sara Osama, and Mohamed Albaity. 2020. Retirement saving behavior: Evidence from UAE. Journal of Islamic Marketing 13: 265–86. [Google Scholar] [CrossRef]

- Almenberg, Johan, and Jenny Säve-Söderbergh. 2011. Financial literacy and retirement planning in Sweden. Journal of Pension Economics & Finance 10: 585–98. [Google Scholar]

- Al-Tamimi, Hussein Al Hassan, and Al Anood Bin Kalli. 2009. Financial literacy and investment Decisions of UAE investors. Journal of Risk Finance 10: 500–16. [Google Scholar] [CrossRef]

- Altman, Morris. 2012. Implications of behavioural economics for financial literacy and public policy. The Journal of Socio-Economics 41: 677–90. [Google Scholar] [CrossRef]

- Aluodi, Emma, Amos Njuguna, and Bernard Omboi. 2017. Effect of Financial Literacy on Retirement Preparedness among Employees in the Insurance Sector in Kenya. Nairobi: United States International University Africa. [Google Scholar]

- Amirio, Dylan. 2015. RI’s Financial Literacy Remains among Lowest in Asia. Retrieved from The Jakarta Post Website. Available online: http://www.thejakartapost.com/news/2015/09/04/ri-s-financial-literacy-remains-among-lowest-asia.html (accessed on 4 September 2015).

- Anderson, Anders, Forst Baker, and David T. Robinson. 2017. Precautionary savings, retirement planning and misperceptions of financial literacy. Journal of Financial Economics 126: 383–98. [Google Scholar] [CrossRef]

- Ariadi, Gede, Surachman Sumiati, and Fathur Rohman. 2020. The effect of strategic external integration on financial performance with mediating role of manufacturing flexibility: Evidence from bottled drinking industry in Indonesia. Management Science Letters 10: 3495–506. [Google Scholar] [CrossRef]

- Ariadi, Gede, Surachman Sumiati, and F. Rohman. 2021. The effect of lean and agile supply chain strategy on financial performance with mediating of strategic supplier integration & strategic customer integration: Evidence from bottled drinking-water industry in Indonesia. Cogent Business & Management 8: 1930500. [Google Scholar] [CrossRef]

- Baskoro, Rahmat Aryo, and Rensi Aulia. 2019. The Effect of Financial Literacy and Financial Inclusion on Retirement Planning. International Journal of Business Economics 1: 49–58. [Google Scholar] [CrossRef]

- Beckmann, Elisabeth. 2013. Numeracy Advancing Education in Quantitative Literacy Financial Literacy and Household Savings in Romania Financial Literacy and Household Savings in Romania. Numeracy 6: 1–24. [Google Scholar] [CrossRef]

- Boisclair, David, Annamaria Lusardi, and Pierre Carl Michaud. 2017. Financial literacy and retirement planning in Canada. Journal of Pension Economics & Finance 16: 277–96. [Google Scholar]

- Bucher-Koenen, Tabea, and Annamaria Lusardi. 2011. Financial literacy and retirement planning in Germany. Journal of Pension Economics & Finance 10: 565–84. [Google Scholar]

- Chan, C. S. Ricard, Annaleena Parhankangas, Arvin Sahaym, and Pyayt Oo. 2020. Bellwether and the herd? Unpacking the u-shaped relationship between prior funding and subsequent contributions in reward-based crowdfunding. Journal of Business Venturing 35: 105934. [Google Scholar] [CrossRef]

- Chatterjee, Swarn, and Velma Zahirovic-Herbert. 2010. Retirement planning of younger baby-boomers: Who wants financial advice? Financial Decisions 22: 1–12. [Google Scholar]

- Chatterjee, Swarn, Fan Lu, Jacobs Ben, and Haas Robin. 2017. Risk Tolerance and Goals-based Savings Behavior of Households: The Role of Financial Literacy. Journal of Personal Finance 16: 66–77. [Google Scholar]

- Choi, Ki Hong, and Seong-Min Yoon. 2020. Investor Sentiment and Herding Behavior in the Korean Stock Market. International Journal of Financial Studies 8: 34. [Google Scholar] [CrossRef]

- Clauss, Thomas, Robert J. Breitenecker, Sascha Kraus, Alexander Brem, and Chris Richter. 2018. Directing the wisdom of the crowd: The importance of social interaction among founders and the crowd during crowdfunding campaigns. Economics of Innovation and New Technology 27: 709–29. [Google Scholar] [CrossRef]

- Crossan, Diana, David Feslier, and Roger Hurnard. 2011. Financial literacy and retirement planning in New Zealand. Journal of Pension Economics & Finance 10: 619–35. [Google Scholar]

- Disney, Richard, and John Gathergood. 2013. Financial literacy and consumer credit portfolios. Journal of Banking & Finance 37: 2246–54. [Google Scholar]

- Dohmen, Thomas, Armin Falk, David Huffman, Uwe Sunde, Jurgen Schupp, and Gert G. Wagner. 2011. Individual risk attitudes: Measurement, determinants, and behavioral consequences. Journal of the European Economic Association 9: 522–50. [Google Scholar] [CrossRef]

- Duckworth, Angela, Peterson Christopher, Michael D. Matthews, and Dennis R. Kelly. 2007. Grit: Perseverance and passion for long-term goals. Journal of Personality and Social Psychology 92: 1087–1101. [Google Scholar] [CrossRef] [PubMed]

- Faff, Robert, Daniel Mulino, and Daniel Chai. 2008. On the linkage between financial risk tolerance and risk aversion. Journal of Financial Research 31: 1–23. [Google Scholar] [CrossRef]

- Farrar, Sue, Jonathan Moizer, Jonathan Lean, and Mark Hyde. 2019. Gender, financial literacy, and preretirement planning in the UK. Journal of Women and Aging 31: 319–39. [Google Scholar] [CrossRef] [PubMed]

- Faught, Austin M., Olsen Lindsey Schubert, Chad Rusthoven, Edward Castillo, Richard Castillo, Jingjing Zhang, Thomas Guerrero, Moyed Miften, and Yevgeniy Vinogradskiy. 2018. Functional-guided radiotherapy using knowledge-based planning. Radiotherapy and Oncology 129: 494–8. [Google Scholar] [CrossRef]

- Fornell, Clae, and David F. Larcker. 1981. Evaluating structural equation models with unobservable variables and measurement error. Journal of Marketing Research 18: 39–50. [Google Scholar] [CrossRef]

- Giesler, Markus, and Ela Veresiu. 2014. Creating the responsible consumer: Moralistic governance regimes and consumer subjectivity. Journal of Consumer Research 41: 840–57. [Google Scholar] [CrossRef]

- Gold, Andrew H., Arvind Malhotra, and Albert H. Segars. 2001. Knowledge management: An organizational capabilities perspective. Journal of Management Information Systems 18: 185–214. [Google Scholar] [CrossRef]

- Grable, John. E. 2008. Risk tolerance. In Handbook of Consumer Finance Research. New York: Springer, pp. 3–19. [Google Scholar] [CrossRef]

- Graf, Stefan. 2017. Life-cycle funds: Much ado about nothing? The European Journal of Finance 23: 974–98. [Google Scholar] [CrossRef]

- Griffin, Barbara, Hesketh Beryl, and Loh Vanessa. 2012. The influence of subjective life expectancy on retirement transition and planning: A longitudinal study. Journal of Vocational Behavior 81: 129–37. [Google Scholar] [CrossRef]

- Gunnarsson, Jonas, and Richard Wahlund. 1997. Household financial strategies in Sweden: An exploratory study. Journal of Economic Psychology 18: 201–33. [Google Scholar] [CrossRef]

- Gustafsson, Carina, and Lisa Omark. 2015. Financial Literacy’s Effect on Financial Risk Tolerance—A Quantitative Study on Whether Financial Literacy Has an Increasing or Decreasing Impact on Financial Risk Tolerance. Umeå: Umeå School of Business and Economics, pp. 1–76. Available online: http://www.diva-portal.org/smash/get/diva2:826787/FULLTEXT01.pdf (accessed on 4 August 2022).

- Hallahan, Terrence A., Robert W. Faff, and Michael D. McKenzie. 2004. An empirical investigation of personal financial risk tolerance. Financial Services Review 13: 57–78. [Google Scholar]

- Hariharan, Govind, Kenneth S. Chapman, and Dale L. Domian. 2000. Risk tolerance and asset allocation for investors nearing retirement. Financial Services Review 9: 159–70. [Google Scholar] [CrossRef]

- Hassan, Kamal, Rohani Rahim, Fariza Ahmad, Tengku Nurn Azira Tengku Zainuddin, Rooshida Rahim Merican, and Siti Kholija Bahari. 2016. Retirement planning behaviour of working individuals and legal proposition for new pension system in Malaysia. Journal of Politics and Law 9: 43. [Google Scholar] [CrossRef]

- Hauff, Jeanette C., Anders Carlander, Tommy Gärling, and Gianni Nicolini. 2020. Retirement financial behaviour: How important is being financially literate? Journal of Consumer Policy 43: 543–64. [Google Scholar] [CrossRef]

- Hayat, Amir, and Muhammad Anwar. 2016. Impact of behavioral biases on investment decision; moderating role of financial literacy. Moderating Role of Financial Literacy. [Google Scholar] [CrossRef]

- Heenkenda, Shirantha. 2014. Determination of Financial Risk Tolerance among Different Household Sectors in Sri Lanka. Nagoya: Nagoya University, pp. 1–20. [Google Scholar]

- Henseler, Jorg, Christian M. Ringle, and Marko Sarstedt. 2015. A new criterion for assessing discriminant validity in variance-based structural equation modeling. Journal of the Academy of Marketing Science 43: 115–35. [Google Scholar] [CrossRef]

- Hermansson, Cecilia, and Sara Jonsson. 2021. The impact of financial literacy and financial interest on risk tolerance. Journal of Behavioral and Experimental Finance 29: 100450. [Google Scholar] [CrossRef]

- Hershey, Douglas A., Joy M. Jacobs-Lawson, and James T. Austin. 2013. Effective Financial Planning for Retirement. Oxford: Oxford University Press. [Google Scholar]

- Hilgert, Marianne A., Jeanne M. Hogarth, and Sondra G. Beverly. 2003. Household financial management: The connection between knowledge and behavior. Federal Reserve Bulletin 89: 309. [Google Scholar]

- Hills, John, and Francesca Bastagli. 2013. Wealth accumulation, ageing and house prices. In Wealth in the UK: Distribution, Accumulation, and Policy. Oxford: OUP Oxford, p. 63. [Google Scholar]

- Indonesia Financial Service Authority. 2020. Pension Fund Statistic 2020. Directorate of Statistic and Infromation Non Bank Financial Institutions Financial Service Authority. Available online: https://www.ojk.go.id/id/kanal/iknb/data-dan-statistik/dana-pensiun/Documents/Pages/Buku-Statistik-Dana-Pensiun-2020/BUKU STATISTIK DANA PENSIUN 2020.pdf (accessed on 4 August 2022).